As filed with the Securities and Exchange Commission on April 2, 2020.

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

________________________________________________

FORM 20-F

________________________________________________

|

¨ |

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

|

|

OR | |

|

x |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

|

|

OR | |

|

¨ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

|

|

OR | |

|

¨ |

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Commission File Number 1-14732 |

|

COMPANHIA SIDERÚRGICA NACIONAL

(Exact name of registrant as specified in its charter)

NATIONAL STEEL COMPANY

(Translation of registrant’s name into English)

_______________________________________________

THE FEDERATIVE REPUBLIC OF BRAZIL

(Jurisdiction of incorporation or organization)

Marcelo Cunha Ribeiro, Chief Financial and Investor Relations Officer

Phone: +55 11 3049-7454 Fax: +55 11 3049-7212

marcelo.ribeiro@csn.com.br

Av. Brigadeiro Faria Lima, 3400 – 20th floor

04538-132, São Paulo, SP, Brazil

(Address of principal executive offices)

________________________________________________

Securities registered or to be registered pursuant to Section 12(b) of the Act.

|

Title of each class |

Trading symbol |

Name of each exchange on which registered |

|

Common Shares without Par Value |

* |

New York Stock Exchange |

|

American Depositary Shares (as evidenced by American Depositary Receipts), each representing one share of Common Stock |

SID |

New York Stock Exchange |

____________________

40550.00004

1

None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of December 31, 2019:

1,387,524,047 Common Shares without Par Value

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes þ No

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Yes þ No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

þ Yes No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

þ Yes No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or an emerging growth company. See definition of “large accelerated filer,” “accelerated filer” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer þ |

Accelerated filer |

Non-accelerated filer |

Emerging growth company |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act.

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

|

U.S. GAAP |

International Financial Reporting Standards as issued by the International Accounting Standards Board þ |

Other |

2

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow:

Item 17 Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes þ No

3

TABLE OF CONTENTS

440550.00004

5

INTRODUCTION

Unless otherwise specified, all references in this annual report to:

· “we,” “us,” “our” or “CSN” are to Companhia Siderúrgica Nacional and its consolidated subsidiaries;

· “Brazil” are to the Federative Republic of Brazil;

· “Brazilian government” are to the federal government of Brazil;

· “real,” “reais” or “R$” are to Brazilian reais, the official currency of Brazil;

· “U.S. dollars” or “US$” are to United States dollars;

· “km” are to kilometers, “m” are to meters, “mt” or “tons” are to metric tons, “mtpy” are to metric tons per year and “MW” are to megawatts;

· “TEUs” are to twenty-foot equivalent units;

· “consolidated financial statements” are to our audited consolidated financial statements prepared in accordance with International Financial Reporting Standards, or IFRS, as issued by the International Accounting Standards Board, or IASB, as of December 31, 2019 and 2018 and for the years ended December 31, 2019, 2018 and 2017, together with the corresponding report of our independent registered public accounting firm; and

· “ADSs” are to the American depositary shares and “ADRs” are to the American depositary receipts representing our common shares.

FORWARD-LOOKING STATEMENTS

This annual report includes forward-looking statements, within the meaning of Section 27A of the U.S. Securities Act of 1933, as amended, or the Securities Act, and Section 21E of the U.S. Securities Exchange Act of 1934, as amended, or the Exchange Act, principally under the captions “Item 3. Key Information,” “Item 4. Information on the Company,” “Item 5. Operating and Financial Review and Prospects” and “Item 11. Quantitative and Qualitative Disclosures About Market Risk.” We have based these forward-looking statements largely on our current beliefs, expectations and projections about future events and financial trends affecting us. Although we believe these estimates and forward-looking statements are based on reasonable assumptions, these estimates and statements are subject to several risks and uncertainties and are made in light of the information currently available to us.

Many important factors, in addition to those discussed elsewhere in this annual report, could cause our actual results to differ substantially from those anticipated in our forward-looking statements, including, among others:

· general economic, political and business conditions in Brazil and abroad, especially in China, which is the largest world steel producer and main consumer of our iron ore;

· demand for and prices of steel and mining products;

· the effects of the global financial markets and economic slowdowns;

· changes in competitive conditions and the general level of demand and supply for our products;

· our liquidity position and leverage and our ability to obtain financing on satisfactory terms;

· management’s expectations and estimates concerning our future financial performance and financing plans;

· availability and price of raw materials;

· changes in international trade or international trade regulations;

· protectionist measures imposed by Brazil and other countries;

· our capital expenditure plans;

· inflation, interest rate levels and fluctuations in foreign exchange rates;

40550.00004

6

· our ability to develop and deliver our products on a timely basis;

· lack of infrastructure in Brazil;

· electricity and natural gas shortages and government responses to these;

· existing and future governmental regulation;

· threats or outbreaks of diseases or natural disasters affecting the global economy and international trade; and

· the risk factors discussed under the caption “Item 3D. Risk Factors.”

We caution you that the foregoing list of significant factors may not contain all of the material factors that are important to you. The words “believe,” “may,” “will,” “aim,” “estimate,” “plan,” “continue,” “anticipate,” “intend,” “expect” and similar words are intended to identify forward-looking statements. Forward-looking statements include information concerning our possible or assumed results of operations, business strategies, financing plans, competitive position, industry environment, potential growth opportunities, the effects of regulation and the effects of competition, among others.

Forward-looking statements speak only as of the date they were made, and we undertake no obligation to publicly update or to revise any forward-looking statements after we distribute this annual report because of new information, future events or other factors. In light of the risks and uncertainties described above, the forward-looking events and circumstances discussed in this annual report might not occur and are not an indication of future performance. As a result of various factors, including those risks described in “Item 3D. Risk Factors,” undue reliance should not be placed on these forward-looking statements.

PRESENTATION OF FINANCIAL AND OTHER INFORMATION

Our audited consolidated financial statements as of December 31, 2019 and 2018 and for the years ended December 31, 2019, 2018 and 2017 included elsewhere in this annual report have been presented in thousands of reais and prepared in accordance with IFRS as issued by the IASB. See note 2.a. to our audited consolidated financial statements.

We have translated some of the Brazilian real amounts contained in this annual report into U.S. dollars solely for the convenience of the reader at the rate of R$4.0307 to US$1.00, which was the U.S. dollar selling rate as of December 31, 2019, as reported by the Central Bank of Brazil, or the Central Bank. As a result of fluctuations in the real/U.S. dollar exchange rate, the U.S. dollar selling rate as of December 31, 2019 may not be indicative of current or future exchange rates. As of March 31, 2020, the U.S. dollar selling rate was R$5.199 to US$1.00, as reported by the Central Bank, representing a 29% depreciation of the real against the U.S. dollar in 2020 to date. The U.S. dollar equivalent information presented in this annual report should not be construed as implying that the real amounts represent, or could have been or could be converted into, U.S. dollars at such rates or at any other rate.

Certain figures included in this annual report have been subject to rounding adjustments. Accordingly, figures shown as totals in certain tables may not represent an arithmetic sum of the figures that precede them.

Certain Non-IFRS Financial Measures

This annual report includes certain references to the non-IFRS measures of EBITDA and Adjusted EBITDA.

We calculate EBITDA as net income (loss) for the period plus net financial income (expenses), income tax and social contribution, depreciation and amortization and results from discontinued operations. We calculate adjusted EBITDA as net income (loss) for the period plus net financial income (expenses), income tax and social contribution, depreciation and amortization and results of discontinued operations, plus other operating income (expenses), equity in results of affiliated companies and the proportionate EBITDA of joint ventures. EBITDA and adjusted EBITDA are not measures of financial performance recognized under Brazilian GAAP or IFRS and they should not be considered alternatives to net income (loss) as measures of operating performance, or as alternatives to operating cash flows, or as measures of liquidity. EBITDA and adjusted EBITDA are not calculated using a standard methodology and may not be comparable to the definition of EBITDA or adjusted EBITDA, or similarly titled measures, used by other companies.

40550.00004

7

PART I

Item 1. Identity of Directors, Senior Management and Advisors

Not applicable.

Item 2. Offer Statistics and Expected Timetable

Not applicable.

Item 3. Key Information

3A. Selected Financial Data

We present in this section summary consolidated financial data derived from, and that should be read in conjunction with, our audited consolidated financial statements included elsewhere in this annual report, and summary consolidated operating data.

Due to the adoption of IFRS 16 as of January 1, 2019, which we did not apply retroactively, financial information as of and for the year ended December 31, 2019 may not be comparable with financial information for prior periods. For further information on our adoption of IFRS 16, see note 13.a to our audited consolidated financial statements included elsewhere in this annual report.

Summary Financial and Operating Data

The following tables present summary consolidated financial and operating data for each of the periods indicated:

|

|

Year ended December 31, | |||||

|

Income Statement Data: |

2015(4) |

2016(4) |

2017 |

2018(1) |

2019(2) |

2019(3) |

|

|

(in million of R$, except per share data) |

(in million of US$, except per share data) | ||||

|

Net operating revenues |

15,262 |

16,126 |

18,525 |

22,969 |

25,436 |

6,311 |

|

Cost of products sold |

(11,740) |

(11,592) |

(13,596) |

(16,106) |

(17,263) |

(4,283) |

|

Gross profit |

3,522 |

4,534 |

4,929 |

6,863 |

8,173 |

2,028 |

|

Operating expenses |

|

|

|

|

|

|

|

Selling |

(1,430) |

(1,042) |

(1,815) |

(2,264) |

(2,343) |

(581) |

|

General and administrative |

(470) |

(438) |

(416) |

(494) |

(511) |

(127) |

|

Equity in results of affiliated companies |

1,160 |

331 |

109 |

136 |

126 |

31 |

|

Other expenses |

(1,341) |

(657) |

(647) |

(1,331) |

(2,407) |

(597) |

|

Other income |

3,610 |

90 |

824 |

4,036 |

504 |

125 |

|

Total |

1,529 |

(1,716) |

(1,945) |

83 |

(4,631) |

(1,149) |

|

|

|

|

|

|

|

|

|

Operating income |

5,051 |

2,818 |

2,984 |

6,946 |

3,542 |

879 |

|

Non-operating income (expenses), net |

|

|

|

|

|

|

|

Financial income |

488 |

172 |

295 |

1,311 |

379 |

94 |

|

Financial expenses |

(3,853) |

(3,253) |

(2,759) |

(2,806) |

(2,510) |

(623) |

|

|

|

|

|

|

|

|

|

Income (loss) before taxes |

1,686 |

(263) |

520 |

5,451 |

1,411 |

350 |

|

Income tax |

|

|

|

|

|

|

|

Current |

(136) |

(528) |

(359) |

(827) |

(1,564) |

(388) |

|

Deferred |

(2,768) |

679 |

(50) |

577 |

2,398 |

595 |

|

|

|

|

|

|

|

|

|

Net income (loss) for the period |

(1,218) |

(112) |

111 |

5,201 |

2,245 |

557 |

|

|

|

|

|

|

|

|

|

Net income (loss) attributable to noncontrolling interest |

(2) |

(7) |

101 |

126 |

455 |

113 |

|

Net income (loss) attributable to Companhia Siderúrgica Nacional |

(1,213) |

(105) |

10 |

5,075 |

1,789 |

444 |

|

Basic earnings per common share |

(0.89461) |

(0.07443) |

0.00757 |

3.69498 |

1.29632 |

0.32161 |

|

Diluted earnings per common share |

(0.89461) |

(0.07443) |

0.00757 |

3.69498 |

1.29632 |

0.32161 |

40550.00004

8

|

|

As of December 31, | |||||

|

Balance Sheet Data: |

2015 |

2016 |

2017 |

2018(2) |

2019(3) |

2019(1) |

|

|

(in million of R$) |

(in million of US$, except per share data) | ||||

|

Current assets |

16,431 |

12,445 |

11,881 |

12,014 |

12,726 |

3,157 |

|

Investments |

3,998 |

4,568 |

5,499 |

5,631 |

3,584 |

889 |

|

Property, plant and equipment |

17,826 |

18,136 |

17,965 |

18,047 |

19,701 |

4,888 |

|

Other assets |

9,084 |

9,005 |

9,865 |

11,636 |

14,858 |

3,686 |

|

Total assets |

47,339 |

44,154 |

45,210 |

47,328 |

50,869 |

12,620 |

|

Current liabilities |

5,082 |

5,497 |

10,670 |

11,439 |

11,620 |

2,883 |

|

Non -current liabilities |

35,166 |

31,272 |

26,252 |

25,876 |

27,887 |

6,919 |

|

Stockholders’ equity |

7,091 |

7,385 |

8,288 |

10,013 |

11,362 |

2,819 |

|

Total liabilities and stockholders’ equity |

47,339 |

44,154 |

45,210 |

47,328 |

50,869 |

12,620 |

|

Paid-in capital (in millions of reais ) |

4,540 |

4,540 |

4,540 |

4,540 |

4,540 |

1,126 |

|

Common shares (quantities) |

1,388 |

1,388 |

1,388 |

1,388 |

1,388 |

1,388 |

|

Dividends declared and interest on stockholders’ equity |

275 |

- |

- |

898 |

1,023 |

254 |

|

Dividends declared and interest on stockholders’ equity per common share (in reais )(4) |

0.20 |

- |

- |

0.65 |

0.74 |

0.18 |

_______________________

(1) Due to the adoption of IFRS 9 and IFRS 15 as of January 1, 2018, which we did not apply retroactively, financial information as of and for the year ended December 31, 2018 may not be comparable with financial information as of and for prior periods. For further information on our adoption of IFRS 9 and IFRS 15, see note 2.w and 2.q, respectively, to our audited consolidated financial statements included elsewhere in this annual report.

(2) Due to the adoption of IFRS 16 as of January 1, 2019, which we did not apply retroactively, financial information as of and for the year ended December 31, 2019 may not be comparable with financial information as of and for prior periods. For a description of the impact of IFRS 16 on our results of operations, see note 13.a to our audited consolidated financial statements included elsewhere in this annual report.

(3) Translated solely for the convenience of the reader at the rate of R$4.0307 to US$1.00, which was the U.S. dollar selling rate as of December 31, 2019, as reported by the Central Bank. As of March 31, 2020, the U.S. dollar selling rate was R$5.199 to US$1.00, as reported by the Central Bank.

(4) Due to the adoption of IFRS 9 and IFRS 15 as of January 1, 2018, which we did not apply retroactively, financial information as of and for the year ended December 31, 2018 is not comparable with financial information as of and for prior periods.

|

|

Year ended December 31, | |||

|

|

2017 |

2018 |

2019 |

2019(1) |

|

Reconciliation of Net Income (Loss) to EBITDA and Adjusted EBITDA |

(in millions of US$) |

(in millions of R$) | ||

|

Net income (loss) |

111.2 |

5,200.6 |

2,244.5 |

556.9 |

|

Depreciation/amortization/depletion |

1,408.8 |

1,175.1 |

1,421.7 |

352.7 |

|

Income tax and social contribution |

409.1 |

250.3 |

(833.8) |

(206.9) |

|

Financial income (expenses) |

2,463.6 |

1,495.6 |

2,131.2 |

528.7 |

|

EBITDA(2) |

4,392.7 |

8,121.7 |

4,963.6 |

1,231.5 |

|

Other operating income (expenses) |

(177.3) |

(2,705.3) |

1,903.1 |

472.1 |

|

Equity in results of affiliated companies |

(109.1) |

(135.7) |

(125.7) |

(31.2) |

|

Proportionate EBITDA of joint ventures |

538.2 |

568.0 |

510.1 |

126.5 |

|

Adjusted EBITDA(3) |

4,644.4 |

5,848.7 |

7,251.0 |

1,799.0 |

_______________________

(1) Translated solely for the convenience of the reader using the U.S. dollar selling rate as reported by the Central Bank of R$4.0307 to US$1.00 as of December 31, 2019. As of March 31, 2020, the U.S. dollar selling rate was R$5.199 to US$1.00, as reported by the Central Bank.

(2) We calculate EBITDA as net income (loss) for the period plus net financial income (expenses), income tax and social contribution, depreciation and amortization and results from discontinued operations.

(3) We calculate adjusted EBITDA as net income (loss) for the period plus net financial income (expenses), income tax and social contribution, depreciation and amortization and results of discontinued operations, plus other operating income (expenses), equity in results of affiliated companies and the proportionate EBITDA of joint ventures. EBITDA and adjusted EBITDA are not measures of financial performance recognized under Brazilian GAAP or IFRS and they should not be considered alternatives to net income (loss) as measures of operating performance, or as alternatives to operating cash flows, or as measures of liquidity. EBITDA and adjusted EBITDA are not calculated using a standard methodology and may not be comparable to the definition of EBITDA or adjusted EBITDA, or similarly titled measures, used by other companies.

3B. Capitalization and Indebtedness

Not applicable.

40550.00004

9

3C. Reasons for the Offer and Use of Proceeds

Not applicable.

3D. Risk Factors

An investment in the ADSs or our common shares involves a high degree of risk. You should carefully consider the risks described below before making an investment decision. Our business, financial condition and results of operations could be materially and adversely affected by any of these risks. The trading price of the ADSs could decline due to any of these risks or other factors, and you may lose all or part of your investment.

For purposes of this section, when we state that a risk, uncertainty or problem may, could or will have an “adverse effect” on us or “adversely affect” us, we mean that the risk, uncertainty or problem could have an adverse effect on our business, financial condition, results of operations, cash flow, prospects and/or the trading price of the ADSs, except as otherwise indicated. The risks described below are those that we currently believe may materially and adversely affect us.

The Brazilian government has exercised, and continues to exercise, significant influence over the Brazilian economy and such involvement, along with general political and economic conditions, could adversely affect us.

The Brazilian government has frequently intervened in the Brazilian economy and occasionally made changes in policy and regulations. The Brazilian government’s actions to control inflation and affect policies and regulations have often involved, among other measures, increases in interest rates, changes in tax and social security policies, price controls, currency exchange and remittance controls, devaluations, capital controls and limits on imports. We may be adversely affected by changes in policy or regulations at the federal, state or municipal level involving or affecting the following factors, among others:

· interest rates;

· exchange controls;

· currency fluctuations;

· inflation;

· price volatility of raw materials and our final products;

· lack of infrastructure in Brazil;

· energy and water supply shortages and rationing programs;

· liquidity of the domestic capital and lending markets;

· regulatory policy for the mining, steel, cement, logistics and energy industries;

· environmental policies and regulations;

· tax policies and regulations, including frequent changes that may result in uncertainties regarding future taxation; and

· other political, social and economic developments in or affecting Brazil.

Uncertainty over whether the Brazilian government will implement changes in policy or regulation affecting these or other factors may contribute to economic uncertainty in Brazil and to heightened volatility in the Brazilian securities markets and securities issued abroad by Brazilian companies.

According to the Brazilian Institute of Geography and Statistics (Instituto Brasileiro de Geografia e Estatística), or the IBGE, Brazil’s gross domestic product, or GDP, grew by 1.0% in 2017, 1.1% in 2018 and 1.1% in 2019, following an economic recession in 2015 and 2016.

These uncertainties, together with a slow economic recovery that Brazil is undergoing and other future developments in the Brazilian economy, may adversely affect us.

40550.00004

10

Political instability may adversely affect us.

The Brazilian economy has been affected by political events in Brazil, which have also affected the confidence of investors and the public in general.

Brazilian markets have been experiencing heightened volatility due to uncertainties derived from the ongoing Lava Jato investigation and other investigations, which are conducted by the Brazilian Federal Police and the Federal Prosecutor’s Office, and the impact of these investigations on the Brazilian economy and political environment. Numerous members of the Brazilian government and of the legislative branch, as well as senior officers of large state-owned and private companies have been convicted of political corruption related to bribes by means of kickbacks on contracts granted by the government to several infrastructure, oil and gas and construction companies, among others. Profits from these kickbacks allegedly financed the political campaigns of political parties that were unaccounted for or not publicly disclosed, and served to further the personal enrichment of the recipients of the bribery scheme. As a result, a number of politicians and officers of large state-owned and private companies in Brazil have resigned and/or have been arrested and others remain under investigation for unethical and illegal behavior.

The ultimate outcome of these investigations is uncertain, but they have already had an adverse impact on the image and reputation of the implicated companies, and on the general market perception of the Brazilian economy. The development of these unethical conduct cases has and may continue to adversely affect us. We cannot predict whether the investigations in course will result in heightened economic and political volatility in Brazil or whether new investigations against politicians or officers of private companies will occur in the future.

In addition, in October 2018, following a divisive presidential race, congressman Jair Bolsonaro became Brazil’s president on January 1, 2019. It is unclear if and for how long the political divisions in Brazil that arose prior to the elections will continue under Mr. Bolsonaro’s presidency and the effects that any such divisions will have on Mr. Bolsonaro’s ability to govern Brazil and implement reforms. Any continuation of such divisions could result in congressional deadlock, political unrest and massive demonstrations or strikes that could materially adversely affect our operations. Uncertainties in relation to the new government’s implementation of monetary, tax and pension fund policy changes may contribute to economic instability. These uncertainties and new measures may increase market volatility of securities issued by Brazilian companies.

The president of Brazil has the power to determine policies and issue governmental acts relating to the Brazilian economy that affect the operations and financial performance of companies in Brazil, including ours. We cannot predict which policies the newly elected president will adopt or if these policies or changes in current policies may have an adverse effect on the Brazilian economy or us.

Exchange rate instability may adversely affect us and the market price of our common shares and ADSs.

The Brazilian currency has, during the last decade, experienced frequent and substantial variations compared to the U.S. dollar and other foreign currencies. As of December 31, 2017, the U.S. dollar selling rate was R$3.308 per US$1.00. In 2018 and 2019, the real depreciated against the U.S. dollar and the U.S. dollar selling rate was R$3.8748 per US$1.00 as of December 31, 2018 and R$4.0307 per US$1.00 as of December 31, 2019, as reported by the Central Bank. As of March 31, 2020, the U.S. dollar selling rate was R$5.199 per US$1.00, as reported by the Central Bank, representing a 29% depreciation of the real against the U.S. dollar in 2020 to date.

Depreciation of the real against the U.S. dollar creates inflationary pressures in Brazil and causes increases in interest rates, which negatively affect the growth of the Brazilian economy as a whole, curtail access to foreign financial markets and may prompt government intervention, including recessionary governmental policies. Depreciation of the real against the U.S. dollar may also, in the context of an economic slowdown, lead to decreased consumer spending, deflationary pressures and reduced growth of the Brazilian economy.

On the other hand, appreciation of the real relative to the U.S. dollar and other foreign currencies could lead to a deterioration of the Brazilian foreign exchange current accounts, as well as dampen export-driven growth. Depending on the circumstances, either depreciation or appreciation of the real could materially affect our growth and that of the Brazilian economy, as well as impact the U.S. dollar value of distributions and dividends on and the U.S. dollar equivalent of the market price of our common shares and ADSs.

40550.00004

11

In the event the real depreciates in relation to the U.S. dollar, the cost in reais of our foreign currency-denominated borrowings and imports of raw materials, particularly coal and coke, will increase. On the other hand, if the real appreciates in relation to the U.S. dollar, it will cause real-denominated production costs to increase as a percentage of total production costs and cause our exports to be less competitive. We have a total U.S. dollar-denominated or -linked indebtedness of R$16,558 million, which represents 59% of our total indebtedness, as of December 31, 2019.

Government efforts to combat inflation may hinder the growth of the Brazilian economy and could harm us.

Historically, Brazil has experienced high inflation rates. Inflation and certain actions taken by the Central Bank to curb it have had significant negative effects on the Brazilian economy. Inflation as measured by the national broad consumer price index (Índice Nacional de Preços ao Consumidor Amplo), or IPCA, was 3.0%, 3.8% and 4.3% in 2017, 2018 and 2019, respectively, and (0.5)%, 7.5% and 7.3%, respectively, as measured by the general market price index (Índice Geral de Preços do Mercado), or IGP-M.

The base interest rate for the Brazilian banking system is the Central Bank’s Special System for Settlement and Custody (Sistema Especial de Liquidação e Custódia) rate, or SELIC rate. As of December 31, 2017, 2018 and 2019, the SELIC rate was 7.00%, 6.50% and 4.5%, respectively.

Inflation and the Brazilian government’s measures to fight it, principally the Central Bank’s monetary policy, have had and may have significant effects on the Brazilian economy and us. Tight monetary policies with high interest rates have restricted and may restrict Brazil’s growth and the availability of credit. Conversely, more lenient government and Central Bank policies and interest rate decreases have triggered and may trigger increases in inflation, and, consequently, growth volatility and the need for sudden and significant interest rate increases, which could negatively affect us and increase the payments on our indebtedness.

Developments and the perception of risk in other countries, especially other emerging market countries, may adversely affect the trading price of Brazilian securities, including our common shares and ADSs.

The market value of securities of Brazilian issuers is affected by economic and market conditions in other countries, especially other emerging market countries. Although economic conditions in these countries may differ significantly from economic conditions in Brazil, investors’ reactions to developments in these other countries may have an adverse effect on the market value of securities of Brazilian issuers. Crises in the United States, the European Union or emerging market countries may diminish investor interest in securities of Brazilian issuers, including ours. This could adversely affect the trading price of our common shares and/or ADSs, and could also make it more difficult for us to gain access to the capital markets and finance our operations on acceptable terms, or at all.

Further, crises in world financial markets, such as in 2008, as well as global economic challenges as of the date of this annual report deriving from the outbreak of the new coronavirus, or COVID-19, and government measures to contain it, could affect investors’ views of securities issued by companies that operate in emerging markets. These developments could adversely affect the trading price of our common shares and the ADSs, and could also make it more difficult for us to access the capital markets and finance our operations on acceptable terms, or at all.

Risks Relating to Us and the Industries in Which We Operate

We are exposed to substantial changes in the demand for steel and iron ore, which significantly affect the prices of our products and may adversely affect us.

The steel and mining industries are highly cyclical, both in Brazil and abroad. The demand for steel and mining products and, thus, the financial condition and results of operations of companies in these industries, including us, are generally affected by macroeconomic fluctuations in the world economy and the economies of steel-producing countries, including trends in the automotive, construction, home appliances and packaging industries, as well as other industries which rely on steel distributors. A worldwide recession, an extended period of below-trend growth in developed countries or a slowdown in the emerging markets that are large consumers of our products (such as the domestic Brazilian market for our steel products and the Chinese market for iron ore) could sharply reduce demand for our products. In addition, flat steel competes with other materials that may be used as substitutes, such as aluminum (particularly in the automotive and packaging industry), cement, composites, glass, plastic and wood. Government regulatory initiatives mandating the use of such materials in lieu of steel, whether for environmental or other reasons, as well as the development of other new substitutes for steel products, could also significantly reduce market prices and demand for steel products and thereby reduce our cash flow and profitability. In addition, public health epidemics such as the outbreak of COVID-19 could materially and adversely affect global macroeconomic conditions and, consequently, the demand for steel and iron ore. Any material decrease in demand or increase in supply for steel and iron ore in the domestic or export markets served by us could have a material adverse effect on us.

40550.00004

12

Prices charged for iron ore are subject to volatility. International iron ore prices may decrease significantly and have a material and adverse impact on us or require us to suspend certain of our projects and operations.

Our iron ore prices are based on a variety of pricing terms, which generally use market price indices as a basis for determining customer prices. Our prices for and revenues from iron ore are consequently volatile, which may adversely affect us. In 2019, average iron ore prices increased 34.5% to US$93.4/dmt, from US$69.5/dmt in 2018. In 2018, average iron ore prices decreased 2.6% to US$69.5/dmt, from US$71.3/dmt in 2017, according to the average Platts IODEX (62% Fe CFR China). On March 30, 2020, the index was US$82.55/dmt. A decrease in market prices for iron ore may require us to change the way we operate or, depending on the magnitude of price decreases, even to suspend certain of our projects and operations and impair certain assets, which could adversely affect us.

Adverse economic conditions in China and an increase in global iron ore production capacity could have a negative impact on us.

China has been the main driver of global demand for minerals and metals over the past years, effectively driving global prices for iron ore and steel. In 2019, China accounted for 71% of the global seaborne iron ore trade and 74% of our iron ore export sales were to the Asian market, mainly China. China is also the largest steel producer in the world, accounting for approximately 53% of the global steel production in 2019.

A contraction of China’s economic growth could result in lower global demand for iron ore and steel and increase the global steel industry’s over-capacity, which would materially and adversely affect companies in the industry, including us. Poor performance in the Chinese real estate sector and low investments in infrastructure, two of the largest markets for carbon steel in China, could also negatively affect us. China’s GDP increased 6.1% in 2019, as compared to 6.6% in 2018 and 6.8% in 2017.

In addition, the ramp-up of projects started in past years by major iron ore suppliers could affect seaborne iron ore prices and adversely affect us. Moreover, the recent upsurge in iron ore prices could also stimulate high cost producers to resume operations, expanding our supply base, which may adversely affect us.

We may not be able to adjust our mining production volume in a timely or cost-efficient manner in response to changes in demand.

Revenues from our mining business represented 23%, 25% and 39% of our total net revenues in 2017, 2018 and 2019, respectively. Operating at significant idle capacity during periods of weak demand may expose us to higher unit production costs since a significant portion of our cost structure is fixed in the short-term due to the high capital intensity of mining operations. In addition, efforts to reduce costs during periods of weak demand could be limited by labor regulations or labor or government agreements.

Conversely, our ability to rapidly increase production capacity is limited, which could render us unable to fully satisfy demand for our iron ore. When demand exceeds our production capacity, we may meet excess customer demand by purchasing iron ore from unrelated parties and reselling it, which would increase our costs and narrow our operating margins. If we are unable to satisfy excess customer demand in this way, we may lose customers. In addition, operating close to full capacity may expose us to higher costs, including demurrage fees due to capacity restraints in our logistics systems.

A decrease in the availability or an increase in the price of raw materials for steel production, particularly coal and coke, may adversely affect us.

In 2019, raw material costs accounted for 65% of our total steel production costs. Our main raw materials include iron ore, coal, coke, limestone, dolomite, manganese, zinc, tin and aluminum. We depend on third parties for some of our raw material requirements, including importing all of the coal required to produce coke. In addition, we require significant amounts of energy, in the form of natural gas and electricity, to power our plants and equipment.

40550.00004

13

Any prolonged interruption in the supply of raw materials, natural gas, or electricity, or substantial increases in their prices, could materially and adversely affect us. Interruptions and price increases could result from changes in laws or trade regulations, the availability and cost of transportation, suppliers’ allocations to other purchasers, interruptions in production by suppliers and/or accidents or similar events on suppliers’ premises or along the supply chain. In addition, public health epidemics such as the outbreak of COVID-19 could adversely affect global macroeconomic conditions and, consequently, the availability and price of raw materials for steel production.

Our inability to pass these cost increases onto our customers or to meet our customer demand because of unavailability of key raw materials could also have a material and adverse effect on us.

Our steel products face significant competition, including price competition, from other domestic or foreign producers, which may adversely affect our profitability and market share.

The global steel industry is highly competitive with respect to price, product quality, customer service and technological advances permitting reduced production costs. Several factors influence Brazil’s export of steel products, including protectionist policies of other countries, especially the United States, disputes regarding these policies before the World Trade Organization, the Brazilian government’s exchange rate policy and the growth rate of the world economy. Further, continuous advances in materials sciences and technology have given rise to improvements in products such as plastics, aluminum, ceramics and glass, permitting them to serve as substitutes for steel. Due to high start-up costs, the economics of operating a steelworks facility on a continuous basis may encourage mill operators to maintain high levels of output, even in times of low demand, which results in oversupply and increases the pressure on industry profit margins. In addition, downward pressure on steel prices by our competitors may affect our profitability.

The steel industry has historically suffered from structural over-capacity which has worsened due to a substantial increase in production capacity in the developing world, particularly China and India, as well as other emerging markets. China is the largest global steel producer and, in addition, Chinese and certain steel exporting countries have favorable conditions (excess steel capacity, undervalued currency or higher market prices for steel in non-domestic markets), which can have a significant impact on steel prices in other markets. If we are not able to remain competitive in relation to competitors in China or other steel-producing countries, we may be adversely affected.

Steel companies in Brazil face strong competition from imported products, mainly as a result of the global excess in steel production, reduction in demand for steel products in mature markets, exchange rate appreciation and tax incentives in some of the main exporting countries. Despite Brazilian import duties to protect domestic producers, a substantial volume of steel products is imported. If the Brazilian government does not implement measures against subsidized steel imports and there is an increase in imports, we may be materially and adversely affected. Apart from direct steel imports, the Brazilian industry also faces competition from imported finished goods, which adversely affects the whole steel supply and production chain.

Protectionist and other measures adopted by foreign governments could adversely affect our export sales.

In response to increased production and steel exports from many countries, anti-dumping and countervailing duty and safeguard measures were imposed in the late 1990s and early 2000s by foreign governments representing the main markets for our exports.

This scenario returned in 2015, when U.S. authorities initiated anti-dumping and countervailing duty investigations on hot-rolled and cold-rolled steel sheets and coils imported from Brazil and other countries. In 2016, the European Commission initiated an anti-dumping investigation of hot-rolled sheets and coils imported from Brazil and other countries.

In April 2017, the President of the United States, Donald Trump, requested an investigation under Section 232 of the Trade Expansion Act to determine if steel imports are harming national security. As a result of this investigation, in March 2018, U.S. government established the entry in force of Section 232, which imposes an ad valorem tariff of 25% on imported steel. In the same month, prompted by the United States’ adoption of Section 232 measures, the European Union initiated a safeguard investigation into imports of 26 categories of steel products. In February 2019, a definitive E.U. regulation imposed safeguard measures on imports of certain steel products and imposed quotas for the next three years. In the United States, Section 232 subjects us to a quota for exports of slabs, hot and cold-rolled steel sheets, pre-painted corrosion resistant, Al-Zn and tin mill products. In Europe, we are subject to a quota for exports of hot and cold-rolled steel sheets and tin mill products. Because we were already subject to an anti-dumping duty of $53.4 EUR/ton of hot-rolled sheets in Europe, these developments did not affect our hot-rolled sheets exports to Europe.

40550.00004

14

The imposition of these and other protectionist measures by foreign countries may materially and adversely affect our export sales.

Our activities depend on authorizations, concessions, licenses and permits and changes in applicable laws, regulations or government measures could adversely affect us.

Our activities and the activities of our subsidiaries and joint ventures are subject to governmental authorizations, concessions, licenses and permits, which include environmental licenses, as well as water grants, for our infrastructure projects and concessions, including for the port terminals we operate and the railways in which we have an equity interest. Although we believe that such authorizations, concessions, licenses and permits will be granted and/or renewed as and when requested, we cannot guarantee that we will be able to maintain, renew or obtain any required authorization, concession, license or permit, or that no additional requirement will be imposed on us in connection with our requests.

Authorizations, concessions, licenses or permits required for the development of our activities may require that we meet certain performance thresholds or completion milestones. In case we are unable to meet these thresholds or milestones, we may lose or not be able to obtain or renew such authorizations, concessions, licenses or permits, or we may not be able to do so under the terms of new concession laws, claims for amicable contractual termination and subsequent re-bidding for concessions. We also cannot guarantee that we, our controlled entities and our joint ventures that hold concessions will timely comply with our or their obligations under any relevant concession agreement or in conduct adjustment agreement (Termos de Ajustamento de Conduta), or TACs, entered into with governmental agencies. In addition, we are exposed to supervision, penalties and fiscalization from governmental entities, including the Brazilian court of audit (Tribunal de Contas da União), or TCU, and regulatory agencies. A material breach of those obligations may result in the loss or early termination of concessions, authorizations, permits and/or licenses, the restriction of access to public financing for the concession or the amortization of the public financing before a project begins to operate, the acceleration or an event of default under our indebtedness. Additionally, we would be subject to penalties, including fines or the closure of facilities. In case of a takeover or concession agreement termination due to government default, if we are entitled to any indemnification from granting authorities for our investments, this indemnification may be insufficient to cover our costs, expenses or losses and may be paid long after the events affecting our concessions, permits or licenses occur, if at all.

In addition, changes in applicable laws or regulations could require modifications to our technologies and operations and unexpected capital expenditures. Capital expenditures that we have already made may not generate the returns we expected, if any.

After accidents involving the breaking of upstream mining dams operated by other mining companies in the cities of Mariana and Brumadinho in the state of Minas Gerais, the Brazilian National Mining Agency (Agência Nacional de Mineração), or the ANM, and Brazilian environmental regulatory authorities are applying more stringent environmental licensing requirements for mining project operations, specifically for dams.

The amount and timing of these and other environmental and related expenditures may vary substantially from those currently anticipated and we may encounter delays in obtaining environmental or other operating licenses, or not be able to obtain and/or renew them, which could subject us to civil, administrative or criminal liability and closure orders. Any of the above events, among others, may adversely affect us and our ability to obtain expected returns from our projects, and may render certain projects economically or otherwise unfeasible.

Further new or more stringent environmental licensing requirements for our project operations, specifically for our dams, could be imposed on us. In addition, environmental agencies have intensified the frequency of inspections of tailings dams, including ours. For additional information on mining regulations in Brazil, see “Item 4.B.—Business Overview—Brazil—Mining Regulation.”

40550.00004

15

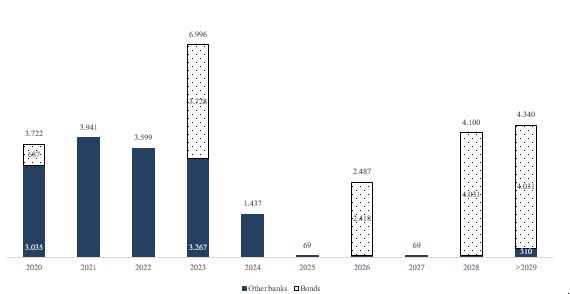

We have a high level of indebtedness that could make it more difficult or expensive to refinance our maturing debt and/or incur new debt.

As of December 31, 2019, our total debt outstanding was R$27,967 million, comprising R$5,126 million of short-term debt and R$22,841 million of long-term debt. We had R$1,089 million in cash and cash equivalents as of December 31, 2019. Our planned investments across our business segments will require a significant amount of cash over the course of 2020 and following years. See “Item 4D. Property, Plant and Equipment—Acquisitions and Dispositions.”

Our level of indebtedness could affect our credit rating and our ability to obtain any necessary financing in the future and may increase our cost of borrowing. In addition, our level of indebtedness could make it more difficult to refinance our existing indebtedness and could make us more vulnerable in the event of a downturn in our business. In these and other circumstances, servicing our indebtedness may use a substantial portion of our cash flow from operations, which could adversely affect us and make it more difficult for us to make payments of dividends and other distributions to our shareholders, including the holders of ADSs, as well as to fund our operations, working capital and capital expenditures necessary for the maintenance and expansion of our business activities.

Our ability to refinance our indebtedness maturing in 2020 and 2021 is subject to market conditions and creditor approvals. In the event conditions are not favorable or approvals are not obtained, we will be required to make significant payments in the next 24 months under our financings, which would adversely affect our financial and cash position and may result in downgrades in our credit ratings.

We cannot assure you that our credit ratings will not be lowered, suspended or withdrawn by the rating agencies.

Our credit ratings are limited in scope, and do not address all material risks relating to an investment in our common shares or ADSs, but rather reflect only the views of the rating agencies at the time the ratings are issued. These ratings may affect the cost and other terms upon which we are able to obtain funding and are subject to change due to factors specific to us, trends in the industries we operate or in the credit and capital markets generally. On December 31, 2019, our Fitch, Moody’s and S&P credit ratings were B, B2 and B, respectively. Credit rating agencies regularly evaluate us and their ratings are based on a number of factors, including our financial strength. We cannot assure that credit rating agencies will not downgrade our credit ratings or that credit ratings will remain in effect for any given period of time or not be withdrawn entirely by the rating agencies, if in their judgment circumstances so warrant.

Any lowering, suspension or withdrawal of our credit ratings may have an adverse effect on us and our ability to refinance our existing indebtedness.

Accidents or malfunctioning equipment on our premises, railways or ports may decrease or interrupt production, internal logistics or distribution of our products and adversely affect us.

The steel and iron ore production processes depend on certain critical equipment, such as blast furnaces, steel converters, continuous casting machines, rolling mills, drillers, reclaimers, conveyor belts, crushing and screening equipment and ship loaders, as well as on internal logistics and distribution channels, such as railways and seaports. This equipment and infrastructure may be affected in the case of malfunction or damage. Any significant interruptions in our production process, internal logistics or distribution channels (including our ports and railways) could materially and adversely affect us.

In addition, our operations involve the use, handling, storage, discharge and disposal of hazardous substances into the environment. Our mining, steel and cement businesses are generally subject to significant risks and hazards, including fire, explosions, toxic gas leaks, spilling of polluting substances or other hazardous materials, rockfall incidents in mining operations and incidents involving mobile equipment or machinery and accidents involving our tailings dams. Such events could occur by accident or by breach of operating and maintenance standards, and could result in a significant environmental impact, damage to or destruction of our mineral properties and/or production facilities, personal injury or death, delays or suspensions in production, monetary losses and exposure to civil responsibilities, administrative penalties, criminal sanctions and closure orders for non-compliance with these regulations. Failure to comply with our health, safety and environmental standards and risk management programs and procedures may be insufficient to prevent incidents or accidents that could adversely affect us.

40550.00004

16

Failures in or interruptions to our telecommunications, information technology systems or automated machinery could adversely affect us.

Our operations are heavily reliant on telecommunications, information technology systems and automated machinery. Disruptions to these systems, caused by obsolescence, technical failures or intentional acts, may adversely affect us. In addition, any failure in our systems related to confidential information, caused by external cyber‑attacks or internal actions, including negligence or misconduct of our employees, could have a negative impact on our reputation and our interactions with competitors and other third parties, including governmental and regulatory bodies, suppliers and others.

Our information technology systems are protected by security layers, including security solutions and monitoring processes; however, they may be vulnerable to external factors such as natural disasters, viruses, cyber‑attacks and other security breaches. Any damage or interruption to our information technology systems may adversely affect our results of our business and expose us to fines and litigation.

In 2018, Law No. 13,709/2018, or the Brazilian General Data Protection Law, was enacted to take effect in August 2020 and to change the personal data protection system in Brazil. This law sets forth a new legal framework for the treatment of personal data, including the rights of personal data holders, the legal basis applicable to personal data protection, the requirements to obtain consent, the obligations and requirements related to security incidents, personal data leaks and transfers and the creation of the Brazilian Data Protection Authority, among others. If we fail to adapt our processes to comply with this law, we may be subject to penalties, including mandatory disclosure of our non-compliance, temporary blocking and/or deletion of personal data and fines of up to 2% of our revenue in the last fiscal year, excluding taxes, up to an aggregate amount of R$50.0 million per infraction.

Our insurance policies may not be sufficient to cover all our losses.

We maintain several types of insurance policies as part of our risk management for each of our businesses and seek to follow industry practice regarding best coverage, which encompasses domestic and international (import and export) cargo transportation (road, rail, sea or air), life insurance, personal accidents, health, automobile, directors and officers, general liability, CAR (construction and erection risks), trade credit insurance, surety, named perils, ports and terminal liabilities.

We also have an insurance policy covering the operational risks, material damages and loss of profits of the following operations and subsidiaries: Presidente Vargas Steelworks, CSN Mineração S.A., or CSN Mineração, and the container terminal Sepetiba Tecon S.A., or TECON. This policy was renewed with domestic and foreign insurers and reinsurers and is valid until June 30, 2020, with a limited indemnity of US$600 million (for an insured value of US$10.2 billion) and a deductible of US$385 million for material damages and 45 days to loss of profits.

The coverage obtained in our insurance policies may not be sufficient to cover all risks or the extent of the risks we are exposed to, which could expose us to significant costs. Additionally, we may not be able to successfully contract or renew our insurance policies or to do so on terms satisfactory to us. The occurrence of one or more of these events may adversely affect us.

Our projects are subject to risks that, if materialized, may result in increased costs and/or delays or that could prevent their timely or successful implementation.

We are investing to further increase our steel, mining and cement production capacity, as well as our logistics capabilities. The success of these projects is subject to a number of risks that, if materialized, may adversely affect our growth prospects and profitability, including, among others:

· delays, availability issues or higher than expected costs in obtaining the necessary equipment, services and materials to build and operate a project;

· lack of infrastructure, including waste disposal areas and reliable power and water supply;

· environmental remediation costs;

· delays or higher than expected costs in obtaining or renewing required authorizations, concessions, licenses or permits and/or regulatory approvals to build or continue a project; and

40550.00004

17

· changes in market conditions, laws or regulations that render a project less profitable than expected or economically or otherwise unfeasible.

Any one or a combination of the factors described above may materially and adversely affect us.

We are subject to environmental, health and safety incidents. Additionally, current, new or more stringent environmental, health and safety regulations applicable to us may result in liability exposure and increased capital expenditures.

Our steel production, mining, cement, energy and logistics facilities are subject to a broad range of laws, regulations and permit requirements in the countries where we operate relating to the protection of the environment, health and safety.

Brazilian pollution standards are subject to change, including new effluent and air emission standards, water management and solid waste-handling regulations, wildlife maintenance regulations, restrictions on business expansions, native forest preservation requirements and the obligation to support the creation of an integral protection conservation unit, as privately owned conservation areas (Reserva Particular do Patrimônio Natural), or national parks, or areas of relevant ecological interest (ARIE), including the Cicuta Forest, as environmental compensation for industrial and mining expansion projects. The Brazilian government has adopted a decree under the national policy for climate change (Política Nacional de Mudanças Climáticas) that contemplates a reduction in carbon emissions for the industry (including steel making and cement sectors) and an action plan is being developed by a technical committee composed of representatives from the government, industry associations and academia. The target reduction for the mining sector is yet to be established.

In addition, the state of Rio de Janeiro, through the State Environment Institute (Instituto Estadual do Ambiente), or INEA, issued a law that requires steel making and cement facilities to present action plans to reduce greenhouse gas emissions when renewing or applying for operational licenses. At the federal level, the environmental national council, (Conselho Nacional do Meio Ambiente), or CONAMA, issued Resolution No. 436/2011 to address air emissions that obliged steel companies to comply with certain emission standards as of December 2018, including adjustments in the filters of plant chimneys. In September 2018, we entered into a TAC with the state of Rio de Janeiro relating to this resolution. Any failure to comply with these or other laws, resolutions and standards may expose us to civil, criminal and administrative liability. The Brazilian government has also established a national policy for solid waste (Política Nacional de Resíduos Sólidos), which provides for strict guidelines for solid waste management and industry targets for reverse logistics as part of the environmental licensing process. Finally, a new regulatory framework for mining operations was issued in June 2018, which may impose stricter regulations on our mining operations, including requests for environmental recovery of areas and investments for the granting of mining concessions.

Our operations involve the use, handling, storage, discharge and disposal of hazardous substances into the environment and the use of natural resources, and are subject to significant risks and hazards, including fire, explosion, toxic gas leaks, spilling of polluting substances or other hazardous materials, rockfalls, incidents involving dams, failure of operational structures and incidents involving mobile equipment, vehicles or machinery. This could occur by accident or by breach of operating and maintenance standards, and could result in significant environmental and social impacts, damage to or destruction of mineral properties or production facilities, personal injury, illness or death of employees, contractors or community members close to operations, environmental damage, delays in production, monetary losses and possible legal liability. Additionally, in remote localities, our employees may be exposed to tropical and contagious diseases that may affect their health and safety. Notwithstanding our standards, policies and controls, our operations remain subject to incidents or accidents that could adversely affect us and our stakeholders.

New or more stringent environmental, safety and health standards imposed on us could require increased capital expenditures, additional legal preservation areas within our properties or modifications to our operating practices or projects. For further information on environmental regulations and claims, see “Item 4.B.—Business Overview—Governmental Regulation and Other Legal Matters.”

In addition, in July 2018, the Federal Prosecutor’s Office and the State Public Prosecutor of Rio de Janeiro filed a public civil action against us, HARSCO and INEA, for immediate removal of slag piles in the city of Volta Redonda, in the state of Rio de Janeiro, that adjoin the Paraíba do Sul River. The amount and timing of these and other environmental and related expenditures may vary substantially from those currently anticipated. These additional costs may also have a negative impact on the profitability of the projects we intend to implement or may make such projects economically unfeasible. We could also be exposed to civil, administrative or criminal liability and closure orders for non-compliance with these regulations, as well as encounter delays in obtaining environmental or other operating licenses. Waste disposal, including our slag piles, and emission practices may result in the need for us to clean up or retrofit our facilities or our disposal locations at substantial costs and/or could result in substantial civil, criminal and administrative liability, including, among others, pursuant to public civil actions. Environmental legislation in foreign markets to which we export our products may also materially and adversely affect our export sales and us.

40550.00004

18

In addition, we may enter into TACs with Brazilian regulatory agencies that require us to minimize or eliminate the risk of environmental impacts in the areas where we operate. If we are unable to comply with a TAC or to remediate non-compliance in a timely manner, we may be exposed to penalties, such as fines, revocation of permits or closure of facilities.

Our governance and compliance procedures may fail to prevent regulatory penalties and reputational harm.

We operate in a global environment and our activities straddle multiple jurisdictions and complex regulatory frameworks subject to enforcement worldwide. Our governance and compliance procedures may not prevent breaches of law, accounting and/or governance standards applicable to us, and we may be unable to identify wrongdoing or improper activities by members of our management, employees or third parties. We may be subject to breaches of our Code of Ethics, business conduct protocols and to instances of fraudulent behavior, dishonesty and unlawful conduct by members of our management, employees, contractors or other agents, which could subject us to fines, loss of our operating licenses and reputational harm, as well as other penalties, which may materially and adversely affect us.

We may fail to maintain an effective system of internal controls, which could prevent us from timely and accurately reporting our financial results.

Our internal controls over financial reporting may not prevent or detect misstatements in a timely manner due to inherent limitations, including human error, circumvention or overriding of controls, or fraud. Even effective internal controls can provide only reasonable assurance with respect to the preparation and fair presentation of financial statements. If we fail to maintain the adequacy of our internal controls, including implementing new or improved required controls, we could fail to meet our financial reporting obligations, which could trigger a default under some of our agreements. In this regard, and in connection with management’s evaluation of the effectiveness of our internal control over financial reporting, we concluded that, as of December 31, 2019, our internal control over financial reporting is effective.

Some of our operations depend on joint ventures, jointly controlled entities, consortia and other forms of cooperation, and our business could be adversely affected if our partners fail to observe their commitments.

We currently operate parts of our business through joint ventures, strategic alliances and consortia with other companies. We have, among others: (i) established a strategic alliance with an Asian consortium at our controlled investee CSN Mineração to mine iron ore; (ii) a joint venture with other Brazilian steel and mining companies at MRS Logística S.A., or MRS, to explore railway transportation in the Southeastern region of Brazil; (iii) a joint venture with certain Brazilian governmental entities at Transnordestina Logística S.A., or TLSA, to explore railway transportation in the Northeastern region of Brazil; (iv) a joint venture with Engie Brasil Energia S.A. and Companhia de Cimento Itambé, or Itambé, at Itá Energética S.A., or ITASA, to produce electricity; and (v) a consortium with L.D.R.S.P.E Geração de Energia e Participações, Aliança Geração de Energia S.A. (union of Vale S.A., or Vale, and CEMIG Geração e Transmissão S.A.), or Aliança, and AngloGold Ashanti Córrego do Sítio Mineração S.A., or AngloGold, at Igarapava hydroelectric facility to produce electricity.

Our forecasts and plans for these strategic alliances, joint ventures and consortia assume that our partners will observe their obligations to make capital contributions, purchase products and, in some cases, provide managerial personnel or financing. In addition, many of the projects contemplated by our joint ventures or consortia rely on financing commitments, which contain certain preconditions for each disbursement. If any of our partners fails to observe their commitments or we fail to comply with all preconditions required under our financing commitments or other partnership arrangements, the affected joint venture, consortium or other project may not be able to operate in accordance with its business plans, or we may have to increase the level of our investment to implement these plans, which could adversely affect us.

40550.00004

19

Risks associated with drilling and production could render mining projects economically unfeasible.

Once mineral deposits are discovered, it can take a number of years from the initial phases of drilling until production is possible, during which time the economic feasibility of production may change. Substantial time and expenditures are required to:

· establish mineral reserves through drilling;

· determine appropriate mining and metallurgical processes for optimizing the recovery of metal contained in ore;

· obtain environmental and other licenses;

· construct mining, processing facilities and infrastructure required for greenfield properties; and

· obtain the ore or extract the minerals from the ore.

If a mining project proves not to be economically feasible by the time we are able to profit from it, we may incur substantial losses and be obliged to record write-offs. In addition, potential changes or complications involving metallurgical and other technological processes arising during the life of a project may result in delays and cost overruns that may render the project not economically feasible.

Our mineral reserve and mine life may prove inaccurate, market price fluctuations and cost changes may render certain ore reserves uneconomical to mine and we may face rising extraction costs or investment requirements over time as our reserves deplete.

Our reported ore reserves are estimated quantities of ore and minerals that we have determined can be economically mined and processed under present and anticipated conditions to extract their mineral content. There are numerous uncertainties inherent in estimating quantities of reserves and in projecting potential future rates of mineral production, including many factors beyond our control. Reserve engineering involves estimating deposits of minerals that cannot be measured in an exact manner, and the accuracy of any reserve estimate is a function of the quality of available data and engineering and geological interpretation and judgment. As a result, no assurance can be given that the indicated amount of ore will be recovered or that it will be recovered at the rates we anticipate. Estimates of different engineers may vary, and results of our mining production subsequent to the date of an estimate may lead to revision of estimates. Reserve estimates and estimates of mine life may require revision based on actual production experience and other factors. For example, fluctuations in the market prices of minerals and metals, reduced recovery rates or increased operating and capital costs due to inflation, exchange rates or other factors may render proven and probable reserves uneconomic to exploit and may ultimately result in a restatement of reserves.

In addition, reserves are gradually depleted in the ordinary course of our exploration activities. As mining progresses, distances to the primary crusher and to waste deposits becomes longer and pits become steeper. Also, for some types of reserves, mineralization grade decreases and hardness increases at increased depths. As a result, over time we may experience rising unit extraction costs with respect to each mine, or we may need to make additional investments, including adaptation or construction of processing plants and expansion or construction of tailings dams. Our exploration programs may also fail to result in the expansion or replacement of reserves depleted by current production. If we do not enhance existing reserves or develop new operations, we may not be able to sustain our current level of production beyond the remaining lives of our existing mines. See “Item 4B—Business Overview—Our Mining Segment—Mineral Reserves.”

Natural and other disasters, or extreme weather conditions, could disrupt our operations.

Because of our exposure to raw materials costs, extreme weather conditions, such as heavy rainfall or flooding, could reduce the available supply of our raw materials and increase our raw materials costs, which would have a material adverse impact on us. Additionally, we are subject to technical or physical risks including fire, power loss, water supply loss, reduction or rationing, leakages, accidents and failures in telecommunications and information technology systems, any of which could disrupt our operations.

We may not be able to consummate proposed acquisitions or integrate acquired businesses successfully.

From time to time, we may evaluate acquisition opportunities that would strategically fit our business objectives. If we are unable to complete acquisitions, or integrate acquisitions successfully and develop these businesses to realize revenue growth and cost savings, we could be adversely affected. Acquisitions also pose the risk that we may be exposed to successor liability involving an acquired company. Due diligence conducted in connection with an acquisition, and any contractual guarantees or indemnities that we receive, may not be sufficient to protect us from, or compensate us for, actual liabilities. A material liability associated with an acquisition, such as labor or environmental liabilities, could adversely affect us and reduce the expected and bargained-for benefits of the acquisition.

40550.00004

20

In addition, we may incur asset impairment charges related to acquisitions, which may reduce our profitability. Our acquisition activities may also present financial, managerial and operational risks, including diversion of management attention from existing core businesses, difficulties integrating or separating personnel, financial and other systems, failure to achieve the operational benefits that were anticipated at the time of the transaction, adverse effects on existing business relationships with suppliers and customers, inaccurate estimates of fair value made in the accounting for acquisitions and/or amortization of acquired intangible assets which would reduce future reported earnings, potential loss of customers or key employees of acquired businesses and indemnities and potential disputes with buyers or sellers. Finally, proposed acquisitions may also be subject to review from the competition authorities of the countries involved in the transaction, which may approve the transaction, do so subject to restrictions, including the divestment of assets, or reject it. Any of these developments or adverse regulatory decisions could negatively affect us.

We may not be able to maintain adequate liquidity and our cash flows from operations and available capital may not be sufficient to meet our obligations.

While our cash flows from operations and available capital have been sufficient to meet our current operating expenses, contractual obligations and debt service requirements to date, our liquidity, cash flows from operations and available capital may be negatively impacted by the pricing environment for our steel and iron ore products, the exchange rate environment and the effects of weak economic conditions in Brazil. These factors have materially and adversely affected our liquidity and we expect this to continue. Recent cost cutting measures implemented by us may not be sufficient to offset these effects or to improve our liquidity position.

We have announced certain measures to improve our liquidity and debt profile, including the potential sale of certain assets. In addition, we are negotiating the extension of certain of our credit facilities. If we are unable to successfully sell certain assets and/or extend our debt amortization profile, we may not be able to maintain adequate liquidity and our cash flows from operations and available capital may not be sufficient to meet our obligations.