As filed with the Securities and Exchange Commission on April 25, 2024

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

________________________________________________

FORM 20-F/A

________________________________________________

| ☐ |

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

| OR | ||

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2022 |

|

| OR | ||

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

| OR | ||

| ☐ |

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number 1-14732

COMPANHIA SIDERÚRGICA

NACIONAL

(Exact name of registrant as specified in its charter)

NATIONAL STEEL

COMPANY

(Translation of registrant’s name into English)

_______________________________________________

THE FEDERATIVE REPUBLIC

OF BRAZIL

(Jurisdiction of incorporation or organization)

Antonio Marco Campos Rabello, Chief Financial and Investor

Relations Officer

Phone: +55 11 3049-7454 Fax: +55 11 3049-7212

invrel@csn.com.br

Av. Brigadeiro Faria Lima, 3400 – 20th floor

04538-132, São Paulo, SP, Brazil

(Address of principal executive offices)

________________________________________________

Securities registered or to be registered pursuant to Section 12(b) of the Act.

| Title of each class | Trading symbol | Name of each exchange on which registered |

| Common Shares without Par Value | * | NYSE |

| American Depositary Shares (as evidenced by American Depositary Receipts), each representing one share of Common Stock | SID | NYSE |

_____________

* Not for trading purposes, but only in connection with the registration of American Depositary Shares pursuant to the requirements of the U.S. Securities and Exchange Commission.

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of December 31, 2022:

1,326,093,947 Common Shares without Par Value

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

☑ Yes ☐ No

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

☐ Yes ☑ No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

☑ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

☑ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or an emerging growth company. See definition of “large accelerated filer,” “accelerated filer” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☑ | Accelerated filer ☐ | Non-accelerated filer ☐ | Emerging growth company ☐ |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act.

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

☑ Yes ☐ No

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

☐ Yes ☑ No

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b).

☐ Yes ☐ No

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| U.S. GAAP ☐ | International Financial Reporting Standards as issued by the International Accounting Standards Board ☑ | Other ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow:

Item 17 ☐ Item 18 ☐

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

☐ Yes ☑ No

EXPLANATORY NOTE

This amendment (“Amendment”) to National Steel Company’s (Companhia Siderúrgica Nacional – CSN) annual report on Form 20-F for the fiscal year ended December 31, 2022 (the “2022 Form 20-F”) hereby amends and restates Item 4 and Item 19 of the 2022 Form 20-F, initially filed on April 27, 2023. This Amendment is prepared for the purpose of providing clarifying information and certain updates to the mining disclosure set forth in the 2022 Form 20-F in response to comments received from the staff of the U.S. Securities and Exchange Commission in connection with its review of the 2022 Form 20-F.

This Amendment does not reflect events occurring after the filing of the 2022 Form 20-F and does not modify, update or restate any other information in the 2022 Form 20-F in any way other than as required to reflect the amendments discussed above.

| ITEM 4. | Information on the Company |

4A. History and Development of the Company

Companhia Siderúrgica Nacional is a Brazilian corporation (sociedade por ações) incorporated in 1941 pursuant to a decree of Brazilian president Getúlio Vargas. The Presidente Vargas Steelworks, located in the city of Volta Redonda, in the state of Rio de Janeiro, began its production of coke, pig iron and steel products in 1946, when we also incorporated the Casa de Pedra mine, located in the city of Congonhas, state of Minas Gerais, and the Arcos mine, located in the city of Arcos, state of Minas Gerais. The Casa de Pedra mine assures us self-sufficiency in iron ore and the Arcos mine provides limestone and dolomite.

We were privatized through a series of auctions held in 1993 and early 1994, through which the Brazilian government sold its 91% ownership interest.

Between 1993 and 2002, we implemented a capital improvement program aimed at increasing our annual production of crude steel, improving the quality of our products, and enhancing our environmental protection and cleanup programs. As part of these investments, since February 1996, all our production involves continuous casting, which requires lower energy use and results in decreased metal loss as compared to ingot casting. From 1996 until 2002, we invested the equivalent of US$2.4 billion in our capital improvement program and on maintaining our operational capacity, culminating with the renovation of our blast furnace no. 3 at the President Vargas Steelworks and Hot Strip Mill No. 2 in 2001.

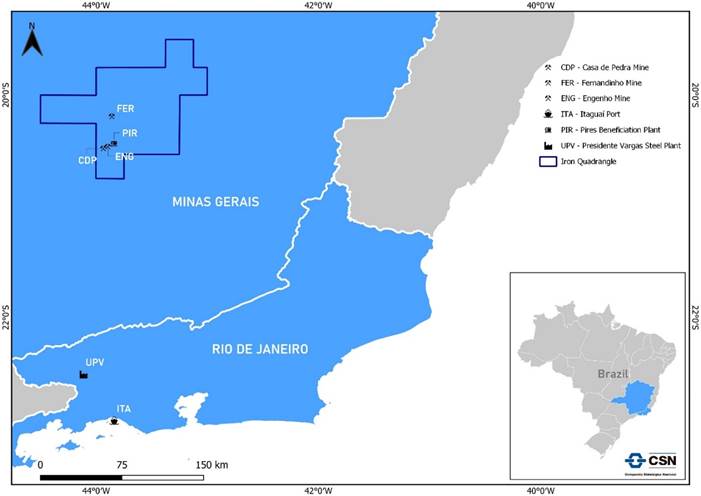

In 2007, we started to sell iron ore in the seaborne market. Today, we, through our subsidiary CSN Mineração, are an important exporter of iron ore, drawing from the high-quality iron ore reserves in the Casa de Pedra and Engenho mines, located in the state of Minas Gerais. CSN Mineração holds the concession to operate the Terminal de Carvão, or TECAR, a solid bulks terminal located in Itaguaí Port in the state of Rio de Janeiro, through which we export iron ore, coal and coke.

| 1 |

In 2009, we entered the cement market with our first grinding mill, in the Presidente Vargas Steelworks in Volta Redonda, in the state of Rio de Janeiro, taking advantage of the synergies of the cement business with our steel business.

In order to diversify our product portfolio, we entered the long steel market in 2012, with the acquisition of Stahlwerk Thüringen Gmbh, or SWT, a long steel manufacturer located in Unterwellenborn, Germany.

In addition, we installed a new plant for production of long steel products at Volta Redonda, which began operations in December 2013. The plant consists of an electric arc steelmaking furnace, continuous casting for billets and a hot rolling mill for round section long products. This plant provides the domestic Brazilian market with rebar for civil construction and wire rod for industrial and civil construction.

In 2015, we inaugurated two new grinding mills and, in 2016, we concluded a new 6,500 tons per day kiln line, reaching an aggregate annual capacity of 4.7 million tons in our cement plants.

In June 2018, we sold Heartland Steel Processing, LLC (formerly Companhia Siderúrgica Nacional, LLC) to Steel Dynamics, Inc. for US$400.0 million. We continue our commercial import and distribution activities in the North American market through our U.S. subsidiary Companhia Siderúrgica Nacional, LLC.

In 2019, investments of approximately R$250.0 million in the maintenance of blast furnace no. 3 increased its steel production capacity by 500,000 tons per year.

In 2020, we invested R$848.0 million in our steel segment, R$710.0 million in our mining segment and approximately R$140.0 million in our other segments. In early 2021, CSN Mineração completed its initial public offering, and its shares are now traded on the B3.

In 2021, we reached historically high net revenue and EBITDA and, in 2021 and 2022, we took advantage of the following acquisition opportunities: in our cement segment, Elizabeth Cimentos S.A. and Elizabeth Mineração Ltda., which operate in the Northeast region of Brazil, and LafargeHolcim (Brasil) S.A., as a result of which we are, as of the date of this annual report, the second largest cement producer in Brazil, with a total installed capacity of 17 million tons per year; in our steel segment, Metalgráfica Iguaçu S.A., or Metalgráfica, which, operates in Ponta Grossa, in the state of Paraná, and Goiânia, in the state of Goiás, produces steel cans for the national and international market of metal food packaging, as a strategic step to expand the production capacity of our packaging division; and, in our energy segment, Santa Ana Energética S.A., Topázio Energética S.A. and Companhia Energética Chapecó, or CEC, each of which holds concessions for hydroelectric power plants, and Companhia Estadual de Geração de Energia Elétrica, or CEEE-G, which holds concessions for hydroelectric power plants and greenfield wind power plant projects. These acquisitions collectively provide us with enhanced energy independence in certain of our operations.

General

We are one of the largest fully integrated steel producers in Brazil and Latin America in terms of crude steel production. We operate throughout the entire steel production chain, from the mining of iron ore to the production and sale of a diversified range of high value-added steel products. We divide our business into five segments: steel, mining, cement, logistics and energy.

Steel

Our steel segment comprises a portfolio of diverse products and provides us an international footprint by means of our international subsidiaries and our exports from Brazil. In our flat steel segment, we are an almost fully integrated steelmaker. Our main industrial facility, Presidente Vargas Steelworks, produces a broad line of steel products, including slabs, hot- and cold-rolled, galvanized and tin mill products for the distribution, packaging, automotive, home appliance and construction industries.

Our production process is based on the integrated steelworks concept. Our current annual crude steel capacity and rolled product capacity at Presidente Vargas Steelworks is, in each case, 5.6 million tons.

We obtain all of our iron ore (except for pellets), limestone and dolomite requirements, and a portion of our tin requirements, from our own mines. Using imported coal, we produce approximately 55% of our coke requirements at current production levels in our own coke batteries at Volta Redonda. Imported coal is also pulverized and used directly in the pig iron production process. Zinc, manganese ore, aluminum and a portion of our tin requirements are purchased in local markets. Our steel production and distribution processes also require water, industrial gases, energy, rail and road transportation and port facilities.

| 2 |

In addition, we have an annual production capacity of approximately 330,000 tons of galvanized steel products, operated through our subsidiary Lusosider Aços Planos, S.A. in Portugal, and an annual production capacity of approximately 1.1 million tons of steel products operated through SWT in Germany.

We own and operate a plant in Volta Redonda for production of long steel products. The plant consists of an electric arc steelmaking furnace, continuous casting for billets and a hot rolling mill for round section long products – wire rod and rebar.

Mining Activities

We own a number of high quality iron ore mines, strategically located within Brazil’s “Iron Ore Quadrangle” (Quadrilátero Ferrífero) in the state of Minas Gerais, including the Casa de Pedra and Engenho mines, located in the city of Congonhas, pertaining to our subsidiary CSN Mineração, and the Fernandinho mines, located in the city of Itabirito, and the Cayman and Pedras Pretas mining rights, located in the city of Rio Acima and the city of Congonhas, respectively, pertaining to our wholly owned subsidiary Minérios Nacional S.A., or Minérios Nacional.

Our mining assets also include (i) the solid bulks cargo terminal TECAR, in the state of Rio de Janeiro, which pertains to CSN Mineração; (ii) the Bocaina mines, located in the city of Arcos, in the state of Minas Gerais, which produce dolomite and limestone; and (iii) Estanho de Rondônia S.A., or ERSA, located in the city of Ariquemes, in the state of Rondônia, which mines and casts tin.

We sold 26.9 million tons, 28.3 million tons and 29.2 million tons of iron ore to third parties in 2020, 2021 and 2022, respectively.

Cement

We entered the cement market in 2009 in order to take advantage of the synergy potential with our steelmaking business. Our cement operations use as inputs slag generated by our blast furnaces at Volta Redonda and limestone from our limestone reserves in our Bocaina mines, which is used to produce clinker. Slag and clinker are the main inputs in cement production.

In 2015, we inaugurated two grinding mills and, in 2016, we concluded construction of a new kiln line with a capacity of 6,500 tons per day, reaching an aggregate capacity of 4.7 million tons per year of cement production including our Volta Redonda and Arcos plants.

In August 2021, our cement subsidiary, CSN Cimentos, acquired Elizabeth Cimentos S.A., which operates in the Northeast region of Brazil. This acquisition increased our cement production capacity by 1.3 million tons, from 4.7 million tons to 6.0 million tons.

In September 2022, CSN Cimentos acquired the entirety of LafargeHolcim (Brasil) S.A., at a value of US$960.7 million. This acquisition added 11 million tons of cement per year to our production capacity, bringing our total production capacity to 17 million tons of cement per year, by means of plants strategically located in the Southeast, Northeast and Midwest regions of Brazil, as well as substantial high-quality limestone reserves.

We plan to further increase our market share in the cement segment in Brazil in order to diversify our product mix and markets, which will allow us to reduce our risk exposure.

Energy

Steelmaking requires significant amounts of electrical energy to power rolling mills, production lines, hot metal processing, coking plants, cryogenic plant and auxiliary units. In 2022, our Presidente Vargas Steelworks consumed approximately 2.86 million MWh of electrical energy.

Cement production also requires significant amounts of electrical energy and, as a result of the expansion of our cement operations over the last two years, the energy needs of our cement segment represent a larger share of our energy demand. Our acquiree, LafargeHolcim (Brasil) S.A., provides 3.4 MW of installed capacity annually from a hydroelectric power plant.

| 3 |

Mining operations require electrical energy principally for crushing and excavation. In 2022, our mining operations at Casa de Pedra consumed 285,000 MWh of electrical energy.

Our main source of electrical energy is our thermoelectric co-generation power plant at the Presidente Vargas Steelworks, which is fueled by gas from the steel production process, with 267 MW of installed capacity. In addition, as of the date of this annual report, we hold a 29.50% equity interest in the Itá hydroelectric facility in the state of Santa Catarina, through a 48.75% equity interest in ITASA and a 17.92% equity interest in the Igarapava hydroelectric facility. Through these equity interests, we have secured an average of 167 MWavg in annual power supply for our operations under power purchase agreements at a fixed price per MW hour, adjusted annually according to ITASA’s board decision and 24 MWavg at a cost price of the annual generation of Igarapava’s hydroelectric power plant. At the end of 2022, ITASA’s board of directors decided it would not implement any price adjustments for 2023.

For our energy needs that are not provided by our internal generation, we rely on fixed price long-term contracts with external generators. In 2022, we seized the following acquisition opportunities in Brazil in order to enhance the energy independence of our steelmaking, cement production and mining operations: Santa Ana Energética S.A., Brasil Central Energia Ltda. and CEC, which hold concessions for hydroelectric power plants, and CEEE-G, which holds concessions for hydroelectric power plants and greenfield wind power plant projects.

Logistics

Our vertical integration strategy and the synergies among our business units are strongly dependent on the logistics needed to guarantee the transportation of inputs at low cost. A number of railways and port terminals comprise the logistics system that integrates our mining, steelmaking and cement units.

We operate a port terminal for containers, TECON at Itaguaí Port, in the state of Rio de Janeiro, and CSN Mineração operates TECAR.

We also have the following participation in three railways: (i) we share control in MRS, which operates in the Southeast region of the federal railway system, along the Rio de Janeiro – São Paulo – Belo Horizonte axis; (ii) we have an interest in joint venture TLSA, which has a concession to construct and operate the Northeastern Railway System II; and (iii) we control Ferrovia Transnordestina Logística S.A., or FTL, which operates the Northeastern Railway System I.

Recent Developments

Pre-Payment Export Financing Agreement

In March 2023, we signed a pre-payment export financing agreement, in the aggregate amount of US$1.4 billion for a term of twelve years. Up to US$980.0 million will be granted by Japan Bank for International Cooperation and up to US$420.0 million will be granted by a syndicate of banks. The agreement is part of our strategy to finance growth using financial instruments for long-term projects, including our project to build a new pellet feed plant in our Casa de Pedra mine. The consummation of this transaction is subject to the fulfillment of customary conditions precedent, including the signing of an offtake agreement with a Japanese customer for part of the volume contracted.

Other Information

Our legal and commercial name is Companhia Siderúrgica Nacional. We are organized under the laws of the Federative Republic of Brazil with head offices located at Av. Brigadeiro Faria Lima, 3400, 19th and 20th floors, Itaim Bibi, São Paulo, Brazil, CEP 04538-132, and our telephone number is +55 (11) 3049-7100. Our agent for service of process in the United States is Cogency Global Inc., located at 122 East 42nd Street, 18th Floor, New York, New York 10016. Our website is www.csn.com.br. The U.S. Securities and Exchange Commission, or the SEC, maintains a website that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC, including our filings, at http://www.sec.gov.

| 4 |

Competitive Strengths

We believe that we have the following competitive strengths:

Integrated business model. We are a highly integrated steelmaker and we believe this integration supports resilient and profitable operations. Our integrated business model comprises our captive sources of raw materials, principally iron ore, and our infrastructure, including railways and deep-water port facilities. In terms of raw materials, we own a number of high-quality iron ore mines, strategically located within Brazil’s “Iron Ore Quadrangle,” which distinguishes us from our main competitors in Brazil who are required to purchase all or a portion of their iron ore from mining companies.

Strong presence in domestic market and strategic international exposure for steel products. We have a strong presence in the Brazilian market for steel products, with a market share in 2022 of approximately 25% of the domestic flat steel market. In addition, through our international subsidiaries, we sell our flat steel products in the United States and in Europe, which aggregate sales accounted for approximately 13% of our total flat steel sales in 2022. In 2012, we acquired SWT, a long steel producer in Germany with annual production capacity of approximately 1.1 million tons of steel profiles, strengthening our steel products mix and geographical diversification. In 2022, SWT accounted for 76% of our total long steel sales, representing 718,643 tons.

Diverse product portfolio and product mix. We have a diversified flat steel product mix that includes hot-rolled, cold-rolled, galvanized and tin mill products, in order to meet a wide range of customer needs across all steel-consuming industries. We focus on selling high-margin products, including tin-coated, pre-painted, Galvalume® and galvanized products. Galvalume® is a registered trademark owned by BIEC International Inc. or its affiliates. Our galvanized products provide material for exposed auto parts, using hot-dip galvanized steel and laser-welded blanks. Our CSN Paraná branch provides us with additional capacity to produce high-quality galvanized, Galvalume® and pre-painted steel products for the construction and home appliance industries. In addition, our distribution subsidiary, Prada, provides a strong sales channel in the domestic market, enabling us to meet demand from smaller customers and to establish an important presence in this market.

Profitable mining business. We have invested significantly in our mining business, placing us in a prominent position among the world’s leading iron ore players. Further mining expansions will enable us to expand our product portfolio and total output, increasing our presence in seaborne markets.

We have high-quality iron ore reserves in Casa de Pedra, Engenho, Fernandinho and other mines, all located in the state of Minas Gerais. Our mining activities are an important contributor to our EBITDA. We sold 31.2 million tons of iron ore in 2020, 33.2 million tons in 2021 and 33.3 million tons in 2022. Our mining business also includes TECAR, a solid bulks terminal at Itaguaí Port in the state of Rio de Janeiro, with a capacity to handle (i) shipments of 45 million tons per year of iron ore and (ii) landings of 4.0 million tons per year and the Bocaina mine, located in the city of Arcos in the state of Minas Gerais, which produces dolomite and limestone, as well as our subsidiary ERSA, which mines and casts tin.

Second largest player in Brazilian cement market. Following our strategic acquisitions in the Brazilian cement market in 2021 and 2022, as part of which we now own Elizabeth Cimentos S.A. and LafargeHolcim (Brasil) S.A., we are the second largest player in the Brazilian cement market with an installed capacity of 17.0 million tons, seven integrated plants, six grinding and mixing plants and 15 distribution centers throughout Brazil, in each case as of December 31, 2022. Our cement segment further diversifies our business model and permits us to use by-products of our other operations as inputs in our cement production.

Energy generation. We generate power through our hydroelectric facilities of Itá and Igarapava, as well as our thermoelectric plant located inside Presidente Vargas Steelworks, which allow us to benefit from reduced energy tariffs. We sell excess energy we generate in the energy market on a spot basis. Our 267 MW thermoelectric cogeneration plant can provide Presidente Vargas Steelworks with approximately 20% of its energy needs for its steel mills, and uses as its primary fuel the waste gases generated by our coke ovens, blast furnaces and steel processing facilities. We hold a 29.50% equity interest in the Itá hydroelectric facility in the state of Santa Catarina, through a 48.75% equity interest in ITASA, and a 17.92% equity interest in the Igarapava hydroelectric facility. Through these equity interests, we have secured an average of 167 MWavg in annual power supply for our operations under power purchase agreements at a fixed price per MWh, adjusted annually according to ITASA’s board decision and 24 MWavg at a cost price of the annual generation of Igarapava’s hydroelectric power plant.

| 5 |

Thoroughly developed transport infrastructure. We have a thoroughly developed transport infrastructure, connecting our iron ore mines to our steel mills and to the port terminals we operate. Our Presidente Vargas Steelworks facility is located next to railway and port systems, which facilitates its supply of raw materials, product shipments and access to our main customers. Our steelworks are close to the main steel consumer centers in Brazil, with easy access to port facilities and railways. The concession for the main railway we use and operate is owned by MRS, in which we hold, directly and indirectly, as of December 31, 2022, a total of 37.27% (before non-controlling interest) ownership interest. The railway connects our Casa de Pedra mine to the Presidente Vargas Steelworks and to our terminals at Itaguaí Port, which handle our iron ore exports and most of our steel exports, as well as our imports of coal and metallurgical coke.

Low cost structure. As a result of our fully integrated business model, our thoroughly developed transportation infrastructure and our energy generation, we have been consistently generating high margins compared to peer companies in both the steel and mining segments. Other factors that lead to our low-cost structure include the strategic location of our steelworks facility along with our low-cost, skilled workforce.

Our Strategies

Our goal is to make the most of our high-quality product portfolio, low-cost production and diverse consumer market to preserve our position as one of the world’s lowest-cost steel producers and as a global player in the mining of iron ore, increase our cement segment’s market share and optimize our infrastructure assets, including ports, railways and power generating plants, which support our high integration and low cost structure. To achieve these goals, we have developed specific strategies for each of our business segments, as described below.

Steel

The strategy for our steel business comprises:

| · | Focus on the domestic market, by increasing market share in the flat steel segment and long steel market; |

| · | Emphasis on high-margin coated steel products, such as galvanized, Galvalume®, pre-painted and tin plate; |

| · | Investments in technology startups and other disruptive companies through our subsidiary CSN Inova Ventures, in order to foster innovation and efficiency; |

| · | Geographical diversification through our flat and long steel facilities abroad and our focus on diversifying our exports through, among others, coated steels; |

| · | Constant pursuit of operational excellence by developing and implementing cost reduction projects, including energy efficiency, and process review programs, including internal logistics optimization, project development and implementation discipline; |

| · | Exploring marketing and commercial synergies through our flat steel distribution network and product portfolio to accelerate our entrance into the domestic long steel market; and |

| · | Increased customized services and distribution abilities through our expanding distribution network. |

Mining

In order to strengthen our position in the iron ore market, we plan to invest in our mining assets, including through CSN Mineração, to generate low operational costs and long-term growth opportunities.

In the coming years, we expect to reach an annual shipment level of over 60 million tons per year of iron ore products, including third-party products, by increasing mine capacities, including Casa de Pedra, and developing export services for third-party producers. In the short-term, considering the 26.7% increase in iron ore prices in the first quarter of 2023 compared to the last quarter of 2022, our focus is to export high-quality iron ore at optimal margins without affecting the balance of supply and demand in the transoceanic market. To sustain this growth, we plan to increase TECAR’s capacity from 45 million tons per year in 2022 to 60 million tons per year in 2027. For more information on risks relating to iron ore price volatility, see “Item 3. Key Information––3D. Risk Factors—Risks Relating to Us and the Industries in Which We Operate—We are exposed to substantial changes in the demand for steel and iron ore, which significantly affect the prices of our products and may adversely affect us.”

| 6 |

This expansion will be funded by CSN Mineração’s financings. For more information on CSN Mineração’s financings, see “Item 5. Operating and Financial Review and Prospects—5B. Liquidity and Capital Resources—Sources of Funds and Working Capital—Debt Maturity Profile” and future issuances of debentures or other debt instruments.

To maximize the profitability of our product portfolio, we are focused on increasing our output of high-quality pellet feed with Itabirite deposits and investing with strategic partners and customers in providing pellet feed to pellet producers.

Cement

We have invested heavily in our cement business and completed two important acquisitions in the last two years: Elizabeth Cimentos S.A. in 2021 and LafargeHolcim (Brasil) S.A. in 2022. These acquisitions allowed us to become the second largest player in the Brazilian cement market with an installed capacity of 17.0 million tons, seven integrated plants, six grinding and mixing plants and 15 distribution centers throughout Brazil, in each case as of December 31, 2022.

We intend to further consolidate the Brazilian cement market. Our cement business strategy looks to increased production and competitiveness, portfolio diversification and capillarity expansion by means of greenfield and brownfield projects, as well as possible acquisition opportunities. In addition, we expect favorable market perspectives in upcoming years due to a robust pipeline of infrastructure projects and higher industry utilization rates, each of which we expect will sustain cement consumption and favorable pricing in Brazil. The focus of our cement sales strategy is on the retail segment, which operates with a low level of inventory and for which our distribution centers provide a competitive advantage.

Energy

We intend to continue to take advantage of certain acquisition opportunities in our energy segment and to increase our generation of clean energy in order to support the operations and expansion of our other segments. The operations in our energy segment provide us with autonomy in meeting certain of our energy requirements and reduce our exposure to fluctuations in energy prices in the spot market.

Logistics

We expect to expand our logistics capabilities, which comprise our integrated infrastructure operations of railways and ports, in order to increase the transportation efficiency of both our incoming raw materials and distributed products. We will continue to improve our product delivery in the Brazilian market (mainly steel and cement) by implementing low-cost measures, increasing our use of rail transportation and providing more distribution centers to reach end-customers.

In addition to our bulk terminal TECAR, our TECON container terminal has a capacity of 660,000 twenty-foot equivalent units, or TEUs, per year.

In terms of railways, we are developing the TLSA project, which focuses on iron ore, agricultural commodities, gypsum and fuel. We also plan to invest in increased efficiency and capacity in the South of Brazil through our participation in MRS. Because MRS will primarily use its own operating income and other funding strategies to invest in its expansion projects, these investments will not require material capital expenditures by us.

Investments and Divestitures

In addition to our planned investments and capital expenditures, we continue to evaluate acquisition opportunities, as well as joint ventures and brownfield or greenfield projects, to improve our steel, mining and cement cost competitiveness and production, along with our energy generation, logistics capabilities and infrastructure.

| 7 |

We also continue to evaluate business opportunities in order to improve our liquidity position in the short- to medium-term, including in the form of streaming transactions related to our iron ore business and the sale of our investment in Usinas Siderúrgicas de Minas Gerais S.A., or Usiminas.

Acquisition Activity

Elizabeth Cimentos S.A. and Elizabeth Mineração Ltda.

In August 2021, our cement subsidiary, CSN Cimentos, acquired Elizabeth Cimentos S.A. and Elizabeth Mineração Ltda., which operate in the Northeast region of Brazil. These acquisitions increased our cement production capacity by 1.3 million tons, from 4.7 million tons to 6.0 million tons.

LafargeHolcim (Brasil) S.A.

In September 2022, CSN Cimentos acquired the entirety of LafargeHolcim (Brasil) S.A., at a value of US$960.7 million. This acquisition added 11 million tons of cement per year to our production capacity, bringing our total production capacity to 17 million tons of cement per year, by means of plants strategically located in the Southeast, Northeast and Midwest regions of Brazil, as well as substantial high-quality limestone reserves.

Metalgráfica Iguaçu S.A.

In September 2022, our subsidiary Companhia Metalúrgica Prada acquired Metalgráfica, which, operating in Ponta Grossa, in the state of Paraná, and in Goiânia, in the state of Goiás, produces steel cans for the national and international market of metal food packaging. This acquisition improved the competitiveness, and represents a strategic step in expanding the capacity, of our packaging division.

Santa Ana Energética S.A. and Topázio Energética S.A.

In June 2022, CSN Cimentos and our energy subsidiary, CSN Energia S.A., or CSN Energia, acquired Santa Ana Energética S.A., which holds the concession for the hydroelectric power plant of Santa Ana, and Topázio Energética S.A., which holds, through its subsidiary Brasil Central Energia Ltda., the concession for the hydroelectric power plant of Sacre II.

Companhia Estadual de Geração de Energia Elétrica – CEEE-G

In 2022, our subsidiary Companhia Florestal do Brasil, or CFB, acquired CEEE-G, which holds concessions for hydroelectric power plants and greenfield wind power plant projects, for a total price of R$1,295.0 million. The purpose of this acquisition is to support and strengthen our business expansion strategy, through investments in renewable energy, as we seek self-sufficiency for greater competitiveness of our business.

Companhia Energética Chapecó – CEC

In July 2022, CSN Mineração acquired CEC, which holds the concession for a hydroelectric power plant that has an installed capacity of 120 MW.

The energy generated by the acquisitions in our energy segment support our cement and mining operations and will permits us to reduce the volume contracted pursuant to our largest external energy contract from 150 MWavg to 50 MWavg per year and, consequently, to reduce the costs of our energy consumption.

For more information, see “Item 3. Key Information—3D. Risk Factors—Risks Relating to Us and the Industries in Which We Operate—We may not be able to consummate proposed acquisitions or integrate acquired businesses successfully.”

Joint Ventures, Strategic Alliances and Consortia

We currently operate parts of our business through joint ventures, strategic alliances and consortia with other companies. We have, among others: (i) a strategic alliance with an Asian consortium at our controlled investee CSN Mineração to mine iron ore; (ii) a concession jointly held with other Brazilian steel and mining companies at MRS Logística S.A., or MRS, to explore railway transportation in the Southeastern region of Brazil; (iii) a concession jointly held with certain Brazilian governmental entities at Transnordestina Logística S.A., or TLSA, to explore railway transportation in the Northeastern region of Brazil; (iv) a joint venture with Engie Brasil Energia S.A., or Engie Brasil, and Companhia de Cimento Itambé, or Itambé, at Itá Energética S.A., or ITASA, to produce electrical energy; and (v) an energy consortium with Aliança, L.D.R.S.P.E. Geracão de Energia e Participações Ltda. and AngloGold.

| 8 |

Description of our Operating Segments

Our Steel Segment

We produce carbon steel, which is the world’s most widely produced type of steel, representing the vast bulk of global consumption. From carbon steel, we sell a variety of products, both domestically and abroad, to manufacturers in several industries.

Flat Steel

Our Presidente Vargas Steelworks produces flat steel products, which comprise slabs, hot-rolled, cold-rolled, galvanized and tin mill products. For more information on our flat steel production process, see “—Production Output.”

Slabs

Slabs are semi-finished products used for processing hot-rolled, cold-rolled or coated coils and sheet products. We are able to produce continuously cast slabs with a standard thickness of 250 millimeters, widths ranging from 830 to 1,600 millimeters and lengths ranging from 5,250 to 10,500 millimeters. We produce high, medium and low carbon slabs, as well as micro-alloyed, ultra-low-carbon and interstitial free slabs. The slabs are then slit and finished, generating blooms which are delivered to the long products plant.

Hot-Rolled Products

Hot-rolled products include heavy and light-gauge hot-rolled coils and sheets. A heavy gauge hot-rolled product, as defined by Brazilian standards, is a flat-rolled steel coil or sheet with a minimum thickness of 5.01 millimeters. We are able to provide coils of heavy gauge hot-rolled sheet with a maximum thickness of 12.70 millimeters used to manufacture automobile parts, pipes, structural beams and other construction products. We produce light gauge hot-rolled coils and sheets with a minimum thickness of 1.20 millimeters, which are used for welded pipe and tubing, automobile parts, gas containers, compressor bodies and light cold-formed shapes, channels and profiles for the construction industry.

Cold-Rolled Products

Cold-rolled products include cold-rolled coils and sheets. A cold-rolled product, as defined by Brazilian standards, is a flat cold-rolled steel coil or sheet with thickness ranging from 0.30 millimeters to 3.00 millimeters. Cold-rolled products have more uniform thickness and better surface quality when compared to hot-rolled products and their main applications are automotive parts, home appliances and construction. We supply cold-rolled coils with thickness ranging from 0.30 millimeters to 2.99 millimeters.

Galvanized Products

Galvanized products comprise flat-rolled steel coated on one or both sides with zinc or a zinc-based alloy applied by either a hot-dip or an electrolytic process. We use the hot-dip process, which is approximately 20% less expensive than the electrolytic process. Galvanizing is one of the most effective and low-cost processes used to protect steel against corrosion caused by exposure to water and the atmosphere. Galvanized products are highly versatile and can be used to manufacture a broad range of products, such as:

| · | automobiles, trucks and bus bodies; |

| · | manufactured products for the construction industry, such as panels for roofing and siding, dry wall and roofing support frames, doors, windows, fences and light structural components; |

| · | air ducts and parts for hot air, ventilation and cooling systems; |

| · | culverts, garbage containers and other receptacles; |

| · | storage tanks, grain bins and agricultural equipment; |

| · | panels and sign panels; and |

| · | pre-painted parts. |

| 9 |

Galvanized sheets, both painted and bare, are also frequently used for gutters and downspouts, outdoor and indoor cabinets and home appliances, among others. We produce galvanized sheets and coils in continuous hot-dip processing lines, with thickness ranging from 0.30 millimeters to 3.00 millimeters. The continuous process allows for products with highly adherent and uniform zinc coatings capable of being processed in nearly all kinds of bending and forming machinery.

We produce Galvanew in addition to standard galvanized products. Galvanew is produced by an additional annealing cycle just after the zinc hot-dip coating process. This annealing process causes iron to diffuse from the base steel into the zinc coating. The resulting iron-zinc alloy coating allows better welding and paint performance. The combination of these qualities makes our Galvanew product particularly well suited for manufacturing automobile and home appliance parts, including high gloss exposed parts.

At CSN Paraná, one of our branches, we produce Galvalume®, a continuous Al-Zn coated material. Although the production process is similar to hot-dip galvanized coating, Galvalume® has at least twice the corrosion resistance of standard galvanized steel. Galvalume® is primarily used in outdoor construction applications that may be exposed to severe acid corrosion, like marine uses.

The value added from the galvanizing process permits us to price our galvanized products with a higher margin. Our management believes that our expertise in value-added galvanized products presents one of our best opportunities for profitable growth because of the increase in Brazilian demand for these products.

Through CSN Paraná, we also produce pre-painted flat steel, which is manufactured in a continuous painting line. In this production line, a layer of resin-based paint in a choice of colors is deposited over either cold-rolled or galvanized base materials. Pre-painted material is a higher value-added product used primarily in the construction and home appliance markets.

Tin Mill Products

Tin mill products consist of flat-rolled low-carbon steel coils or sheets with, as defined by Brazilian standards, a maximum thickness of 0.45 millimeters, coated or uncoated. We apply coatings of tin or chromium by electrolytic process. Coating costs place tin mill products among our highest priced products. The added value from the coating process permits us to price our tin mill products at a higher margin. There are four types of tin mill products, all produced by us in coil and sheet forms:

| · | Tin plate: coated on one or both sides with a thin metallic tin layer plus a chromium oxide layer, covered with a protective oil film; |

| · | Tin free steel: coated on both sides with a very thin metallic chromium layer plus a chromium oxide layer, covered with a protective oil film; |

| · | Low tin coated steel: coated on both sides with a thin metallic tin layer plus a thicker chromium oxide layer, covered with a protective oil film; and |

| · | Black plate: uncoated product used as the starting material for the coated tin mill products. |

Tin mill products are primarily used to make cans and other containers. With six electrolytic coating lines, we are one of the largest producers of tin mill products in the world and the sole producer of coated tin mill products in Brazil.

Quality Management System

We maintain a quality management system that is certified to comply with the International Standardization Organization, or ISO, 9001:2015 standard and the automotive industry’s International Automotive Task Force, or IATF, standard 16949:2016. ISO 9001:2015 is for the design and manufacture of slabs, blooms, billets, hot-rolled flat, pickled and oiled, cold-rolled and galvanized steel, tin mill products and long steel products; and IATF 16949:2016, third edition, is for the manufacture of hot-rolled flat, pickled and oiled steel products, cold-rolled and galvanized steel products. We maintain product certifications for hot-rolled steel in accordance with European Standards EN10025 and regulation (EU) no. 305/2011, CE Mark, and for the supply of steel wires and bars intended for reinforcing of concrete structures in accordance with applicable Brazilian regulations. In addition, as a manufacturer and supplier of products for the food packaging industry, we hold the food safety management system certification, or FSSC 22000, recognized by the Global Food Safety Initiative, most recently audited in December 2022.

| 10 |

Production Output

The following table sets forth the aggregate annual production of crude steel in Brazil and by us, and the percentage of Brazilian production attributable to us for the periods indicated:

|

Brazil |

CSN |

CSN as % of Brazil | |

| 2022 | 33.9 | 3.6 | 11.2% |

| 2021 | 36.0 | 4.0 | 11.1% |

| 2020 | 30.9 | 3.5 | 11.3% |

_____________

Source: Brazilian Steel Institute (Instituto Aço Brasil), or IABr.

The following table sets forth selected operating statistics for the periods indicated:

|

2020 |

2021 |

2022 | |

| (in millions of tons) | |||

| Production of: | |||

| Molten steel | 3.6 | 4.2 | 3.7 |

| Crude steel | 3.5 | 4.0 | 3.6 |

| Hot-rolled coils and sheets | 3.5 | 4.0 | 3.6 |

| Cold-rolled coils and sheets | 2.4 | 2.5 | 2.2 |

| Galvanized products | 1.5 | 1.5 | 1.4 |

| Tin mill products | 0.4 | 0.4 | 0.4 |

Raw Materials and Suppliers

The main raw materials we use in our integrated steel mill include iron ore, coke, coal (from which we make coke), limestone, dolomite, aluminum, tin and zinc. In addition, our production operations consume water, gases, energy and ancillary materials.

Iron Ore

We are able to obtain the majority of our iron ore requirements from our Casa de Pedra and Engenho mines located in the state of Minas Gerais. The only iron ore product that we buy from third parties is pellet. For more information, see “—Our Mining Segment.”

Coal

In 2022, our metallurgical coal consumption was 1.37 million tons. Metallurgical coal includes coking coal and PCI coal, which is a lower grade coal injected into blast furnaces, in pulverized form, to reduce coke consumption. The PCI system reduces our need for imported coke, thereby reducing production costs. Our total PCI coal consumption in 2022 was 0.50 million tons, all of which was imported. The sources of the hard coking coal consumed in our plants in 2022 were as follows: United States (59.4%) and Australia (40.6%); and for PCI: Russia (83.9%), China (15.2%) and Colombia (0.9%).

Coke

In 2022, in addition to approximately 0.64 million tons of coke we produced, we also consumed 1.23 million tons of coke purchased from third parties in China, Japan, India, United States, Australia and Colombia, which represented a decrease of 11.9% compared to our consumption in 2021.

Limestone and Dolomite

Our Bocaina Mine is located in the city of Arcos, in the state of Minas Gerais, and has been supplying, since the early 1970s, limestone (calcium carbonate) and dolomite (dolomitic limestone) to our Presidente Vargas Steelworks in Volta Redonda. These products are used in the process of sintering and calcination. Arcos has one of the largest and highest quality reserves of limestone in the world. Limestone is used in the production of various products, including clinker and cement.

The annual production of limestone and dolomite for our steelworks is approximately 5.9 million tons.

| 11 |

The main products obtained from limestone and dolomite that are transferred to our steelworks in Volta Redonda are:

| · | Limestone and dolomite calcination: with a granulometry between 32 and 76 mm, they are used in the lime plant in Volta Redonda to produce calcitic and dolomitic lime, for further use in the steelmaking process and sintering. At the steelworks, lime is used for chemical controlling of liquid slag, in order to preserve the refractory of the converters and assist in the stabilization of the chemical reactions that occur during the steel manufacturing process. During sintering, the purpose of lime is to increase the performance of this process and the final quality of the sinter that is produced. |

| · | Limestone and dolomite fines for sintering: used in the production of “sinter” in our steelworks. The sintering process mixes and heats together with fine ores, solid fuel and flux, producing a highly reactive granulated burden. The sinter is used in blast furnaces as the main source of iron for the production of pig iron. |

The Bocaina Mine is also responsible for supplying limestone for cement manufacturing in Volta Redonda and Arcos.

Aluminum, Zinc and Tin

Aluminum is mostly used for steelmaking. Zinc and tin are important raw materials used in the production of certain higher-value steel products, such as galvanized and tin plate. We typically purchase aluminum and tin from third-party domestic suppliers and zinc from third-party domestic and international suppliers under annual contracts. We purchase part of our tin from our subsidiary ERSA. We maintain approximately 55, 23 and 25 days’ inventory of tin, aluminum and zinc, respectively, at the Presidente Vargas Steelworks.

Other Raw Materials

In our production of steel, we consume, on an annual basis, significant amounts of spare parts, refractory bricks and lubricants, which we generally purchase from domestic suppliers.

We also consume significant amounts of oxygen, nitrogen, hydrogen, argon and other gases at the Presidente Vargas Steelworks. These gases are supplied by a third-party under a long-term contract from gas production facilities located on the Presidente Vargas Steelworks site.

In 2022, we used 568,661 tons of oxygen in the Presidente Vargas Steelworks site.

Water

We require large quantities of water in the production of steel. Water serves as a solvent, a catalyst and a cleaning agent. It is also used to cool, carry waste, help produce and distribute heat and power and dilute liquids. Our source of water is the Paraíba do Sul River, which runs through the city of Volta Redonda. 94.4% of the water used in the steelmaking process is recirculated and the balance, after careful processing, is returned to the Paraíba do Sul River. Since March 2003, the Brazilian government has imposed an annual tax of R$3.1 million for our use of water from the Paraíba do Sul River.

Natural Gas

The market for natural gas is strongly correlated with the energy market and we consume both natural gas and electrical energy, mainly in our hot strip mill. Naturgy (formerly Companhia Estadual de Gás do Rio de Janeiro S.A.) is our primary natural gas supplier. To secure natural gas supply, we maintain a “take-or-pay” agreement with Naturgy, pursuant to which we committed to acquire at least 70% of the gas volume it provides. If we do not acquire this minimum volume, we may compensate the difference in amount paid in future years up to one year after the contract’s termination. In 2022, the Presidente Vargas Steelworks consumed 422.8 million cubic meters of natural gas.

Diesel Oil

We maintain agreements with Companhia Brasileira de Petróleo Ipiranga, or Ipiranga, to receive diesel oil in order to supply our equipment in our mining plants in the state of Minas Gerais, which provide the iron ore, dolomite and limestone used in our steel plant in Volta Redonda.

| 12 |

In 2022, our diesel oil consumption was 73,942 kiloliters, used to produce 24.3 million tons of iron ore, for which we paid R$362.4 million. For more information, see “Item 3. Key Information––3D. Risk Factors—Risks Relating to Us and the Industries in Which We Operate—We are exposed to substantial changes in commodities prices, including oil prices, which significantly affect the prices of our inputs and the prices of our products, and may adversely affect us.”

Suppliers

We acquire our inputs in Brazil and abroad. Aluminum, zinc, tin, spare parts, refractory bricks, lubricants, oxygen, nitrogen, hydrogen and argon are the main inputs we acquire in Brazil. Coal and coke are the only inputs we acquire abroad.

In 2020, 2021 and 2022, we consumed 75,971 tons, 207,344 tons and 190,256 tons, respectively, of third-party slabs.

Following are our main raw materials suppliers:

|

Main Suppliers |

Raw Material |

| Ternium | Slabs |

| BHP, Kru Overseas, Warrior, Alpha Metallurgical, Suek AG, E-Commodities and German Creek | Coal |

| CI Milpa, Trafigura, Sinochem and Noble | Coke |

| TAG, Ibrame and IBM Metais | Aluminum |

| Zinco Ligas, Sorin and IBM Metais | Zinc |

| ERSA, Fabrica Auricchio and Mineração Taboca | Tin |

| Sotreq, Minas Máquina, Komatsu, Inova, WLM, Metso and Sany | Spare parts |

| RHI Magnesita, Vesuvius, IBAR, Togni S/A and Saint Gobain | Refractory bricks |

| Iconic, Quaker-Houghton and Daido | Lubricants |

| Vale, Vallourec and Samarco | Pellet |

| Ipiranga | Diesel oil |

Flat Steel Mill

The Presidente Vargas Steelworks, located in the city of Volta Redonda, in the state of Rio de Janeiro, began operating in 1946. It is an integrated facility covering approximately four square km and containing five coke batteries, three of which are in operation, three sinter plants, two blast furnaces, a basic oxygen furnace steel shop, with three converters, three continuous casting units, one hot strip mill, three cold strip mills, two continuous pickling lines, one continuous annealing line, 28 batch annealing furnaces, three continuous galvanizing lines, four continuous annealing lines exclusively for tin mill products, three of which are in operation, and six electrolytic tinning lines, three of which are in operation.

The annual production capacity of steel at the Presidente Vargas Steelworks is 5.4 million tons.

Downstream Facilities

CSN Paraná

Our CSN Paraná branch produces and supplies plain regular galvanized products, Galvalume® products and pre-painted steel products for the automotive, construction and home appliance industries. The plant has an annual capacity of 295,000 tons of galvanized products and Galvalume® products, 131,000 tons of pre-painted products, which can use cold-rolled or galvanized steel as substrate, service capacity of 150,000 tons of sheets and narrow strips, and 384,000 tons of pickled hot-rolled coils in excess of the coils required for the coating process.

CSN Porto Real

Our CSN Porto Real branch produces and supplies plain regular galvanized, Galvanew and tailored blanks mainly for the automotive industry. The plant has an annual capacity of 350,000 tons of galvanized products, including Galvanew products, and 354,000 tons of tailored blanks, sheets and narrow strips, which can use cold-rolled or galvanized steel as a substrate.

| 13 |

Companhia Metalúrgica Prada

Established in 1936, Companhia Metalúrgica Prada is the largest Brazilian steel can manufacturer and has an annual production capacity of over one billion cans in its five industrial facilities located in the states of São Paulo, Minas Gerais, Rio de Janeiro and Rio Grande do Sul and in the city of Brasília. We are the only Brazilian producer of tin plate, which is Companhia Metalúrgica Prada’s main raw material, making it one of our most important products. Companhia Metalúrgica Prada has important customers in the food and chemical industries, including packages of vegetables, fish, dairy products, meat, aerosols, infant nutrition and other business activities.

Prada Distribuição, the distribution arm of Companhia Metalúrgica Prada, is one of the leaders in the Brazilian distribution market for steel products with 600,000 tons per year of installed processing capacity. Prada Distribuição has two steel service centers and three distribution centers strategically located in the Southeast region of Brazil. The service centers are located in the city of Mogi das Cruzes, in the state of São Paulo, and in the city of Valença, in the state of Rio de Janeiro. Its product mix also includes sheets, slit coils, sections, tubes and roofing in standard or customized format, according to customers’ specifications. Prada Distribuição processes the entire range of products produced by us and services 4,000 customers annually from the civil construction, automotive and home appliances sectors, among others.

For more information on Companhia Metalúrgica Prada’s operations, see “—Investments and Divestitures—Acquisition Activity—Metalgráfica Iguaçu S.A.”

Lusosider Aços Planos, S.A.

Lusosider Aços Planos S.A., or Lusosider, is a flat steel processing facility located in Seixal, near Lisbon, Portugal. Lusosider has the capacity to produce approximately 105,000 tons of hot-rolled pickled coils, 36,000 tons of cold-rolled steel products and 276,000 tons of galvanized steel products per year. Its main customers include service centers and tube making industries.

CSN Distribuição

We have one service center, located in the city of Camaçari, in the state of Bahia, to support sales in the Northeastern and Northern regions of Brazil. We also have a distribution center in the city of Canoas, in the state of Rio Grande do Sul, to support sales in the Southern region of Brazil.

CSN Cut and Bend

We have one service center, located in the city of Vargem Grande Paulista, in the state of São Paulo, to support sales in the Southeast region of Brazil.

SWT Long Steel Mill

In February 2012, we acquired SWT in Germany, which marked our entry into the long steel market. SWT specializes in the production of profiles, including IPE (European I Beams) and HE (European Wide Flange Beams) sections, channels and UPE (Channels with Parallel Flanges) sections and steel sleepers. In total, SWT produces more than 200 types of sections according to different German and international standards. The following table sets forth SWT’s production:

|

2020 |

2021 |

2022 | |

| Production of: | |||

| Beam blank (crude steel) | 812 | 811 | 758 |

| Long steel (finished products) | 769 | 748 | 712 |

SWT possesses a 28 km internal railway system, as well as the logistics infrastructure to ensure supply of scrap and delivery of finished products. The main markets served by SWT include non-residential construction, equipment industries and engineering and transport, in Germany and in neighboring countries, including Poland and the Czech Republic. The following table sets forth SWT’s capacity:

| 14 |

|

Tons per year |

Equipment in operation | |

| Process: | ||

| EAF – Electric Arc Furnace | 1,100,000 | 1 furnace |

| Ladle Furnace | 1,100,000 | 1 furnace |

| Finished Products: | ||

| Section Mill | 1,000,000 | 1 mill |

Raw Materials

The main raw material we use in our long steel production is scrap. In addition, we require electrical energy, natural and technical gases and ancillary materials like ferroalloys, lime, dolomite and foaming coal.

Scrap

Our scrap consumption in 2022 was 0.85 million tons, as compared to 0.92 million tons in 2021. Scrap accounted for approximately 67% and 72% of our production costs in 2022 and 2021, respectively. In 2022, scrap prices increased 13%, as compared to 2021, while production costs increased 23%, mainly due to increased energy costs. We are able to obtain approximately 70% of our scrap needs from within a 250 km vicinity of our production facilities.

Ferroalloys, Lime and Foaming Coal

Because we do not own any sources of ferroalloys, lime or foaming coal, we must buy these raw materials from third-party traders, most of which are located in Europe and source these raw materials from producers around the world.

Rolls

We consume different types of rolls in our rolling mill, usually cast rolls that come from Germany, Italy, Slovenia and China.

Graphite Electrodes

In the smelting shop, which is an electric arc furnace, we use graphite electrodes with a diameter of 750mm. In the ladle furnace, we use electrodes with a diameter of 400mm. We source these electrodes from Europe, Japan and China.

Other Raw Materials

Our production of steel also requires the use of electrodes, rolls, refractory materials and materials for packaging and spare parts, which are mostly purchased from domestic suppliers.

Water

Large amounts of water are required in the production process. Our source of water is the Saale River, located five km from the plant. We use our own water station to pump water via pipelines to the plant.

Electrical Energy and Natural Gas

Steelmaking also requires significant amounts of electrical energy and natural gas, for which we have supply contracts. Under normal conditions, we consume approximately 422 GWh of electrical energy and 392 GWh of natural gas annually.

In 2022, SWT was able to meet its energy needs pursuant to contracts negotiated before the beginning of the conflict between Russia and Ukraine, which conflict resulted in steep price increases for natural gas in Europe throughout the year. In 2023, SWT will need to contract its energy supply in the spot market at significantly higher prices than those paid in 2022.

Suppliers

We acquire the inputs necessary for the production of our products globally. The following table sets forth our main raw materials suppliers:

|

Main Suppliers |

Raw Material |

| Scholz, TSR | Scrap |

| RWE Supply & Trading GmbH | Electrical energy |

| GETEC Energie Gas GmbH | Natural gas |

| Refractories Site Service GmbH | Refractory |

| Graftec, W.A.S., SHOWA DENKO | Electrodes |

| Siemens, Schneider, Voith | Spare parts |

| Irle, Walzengießerei Coswig | Rolls |

| 15 |

Volta Redonda Long Steel Mill

Our Volta Redonda plant for the production of long steel products comprises a 50-ton electric arc steelmaking furnace, 50-ton ladle furnace, continuous casting machine for billets and a hot rolling mill for wire rod and reinforcing bar. This plant is operational and its production increases annually, providing the Brazilian market with products for civil construction and high quality drawing and cold heading applications. In addition to our operational performance improvements, we are developing and negotiating certain equipment enhancements that we expect will provide for nominal capacity of 383 kt/year of billets and 450 kt/year of laminates.

Steelmaking Shop

Designed for an output of 200,000 tons per year, this unit mainly consists of one 50 ton UHP, AC electric arc furnace, one 50 ton ladle furnace, one continuous casting machine for billets with three strands, mobile equipment and cranes, power supply, distribution facilities and auxiliary equipment.

Rolling Mill

Designed for an output of 500,000 tons per year, this unit has one walking-beam reheating furnace, or RHF, a four-stand blooming mill, a 250 ton hot shear, a six-stand roughing mill, a six-stand intermediate mill, a six-stand pre-finishing mill, internal water cooling, a double length flying shear, a stepping cooling bed, a 500 ton cold shear, transfer inspection stand, bundling machine, a water-cooling section before wire finishing mill, a 10-stand high-speed wire finishing mill, a water-cooling section after wire finishing mill, a laying head, a loose coil cooling line, reforming device, bundling machine, stripper and coil handling devices.

Production Output

The following table sets forth the production output of our Volta Redonda long steel mill:

|

2020 |

2021 |

2022 | |

| (in thousands of tons) | |||

| Billets (crude steel) | 223 | 228 | 208 |

| Long steel (finished products) | 216 | 236 | 217 |

Raw Materials and Energy Suppliers

The main raw material we use in our long steel production in Volta Redonda is scrap, in addition to pig iron. We also use blooms, which we produce in our blast furnace. In addition, our production operations consume electrical energy, natural and technical gases and ancillary materials like ferroalloys, lime, dolomite and foaming coal. The supply sources for these materials are the same used for our flat steel operations. See “—Raw Materials and Suppliers.”

| 16 |

Our Mining Segment

Following is an overview of our material mining properties:

Material Mining Properties

|

Name of mining operation |

Location of the mining operation |

Type and amount of ownership interest (%) |

Operator |

Surface (Ha) |

Stage of the mining operation |

Permits |

Key condition of permit |

Type of mine/material |

Beneficiation plant and other installations |

| Casa de Pedra | Congonhas, MG | 79.75 | CSN Mineração | 2,516 | Production | Yes | EIA(1) and others | Open Pit / Iron Ore | Mining facilities and Pires |

| Engenho | Congonhas, MG | 79.75 | CSN Mineração | 344 | Production | Yes | EIA(1) and others | Open Pit / Iron Ore | Mining facilities and Pires |

_____________

| (1) | Environmental Impact Assessment – EIA. Permits or licenses have been obtained, are being renewed or are being processed in accordance with current regulations. |

Following is an overview of our non-material mining properties:

Non-material Mining Properties

|

Name of mining operation |

Location of the mining operation |

Type and amount of ownership interest (%) |

Operator |

Surface (Ha) |

Stage of the mining operation |

Permits |

Key condition of permit |

Type of mine/ material |

Beneficiation plant and other installations |

| Bocaina | Arcos, MG | 100 | CSN Cimentos Brasil | 342.9 | Production | Yes | (2) | Open Pit / Limestone, Dolomite | Bocaina Mining Facilities and Tin (ERSA) |

| Pitimbu | Alhandra, PB | 100 | CSN Cimentos Brasil | 746.7 | Production | Yes | (2) | Open Pit / Limestone, Clay, Sand | Pitimbu Mining Facilities |

| Capoeira Grande | Barroso, MG | 100 | CSN Cimentos Brasil | 93.4 | Production | Yes | (2) | Open Pit / Limestone | Capoeira Grande Mining Facilities |

| Mata do Ribeirão | Barroso, MG | 100 | CSN Cimentos Brasil | 129.7 | Production | Yes | (2) | Open Pit / Limestone | Mata do Ribeirão Mining Facilities |

| Fazenda Campinho | Pedro Leopoldo, MG | 100 | CSN Cimentos Brasil | 661.4 | Production | Yes | (2) | Open Pit / Limestone | Fazenda Campinho Mining Facilities |

| Boa Vista | Montes Claros, MG | 100 | CSN Cimentos Brasil | 432.9 | Production | Yes | (2) | Open Pit / Limestone | Boa Vista Mining Facilities |

| Saudade | Cantagalo, RJ | 100 | CSN Cimentos Brasil | 514.6 | Production | Yes | (2) | Open Pit / Limestone | Saudade Mining Facilities |

| Miramar | Caaporã, PB | 100 | CSN Cimentos Brasil | 983.7 | Production | Yes | (2) | Open Pit / Limestone | Miramar Mining Facilities |

| Fernandinho | Itabirito, MG | 79.75 | Minerios Nacional | 147.0 | Deactivated | Yes | - | Open Pit / Iron Ore | - |

_____________

| (1) | The key permissions to guarantee the respective reserves are: mineral concessions; environmental licenses; and rights to use the property. |

| 17 |

The following tables set forth each individual property’s production information:

Material Mining Properties

|

Name of mining operation |

Location of the mining operation |

Beneficiation plant and other installations |

Aggregate production 2020 (*1000) |

Aggregate production 2021 (*1000) |

Aggregate production 2022 (*1000) |

| Casa de Pedra | Congonhas, MG | Mining facilities and Pires | 25,680 | 26,790 | 23,725 |

| Engenho | Congonhas, MG | Mining facilities and Pires | 2,200 | 5,566 | 7,024 |

Non-material Mining Properties

|

Name of mining operation |

Location of the mining operation |

Beneficiation plant and other installations |

Aggregate production 2020 (tons.) |

Aggregate production 2021 (tons.) |

Aggregate production 2022 (tons.) |

| Bocaina | Arcos, MG | Bocaina Mine and Tin (ERSA) | 2,280,760 | 1,823,878 | 2,315,465 |

| Pitimbu | Alhandra, PB | Pitimbu Mine | 1,734,110 | 1,762,657 | 1,417,962 |

| Capoeira Grande | Barroso, MG | Capoeira Grande Mine | 294,002 | 281,095 | 329,795 |

| Mata do Ribeirão | Barroso, MG | Mata do Ribeirão Mine | 1,323,850 | 1,397,347 | 1,772,303 |

| Fazenda Campinho | Pedro Leopoldo, MG | Fazenda Campinho Mine | 1,168,741 | 1,518,200 | 1,238,936 |

| Boa Vista | Montes Claros, MG | Boa Vista Mine | 864,201 | 906,417 | 1,004,218 |

| Saudade | Cantagalo, RJ | Saudade Mine | 934,103 | 1,037,009 | 986,374 |

| Miramar | Caaporã, PB | Miramar Mine | 1,376,697 | 1,677,637 | 1,833,328 |

| Fernandinho | Itabirito, MG | Fernandinho Mine | - | - | - |

Iron Ore Mining Properties

Our iron ore business is conducted by our subsidiary CSN Mineração in the state of Minas Gerais, within the area called the Iron Quadrangle. Casa de Pedra mine, Engenho mine and Fernandinho mine are our open pit mines. Casa de Pedra mine and Engenho mine belong to the same mining complex and run their own transportation and shipping capabilities. The mining complex comprises the Casa de Pedra Central Plant and the Pires Benefitiation Plant. Fernandinho mine, which is currently deactivated, is located on the North side and, when it was active until 2015, it also ran its own transportation and shipping capabilities.

To complement its iron ore mining properties, CSN Mineração runs the Itaguaí Port, located in the municipality of Itaguaí, state of Rio de Janeiro, and the Presidente Vargas Steel Plant, in the municipality of Volta Redonda, also in the state of Rio de Janeiro.

| 18 |

The following map presents an overview of our iron ore operations:

Our iron ore properties comprise Casa de Pedra and Engenho (both material properties) and Fernandinho (non-material property), as further described below:

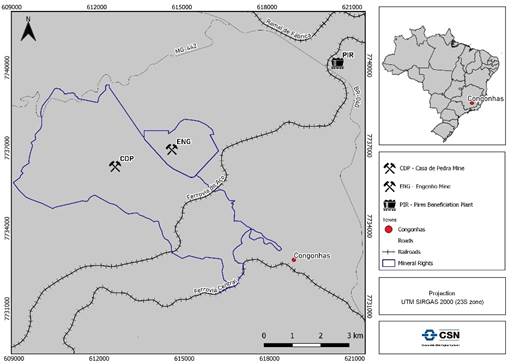

Casa de Pedra Mine – Congonhas, MG

Casa de Pedra mine is our main iron ore mine. It is located in the municipality of Congonhas, 80 km to the South of Belo Horizonte, the capital of the state of Minas Gerais. Its mining concession has no expiration date and covers 2,516 hectares. Casa de Pedra is in full production stage.

Casa de Pedra mine has all the necessary permits for current operations, and the authorization process related to its planned production expansion is running according to schedule. Related facilities, such as waste piles and tailings dams, also comply with applicable legislation.

Casa de Pedra mine is an open pit operation with high grade hematite ore type (iron grade of approximately 64%) mixed with a minor amount of Itabirite ore type (iron grade of approximately 30-60%). Mine occurrences are represented by banded iron formations, varying from low grade (~Fe@30%) to medium/high grade types (~Fe@60%), and supergenous/hypogenous hematite (Fe@64%), all varying from fresh to hard material types. Some types of mineralized covers are also mixed to feed the plant. The geology framework is complex as a consequence of innumerous geological events that created an integrate grade variability scenario. For this reason, mapping and drilling are always reinforced and are one of the work priorities at Casa de Pedra.

The Central Plant is fed with natural high grade run of mine, and the beneficiation process comprises crushing, screening, and flotation. The Central Plant generates lump ore, sinter feed and pellet feed. The Pires beneficiation plant is fed with low to medium grade in a dry beneficiation process.

All products from Casa de Pedra are transported by MRS’s railroad, which transports iron ore to the Itaguaí maritime terminal in the state of Rio de Janeiro.

| 19 |

Engenho Mine – Congonhas, MG

Engenho mine covers 344 hectares and has been integrated in the Casa de Pedra mining complex since 2012. Engenho mine production is constantly mixed with Casa de Pedra mine production, following the same process route.

The following map sets forth a detailed illustration of Casa de Pedra mine and Engenho mine locations:

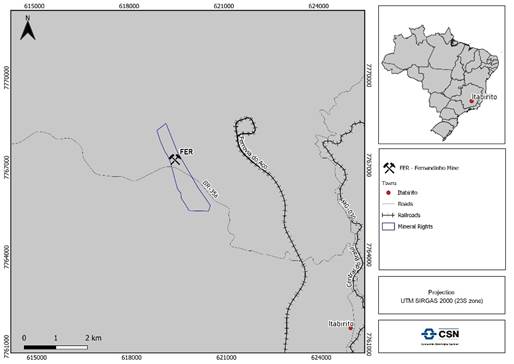

Fernandinho Mine – Itabirito, MG

Fernandinho mine covers 147 hectares and has been integrated in the Casa de Pedra mining complex since 2012. Fernandinho mine’s operations were deactivated in 2015 as part of an internal strategic decision. In the future, additional geological, drilling and resource studies and estimations will be performed in order to update mineral resources conversion to mineral reserves.

The following map sets forth a detailed illustration of Fernandinho mine and its related facilities:

| 20 |

In addition to the mining properties detailed above, CSN Mineração conducts initial exploration activities in the surrounding areas of our mining operations.

The following chart sets forth a summary of our iron ore resources and reserves, updated to December 31, 2022, considering our ownership interest in each property:

|

Measured mineral resources |

Indicated mineral resources |

Measured + Indicated mineral resources |

Inferred mineral resources |

||||||

|

Amount |

Grades/ Qualities |

Amount |

Grades/ Qualities |

Amount |

Grades/ Qualities |

Amount |

Grades/ Qualities |

||

| (Million tonnes) | (% Fe) | (Million tonnes) | (% Fe) | (Million tonnes) | (% Fe) | (Million tonnes) | (% Fe) | ||

| Iron ore: | |||||||||

| Casa de Pedra Mine | 166 | 39.8 | 1,166 | 37.6 | 1,332 | 38.1 | 1,364 | 37.1 | |

| Engenho Mine | 178 | 40.2 | 44 | 46.9 | 222 | 41.6 | 11 | 43.5 | |

| Fernandinho Mine | 42 | 39.8 | 49 | 39.2 | 92 | 39.5 | 50 | 38.6 | |

_____________

Updated December/2022.

|

Proven mineral reserves |

Probable mineral reserves |

Total mineral reserves |

|||||

|

Amount |

Grades/ Qualities |

Amount |

Grades/ Qualities |

Amount |

Grades/ Qualities |

||

| (Million tonnes) | (% Fe) | (Million tonnes) | (% Fe) | (Million tonnes) | (% Fe) | ||

| Iron ore: | |||||||

| Casa de Pedra Mine | 305 | 43.4 | 1,150 | 40.6 | 1,455 | 41.2 | |

| Engenho Mine | 154 | 39.8 | 25 | 46.3 | 179.0 | 40.7 | |

_____________

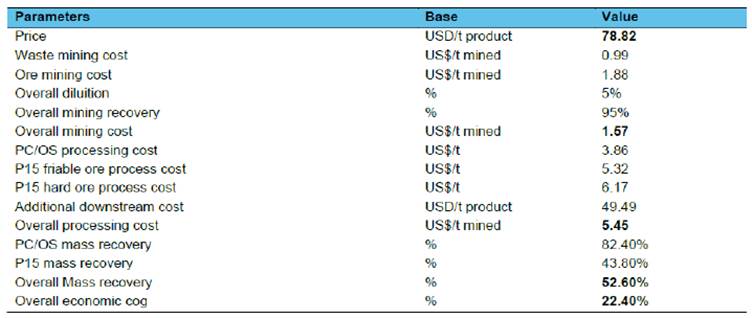

*CSN considers an average price of US$95 per ton for the economic analysis.

Updated December/2022

Casa de Pedra mine and Engenho mine are mill feed material (Run of Mine – ROM) and the point of reference for the mineral reserves is ore delivered to the processing facility.

The following tables set forth Casa de Pedra mine and Engenho mine reserves pit optimization parameters:

_____________

Notes:

Metallurgical recovery or mass recovery for PC/OS = 82.40%

Metallurgical recovery or mass recovery for P15 = 43.80%

Overall metallurgical recovery or mass recovery = 52.60%

Cut-off grade: 22.40%

| 21 |

Cement Mining Properties

The following maps present the location of each non-material cement mining property set forth below:

Bocaina Mine – Arcos, MG:

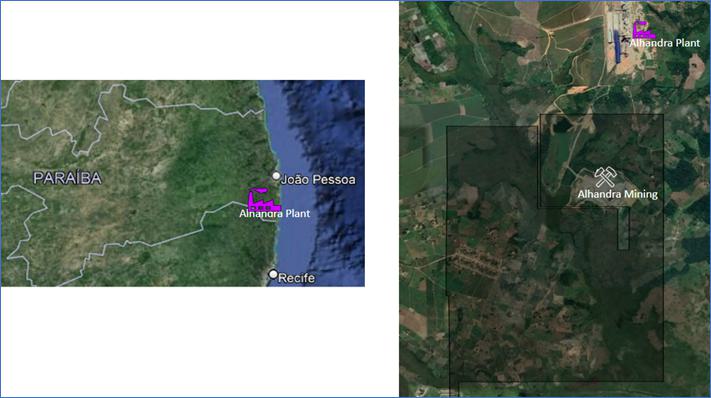

Pitimbu – Alhandra, PB:

| 22 |

Mata do Ribeirão and Capoeira Grande – Barroso, MG:

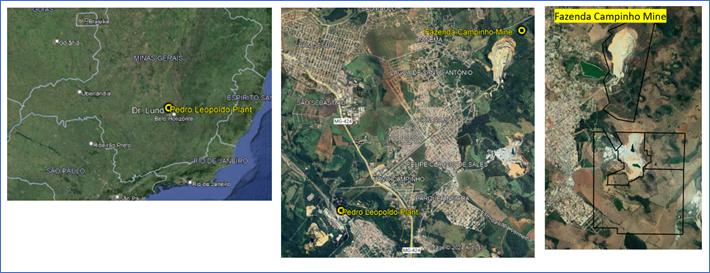

Fazenda Campinho – Pedro Leopoldo, MG:

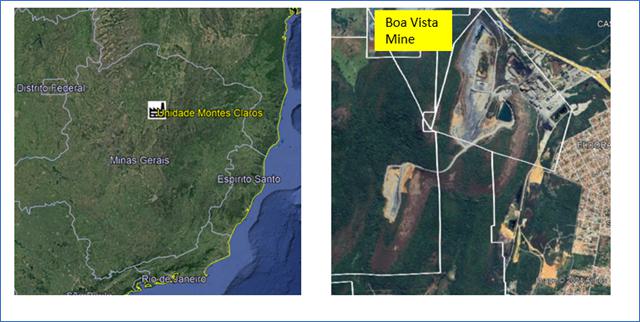

Boa Vista – Montes Claros, MG:

| 23 |

Saudade – Cantagalo, RJ:

Miramar – Caaporã, PB:

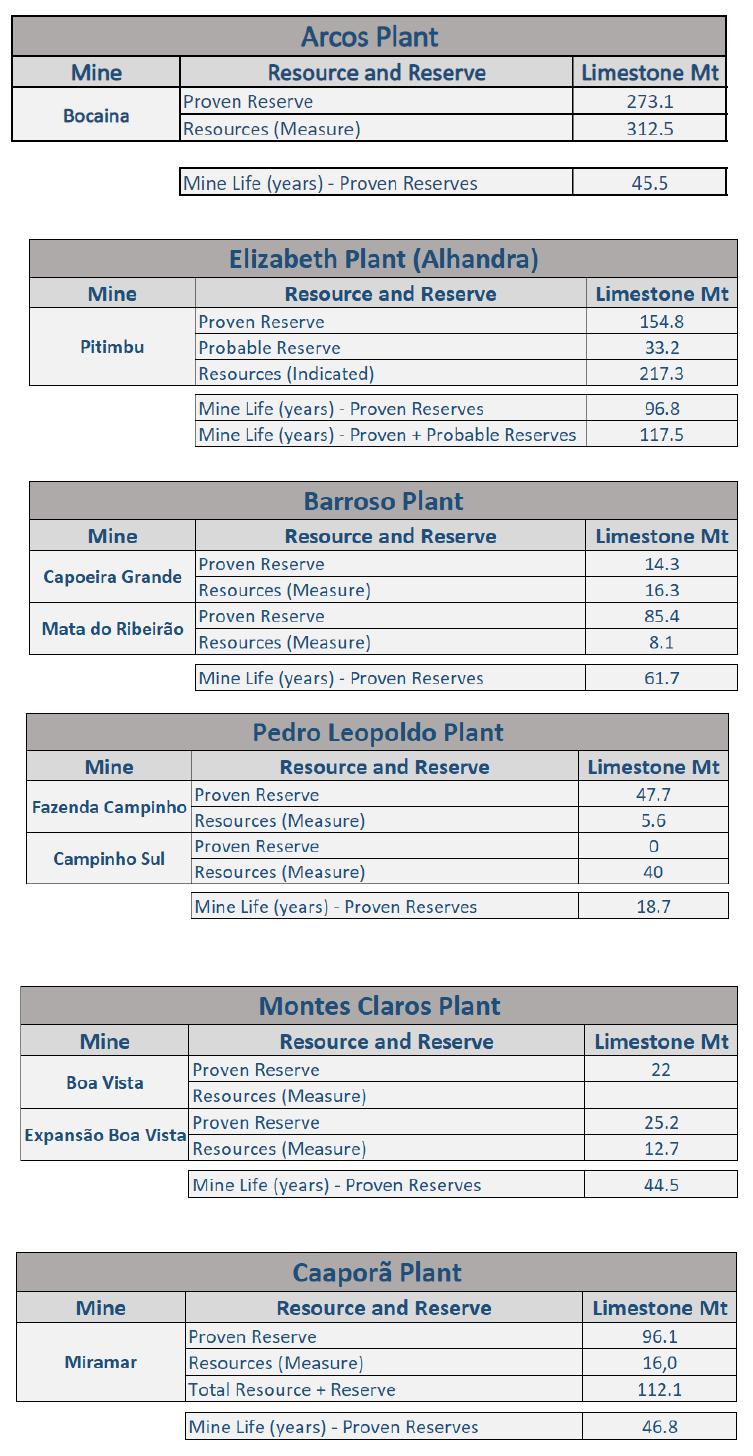

Each property includes a mine: (i) Elizabeth Plant – Pitimbu Mine; (ii) Barroso Plant – Capoeira Grande Mine and Mata do Ribeirão Mine; (iii) Pedro Leopoldo Plant – Pedro Leopoldo Mine (Fazenda Campinho); (iv) Cantagalo Plant – Cantagalo (Saudade Mine); (v) Caaporã Plant – Caaporã (Miramar Mine); (vi) Montes Claros Plant – Mining complex of Montes Claros; and (vii) Arcos – Bocaina Mine.

Each cement mining property is owned 100% by us and holds the respective mining and property rights.