Table of Contents

Exhibit 99.1

Management Proxy Circular

Notice of Annual Meeting of Shareholders

April 8, 2021

Your participation is important. Please read this document and vote.

Table of Contents

Notice of Annual Meeting of Shareholders

| When: | Thursday, April 8, 2021, 10:30 a.m. Eastern Daylight Time (EDT) | |

| Virtual Meeting: |

We are holding our 2021 annual meeting virtually to continue protecting the health and safety of our shareholders, employees and other stakeholders from the ongoing impact of the COVID-19 pandemic. Please join our webcast at https://cibc.pividal.tv/agm2021 or on our phone line at 1 800 898-3989, passcode 6875673# (English) or 1 877 395-0279 passcode 9080240# (French). | |

At the meeting you will be asked to:

| 1. | receive our financial statements for the year ended October 31, 2020 and the auditors’ report on the statements; |

| 2. | elect directors; |

| 3. | appoint auditors; |

| 4. | vote on an advisory resolution on our executive compensation approach; |

| 5. | vote on shareholder proposals; and |

| 6. | consider any other business properly brought before the meeting. |

Voting instructions start on page 2 of our 2021 Management Proxy Circular (the “Circular”). Please read our Circular carefully.

Delivery of meeting materials by notice-and-access

Protecting the environment – We are proud to let you know that we have furthered our commitment to protect the environment by reducing the amount of paper we send to our shareholders. You have told us how important environmental sustainability is to you as shareholders and we are listening.

Our Management Proxy Circular – Starting this year, we are using notice-and-access to send our registered and non-registered shareholders the 2021 management proxy circular as permitted by the Canadian Securities Administrators and with the authorization of the Office of the Superintendent of Financial Institutions Canada. This means that our Circular will be posted online for you to access, rather than being printed and mailed to you. You will still receive a proxy form or a voting instruction form by mail so that you can vote your shares. You will also receive a notice with information about how you can access our Circular online and how to request a paper copy.

Our Annual Financial Statements and Management’s Discussion and Analysis – The way we send you our annual financial statements and management’s discussion and analysis (MD&A) depends on whether you are a registered shareholder or a non-registered shareholder.

You are a registered shareholder if you hold a paper share certificate in your name or your shares are held through the direct registration system. You are a non-registered shareholder if your shares are registered in the name of an intermediary, such as a bank, broker or trust company.

If you are a registered shareholder and you did not sign-up for e-delivery or opt out of receiving our annual financial statements, then we are required to send you our annual financial statements and you will receive a paper copy of our Annual Report with the notice.

If you are a non-registered shareholder, then we will use notice-and-access to send you our annual financial statements and MD&A as permitted by securities law so that you can access this material online the same way as our Circular.

Our Circular and Annual Report (the “meeting materials”) are available on the website of our transfer agent AST Trust Company (Canada) (AST) (www.meetingdocuments.com/astca/cibc), on our website (www.cibc.com), SEDAR (www.sedar.com) and EDGAR (www.sec.gov/edgar.shtml).

Table of Contents

How to request a paper copy of the meeting materials

You may request a paper copy of the Circular or the Annual Report, free of charge, up to one year from the date the meeting materials were filed on SEDAR.

To make your request before the meeting, contact AST at www.meetingdocuments.com/astca/cibc or 1 888 433-6443 (toll free in Canada and the United States) or 416 682-3801 (other countries) or email fulfilment@astfinancial.com. Please follow AST’s instructions. A paper copy of the requested documents will be sent to you within three business days of your request. Please note that you will not receive another proxy form or voting instruction form so please retain your original form to vote your shares.

To ensure receipt of the paper copy before the voting deadline and meeting date, we estimate that your request must be received no later than 5:00 p.m. (EDT) on March 25, 2021. This reflects the three business day period for processing requests as well as typical mailing times.

To make your request on or after the date of the meeting, call AST at 1 888 433-6443 (toll free in Canada and the United States) or 416 682-3801 (other countries) or email fulfilment@astfinancial.com. The requested documents will be sent to you within ten calendar days of your request.

Eligibility to vote

There were 447,964,315 common shares outstanding on February 8, 2021, our record date. Holders of common shares on that date are eligible to vote at our meeting (subject to Bank Act (Canada) restrictions).

Your vote is important

We encourage you to read the Circular and vote before the meeting. For more information on how you can vote or appoint someone else to vote for you see “Voting” starting on page 2 of the Circular. Please vote as early as possible so that your shares are represented at the meeting. AST must receive your vote no later than 10:30 a.m. (EDT) on April 7, 2021.

You may also vote online at the virtual meeting, provided you follow certain steps. These steps are set out on pages 3 and 4 of the Circular.

Questions

If you have questions about notice-and-access or our virtual meeting, you may contact AST at 1 800 258-0499 (toll free in Canada and the United States) or 416 682-3860 (other countries).

Our Board and management would like to answer as many shareholder questions as possible during the meeting. We encourage you to submit questions in advance to the Corporate Secretary at corporate.secretary@cibc.com or mailed to CIBC Corporate Secretary’s Division, 199 Bay Street, Commerce Court West, Suite 4460, Toronto, Ontario M5L 1A2.

By Order of the Board

Michelle Caturay

Senior Vice-President, Associate General

Counsel and Corporate Secretary

February 16, 2021

Table of Contents

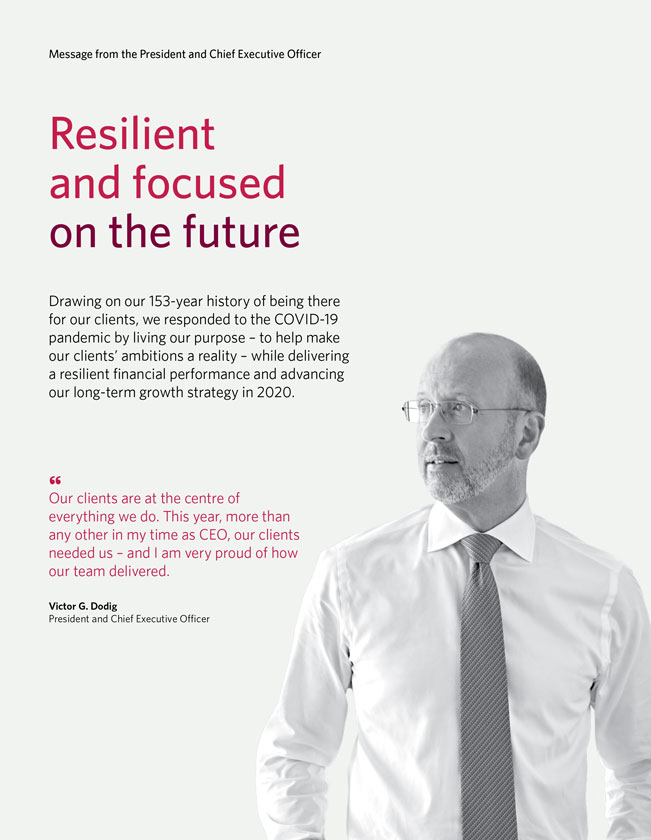

Dear fellow shareholder,

We are pleased to invite you to attend CIBC’s Annual Meeting of Shareholders on Thursday, April 8, 2021, at 10:30 a.m. (EDT).

Engaging with you – The health and well-being of our team, clients, investors and communities remains our top priority. In line with the latest directives from public health and government authorities, this year’s meeting will be virtual. Shareholders will have the opportunity to attend the meeting online in real time regardless of their location, submit questions and vote. Please see our Circular for information on how to participate in our virtual meeting, the business to be conducted at the meeting, our executive compensation approach and our governance practices. You have the opportunity to vote and your vote matters!

Our purpose – This past year, amidst a global pandemic, we lived our purpose to help make your ambition a reality. This shared purpose is the foundation for the efforts of our team to work collaboratively to meet the needs of our clients. The investments we have made in building a client-focused culture were realized this year, as our team responded with urgency and focus to address immediate client needs created by the onset of the pandemic, and support our clients in keeping their long-term ambitions on track. Our bank played a critical role in supporting clients, including providing payment relief to those affected by the pandemic, and working closely with governments to administer critical relief programs. We continue to be there for clients affected by the pandemic with advice and solutions to address financial hardship.

Creating value – We delivered resilient business performance in 2020. Pre-provision earnings were up over 2019 and our capital position remained strong. Our investments in technology over the past several years to digitize and simplify our bank are allowing us to provide real-time remote support to our clients at a time when physical distancing has become the norm. These efforts are being recognized by our clients with our highest client experience scores on record.

We remain focused on meeting our responsibilities to support the long-term strength and prosperity of the people and communities we serve. This is true at the corporate level with our commitment to sustainability and our support for social and economic development, as well as at the individual level, where our generous team members give back, day in and day out.

Join us – At our meeting, you will hear more about CIBC’s 2020 performance and progress on our strategy. Board members and executive officers will be available to answer your questions.

We thank you for your continued support of CIBC and look forward to your participation in our virtual meeting at https://cibc.pividal.tv/agm2021 or by phone at 1 800 898-3989, passcode 6875673# (English) or 1 877 395-0279 passcode 9080240# (French). The meeting will be archived on our website until the next annual meeting.

Sincerely,

|

| |

| John P. Manley | Victor G. Dodig | |

| Chair of the Board | President and Chief Executive Officer | |

Table of Contents

Management Proxy Circular

In this 2021 Management Proxy Circular (the “Circular”) information is as at February 11, 2021. All dollar figures are in Canadian currency, unless indicated otherwise. ‘You’, ‘your’ and ‘shareholder’ mean common shareholders of CIBC.

Glossary of Acronyms

The CIBC Logo is a trademark of CIBC in Canada and other countries.

Table of Contents

1. Financial Statements

The consolidated financial statements for the year ended October 31, 2020 are in our 2020 Annual Report available at https://www.cibc.com/en/about-cibc/investor-relations.html.

| 2. Election of Directors

You will be asked to elect 14 director nominees to serve on our Board until the earlier of the next annual meeting or the director’s retirement from the Board. The Board recommends that you vote for each director nominee. |

See pages 14 to 28 for information about our director nominees.

|

| 3. Appointment of Auditors

You will be asked to appoint Ernst & Young LLP (EY) as auditors of CIBC. EY has served as the auditors of CIBC since December 2002. The Board recommends that you vote for EY as our auditors. |

See page 37 for information on the Audit Committee’s annual assessment of EY’s effectiveness and audit quality and a description of fees paid to the auditors.

|

| 4. Advisory Resolution on our Executive Compensation Approach

You can have a “say on pay” by voting on an advisory resolution about our approach to executive compensation. Last year, 95% of shareholder votes were for our executive compensation approach. We consider the vote part of our shareholder engagement process. This vote is advisory under applicable law and does not diminish the Board’s role and responsibilities. Even though the resolution is not binding, the Board and Management Resources and Compensation Committee consider the results of the vote in making future executive compensation decisions. |

See pages 61 to 84 for Message to our Fellow Shareholders and Compensation Discussion and Analysis.

|

When reviewing its approach to executive compensation, the Committee considers shareholder feedback and any concerns that have been raised. If a concern is significant, we will disclose the Committee’s review process and the outcome of that review in our next management proxy circular. The Board recommends that you vote for the following advisory resolution on our approach to executive compensation.

RESOLVED that the shareholders accept the approach to executive compensation disclosed in CIBC’s management proxy circular for the 2021 Annual Meeting of Shareholders.

| 5. Shareholder Proposals You will be asked to vote on a shareholder proposal from the Mouvement d’education et de défense des actionnaires (MÉDAC) set out on page 6. The Board recommends that you vote against this proposal for the reasons explained in the Board’s response on page 6. In addition, MÉDAC withdrew seven shareholder proposals set out on pages 7 to 13. |

See pages 6 to 13 for shareholder proposals and management’s responses.

|

Æquo Shareholder Engagement Services, on behalf of Comité syndical national de retraite Bâtirente inc., withdrew a shareholder proposal described on page 7.

Shareholder proposals for next year’s annual meeting must be submitted by November 18, 2021.

Each item being voted on requires the approval of a majority (more than 50%) of the votes cast by proxy or during the meeting by online ballot through the live webcast. For information on voting and appointing a proxyholder see pages 2 to 5.

| C I B C P R O X Y C I R C U L A R | 1 |

Table of Contents

Who can vote

You are entitled to one vote for each common share you own on February 8, 2021, our record date. There were 447,964,315 outstanding common shares eligible to vote on that date.

Shares cannot be voted if they are beneficially owned by:

| • | the government of Canada or any of its agencies; |

| • | the government of a province or any of its agencies; |

| • | the government of a foreign country, any political subdivision of a foreign country or any of its agencies; |

| • | a person who has acquired more than 10% of any class of our shares without Minister of Finance approval; or |

| • | a person or entity controlled by a person that, in aggregate, are more than 20% of the eligible votes that may be cast unless permitted by the Minister of Finance. |

Our directors and officers are not aware of any person or company that beneficially owns, directly or indirectly, or exercises control or direction over, more than 10% of the votes attached to any class of CIBC shares.

How to vote

There are two ways to vote your shares: before the meeting by proxy or during the meeting by online ballot through the live webcast. The voting process you follow depends on whether you are a registered shareholder or a non-registered shareholder.

|

Registered shareholders

|

Non-registered shareholders

| |||

|

You are a registered shareholder if you hold a paper share certificate in your name or your shares are held through the direct registration system.

|

You are a non-registered shareholder if your shares are registered in the name of an intermediary, such as a bank, broker or trust company.

|

|

How to vote if you are a registered shareholder

|

If you are a registered shareholder you received a proxy form with a control number. If you did not receive this form, please contact AST at 1 800 258-0499 (toll free in Canada and the United States) or 416 682-3860 (other countries).You may vote by proxy before the meeting using the proxy form that was sent to you or you may vote during the meeting by online ballot through the live webcast.

If you want to vote by proxy before the meeting – To vote your shares by proxy, you may provide your voting instructions in one of these ways:

|

Online – go to www.astvotemyproxy.com, enter the 13-digit control number on your proxy form and follow the instructions on the screen; or

– scan both sides of your proxy form and email it to proxyvote@astfinancial.com; | |

|

Fax – complete your proxy form and fax both sides to AST at 1 866 781-3111 (Canada and the United States) or 1 416 368-2502 (outside North America); or | |

|

Mail – complete your proxy form and return it in the envelope provided. | |

Return your completed proxy by 10:30 a.m. (EDT) on April 7, 2021 to ensure your vote is counted. We encourage you to vote your shares early.

| 2 | C I B C P R O X Y C I R C U L A R |

Table of Contents

Voting

If you want to vote during the meeting – To attend our virtual meeting and vote your shares during the meeting, do not complete or return your proxy form. You will be able to vote online in real time by completing an online ballot through the live webcast as long as you are connected to the internet and follow these steps.

|

Step 1

|

Log in at https://cibc.pividal.tv/agm2021 at least 15 minutes before the meeting starts and check browser compatibility. There must be internet connectivity for the duration of the meeting to vote.

| |

|

Step 2

|

Select “Vote” and a separate browser will open. Enter the control number from your proxy form as your user name. Enter “cibc2021” (case sensitive) as your password. Any vote you cast at the meeting will revoke any proxy you previously submitted. If you do not wish to revoke a previously submitted proxy, you should not vote during the meeting.

|

If you want to appoint a proxyholder to vote during the meeting for you – You may appoint a proxyholder, other than management’s nominees, John Manley, Chair of the Board, and Victor Dodig, President and Chief Executive Officer, to attend, vote and act on your behalf at the meeting and any continuation or adjournment of the meeting. You should be sure your proxyholder is attending the meeting and is aware they have been appointed to vote your shares. To appoint a proxyholder you must follow these steps:

|

Step 1 |

Insert your proxyholder’s name in the space provided on your proxy form and return it online, by fax or mail as described on the previous page. The person you appoint as your proxyholder does not need to be a CIBC shareholder. You may leave the voting section blank, or you may provide voting instructions that your proxyholder must follow. | |

|

Step 2 |

You must register your proxyholder by calling AST at 1 866 751-6315 (within North America) or 1 212 235-5754 (outside North America) by 10:30 a.m. on April 7, 2021. AST will provide your proxyholder with a control number to vote during the meeting. If you do not take the additional step of registering your proxyholder with AST, your proxyholder will not receive a control number to vote your shares during the meeting. | |

|

Step 3 |

Your proxyholder should log in at https://cibc.pividal.tv/agm2021 at least 15 minutes before the meeting starts and check browser compatibility. There must be internet connectivity for the duration of the meeting to vote. | |

|

Step 4 |

Your proxyholder should select “Vote” and a separate browser will open. Your proxyholder will enter a user name and password. The user name is the control number emailed to your proxyholder after you registered your proxyholder with AST. The password is “cibc2021” and is case sensitive. | |

If you want to change your vote before the meeting – If you change your mind on the voting instructions you sent, you may revoke your proxy in one of these ways:

| • | If you returned your proxy form by fax or mail, you should sign a written statement that you revoke your proxy, provide your new instructions (or authorize your lawyer in writing to sign the statement) and send it to CIBC Corporate Secretary’s Division, 199 Bay Street, Commerce Court West, Suite 4460, Toronto, Ontario M5L 1A2, before 10:30 a.m. (EDT) on April 7, 2021. |

| • | If you voted online, you may vote online again before 10:30 a.m. (EDT) on April 7, 2021, using the control number on your proxy form. |

|

How to vote if you are a non-registered shareholder

|

If you are a non-registered shareholder, you received a voting instruction form with a control number. If you did not receive this form, please contact the intermediary where your shares are registered. You may vote by proxy before the meeting using the voting instruction form that was sent to you or you may vote during the meeting by online ballot through the live webcast provided you follow the steps below to register yourself as a proxyholder.

If you want to vote by proxy before the meeting – To vote your shares by proxy, you may provide your voting instructions in one of these ways:

|

|

Online – go to www.proxyvote.com, enter the 16-digit control number on your voting instruction form and follow the instructions on the screen; |

| C I B C P R O X Y C I R C U L A R | 3 |

Table of Contents

Voting

|

|

Mail – complete your voting instruction form and return it in the envelope provided; or | |

|

Phone – call 1 800 474-7493 (English) or 1 800 474-7501 (French) and follow the prompts. | |

You must allow sufficient time for your intermediary to receive and act on your voting instructions by 10:30 a.m. (EDT) on April 7, 2021. Please check your voting instruction form for information on the deadline for returning your form.

If you want to vote during the meeting or appoint a proxyholder to vote for you – To attend and vote at our virtual meeting, or appoint a proxyholder to attend and vote for you, you or your proxyholder will be able to vote online in real time by completing an online ballot through the live webcast as long as you, or your proxyholder, are connected to the internet and follow these steps:

|

Step 1 |

If you want to attend and vote during the meeting you must insert your name in the space provided on your voting instruction form and return it online or by mail, as described above. Do not complete the voting section if you plan to vote at the meeting.

If you want to appoint someone other than yourself, or management’s nominees, John Manley and Victor Dodig, as your proxyholder, to attend, vote and act for you at the meeting and any continuation or adjournment of the meeting, you must insert their name in the space provided on your voting instruction form and return it online or by mail, as described above. You may leave the voting section blank, or you may provide voting instructions that your proxyholder must follow. You should be sure your proxyholder is attending the meeting and is aware they have been appointed to vote your shares. The person you appoint as your proxyholder does not need to be a CIBC shareholder. | |

|

Step 2 |

You must register yourself, or your proxyholder by calling AST at 1 866 751-6315 (within North America) or 1 212 235-5754 (outside North America) by 10:30 a.m. on April 7, 2021. AST will provide you, or your proxyholder, with a control number to vote during the meeting. If you do not take the additional step of registering with AST, you, or your proxyholder, will not receive a control number to vote your shares during the meeting.

If you are a non-registered shareholder in the United States and want to vote at the meeting, you must obtain a legal proxy form from your intermediary by following the steps on the voting instruction form sent to you, or if you have not received one, contact your intermediary to request a legal proxy form. After obtaining the legal proxy form, appoint yourself, or someone else, as proxyholder. For instructions on how to appoint yourself, or someone else, as proxyholder, see Step 1 above then register yourself or your proxyholder with AST.

Legal proxies may be returned to AST by email at proxyvote@astfinancial.com or by mail: AST Trust Company (Canada), Attn: Proxy Department, P.O. Box 721, Agincourt, Ontario M1S 0A1 and must be labeled “Legal Proxy”.

Please allow sufficient time for the return of your legal proxy by the cut-off date of 10:30 a.m. (EDT) on April 7, 2021. | |

|

Step 3 |

You or your proxyholder should log in at https://cibc.pividal.tv/agm2021 at least 15 minutes before the meeting starts and check browser compatibility. There must be internet connectivity for the duration of the meeting to vote. | |

|

Step 4 |

You or your proxyholder should select “Vote” and a separate browser will open. You or your proxyholder will enter a user name and password. The user name is the control number emailed to you or your proxyholder after you registered yourself or your proxyholder with AST. The password is “cibc2021” and is case sensitive. | |

If you want to change your vote before the meeting – If you change your mind on the voting instructions you sent through your intermediary and would like to change your vote or vote during the meeting, contact your intermediary to discuss whether this is possible and what procedures you need to follow.

| 4 | C I B C P R O X Y C I R C U L A R |

Table of Contents

Voting

Other voting information

How your proxyholder will vote – If you have given voting instructions in your proxy form or voting instruction form, your proxyholder must vote according to those instructions. If you have not given voting instructions, your proxyholder will decide how to vote. Your proxyholder will also decide how to vote on any amendment or variation to any of the matters in the notice of meeting or any matters that are properly brought before the meeting.

You can vote:

| FOR or WITHHOLD |

• on each director nominee

• on the appointment of auditors | |

| FOR or AGAINST |

• the advisory resolution on our executive compensation approach | |

| FOR, AGAINST or ABSTAIN |

• on the shareholder proposal | |

If the you blank or your space proxyholder on your proxy do not form give or specific voting instruction voting instructions, form, then or management’s you do not insert nominees, a name John in Manley and Victor Dodig will be appointed as your proxyholder and your shares will be voted:

| FOR |

• each director nominee listed in the Circular

• the appointment of Ernst & Young LLP as auditors

• the advisory resolution on our executive compensation approach | |

| AGAINST |

• the shareholder proposal | |

Confidentiality of your vote – To protect the confidentiality of your vote, AST counts proxies and tabulates the results independently and does not inform CIBC about how individual shareholders have voted except where required by law or where a shareholder’s comments are intended for management.

How we solicit proxies – We are soliciting proxies primarily by mail but CIBC employees may contact you by phone or in writing. CIBC pays any costs associated with proxy solicitation.

We reserve the right to accept late proxies and to waive or extend the proxy deadline with or without notice, but are under no obligation to accept or reject a late proxy.

If you want to attend the meeting as a guest – Non-registered shareholders and others who have not been duly appointed and registered with AST as proxyholders may attend the meeting as guests. Guests will not be able to vote at the meeting. You may attend the meeting as a guest in one of these ways:

|

|

Online – go to https://cibc.pividal.tv/agm2021 to join the live webcast; or | |

|

|

Phone – call 1 800 898-3989 passcode 6875673# (English) or 1 877 395-0279 passcode 9080240# (French) for an audio only experience. | |

| Go Paperless!

|

|

Sign up for electronic delivery of our meeting materials and other continuous disclosure documents for future years. Enrolling is easy and electronic delivery is secure, free, convenient and environmentally friendly.

If you are a registered shareholder, go to https://ca.astfinancial.com/edelivery, select Canadian Imperial Bank of Commerce, complete the consent form and hit “submit”.

If you are a non-registered shareholder, go to www.proxyvote.com and use the control number provided on your voting instruction form. |

| C I B C P R O X Y C I R C U L A R | 5 |

Table of Contents

Shareholders will be asked to vote on a shareholder proposal from MÉDAC, 82 Sherbrooke Street West, Montreal, Québec H2X 1X3, telephone: 514 286-1155, email: admin@medac.qc.ca. MÉDAC’s proposal and supporting argument, and the Board’s response, are set out below.

| Proposal No. 1

Circular Economy - It is proposed that the Bank produce a report on the loans it has made in recent years to support the circular economy. |

Argument

According to the Institut de l’environnement, du développement durable et de l’économie circulaire du Québec, the circular economy is “a system of production, trade and consumption designed to optimize the use of resources at all stages of the life cycle of a good or service, taking a circular approach, while reducing the environmental footprint and contributing to the well-being of individuals and communities.”1

Circular business models are rethinking systems and processes, starting at the design stage, to find opportunities to recycle, repair, reuse, repurpose or refurbish products and materials, in order to reduce waste and greenhouse gas emissions. In Canada, as a government publication states, many of our innovators and industries are seeing the benefits of using circular models to save money or open up new market opportunities – from turning pulp-and-paper-mill waste into renewable bioproducts to launching product buy-back programs that enhance customer interaction and recover usable materials such as metals and alloys. These innovative solutions are leading the way toward a more circular economy that benefits the environment while creating wealth and opportunities in industries.

This new approach cannot be developed without financing from Canadian banks. The objective of this proposal is to expand shareholders’ awareness of the Bank’s support for the growth of this new economy in recent years.

1 http://instituteddec.org/themes/economie-circulaire/

The Board recommends that you vote against this proposal.

At CIBC, we are a strong supporter of circular business models and understand the important role that they can play in reducing the environmental impact on society.

Since 2006, we have procured paper from sources that are environmentally and socially responsible, with a preference for FSC-certified stock. At present, CIBC recognizes FSC as the most rigorous third-party certification, which guarantees that purchased forest products come from responsibly managed forests. By purchasing FSC-certified paper products, we are supporting the circular economy by promoting the regeneration of vital natural resources in responsibly managed forests. In 2020, more than 94% of our total paper use was FSC-certified. We also reduced our internal paper consumption in 2020 by 25%.

In 2019, 100% of our used electronics in Canada, the United States, the United Kingdom and the Asia-Pacific region were donated, reused, recycled or upcycled. Where feasible, we redeployed used electronics within the organization. Equipment sent for recycling was broken down into its individual material components and recycled or upcycled into new, innovative products. In 2019, we diverted 538 tonnes of e-waste from landfill.

A portion of our used electronics is donated to a not-for-profit, charitable organization in Canada that is helping to meet the need for computers in schools, public libraries and not-for-profit learning organizations. We have been the largest corporate supporter of the program since our partnership began in 1993. In 2019, we donated approximately 5,000 computer components to the program, which diverted more than 37,000 kilograms of electronic waste from landfills.

Lastly, CIBC supports the circular economy through our procurement practices and supplier partnerships. Our Environmentally Responsible Procurement Standard describes our requirements for the procurement of goods and services that may be associated with significant adverse environmental impacts. Through our supplier questionnaire, we ask our suppliers about the reuse, repair, refurbishment, remanufacturing and recycling of their products, including take-back programs.

We currently do not report on clients supporting the circular economy in our public disclosure. The content of our disclosure is guided by a detailed materiality assessment where we receive input from investors, clients, employees, non-governmental organizations (NGOs) and professional organizations around material topics. Our disclosure will continue to change as new material topics, such as the circular economy, emerge.

| 6 | C I B C P R O X Y C I R C U L A R |

Table of Contents

Shareholder Proposals

Withdrawn Shareholder Proposals

Æquo Shareholder Engagement Services for Comité syndical national de retraite Bâtirente inc.

Æquo Shareholder Engagement Services submitted a shareholder proposal on behalf of Comité syndical national de retraite Bâtirente inc. requesting that CIBC adopt a corporate-wide target to achieve net-zero greenhouse gas emissions associated with its lending and investment activities as defined by best practice carbon accounting standards by 2050.

After discussion with CIBC, Æquo withdrew the proposal based on CIBC signing the requisite forms to join the Partnership for Carbon Accounting Financials and furthering the due diligence underway at CIBC during the course of the year, to measure emissions and develop metrics. CIBC will also consider setting targets in alignment with the Paris Climate Agreement and will report on its activities by the time of the next annual shareholders meeting.

MÉDAC

MÉDAC withdrew seven shareholder proposals after discussion with CIBC. At MÉDAC’s request, the text of each proposal, MÉDAC’s supporting statement and CIBC’s response are set out below.

| 1. Purpose and Commitment - It is proposed that the Board of Directors and management state the purpose of the Canadian Imperial Bank of Commerce as an organization and that a committee of the Board of Directors be instructed to monitor the implementation of the policies, commitments and initiatives put in place in order to give concrete expression to this new strategic orientation, in particular in connection with health, the environment, human resources, and stakeholder relations. |

Argument

In August 2019, the Business Roundtable, an association whose members are the CEOs of large American corporations, published a statement asserting that the purpose of a corporation could not be limited to the pursuit of profit alone, and had to take into account all of the stakeholders who may be affected by its activity: customers, employees, suppliers, communities and shareholders. If corporations are of no social utility, they lose all purpose.

The purpose of a corporation refers to the manner in which it intends to play a role in society, beyond just its economic activity. Jean-Dominique Senard, Chairman of the Board of Renault, has said: “A corporation’s purpose brings together past and present; it is its DNA. It has no economic significance; rather, it falls into the realm of vision and meaning.”1 Essentially, it is “the contribution that the corporation seeks to make to the key social, societal, environmental and economic issues in its business or industry by involving its key stakeholders.”

While many corporations have instituted a number of good initiatives in this direction over time, no purpose that would correspond to this definition can be discerned from the various institutional reports. In addition, there is no committee of the Board whose mandate is to coordinate all of the actions taken to give concrete expression to the purpose chosen. More specifically, that committee’s mission should be:

| • | to prepare and inform the work of the Board in implementing the policies, commitments and initiatives put in place by the Canadian Imperial Bank of Commerce; |

| • | in connection with its strategic orientations, in particular health, the environment, and human resources; |

| • | to dialogue with the various stakeholders regarding its progress in achieving those objectives and report to the Board on its meetings; |

| • | to examine the systems for non-financial accountability and oversight and the key results of the non-financial information published by the Canadian Imperial Bank of Commerce; |

| • | to inform shareholders about the various issues raised by its work. |

In order for this concept of purpose to take on concrete form and not remain simply a marketing slogan, it must be given tangible expression in an institution’s governance practices.

In conclusion, we would note that for a growing number of investors, organizations that have no social utility cease to have a purpose.

1 Jean-Dominique Senard: “Le sens et le pourquoi nourrissent la motivation”, Les Échos, June 8, 2018

https://business.lesechos.fr/directions-generales/innovation/innovation-sociale/0301754783119-jean-dominique-senard-president-de-michelin-le-sens-et-le-pourquoi-nourrissent-la-motivation-321483.php

| C I B C P R O X Y C I R C U L A R | 7 |

Table of Contents

Shareholder Proposals

Board statement

In 2019, CIBC stated, and engaged our 44,000 employees around, our common purpose – to help make your ambition a reality. The word ‘your’ in our purpose statement represents all our key stakeholders: clients, employees, communities and shareholders. Externally, our purpose is clearly stated and disclosed in our Annual Report, Management Proxy Circular and Sustainability Report.

Our shared purpose has served as a galvanizing north star for our bank to accelerate our transformation and guide everything we do – how we act, how we operate and how we make decisions as we ensure sustainable value creation for all our stakeholders. Through strong leader and employee engagement, we have made significant progress to embed our purpose across the organization. This includes embedding our purpose in our strategy, Code of Conduct, learning and development, and performance measurement and management for all employees.

As a cornerstone of our strategic framework and enterprise value framework, our purpose guides our business decisions, our commitment to stakeholders, and the concrete initiatives we have undertaken to ensure our purpose is a fundamental part of how we do business. From our strategy, to how we engage with our clients, to our corporate giving program – our purpose underpins everything we do.

While our Board of Directors has overseen our multi-year purpose journey, from initial development, to enterprise-wide team engagement and strategic initiatives, to how we measure progress, the Board has committed to mandating the Corporate Governance Committee with responsibility to oversee CIBC’s alignment to our purpose and related initiatives.

| 2. Human Resources Committee with Full Committee Status - It is proposed that the Board of Directors revise the mandate of its compensation or human resources committee to include a more specific statement of its responsibilities in connection with the health, safety and wellness of all its employees. |

Argument

Since the COVID-19 crisis began, employee health, safety and wellness have been a subject of growing concern for the senior management of our organizations. In addition to those concerns, employee talent development is important for meeting the challenges presented by new technologies.

The mandate and responsibilities of compensation or human resources committees should be adjusted in order to assure shareholders and other stakeholders that all strategies and policies are being put in place to address these concerns. At present, a large part of these committees’ work focuses on managing executive performance and compensation.

The purpose of this proposal is to ask that the Board of Directors revise the mandate of the human resources committee or create a specific committee whose mandate would be to assist it in carrying out its responsibilities in connection with deciding the vision and overseeing issues relating to employee health, safety and wellness, in particular as they relate to its strategies, policies, systems and practices in that regard and management of the associated risks. For example, the committee could be asked to address the following subjects: training and talent development, diversity, labour relations, pay equity, organizational culture, physical design of the workplace, impact of teleworking on employees’ health, both physical and mental, and employee engagement and satisfaction. These strategic aspects of human resources management should be disclosed in the management circular. This proposal is based on the standards and indicators adopted by the Sustainability Accounting Standards Board (SASB), which are often cited as a roadmap for standardizing human resources management information.

Employee health and wellness do not just supplement an organization’s strategy; they are essential to it, and that is our perspective in submitting this proposal.

Board statement

The mandate of our Management Resources and Compensation Committee (MRCC) outlines the MRCC’s responsibility to assist the Board of Directors in their global oversight of CIBC’s human capital strategy, including talent and total rewards, which incorporates health, safety and well-being, and the alignment with CIBC’s strategy, risk appetite and controls. The MRCC spends a significant portion of its time on human capital strategy, culture, talent management and succession planning.

The health, safety and well-being (including physical, emotional and financial well-being) of our team members is always a priority and this was even more critical during the COVID-19 pandemic. The Board, including our MRCC members, held a number of special meetings to discuss CIBC’s response to the pandemic. CIBC took a number of actions to support the health, safety and well-being of our team, such as: the immediate transition of the majority of our team members to work remotely, new safety measures and protocols for team members working onsite, continued pay for

| 8 | C I B C P R O X Y C I R C U L A R |

Table of Contents

Shareholder Proposals

employees while on precautionary leaves, per diem pay for team members working onsite, increase in the amount of interest-free loans offered to all team members, top-up pay for part-time and casual employees, virtual access to medical professionals for team members and their families, and on-site nurses at key locations.

The MRCC’s report is included starting on page 39 of this Circular and highlights the topics discussed in 2020. CIBC’s response to COVID-19 for employees, clients and communities is one of those topics and includes discussion of an employee pulse check survey and issues related to employee health, safety and well-being; our return to the office strategy, which also has a specific focus on employee health, safety and well-being; talent management and succession planning for key leadership roles; progress against CIBC’s inclusion and diversity strategy; CIBC’s gender pay analysis; an update on our purpose, brand and marketing programs; real estate transformation; launch of CIBC’s new recognition program; and updates on the launch of CIBC’s modern human resources platform.

For more detailed information, see our Message to our Fellow Shareholders and Compensation Discussion and Analysis (CD&A), starting on page 61, “Talent Management and Succession Planning” on page 83 and “Inclusion and Diversity” on page 84.

Given the MRCC’s current responsibilities pertaining to the health, safety and well-being of our team members, the Board has committed to including these words specifically in the MRCC’s mandate.

| 3. Diversity Target - It is proposed that the Bank adopt a target of more than 40% for the composition of its Board of Directors for the next five years. |

Argument

At the last annual meeting, this proposal received 9.0% support among shareholders who voted. At present, the Bank has adopted a target of 30% representation of each sex, while representation has exceeded 40% in the last two years.

Because banks often act as beacons of sound governance for small and medium-sized enterprises, failing to update the target may suggest that this objective is the ideal to be achieved. In fact, it is recognized that there are more competent women than there are positions to be filled and that various stereotypes and biases have impeded women’s access to these positions. With this in mind, it is therefore proposed that the Bank review its diversity policy with a view to raising the minimum representation of both sexes on their boards of directors to 40%.

Board statement

As set out in CIBC’s Board Diversity Policy, the Board seeks gender parity. Our Board is proud that the percentage of directors who are women will be 50% upon the election of the director nominees identified in this Circular at CIBC’s annual meeting. This calculation includes the CEO. In addition, the Board is proud to have announced on December 3, 2020, that CIBC’s successor Chair of the Board will be Katharine B. Stevenson, effective upon her election as a director at CIBC’s annual meeting.

The appointment or retirement of a single Board member has a notable impact on the percentage of men and women on the Board. In the coming years, that percentage will fluctuate as directors who reach their maximum term of service retire and new directors join. Therefore, the Board’s minimum target for gender diversity continues to be at least 30% women and at least 30% men.

In 2020, the Board updated CIBC’s Board Diversity Policy on the Board’s commitment to reflect the diversity of CIBC’s employees, clients and the communities CIBC serves. See “Inclusion and Diversity” on page 54 of our Circular for a detailed description of the Board Diversity Policy.

| 4. Virtual Meetings and Shareholders’ Rights - It is proposed that the Board of Directors adopt a policy stating the procedure for holding virtual annual meetings. |

Argument

Over the last year, the banks and a number of other organizations have relied on new teleconferencing technologies for holding their annual general meetings, because of the pandemic. While MÉDAC is well aware that these new technologies were often being used by the organizations for the first time, it and other individuals or organizations that are submitting shareholder proposals or that would like to make comments or suggestions at these virtual meetings have unfortunately experienced problems that limited the extent to which they were able to participate. More specifically, our impression of the 2020 virtual annual meetings was as follows: “We were unfortunately unable to speak at these meetings, since it was impossible for shareholders to access the microphone during the virtual meetings. The only people who spoke at the meetings were representatives [of the companies]: the chairperson (of the Board, and thus of the meeting), the CEOs, etc.”1 For small

| C I B C P R O X Y C I R C U L A R | 9 |

Table of Contents

Shareholder Proposals

shareholders, this limited presence at annual meetings can have an impact on the success of their proposals in the long term, since they are unable to advocate for their proposals in person and thus build additional support for potential submission of their proposals in future.

These threats are a source of concern about participation by shareholders who, whether because dialogue with the issuer was fruitless or for some other reason, take the route of submitting shareholder proposals in management circulars and at annual meetings.

Experience with shareholder participation and shareholder proposals over the last 20 years has demonstrated the added value that they bring to governance, for example regarding separation of the office of president and CEO from that of chair of the Board of Directors, advisory votes on executive compensation, disclosure of fees paid to auditors and compensation advisors, women’s representation on boards of directors and in executive positions, access to proxies for nominating directors, etc.

We recommend that the Board of Directors adopt a policy stating the procedure for shareholder participation at virtual annual meetings:

| • | oral presentation of shareholder proposals by the individuals or organizations that submitted them, lasting at least as long as the time needed to read the proposals; |

| • | visible electronic image of shareholders during their presentations and also of members of senior management; |

| • | opportunity to ask spontaneous questions following management presentations; |

| • | interaction in real time between shareholders and with the chairperson of the meeting; |

| • | in the event that questions raised by shareholders cannot be addressed at the annual meeting, management answers to be put online, on the company’s website and in SEDAR, within ten days after the meeting is held. |

1 https://medac.qc.ca/1798/

Board statement

In March 2020 and December 2020, CIBC and certain other financial institutions obtained a court order to permit a virtual annual meeting as a proactive and precautionary measure to support public health protocols related to the COVID-19 pandemic and to help protect the health and well-being of our employees, clients, shareholders and communities.

For our 2020 annual meeting, we established and disclosed procedures enabling shareholders to:

| • | access the meeting by phone or online; |

| • | vote online; |

| • | view online images of our Board members and management; |

| • | submit questions to our Board members and management in real time through the webcast and receive responses in real time; |

| • | have sufficient time throughout the meeting to submit questions or comments by opening the webcast for questions at the beginning of the meeting rather than when the Q&A period started; and |

| • | view an archived recording of the meeting at www.cibc.com when convenient for shareholders. |

We are pleased that attendance at our 2020 virtual annual meeting increased by 168% compared to our 2019 annual meeting. We thank MÉDAC and other shareholders for their feedback on our 2020 virtual meeting. We considered that feedback, the virtual meetings at other Canadian public companies, and available technological solutions.

For our 2021 virtual annual meeting, we are pleased that we have more capability to provide a better shareholder experience with improvements to the quality of video presentations during the meeting; opportunity for shareholders to present their proposals published in our Circular live by video; the ability for shareholders to make comments or ask questions verbally by phone as well as in writing through the online webcast; and the ability for shareholders to submit questions in advance of the meeting by email or mail. We look forward to the time we can host an in-person annual meeting but for those shareholders who prefer the online experience, we will continue to evolve our approach based on shareholder feedback and available technological solutions.

| 10 | C I B C P R O X Y C I R C U L A R |

Table of Contents

Shareholder Proposals

| 5. COVID-19 — Sharing the Burden of the Recovery Fairly - It is proposed that the Board of Directors disclose the actions taken by the organization to ensure that both the corporation’s executives and other employees bear their fair share of the economic recovery effort when the pandemic is over. |

Argument

The 2008 economic crisis left a bitter taste in the mouths of some shareholders. While their stock portfolios saw sharp declines in value, senior executives and directors continued to receive what some considered to be excessive pay increases unrelated to the corporation’s performance. That situation paved the way for the introduction of the non-binding advisory vote relating to executive compensation and sullied the reputations of a number of organizations.

The current pandemic and economic crisis has forced some corporations to make difficult decisions, including having to lay off employees both temporarily and permanently. When it comes to executives and Board members, little information has been disclosed concerning actions taken in their regard in order to reduce the number of people in those positions or their compensation.

The objective of this proposal is to ask that the Board of Directors disclose the following information in the next management circular:

| • | The percentage and number of people laid off, both permanently and temporarily, as a result of the pandemic, for both executive and other employees; |

| • | The percentage reduction in compensation applied to the two categories of employees; |

| • | The discretion enjoyed by the compensation committee or the Board of Directors for granting pay increases to executives even though some performance objectives have not been achieved because of the economic crisis and pandemic; |

| • | The adjustments made to the compensation policy for the coming years to reflect the declines in compensation that some of its employees may have suffered; |

| • | Any other adjustment made to the policy for granting stock or stock options to compensate executives for earnings losses suffered in 2020. |

Board statement

Throughout the COVID-19 pandemic, CIBC has been open in disclosing actions to support our employees, clients and communities. In February 2020, before the onset of the COVID-19 pandemic in Canada, we announced a restructuring charge of $339 million to cover severance from staff reductions affecting approximately 5% of employees in support of an enterprise-wide program to accelerate the delivery of our priorities, including improving efficiency. The restructuring was a difficult decision but necessary to adapt our cost structure in order to simplify, reinvest in and position our bank to further strengthen our relationships with our clients.

In March 2020, when the pandemic took hold with unexpected health and economic impacts, we put a temporary pause on implementing the planned staff reductions. We supported our employees by transitioning the majority of our team to work remotely and honoured our commitments to new hires and summer students. In addition, we provided a per diem payment to team members who were needed on site to support our clients, full pay to those whose hours were reduced temporarily to protect the health of our clients and employees, and additional paid time off.

As we disclose in our Circular, executive pay is based on Total Direct Compensation (TDC) targets which include annual salary and variable incentive awards. Targets are reviewed annually against market data and adjusted over time to ensure progression within the role is taken into account. The Board and MRCC review the TDC targets for the Named Executive Officers (NEOs) and other senior roles and only approve increases when required to appropriately align the executive’s pay with the market. In fiscal 2020, no reductions were made to salaries for executives or employees as a result of the COVID-19 pandemic. However, as discussed in our Message to our Fellow Shareholders and CD&A, based on CIBC’s fiscal 2020 performance, the calculated Business Performance Factor (BPF) was 94% and the Board approved a qualitative adjustment of -5% for our executives, in recognition of the impact of COVID-19 on our business, shareholders and communities. As a result, the BPF for our executives was 11% below our target and well below the maximum payout opportunity, while the reduction in the BPF for our employees was 10% below our target, ensuring that bonuses for those in more senior roles were impacted more than the rest of our employees during these challenging times.

We did not make any adjustments to the compensation policy to offset declines in compensation levels or to our stock option grant policy. As disclosed in our 2021 Proxy Circular, prior year stock options are out-of-the-money, shares are valued at less than their notional value, however, we have not made any adjustments to compensate our executives for losses suffered in 2020.

| C I B C P R O X Y C I R C U L A R | 11 |

Table of Contents

Shareholder Proposals

| 6. Global Warming - It is proposed that the Bank produce a report on the loans it has made to projects with polluting impacts that lead to a significant rise in global temperatures. |

Argument

The aim of the Paris Agreement is to keep the global temperature rise to 2°C and, if possible, to 1.5°C. According to Mark Carney, the former Governor of the Bank of Canada and the Bank of England, now the United Nations Special Envoy on Climate, the funds provided by banks and investment firms to support a number of large polluting projects will bring about an increase of 4°C, while the Paris Agreement seeks to keep the global temperature rise to 2°C or even 1.5°C.

He also says that the objectives of the Agreement are clear, but organizations’ policies are inconsistent; when the 20 largest energy companies in the world are responsible for a third of all carbon emissions on Earth, it is time, according to the Governor of the Bank of England, to put the brakes on the appetite of the financial system, which does not seem to be concerned about the climate emergency.

The purpose of this proposal is to ask that the Bank publish information about the amounts lent to projects that have significant impacts on global temperatures.

Board statement

CIBC has a strong commitment to climate action as demonstrated by our continued improvements in the areas of target setting, transparency and reporting. Communicating openly and regularly about our climate-related work is important to our stakeholders and it helps us track our progress and identify where we can improve. Our commitment to climate action was recognized by CDP, which gave us a score of A- for our 2020 disclosure - above the banking sector average score of B.

In 2019, we published our first report under the Task Force on Climate Related Financial Disclosure and committed to support $150 billion in environmental and sustainable finance by 2027. CIBC is committed to sustainable finance to help direct capital towards important development projects and innovations that address urgent environmental and social challenges. In 2020, we furthered our support and commitment:

| • | We increased lending and capital markets activities to businesses focused on sustainable development. |

| • | We developed a green bond framework with our second-party opinion from Sustainalytics and issued our first green bond in October 2020. |

| • | We supported $42.1 billion in environmental and sustainable financial activities, achieving a cumulative 28% of our 10-year target. |

| • | We committed to become carbon neutral and source 100% of our electricity from renewable sources by 2024. |

| • | We established a partnership with Bullfrog Power to offset 15,000 MWh of electricity use through the purchase of Ecologo certified renewable energy credits. |

| • | We disclosed our Environmental Policy and Lending Policy, which include a statement related to not financing oil and gas exploration in the Arctic National Wildlife Refuge (ANWR). |

| • | Through our partnerships with the United Nations Environment Program – Finance Initiative (UNEPFI) and the Canadian Standards Association (CSA), we are working with other stakeholders to enhance climate disclosure and ensure that financial instruments to support the transition to net zero include all sectors of our economy. |

| • | We committed $1.25 million over five years to the Institute for Sustainable Finance (ISF), which is a partnership between Canadian banks and Canadian universities to advance sustainable finance and put Canada in a leadership position related to the transition of net zero. |

We are committed to supporting our clients as they transition to a low carbon future and we recognize the important role banks will have in financing an orderly transition. According to Mark Carney, the former Governor of the Bank of Canada and the Bank of England, now the United Nations Special Envoy on Climate, “Certain people look at climate change and think they need to divest from energy companies, but they are very much part of the solution”. Transparency is extremely important and we have begun evaluating methodologies to measure the impact of our financing which we plan to disclose when available.

| 12 | C I B C P R O X Y C I R C U L A R |

Table of Contents

Shareholder Proposals

| 7. Discretion of the Board of Directors and the Compensation Committee - It is proposed that the management circular expressly set out the benchmarks used by both of these bodies for revising the objectives associated with executive compensation and performance. |

Argument

Over the last year, the health and economic crisis has certainly had an impact on key performance measures and the associated targets that executives had to meet during 2020. Have the Board of Directors and the human resources committee adjusted the objectives, if necessary, or have they used a special power to revise the compensation policy, given that performance in relation to the predetermined targets does not entirely reflect the overall quality of these executives’ performance?

The objective of this proposal is to ask that the corporation disclose precisely the adjustments made to key performance measures, to targets and to the associated compensation paid, for all executives, if such is the case.

Board statement

The CD&A section of CIBC’s Circular provides robust disclosure on our approach to executive compensation and performance. CIBC’s Board of Directors and the MRCC have not adjusted the objectives or used any special powers to revise the compensation policy in fiscal 2020.

As discussed on page 73 of our Circular, the Board and the MRCC have the discretion to adjust the calculated BPF based on qualitative factors including:

| • | relative performance vs. peers to assess our performance against key financial measures such as revenue and EPS growth; |

| • | risk, to ensure compensation is aligned with our risk appetite and objectives by considering risk outcomes with adjustments being made only to reduce the BPF (or individual awards); |

| • | unexpected outcomes and other items that either should be included or excluded from the performance that determines the BPF; and |

| • | any other factors the MRCC and the Board consider appropriate. |

When the Board and the MRCC make such discretionary adjustments to our BPF, we disclose the fact in our Circular. For example: on page 59 of our 2017 Circular, the first year that the BPF was introduced, we disclosed that the calculated BPF was 113.4% and the Board approved a qualitative adjustment of -4.4%, taking into consideration our Total Shareholder Return performance relative to our peer group and other items that the Board agreed should be considered in assessing the performance results used to calculate compensation; and on pages 60 and 71 of our 2018 Circular, we disclosed the fact that based on CIBC’s fiscal 2017 performance, the calculated BPF was 112.3% and that the Board approved a qualitative adjustment of -4.3% based on CIBC’s performance relative to our peer group.

As you can read in our current 2021 Circular, on page 62 of the Message to our Fellow Shareholders and page 74 in the CD&A, we have continued this approach to our disclosure and have noted that based on CIBC’s fiscal 2020 performance, the calculated BPF was 94% and that the Board approved a qualitative adjustment of -5%, in recognition of the impact of COVID-19 on our business, shareholders and our communities. As a result, the final BPF for our executives was 89%, 11% below our target and well below the maximum payout opportunity.

| C I B C P R O X Y C I R C U L A R | 13 |

Table of Contents

There are 14 director nominees. Each nominee was elected at the last annual meeting of shareholders on April 8, 2020, except Mary Lou Maher who is a new nominee.

On December 3, 2020, CIBC announced that The Honourable John Manley, current Chair of the Board, will retire at the close of our 2021 annual shareholders’ meeting and Katharine Stevenson will be the Chair of the Board effective on her re-election as a director at the meeting. In addition, Brent Belzberg retires at the close of our annual meeting. The Board would like to thank Mr. Manley and Mr. Belzberg for their years of dedicated service to the Board and to CIBC.

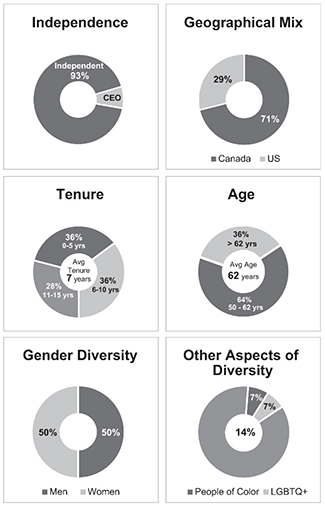

Information on each nominee starts on page 15. Below are key highlights about CIBC’s board composition if each nominee is elected by shareholders.

|

|

2020 Overall Attendance

100%

| |||

|

2020 Average votes FOR

99%

| ||||

|

Senior Leadership Experience

100%

| ||||

|

For information about the nomination process see the Statement of Corporate Governance Practices – “Director Nomination Process” and “Director Tenure” starting on page 49. | ||||

| 14 | C I B C P R O X Y C I R C U L A R |

Table of Contents

Directors

CHARLES J.G. BRINDAMOUR, Toronto, Ontario, Canada

| Skills: • Strategy | • Risk Management/Risk Governance |

|||||||

|

Director since: 2020

Age: 50

Independent

2020 Shareholder votes in favour: 99.5% |

• Financial Services |

• Corporate Responsibility/Sustainability |

||||||

| • Financial Expertise

|

• Public/Government Relations

|

|||||||

|

| ||||||||

|

Principal occupation: Chief Executive Officer, Intact Financial Corporation

| ||||||||

|

| ||||||||

|

Experience: Mr. Brindamour is Chief Executive Officer of Intact Financial Corporation, the largest provider of property and casualty insurance in Canada and a leading provider of specialty insurance in North America. Mr. Brindamour began his career with Intact in 1992 and has held progressively senior roles in Canada and abroad with Intact and its former affiliates. He was appointed President and Chief Executive Officer of Intact Financial Corporation in January 2008. Mr. Brindamour has deep experience in the North American financial services industry and is a respected business leader with more than 25 years of operating experience. In addition to the public company directorship noted below, Mr. Brindamour serves on the board of the Business Council of Canada, is Chair of the Board of the Geneva Association and co-founder of the Intact Centre for Climate Adaptation at the University of Waterloo. Mr. Brindamour is also a member of the 30% Club Canada.

| ||||||||

|

| ||||||||

|

Education: Mr. Brindamour is a graduate of Laval University in Actuarial Sciences and an Associate of the Casualty Actuarial Society and was awarded an honorary Doctorate from HEC Montréal.

| ||||||||

|

Other public company board directorships during last five years

| ||||||||

|

Current: |

Current committee memberships: | |||||||

|

Intact Financial Corporation – since 2008

|

– |

|||||||

|

| ||||||||

|

Former: |

||||||||

|

Hydro One – 2015 to 2018

|

||||||||

|

2020 Board and committee membership and attendance

| ||||||||

|

Overall attendance: 100% |

||||||||

|

Board (from February 2020): 6/6 |

||||||||

|

Risk Management Committee (from February 2020): 5/5 |

||||||||

|

CIBC equity - Mr. Brindamour meets the equity ownership guideline

| ||||||||||||||||||||

| Year | Shares(1) (#) |

DSUs(2) (#) |

Total Shares/DSUs (#) |

Total value of Shares/DSUs(3) ($) |

Total as a multiple of share ownership guideline(5) | |||||||||||||||

| 2021 |

12,532 | 0 | 12,532 | 1,362,479 | 1.8x | |||||||||||||||

| 2020 |

11,604 | 0 | 11,604 | 1,253,928 | 1.7x | |||||||||||||||

| C I B C P R O X Y C I R C U L A R | 15 |

Table of Contents

Directors

NANCI E. CALDWELL, Woodside, California, USA

| Skills: • Strategy | • Corporate Responsibility/Sustainability |

|||||||

|

Director since: 2015

Age: 62

Independent

2020 Shareholder votes in favour: 99.5% |

• Human Resources Management/ Compensation

|

• Information Technology |

||||||

|

| ||||||||

|

Principal occupation: Corporate Director

| ||||||||

|

| ||||||||

|

Experience: Ms. Caldwell was Executive Vice-President and Chief Marketing Officer for PeopleSoft, Inc. from 2002 through 2004. She held increasingly senior and executive sales and marketing roles at Hewlett Packard Company in Canada and the US from 1982 to 2001. Ms. Caldwell has served on several public and private technology company boards since 2005 and has more than 25 years of operating experience in the global technology and software industries. In addition to the public company directorships listed below, Ms. Caldwell has served as a director on private company boards including RedPrairie, Inc., now known as JDA Software, LiveOps Inc., Sophos, plc and Network General Corporation.

| ||||||||

|

| ||||||||

|

Education: Ms. Caldwell holds a Bachelor of Arts degree from Queen’s University and completed Western University’s Executive Marketing Management Program.

| ||||||||

|

Other public company board directorships during last five years

| ||||||||

|

Current: |

Current committee memberships: | |||||||

|

Citrix Systems, Inc. – since 2008

|

Independent Lead Director; Nominating and Corporate Governance (Chair); Compensation

|

|||||||

|

Equinix, Inc. – since 2015

|

Governance (Chair)

|

|||||||

|

| ||||||||

|

Former: |

||||||||

|

Donnelley Financial Solutions Inc. – 2016 to 2020

Talend – 2017 to 2020

|

||||||||

|

2020 Board and committee membership and attendance

| ||||||||

|

Overall attendance: 100% |

||||||||

|

Board: 7/7 |

||||||||

|

Management Resources and Compensation Committee: 6/6 |

||||||||

|

CIBC equity - Ms. Caldwell has until December 4, 2022 to meet the equity ownership guideline(4)

| ||||||||||||||||||||

| Year | Shares(1) (#) |

DSUs(2) (#) |

Total Shares/DSUs (#) |

Total value of Shares/DSUs(3) ($) |

Total as a multiple of share ownership guideline(5) | |||||||||||||||

| 2021 |

7,209 | 0 | 7,209 | 783,762 | 0.8x | |||||||||||||||

| 2020 |

4,582 | 0 | 4,582 | 495,131 | 0.5x | |||||||||||||||

| 16 | C I B C P R O X Y C I R C U L A R |

Table of Contents

Directors

MICHELLE L. COLLINS, Chicago, Illinois, USA

| Skills: • Financial Services

|

• Financial Expertise

|

|||||||

|

| ||||||||

|

Director since: 2017

Age: 60

Independent

2020 Shareholder votes in favour: 99.7% |

Principal occupation: President, Cambium LLC

| |||||||

|

| ||||||||

|

Experience: Ms. Collins has been President of Cambium LLC since 2007. Cambium is a Chicago-based business and financial advisory firm that serves small and medium-sized businesses. She brings 30 years of experience in corporate governance, investment banking, and private equity and has significant corporate board experience, having served as a director for several publicly traded companies across a wide range of industries. In addition to the public company directorship noted below, Ms. Collins is a director of CIBC Bancorp USA Inc., CIBC Bank USA, Health Care Service Corporation and Strategic Marketing Inc. and is a member of the Global Risk Institute. She is also a member of the Advisory Boards of Svoboda Capital Partners, LLC and Cedar Street Asset Management and has served on several philanthropic and non-profit boards, including the Chicago Public Library Foundation and the Museum of Science and Industry.

Ms. Collins received the 2018 Spirit of Erikson Award from Erikson Institute in recognition of her 22 years of service on the board, including as chair from 2014 to 2017, and her commitment to children and families that Erikson serves. Ms. Collins also received the 2018 Outstanding Leader Award for Business from the YWCA in recognition of her distinguished career in business, her community involvement and willingness to take on leadership positions on impacting women’s lives and racial justice.

| ||||||||

|

| ||||||||

|

Education: Ms. Collins holds a Bachelor of Arts degree in Economics from Yale University and a Master of Business Administration degree from Harvard University.

| ||||||||

|

Other public company board directorships during last five years

| ||||||||

|

Current: |

Current committee memberships: | |||||||

|

Ulta Beauty Inc. – since 2014

|

Audit; Nominating and Corporate Governance (Chair)

|

|||||||

|

| ||||||||

|

Former: |

||||||||

|

PrivateBancorp, Inc. – 2015 to 2017 (ceased to be a public company in 2017)

|

||||||||

|

2020 Board and committee membership and attendance

| ||||||||

|

Overall attendance: 100% |

||||||||

|

Board: 7/7 |

||||||||

|

Audit Committe (from April 2020): 3/3 |

||||||||

|

Risk Management Committee (to April 2020): 3/3 |

||||||||

|

CIBC equity - Ms. Collins meets the equity ownership guideline

| ||||||||||||||||||||

| Year | Shares(1) (#) |

DSUs(2) (#) |

Total Shares/DSUs (#) |

Total value of Shares/DSUs(3) ($) |

Total as a multiple of share ownership guideline(5) | |||||||||||||||

| 2021 |

1,357 | 10,064(6) | 11,421 | 1,241,691 | 1.2x | |||||||||||||||

| 2020 |

1,357 | 6,070(6) | 7,427 | 802,562 | 0.8x | |||||||||||||||

| C I B C P R O X Y C I R C U L A R | 17 |

Table of Contents

Directors

PATRICK D. DANIEL, Calgary, Alberta, Canada

| Skills: • Strategy | • Corporate Responsibility/Sustainability |

|||||||

|

Director since: 2009

Age: 74

Independent

2020 Shareholder votes in favour: 99.0% |

• Human Resources Management/Compensation

|

• Information Technology |

||||||

|

| ||||||||

|

Principal occupation: Corporate Director

| ||||||||

|

| ||||||||

|

Experience: Mr. Daniel was President and Chief Executive Officer of Enbridge Inc. from 2001 to 2012. Prior to his appointment as President and CEO, he was a senior executive officer of Enbridge Inc. or its predecessor since 1994. Mr. Daniel is a past recipient of Canada’s Outstanding CEO of the Year award and Chair of the Daniel Family Foundation.

| ||||||||

|

| ||||||||

|

Education: Mr. Daniel holds a Bachelor of Science degree from the University of Alberta and a Master of Science degree from the University of British Columbia.

| ||||||||

|

Other public company board directorships during last five years

| ||||||||

|

Former: |

||||||||

|

Capital Power Corporation – 2015 to 2018

Cenovus Energy Inc. – 2009 to 2020

|

||||||||

|

2020 Board and committee membership and attendance

| ||||||||

|

Overall attendance: 100% |

||||||||

|

Board: 7/7 |

||||||||

|

Corporate Governance Committe (to April 2020): 3/3 |

||||||||

|

Management Resources and Compensation Committee (Chair): 6/6 |

||||||||

|

CIBC equity - Mr. Daniel meets the equity ownership guideline

| ||||||||||||||||||||

| Year | Shares(1) (#) |

DSUs(2) (#) |

Total Shares/DSUs (#) |

Total value of Shares/DSUs(3) ($) |

Total as a multiple of share ownership guideline(5) | |||||||||||||||

| 2021 |

10,100 | 26,451 | 36,551 | 3,973,825 | 5.3x | |||||||||||||||

| 2020 |

10,100 | 23,504 | 33,604 | 3,631,248 | 4.8x | |||||||||||||||

| 18 | C I B C P R O X Y C I R C U L A R |

Table of Contents

Directors

LUC DESJARDINS, Toronto, Ontario, Canada

| Skills: • Strategy | • Corporate Responsibility/Sustainability |

|||||||

|

Director since: 2009

Age: 68

Independent

2020 Shareholder votes in favour: 98.1% |

• Financial Services |

• Legal/Regulatory/Compliance |

||||||

| • Financial Expertise |

• Public/Government Relations |

|||||||

| • Human Resources Management/Compensation

|

• Information Technology

|

|||||||

|

| ||||||||

|

Principal occupation: President and Chief Executive Officer, Superior Plus Corp.

| ||||||||

|

| ||||||||

|

Experience: Mr. Desjardins has been President and Chief Executive Officer of Superior Plus Corp., a Toronto-based public company that provides propane distribution and marketing services and specialty chemical production, since 2011. Mr. Desjardins was an equity partner at The Sterling Group, LP from 2008 to 2011 and President and Chief Executive Officer of Transcontinental Inc. from 2004 to 2008. In addition to the public company directorship noted below, Mr. Desjardins is a director of Gestion Jourdan SEC, a member of the Chief Executives Organization and a member of the 30% Club Canada. Mr. Desjardins is also a recipient of the Harvard Presidents’ Seminar “Leader of Leaders” award and the Presidents’ Program in Leadership diploma from Harvard Business School.

| ||||||||

|

| ||||||||

|

Education: Mr. Desjardins holds a Master of Business Administration degree from Université du Québec à Montréal and is a graduate of the Harvard Business School Management Development Program.

| ||||||||

|

Other public company board directorships during last five years

| ||||||||

|

Current: |

Current committee memberships: | |||||||

|

Superior Plus Corp. – since 2011

|

– |

|||||||

|