false2021FY0001043186http://www.stabilisenergy.com/20211231#OperatingLeaseRightOfUseAssetAndOtherAssetsNoncurrenthttp://www.stabilisenergy.com/20211231#OperatingLeaseRightOfUseAssetAndOtherAssetsNoncurrenthttp://fasb.org/us-gaap/2021-01-31#PropertyPlantAndEquipmentAndFinanceLeaseRightOfUseAssetAfterAccumulatedDepreciationAndAmortizationhttp://fasb.org/us-gaap/2021-01-31#PropertyPlantAndEquipmentAndFinanceLeaseRightOfUseAssetAfterAccumulatedDepreciationAndAmortization00010431862021-01-012021-12-3100010431862021-06-30iso4217:USD00010431862022-03-09xbrli:shares00010431862021-12-3100010431862020-12-31iso4217:USDxbrli:shares0001043186us-gaap:NaturalGasGatheringTransportationMarketingAndProcessingMember2021-01-012021-12-310001043186us-gaap:NaturalGasGatheringTransportationMarketingAndProcessingMember2020-01-012020-12-310001043186slng:RentalServiceAndOtherMember2021-01-012021-12-310001043186slng:RentalServiceAndOtherMember2020-01-012020-12-310001043186slng:PowerDeliveryMember2021-01-012021-12-310001043186slng:PowerDeliveryMember2020-01-012020-12-3100010431862020-01-012020-12-310001043186us-gaap:CommonStockMember2019-12-310001043186us-gaap:AdditionalPaidInCapitalMember2019-12-310001043186us-gaap:AccumulatedOtherComprehensiveIncomeMember2019-12-310001043186us-gaap:RetainedEarningsMember2019-12-3100010431862019-12-310001043186us-gaap:CommonStockMember2020-01-012020-12-310001043186us-gaap:AdditionalPaidInCapitalMember2020-01-012020-12-310001043186us-gaap:RetainedEarningsMember2020-01-012020-12-310001043186us-gaap:AccumulatedOtherComprehensiveIncomeMember2020-01-012020-12-310001043186us-gaap:CommonStockMember2020-12-310001043186us-gaap:AdditionalPaidInCapitalMember2020-12-310001043186us-gaap:AccumulatedOtherComprehensiveIncomeMember2020-12-310001043186us-gaap:RetainedEarningsMember2020-12-310001043186us-gaap:CommonStockMember2021-01-012021-12-310001043186us-gaap:AdditionalPaidInCapitalMember2021-01-012021-12-310001043186us-gaap:RetainedEarningsMember2021-01-012021-12-310001043186us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-01-012021-12-310001043186us-gaap:CommonStockMember2021-12-310001043186us-gaap:AdditionalPaidInCapitalMember2021-12-310001043186us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-12-310001043186us-gaap:RetainedEarningsMember2021-12-310001043186slng:BomayMember2021-12-31xbrli:pure0001043186slng:StabilisEnergyLLCMemberslng:AmericanElectricTechnologiesIncMemberslng:ShareExchangeAgreementMember2019-07-262019-07-260001043186slng:AmericanElectricTechnologiesIncMemberslng:PegPartnersLlcMemberslng:ShareExchangeAgreementMember2019-07-262019-07-260001043186slng:AEGISNGLLCMemberslng:PegPartnersLlcMemberslng:ShareExchangeAgreementMember2019-07-260001043186slng:StabilisEnergyLLCMemberslng:PegPartnersLlcMemberslng:ShareExchangeAgreementMember2019-07-262019-07-260001043186slng:AmericanElectricTechnologiesIncMemberslng:StabilisEnergyLLCMemberslng:ShareExchangeAgreementMember2019-07-262019-07-260001043186slng:PrometheusEnergyGroupIncoporatedMemberslng:AmericanElectricTechnologiesIncMemberslng:ShareExchangeAgreementMember2019-07-262019-07-260001043186slng:StabilisEnergyLLCMemberslng:ShareExchangeAgreementMember2019-07-262019-07-260001043186slng:AmericanElectricTechnologiesIncMemberslng:ShareExchangeAgreementMember2019-07-262019-07-260001043186srt:BoardOfDirectorsChairmanMemberslng:ShareExchangeAgreementMember2019-07-262019-07-260001043186slng:AmeriStateBankMemberslng:LoanAgreementMember2021-04-080001043186slng:AmeriStateBankMemberslng:LoanAgreementMember2021-04-082021-04-080001043186us-gaap:CustomerConcentrationRiskMember2021-01-012021-12-310001043186slng:ProductContractsMember2021-01-012021-12-310001043186slng:RentalContractsMember2021-01-012021-12-310001043186slng:ServiceContractsMember2021-01-012021-12-310001043186slng:LNGSegmentMember2021-01-012021-12-310001043186slng:RentalServiceMember2021-01-012021-12-310001043186slng:RentalServiceMember2020-01-012020-12-310001043186us-gaap:ServiceMember2021-01-012021-12-310001043186us-gaap:ServiceMember2020-01-012020-12-310001043186us-gaap:ProductAndServiceOtherMember2021-01-012021-12-310001043186us-gaap:ProductAndServiceOtherMember2020-01-012020-12-31slng:segment0001043186slng:PowerDeliverySegmentMember2021-01-012021-12-310001043186slng:LNGSegmentMember2021-12-310001043186slng:PowerDeliverySegmentMember2021-12-310001043186slng:LNGSegmentMember2020-01-012020-12-310001043186slng:PowerDeliverySegmentMember2020-01-012020-12-310001043186slng:LNGSegmentMember2020-12-310001043186slng:PowerDeliverySegmentMember2020-12-310001043186country:BR2021-01-012021-12-310001043186country:BR2020-01-012020-12-310001043186country:MX2021-01-012021-12-310001043186country:MX2020-01-012020-12-310001043186country:US2021-01-012021-12-310001043186country:US2020-01-012020-12-310001043186country:BR2021-12-310001043186country:BR2020-12-310001043186country:CN2021-12-310001043186country:CN2020-12-310001043186country:MX2021-12-310001043186country:MX2020-12-310001043186country:US2021-12-310001043186country:US2020-12-310001043186slng:LNGSegmentMemberslng:Customer1Memberus-gaap:CustomerConcentrationRiskMemberus-gaap:RevenueFromContractWithCustomerMember2021-01-012021-12-310001043186slng:LNGSegmentMemberslng:Customer1Memberus-gaap:CustomerConcentrationRiskMemberus-gaap:RevenueFromContractWithCustomerMember2020-01-012020-12-310001043186slng:LNGSegmentMemberus-gaap:CustomerConcentrationRiskMemberus-gaap:RevenueFromContractWithCustomerMemberslng:Customer2Member2021-01-012021-12-310001043186slng:LNGSegmentMemberus-gaap:CustomerConcentrationRiskMemberus-gaap:RevenueFromContractWithCustomerMemberslng:Customer2Member2020-01-012020-12-310001043186slng:LNGSegmentMemberslng:Customer3Memberus-gaap:CustomerConcentrationRiskMemberus-gaap:RevenueFromContractWithCustomerMember2021-01-012021-12-310001043186slng:LNGSegmentMemberslng:Customer3Memberus-gaap:CustomerConcentrationRiskMemberus-gaap:RevenueFromContractWithCustomerMember2020-01-012020-12-310001043186us-gaap:CustomerConcentrationRiskMemberus-gaap:RevenueFromContractWithCustomerMember2021-01-012021-12-310001043186us-gaap:CustomerConcentrationRiskMemberus-gaap:RevenueFromContractWithCustomerMemberslng:Customer12And3Member2021-01-012021-12-310001043186us-gaap:CustomerConcentrationRiskMemberus-gaap:RevenueFromContractWithCustomerMember2020-01-012020-12-310001043186us-gaap:CustomerConcentrationRiskMemberus-gaap:RevenueFromContractWithCustomerMemberslng:Customer12And3Member2020-01-012020-12-310001043186slng:LNGSegmentMemberslng:Customer1Memberus-gaap:CustomerConcentrationRiskMemberus-gaap:AccountsReceivableMember2021-01-012021-12-310001043186slng:LNGSegmentMemberslng:Customer1Memberus-gaap:CustomerConcentrationRiskMemberus-gaap:AccountsReceivableMember2020-01-012020-12-310001043186slng:LNGSegmentMemberus-gaap:CustomerConcentrationRiskMemberus-gaap:AccountsReceivableMemberslng:Customer2Member2021-01-012021-12-310001043186slng:LNGSegmentMemberus-gaap:CustomerConcentrationRiskMemberus-gaap:AccountsReceivableMemberslng:Customer2Member2020-01-012020-12-310001043186slng:LNGSegmentMemberslng:Customer3Memberus-gaap:CustomerConcentrationRiskMemberus-gaap:AccountsReceivableMember2021-01-012021-12-310001043186slng:LNGSegmentMemberslng:Customer3Memberus-gaap:CustomerConcentrationRiskMemberus-gaap:AccountsReceivableMember2020-01-012020-12-310001043186us-gaap:CustomerConcentrationRiskMemberus-gaap:AccountsReceivableMember2021-01-012021-12-310001043186us-gaap:CustomerConcentrationRiskMemberus-gaap:AccountsReceivableMemberslng:Customer12And3Member2021-01-012021-12-310001043186us-gaap:CustomerConcentrationRiskMemberus-gaap:AccountsReceivableMember2020-01-012020-12-310001043186us-gaap:CustomerConcentrationRiskMemberus-gaap:AccountsReceivableMemberslng:Customer12And3Member2020-01-012020-12-310001043186srt:MinimumMemberslng:LiquefactionPlantsAndSystemsMember2021-01-012021-12-310001043186slng:LiquefactionPlantsAndSystemsMembersrt:MaximumMember2021-01-012021-12-310001043186slng:LiquefactionPlantsAndSystemsMember2021-12-310001043186slng:LiquefactionPlantsAndSystemsMember2020-12-310001043186srt:MinimumMemberslng:RealEstateandBuildingsMember2021-01-012021-12-310001043186slng:RealEstateandBuildingsMembersrt:MaximumMember2021-01-012021-12-310001043186slng:RealEstateandBuildingsMember2021-12-310001043186slng:RealEstateandBuildingsMember2020-12-310001043186srt:MinimumMemberus-gaap:VehiclesMember2021-01-012021-12-310001043186us-gaap:VehiclesMembersrt:MaximumMember2021-01-012021-12-310001043186us-gaap:VehiclesMember2021-12-310001043186us-gaap:VehiclesMember2020-12-310001043186srt:MinimumMemberslng:ComputerandOfficeEquipmentMember2021-01-012021-12-310001043186slng:ComputerandOfficeEquipmentMembersrt:MaximumMember2021-01-012021-12-310001043186slng:ComputerandOfficeEquipmentMember2021-12-310001043186slng:ComputerandOfficeEquipmentMember2020-12-310001043186us-gaap:ConstructionInProgressMember2021-12-310001043186us-gaap:ConstructionInProgressMember2020-12-310001043186us-gaap:LeaseholdImprovementsMember2021-12-310001043186us-gaap:LeaseholdImprovementsMember2020-12-3100010431862021-06-012021-06-010001043186slng:BaojiOilfieldMachineryCoLtdMemberslng:BomayMember2021-12-310001043186slng:AAEnergiesIncMemberslng:BomayMember2021-12-310001043186srt:AffiliatedEntityMember2020-01-012020-12-310001043186srt:AffiliatedEntityMember2021-01-012021-12-310001043186slng:BomayMemberus-gaap:EquityMethodInvestmentNonconsolidatedInvesteeOrGroupOfInvesteesMember2021-01-012021-12-310001043186slng:BomayMemberus-gaap:EquityMethodInvestmentNonconsolidatedInvesteeOrGroupOfInvesteesMember2020-01-012020-12-310001043186slng:BomayMemberus-gaap:EquityMethodInvestmentNonconsolidatedInvesteeOrGroupOfInvesteesMember2021-12-310001043186slng:BomayMemberus-gaap:EquityMethodInvestmentNonconsolidatedInvesteeOrGroupOfInvesteesMember2020-12-310001043186slng:BomayMember2020-12-310001043186slng:BomayMember2019-12-310001043186slng:BomayMember2021-01-012021-12-310001043186slng:BomayMember2020-01-012020-12-310001043186slng:EnergiaSuperiorGasNaturalLLCMember2019-08-200001043186us-gaap:NotesPayableToBanksMemberslng:CadenceBankNAMemberslng:LoanPursuantToCARESActMember2020-12-3100010431862021-06-012021-06-300001043186us-gaap:PrimeRateMemberslng:AmeriStateBankMemberslng:LoanAgreementMember2021-04-082021-04-080001043186srt:AffiliatedEntityMemberslng:ChartEnergyChemicalsIncMember2021-12-310001043186slng:SeniorSecuredTermNoteMemberMemberus-gaap:LondonInterbankOfferedRateLIBORMember2021-12-310001043186slng:SeniorSecuredTermNoteMemberMember2021-01-012021-12-310001043186us-gaap:SecuredDebtMemberslng:MGFinanceCo.Ltd.Memberslng:SecuredPromissoryNoteMember2019-08-160001043186slng:ToDecember102020Memberus-gaap:SecuredDebtMemberslng:MGFinanceCo.Ltd.Memberslng:SecuredPromissoryNoteMember2019-08-160001043186us-gaap:SecuredDebtMemberslng:December112020andThereafterMemberslng:MGFinanceCo.Ltd.Memberslng:SecuredPromissoryNoteMember2019-08-160001043186us-gaap:SubsequentEventMemberus-gaap:SecuredDebtMembersrt:MaximumMemberslng:MGFinanceCo.Ltd.Memberslng:SecuredPromissoryNoteMember2022-03-090001043186us-gaap:SubsequentEventMembersrt:MinimumMemberus-gaap:SecuredDebtMemberslng:MGFinanceCo.Ltd.Memberslng:SecuredPromissoryNoteMember2022-03-090001043186us-gaap:SubsequentEventMemberus-gaap:SecuredDebtMemberslng:MGFinanceCo.Ltd.Memberslng:SecuredPromissoryNoteMember2022-03-090001043186srt:MinimumMember2021-01-012021-12-310001043186srt:MaximumMember2021-01-012021-12-310001043186slng:InsuranceNotesPayable2021To2022Member2021-01-012021-12-310001043186slng:InsuranceNotesPayable2020To2021Member2021-01-012021-12-310001043186slng:FormerExecutiveChairmanofBoardofDirectorsofAmericanElectricTechnologiesIncMemberslng:SeniorSecuredTermNoteMemberslng:LoanAgreementMemberslng:MandIElectricBrazilSistemaseServiciosemEnergiaLTDAMember2019-07-2600010431862020-04-072020-04-070001043186slng:BrazilianInterbankMember2021-12-310001043186srt:MinimumMemberslng:BrazilianInterbankMember2021-12-310001043186srt:MaximumMemberslng:BrazilianInterbankMember2021-12-310001043186slng:UnsecuredPromissoryNoteMember2021-01-012021-12-310001043186slng:UnsecuredPromissoryNoteMember2020-01-012020-12-310001043186slng:SecuredTermNoteMember2021-01-012021-12-310001043186slng:SecuredTermNoteMember2020-01-012020-12-310001043186slng:SeniorSecuredTermNoteMember2021-01-012021-12-310001043186slng:SeniorSecuredTermNoteMember2020-01-012020-12-310001043186slng:SecuredPromissoryNoteMember2021-01-012021-12-310001043186slng:SecuredPromissoryNoteMember2020-01-012020-12-310001043186slng:InsuranceandOtherNotesPayableMember2021-01-012021-12-310001043186slng:InsuranceandOtherNotesPayableMember2020-01-012020-12-3100010431862021-07-3000010431862021-07-302021-07-3000010431862021-11-012021-11-3000010431862021-11-3000010431862021-01-25slng:lease00010431862021-01-252021-01-250001043186us-gaap:CostOfSalesMember2021-01-012021-12-310001043186us-gaap:CostOfSalesMember2020-01-012020-12-310001043186us-gaap:SellingGeneralAndAdministrativeExpensesMember2021-01-012021-12-310001043186us-gaap:SellingGeneralAndAdministrativeExpensesMember2020-01-012020-12-310001043186slng:DenverColoradoMember2021-01-012021-12-310001043186slng:DenverColoradoMember2020-01-012020-12-310001043186slng:LiquefactionPlantsAndSystemsMember2021-12-012021-12-310001043186slng:MandIElectricBrazilSistemaseServiciosemEnergiaLTDAMember2021-01-012021-12-31slng:City0001043186slng:MrAivalisAndEnatekServicesLLCMember2021-10-252021-10-250001043186srt:AffiliatedEntityMemberus-gaap:EquipmentMemberslng:TmgMember2019-12-010001043186srt:AffiliatedEntityMemberslng:TmgMember2019-12-012019-12-010001043186srt:AffiliatedEntityMemberslng:TmgMember2019-12-010001043186slng:TmgMembersrt:AffiliatedEntityMembersrt:BoardOfDirectorsChairmanMember2019-12-012019-12-010001043186slng:StabilisEnergyLLCMembersrt:SubsidiariesMember2018-12-310001043186slng:StabilisEnergyLLCMembersrt:SubsidiariesMember2018-01-012018-12-310001043186slng:SeniorSecuredTermNoteMemberus-gaap:LondonInterbankOfferedRateLIBORMember2021-09-300001043186slng:MGFinanceCo.Ltd.Memberslng:SecuredPromissoryNoteMember2019-08-160001043186us-gaap:BuildingMember2020-01-012020-12-310001043186slng:AppliedCryoTechnologiesMembersrt:AffiliatedEntityMember2021-12-310001043186slng:AppliedCryoTechnologiesMembersrt:AffiliatedEntityMember2021-01-012021-12-310001043186slng:AppliedCryoTechnologiesMembersrt:AffiliatedEntityMember2020-01-012020-12-310001043186slng:AppliedCryoTechnologiesMembersrt:AffiliatedEntityMember2020-12-310001043186srt:AffiliatedEntityMemberslng:TmgMember2021-01-012021-12-310001043186srt:AffiliatedEntityMemberslng:TmgMember2020-01-012020-12-310001043186srt:AffiliatedEntityMemberslng:TmgMember2021-12-310001043186srt:AffiliatedEntityMemberslng:TmgMember2020-12-310001043186srt:AffiliatedEntityMember2021-12-310001043186srt:AffiliatedEntityMember2020-12-310001043186slng:PriorToDecember312017Member2021-12-3100010431862018-10-012018-10-3100010431862020-02-012020-02-2900010431862020-04-012020-04-3000010431862021-05-012021-05-310001043186us-gaap:SeriesAPreferredStockMember2019-07-260001043186us-gaap:SeriesAPreferredStockMember2021-12-310001043186slng:A2019LongTermIncentivePlanMember2021-07-310001043186slng:AmendedAndRestated2019LongTermIncentivePlanMember2021-07-310001043186slng:ParticipantMember2021-07-012021-07-310001043186slng:NonEmployeeBoardMemberMember2021-07-012021-07-310001043186us-gaap:RestrictedStockMember2021-01-012021-12-310001043186us-gaap:RestrictedStockMemberus-gaap:GeneralAndAdministrativeExpenseMember2021-01-012021-12-310001043186us-gaap:RestrictedStockMemberus-gaap:GeneralAndAdministrativeExpenseMember2020-01-012020-12-310001043186slng:A2019LongTermIncentivePlanMemberus-gaap:RestrictedStockUnitsRSUMemberslng:FormerChiefExecutiveOfficerMember2021-08-222021-08-220001043186us-gaap:RestrictedStockUnitsRSUMembersrt:ChiefExecutiveOfficerMember2021-08-232021-08-230001043186us-gaap:ShareBasedCompensationAwardTrancheOneMemberslng:August232022Memberus-gaap:RestrictedStockUnitsRSUMember2021-08-222021-08-220001043186us-gaap:ShareBasedCompensationAwardTrancheTwoMemberslng:August232023Memberus-gaap:RestrictedStockUnitsRSUMember2021-08-222021-08-220001043186us-gaap:RestrictedStockUnitsRSUMembersrt:ChiefExecutiveOfficerMember2021-08-23slng:tranche0001043186us-gaap:RestrictedStockUnitsRSUMember2021-01-012021-12-310001043186us-gaap:RestrictedStockUnitsRSUMember2020-01-012020-12-310001043186slng:RestrictedStockAwardsAndRestrictedStockUnitsMember2019-12-310001043186slng:RestrictedStockAwardsAndRestrictedStockUnitsMember2020-01-012020-12-310001043186slng:RestrictedStockAwardsAndRestrictedStockUnitsMember2020-12-310001043186slng:RestrictedStockAwardsAndRestrictedStockUnitsMember2021-01-012021-12-310001043186slng:RestrictedStockAwardsAndRestrictedStockUnitsMember2021-12-310001043186us-gaap:RestrictedStockUnitsRSUMember2021-08-232021-08-230001043186us-gaap:RestrictedStockUnitsRSUMembersrt:ChiefExecutiveOfficerMember2021-01-012021-12-310001043186slng:OtherEmployeesMemberus-gaap:RestrictedStockUnitsRSUMember2021-01-012021-12-310001043186us-gaap:RestrictedStockUnitsRSUMember2021-12-310001043186srt:ChiefExecutiveOfficerMember2021-08-232021-08-230001043186us-gaap:ShareBasedCompensationAwardTrancheOneMembersrt:ChiefExecutiveOfficerMemberslng:August232022Member2021-08-230001043186us-gaap:ShareBasedCompensationAwardTrancheTwoMemberslng:August232023Memberus-gaap:RestrictedStockUnitsRSUMember2021-08-230001043186slng:August232024Memberus-gaap:ShareBasedCompensationAwardTrancheThreeMemberus-gaap:RestrictedStockUnitsRSUMember2021-08-230001043186slng:BlackScholesValuationModelMember2021-08-232021-08-230001043186slng:BlackScholesValuationModelMember2021-08-230001043186slng:BlackScholesValuationModelMember2021-01-012021-12-3100010431862021-08-232021-08-230001043186slng:WarrantNovember132022ExpirationMember2021-12-31

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

______________________________

FORM 10-K

________________________

| | | | | |

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Fiscal Year Ended December 31, 2021

or

| | | | | |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 001-40364

_____________________________

STABILIS SOLUTIONS, INC.

(Exact name of registrant as specified in its charter)

_____________________________

| | | | | |

| Florida | 59-3410234 |

(State or other jurisdiction

of incorporation or organization) | (I.R.S. Employer

Identification No.) |

11750 Katy Freeway, Suite 900, Houston, TX 77079

(Address of principal executive offices, including zip code)

(832) 456-6500

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | |

| Title of each class | Trading Symbol | Name of each exchange on which registered |

| Common Stock, $.001 par value | SLNG | The Nasdaq Stock Market LLC |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§. 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Act:

| | | | | | | | | | | | | | | | | | | | |

| Large accelerated filer | | ☐ | | Accelerated filer | | ☐ |

| Non-accelerated filer | | ☒ | | Smaller reporting company | | ☒ |

| | | | Emerging growth company | | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The aggregate market value of the registrant’s common stock held by non-affiliates of the registrant on June 30, 2021 was $43,832,775 based on the closing sale price, as reported by The Nasdaq Stock Market LLC.

As of March 9, 2022, there were 17,691,268 outstanding shares of our common stock, par value $.001 per share.

Documents Incorporated by Reference: None

STABILIS SOLUTIONS, INC. AND SUBSIDIARIES

ANNUAL REPORT ON FORM 10-K

For the Fiscal Year Ended December 31, 2021

TABLE OF CONTENTS

| | | | | | | | |

| | Page |

| | |

| |

| |

| | |

| | |

| Item 1. | | |

Item 1A. | | |

Item 1B. | | |

Item 2. | | |

Item 3. | | |

Item 4. | | |

| | |

| | |

| Item 5. | | |

| Item 6. | Reserved | |

Item 7. | | |

Item 7A. | | |

Item 8. | | |

Item 9. | | |

Item 9A. | | |

Item 9B. | | |

Item 9C. | | |

| | |

| | |

Item 10. | | |

Item 11. | | |

Item 12. | | |

Item 13. | | |

Item 14. | | |

| | |

| | |

Item 15. | | |

Item 16. | | |

| |

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This document includes statements that constitute forward-looking statements within the meaning of the federal securities laws. Forward-looking statements represent intentions, plans, expectations, assumptions and beliefs about future events and are subject to risks and uncertainties and other factors. These statements may relate to, but are not limited to, information or assumptions about us, our capital and other expenditures, dividends, financing plans, capital structure, cash flow, pending legal and regulatory proceedings and claims, including environmental matters, future economic performance, operating income, cost savings, and management’s plans, strategies, goals and objectives for future operations and growth. These forward-looking statements generally are accompanied by words such as “intend,” “anticipate,” “believe,” “estimate,” “expect,” “should,” “seek,” “project,” “plan” or similar expressions. Any statement that is not a historical fact is a forward-looking statement. It should be understood that these forward-looking statements are necessary estimates reflecting the best judgment of senior management, not guarantees of future performance. Many of the factors that impact forward-looking statements are outside of our control and could cause actual results to differ materially from the results expressed or implied by those forward-looking statements. When considering forward-looking statements, you should keep in mind the risk factors and other cautionary statements as summarized below and further described in Part I. “Item 1A. Risk Factors” in this document.

We undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws. All forward-looking statements included in this document are expressly qualified in their entirety by the cautionary statements contained or referred to in this section. This cautionary statement should also be considered in connection with any subsequent written or oral forward-looking statements that we or persons acting on our behalf may issue.

In this Annual Report on Form 10-K, we may rely on and refer to information from market research reports, analyst reports and other publicly available information. Although we believe that this information is reliable, we cannot guarantee the accuracy and completeness of this information, and we have not independently verified it.

RISK FACTOR SUMMARY

Our business is subject to significant risks and uncertainties of which you should be aware before making an investment decision in our business. Below is a bulleted summary of our principal risk factors, however this list does not fully represent all of our known risk factors. You should take time to carefully review and consider the full discussion of our risk factors (See Item 1A. Risk Factors).

Risks Relating to Our Business and Industry

•We may not be able to implement our business strategy;

•Our business may require additional funding from various sources, which may be on unfavorable terms;

•We may not be profitable for an indeterminate period of time;

•The loss of a significant customer could adversely affect our operating results;

•We could be materially and adversely affected if any customer fails to perform its contractual obligations;

•Any failure to perform by our counterparties under agreements may adversely affect our operating results, liquidity and access to financing;

•Our customer contracts are subject to termination under certain circumstances;

•Cyclical or other changes in the demand for and price of LNG and natural gas may adversely affect us;

•Failure to maintain sufficient working capital could limit our growth and harm our business;

•Operation of our LNG infrastructure, plants and other assets involves particular, significant risks;

•Climate change may increase the frequency and severity of weather events and other natural disasters that could result in an interruption of our operations, a delay in the completion of future facilities, or delays in payments from our customers;

•Our insurance may be insufficient to cover losses that may occur to our property or result from our operations;

•Our energy-related infrastructure is subject to operational, regulatory, environmental, political, legal and economic risks;

•We are relying on third party contractors to operate our business and execute our strategy;

•We may not be able to purchase or receive physical delivery of natural gas in sufficient quantities and/or at economically attractive prices to satisfy our delivery obligations;

•Changes in legislation and regulations could have a material adverse impact on our business, results of operations, financial condition, liquidity and prospects;

•We face competition in the LNG industry which is intense, and some of our competitors have greater financial, technological and other resources than we currently possess;

•Failure of LNG to be a competitive source of energy in the markets in which we operate, and seek to operate, could adversely affect our expansion strategy;

•Our lack of diversification could have an adverse effect on our business, operating results, liquidity and prospects;

•Our risk management strategies cannot eliminate all LNG price and supply risks; any non-compliance with our risk management strategies could result in significant financial losses;

•We may experience increased labor costs, and the unavailability of skilled workers or failure to attract and retain qualified personnel could adversely affect us;

•We may incur impairments to goodwill or long-lived assets;

•A major health and safety incident involving LNG or within the energy industry may lead to more stringent regulation of LNG operations or the energy business generally, resulting in difficulties in obtaining permits, on favorable terms, and may otherwise lead to significant liabilities and reputational damage;

•Failure to obtain and maintain permits, approvals and authorizations from governmental and regulatory agencies could impede operations and could have a material adverse effect on us;

•Existing and future environmental, health and safety laws and regulations could result in increased compliance costs or additional operating costs or construction costs and restrictions;

•Environmental, social, and governance (“ESG”) goals, programs, and reporting may impact our access to capital;

•Our Chinese Joint Venture, BOMAY, has a limited life and is subject to risk that it may not be renewed;

•We have operations and investment in foreign countries and we could experience losses from foreign economies as well as unexpected operating, financial, political or cultural factors; and

•Our ability to maintain our liquidity may be materially and adversely affected if we are unable to access the capital markets or if any significant customer fails to perform its contractual obligations for any reason.

Risks Inherent in an Investment in Us

•Investment in us is speculative, and our common stock is thinly traded with a limited market and volatile;

•We may continue to incur losses and may never achieve profitability;

•Our Company may need substantial additional funding or we may be compelled to delay, reduce or eliminate portions of our existing business operations and development efforts;

•Raising additional capital may cause dilution to our stockholders or restrict our operations;

•Casey Crenshaw has voting control over our Company, and we may have conflicts of interest arising out of transactions with parties related to Casey Crenshaw;

•Provisions in our corporate charter documents and under Florida law could make an acquisition of the Company, which may be beneficial to its stockholders, more difficult and prevent attempts by our stockholders to replace or remove our current management;

•We do not anticipate that we will pay any cash dividends in the foreseeable future;

•Our present and future success depends on key members of our management team and certain employees and our ability to retain such key members, the loss of any of whom could disrupt our business operations; and

•Our success will depend on pre-existing relationships with third parties; any adverse changes in these relationships could adversely affect our business, financial condition or results of operations.

General Risk Factors

•Weakened global macro-economic conditions may adversely affect our industry, ability to access capital, business and results of operations;

•Increased inflation or periods of prolonged inflation may adversely impact the economy, our industry and results of operations;

•The spread of a contagious illness such as COVID-19 or resurgence of a COVID-19 variant, may adversely affect our business, operations and financial condition;

•A cyber incident could result in information theft, data corruption, operational disruption, operational delays and/or financial loss;

•From time to time, we may be involved in legal proceedings and may experience unfavorable outcomes;

•We will continue to incur costs and demands upon management as a result of complying with the laws and regulations affecting public companies; and

•If we fail to establish and maintain proper and effective internal control over financial reporting, our operating results and our ability to operate our business could be harmed.

PART I

ITEM 1. BUSINESS

OVERVIEW

Our Company

Stabilis Solutions, Inc. and its subsidiaries (the “Company”, “Stabilis”, “our”, “us” or “we”) is an energy transition company that provides turnkey clean energy production, storage, transportation and fueling solutions primarily using liquefied natural gas (“LNG”) to multiple end markets across North America. We have safely delivered over 360 million gallons of LNG through more than 36,000 truck deliveries during our 17-year operating history, which we believe makes us one of the largest and most experienced small-scale LNG providers in North America. We define “small-scale” LNG production to include liquefiers that produce less than 1,000,000 LNG gallons per day and “small-scale” LNG distribution to include distribution by trailer or tank container up to 15,000 LNG gallons or marine vessels that carry less than 8,000,000 LNG gallons. We provide LNG solutions to customers in diverse end markets, including aerospace, agriculture, industrial, utility, pipeline, mining, energy, remote clean power, and high horsepower transportation markets. Our customers use LNG as a partner fuel for renewable energy, and as an alternative to traditional fuel sources, such as distillate fuel oil and propane, to reduce harmful environmental emissions and lower fuel costs. Our customers also use LNG as a “virtual pipeline” solution when natural gas pipelines are not available or are curtailed. We also have the capability, knowledge and expertise to deliver other clean energy fuels still in commercial development such as hydrogen, renewable natural gas and synthetic natural gas.

We also provide electrical switch-gear, generator and instrumentation construction, installation and service to the marine, power generation, oil and gas, and broad industrial market segments in Brazil. Our products are used to safely distribute and control the flow of electricity from a power generation source to mechanical devices utilizing the power. We also offer a range of electrical and instrumentation turnarounds, maintenance and renovation projects.

Additionally, we build power and control systems for the energy industry in China through our 40% interest in our Chinese joint venture, BOMAY Electric Industries, Inc (“BOMAY”).

Our Industry

LNG can be used to deliver natural gas to locations where pipeline service is not available, has been interrupted, or needs to be supplemented. LNG can also be used to replace a variety of alternative fuels, including distillate fuel oil (including diesel fuel and other fuel oils) and propane, among others to provide both environmental and economic benefits. We believe that these alternative fuel markets are large and provide significant opportunities for LNG substitution.

In addition, other clean energy solutions such as hydrogen will play an increasingly important role in the energy transition as clean energy initiatives increase globally. We believe that LNG as well as other clean energy solutions will provide an important balance between environmental sustainability, security and accessibility, and economic viability and will play a key role in the energy transition.

BACKGROUND AND HISTORY

On July 26, 2019 (the “Effective Date”), we completed a share exchange with American Electric Technologies, Inc. (“American Electric”) and its subsidiaries (the "Share Exchange"). In the Share Exchange, American Electric acquired directly 100% of the outstanding limited liability company membership interests of Stabilis Energy, LLC (“Stabilis LLC”) from LNG Investment Company, LLC (“LNG Investment”) and 20% of the outstanding limited liability membership interests of PEG Partners, LLC (“PEG”) from AEGIS NG LLC (“AEGIS”). AEGIS owned a 20% noncontrolling interest of PEG. The remaining 80% of the outstanding limited liability company interests of PEG were owned directly by Stabilis LLC. As a result, Stabilis LLC became a direct 100% owned subsidiary of American Electric and PEG became an indirectly-owned 100% subsidiary of American Electric. Under the Share Exchange Agreement, American Electric issued 13,178,750 post-split shares of common stock to acquire Stabilis LLC, which represented approximately 90% of the total amount of common stock of American Electric, which was issued and outstanding as of July 26, 2019. The proposed transaction was approved by the shareholders of American Electric at a Special Meeting of Stockholders. The Share Exchange resulted in a change of control of American Electric to control by Casey Crenshaw by virtue of his beneficial ownership of 88.4% of the common stock of American Electric to be outstanding as of July 26, 2019.

Immediately following the Effective Date, the Company declared a reverse stock split of its outstanding common stock at a ratio of one-for-eight, American Electric changed its name to Stabilis Energy, Inc., and its common stock began trading under the ticker symbol “SLNG.” The change of name did not result in changes to the Company’s CUSIP number for the Company’s

outstanding shares of common stock. The Company subsequently changed its name to Stabilis Solutions, Inc. Our common stock traded under the symbol “SLNG” on the Nasdaq Stock Market from July 29, 2019 to October 2, 2019. On October 3, 2019 the Company’s common shares commenced trading on the OTCQX Best Market under the same symbol. On April 26, 2021, the Company was approved for listing on the Nasdaq Stock Market under the same symbol.

Because the former owners of Stabilis LLC owned 88.4% of the voting stock of the combined company immediately following the Effective Date, and certain other factors including that directors designated by LNG Investment constitute a majority of the post-closing board of directors, Stabilis LLC is treated as the acquiror of American Electric in the Share Exchange for accounting purposes. As a result, the Share Exchange is treated by American Electric as a reverse acquisition under the purchase method of accounting in accordance with United States generally accepted accounting principles (“U.S. GAAP”).

On August 20, 2019, we completed our acquisition of Diversenergy, LLC (“Diversenergy”) and its subsidiaries. Diversenergy specializes in LNG distribution, providing LNG to customers who use it as a fuel in mobile high horsepower applications and to customers who do not have natural gas pipeline access. We purchased all of the issued and outstanding membership interests of Diversenergy for total consideration of 684,963 shares of the Company's common stock valued at $3.0 million at the closing date and $2.0 million in cash. The completion of the acquisition expanded the Company's presence in the distributed LNG and compressed natural gas (“CNG”) markets in Mexico.

On June 1, 2021, the Company closed on the purchase of an LNG production facility in Port Allen, Louisiana. The acquisition included an LNG liquefaction facility, the related assets and real property. The Company paid consideration of $5.0 million in cash plus legal fees and closing costs of approximately $0.1 million and 500,000 shares of Company common stock, which shares were valued at $3.8 million.

OUR BUSINESS

During 2021, the Company operated and managed its business through two operating segments: LNG and Power Delivery.

LNG Segment

Stabilis is an energy transition company that provides turnkey clean energy production, storage, transportation and fueling solutions to multiple end markets in North America through its LNG segment. Our diverse customer base utilizes LNG solutions as a fuel source in a variety of applications in the aerospace, industrial, utilities and pipelines, mining, energy, remote clean power and high horsepower transportation markets. Our customers use LNG as a partner fuel for renewable energy and as an alternative to traditional fuel sources, such as diesel, fuel oil, and propane, to reduce harmful environmental emissions and to lower fuel costs. Our customers also use LNG as a “virtual pipeline” solution when natural gas pipelines are not available or are curtailed. We provide multiple products and services to our customers, including:

LNG Production, LNG Sales—Stabilis builds and operates cryogenic natural gas processing facilities, called “liquefiers”, which convert natural gas into LNG through a multiple stage cooling process.

We currently own and operate a liquefier that can produce up to 100,000 LNG gallons per day in George West, Texas and a liquefier that can produce up to 30,000 LNG gallons per day in Port Allen, Louisiana, which was purchased on June 1, 2021. We also purchase LNG from third-party production sources which allows us to support customers in markets where we do not own liquefiers.

Transportation and Logistics Services—Stabilis offers its customers a “virtual natural gas pipeline” by providing them with turnkey LNG transportation and logistics services in North America. We deliver LNG to our customers’ work sites from both our own production facility and our network of approximately 37 third-party production sources located throughout North America. We own a fleet of LNG fueled trucks and cryogenic trailers to transport and deliver LNG. We also outsource similar equipment and transportation services for LNG from qualified third-party providers as required to support our customer base.

Cryogenic Equipment Rental—Stabilis owns and operates a rental fleet of approximately 162 mobile LNG storage and vaporization assets, including: transportation trailers, electric and gas-fired vaporizers, ambient vaporizers, storage tanks, and mobile vehicle fuelers. We also own several stationary storage and regasification assets. We believe this is one of the largest fleets of small-scale LNG equipment in North America. Our fleet consists primarily of trailer-mounted mobile assets, making delivery to and between customer locations more efficient. We deploy these assets on job sites to provide our customers with the equipment required to transport, store, and consume LNG in their fueling operations. Our equipment is designed specifically for use in small-scale LNG applications and includes the safety and operational features that our customers and our regulators require.

The table below details our mobile asset base by type and number of assets at December 31, 2021.

| | | | | | | | | | | | | | |

| Asset Type | | Qty | | Description |

| Mobile Storage and Vaporization Units | | 93 | | | Located on customer sites for storage and delivery of LNG fuel |

| Transport Trailers | | 50 | | | Deliver LNG from production sources to customer sites |

| Mobile Truck Fuelers | | 10 | | | Mobile fueling station used to fill heavy duty trucks |

| Other Cryogenic Assets | | 9 | | | Includes hose reels, pump skids, generators, and other |

| Total | | 162 | | | |

Engineering and Field Support Services—Stabilis has experience in the safe, cost effective, and reliable use of LNG in multiple customer applications. We have also developed many processes and procedures that we believe improve our customers’ use of LNG in their operations. Our engineers help our customers design and integrate LNG into their fueling operations and our field service technicians help our customers mobilize, commission and reliably operate on the job site.

Stabilis generates revenue by selling and delivering LNG to our customers. We also generate revenue by renting cryogenic equipment and providing engineering and field support services. We sell our products and services separately or as a bundle depending on the customer’s needs. LNG pricing depends on market pricing for natural gas and competing fuel sources (such as diesel, fuel oil, and propane among others), as well as the customer’s purchased volume, contract duration and credit profile.

Stabilis’ customers use LNG in their operations for multiple reasons, including lower and more stable fuel costs, reduced environmental emissions, and improved operating performance. We serve customers in a variety of end markets, including aerospace, industrial, energy, mining, remote clean power, utilities and pipelines, and high horsepower transportation. We believe that LNG consumption will continue to increase in these end markets in the future.

Stabilis believes that our extensive operating experience positions us to be a leader in the North American small-scale LNG markets. We plan to leverage this experience to grow our business by investing in new LNG production and LNG distribution assets throughout North America.

Power Delivery Segment

Stabilis provides power delivery equipment and services for the marine, power generation, oil and gas, and industrial market segments in Brazil through its Power Delivery segment. Our products are used to safely distribute and control the flow of electricity from a power generation source to mechanical devices utilizing the power. We also offer a range of electrical and instrumentation turnarounds, maintenance and renovation projects.

Additionally, we build power and control systems for the energy industry in China through our 40% interest in BOMAY.

Market for Small-Scale LNG in North America

LNG can serve as a partner fuel for renewable energy sources and provides an important balance between environmental sustainability, security and access, and economic viability as a source of fuel. LNG can also be used to deliver natural gas to locations where pipeline service is not available, has been interrupted, or needs to be supplemented and to replace a variety of other carbon-based fuels. We believe that the current and future markets for LNG are significant and will continue to grow for a number of years.

We believe that the following factors could drive significant LNG market growth in North America over the next decade:

Lower Emissions than Alternative Fossil Fuels. Natural gas contains less carbon than most other fossil fuels and, as a result, produces fewer carbon dioxide emissions when burned. The National Energy Technology Laboratory indicates that new natural gas power plants emit between 50% and 60% less carbon dioxide compared with emissions from a typical coal plant. The Argonne National Laboratory indicates that natural gas vehicles produce between 13% and 21% fewer greenhouse gas emissions than comparable gasoline and diesel fueled vehicles. Additional studies indicate that natural gas also produces lower particulate matter and sulfur emissions than other fossil fuels. We believe the relative environmental benefits of natural gas as a fuel is

becoming increasingly important as our customers expand their corporate sustainability mandates to lower greenhouse gas emissions and increase decarbonization initiatives.

Increasing Growth in Renewable Energy Production. Energy production from renewable energy sources, in particular wind and solar, is growing rapidly across the world as many governments and businesses seek to reduce their carbon emissions. However, wind and solar are intermittent energy sources that require back-up energy sources that can come into service quickly and reliably. We believe that natural gas driven turbines and engines are the preferred viable back-up power source as they meet these operating requirements and use relatively clean natural gas. We believe that natural gas power generation could support the growth of wind and solar energy production and that LNG could be a preferred source of natural gas for off-pipeline applications.

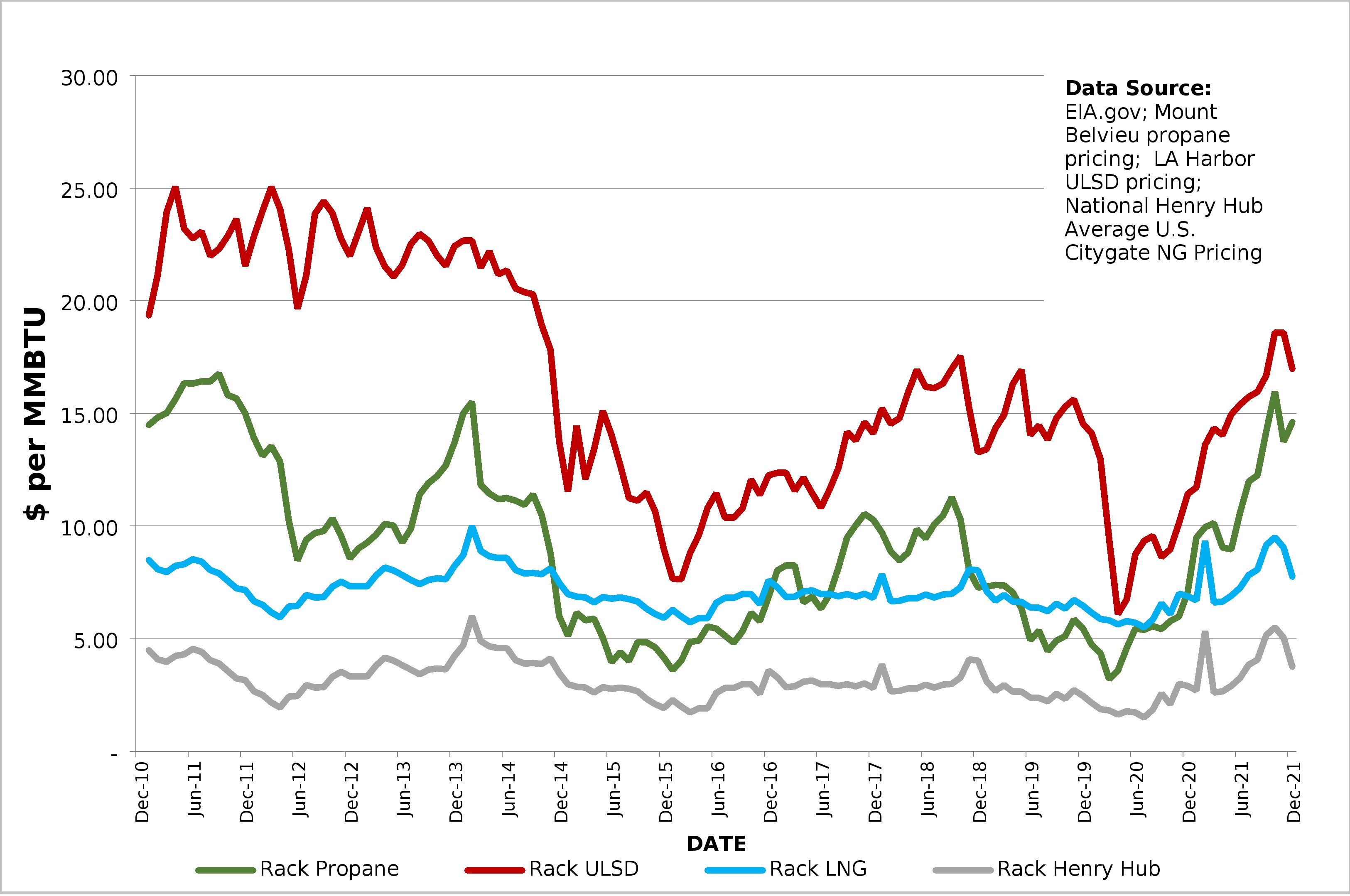

Less Expensive than Other Traditional Fuels. The cost of natural gas compared to other energy sources is a significant driver for the future demand for natural gas and LNG. Technological advances in natural gas production have unlocked significant new gas reserves in North America. We believe that these proven, abundant and growing reserves of natural gas have the potential to produce among the highest volumes of natural gas in the world. This abundant supply of natural gas has supported relatively low natural gas prices in North America. The cost of natural gas in the United States and Canada currently is less than the cost of crude oil on an energy equivalent basis. In addition, because the price of the natural gas commodity makes up a smaller portion of the total cost of LNG relative to the commodity portion of competing fuels, the price of LNG is less sensitive to variations in the underlying commodity cost. These factors have made LNG more economical than competing fuel sources, and we believe that LNG will maintain this cost advantage into the foreseeable future.

The following chart illustrates the lower cost and decreased price sensitivity of LNG by comparing the historical wholesale price of Propane, Ultra-Low No. 2 Diesel, Indicative Liquefied Natural Gas and Natural Gas (Henry Hub).

ULSD, Propane & LNG pricing-2011 to December 31, 2021

Better Safety than Alternative Fuels. The physical characteristics of LNG make it a safer and more environmentally friendly fuel when compared to diesel and propane because it boils and dissipates rapidly into the air when spilled instead of pooling on or near the ground. If released, LNG is also less combustible than diesel and propane because it ignites at relatively high

temperatures and within a narrow flammability range when mixed with air. In addition, LNG fuel tanks and systems used in natural gas applications are subjected to a number of federal and state required safety tests, such as fire, environmental hazard, burst pressure and crash testing that ensure their safety.

Established LNG Production and Distribution Technology. Small-scale LNG production and distribution technologies have been proven and are now widely available from multiple vendors. Small-scale liquefiers are available in modular formats from several vendors and many of them have established track records of reliable and safe operating performance. LNG transport trailers, storage vessels, and vaporization equipment are also available from multiple vendors, and most of this equipment also comes with an established operating track record. We believe that the availability of proven small-scale LNG production and distribution technologies reduces the technology risk in growing the industry, but it also places a premium on the owner’s or operator’s construction and operating capabilities.

Other Markets, Demand and Opportunities for Our Services

Other Clean Energy Fuels such as Hydrogen, Renewable Natural Gas and Synthetic Natural Gas. We believe that our technical expertise, production, transportation and storage capabilities allows us to provide other clean energy fuels such as hydrogen, renewable natural gas and synthetic natural gas. The current market demand for these is currently very small as they are generally not yet commercially viable compared to more traditional hydrocarbon-based fuel sources (including natural gas). However, production and distribution technologies are currently under development by various manufacturers for all of these. As we believe societies and governments strive for a decarbonized world, development of commercially viable, zero emission fuel technologies could make these other energy transition fuels more prevalent in the coming decades. According to a 2021 study published by the Hydrogen Council, over 200 hydrogen projects have been announced worldwide, including over 19 in North America, including projects for large-scale industrial usage, use as a transportation fuel in ships and buses, and distribution, transportation, and storage infrastructure. Hydrogen spending projections across the value chain based on project announcements add up to more than $300 billion through 2030. Hydrogen can be transported by trucks, pipelines or ships depending on the targeted end-use. We expect that small-scale hydrogen distribution using equipment and expertise similar to that used for small-scale LNG will play an important role in the ultimate acceptance and utilization of hydrogen as a low to zero emission fuel source.

Our Customers

Stabilis serves customers in a variety of end markets, including aerospace, industrial, utilities and pipelines, mining, energy, commercial, and transportation within the United States and Mexico. We believe these customer markets are well suited to use LNG and hydrogen because they consume relatively high volumes of fuel, operate in mobile, temporary or off-pipeline locations, have limited access to alternative fuel sources, and/or are facing increasingly stringent emissions or other environmental requirements. We currently serve approximately 120 customers. For the year ended December 31, 2021, Aggreko Plc, Minera Penmont and Chevron Corporation each accounted for more than 10% of our revenues. For the year ended December 31, 2020, Chevron Corporation and Aggreko Plc each accounted for more than 10% of our revenues. During such periods, no other purchaser accounted for 10% or more of our revenue.

Aerospace. The Aerospace industry utilizes LNG as a propellant for rocket propulsion systems and LNG provides an economical, readily available, and easily stored fuel for rockets engines. Aerospace firms may also utilize LNG for power generation at remote facilities. Consumption of LNG at aerospace facilities vary significantly by project type.

Industrial. Industrial applications for LNG include sand and aggregate producers, asphalt plants, greenhouses, food processers, paper mills, agricultural dryers, and general manufacturing facilities. Remote sand producers and mobile asphalt plants that use LNG to produce heat for their processing and drying operation are among our largest customers. LNG often replaces propane, fuel oil, or diesel fuel in these applications. These customers often cannot justify the cost of new pipeline infrastructure and using LNG requires minimal up-front costs, regulatory approvals, and lead time requirements. We believe LNG is optimal for these applications because it is cost-effective with stable pricing, offers consistent supply without curtailments, provides an energy density that minimizes storage requirements, and has a clean and consistent burn that makes heating operations more predictable. Based on our experience, sand production facilities can consume 10,000 to 20,000 LNG gallons per day, and asphalt plants can use 5,000 to 10,000 LNG gallons per day.

Utilities and Pipelines. North America has an expansive network of pipelines that, based on age and increasingly more stringent regulations, require routine testing and maintenance. During such events LNG fueling solutions can provide flow assurance to address natural gas supply interruptions during pipeline hydrostatic testing, repairs, gas distribution system curtailments, or unplanned outages. Such solutions can also provide a bridge for large industrial or utility customers before permanent pipelines are installed. LNG is becoming more predominant in regions where natural gas demand is growing and utilities and pipelines are required to continue to meet critical peak gas demand. LNG can provide an economic solution to

support these supply requirements during peak weather conditions, gas curtailments and/or pipeline repairs. In addition, utilities and other power providers can also utilize LNG to provide clean distributed power when access to an electrical grid is limited, additional power is needed during times of peak load, or power infrastructure is damaged due to storms such as hurricanes or wildfires. LNG usage in utility and pipeline applications varies significantly by project type. Hydrogen and methane blends are currently being tested by pipelines as a method of reducing emissions from pipeline gas.

Mining. Mines, including those producing metals, rare earth materials, and coal, are often located in remote locations that are off the electrical grid and do not have natural gas pipeline access. Mines use LNG to fuel electrical generators and to produce heat for their processing activities. Several mines have also tested using LNG as a fuel for their mine trucks and other high horsepower engine equipment. In addition to fuel cost benefits, LNG can help reduce emissions at mines that are often located in environmentally sensitive areas. Based on our experience, power generation and heating applications at mines can consume 10,000 to 100,000 LNG gallons per day.

Energy. Energy producers use high horsepower engines to power their drilling and pressure pumping operations. LNG displaces some of the total diesel fuel consumption in these applications using dual-fuel engine technology. We believe that energy producers can use LNG to reduce fuel costs and to meet environmental emissions requirements. Based on our experience, dual-fuel drill rigs can consume 1,000 to 5,000 LNG gallons per day and dual-fuel pressure pumping spreads can consume 10,000 to 20,000 LNG gallons per day. Energy producers use the field gas being produced in their operations to fuel the turbine engines that power their pressure pumping spreads. While turbines can burn field gas, they often require significant amounts of LNG for primary or back-up fuel supply because field gas often varies widely in volume, composition, and pressure. Based on our experience, turbine driven pressure pumping operations can consume 30,000 to 60,000 LNG gallons per day when using LNG as the primary fuel.

Commercial. Commercial locations, including offices, call centers, data centers and campuses, often need fuel for primary or back-up power generation. LNG often replaces propane or diesel fuel in these applications. LNG usage in commercial applications varies significantly by location size and purpose.

Transportation. LNG is being used to fuel high horsepower engines in multiple transportation applications, including over-the-road trucking, mine haul trucks, locomotives, and marine engines, due to reduced emissions and cost savings benefits. Extensive LNG fueling networks exist currently in the United States, the European Union, and China. Regulatory requirements are accelerating the adoption of LNG as a transportation fuel in other markets, particularly in the marine sector. LNG usage in transportation application varies by the horsepower requirements of the application.

Marine Bunkering of LNG. We believe that opportunities to provide LNG as a fuel source to the marine transportation industry represents a significant opportunity for us. As shipping and marine transportation companies expand the use of LNG as a fuel source, we believe that we are positioned to capitalize on future growth. The International Maritime Organization (“IMO”) has imposed a global sulfur cap of 0.5% on ships trading outside of established emission control areas starting in January 2020, a level that could be difficult to achieve using common marine fuels, such as heavy fuel oil, but could be achieved using LNG. Large marine vessels can take several hundred thousand gallons of LNG in a single fuel bunkering event.

We actively deliver LNG through virtual distribution systems, providing LNG to customers who use it as a fuel in mobile high horsepower applications and to customers who do not have natural gas pipeline access.

Brazil. We offer a range of electrical and instrumentation construction and installation services to our customers. These services include new construction as well as electrical and instrumentation turnarounds, maintenance and renovation projects.

China. Through our 40% interest in BOMAY, we provide power and control systems for the land drilling and production market in China.

Competitive Strengths

Stabilis believes that we are well positioned to execute our business strategies based on the following competitive strengths:

LNG is an economically and environmentally attractive product. Stabilis believes that many of our customers use LNG because it can significantly reduce harmful carbon dioxide, nitrogen oxide, sulfur, particulate matter, and other emissions as compared to other hydrocarbon-based fuels. LNG is also an important partner fuel for renewables such as solar and wind power and will be a key component of the energy transition to more sustainable sources of energy. We also believe that the combination of cost and environmental benefits makes LNG a compelling fuel source for many energy consumers. We believe that LNG can

be delivered to customers at prices that are lower and more stable than what they would pay for distillate fuels or propane. In addition, several of our customers have reported that LNG as a fuel decreases their operating costs by reducing equipment maintenance requirements and providing more consistent burn characteristics.

Demonstrated ability to execute LNG projects safely and cost effectively. Stabilis has produced and delivered over 360 million gallons of LNG to our customers throughout our 17 year operating history. Our experience includes building and operating LNG production facilities, delivering LNG from third-party sources to our customers, and designing and executing a wide-variety of turnkey LNG fueling solutions for our customers using our cryogenic equipment fleet supported by our field service team. We have experience serving customers in multiple end markets including aerospace, industrial, utilities and pipelines, mining, energy, remote clean power, and transportation. We also have experience exporting LNG to Mexico and Canada. Finally, we believe our team is among the most experienced in the small-scale LNG industry. We believe that we can leverage this proven LNG execution experience to grow our business in existing markets and expand our business into new markets including the nascent hydrogen market. The production and distribution of hydrogen shares many attributes with LNG and we believe hydrogen will be a safe fuel and increasingly cost effective as acceptance grows.

Comprehensive provider of “virtual natural gas pipeline” solutions throughout North America. Stabilis offers our customers a comprehensive off-pipeline natural gas solution by providing the supply infrastructure, transportation and logistics, and field service support necessary to deliver LNG to them in a program that is tailored to their consumption needs. We believe we own one of the largest fleets of cryogenic transportation, storage, and vaporization equipment in North America. We can provide our customers LNG and related services for a wide variety of applications almost anywhere in the United States, Canada and Mexico. We believe that our ability to be a “one stop shop” for all of our customers’ off-pipeline natural gas requirements throughout North America is unique among LNG providers. We believe our LNG experience allows us to expand our comprehensive offerings using hydrogen.

Ability to leverage existing LNG production and delivery capabilities into new markets. Stabilis believes that our experience producing and distributing LNG can be leveraged to grow into new geographic and service end markets. Since our founding we have expanded our service area across the United States, northern Mexico, and western Canada. We have also expanded our industry coverage to include multiple new end markets and customers. We accomplished this expansion into new markets by leveraging our LNG production and distribution expertise, in combination with our cryogenic engineering and project development capabilities, to meet new customer needs.

Competition

The market for natural gas is highly competitive. Stabilis believes the biggest competition for LNG in these applications are distillate fuels and propane as they power the majority of engines and generators in our target markets. We also compete with other fuel sources including pipeline natural gas and CNG. We believe we have multiple competitors in the market for natural gas fuel, including, but not limited to:

•Producers and distributors of LNG, including New Fortress Energy LLC, Clean Energy Fuels Corp., BHE GT&S Berkshire Hathaway Energy (formerly Dominion Energy), Eagle LNG, Applied LNG, Kinetrex Energy, numerous utilities located across the country which produce LNG for peak shaving purposes, and numerous local providers of cryogenic distribution and field services; and

•Producers and distributors of CNG, including NG Advantage LLC, Xpress Natural Gas LLC (Basalt Infrastructure Partners), Compass Natural Gas Partners LP and Certarus Ltd.

Stabilis competes with other natural gas companies, as well as other fossil fuel sources, based on a variety of factors, including, among others, cost, supply, availability, quality, emissions, and safety of the fuel. Location is often a primary competitive factor as transportation costs limit the distance LNG can be hauled at competitive prices. We believe we compare favorably with many of our competitors on the basis of these factors; however, some of our competitors have longer operating histories and market-based experience, larger customer bases, more expansive brand recognition, deeper market penetration and substantially greater financial, marketing and other resources than our business. As a result, they may be able to respond more quickly to changes in customer preferences, legal requirements or other industry or regulatory trends, devote greater resources to the development, promotion and sale of their products, adopt more aggressive pricing policies, dedicate more effort to infrastructure and systems development in support of their business or product development activities and exert more influence on the regulatory landscape that impacts the natural gas fuel market. Additionally, utilities and their affiliates typically have unique competitive advantages, including a lower cost of capital, substantial and predictable cash flows, long-standing customer relationships, greater brand awareness, and large sales and marketing organizations.

Stabilis does not believe that we compete with mid-scale and world-scale LNG liquefiers that produce more than 1,000,000 LNG-gallons per day. These large LNG production facilities, such as those operated by Cheniere Energy and Freeport LNG, typically are designed and permitted to fill large marine vessels that deliver cargos of 21,120,000 LNG-gallons or more to large import terminals in foreign markets. We do not believe that any of them currently have or plan to have truck loading facilities that would be required to supply LNG to small-scale LNG customers. We also do not believe that any mid-scale or large-scale liquefiers currently have plans to install LNG loading capabilities for vessels smaller than 7,920,000 LNG-gallons.

Sales and Marketing

Stabilis markets our products and services primarily through our direct sales force, which includes sales representatives covering all of our major geographic and customer markets, as well as attendance at trade shows and participation in industry conferences and events. Our technical, sales and marketing teams also work closely with federal, state and local government agencies to provide education about the value of natural gas as a fuel and to keep abreast of proposed and newly adopted regulations that affect our industry.

Seasonality

We did not experience significant seasonal variations in volume of LNG delivered to our customers during 2021, and we do not expect future volumes to be significantly impacted by seasonal variations. However, our revenues are susceptible to variations due to changes in the price of natural gas as we pass this cost onto our customer. The price of natural gas can fluctuate at any time during the year due to isolated factors, but on average, natural gas prices tend to be higher in peak winter and peak summer months when heating and cooling demand is seasonally higher.

Government Regulation and Environmental Matters

Stabilis is subject to a variety of federal, international, state, provincial and local laws and regulations relating to the environment, health and safety, labor and employment, building codes and construction, zoning and land use, public reporting and taxation, among others. Any changes to existing laws or regulations, the adoption of new laws or regulations, or failure by us to comply with applicable laws or regulations could result in significant additional expense to us or our customers or a variety of administrative, civil and criminal enforcement measures, any of which could have a material adverse effect on our business, reputation, financial condition and results of operations. Regulations that significantly affect our operating activities are described below. Compliance with these regulations has not had a material effect on our capital expenditures, earnings or competitive position to date, but new laws or regulations or amendments to existing laws or regulations to make them more stringent could have such an effect in the future. We cannot estimate the costs that may be required for us to comply with potential new laws or changes to existing laws, and these unknown costs are not contemplated by our existing customer agreements or our budgets and cost estimates. We believe that we are in compliance with all environmental and other governmental regulations. Our compliance has, to date, had no material effect on our capital expenditures, earnings, or competitive position.

Construction and Operation of LNG Liquefaction Plants. To build and operate LNG liquefaction plants, Stabilis must apply for facility permits or licenses that address many factors, including storm water and wastewater discharges, waste handling, and air emissions related to production activities and equipment operation. The construction of LNG plants must also be approved by local planning boards and fire departments.

Transportation of LNG. Federal and state safety standards require that LNG is moved by qualified drivers in cryogenic containers designed for LNG transportation. Drivers are subject to U.S. Department of Transportation (“USDOT”) regulations, such as Federal Motor Carrier Safety Administration (“FMCSA”), Hazardous Materials Regulations, and state certification requirements, such as certifications by the Alternative Energy Division of the Railroad Commission of Texas. Cryogenic containers have to undergo annual USDOT visual inspections and periodic pressure tests. Motor vehicles equipped with an LNG container or other motor vehicles used principally for transporting LNG in portable containers in Texas have to be registered with the Railroad Commission of Texas.

Transfer of LNG. Federal safety standards require each transfer of LNG to be conducted in accordance with specific written safety procedures. These procedures must require that qualified personnel be in attendance during all LNG transfer operations, and these procedures must be implemented, and copies of the procedures must be available/displayed, at each LNG transfer location.

Storage and Vaporization of LNG at Customer Sites. To install and operate both temporary and permanent storage and vaporization equipment, Stabilis may apply for permits or licenses that address many factors, including waste handling and air

emissions related to onsite storage and equipment operation or consult with customers so they may apply for needed permits. The operation and siting of storage and vaporization of LNG may also require approval by local planning boards and fire departments.

Import & Export of LNG. To import or export LNG from the United States to Mexico and Canada via truck, numerous authorizations are required. In support of our business in Canada, Stabilis maintains an import and export license from the United States Department of Energy (“DOE”) and from the National Energy Board of Canada (“NEB”). We maintain an Emergency Response Action Plan (“ERAP”) with Transport Canada. In support of our business in Mexico, we maintain an export license from the DOE and maintain import permits to bring the LNG into the country. Exporting LNG in large quantities would require additional permits and licenses from various regulatory agencies, including the DOE and the Federal Energy Regulatory Commission (“FERC”). We do not have these permits at this time but could file for such authorizations in the future.

Human Capital Resources

Stabilis believes that one of its key assets is the collective expertise, experience and diversity of its workforce. The Company depends on all of its employees, including its executive officers and senior management, to successfully operate its businesses and to successfully execute its strategy going forward. As of December 31, 2021, Stabilis had 293 employees, 249 of whom were full-time employees. We believe our relations with employees are satisfactory. None of our employees are currently subject to a collective bargaining agreement.

Stabilis seeks to attract and retain its employees by offering competitive compensation packages including base and incentive compensation, attractive benefits and opportunities for advancement and rewarding careers. The Company periodically reviews and adjusts, if needed, its employees’ compensation to ensure that it is competitive within the industry and is consistent with their level of performance. Stabilis considers employee benefits to be an important part of employee total compensation. For this reason, the Company’s benefits include medical, dental, and vision and insurance, short- and long-term disability insurance, accidental death and disability insurance, travel and accident insurance, as well as a 401(k) contribution retirement plan. The Company’s ability to attract employees is also significantly influenced by our efforts to create a culture founded on opportunity, personal growth, respect, collaboration and its ability to value the diverse backgrounds, skills and contributions that its employees offer.

Stabilis strives to provide its people with all of the tools and support necessary for them to succeed and safely perform their duties. The safety of its employees, contractors, customers and communities is paramount to the Company’s success. To ensure safe, reliable and efficient operations in a highly regulated environment, the Company supports and utilizes various employee training, educational programs as well as safety programs with detailed safety and health related procedures that all are required to follow. In response to the COVID-19 pandemic, the Company has implemented workplace controls and risk mitigation measures that have enabled the Company to work through several periods of elevated impacts from COVID-19, including the Delta and Omicron variants.

Intellectual Property

The intellectual property portfolio of Stabilis and its subsidiaries includes patents and trademarks. The Company has a patent in both US and Canada for the use of natural gas for well enhancement. The Company has two patents for rotary fluid processing systems and a US patent for a gas processing system. The Company also has three pending foreign patent applications (one in Canada and two in Mexico). The last patent to expire in the U.S. will expire in July 2038, absent any adjustments or extensions. The Company has ten U.S. trademark registrations and one foreign trademark registration (Canada). The Company has no pending trademark applications.

Available Information

Stabilis’ principal executive office is located at 11750 Katy Freeway, Suite 900, Houston, Texas 77079. Our telephone number is 832-456-6500 and our website address is www.stabilis-solutions.com. We make our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, amendments to those reports and other information filed with or furnished to the SEC available, free of charge, through our website, as soon as reasonably practicable after those reports and other information are electronically filed with or furnished to the SEC. The reference to Stabilis’ website is not intended to incorporate the information on the website into this report or any of our filings with the SEC. In addition, the SEC maintains a website that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC at http://www.sec.gov. This annual report on Form 10-K, including all exhibits and amendments, has been filed electronically with the SEC.

ITEM 1A. RISK FACTORS

Investing in shares of our common stock involves a high degree of risk. You should carefully consider the risks described below with all of the other information included in this report in evaluating an investment in our common stock. If any of the following risks were to occur, our business, financial condition, results of operations, and cash flows could be materially adversely affected. In that case, the trading price of our common stock could decline and you could lose all or part of your investment. Additional risks not presently known to us or that we currently deem immaterial may also impair our business operations.

Risks Related to Our Business

Our ability to implement our business strategy may be materially and adversely affected by many known and unknown factors.

Our business strategy relies upon our future ability to successfully market natural gas to end-users, develop and maintain cost-effective logistics in our supply chain and construct, develop and operate energy-related infrastructure in North America. Our business strategy assumes that we will be able to expand our operations further in North America, enter into long-term purchase and supply contracts with end-users, acquire and transport LNG at attractive prices, develop infrastructure, and other future projects, into efficient and profitable operations in a timely and cost-effective way, obtain approvals from all relevant federal, international, state and local authorities, as needed, for the construction and operation of these projects and other relevant approvals, and obtain long-term capital appreciation and liquidity with respect to such investments. Our strategy may also be affected by future governmental laws and regulations. It also assumes that we will be able to enter into strategic relationships with energy end-users, power utilities, LNG providers, transportation companies, infrastructure developers, financing counterparties and other partners. These assumptions are subject to significant economic, competitive, regulatory and operational uncertainties, contingencies and risks, many of which are beyond our control. Additionally, in furtherance of our business strategy, we may acquire operating businesses or other assets in the future. Any such acquisitions would be subject to significant risks and contingencies, including the risk of integration, and we may not be able to realize the benefits of any such acquisitions.