|

The information in this pricing supplement is not complete and may be changed. This preliminary pricing supplement is not an offer to sell

these securities, and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted. Subject to completion dated April 18, 2011.

|

|

Preliminary Pricing Supplement No. F14

To the Product Supplement No. F-I dated March 10, 2011,

Prospectus Supplement dated March 25, 2009 and

Prospectus dated March 25, 2009

|

Filed Pursuant to Rule 424(b)(2)

Registration Statement No. 333-158199-10

April 18, 2011

|

|

|

$

1 year 8.40% - 10.40% per annum Reverse Convertible Securities due April 30, 2012

Linked to the Common Stock of Caterpillar Inc.

|

|

General

|

•

|

The securities are designed for investors who are mildly bearish, neutral or mildly bullish on the Reference Shares. Investors should be willing to forgo the potential to participate in any appreciation of the Reference Shares, be willing to accept the risks of owning equities in general and the common stock of Caterpillar Inc. in particular, and be willing to lose some or all of their investment. Any payment on the securities is subject to our ability to pay our obligations as they become due.

|

|

•

|

Interest will be paid quarterly in arrears at a rate expected to be between 8.40% and 10.40% per annum (to be determined on the Trade Date). Interest will be calculated on a 30/360 basis.

|

|

•

|

Senior unsecured obligations of Credit Suisse AG, acting through its Nassau Branch, maturing April 30, 2012.†

|

|

•

|

Minimum purchase of $1,000. Minimum denominations of $1,000 and integral multiples in excess thereof.

|

|

•

|

The securities are expected to price on or about April 20, 2011 (the “Trade Date”) and are expected to settle on or about April 28, 2011. Delivery of the securities in book-entry form only will be made through The Depository Trust Company.

|

Key Terms

|

Issuer:

|

Credit Suisse AG (“Credit Suisse”), acting through its Nassau Branch

|

|

|

Reference Shares:

|

The common stock of Caterpillar Inc. (the “Reference Share Issuer”) (Bloomberg ticker symbol “CAT UN”). For additional information, please see “The Reference Shares” herein.

|

|

|

Interest Rate:

|

Expected to be between 8.40% and 10.40% per annum (to be determined on the Trade Date). Interest will be calculated on a 30/360 basis.

|

|

|

Interest Payment Dates:

|

Interest will be paid quarterly in arrears on July 29, 2011, October 31, 2011, January 31, 2012 and the Maturity Date, subject to the modified following business day convention.

|

|

|

Redemption Amount:

|

At maturity, you will be entitled to receive a Redemption Amount in cash dependent upon the performance of the Reference Shares and whether a Knock-In Event occurs and calculated as follows:

|

|

|

•

|

If a Knock-In Event has not occurred, you will be entitled to receive a cash payment equal to 100% of the principal amount of your securities.

|

|

|

•

|

If a Knock-In Event has occurred and the Final Share Price is greater than or equal to the Initial Share Price, you will be entitled to receive a cash payment equal to 100% of the principal amount of your securities.

|

|

|

•

|

If a Knock-In Event has occurred and the Final Share Price is less than the Initial Share Price, you will be entitled to receive the Physical Delivery Amount.

|

|

|

If a Knock-In Event has occurred and the Final Share Price is less than the Initial Share Price, you will receive Reference Shares with a value less than the principal amount of your securities. You could lose your entire principal amount.

|

||

|

Physical Delivery Amount:

|

A number of Reference Shares per $1,000 principal amount of securities, rounded down to the nearest whole number and equal to the product of (i) $1,000 divided by the Initial Share Price and (ii) the share adjustment factor, plus a cash amount equal to the proportion of the Final Share Price corresponding to any fractional share. If the fractional share amount to be paid in cash is a de minimis amount, as determined by the calculation agent, the holder will not receive such amount.

|

|

|

Knock-In Event:

|

A Knock-In Event will occur if on any trading day during the Observation Period, the closing price of the Reference Shares is less than or equal to the Knock-In Price.

|

|

|

Knock-In Price:

|

Approximately 80% of the Initial Share Price.

|

|

|

Initial Share Price:*

|

The closing price of the Reference Shares on the Trade Date.

|

|

|

Observation Period:

|

The period from but excluding the Trade Date to and including the Valuation Date.

|

|

|

Final Share Price:

|

The closing price of the Reference Shares on the Valuation Date.

|

|

|

Valuation Date:†

|

April 20, 2012

|

|

|

Maturity Date:†

|

April 30, 2012

|

|

|

Listing:

|

The securities will not be listed on any securities exchange.

|

|

|

CUSIP:

|

22546E5A8

|

|

* In the event that the closing price of the Reference Shares is not available on the Trade Date, the Initial Share Price will be determined on the immediately following trading day on which a closing price is available.

† The Valuation Date is subject to postponement if such date is not an underlying business day or as a result of a market disruption event and the Maturity Date is subject to postponement if such date is not a business day or if the Valuation Date is postponed, in each case as described in the accompanying product supplement under “Description of the Securities—Market disruption events.”

Investing in the securities involves a number of risks. See “Selected Risk Considerations” beginning on page 5 of this pricing supplement and “Risk Factors” beginning on page PS-3 of the accompanying product supplement.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the securities or passed upon the accuracy or the adequacy of this pricing supplement or the accompanying product supplement, the prospectus supplement and the prospectus. Any representation to the contrary is a criminal offense.

|

Price to Public

|

Underwriting Discounts and Commissions(1)

|

Proceeds to Issuer

|

|

|

Per security

|

$1,000.00

|

$

|

$

|

|

Total

|

$

|

$

|

$

|

(1) We or one of our affiliates may pay varying discounts and commissions of between $0.00 and $2.50 per $1,000 principal amount of securities. In addition, an affiliate of ours may pay referral fees of up to $5.00 per $1,000 principal amount of securities. For more detailed information, please see “Supplemental Plan of Distribution (Conflicts of Interest)” on the last page of this pricing supplement.

The agent for this offering, Credit Suisse Securities (USA) LLC (“CSSU”), is our affiliate. For more information, see “Supplemental Plan of Distribution (Conflicts of Interest)” on the last page of this pricing supplement.

The securities are not deposit liabilities and are not insured or guaranteed by the Federal Deposit Insurance Corporation or any other governmental agency of the United States, Switzerland or any other jurisdiction.

Credit Suisse

April , 2011

You may revoke your offer to purchase the securities at any time prior to the time at which we accept such offer on the date the securities are priced. We reserve the right to change the terms of, or reject any offer to purchase the securities prior to their issuance. In the event of any changes to the terms of the securities, we will notify you and you will be asked to accept such changes in connection with your purchase. You may also choose to reject such changes in which case we may reject your offer to purchase.

Additional Terms Specific to the Securities

You should read this pricing supplement together with the product supplement dated March 10, 2011, the prospectus supplement dated March 25, 2009 and the prospectus dated March 25, 2009, relating to our Medium-Term Notes of which these securities are a part. You may access these documents on the SEC website at www.sec.gov as follows (or if such address has changed, by reviewing our filings for the relevant date on the SEC website):

|

|

•

|

Product supplement No. F-I dated March 10, 2011:

|

|

|

•

|

Prospectus supplement dated March 25, 2009:

|

|

|

•

|

Prospectus dated March 25, 2009:

|

Our Central Index Key, or CIK, on the SEC website is 1053092. As used in this pricing supplement, the “Company,” “we,” “us,” or “our” refers to Credit Suisse.

This pricing supplement, together with the documents listed above, contains the terms of the securities and supersedes all other prior or contemporaneous oral statements as well as any other written materials including preliminary or indicative pricing terms, fact sheets, correspondence, trade ideas, structures for implementation, sample structures, brochures or other educational materials of ours. You should carefully consider, among other things, the matters set forth in “Selected Risk Considerations” in this pricing supplement and “Risk Factors” in the accompanying product supplement, as the securities involve risks not associated with conventional debt securities. You should consult your investment, legal, tax, accounting and other advisors before deciding to invest in the securities.

1

Hypothetical Redemption Amounts at Maturity

The table and scenarios below illustrate hypothetical Redemption Amounts payable at maturity for a $1,000 principal amount of securities for a hypothetical range of performance of the Reference Shares. The table and the scenarios below assume a hypothetical Initial Share Price of $110, a Knock-In Price of $88, a share adjustment factor of 1.0 and that the term of the securities is exactly one year. The table and scenarios are intended to illustrate hypothetical calculations of only the Redemption Amount and do not illustrate the calculation or payment of any interest payment. The Redemption Amounts set forth below are provided for illustration purposes only. The actual Redemption Amount applicable to a purchase of the securities will depend on whether, on any trading day during the Observation Period, the closing price of the Reference Shares is less than or equal to the Knock-In Price. It is not possible to predict whether a Knock-In Event will occur, and in the event that there is a Knock-In Event, whether and by how much the Final Share Price will decrease in comparison to the Initial Share Price. The numbers appearing in the table and the scenarios below have been rounded for ease of analysis. Any payment on the securities is subject to our ability to pay our obligations as they become due.

If a Knock-In Event occurs and the Final Share Price is less than the Initial Share Price, you will be entitled to receive on the Maturity Date a Redemption Amount per $1,000 principal amount of securities that will consist of a whole number of Reference Shares plus an amount in cash corresponding to any fractional Reference Share. If the fractional share amount to be paid in cash is a de minimis amount, as determined by the calculation agent, the holder will not receive such amount.

The value of any such Redemption Amount on the Valuation Date will be less than $1,000 and may fluctuate, possibly decreasing, in the period between the Valuation Date and the Maturity Date. If a Knock-In Event occurs and the Final Share Price is less than the Initial Share Price, you could lose your entire investment in the securities.

The hypothetical Redemption Amounts in the table and scenarios below do not reflect any interest payments on the securities. A holder of the securities will be entitled to receive interest payable on the securities in cash regardless of whether or not a Knock-In Event occurs.

|

A Knock-In Event

Does Not Occur

|

A Knock-In Event

Does Occur

|

|||||||||

|

Final Share

Price ($)

|

Percentage Change in the price of the Reference Shares

|

Return on the

Securities

(excluding interest payable on the securities)

|

Redemption

Amount

|

Return on the

Securities (excluding interest payable on the securities)

|

Redemption

Amount

|

|||||

|

220.00

|

100.00%

|

0.00%

|

$1,000.00

|

0.00%

|

$1,000.00

|

|||||

|

209.00

|

90.00%

|

0.00%

|

$1,000.00

|

0.00%

|

$1,000.00

|

|||||

|

198.00

|

80.00%

|

0.00%

|

$1,000.00

|

0.00%

|

$1,000.00

|

|||||

|

187.00

|

70.00%

|

0.00%

|

$1,000.00

|

0.00%

|

$1,000.00

|

|||||

|

176.00

|

60.00%

|

0.00%

|

$1,000.00

|

0.00%

|

$1,000.00

|

|||||

|

165.00

|

50.00%

|

0.00%

|

$1,000.00

|

0.00%

|

$1,000.00

|

|||||

|

154.00

|

40.00%

|

0.00%

|

$1,000.00

|

0.00%

|

$1,000.00

|

|||||

|

143.00

|

30.00%

|

0.00%

|

$1,000.00

|

0.00%

|

$1,000.00

|

|||||

|

132.00

|

20.00%

|

0.00%

|

$1,000.00

|

0.00%

|

$1,000.00

|

|||||

|

121.00

|

10.00%

|

0.00%

|

$1,000.00

|

0.00%

|

$1,000.00

|

|||||

|

110.00

|

0.00%

|

0.00%

|

$1,000.00

|

0.00%

|

$1,000.00

|

|||||

|

104.50

|

−5.00%

|

0.00%

|

$1,000.00

|

−5.00%

|

9 shares + $9.50

|

|||||

|

99.00

|

−10.00%

|

0.00%

|

$1,000.00

|

−10.00%

|

9 shares + $9.00

|

|||||

|

88.00

|

−20.00%

|

N/A

|

N/A

|

−20.00%

|

9 shares + $8.00

|

|||||

|

77.00

|

−30.00%

|

N/A

|

N/A

|

−30.00%

|

9 shares + $7.00

|

|||||

|

66.00

|

−40.00%

|

N/A

|

N/A

|

−40.00%

|

9 shares + $6.00

|

|||||

|

55.00

|

−50.00%

|

N/A

|

N/A

|

−50.00%

|

9 shares + $5.00

|

|||||

|

44.00

|

−60.00%

|

N/A

|

N/A

|

−60.00%

|

9 shares + $4.00

|

|||||

|

33.00

|

−70.00%

|

N/A

|

N/A

|

−70.00%

|

9 shares + $3.00

|

|||||

|

22.00

|

−80.00%

|

N/A

|

N/A

|

−80.00%

|

9 shares + $2.00

|

|||||

|

11.00

|

−90.00%

|

N/A

|

N/A

|

−90.00%

|

9 shares + $1.00

|

|||||

2

The following scenarios illustrate how the Redemption Amount is calculated. Regardless of the performance of the Reference Shares or the payment you receive at maturity, you will be entitled to receive interest payments on each of the Interest Payment Dates.

Scenarios 1: The price of the Reference Shares increases from the Initial Share Price of $110 to a Final Share Price of $132 and a Knock-In Event does not occur. Since a Knock-In Event has not occurred during the Observation Period, the Redemption Amount is equal to the principal amount and the investor is entitled to receive at maturity a payment in cash equal to $1,000 per $1,000 principal amount of securities.

Scenario 2: The price of the Reference Shares decreases from the Initial Share Price of $110 to a Final Share Price of $99 and a Knock-In Event does not occur. Since a Knock-In Event has not occurred during the Observation Period, the Redemption Amount is equal to the principal amount even though the Final Share Price is less than the Initial Share Price and the investor is entitled to receive at maturity a payment in cash equal to $1,000 per $1,000 principal amount of securities.

Scenarios 3: The price of the Reference Shares increases from the Initial Share Price of $110 to a Final Share Price of $132 and a Knock-In Event does occur. Since a Knock-In Event has occurred during the Observation Period, but the Final Share Price is greater than the Initial Share Price, the Redemption Amount is equal to the principal amount and the investor is entitled to receive at maturity a payment in cash equal to $1,000 per $1,000 principal amount of securities.

Scenario 4: The price of the Reference Shares decreases from the Initial Share Price of $110 to a Final Share Price of $88. Since a Knock-In Event has occurred during the Observation Period and the Final Share Price is less than the Initial Share Price, the Redemption Amount is equal to the Physical Delivery Amount, calculated as follows:

|

Physical Delivery Amount

|

=

|

$1,000/Initial Share Price

|

+

|

plus a cash amount equal to the

proportion of the Final Share

Price corresponding to any

fractional share

|

|

|

=

|

$1,000/$110 + cash amount

|

||||

|

=

|

9 Reference Shares (9.090909 rounded down) +

(0.090909 × $88)

|

||||

|

=

|

9 Reference Shares + $8

|

||||

In this scenario, at maturity an investor would be entitled to receive a Redemption Amount consisting of 9 Reference Shares and a cash payment of $8. The value of the Redemption Amount on the Valuation Date, which is the date on which the Final Share Price is determined, is $800, calculated as follows:

|

Value of Redemption Amount

|

=

|

(9 Reference Shares × Final Share Price) + $8

|

|

|

=

|

(9 Reference Shares × $88) + $8

|

||

|

=

|

$792 + $8

|

||

|

=

|

$800

|

In these circumstances, the investor will participate in any depreciation in the price of the Reference Shares from the Initial Share Price to the Final Share Price.

3

Selected Risk Considerations

An investment in the securities involves significant risks. Investing in the securities is not equivalent to investing directly in the Reference Shares. These risks are explained in more detail in the “Risk Factors” section of the accompanying product supplement.

|

|

•

|

YOU MAY RECEIVE LESS THAN THE PRINCIPAL AMOUNT AT MATURITY – You may receive less at maturity than you originally invested in the securities, or you may receive nothing, excluding any accrued and unpaid interest. If the closing price of the Reference Shares is less or equal to the Knock-In Price on any trading day during the Observation Period and the Final Share Price is less than the Initial Share Price, you will be fully exposed to any depreciation in the Reference Shares. In this case, the Redemption Amount you will be entitled to receive will be less than the principal amount of the securities, and you could lose your entire investment. It is not possible to predict whether a Knock-In Event will occur, and in the event that there is a Knock-In Event, whether and by how much the Final Share Price will decrease in comparison to the Initial Share Price. Any payment on the securities is subject to our ability to pay our obligations as they become due.

|

|

|

•

|

THE SECURITIES ARE SUBJECT TO THE CREDIT RISK OF CREDIT SUISSE – Although the return on the securities will be based on the performance of the Reference Shares, the payment of any amount due on the securities, including any applicable interest payment or payment at maturity, is subject to the credit risk of Credit Suisse. Investors are dependent on our ability to pay all amounts due on the securities, and therefore, investors are subject to our credit risk. In addition, any decline in our credit ratings, any adverse changes in the market’s view of our creditworthiness or any increase in our credit spreads is likely to adversely affect the value of the securities prior to maturity.

|

|

|

•

|

THE REDEMPTION AMOUNT WILL BE AFFECTED BY THE KNOCK-IN PRICE AND THE OCCURRENCE OF A KNOCK-IN EVENT – If the closing price of the Reference Shares is less than or equal to the Knock-In Price on any trading day during the Observation Period, a Knock-In Event will occur. If a Knock-In Event occurs and the Final Share Price is less than the Initial Share Price, the Redemption Amount will consist of a number of Reference Shares plus an amount in cash corresponding to any fractional share, as described above. Under these circumstances, the Redemption Amount will be significantly less than the principal amount of the securities and may be zero.

|

|

|

•

|

THE SECURITIES WILL NOT PAY MORE THAN THE PRINCIPAL AMOUNT, PLUS ACCRUED AND UNPAID INTEREST – The securities will not pay more than the principal amount, plus accrued and unpaid interest, at maturity. If the Final Share Price is greater than the Initial Share Price, regardless of whether a Knock-In Event occurs, you will not benefit from any appreciation, which may be significant, in the price of the Reference Shares. If the Final Share Price is greater than or equal to the Initial Share Price, you will be entitled to receive a cash payment of $1,000 per $1,000 principal amount of securities that you hold at maturity, plus accrued and unpaid interest.

|

|

|

•

|

IF THE REDEMPTION AMOUNT CONSISTS OF THE PHYSICAL DELIVERY AMOUNT, THE VALUE OF SUCH REDEMPTION AMOUNT COULD BE LESS ON THE MATURITY DATE THAN ON THE VALUATION DATE – If a Knock-In Event occurs and the Final Share Price is less than the Initial Share Price, you will be entitled to receive on the Maturity Date the Physical Delivery Amount which will consist of a whole number of Reference Shares plus an amount in cash corresponding to

|

4

any fractional share. The value of the Physical Delivery Amount on the Valuation Date will be less than $1,000 per $1,000 principal amount of securities and could fluctuate, possibly decreasing, in the period between the Valuation Date and the Maturity Date. We will make no adjustments to the Physical Delivery Amount to account for any such fluctuation and you will bear the risk of any decrease in the value of the Physical Delivery Amount between the Valuation Date and the Maturity Date.

|

|

•

|

CERTAIN BUILT-IN COSTS ARE LIKELY TO ADVERSELY AFFECT THE VALUE OF THE SECURITIES PRIOR TO MATURITY – While the payment at maturity described in this pricing supplement is based on the full principal amount of your securities, the original issue price of the securities includes the agent’s commission and the cost of hedging our obligations under the securities through one or more of our affiliates. As a result, the price, if any, at which Credit Suisse (or its affiliates), will be willing to purchase securities from you in secondary market transactions, if at all, will likely be lower than the original issue price, and any sale prior to the Maturity Date could result in a substantial loss to you. The securities are not designed to be short-term trading instruments. Accordingly, you should be able and willing to hold your securities to maturity.

|

|

|

•

|

NO OWNERSHIP RIGHTS IN THE REFERENCE SHARES – You return on the securities will not reflect the return you would realize if you actually owned the Reference Shares. The return on your investment, which is based on the percentage change in the Reference Shares, is not the same as the total return based on a purchase of the Reference Shares.

|

|

|

•

|

NO DIVIDEND PAYMENTS OR VOTING RIGHTS – As a holder of the securities, you will not have any ownership interest or rights in the Reference Shares, such as voting rights or dividend payments. In addition, the issuer of the Reference Shares will not have any obligation to consider your interests as a holder of the securities in taking any corporate action that might affect the value of the Reference Shares and therefore, the value of the securities.

|

|

|

•

|

LACK OF LIQUIDITY – The securities will not be listed on any securities exchange. Credit Suisse (or its affiliates) intends to offer to purchase the securities in the secondary market but is not required to do so. Even if there is a secondary market, it may not provide enough liquidity to allow you to trade or sell the securities when you wish to do so. Because other dealers are not likely to make a secondary market for the securities, the price at which you may be able to trade your securities is likely to depend on the price, if any, at which Credit Suisse (or its affiliates) is willing to buy the securities. If you have to sell your securities prior to maturity, you may not be able to do so or you may have to sell them at a substantial loss.

|

|

|

•

|

POTENTIAL CONFLICTS – We and our affiliates play a variety of roles in connection with the issuance of the securities, including acting as calculation agent and hedging our obligations under the securities. In performing these duties, the economic interests of the calculation agent and other affiliates of ours are potentially adverse to your interests as an investor in the securities. We and/or our affiliates may also currently or from time to time engage in business with the Reference Share Issuer, including extending loans to, or making equity investments in, the Reference Share Issuer or providing advisory services to the Reference Share Issuer. In addition, one or more of our affiliates may publish research reports or otherwise express opinions with respect to the Reference Share Issuer and these reports may or may not recommend that investors buy or hold the Reference Shares. As a prospective purchaser of the securities, you should undertake an independent investigation of the Reference Share Issuer that in your judgment is appropriate to make an informed decision with respect to an investment in the securities.

|

|

|

•

|

ANTI-DILUTION PROTECTION IS LIMITED – The calculation agent will make anti-dilution adjustments for certain events affecting the Reference Shares. However, an adjustment will not be required in response to all events that could affect the Reference Shares. If an event occurs that does not require the calculation agent to make an adjustment, the value of the securities may be materially and adversely affected. See “Description of the Securities—Adjustments” in the accompanying product supplement.

|

|

|

•

|

MANY ECONOMIC AND MARKET FACTORS WILL AFFECT THE VALUE OF THE SECURITIES – In addition to the price of the Reference Shares on any trading day during the

|

5

|

|

|

Observation Period, the value of the securities will be affected by a number of economic and market factors that may either offset or magnify each other, including:

|

|

|

o

|

the expected volatility of the Reference Shares;

|

|

|

o

|

the time to maturity of the securities;

|

|

|

o

|

the dividend rate on the Reference Shares;

|

|

|

o

|

interest and yield rates in the market generally;

|

|

|

o

|

events affecting companies engaged in the mining industry including those relating to international political and economic developments, energy conservation, the success of exploration projects, commodity prices, and tax and other government regulations;

|

|

|

o

|

geopolitical conditions and a variety of economic, financial, political, regulatory or judicial events that affect the Reference Share Issuer or markets generally and which may affect the price of the Reference Shares; and

|

|

|

o

|

our creditworthiness, including actual or anticipated downgrades in our credit ratings.

|

|

|

Some or all of these factors may influence the price that you will receive if you choose to sell your securities prior to maturity. The impact of any of the factors set forth above may enhance or offset some or all of any change resulting from another factor or factors.

|

Supplemental Use of Proceeds and Hedging

We intend to use the proceeds of this offering for our general corporate purposes, which may include the refinancing of existing debt outside Switzerland. Some or all of the proceeds we receive from the sale of the securities may be used in connection with hedging our obligations under the securities through one or more of our affiliates. Such hedging or trading activities on or prior to the Trade Date and during the term of the securities (including on the Valuation Date) could adversely affect the value of the Reference Shares and, as a result, could decrease the amount you may receive on the securities at maturity. For further information, please refer to “Use of Proceeds and Hedging” in the accompanying product supplement.

6

The Reference Shares

All information contained herein with respect to the Reference Shares and on Caterpillar Inc. is derived from publicly available sources and is provided for informational purposes only. Companies with securities registered under the Exchange Act are required to periodically file certain financial and other information specified by the SEC. Information provided to or filed with the SEC by a Reference Share Issuer pursuant to the Exchange Act can be located by reference to the SEC file number provided below. According to its publicly available filings with the SEC, Caterpillar designs, manufactures, markets and sells construction, mining and forestry machinery, offers logistics services for other companies, and designs, manufactures, remanufactures, maintains and services rail-related products. Caterpillar also designs, manufactures, markets and sells engines for Caterpillar machinery and for a variety of other systems and applications. In addition, Caterpillar provides financings and insurance to customers and dealers. The common stock of Caterpillar, par value $1.00 per share, is listed on the New York Stock Exchange. Caterpillar’s SEC file number is 1-768 and can be accessed through www.sec.gov. We do not make any representation that these publicly available documents are accurate or complete.

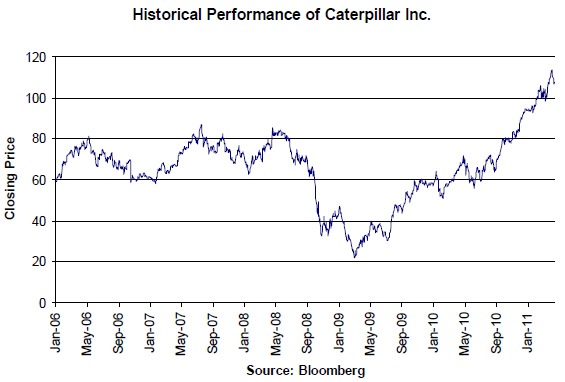

Historical Information

The following graph sets forth the historical performance of the Reference Shares based on the closing prices of the Reference Shares from January 1, 2006 through April 14, 2011. The closing price of the Reference Shares on April 14, 2011 was $107.58. We obtained the closing prices below from Bloomberg, without independent verification. The closing prices and this other information may be adjusted by Bloomberg for corporate actions such as public offerings, mergers and acquisitions, spin-offs, delistings and bankruptcy. We make no representation or warranty as to the accuracy or completeness of the information obtained from Bloomberg. The price source for determining the Final Share Price will be the Bloomberg page “CAT” or any successor page.

The historical prices of the Reference Shares should not be taken as an indication of future performance, and no assurance can be given as to the closing price of the Reference Shares on any trading day during the Observation Period, including on the Valuation Date. The closing price of the Reference Shares may decrease so that a Knock-In Event occurs and at maturity you will be entitled to receive a Redemption Amount that is less than the principal amount of the securities. We cannot give you assurance that the performance of the Reference Shares will result in the return of any of your initial investment.

7

Supplemental Information Regarding Certain United States Federal Income Tax Considerations

The amount of the stated interest rate on the security that constitutes interest on the Deposit (as defined in the accompanying product supplement) equals 0.4195%, and the remaining balance constitutes the Option Premium (as defined in the accompanying product supplement). Please refer to “Certain U.S. Federal Income Tax Considerations” in the accompanying product supplement.

Supplemental Plan of Distribution (Conflicts of Interest)

Under the terms and subject to the conditions contained in a distribution agreement dated May 7, 2007, as amended, which we refer to as the distribution agreement, we have agreed to sell the securities to CSSU.

The distribution agreement provides that CSSU is obligated to purchase all of the securities if any are purchased.

CSSU proposes to offer the securities at the offering price set forth on the cover page of this pricing supplement and may receive varying underwriting discounts and commissions of between $0.00 and $2.50 per $1,000 principal amount of securities. CSSU may re-allow some or all of the discount on the principal amount per security on sales of such securities by other brokers or dealers. If all of the securities are not sold at the initial offering price, CSSU may change the public offering price and other selling terms.

In addition, Credit Suisse International, an affiliate of Credit Suisse, may pay referral fees to some broker-dealers of up to $5.00 per $1,000 principal amount of securities in connection with the distribution of the securities. An affiliate of Credit Suisse has paid or may pay in the future a fixed amount to broker-dealers in connection with the costs of implementing systems to support these securities.

The agent for this offering, CSSU, is our affiliate. In accordance with FINRA Rule 5121, CSSU may not make sales in this offering to any of its discretionary accounts without the prior written approval of the customer. A portion of the net proceeds from the sale of the securities will be used by CSSU or one of its affiliates in connection with hedging our obligations under the securities.

We expect that delivery of the securities will be made against payment for the securities on or about April 28, 2011, which will be the sixth business day following the Trade Date for the securities (this settlement cycle being referred to as T+6). Under Rule 15c6-1 under the Securities Exchange Act of 1934, as amended, trades in the secondary market generally are required to settle in three business days, unless the parties to that trade expressly agree otherwise. Accordingly, purchasers who wish to trade the securities on the Trade Date or the following two business days will be required to specify an alternate settlement cycle at the time of any such trade to prevent a failed settlement and should consult their own advisors.

For further information, please refer to “Underwriting (Conflicts of Interest)” in the accompanying product supplement

8

Credit Suisse