SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

[X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934

FOR THE FISCAL YEAR ENDED: DECEMBER 31, 2015

OR

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934

FOR THE TRANSITION PERIOD FROM _______________ TO _________________

COMMISSION FILE NUMBER: 1-13447

ANNALY CAPITAL MANAGEMENT, INC.

(Exact Name of Registrant as Specified in its Charter)

| MARYLAND | 22-3479661 | |

| (State or other jurisdiction of incorporation or organization) | (IRS Employer Identification No.) | |

| 1211 AVENUE OF THE AMERICAS | 10036 | |

| NEW YORK, NEW YORK | (Zip Code) | |

| (Address of principal executive offices) |

(212) 696-0100

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

|

Title of Each Class

|

Name of Each Exchange on Which Registered

|

|

Common Stock, par value $.01 per share

|

New York Stock Exchange

|

|

7.875% Series A Cumulative Redeemable Preferred Stock

|

New York Stock Exchange

|

|

7.625% Series C Cumulative Redeemable Preferred Stock

|

New York Stock Exchange

|

|

7.50% Series D Cumulative Redeemable Preferred Stock

|

New York Stock Exchange

|

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark whether the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes þ No o

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No þ

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days:

Yes þ No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes þ No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer or a smaller reporting company. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer þ | Accelerated filer o | Non-accelerated filer o | Smaller reporting company o |

| (Do not check if a smaller reporting company) |

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No þ

At June 30, 2015, the aggregate market value of the voting common stock held by non-affiliates of the Registrant was approximately $8.7 billion, based on the closing sales price of the Registrant’s common stock on such date as reported on the New York Stock Exchange.

The number of shares of the Registrant’s Common Stock outstanding on February 19, 2016 was 924,829,841.

DOCUMENTS INCORPORATED BY REFERENCE

The registrant intends to file a definitive proxy statement pursuant to Regulation 14A within 120 days of the end of the fiscal year ended December 31, 2015. Portions of such proxy statement are incorporated by reference into Part III of this Form 10-K.

ANNALY CAPITAL MANAGEMENT, INC. AND SUBSIDIARIES

|

ANNALY CAPITAL MANAGEMENT, INC.

|

||

|

2015 FORM 10-K ANNUAL REPORT

|

||

|

TABLE OF CONTENTS

|

||

|

PART I

|

PAGE

|

|

|

1

|

||

|

11

|

||

|

40

|

||

|

40

|

||

|

40

|

||

|

40

|

||

|

PART II

|

||

|

41

|

||

|

45

|

||

|

46

|

||

|

84

|

||

|

84

|

||

|

84

|

||

|

84

|

||

|

87

|

||

|

PART III

|

||

|

89

|

||

|

89

|

||

|

89

|

||

|

89

|

||

|

89

|

||

|

PART IV

|

||

|

90

|

||

|

90

|

||

|

93

|

||

|

II-1

|

||

i

ANNALY CAPITAL MANAGEMENT, INC. AND SUBSIDIARIES

PART I

ITEM 1. BUSINESS

| “Annaly,” “we,” “us,” or “our” refers to Annaly Capital Management, Inc. and our wholly-owned subsidiaries, except where it is made clear that the term means only the parent company.

Refer to the section titled “Glossary of Terms” located at the end of Part II. Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” for definitions of certain of the commonly used terms in this annual report on Form 10-K.

|

The following description of our business should be read in conjunction with the Consolidated Financial Statements and the related Notes thereto, and the information set forth under the heading “Special Note Regarding Forward-Looking Statements” in Item 7 – Management’s Discussion and Analysis of Financial Condition and Results of Operation. |

|

INDEX TO ITEM 1. BUSINESS

|

|

|

Page

|

|

|

Business Overview

|

2

|

|

Investment Strategy and Capital Allocation Policy

|

2

|

|

Our Portfolio and Capital Allocation

|

3

|

|

Risk Appetite Statement

|

3

|

|

Target Assets

|

4

|

|

Capital Structure and Financing

|

6

|

|

Operating Platform

|

7

|

|

Risk Management

|

7

|

|

Management Agreement

|

7

|

|

Executive Officers

|

8

|

|

Employees

|

8

|

|

Regulatory Requirements

|

8

|

|

Competition

|

9

|

| Corporate Governance | 9 |

|

Distributions

|

10

|

|

Available Information

|

10

|

1

ANNALY CAPITAL MANAGEMENT, INC. AND SUBSIDIARIES

Business

|

Business Overview

We are a leading mortgage real estate investment trust (or REIT) that is externally managed by Annaly Management Company LLC (or Manager). Our common stock is listed on the New York Stock Exchange under the ticker symbol “NLY”. Since our founding in 1997, we have strived to generate net income for distribution to our stockholders and preserve capital through the prudent selection

|

and management of our investments. We own a portfolio of real estate related investments. We use our capital coupled with borrowed funds to invest in real estate related investments, earning the spread between the yield on our assets and the cost of our borrowings.

Our business operations are primarily comprised of the following:

|

|

Business Operations

|

Year Formed

|

Description

|

|

Annaly, the parent company

|

1997

|

Invests primarily in various types of Agency mortgage-backed securities and related derivatives to hedge these investments. Its portfolio also includes residential credit investments such as credit risk transfer securities and non-Agency mortgage-backed securities.

|

|

Annaly Commercial Real Estate Group, Inc. (or ACREG)

|

2009

|

Wholly-owned subsidiary that specializes in originating or acquiring, financing and managing commercial loans and other commercial real estate debt, commercial mortgage-backed securities and other commercial real estate-related assets.

|

|

Annaly Middle Market Lending LLC (or MML)

|

2010

|

Wholly-owned subsidiary that engages in corporate middle market lending transactions.

|

|

RCap Securities, Inc. (or RCap)

|

2008

|

Wholly-owned subsidiary that operates as a broker-dealer, and is a member of the Financial Industry Regulatory Authority (or FINRA)

|

|

We have made significant investments in our business as part of the diversification of our investment strategy. Our operating platform has expanded in support of our diversification strategy, and has included investments in systems, infrastructure and personnel. Our operating platform now supports our investments in Agency and residential credit assets, commercial real estate and corporate loans. The diversity of our investment alternatives provides us the flexibility to adapt to changes in market conditions and to take advantage of potential resulting opportunities.

We believe that our business objectives are supported by our size and conservative financial posture relative to the industry, the extensive experience of our Manager’s employees, the diversity of our investment strategy, a comprehensive risk management approach, the availability and diversification of financing sources, our corporate structure and our operational efficiencies.

|

Investment Strategy and Capital Allocation Policy

Our principal business objectives are to generate net income for distribution to our stockholders from our investments and capital preservation.

We seek to achieve attractive risk-adjusted returns and preservation of capital over the long term through investment in a diversified portfolio of target assets. As part of our diversification strategy, in February 2016, our board of directors (or Board) made changes to the capital allocation policy. The updated policy allows us greater flexibility to generate attractive returns for our stockholders. Under our capital allocation policy, subject to oversight by our Board, we may allocate our investments within our target asset classes as we determine is appropriate from time to time. The following target assets have been approved for investment under our capital allocation policy.

|

2

ANNALY CAPITAL MANAGEMENT, INC. AND SUBSIDIARIES

Business

| Residential | Commercial |

|

Ø Agency mortgage-backed securities

|

Ø Commercial real estate, including:

|

|

Ø To-be-announced forward contracts (or TBAs)

|

Commercial mortgage loans

|

|

Ø Agency debentures

|

Commercial mortgage-backed securities

|

| Ø Residential credit investments, including: |

Preferred equity

|

| Residential mortgage loans |

Other real estate-related debt investments

|

| Residential mortgage-backed securities |

Real property

|

| Agency credit risk sharing transactions |

Ø Corporate debt including loans and securities of

|

| middle market companies |

|

Our Board may adopt changes to our capital allocation policy and targeted assets as it deems appropriate at its discretion.

The nature of our assets and our operations are intended to meet our REIT qualification requirements and our exemption from registration as an investment company under the Investment Company Act.

|

Our Portfolio and Capital Allocation

Our portfolio composition and capital allocation as of December 31, 2015 and 2014 were as follows:

|

|

December 31, 2015

|

December 31, 2014

|

|||||||||||||||

|

Category

|

Percentage of

Portfolio

|

Capital

Allocation (1)

|

Percentage of

Portfolio

|

Capital

Allocation (1)

|

||||||||||||

|

Residential

|

||||||||||||||||

|

Agency mortgage-backed securities and debentures

|

90.5 | % | 77 | % | 97.8 | % | 89 | % | ||||||||

|

Residential credit investments

|

1.8 | % | 5 | % | - | - | ||||||||||

|

Commercial

|

||||||||||||||||

|

Commercial real estate

|

7.0 | % | 14 | % | 2.0 | % | 10 | % | ||||||||

|

Corporate debt

|

0.7 | % | 4 | % | 0.2 | % | 1 | % | ||||||||

|

(1)

|

Capital allocation represents the percentage of stockholders’ equity invested in each category.

|

|

Risk Appetite Statement

We maintain a firm-wide risk appetite statement which defines the level and types of risk that we are willing to take in order to achieve our business objectives and reflects our risk management philosophy. Fundamentally, we will only engage in risk activities that are expected to enhance value for our stockholders based on our core expertise. Our activities focus on capital

|

preservation and income generation through proactive portfolio management, supported by a conservative liquidity and leverage posture.

Our risk appetite statement asserts the following key risk parameters to guide our investment management activities:

|

|

Risk Parameter

|

Description

|

|

Portfolio composition

|

We will maintain a portfolio comprised of target assets approved by our Board and in accordance with our capital allocation policy.

|

|

Leverage

|

We will operate at an economic leverage ratio no greater than 10:1.

|

|

Liquidity Risk

|

We will seek to maintain an unencumbered asset portfolio sufficient to meet our liquidity needs under adverse market conditions.

|

|

Interest rate risk

|

We will seek to manage interest rate risk to protect the portfolio from adverse rate movements utilizing derivative instruments targeting both income and capital preservation.

|

|

Credit Risk

|

We will seek to manage credit risk by making investments which conform within our specific investment policy parameters and optimize risk-adjusted returns.

|

|

Capital preservation

|

We will seek to protect our capital base through disciplined risk management practices.

|

|

Compliance

|

We will comply with regulatory requirements needed to maintain our REIT status and our exemption from registration under the Investment Company Act.

|

3

ANNALY CAPITAL MANAGEMENT, INC. AND SUBSIDIARIES

Business

| Our Board has reviewed and approved the investment and operating policies and strategies established by our Manager and set forth in this Form 10-K. Our Board has the power to modify or waive these policies and strategies without the consent of the stockholders to the extent that our Board determines that the modification or waiver is in the best interests of our stockholders. Among other factors, developments in the market which affect our policies and strategies or which change our assessment of the market may cause our Board to revise our policies and strategies.

We may seek to expand our capital base in order to further increase our ability to acquire new and different types of assets when the potential returns from new investments appear attractive relative to the targeted risk-adjusted returns. We may in the future acquire assets by offering our debt or equity securities in exchange for the assets.

Within the confines of the risk appetite statement, we seek to generate the highest risk-adjusted returns on capital invested, after consideration of the following:

● The amount, nature and variability of anticipated cash flows from the asset across a variety of interest rate, yield spread, financing cost, credit loss and prepayment scenarios;

|

● The liquidity of the asset;

● The ability to pledge the asset to secure collateralized borrowings;

● When applicable, the credit of the underlying borrower;

● The costs of financing, hedging and managing the asset;

● The impact of the asset to our REIT compliance and our exemption from registration under

the Investment Company Act; and

● The capital requirements associated with the purchase and financing of the asset.

The capital requirements associated with the purchase and financing of the asset.

We target the purchase and sale of the following assets as part of our investment strategy. Our targeted assets and asset acquisition strategy may change over time as market conditions change and as our business evolves.

|

4

ANNALY CAPITAL MANAGEMENT, INC. AND SUBSIDIARIES

Business

|

Targeted Asset Class

|

Description

|

|

Residential

|

|

|

Agency mortgage-backed securities

|

Our primary investments consist of Agency pass-through certificates, collateralized mortgage obligations (or CMOs) issued or guaranteed by Freddie Mac, Fannie Mae or Ginnie Mae, and other securities such as interest-only securities and inverse floaters. These securities are backed by single-family or multi-family residences with loan maturities typically ranging from 15 to 40 years and may have fixed or floating coupons.

|

|

TBAs

|

We purchase and sell TBAs which are forward contracts for Agency mortgage-backed securities. TBA contracts specify a few basic characteristics of the Agency mortgage-backed securities, such as the coupon rate, the issuer, term, and the approximate face value of the bonds to be delivered, with the actual bonds to be delivered only identified shortly before the TBA settlement date.

|

|

Agency debentures

|

We invest in debt issued by Freddie Mac, Fannie Mae or the Federal Home Loan Banks. These debentures are not backed by collateral, but by the creditworthiness of the issuer.

|

|

Residential credit investments

|

We invest in residential credit investments including: investments in single-family and multi-family privately-issued certificates that are not issued by one of the Agencies, securities backed by a pool of non-performing or re-performing loans, Agency risk sharing transactions issued by Fannie Mae and Freddie Mac and similarly structured transactions arranged by third party market participants. We may invest in individual residential loans and pools of loans.

|

|

Commercial

|

|

|

Commercial real estate

|

Through our subsidiary ACREG, we originate and acquire commercial real estate debt including commercial mortgage loans, commercial mortgage-backed securities, B-notes, mezzanine loans, preferred equity and other commercial real estate-related debt investments. We also acquire real property for current cash flow, long-term appreciation and earnings growth. In implementing this strategy, we continually evaluate potential acquisition opportunities. These acquisitions may come through joint venture interests or from other equity investments. Although we continuously review our acquisition pipeline, there is not a specific metric that we apply to acquisitions that are under consideration, and our analysis may vary based on property type, transaction structure and other factors.

|

|

Corporate debt

|

Through our subsidiary MML, we invest a small percentage of our assets directly in the ownership of corporate loans and debt securities for middle market companies.

|

| We believe that future interest rates and mortgage prepayment rates are very difficult to predict. |

5

ANNALY CAPITAL MANAGEMENT, INC. AND SUBSIDIARIES

Business

|

Therefore, we seek to acquire assets which we believe will provide attractive returns over a broad range of interest rate and prepayment scenarios.

Our capital structure is designed to offer an efficient complement of funding sources to generate positive risk-adjusted returns for our stockholders while maintaining appropriate liquidity to support our business and meet our financial obligations under periods of market stress. To maintain our desired capital profile, we utilize a mix of debt and equity funding. Debt funding may include the use of repurchase agreements, Federal Home Loan Bank (or FHLB) advances, loans, securitizations, participation sold, lines of credit, asset backed commercial paper conduits, corporate bond issuance, mortgages payable or other liabilities. Equity capital primarily consists of common and preferred stock.

We finance our Agency mortgage-backed securities and residential credit investments primarily with repurchase agreements. We also finance certain commercial real estate investments with repurchase agreements. We enter into repurchase agreements with national broker-dealers, commercial banks and other lenders that typically offer this type of financing. We enter into collateralized borrowings with financial institutions meeting internal credit standards and we monitor the financial condition of these institutions on a regular basis. We seek to diversify our exposure and limit concentrations by entering into repurchase agreements with multiple counterparties. At December 31, 2015, we had $56.2 billion of repurchase agreements outstanding.

Additionally, our wholly owned subsidiary, RCap, provides direct access to bi-lateral and triparty funding as a FINRA member broker-dealer. As an eligible institution, RCap also raises funds through the General Collateral Finance Repo service offered by the Fixed Income Clearing Corporation (or FICC), with FICC acting as the central counterparty. Since its inception in 2008, RCap has provided us greater depth and diversity of repurchase agreement funding while also limiting our counterparty exposure.

Our borrowings pursuant to repurchase transactions include repurchase agreements that have maturities that extend beyond three years. To reduce our liquidity risk we maintain a laddered approach to our repurchase agreements and a conservative weighted average days to maturity. As of December 31, 2015, the weighted average days to maturity was 151 days. |

We maintain access to FHLB funding through our captive insurance subsidiary Truman Insurance Company LLC (or Truman). We finance eligible Agency, residential and commercial investments through the FHLB. While a recent Federal Housing Finance Agency (or FHFA) ruling requires captive insurance companies to terminate their FHLB membership, given the length of its membership Truman has been granted a five year sunset provision whereby its membership is scheduled to expire in February 2021. We believe our business objectives align well with the mission of the FHLB System. While there can be no assurances that such steps will be taken, we believe it would be appropriate for there to be legislative action to permit Truman and similar captive insurance subsidiaries to retain their membership status beyond the current sunset periods.

We utilize diverse funding sources to finance our commercial investments. In addition to FHLB funding, we maintain bilateral borrowing facilities, securitization funding and, in the case of investments in commercial real estate, mortgage financing.

We utilize leverage to enhance the risk-adjusted returns generated for our stockholders. We generally expect to maintain an economic leverage ratio of no greater than 10:1. This ratio varies from time to time based upon various factors, including our management’s opinion of the level of risk of our assets and liabilities, our liquidity position, our level of unused borrowing capacity, the availability of credit, over-collateralization levels required by lenders when we pledge assets to secure borrowings and, lastly, our assessment of domestic and international market conditions. Since the financial crisis beginning in 2007, we have maintained an economic leverage ratio below 8:1, which is generally lower than our leverage ratio had been prior to 2007. For purposes of calculating this ratio, our economic debt is equal to our repurchase agreements, other secured financing, convertible senior notes, securitized debt of consolidated VIEs, loan participation sold, mortgages payable and other forms of financing such as TBA dollar roll transactions (excluding liabilities that are non-recourse to us, subject to customary carveouts) as presented on our Consolidated Statements of Financial Condition.

Our target economic leverage ratio is determined under our capital management policy. Should our actual economic leverage ratio increase above the target level due to asset acquisition or market value fluctuations in assets, we would cease to acquire new assets. Our management would, at that time, present a plan to our Board to return to our target economic leverage ratio.

The following table presents our leverage, economic leverage and capital ratios at December 31, 2015 and 2014.

|

6

ANNALY CAPITAL MANAGEMENT, INC. AND SUBSIDIARIES

Business

|

________________________________

2015 2014

Leverage ratio 5.1:1 5.4:1

Economic leverage ratio 6.0:1 5.4:1

Capital ratio 13.3% 15.1%

Operating Platform

We maintain a flexible and scalable operating platform to support the management and maintenance of our diverse asset portfolio. We have invested in our infrastructure to enhance resiliency, efficiency and leveragability while also ensuring coverage of our target assets. Our information technology applications span the portfolio life-cycle including pre-trade analysis, trade execution and capture, trade settlement and financing, and financial accounting and reporting.

Technology applications also support our control functions including risk, middle and back-office functions. We have added breadth to our operating platform to accommodate diverse asset classes and drive automation based efficiencies. Our business operations include a centralized collateral management function that permits in-house settlement and self-clearing, thereby creating greater control and management of our collateral. Through technology, we have also incorporated exception based processing, critical data assurance and paperless workflows. Our infrastructure investment has driven operating efficiencies while we have expanded the platform.

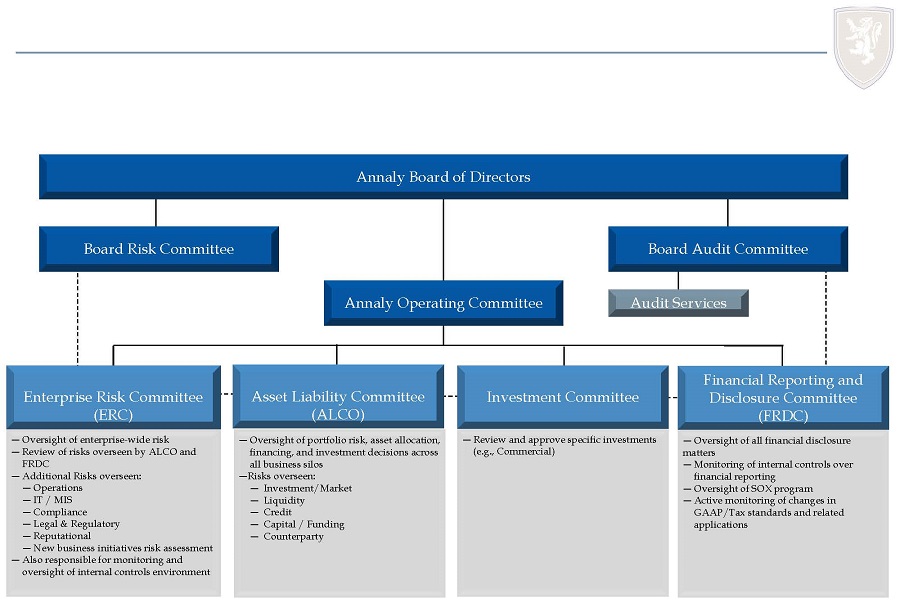

Risk is a natural element of the business and related activities that we conduct. Effective risk management is of critical importance to the success of the firm. The objective of our risk management framework is to measure, monitor and manage the key risks to which we are subject. Our approach to risk management is comprehensive and has been designed to foster a holistic view of risk. For a full discussion of our risk management process and policies please refer to the section titled “Risk Management” of Part II. Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations”.

We have entered into a management agreement with the Manager pursuant to which our management is conducted by the Manager through the authority delegated to it in the Management Agreement and pursuant to the policies established by our Board. The Management Agreement was effective as of July 1, 2013 and applicable for the entire 2013 calendar year and was amended on November 5, 2014 (the management agreement, as amended, is referred to as “Management Agreement”).

|

The Management Agreement provides for a two year term ending December 31, 2016 with automatic two-year renewals unless at least two-thirds of our independent directors or the holders of a majority of our outstanding shares of common stock elect to terminate the agreement in their sole discretion and for any or no reason. At any time during the term or any renewal term we may deliver to the Manager written notice of our intention to terminate the Management Agreement. We must designate a date not less than one year from the date of the notice on which the Management Agreement will terminate. The Management Agreement also provides that the Manager may terminate the Management Agreement by providing to us prior written notice of its intention to terminate the Management Agreement no less than one year prior to the date designated by the Manager on which the Manager would cease to provide services or such earlier date as determined by us in our sole discretion.

Under the Management Agreement, the Manager, subject to the supervision and direction of our Board, is responsible for (i) the selection, purchase and sale of assets for our investment portfolio; (ii) recommending alternative forms of capital raising; (iii) supervising our financing and hedging activities; and (iv) day to day management functions. The Manager also performs such other supervisory and management services and activities relating to our assets and operations as may be appropriate. In exchange for the management services, we pay the Manager a monthly management fee in an amount equal to 1/12th of 1.05% of our stockholders’ equity (as defined in the Management Agreement), and the Manager is responsible for providing personnel to manage us, and paying all compensation and benefit expenses associated with such personnel. All compensation and benefit expenses paid by us to individuals employed by our subsidiaries reduces the management fee. We do not pay the Manager any incentive fees.

The Management Agreement provides that during the term of the Management Agreement and, in the event of termination of this Agreement by the Manager without cause, for a period of one year following such termination, the Manager will not, without our prior written consent, manage any REIT which engages in the management of mortgage-backed securities in any geographical region in which we operate. The Management Agreement may be amended or modified by agreement between us and the Manager. There is no termination fee for a termination of the Management Agreement by either us or the Manager.

|

7

ANNALY CAPITAL MANAGEMENT, INC. AND SUBSIDIARIES

Business

Executive Officers

Our executive officers are provided and compensated by our Manager. The following table sets forth certain information as of February 25, 2016 concerning our executive officers:

|

Name

|

A Age

|

Title

|

|

Kevin G. Keyes

|

48

|

Chief Executive Officer and President

|

|

Wellington J. Denahan

|

52

|

Chairman of the Board and Executive Chairman

|

|

Glenn A. Votek

|

57

|

Chief Financial Officer

|

|

R. Nicholas Singh

|

57

|

Chief Legal Officer and Secretary

|

|

Kevin G. Keyes is Chief Executive Officer and President of Annaly and a member of the Board. Mr. Keyes has served as President of Annaly since October 2012 and as its Chief Executive Officer since September 2015. Mr. Keyes previously served as Chief Strategy Officer and Head of Capital Markets of Annaly, from September 2010 until October 2012. Mr. Keyes joined Annaly as a Managing Director in 2009 and was appointed to the Board in November 2012. Mr. Keyes has over 20 years of Capital Markets and Investment Banking experience. He joined Annaly in 2009 from Bank of America Merrill Lynch where he served in various senior management and business origination roles since 2005. Prior to that, Mr. Keyes also worked at Credit Suisse First Boston from 1997 until 2005 in various capital markets roles and Morgan Stanley Dean Witter from 1990 until 1997 in various investment banking positions. Mr. Keyes has a B.A. in Economics and a B.S. in Business Administration (ALPA Program) from the University of Notre Dame.

Wellington J. Denahan is Chairman of the Board and Executive Chairman of Annaly. Ms. Denahan has served as Chairman of the Board since November 2012 and Executive Chairman of Annaly since September 2015. Previously, Ms. Denahan served as Chief Executive Officer of Annaly from November 2012 to September 2015 and as Co-Chief Executive Officer of Annaly from October 2012 to November 2012. Ms. Denahan was elected in December 1996 to serve as Vice Chairman of the Board. Ms. Denahan was Annaly’s Chief Operating Officer from January 2006 to October 2012 and Chief Investment Officer from 2000 to November 2012. She was a co-founder of Annaly. Ms. Denahan has a B.A. in Finance from Florida State University.

Glenn A. Votek has served as Chief Financial Officer of Annaly since August 2013. Mr. Votek served as Chief Financial Officer of Fixed Income Discount Advisory Company (FIDAC) from August 2013 until October 2015. Mr. Votek joined Annaly in May 2013 from CIT Group where he was an Executive Vice President and Treasurer since 1999 and President of Consumer

|

Finance since 2012. Prior to that, Mr. Votek worked at AT&T and its finance subsidiary from 1986 until 1999 in various financial management roles. Mr. Votek has a B.S. in Finance and Economics from the University of Arizona/Kean College and a M.B.A. in Finance from Rutgers University.

R. Nicholas Singh is Chief Legal Officer and Secretary of Annaly. Mr. Singh joined Annaly in February 2005. Mr. Singh also served as Chief Legal Officer and Secretary of FIDAC from February 2005 until October 2015. From 2001 until he joined Annaly, he was a partner in the law firm of McKee Nelson LLP. Mr. Singh has a B.A. from Carleton College, a M.A. from Columbia University and a J.D. from American University.

Effective July 1, 2013, all of Annaly’s employees were terminated by us and were hired by the Manager. However, a limited number of employees of our subsidiaries remain as employees of our subsidiaries for regulatory or corporate efficiency reasons. As of December 31, 2015, our subsidiaries had eight employees and the Manager had 141 employees. All compensation expenses we incur in connection with the employees of our subsidiaries reduce the management fee. For information about the management, see the discussion in the “Management Agreement” section.

Regulatory Requirements

We have elected, organized and operated in a manner that qualifies us to be taxed as a REIT under the Internal Revenue Code of 1986, as amended and regulations promulgated thereunder (or the Code).

|

8

ANNALY CAPITAL MANAGEMENT, INC. AND SUBSIDIARIES

Business

| If we qualify for taxation as a REIT, we generally will not be subject to federal income tax on our taxable income that is distributed to our stockholders. Furthermore, substantially all of our assets, other than our taxable REIT subsidiaries, consist of qualified REIT real estate assets (of the type described in Section 856(c)(5) of the Code). | we will compete with financial institutions, institutional investors, other lenders, government entities and certain other REITs. For a full discussion of the risks associated with competition see the “Risks Related to Our Investing, Portfolio Management and Financing Activities” section in Item 1A. “Risk Factors.” | ||

|

We regularly monitor our investments and the income from these investments and, to the extent we enter into hedging transactions, we monitor income from our hedging transactions as well, so as to ensure at all times that we maintain our qualification as a REIT and our exemption from registration under the Investment Company Act.

|

Corporate Governance

We strive to conduct our business in accordance with the highest ethical standards and in compliance with applicable governmental laws, rules and regulations. |

||

|

RCap is a member of FINRA and is subject to regulations of the securities business that include but are not limited to trade practices, use and safekeeping of funds and securities, capital structure, recordkeeping and conduct of directors, officers and employees. As a self-clearing, registered broker dealer, RCap is required to maintain minimum net capital by FINRA. RCap consistently operates with capital in excess of its regulatory capital requirements as defined by SEC Rule 15c3-1.

|

●

●

|

Our Board is composed of a majority of independent directors. Our Audit, Compensation, Nominating/Corporate Governance and Risk Committees are compose exclusively of independent directors.

Our independent directors annually select an independent director to serve as lead independent director.

|

|

|

The financial services industry has been the subject of intense regulatory scrutiny in recent years. Financial institutions have been subject to increasing regulation and supervision in the U.S. In particular, the Dodd-Frank Act, which was enacted in July 2010, significantly altered the financial regulatory regime within which financial institutions operate. The implications of the Dodd-Frank Act for our business depend to a large extent on the rules that have been or will be adopted by the Federal Reserve Board, the FDIC, the Securities and Exchange Commission (or SEC), the Commodity and Futures Trading Commission (or CFTC) and other agencies to implement the legislation, as well as the development of market practices and structures under the regime established by the legislation and the implementation of the rules. Other reforms have been adopted or are being considered by other regulators and policy makers worldwide. We will continue to assess our business, risk management, and compliance practices to conform to developments in the regulatory environment.

|

●

●

|

We have adopted a Code of Business Conduct and Ethics, which sets forth the basic principles and guidelines for resolving various legal and ethical questions that may arise in the workplace and in the conduct of our business. This code is applicable to our directors, officers and employees as well as those of our Manager and subsidiaries.

We have adopted Corporate Governance Guidelines which, in conjunction with the charters of our Board committees, provide the framework for the governance of our company.

We have procedures by which any employee, officer or director may raise, on a confidential basis, concerns about our company’s conduct, accounting, internal controls or auditing matters with the lead independent director, the independent directors, or the chair of the Audit Committee or through our company’s whistleblower phone hotline.

|

|

|

Competition

We operate in a highly competitive market for investment opportunities and competition may limit our ability to acquire desirable investments in our target assets and could also affect the pricing of these securities. In acquiring our target assets,

|

● | We have an Insider Trading Policy that prohibits our directors, officers and employees, including employees of our Manager, as well as those of our Manager and subsidiaries from buying or selling our securities on the basis of material nonpublic information and prohibits communicating material nonpublic information about our company to others. | |

9

ANNALY CAPITAL MANAGEMENT, INC. AND SUBSIDIARIES

Business

|

Additionally, our Insider Trading Policy prohibits our directors, officers and employees, including employees of our Manager, from (1) pledging our common or preferred stock as collateral for a loan or (2) engaging in any hedging transactions with respect to our equity securities held by them, which includes the purchase of any financial instrument (including forward contracts and zero cost collars) designed to hedge or offset any decrease in the market value of such equity securities.

Distributions

In accordance with our requirement for maintaining REIT status, we will distribute to stockholders aggregate dividends equaling at least 90% of our REIT taxable income for each taxable year and will endeavor to distribute at least 100% of our REIT taxable income so as not to be subject to tax. Distributions of economic profits from our enterprise could be classified as return of capital due to differences between book and tax accounting rules. We may make additional returns of capital when the potential risk-adjusted returns from new investments fail to exceed our cost of capital. Subject to the limitations of applicable securities and state corporation laws, we can return capital by making purchases of our own capital stock or through payment of dividends.

|

Available Information

Our website is www.annaly.com. We make available on this website under “Investors - SEC Filings,” free of charge, our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports as soon as reasonably practicable after we electronically file or furnish such materials to the SEC.

Also posted on our website, and available in print upon request of any stockholder to our Investor Relations Department, are charters for our Audit Committee, Risk Committee, Compensation Committee, and Nominating/Corporate Governance Committee, our Corporate Governance Guidelines and our Code of Business Conduct and Ethics governing our directors and officers as well as the employees of our subsidiaries and our Manager. Within the time period required by the SEC, we will post on our website any amendment to the Code of Business Conduct and Ethics and any waiver applicable to any executive officer, director or senior financial officer.

Our Investor Relations Department can be contacted at:

Annaly Capital Management, Inc.

1211 Avenue of the Americas

New York, New York 10036

Attn: Investor Relations

Telephone: 888-8ANNALY

E-mail: investor@annaly.com.

The SEC also maintains a website that contains reports, proxy and information statements and other information we file with the SEC at www.sec.gov. Copies of these reports, proxy and information statements and other information may also be obtained, after paying a duplicating fee, by electronic request at publicinfo@sec.gov, or by writing the SEC’s Public Reference Section, 100 F Street, N.E., Washington, D.C. 20549-0102. Information on the operation of the Public Reference Room may be obtained by calling the SEC at 1-800-SEC-0330.

|

10

ANNALY CAPITAL MANAGEMENT, INC. AND SUBSIDIARIES

|

An investment in our stock involves a number of risks. Before making an investment decision, you should carefully consider all of the risks described in this Form 10-K. If any of the risks discussed in this Form 10-K actually occur, our business, financial condition and results of operations could be materially adversely affected.

|

If this were to occur, the trading price of our stock could decline significantly and you may lose all or part of your investment. Readers should not consider any descriptions of these factors to be a complete set of all potential risks that could affect us. |

|

INDEX TO ITEM 1A. RISK FACTORS

|

|

|

Page

|

|

|

Risks Related to Our Investing, Portfolio Management and Financing Activities

|

11

|

|

Risks Related to Our Credit Assets

|

20

|

| Risks Related to Commercial Real Estate Debt, Preferred Equity Investments, Net Lease Real Estate Assets and |

|

| Other Equity Ownership of Real Estate Assets | 24 |

| Risks Related to Our Residential Credit Business | 27 |

|

Risks Related to Our Relationship with Our Manager

|

30

|

|

Risks Related to Our Taxation as a REIT

|

31

|

|

Risks of Ownership of Our Common Stock

|

36

|

|

Regulatory Risks

|

38

|

|

Risks Related to Our Investing, Portfolio Management and Financing Activities

We may change our policies without stockholder approval.

Our Manager is authorized to follow very broad investment guidelines that may be amended from time to time. Our Board and management determine all of our significant policies, including our investment, financing, capital and asset allocation and distribution policies. They may amend or revise these policies at any time without a vote of our stockholders. Policy changes could adversely affect our financial condition, results of operations, the market price of our common stock or our ability to pay dividends or distributions.

Our ongoing investment in new business strategies and new assets is inherently risky, and could disrupt our ongoing businesses.

To date a significant portion of our total assets have consisted of Agency mortgage-backed securities and Agency debentures which carry an implied or actual “AAA” rating. Nevertheless, pursuant to the ongoing diversification of our assets, we acquire assets of lower credit quality.

While we remain committed to the Agency market, given the current environment, we believe it is prudent to diversify a portion of our investment portfolio. We invest in a range of targeted asset classes and continue to explore new business strategies and assets and expect to continue to do so in the future. Additionally, we may enter into or engage in various

|

types of securitizations, transactions, services and other operating businesses that are different than the types we have traditionally entered into or engaged in.

Such endeavors may involve significant risks and uncertainties, including credit risk, diversion of management from current operations, expenses associated with these new investments, inadequate return of capital on our investments, and unidentified issues not discovered in our due diligence of such strategies and assets. Because these new ventures are inherently risky, no assurance can be given that such strategies will be successful and will not materially adversely affect our reputation, financial condition, and operating results.

Our strategy involves the use of leverage, which increases the risk that we may incur substantial losses.

|

11

ANNALY CAPITAL MANAGEMENT, INC. AND SUBSIDIARIES

Item 1A. Risk Factors

|

We expect our leverage to vary with market conditions and our assessment of risk/return on investments. We incur this leverage by borrowing against a substantial portion of the market value of our assets. Leverage, which is fundamental to our investment strategy, creates significant risks.

Because of our leverage, we may incur substantial losses if our borrowing costs increase. Our borrowing costs may increase for any of the following reasons:

● short-term interest rates increase;

● the market value of our investments decreases;

● the "haircut" applied to our assets under the repurchase agreements we are party to

increases;

● interest rate volatility increases;

● interest rate volatility increases;

● the availability of financing in the market decreases; or

● if one or more major market participants fails or otherwise experiences a major liquidity crisis

it could negatively impact the marketability of all fixed income securities, including Agency

and non-Agency mortgage-backed securities, and this could negatively impact the value

of the securities we acquire, thus reducing our net book value

Our leverage may cause margin calls and defaults and force us to sell assets under adverse market conditions.

Because of our leverage, a decline in the value of our interest earning assets may result in our lenders initiating margin calls. A margin call means that the lender requires us to pledge additional collateral to re-establish the ratio of the value of the collateral to the amount of the borrowing. Our fixed-rate mortgage-backed securities generally are more susceptible to margin calls as increases in interest rates tend to more negatively affect the market value of fixed-rate securities.

If we are unable to satisfy margin calls, our lenders may foreclose on our collateral. This could force us to sell our interest earning assets under adverse market conditions. Additionally, in the event of our bankruptcy, our borrowings, which are generally made under repurchase agreements, may qualify for special treatment under the Bankruptcy Code. This special treatment would allow the lenders under these agreements to avoid the automatic stay provisions of the Bankruptcy Code and to liquidate the collateral under these agreements without delay.

We may exceed our target leverage ratios.

|

We generally expect to maintain an economic leverage ratio of less than 10:1. However, we are not required to stay below this economic leverage ratio. We may exceed this ratio by incurring additional debt without increasing the amount of equity we have. For example, if we increase the amount of borrowings under our master repurchase agreements with our existing or new counterparties or the market value of our portfolio holdings declines, our economic leverage ratio would increase. If we increase our economic leverage ratio, the adverse impact on our financial condition and results of operations from the types of risks associated with the use of leverage would likely be more severe.

We may not be able to achieve our optimal leverage.

We use leverage as a strategy to increase the return to our investors. However, we may not be able to achieve our desired leverage for any of the following reasons:

● we determine that the leverage would expose us to excessive risk;

● our lenders do not make funding available to us at acceptable rates; or

● our lenders require that we provide additional collateral to cover our borrowings.

Failure to procure or renew funding on favorable terms, or at all, would adversely affect our results and financial condition.

One or more of our lenders could be unwilling or unable to provide us with financing. This could potentially increase our financing costs and reduce our liquidity. Furthermore, if any of our potential lenders or existing lenders is unwilling or unable to provide us with financing or if we are not able to renew or replace maturing borrowings, we could be forced to sell our assets at an inopportune time when prices are depressed.

Failure to effectively manage our liquidity would adversely affect our results and financial condition.

Our ability to meet cash needs depends on many factors, several of which are beyond our control. Ineffective management of liquidity levels could cause us to be unable to meet certain financial obligations. Potential conditions that could impair our liquidity include: unwillingness or inability of any of our potential lenders to provide us with or renew financing, calls on margin, additional capital requirements, a disruption in the financial markets or declining confidence in our reputation or in financial markets in general. These conditions could force us to sell our assets at inopportune times or otherwise cause us to

|

12

ANNALY CAPITAL MANAGEMENT, INC. AND SUBSIDIARIES

Item 1A. Risk Factors

|

potentially revise our strategic business initiatives.

Purchases and sales of Agency mortgage-backed securities by the Federal Reserve may adversely affect the price and return associated with Agency mortgage-backed securities.

The Federal Reserve owns approximately $1.8 trillion of Agency mortgage-backed securities as of December 31, 2015. The Federal Reserve's current policy is to reinvest principal payments from its holdings of Agency mortgage-backed securities into new Agency mortgage-backed securities purchases. While we cannot predict the impact of this program or any future actions by the Federal Reserve on the prices and liquidity of Agency mortgage-backed securities, we expect that during periods in which the Federal Reserve purchases significant volumes of Agency mortgage-backed securities, yields on Agency mortgage-backed securities may be lower and refinancing volumes may be higher than would have been absent their large scale purchases. As a result, returns on Agency mortgage-backed securities may be adversely affected. There is also a risk that as the Federal Reserve reduces their purchases of Agency mortgage-backed securities or if they decide to sell some or all of their holdings of Agency mortgage-backed securities, the pricing of our Agency mortgage-backed securities portfolio may be adversely affected.

New laws may be passed affecting the relationship between Fannie Mae and Freddie Mac, on the one hand, and the federal government, on the other, which could adversely affect the price of Agency mortgage-backed securities.

The interest and principal payments we expect to receive on the Agency mortgage-backed securities in which we invest will be guaranteed by Fannie Mae, Freddie Mac or Ginnie Mae. Principal and interest payments on Ginnie Mae certificates are directly guaranteed by the U.S. government. Principal and interest payments relating to the securities issued by Fannie Mae and Freddie Mac are only guaranteed by each respective Agency.

In September 2008, Fannie Mae and Freddie Mac were placed into the conservatorship of the FHFA, their federal regulator, pursuant to its powers under The Federal Housing Finance Regulatory Reform Act of 2008, a part of the Housing and Economic Recovery Act of 2008. In addition to FHFA becoming the conservator of Fannie Mae and Freddie Mac, the U.S. Department of the Treasury has taken various actions intended to provide Fannie Mae and Freddie Mac with additional liquidity and ensure their financial stability.

|

Shortly after Fannie Mae and Freddie Mac were placed in federal conservatorship, the Secretary of the U.S. Treasury suggested that the guarantee payment structure of Fannie Mae and Freddie Mac should be re-examined. The future roles of Fannie Mae and Freddie Mac could be significantly reduced and the nature of their guarantees could be eliminated or considerably limited relative to historical measurements. The U.S. Treasury could also stop providing credit support to Fannie Mae and Freddie Mac in the future. Any changes to the nature of the guarantees provided by Fannie Mae and Freddie Mac could redefine what constitutes an Agency mortgage-backed security and could have broad adverse market implications. If Fannie Mae or Freddie Mac was eliminated, or their structures were to change radically, we would not be able to acquire Agency mortgage-backed securities from these entities, which could adversely affect our business operations.

The U.S. Government's efforts to encourage refinancing of certain loans may affect prepayment rates for mortgage loans in mortgage-backed securities.

In addition to the increased pressure upon residential mortgage loan investors and servicers to engage in loss mitigation activities, the U.S. Government has encouraged the refinancing of certain loans, and this action may affect prepayment rates for mortgage loans. To the extent these and other economic stabilization or stimulus efforts are successful in increasing prepayment speeds for residential mortgage loans, such efforts could potentially have a negative impact on our income and operating results, particularly in connection with loans or Agency mortgage-backed securities purchased at a premium or our interest-only securities.

Volatile market conditions for mortgages and mortgage-related assets as well as the broader financial markets can result in a significant contraction in liquidity for mortgages and mortgage-related assets, which may adversely affect the value of the assets in which we invest.

Our results of operations are materially affected by conditions in the markets for mortgages and mortgage-related assets, including Agency mortgage-backed securities, as well as the broader financial markets and the economy generally.

Significant adverse changes in financial market conditions can result in a deleveraging of the global financial system and the forced sale of large quantities of mortgage-related and other financial assets.

|

13

ANNALY CAPITAL MANAGEMENT, INC. AND SUBSIDIARIES

Item 1A. Risk Factors

|

Concerns over economic recession, geopolitical issues, unemployment, the availability and cost of financing, the mortgage market and a declining real estate market may contribute to increased volatility and diminished expectations for the economy and markets.

For example, as a result of the financial market conditions beginning in the summer of 2007, many traditional mortgage investors suffered severe losses in their residential mortgage portfolios and several major market participants failed or have been impaired, resulting in a significant contraction in market liquidity for mortgage-related assets. This illiquidity negatively affected both the terms and availability of financing for all mortgage-related assets. Further increased volatility and deterioration in the markets for mortgages and mortgage-related assets as well as the broader financial markets may adversely affect the performance and market value of our Agency mortgage-backed securities. If these conditions persist, institutions from which we seek financing for our investments may tighten their lending standards or become insolvent, which could make it more difficult for us to obtain financing on favorable terms or at all. Our profitability and financial condition may be adversely affected if we are unable to obtain cost-effective financing for our investments.

We operate in a highly competitive market for investment opportunities and competition may limit our ability to acquire desirable investments in our target assets and could also affect the pricing of these assets.

We operate in a highly competitive market for investment opportunities. Our profitability depends, in large part, on our ability to acquire our target assets at attractive prices. In acquiring our target assets, we will compete with a variety of institutional investors, including other REITs, specialty finance companies, public and private funds, government entities, commercial and investment banks, commercial finance and insurance companies and other financial institutions. Many of our competitors are substantially larger and have considerably greater financial, technical, marketing and other resources than we do. Other REITs with investment objectives that overlap with ours may elect to raise significant amounts of capital, which may create additional competition for investment opportunities. Some competitors may have a lower cost of funds and access to funding sources that may not be available to us, such as funding from the U.S. Government. Many of our competitors are not subject to the operating constraints associated with REIT tax compliance or maintenance of an exemption from the Investment Company Act.

|

In addition, some of our competitors may have higher risk tolerances or different risk assessments, which could allow them to consider a wider variety of investments and establish more relationships than us. Furthermore, competition for investments in our target assets may lead to the price of such assets increasing, which may further limit our ability to generate desired returns. We cannot provide assurance that the competitive pressures we face will not have a material adverse effect on our business, financial condition and results of operations. Also, as a result of this competition, desirable investments in our target assets may be limited in the future and we may not be able to take advantage of attractive investment opportunities from time to time, as we can provide no assurance that we will be able to identify and make investments that are consistent with our investment objectives.

An increase in the interest payments on our borrowings relative to the interest we earn on our interest earning assets may adversely affect our profitability.

We earn money based upon the spread between the interest payments we earn on our interest earning assets and the interest payments we must make on our borrowings. If the interest payments on our borrowings increase relative to the interest we earn on our interest earning assets, our profitability may be adversely affected.

Differences in timing of interest rate adjustments on our interest earning assets and our borrowings may adversely affect our profitability.

We rely primarily on short-term borrowings to acquire interest earning assets with long-term maturities. Some of the interest earning assets we acquire are adjustable-rate interest earning assets. This means that their interest rates may vary over time based upon changes in an objective index, such as:

● LIBOR. The rate banks charge each other for short-term Eurodollar loans.

● Treasury Rate. A monthly or weekly average yield of benchmark U.S. Treasury securities,

as published by the Federal Reserve Board

These indices generally reflect short-term interest rates. The interest rates on our borrowings similarly vary with changes in an objective index. Nevertheless, the interest rates on our borrowings generally adjust more frequently than the interest rates on

|

14

ANNALY CAPITAL MANAGEMENT, INC. AND SUBSIDIARIES

Item 1A. Risk Factors

|

our adjustable-rate interest earning assets, which are also typically subject to periodic and lifetime interest rate caps. Accordingly, in a period of rising interest rates, we could experience a decrease in net income or a net loss because the interest rates on our borrowings adjust faster than the interest rates on our adjustable-rate interest earning assets.

An increase in interest rates may adversely affect the market value of our interest earning assets and, therefore, also our book value.

Increases in interest rates may negatively affect the market value of our interest earning assets because in a period of rising interest rates, the value of certain interest earning assets may fall and reduce our book value. In addition, our fixed-rate interest earning assets are generally more negatively affected by increases in interest rates because in a period of rising rates, the coupon we earn on our fixed-rate interest earning assets would not change. Our book value would be reduced by the amount of decreases in the market value of our interest earning assets.

We may experience declines in the market value of our assets resulting in us recording impairments, which may have an adverse effect on our results of operations and financial condition.

A decline in the market value of our mortgage-backed securities or other assets may require us to recognize an “other-than-temporary” impairment (or OTTI) against such assets under U.S. generally accepted accounting principles (or GAAP). For a discussion of the assessment of OTTI, see the section titled “Significant Accounting Policies” in the Notes to the Consolidated Financial Statements included in Item 15 “Exhibits, Financial Statement Schedules.” The determination as to whether an other-than-temporary impairment exists and, if so, the amount we consider other-than-temporarily impaired is subjective, as such determinations are based on both factual and subjective information available at the time of assessment. As a result, the timing and amount of other-than-temporary impairments constitute material estimates that are susceptible to significant change.

We are subject to reinvestment risk.

We also are subject to reinvestment risk as a result of changes in interest rates. Declines in interest rates are generally accompanied by increased prepayments of mortgage loans, which in turn results in a prepayment of the related mortgage-backed securities. An increase in prepayments could result in the reinvestment of the proceeds we receive from such prepayments into lower yielding assets. |

An increase in prepayment rates may adversely affect our profitability.

The mortgage-backed securities we acquire are backed by pools of mortgage loans. We receive payments, generally, from the payments that are made on these underlying mortgage loans. We often purchase mortgage-backed securities that have a higher coupon rate than the prevailing market interest rates. In exchange for a higher coupon rate, we typically pay a premium over par value to acquire these mortgage-backed securities. In accordance with GAAP, we amortize the premiums on our mortgage-backed securities over the life of the related mortgage-backed securities. If the mortgage loans securing these mortgage-backed securities prepay at a more rapid rate than anticipated, we will have to amortize our premiums on an accelerated basis that may adversely affect our profitability. Defaults on mortgage loans underlying Agency mortgage-backed securities typically have the same effect as prepayments because of the underlying Agency guarantee.

Prepayment rates generally increase when interest rates fall and decrease when interest rates rise, but changes in prepayment rates are difficult to predict. Prepayment rates also may be affected by conditions in the housing and financial markets, general economic conditions and the relative interest rates on fixed-rate and adjustable-rate mortgage loans.

While we seek to minimize prepayment risk to the extent practical, in selecting investments we must balance prepayment risk against other risks and the potential returns of each investment. No strategy can completely insulate us from prepayment risk.

The viability of other financial institutions could adversely affect us.

Financial services institutions are interrelated as a result of trading, clearing, counterparty, borrowing, or other relationships. We have exposure to many different counterparties, and routinely execute transactions with counterparties in the financial services industry, including brokers and dealers, commercial banks, investment banks, mutual and hedge funds, and other institutional clients. Many of these transactions expose us to credit risk in the event of default of our counterparty or, in certain instances, our counterparty’s customers. There is no assurance that any such losses would not materially and adversely impact our revenues, financial condition and earnings.

|

15

ANNALY CAPITAL MANAGEMENT, INC. AND SUBSIDIARIES

Item 1A. Risk Factors

|

Our hedging strategies may be costly, and may not hedge our risks as intended.

Our policies permit us to enter into interest rate swaps, caps and floors, interest rate swaptions, Treasury futures and other derivative transactions to help us mitigate our interest rate and prepayment risks described above. We have used interest rate swaps and options to enter into interest rate swaps (commonly referred to as interest rate swaptions) to provide a level of protection against interest rate risks. We may also purchase or sell to-be-announced forward contracts on Agency mortgage-backed securities (commonly referred to as TBAs) purchase or write put or call options on TBA securities and invest in other types of mortgage derivatives, such as interest-only securities. No hedging strategy can protect us completely. Entering into interest rate hedging may fail to protect or could adversely affect us because, among other things: interest rate hedging can be expensive, particularly during periods of volatile interest rates; available hedges may not correspond directly with the risk for which protection is sought; and the duration of the hedge may not match the duration of the related asset or liability.

Our use of derivatives may expose us to counterparty and liquidity risks.

The CFTC has issued and continues to issue new rules regarding swaps and swaptions, under the authority granted to it pursuant to the Dodd-Frank Wall Street Reform and Consumer Protection Act, or Dodd-Frank. These new rules change, but do not eliminate, the risks we face in our hedging activities.

Most swaps that we enter into must be cleared by a Derivatives Clearing Organization (or DCO). DCOs are subject to regulatory oversight, use extensive risk management processes, and might receive “too big to fail” support from the government in the case of insolvency. We access the DCO through several Futures Commission Merchants (or FCMs). For any cleared swap, we bear the credit risk of both the DCO and the relevant FCM, in the form of potential late or unrecoverable payments, potential difficulty or delay in accessing collateral that we have posted, and potential loss of any positive market value of the swap position. In the event of a default by the DCO or FCM, we also bear market risk, because the asset being hedged is no longer effectively hedged.

Most swaps must be cleared through a DCO. Most swaps must be or are traded on a Swap Execution Facility. We bear additional fees for use of the DCO.

|

We also bear fees for use of the Swap Execution Facility, and bear increased risk of trade errors. Because the standardized swaps available on Swap Execution Facilities and cleared through DCOs are not as customizable as the swaps available before the implementation of Dodd-Frank, we may bear additional basis risk from hedge positions that do not exactly reflect the interest rate risk on the asset being hedged.

Futures transactions are subject to risks analogous to those of cleared swaps, except that for futures transactions we bear a higher risk that collateral we have posted is unavailable to us if the FCM defaults.

Some derivatives transactions, such as swaptions, are not currently required to be cleared through a DCO. Therefore, we bear the credit risk of the dealer with which we executed the swaption. TBA contracts are also not cleared, and we bear the credit risk of the dealer.

Derivative transactions are subject to margin requirements. The relevant contract or clearinghouse rules dictate the method of determining the required amount of margin, the types of collateral accepted, and the timing required to meet margin calls. Additionally, for cleared swaps and futures, FCMs may have the right to require more margin than the clearinghouse requires. The requirement to meet margin calls can create liquidity risks, and we bear the cost of funding the margin that we post. Also, as discussed above, we bear credit risk if a dealer, FCM, or clearinghouse is holding collateral we have posted.

Generally, we attempt to retain the ability to close out of a hedging position or create an offsetting position. However, in some cases we may not be able to do so at economically viable prices, or we may be unable to do so without consent of the counterparty. Therefore, in some situations a derivative position can be illiquid, forcing us to hold it to its maturity or scheduled termination date.

Regulations relating to derivatives continue to be issued and come into effect. Ongoing regulatory change in this area could increase costs, increase risks, and adversely affect our business and results of operations.

We use analytical models and data in connection with the valuation of our assets, and any incorrect, misleading or incomplete information used in connection therewith would subject us to potential risks.

|

16

ANNALY CAPITAL MANAGEMENT, INC. AND SUBSIDIARIES

Item 1A. Risk Factors

|

Given our strategies and the complexity of the valuation of our assets, we must rely heavily on analytical models (both proprietary models developed by us and those supplied by third parties) and information and data supplied by our third party vendors and servicers. Models and data are used to value assets or potential asset purchases and also in connection with hedging our assets. When models and data prove to be incorrect, misleading or incomplete, any decisions made in reliance thereon expose us to potential risks. For example, by relying on models and data, especially valuation models, we may be induced to buy certain assets at prices that are too high, to sell certain other assets at prices that are too low or to miss favorable opportunities altogether. Similarly, any hedging based on faulty models and data may prove to be unsuccessful. Furthermore, despite our valuation validation processes our models may nevertheless prove to be incorrect.

Some of the risks of relying on analytical models and third-party data are particular to analyzing tranches from securitizations, such as commercial or residential mortgage-backed securities. These risks include, but are not limited to, the following: (i) collateral cash flows and/or liability structures may be incorrectly modeled in all or only certain scenarios, or may be modeled based on simplifying assumptions that lead to errors; (ii) information about collateral may be incorrect, incomplete, or misleading; (iii) collateral or bond historical performance (such as historical prepayments, defaults, cash flows, etc.) may be incorrectly reported, or subject to interpretation (e.g., different issuers may report delinquency statistics based on different definitions of what constitutes a delinquent loan); or (iv) collateral or bond information may be outdated, in which case the models may contain incorrect assumptions as to what has occurred since the date information was last updated.

Some of the analytical models used by us, such as mortgage prepayment models or mortgage default models, are predictive in nature. The use of predictive models has inherent risks. For example, such models may incorrectly forecast future behavior, leading to potential losses on a cash flow and/or a mark-to-market basis. In addition, the predictive models used by us may differ substantially from those models used by other market participants, with the result that valuations based on these predictive models may be substantially higher or lower for certain assets than actual market prices. Furthermore, since predictive models are usually constructed based on historical data supplied by third parties, the success of relying on such models may depend heavily on the accuracy and reliability of the supplied historical data and the ability of these historical models to accurately reflect future periods.

|

All valuation models rely on correct market data inputs. If incorrect market data is entered into even a well-founded valuation model, the resulting valuations will be incorrect. However, even if market data is inputted correctly, “model prices” will often differ substantially from market prices, especially for securities with complex characteristics, such as derivative instruments or structured notes.

Accounting rules related to certain of our transactions are highly complex and involve significant judgment and assumptions, and changes in accounting treatment may adversely affect our profitability and impact our financial results.

Accounting rules for valuations of financial instruments, mortgage loan sales and securitizations, investment consolidations, acquisitions of real estate and other aspects of our anticipated operations are highly complex and involve significant judgment and assumptions. These complexities could lead to a delay in preparation of financial information and the delivery of this information to our stockholders. Changes in accounting interpretations or assumptions could impact our financial statements and our ability to prepare our financial statements in a timely fashion. Our inability to prepare our financial statements in a timely fashion in the future would likely adversely affect our share price significantly.

The fair value at which our assets may be recorded may not be an indication of their realizable value. Ultimate realization of the value of an asset depends to a great extent on economic and other conditions. Further, fair value is only an estimate based on good faith judgment of the price at which an investment can be sold since market prices of investments can only be determined by negotiation between a willing buyer and seller. If we were to liquidate a particular asset, the realized value may be more than or less than the amount at which such asset is valued. Accordingly, the value of our common shares could be adversely affected by our determinations regarding the fair value of our investments, whether in the applicable period or in the future. Additionally, such valuations may fluctuate over short periods of time.

We are highly dependent on information systems and third parties, and systems failures could significantly disrupt our business, which may, in turn, negatively affect the market price of our common stock and our ability to pay dividends to our stockholders.

Our business is highly dependent on communications and information systems. Any failure or interruption of our systems or cyber-attacks or security breaches of our networks or systems could cause delays or other problems in our securities trading

|

17

ANNALY CAPITAL MANAGEMENT, INC. AND SUBSIDIARIES

Item 1A. Risk Factors

|

activities, including mortgage-backed securities trading activities, which could have a material adverse effect on our operating results and negatively affect the market price of our common stock and our ability to pay dividends to our stockholders. In addition, we also face the risk of operational failure, termination or capacity constraints of any of the third parties with which we do business or that facilitate our business activities, including clearing agents or other financial intermediaries we use to facilitate our securities transactions, if their respective systems experience failure, interruption, cyber-attacks, or security breaches.