Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION,

WASHINGTON, D.C. 20549

FORM 20-F

| ☐ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2017

OR

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

OR

| ☐ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report

Commission file number 1-14660

(Exact name of Registrant as specified in its charter)

CHINA SOUTHERN AIRLINES COMPANY LIMITED

(Translation of Registrant’s name into English)

THE PEOPLE’S REPUBLIC OF CHINA

(Jurisdiction of incorporation or organization)

278 JI CHANG ROAD

GUANGZHOU, 510405

PEOPLE’S REPUBLIC OF CHINA

(Address of principal executive offices)

Mr. Xie Bing

Telephone: +86 20 86124462

E-mail: ir@csair.com

Fax: +86 20 86659040

Address: 278 JI CHANG ROAD

GUANGZHOU, 510405

PEOPLE’S REPUBLIC OF CHINA

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of each class |

Name of each exchange on which registered | |

| Ordinary H Shares of par value RMB1.00 per share represented by American Depositary Receipts |

New York Stock Exchange |

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act.

None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report: 7,022,650,000 A Shares of par value RMB1.00 per share and 3,065,523,272 H Shares of par value RMB1.00 per share.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ☐ Yes ☒ No

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. ☐ Yes ☒ No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). ☒ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☒ | Accelerated filer | ☐ | |||||

| Non-accelerated filer | ☐ | Emerging growth company | ☐ | |||||

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

| † | The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012. |

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| U.S. GAAP ☐ |

International Financial Reporting Standards as issued by the International Accounting Standards Board ☒ |

Other ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement Item the registrant has elected to follow. ☐ Item 17 ☐ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ☐ Yes ☒ No

Table of Contents

i

Table of Contents

ii

Table of Contents

This Annual Report contains forward-looking statements. These statements appear in a number of different places in this Annual Report. A forward-looking statement is usually identified by the use in this Annual Report of certain terminology such as “estimate”, “project”, “expect”, “intend”, “believe”, “plan”, “anticipate”, “may”, or their negatives or other comparable words. Also look for discussions of strategy that involve risks and uncertainties. Forward-looking statements include statements regarding the outlook for our future operations, forecasts of future costs and expenditures, evaluation of market conditions, the outcome of legal proceedings (if any), the adequacy of reserves, or other business plans. You are cautioned that such forward-looking statements are not guarantees and involve risks, assumptions and uncertainties. Our actual results may differ materially from those in the forward-looking statements due to risks facing our Company or due to actual facts differing from the assumptions underlying those forward-looking statements.

Some of these risks and assumptions, in addition to those identified under Item 3, “Key Information - Risk Factors,” include:

| • | general economic and business conditions in markets where our Company operates, including changes in interest rates; |

| • | the effects of competition on the demand for and price of our services; |

| • | natural phenomena; |

| • | the impact of unusual events on our business and operations; |

| • | actions by government authorities, including changes in government regulations, and changes in CAAC’s regulatory policies; |

| • | our relationship with China Southern Air Holding Limited Company (“CSAH”); |

| • | uncertainties associated with legal proceedings; |

| • | technological development; |

| • | our ability to attract key personnel and attract new talent; |

| • | future decisions by management in response to changing conditions; |

| • | the Company’s ability to execute prospective business plans; |

| • | the availability of qualified flight personnel and airport facilities; and |

| • | misjudgments in the course of preparing forward-looking statements. |

Our Company advises you that these cautionary remarks expressly qualify in their entirety all forward-looking statements attributable to our Company, our Group and persons acting on their behalf.

1

Table of Contents

In this Annual Report, unless the context indicates otherwise, the “Company”, “we”, “us” and “our” means China Southern Airlines Company Limited, a joint stock company incorporated in China on March 25, 1995, our “Group” means our Company and our consolidated subsidiaries, and “CSAH” means China Southern Air Holding Limited Company, our Company’s parent company which directly and indirectly holds a 50.65% interest in our Company as of April 26, 2018.

References to “China” or the “PRC” are to the People’s Republic of China, excluding Hong Kong, Macau and Taiwan. References to “Renminbi” or “RMB” are to the currency of China, references to “U.S. dollars”, “$” or “US$” are to the currency of the United States of America (the “U.S.” or “United States”), and reference to “HK$” is to the currency of Hong Kong. Reference to the “Chinese government” is to the national government of China. References to “Hong Kong” or “Hong Kong SAR” are to the Hong Kong Special Administrative Region of the PRC. References to “Macau” or “Macau SAR” are to the Macau Special Administrative Region of the PRC.

Our Company presents our consolidated financial statements in Renminbi. The consolidated financial statements of our Company have been prepared in accordance with all applicable International Financial Reporting Standards (“IFRSs”), which collective term includes all applicable individual IFRSs, International Accounting Standards (“IASs”) and Interpretations issued by the International Accounting Standards Board (the “IASB”).

Solely for the convenience of the readers, this Annual Report contains translations of certain Renminbi amounts into U.S. dollars at the rate of US$1.00 = RMB6.5342, which is the average of the buying and selling rates as quoted by the People’s Bank of China at the close of business on December 29, 2017. No representation is made that the Renminbi amounts or U.S. dollar amounts included in this Annual Report could have been or could be converted into U.S. dollars or Renminbi, as the case may be, at any particular rate or at all. Any discrepancies in the tables included herein between the amounts listed and the totals are due to rounding.

2

Table of Contents

GLOSSARY OF AIRLINE INDUSTRY TERMS

In this Annual Report, unless the context indicates otherwise, the following terms have the respective meanings set forth below.

| Capacity | ||

| “available seat kilometers” or “ASK” | the number of seats made available for sale multiplied by the kilometers flown | |

| “available ton kilometers” or “ATK” | the tons of capacity available for the transportation of revenue load (passengers and cargo) multiplied by the kilometers flown | |

| Traffic | ||

| “revenue passenger kilometers” or “RPK” | i.e. passenger traffic volume, the number of passengers carried multiplied by the kilometers flown | |

| “revenue ton kilometers” or “RTK” | i.e. total traffic volume, the load (passenger and cargo) in tons multiplied by the kilometers flown | |

| “revenue ton kilometers-cargo” or “RFTK” | i.e. cargo and mail traffic volume or revenue ton kilometers for cargo, the load (cargo) in tons multiplied by the kilometers flown | |

| “revenue ton kilometers-passenger” | the load (passenger) in tons multiplied by the kilometers flown | |

| “ton” | a metric ton, equivalent to 2,204.6 pounds | |

| Yield | ||

| “yield per RPK” | revenue from passenger operations divided by RPK | |

| “yield per RFTK” | revenue from cargo operations divided by RFTK | |

| “yield per RTK” | revenue from airline operations (passenger and cargo) divided by RTK | |

| Cost | ||

| “operating cost per ATK” | operating expenses divided by ATK | |

| Load Factors | ||

| “overall load factor” | RTK expressed as a percentage of ATK | |

| “passenger load factor” | RPK expressed as a percentage of ASK | |

| Utilization | ||

| “utilization rates” | flight hours that aircraft can service during specified time | |

| Equipment | ||

| “expendables” | aircraft parts that are ordinarily used up and replaced with new parts | |

| “rotables” | aircraft parts that are ordinarily repaired and reused | |

| Others | ||

| “ADR” | American Depositary Receipt | |

| “A Shares” | Shares issued by our Company to investors in the PRC for subscription in RMB, with par value of RMB1.00 each | |

| “CSAH” | China Southern Air Holding Limited Company, formerly known as China Southern Air Holding Company | |

| “CAAC” | Civil Aviation Administration of China | |

| “CAOSC” | China Aviation Oil Supplies Company | |

3

Table of Contents

| “CSRC” | China Securities Regulatory Commission | |

| “H Shares” | Shares issued by our Company, listed on The Stock Exchange of Hong Kong Limited and subscribed for and traded in Hong Kong dollars, with par value of RMB1.00 each | |

| “Nan Lung” | Nan Lung Holding Limited (a wholly-owned subsidiary of CSAH) | |

| “NDRC” | National Development and Reform Commission of China | |

| “SA Finance” | Southern Airlines Group Finance Company Limited | |

| “SAFE” | State Administration of Foreign Exchange of China | |

| “SEC” | United States Securities and Exchange Commission | |

| “SPVs” | China Southern Airlines No. 1 Lease (Tianjin); China Southern Airlines No. 2 Lease (Tianjin); China Southern Airlines No. 3 Lease (Tianjin); China Southern Airlines No. 4 Lease (Guangzhou); China Southern Airlines No. 5 Lease (Tianjin); China Southern Airlines No. 6 Lease (Tianjin); China Southern Airlines No. 7 Lease (Tianjin); China Southern Airlines No. 8 Lease (Tianjin); China Southern Airlines No. 9 Lease (Guangzhou); China Southern Airlines No. 12 Lease (Tianjin); China Southern Airlines No. 13 Lease (Tianjin); and China Southern Airlines No. 14 Lease (Tianjin) | |

4

Table of Contents

| ITEM 1. | IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS |

Not applicable.

| ITEM 2. | OFFER STATISTICS AND EXPECTED TIMETABLE |

Not applicable.

| ITEM 3. | KEY INFORMATION |

| A. | SELECTED FINANCIAL DATA. |

The following tables present selected financial data for the five-year period ended December 31, 2017. The selected consolidated income statement data (other than ADR data) for the three-year period ended December 31, 2015, 2016 and 2017 and selected consolidated statement of financial position data as of December 31, 2016 and 2017 are derived from the audited consolidated financial statements of our Company, included elsewhere in this Annual Report. The selected consolidated income statement data (other than ADR data) for the years ended December 31, 2013 and 2014 and selected consolidated statement of financial position data as of December 31, 2013, 2014 and 2015 are derived from our Company’s audited consolidated financial statements that are not included in this Annual Report.

Moreover, the selected financial data should be read in conjunction with our consolidated financial statements together with accompanying notes and “Item 5. Operating and Financial Review and Prospects” which are included elsewhere in this Annual Report. Our consolidated financial statements are prepared and presented in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board, or IFRSs.

| Year ended 31, | ||||||||||||||||||||||||

| 2017 US$ |

2017 RMB |

2016 RMB |

2015 RMB |

2014 RMB |

2013 RMB |

|||||||||||||||||||

| (in million, except per share and per ADR data) | ||||||||||||||||||||||||

| Consolidated Income Statement Data |

||||||||||||||||||||||||

| Operating revenue |

19,560 | 127,806 | 114,981 | 111,652 | 108,584 | 98,547 | ||||||||||||||||||

| Operating expenses |

(18,839 | ) | (123,098 | ) | (106,204 | ) | (101,492 | ) | (106,026 | ) | (98,280 | ) | ||||||||||||

| Operating profit |

1,401 | 9,156 | 12,612 | 13,438 | 4,748 | 1,510 | ||||||||||||||||||

| Profit before income tax |

1,358 | 8,874 | 7,661 | 6,118 | 3,066 | 3,484 | ||||||||||||||||||

| Profit for the year |

1,056 | 6,898 | 5,898 | 4,818 | 2,398 | 2,750 | ||||||||||||||||||

| Profit attributable to: |

||||||||||||||||||||||||

| Equity shareholders of our Company |

912 | 5,961 | 5,044 | 3,736 | 1,777 | 1,986 | ||||||||||||||||||

| Non-controlling interests |

143 | 937 | 854 | 1,082 | 621 | 764 | ||||||||||||||||||

| Basic and diluted earnings per share |

0.09 | 0.60 | 0.51 | 0.38 | 0.18 | 0.20 | ||||||||||||||||||

| Basic and diluted earnings per ADR(1) |

4.59 | 30.03 | 25.69 | 19.03 | 9.05 | 10.11 | ||||||||||||||||||

| Other Financial Data |

||||||||||||||||||||||||

| Cash dividends declared per share |

0.02 | 0.10 | 0.10 | 0.08 | 0.04 | 0.04 | ||||||||||||||||||

| (1) | Basic and diluted earnings per share have been computed by dividing profit attributable to equity shareholders of our Company by the weighted average number of shares in issue. Basic and diluted earnings per ADR have been computed as if all of our issued or potential ordinary shares, including domestic shares and H shares, are represented by ADRs during each of the years presented. Each ADR represents 50 shares. |

5

Table of Contents

| Year ended 31, | ||||||||||||||||||||||||

| 2017 US$ |

2017 RMB |

2016 RMB |

2015 RMB |

2014 RMB |

2013 RMB |

|||||||||||||||||||

| (in million, except per share and per ADR data) | ||||||||||||||||||||||||

| Consolidated Statement of Financial Position Data: |

||||||||||||||||||||||||

| Cash and cash equivalents |

1,045 | 6,826 | 4,152 | 4,560 | 15,414 | 11,748 | ||||||||||||||||||

| Total current assets, excluding cash and cash equivalents |

1,692 | 11,058 | 9,612 | 9,553 | 12,127 | 8,825 | ||||||||||||||||||

| Property, plant and equipment, net |

24,322 | 158,926 | 146,746 | 142,870 | 134,453 | 119,777 | ||||||||||||||||||

| Total assets |

33,473 | 218,718 | 200,442 | 185,989 | 189,688 | 165,207 | ||||||||||||||||||

| Current borrowings |

4,219 | 27,568 | 26,746 | 30,002 | 20,979 | 20,242 | ||||||||||||||||||

| Current portion of obligations under finance leases |

1,277 | 8,341 | 8,695 | 6,416 | 5,992 | 3,636 | ||||||||||||||||||

| Non-current borrowings |

3,171 | 20,719 | 18,758 | 15,884 | 42,066 | 37,246 | ||||||||||||||||||

| Obligations under finance leases, excluding current portion |

9,119 | 59,583 | 53,527 | 49,408 | 43,919 | 31,373 | ||||||||||||||||||

| Total equity |

9,572 | 62,543 | 54,976 | 49,624 | 44,493 | 42,451 | ||||||||||||||||||

| Number of shares (in million) |

10,088 | 10,088 | 9,818 | 9,818 | 9,818 | 9,818 | ||||||||||||||||||

Selected Operating Data

The operating data and the profit analysis and comparison below is calculated and disclosed in accordance with the statistical standards, which have been implemented by our Group since January 1, 2001. See “Glossary of Airline Industry Terms” at the front of this Annual Report for definitions of certain terms used herein.

| Year ended December 31, | ||||||||||||||||||||

| 2017 | 2016 | 2015 | 2014 | 2013 | ||||||||||||||||

| Capacity |

||||||||||||||||||||

| ASK (million) |

280,646 | 255,992 | 235,616 | 209,807 | 186,800 | |||||||||||||||

| ATK (million) |

38,332 | 34,980 | 32,205 | 28,454 | 24,952 | |||||||||||||||

| Kilometers flown (thousand) |

1,623,014 | 1,504,310 | 1,408,500 | 1,275,570 | 1,147,070 | |||||||||||||||

| Hours flown (thousand) |

2,567 | 2,375 | 2,238 | 2,026 | 1,829 | |||||||||||||||

| Number of landing and take-offs |

1,010,460 | 959,110 | 936,750 | 884,070 | 809,870 | |||||||||||||||

| Traffic |

||||||||||||||||||||

| RPK (million) |

230,697 | 206,106 | 189,588 | 166,629 | 148,417 | |||||||||||||||

| RTK (million) |

27,321 | 24,387 | 22,388 | 19,780 | 17,469 | |||||||||||||||

| Passengers carried (thousand) |

126,299 | 114,619 | 109,422 | 100,919 | 91,791 | |||||||||||||||

| Cargo and mail carried (tons) |

1,672,162 | 1,612,550 | 1,511,550 | 1,433,250 | 1,276,350 | |||||||||||||||

| Load Factors |

||||||||||||||||||||

| Passenger load factor (RPK/ASK) (%) |

82.2 | 80.5 | 80.5 | 79.4 | 79.4 | |||||||||||||||

| Overall load factor (RTK/ATK) (%) |

71.3 | 69.7 | 69.5 | 69.5 | 70.0 | |||||||||||||||

| Yield |

||||||||||||||||||||

| Yield per RPK (RMB) |

0.49 | 0.50 | 0.53 | 0.58 | 0.59 | |||||||||||||||

| Yield per RFTK (RMB) |

1.30 | 1.16 | 1.21 | 1.42 | 1.48 | |||||||||||||||

| Yield per RTK (RMB) |

4.46 | 4.50 | 4.78 | 5.27 | 5.42 | |||||||||||||||

| Fleet |

||||||||||||||||||||

| - Boeing |

407 | 372 | 351 | 311 | 282 | |||||||||||||||

| - Airbus |

321 | 304 | 290 | 276 | 253 | |||||||||||||||

| - Others |

26 | 26 | 26 | 25 | 26 | |||||||||||||||

| Total aircraft in service at period end |

754 | 702 | 667 | 612 | 561 | |||||||||||||||

| Average daily utilization rate (hours per day) |

9.79 | 9.53 | 9.6 | 9.6 | 9.6 | |||||||||||||||

6

Table of Contents

Exchange Rate Information

The following table sets forth certain information concerning exchange rates, based on the noon buying rates in New York City for cable transfers in foreign currencies, as certified for customs purposes by the Federal Reserve Bank of New York (the “Noon Buying Rate”), between Renminbi and U.S. dollars for the five most recent financial years.

| Renminbi per U.S. Exchange Rate (1) | ||||||||||||||||

| Period |

Average(2) | Low | High | Period—end | ||||||||||||

| Exchange Rate |

||||||||||||||||

| 2013 |

6.1412 | 6.0537 | 6.2213 | 6.0537 | ||||||||||||

| 2014 |

6.1704 | 6.0402 | 6.2591 | 6.2046 | ||||||||||||

| 2015 |

6.2869 | 6.1870 | 6.4896 | 6.4778 | ||||||||||||

| 2016 |

6.6400 | 6.4480 | 6.9580 | 6.9430 | ||||||||||||

| 2017 |

6.7569 | 6.4773 | 6.9575 | 6.5063 | ||||||||||||

| October |

6.6254 | 6.5712 | 6.6533 | 6.6328 | ||||||||||||

| November |

6.6200 | 6.5967 | 6.6385 | 6.6090 | ||||||||||||

| December |

6.5932 | 6.5063 | 6.6210 | 6.5063 | ||||||||||||

| 2018 |

||||||||||||||||

| January |

6.4233 | 6.8360 | 6.9575 | 6.2841 | ||||||||||||

| February |

6.3183 | 6.2649 | 6.3471 | 6.3280 | ||||||||||||

| March |

6.3174 | 6.2685 | 6.3565 | 6.2726 | ||||||||||||

| April (through April 25, 2018) |

6.2912 | 6.2655 | 6.3229 | 6.3066 | ||||||||||||

| (1) | Source: The source of the exchange rate is the H.10 statistical release of the Federal Reserve Board. |

| (2) | The source of annual averages is the G.5A statistical release of the Federal Reserve Board. The source of monthly averages is the G.5 statistical release of the Federal Reserve Board. |

| B. | CAPITALIZATION AND INDEBTEDNESS |

Not applicable.

| C. | REASONS FOR THE OFFER AND USE OF PROCEEDS |

Not applicable.

| D. | RISK FACTORS |

Risks Relating to our Business

We are indirectly majority owned by the Chinese government, which may exert influence in a manner that may conflict with the interests of holders of ADRs, H Shares and A Shares.

Major Chinese airlines are wholly- or majority-owned either by the Chinese government or by provincial or municipal governments in China. CSAH, an entity wholly-owned by the Chinese government, directly and indirectly holds and exercises the rights of ownership of 50.65% of the equity of our Company. The interests of the Chinese government in our Company and in other Chinese airlines may conflict with the interests of the holders of the ADRs, H Shares and A Shares. The public policy considerations of the Chinese government in regulating the Chinese commercial aviation industry may also conflict with its indirect ownership interest in our Company. In addition, our Company may accept further capital injection from CSAH through non-public subscriptions, which may have dilutive impact for other holders of ADRs, H Shares and A Shares.

7

Table of Contents

Due to high degree of operating leverage and high fixed costs, a decrease in revenue of our Group could result in a disproportionately higher decrease in our profit for the year. The results of our operations are also significantly exposed to fluctuations in foreign exchange rates.

The airline industry is generally characterized by a high degree of operating leverage. In addition, due to high fixed costs, the expenses relating to the operation of any flight do not vary proportionately with the number of passengers carried, while revenues generated from a flight are directly related to the number of passengers carried and the fare structure of such flight. Accordingly, a decrease in revenues could result in a disproportionately higher decrease in our profit for the year. Moreover, as we have substantial obligations denominated in foreign currencies, our results of operations are significantly affected by fluctuations in foreign exchange rates, particularly by fluctuations in the Renminbi-U.S. dollar exchange rate. Our net exchange loss of RMB3,276 million and net exchange gain of RMB1,801 million was recorded in 2016 and 2017, respectively, primarily due to the translation of balances of borrowings and obligations under finance lease which are denominated in USD.

We have significant committed capital expenditures in the next three years, and may face challenges and difficulties as it seeks to maintain liquidity.

We have a substantial amount of debt, lease and other obligations, and will continue to have a substantial amount of debt, lease and other obligations in the future. As of December 31, 2017, our current liabilities exceeded our current assets by RMB 51,693 million. We generated net cash inflow from operating activities of RMB23,764 million and RMB17,732 million for the years ended December 31, 2016 and 2017, respectively. However, our substantial indebtedness and other obligations may in the future negatively impact our liquidity. In addition, we have significant committed capital expenditures in the next three years, due to aircraft acquisitions. In 2017 and thereafter, the liquidity of our Group is primarily dependent on our ability to maintain adequate cash inflow from operations to meet our debt obligations as they fall due, and our ability to obtain adequate external financing to meet our committed future capital expenditures. If our operating cash flow is materially and adversely affected by factors such as increased competition, a significant decrease in demand for our services, or a significant increase in jet fuel prices, our liquidity would be materially and adversely affected. Moreover, we may not be able to meet our debt obligations as they fall due and commit future capital expenditures if certain assumptions about the availability of external financing on acceptable terms are inaccurate. If we are unable to obtain adequate financing for our capital requirements, our liquidity and operations would be materially and adversely affected.

As of December 31, 2017, we had banking facilities with several PRC commercial banks for providing loan finance up to approximately RMB181,922 million, of which approximately RMB142,239 million was unutilized. Our directors believe that sufficient financing will be available to our Group in 2018. However there can be no assurance that such loan financing will be available on terms acceptable to our Group or at all.

CSAH will continue to be our controlling shareholder, and our interests may conflict with those of our Group. CSAH and certain of its affiliates will continue to provide certain important services to our Group. Any disruption of the provision of services by CSAH or its affiliates could affect our operations and financial conditions.

CSAH will continue to be the controlling shareholder of our Company. CSAH and certain of its affiliates will continue to provide certain important services to our Group, including advertising services, provision of air ticket selling services, property management services, leasing of properties and financial services, and repair, overhaul and maintenance services on jet engines. The interests of CSAH may conflict with those of our Group. In addition, any disruption of the provision of services by CSAH’s affiliates or a default by CSAH of its obligations owed to our Group could affect our operations and financial conditions. In particular, as part of our cash management system, our Group periodically places certain amount of demand deposits after independent shareholders’ approval with SA Finance, a PRC authorized financial institution controlled by CSAH and an associate of our Company. We have taken certain measures to monitor the fund flows between us and SA Finance and the placement of funds by SA Finance. Such monitoring measures may help to enhance the safety of our deposits with SA Finance. In addition, we have received a letter of undertakings from CSAH dated March 31, 2009, in which, among other things, CSAH warranted that our deposits and loans with SA Finance were secure and that SA Finance would continue to operate in strict compliance with the relevant rules and regulations. However, the deposits may be exposed to risks associated with the business of SA Finance over which our Group does not have control. As of December 31, 2016 and 2017, we had deposits of RMB3,759 million and RMB6,095 million, respectively, with SA Finance.

8

Table of Contents

Both international and domestic economic conditions and Chinese government’s macroeconomic controls affect the demand for air travel, which will in turn cause volatility to our business and results of our operations.

As a result of the discretionary nature of air travel, the airline industry has been cyclical and particularly sensitive to changes in economic conditions. During periods of unfavorable or volatile economic conditions in the global economy or when global or regional economic conditions are affected by political events, such as the United Kingdom’s exit from the European Union (“EU”) and the trade policies between China and the U.S., demand for air travel can be impacted as business and leisure travelers choose not to travel, seek alternative forms of transportation for short trips or conduct business through videoconferencing. If unfavorable economic conditions occur, particularly for an extended period, our business, financial condition and results of operations may be adversely affected.

Following a referendum in June 2016 in which voters in the U.K. approved an exit from the EU, the U.K. government has initiated a process to leave the EU (often referred to as Brexit) and begun negotiating the terms of the U.K.’s future relationship with the EU. The airline industry faces substantial uncertainty regarding the impact of the exit of the U.K. from the EU. Adverse consequences such as deterioration in economic conditions, volatility in currency exchange rates or adverse changes in regulation of the airline industry or bilateral agreements governing air travel could have a negative impact on our operations, financial condition and results of operations.

On March 8, 2018, the U.S. President Donald Trump proposed a further 25% tariffs, the equivalent of $50 billion on Chinese goods. In response, on April 4, 2018, China released a tariff list of 25% on $50 billion’s US imports, including soybeans, automobiles and aeroplanes. On April 6, 2018, Trump reiterated that by considering adding a further $100 billion in tariffs on goods imported from China, and the Chinese Ministry of Commerce and the Foreign Affairs indicated that they would also adopt new measures. There is no guarantee that more measures will be introduced, and if these trade policies come into force and the scope of them is further expanded, the volume of China-U.S. import and export trade would drop significantly, which will lead to deterioration in economic conditions of both countries and decrease of business and official activities between both countries. Demand for air travel as well as cargo and mail volume can be impacted.

Chinese macroeconomic controls, such as financing adjustments, credit adjustments, taxation policies, price controls and exchange rate policies would also present unexpected changes to the aviation industry. As a result, the changing economic situation and Chinese macroeconomic controls may cause volatility to our business and results of our operations.

We could be adversely affected by an outbreak of a disease or large scale natural disasters that affect travel behavior.

The outbreak of the H1N1 swine flu in March 2009 has had an adverse impact on the aviation industry globally (including our Group). The spread of the swine flu adversely affected our international routes operations in 2009. A future outbreak of an infectious disease or any other serious public health concerns in Asia and elsewhere could have a material adverse effect on our business, financial condition and results of operations.

In 2011, a number of large-scale natural disasters occurred globally, such as the nuclear meltdown in Japan caused by earthquakes and subsequent tsunami, the hurricane on the East Coast of the United States, the flooding in Thailand and the typhoon in the Philippines. Disasters such as these can affect the aviation industry and our Group by reducing revenues and impacting travel behavior.

Lack of adequate documentation for land use rights and ownership of buildings subjects us to challenges and claims by third parties with respect to our Company’s use of such land and buildings.

Although systems for registration and transfer of land use rights and related real property interests in China have been implemented, such systems do not yet comprehensively account for all land and related property interests. We leased certain properties and buildings from CSAH which are located in Guangzhou, Haikou and other PRC cities. However, CSAH lacks adequate documentation evidencing CSAH’s rights to such land and buildings, and, as a result, the lease agreements between CSAH and our Company for such land has not been registered with the relevant authorities. As a result, such lease agreements may not be enforceable. Lack of adequate documentation for land use rights and ownership of buildings subjects our Company to challenges and claims by third parties with respect to our Company’s use of such land and buildings.

As of the date of this Annual Report, we had been occupying all of the land and buildings described above without challenge or claim by third parties. However, if any challenges to the property ownership or other claims are successful, our operation and business may be materially adversely affected. CSAH has agreed to indemnify us against any loss or damage caused by or arising from any challenge of, or interference with, our Company’s right to use certain land and buildings.

9

Table of Contents

Any discontinuity or disruption in the direct flight arrangement between Taiwan and Mainland China may negatively affect our results.

The policy restraint on direct flights between Taiwan and Mainland China has been further loosened in the past few years but there has been no further negotiation on the expansion of such arrangement between Taiwan and Mainland China since mid-2016. As of April 26, 2018, there were 78 cross-Strait direct passenger flights per week. Our Company was the first Chinese carrier to operate non-stop flights from Mainland China to Taiwan and as a result has benefited from the operation of such flights. However, given the cross-Strait flight arrangement is subject to the political relationship between Taiwan and Mainland China, any deterioration in such political relationship may cause the discontinuity or disruption in the flight arrangement, and therefore may have a material adverse impact on our results.

Terrorist attacks or the fear of such attacks, even if not made directly on the airline industry, could adversely affect our Company and the airline industry as a whole. The travel industry continues to face on-going security concerns and cost burdens.

The aviation industry as a whole has been beset with high-profile terrorist attacks, most notably the attack on September 11, 2001 in the United States. Terrorist attacks could also affect the aviation industry in China. Airlines in China have experienced several incidents of terrorist attacks or threats recently. For example, on March 7, 2008, on a China Southern Airlines flight boarding in Urumqi, crew members discovered a terrorist suspect. On July 14, 2010, a passenger jet en route from Urumqi to Guangzhou was forced to make an emergency landing after receiving an anonymous call claiming there was a bomb on the aircraft. On June 29, 2012, there was an attempted hijacking on a passenger flight operated by Tianjin Airlines between Hotan and Urumqi in China’s Xinjiang region. CAAC has enhanced security measures, but the effectiveness of such measures cannot be ascertained. Additional terrorist attacks, even if not made directly on the airline industry, or the fear of or the precautions taken in anticipation of such attacks (including elevated threat warnings or selective cancellation or redirection of flights) could materially and adversely affect our Company and the aviation industry. Potential impacts that terrorist attacks could have on our Company include substantial flight disruption costs caused by grounding of fleet, significant increase in security costs and associated passenger inconvenience, increased insurance costs, substantially higher ticket refunds and significant decrease in traffic measured in revenue passenger kilometers. Additionally, increasingly strict security measures make air travel a hassle in the eyes of some consumers. These factors can have an uncertain impact on the development of the aviation industry.

We may suffer losses in the event of an accident involving our aircraft or the aircraft of any other airline.

An accident involving one of our aircraft could require repair or replacement of a damaged aircraft, and result in our consequential temporary or permanent loss from service and/or significant liability to injured passengers and others. Although we believe that we currently maintain liability insurance in amounts and of the types generally consistent with industry practice, the amounts of such coverage may not be adequate to fully cover the costs related to the accident or incident, which could result in harm to our results of operations and financial condition. In addition, any aircraft accident, even if fully insured, could cause a public perception that we are not as safe or reliable as other airlines, which would harm our competitive position and result in a decrease in our operating revenues. Moreover, a major accident involving the aircraft of any of our competitors may cause demand for air travel to decrease in general, which would adversely affect our results of operations and financial condition.

We could be adversely affected by a failure or disruption of our computer, communications or other technology systems.

We are increasingly dependent on technology to operate our business. In particular, to enhance our management of flight operations, our Group launched the computerized flight operations control system in May 1999. The system utilizes advanced computer and telecommunications technology to manage our flights on a centralized, real-time basis. We believe that the system will enhance the efficiency of flight schedule, increase the utilization of aircraft and improve the coordination of our aircraft maintenance and ground servicing functions. However, the computer and communications systems on which we rely could be disrupted due to various factors, some of which are beyond our control, including natural disasters, power failures, terrorist attacks, equipment failures, software failures and computer viruses and hackers. We have taken certain steps to reduce the risk of some of these potential disruptions. There can be no assurance, however, that the measures we have taken are adequate to prevent or remedy disruptions or failures of those systems. Any substantial or repeated failure of those systems could adversely affect our operations and customer services, result in the loss of important data, loss of revenues, and increased costs, and generally harm our business. Moreover, a failure of certain of our vital systems could limit our ability to operate our flights for an extended period of time, which would have a material adverse effect on our operations and our business.

10

Table of Contents

We may lose investor confidence in the reliability of our financial statements if we fail to achieve and maintain effective internal control over financial reporting, which in turn could harm our business and negatively impact the trading prices of our ADRs, H Shares or A Shares.

The United States Securities and Exchange Commission, or the SEC, as required by Section 404 of the Sarbanes-Oxley Act of 2002, adopted rules requiring every public company in the United States to include a management report on such company’s internal control over financial reporting in its annual report, which contains management’s assessment of the effectiveness of the company’s internal control over financial reporting. In addition, our Company’s independent registered public accounting firm is required to report on the effectiveness of our Company’s internal control over financial reporting.

Since 2011, pursuant to the Basic Standard for Enterprise Internal Control jointly issued by the Ministry of Finance, China Securities Regulatory Commission (“CSRC”) and other three PRC authorities on May 22, 2008, and its application guidelines and other relevant regulations issued subsequently (collectively, “PRC internal control requirements”) , our Company has carried out a self-assessment of the effectiveness of its internal control and issue a self-assessment report annually in accordance with the PRC internal control requirements, and our Company’s auditor for our PRC GAAP financial statements (the “PRC Auditor”) is required to report on the effectiveness of our Company’s internal control over financial reporting.

However, our independent registered public accounting firm or PRC Auditor may not be satisfied with our internal controls, the level at which our controls are documented, designed, operated and reviewed. Our independent registered public accounting firm or PRC Auditor may also interpret the requirements, rules and regulations differently, and reach a different conclusion regarding the effectiveness of our internal control over financial reporting. Although our management have concluded that our internal control over financial reporting as of December 31, 2017 was effective, we may discover deficiencies in the course of our future evaluation of our internal control over financial reporting and may be unable to remediate such deficiencies in a timely manner. If we fail to maintain the adequacy of our internal control over financial reporting, we may not be able to conclude that we have effective internal control over financial reporting on an ongoing basis, as required under the above mentioned rules and regulations. Moreover, effective internal control is necessary for us to produce reliable financial reports and is important to prevent fraud. As a result, our failure to achieve and maintain effective internal control over financial reporting could result in the loss of investor confidence in the reliability of our financial statements, which in turn could harm our business and negatively impact the trading prices of our ADRs, H Shares or A Shares.

Our Company could be classified as a passive foreign investment company by the United States Internal Revenue Service and may therefore be subject to adverse tax impact.

Depending upon the relative values of our passive assets and income as compared to our total assets and income each taxable year, we could be classified as a passive foreign investment company, or PFIC, by the United States Internal Revenue Service, or IRS, for U.S. federal income tax purposes. Our Company believes that we were not a PFIC for the taxable year 2017. However, there can be no assurance that we will not be a PFIC for the taxable year 2018 and/or later taxable years, as PFIC status is re-tested each year and depends on the facts in such year.

Our Company will be classified as a PFIC in any taxable year if either: (1) the average value during the taxable year of our assets that produce passive income, or are held for the production of passive income, is at least 50% of the average value of our total assets for such taxable year (the “Asset Test”) or (2) 75% or more of our gross income for the taxable year is passive income (such as certain dividends, interest or royalties) (the “Income Test”). For purposes of the Asset Test: (1) any cash, cash equivalents, and cash invested in short-term, interest bearing, debt instruments, or bank deposits that is readily convertible into cash, will generally count as producing passive income or as being held for the production of passive income and (2) the average values of our Company’s passive and total assets is calculated based on our market capitalization.

If we were a PFIC, we would generally be subject to additional taxes and interest charges on certain “excess distributions” our Company makes regardless of whether we continue to be a PFIC in the year in which you receive an “excess distribution”. An “excess distribution” would be either (1) the excess amount of a distribution with respect to ADRs during a taxable year in which distributions to you exceed 125% of the average annual distributions to you over the preceding three taxable years or, if shorter, your holding period for the ADRs, or (2) 100% of the gain from the disposition of ADRs. For more information on the United States federal income tax consequences to you that would result from our classification as a PFIC, please see Item 10, “Taxation - United States Federal Income Taxation - U.S. Holders - Passive Foreign Investment Company”.

11

Table of Contents

We may be unable to retain key management personnel.

We are dependent on the experience and industry knowledge of our key management employees, and there can be no assurance that we will be able to retain them. Any inability to retain our key management employees, or attract and retain additional qualified management employees, could have a negative impact on us.

Risks Relating to the Chinese Commercial Aviation Industry

Our business is subject to extensive government regulations, and there can be no assurance as to the equal treatment of all airlines under those regulations.

Our ability to implement our business strategy will continue to be affected by regulations and policies issued or implemented by relevant government agencies, particularly CAAC, which encompasses substantially all aspects of the Chinese commercial aviation industry, such as the approval of route allocation, the administration of certain airport operations and air traffic control. Such regulations and policies limit the flexibility of our Group to respond to market conditions, competition or changes in our cost structure. The implementation of specific government policies could from time to time adversely affect our operations.

Our results may be negatively impacted by the fluctuation in domestic prices for jet fuel, and we would be adversely affected by disruptions in the supply of fuel.

The availability and cost of jet fuel have a significant impact on our results of operations. Our jet fuel cost for 2017 accounted for 50.64% of our flight operations expenses. All of the domestic jet fuel requirements of Chinese airlines (other than at the Shenzhen, Sanya, Haikou, Shanghai Pudong) must be purchased from the exclusive providers, CAOSC and Bluesky Oil Supplies Company, which are supervised by the CAAC. Chinese airlines may also purchase jet fuel at the Shenzhen, Sanya, Haikou, Shanghai Pudong from Sino-foreign joint venture in which CAOSC is a joint venture partner. Jet fuel obtained from the CAOSC’s regional branches is purchased at uniform prices throughout China that are determined and adjusted by the CAOSC from time to time with the approval of the CAAC and the pricing department of the NDRC based on market conditions and other factors. As a result, the costs of transportation and storage of jet fuel in all regions of China are spread among all domestic airlines.

Domestic price for jet fuel has experienced fluctuations in the past few years. Our profit for the year may suffer from an unexpected change in the fuel surcharge collection policies and other factors beyond our control. For more information on the jet fuel prices, please see “Item 4, Information on our Company - Business Overview - Jet Fuel” section below for further discussion.

In summary, given the constant fluctuation of volatile fuel price, no assurance can be given that our operation and financial results will not be negatively impacted by the fluctuation in domestic prices for jet fuel.

In addition, China has experienced jet fuel shortages. On some rare occasions prior to 1993, our Group had to delay or even cancel flights. Although such shortages have not materially affected our operations since 1993, there can be no assurance that such a shortage will not occur in the future. If such a shortage occurs in the future to the extent that our Group has to delay or cancel flights due to fuel shortage, our operational reputation among passengers as well as our operations may suffer.

In 2017, a reasonable possible increase or decrease of 10% in average jet fuel price with volume of fuel consumed and all other variables held constant, would have increased or decreased our annual fuel costs by approximately RMB3,190 million. Accordingly, even if the jet fuel supply remains stable, increases in jet fuel prices will nevertheless adversely impact our financial results.

Our profit for the year may suffer from an unexpected volatility caused by any fluctuation in the level of fuel surcharges.

The level of fuel surcharges, which is regulated by Chinese government, affects domestic customers’ air travel demand as well as our ability to generate profits. On January 14, 2009, the NDRC and the CAAC jointly announced that the collection of passenger fuel surcharge for domestic routes should be suspended from January 15, 2009 onwards. Subsequently, in response to the increase in international fuel prices, the NDRC and CAAC issued a notice on November 11, 2009 to introduce a new pricing mechanism of fuel surcharge that links it with airlines’ jet fuel costs, which was further adjusted subsequently. On October 14, 2011, the NDRC and the CAAC issued a notice to adjust such pricing mechanism. As a result of this adjustment, the maximum rates for fuel surcharge can be adjusted according to the pricing mechanism of fuel surcharge, if the aggregated change in jet fuel costs exceeds RMB250 per ton. Due to the decrease in the jet fuel cost, the fuel surcharge has been suspended since February 5, 2015. On March 24, 2015, NDRC elected to revise the base price of jet fuel which is used to calculate the maximum rate for fuel surcharge. We cannot guarantee that fuel surcharges would not be adjusted further in the future or adjusted in our favour. If fuel surcharges are not adjusted in correspondence to the increase in jet fuel, our profit for the year may be materially adversely affected.

12

Table of Contents

Our results of operations are subject to seasonality.

Our operating revenue is substantially dependent on the passenger and cargo traffic volume carried, which is subject to seasonal and other changes in traffic patterns, the availability of appropriate time slots for our flights and alternative routes, the degree of competition from other airlines and alternate means of transportation, as well as other factors that may influence passenger travel demand and cargo and mail volume. In particular, our airline revenue is generally higher in the second half of the year than in the first half of the year. As a result, our results may fluctuate from season to season.

Our operations may be adversely affected by insufficient aviation infrastructure in Chinese commercial aviation industry.

The rapid increase in air traffic volume in China in recent years has put pressure on many components of the Chinese commercial aviation industry, including China’s air traffic control system, the availability of qualified flight personnel and airport facilities. Airlines, such as our Group, which have route networks that emphasize short- to medium-haul routes, are generally more affected by insufficient aviation infrastructure in terms of on-time performance and high operating costs due to fuel inefficiencies resulting from the relatively short segments flown, as well as the relatively high proportion of time on the ground during turnaround. All of these factors may adversely affect the perception of the service provided by an airline and, consequently, the airline’s operating results. In recent years, the CAAC has placed increasing emphasis on the safety of Chinese airline operations and has implemented measures aimed at improving the safety record of the industry. The ability of our Group to increase utilization rates and to provide safe and efficient air transportation in the future will depend in part on factors such as the improvement of national air traffic control and navigation systems and ground control operations at Chinese airports, factors which are beyond the control of our Group.

We face increasingly intense competition both in domestic aviation industry and in the international market, as well as from alternative means of transportation.

The CAAC’s extensive regulation of the Chinese commercial aviation industry has had the effect of managing competition among Chinese airlines. Nevertheless, competition has become increasingly intense in recent years due to a number of factors, including relaxation of certain regulations by the CAAC and an increase in the capacity, routes and flights of Chinese airlines. Competition in the Chinese commercial aviation industry has led to widespread price-cutting practices that do not in all respects comply with applicable regulations. Until the interpretation of CAAC regulations limiting such price-cutting has been finalized and strictly enforced, discounted tickets from competitors will continue to have an adverse effect on our sales.

We face varying degrees of competition on our regional routes from certain Chinese airlines and Cathay Pacific, Cathay Dragon and Air Macau, and on our international routes, primarily from non-Chinese airlines, most of which have significantly longer operating histories, substantially greater financial and technological resources and greater name recognition than our Group. In addition, the public’s perception of the safety and service records of Chinese airlines could adversely affect our ability to compete against our regional and international competitors. Many of our international competitors have larger sales networks and participate in reservation systems that are more comprehensive and convenient than those of our Group, or engage in promotional activities, which may enhance their ability to attract international passengers.

Furthermore, for short-distance transportation, airplanes, trains and buses are alternatives to each other. Given the recent development of high-speed trains (as discussed below), the construction of nationwide high-speed railway network and the improvement of inter-city expressway network, the commercial aviation sector as a whole faces increasing competition from the alternative means of transportation such as railways and highways.

We expect to face substantial competition from the rapid development of the Chinese rail network.

The PRC government is aggressively implementing the expansion of its high-speed rail network. The mileage of new railway lines put into operation in 2017 reached 3,038 kilometers. In 2017, the Baoji-Lanzhou, Wuhan-Jiujiang, Xi’an-Chengdu and Shijiazhuang-Jinan railways commenced operation. Operation of Shijiazhuang-Jinan railway indicates that the “four horizontal and four vertical” high speed railway corridors have been built ahead of schedule. As of December 31, 2017, China’s railway traffic mileage has reached 127,000 kilometers, among which 25,000 kilometers are covered by high-speed railway. China’s high-speed railway traffic mileage accounts for 66.3% of the world’s total high-speed railway traffic mileage. According to the latest development goal of the China Railway Corporation, China’s railway traffic mileage will reach 175,000 kilometers by 2025, among which 38,000 kilometers are covered by high-speed railway. The operating results of the Company’s air routes which overlap with the high-speed railway corridors (especially air routes with a distance of less than 800 kilometers) will be affected in the future.

13

Table of Contents

Due to limitation on foreign ownership imposed by Chinese government policies, our Company may have limited access to the international equity capital markets.

Chinese government policies limit foreign ownership in Chinese airlines. Under these policies, the percentage ownership of our total outstanding ordinary shares held by investors in Hong Kong and any country outside China (“Foreign Investors”) may not in the aggregate exceed 49%. Currently, we estimate that 30.39% of the total outstanding ordinary shares of our Company are held by Foreign Investors. According to The Provisions on Domestic Investment in Civil Aviation Industry, effective on January 19, 2018, Chinese government has loosen up restrictions on state ownership of our total outstanding ordinary shares, which allows the percentage of state-owned shares to be under 50%. However, for so long as the limitation on foreign ownership is in force, we will have limited access to the international equity capital markets.

The European Emissions Trading Scheme may increase operational cost of our Group.

Starting on January 1, 2012, aviation sector has been included in the European Emissions Trading Scheme (ETS), EU’s mandatory cap-and-trade system for reduction of greenhouse gas emissions. Airline operators in the EU will receive tradable emission permits (aviation allowances) covering a certain level of their CO2 emissions per year for their flights operating to and from EU airports. If an airline fails to obtain free-of-charge emission permits from the EU, it will have to buy around EUR10 million (RMB100 million) worth of CO2 emissions allowances from other greener industries. Pursuant to this policy, the Chinese airlines having flight points in Europe undertake the same carbon emission reductions obligation as the European local airlines, which will result in a significant increase in the operating cost of Chinese airlines in Europe, including our Company, and further have an adverse impact on the results of operations and financial condition. In March 2011, a group representing China’s largest airlines sent a formal notice to the EU expressing strong opposition to non-member-state airlines’ inclusion in the EU’s Emissions Trading Scheme. Also, in early February 2012, CAAC issued instructions to various airlines announcing that without approval from the relevant government authorities, the major airlines are prohibited from joining the ETS and the transport airlines are also prohibited from raising the freight price or increasing fee items by adducing this reason. On November 12, 2012, EU announced to temporarily suspend the implementation of the ETS in the aviation sector in 2013 in order to forge a positive negotiation environment for all parties. In November 2014, CAAC issued a notification on the ETS. The notification provided that CAAC would not prohibit Chinese airlines to take part in the ETS if the relevant flights take off and land between the airports within the EU during 2012 and 2016. We operated few flights between airports within the EU since 2012. We expect we would operate few flights between airports within the EU in the future. Therefore, we submitted emissions report and pay the quota between 2012 and 2016 for our flights between airports within the EU. In April 2015, our Company had completed submission of emissions reports for the years 2012 to 2014 and fulfilled our obligations under the ETS. In 2016, our Company had finished year 2015 compliance cycle. On year 2017-2020 compliance cycle, our Company will be in compliance with the requirements of relevant PRC laws and the ETS. There can be no assurance that the new implementation proposal will not have negative impact on our financial condition and result of operation.

We may utilize fuel hedging arrangements which may result in losses.

While we have not entered into any fuel hedging transactions since the fourth quarter of 2008, we may in the future consider to hedge a portion of our future fuel requirements through various financial derivative instruments linked to certain fuel commodities to lock in fuel costs within a hedged price range. However, these hedging strategies may not always be effective and high fluctuations in aviation fuel prices exceeding the locked-in price ranges may result in losses. Significant declines in fuel prices may substantially increase the costs associated with our fuel hedging arrangements. In addition, where we seek to manage the risk of fuel price increases by using derivative contracts, we cannot assure you that, at any given point in time, our fuel hedging transactions will provide any particular level of protection against increased fuel costs.

Risks Relating to the PRC

We have significant exposure to foreign currency risk as part of our lease obligations and certain bank and other loans are denominated in foreign currencies. Due to rigid foreign exchange control by Chinese government, we may face difficulties in obtaining sufficient foreign exchange to pay dividends or satisfy our foreign exchange liabilities.

Under current Chinese foreign exchange regulations, the Renminbi is fully convertible for current account transactions, but is not freely convertible for capital account transactions. All foreign exchange transactions involving Renminbi must take place either through the People’s Bank of China or other institutions authorized to buy and sell foreign exchange or at a swap centre.

14

Table of Contents

We have significant exposure to foreign currency risk as substantially all of our obligations under leases, certain bank and other loans and operating lease commitment are denominated in foreign currencies, principally U.S. dollars, Euros and Japanese Yen. Depreciation or appreciation of the Renminbi against foreign currencies affects our results significantly because our foreign currency liabilities generally exceed our foreign currency assets. We are not able to hedge our foreign currency exposure effectively other than by retaining our foreign currency denominated earnings and receipts to the extent permitted by SAFE, or subject to certain restrictive conditions, entering into foreign exchange forward option contracts with authorized banks. However, SAFE may limit or eliminate our ability to purchase and retain foreign currencies in the future. In addition, foreign currency transactions under the capital account are still subject to limitations and require approvals from SAFE. This may affect our ability to obtain foreign exchange through debt or equity financing, including by means of loans or capital contributions. No assurance can be given that our Group will be able to obtain sufficient foreign exchange to pay dividends or satisfy our foreign exchange liabilities.

Our operations are subject to immature development of legal system in China. Lack of uniform interpretation and effective enforcement of laws and regulations may cause significant uncertainties to our operations.

Our Company and the major subsidiaries of our Group are organized under the laws of China. The Chinese legal system is based on written statutes and is a system, unlike common law systems, in which decided legal cases have little precedential value. Since 1979, the Chinese government has been developing a comprehensive system of commercial laws and considerable progress has been made in the promulgation of laws and regulations dealing with economic matters, such as corporate organization and governance, foreign investments, commerce, taxation and trade. These laws, regulations and legal requirements are relatively recent, and, like other laws, regulations and legal requirements applicable in China (including with respect to the commercial aviation industry), their interpretation and enforcement involve significant uncertainties.

The PRC tax law may have negative tax impact on holders of H Shares or ADRs of our Company, by requiring the imposition of a withholding tax on dividends paid by a Chinese company to a non-resident enterprise.

The current tax law generally provides for a withholding tax on dividends paid by a Chinese company to a non-resident enterprise at a rate of 10%.

Caishui Notice [2014] No. 81 provides that, “for dividends derived by Mainland individual investors from investing in H Shares listed on the Hong Kong Stock Exchange through Shanghai Hong Kong Stock Connect, H-Share companies shall apply to the China Securities Depository and Clearing Corporation Limited (CSDC). CSDC shall provide the list of Mainland individual investors to H-Share companies who shall withhold individual income tax at a tax rate of 20%. For Mainland securities investment funds investing in shares listed on the Hong Kong Stock Exchange through Shanghai Hong Kong Stock Connect, the above rules shall also apply and individual income tax shall be levied on dividends derived therefrom.”

Caishui Notice [2014] No. 81 further provides that, “dividends derived by Mainland enterprise investors from investing in shares listed on the Hong Kong Stock Exchange through Shanghai Hong Kong Stock Connect shall be included in their gross income and subject to enterprise income tax. For dividends derived by Mainland enterprises where the relevant H Shares have been continuously held for no less than 12 months, enterprise income tax may be exempt according to the tax law. H-Share companies listed on the Hong Kong Stock Exchange shall apply to CSDC to obtain the list of Mainland enterprise investors from CSDC. H-Share companies are not required to withhold income tax on dividends to Mainland enterprise investors which shall report the income and make the tax payment by themselvers.”

In addition, to date, relevant tax authorities have not collected capital gains tax on the gains realized upon the sale or other disposition of overseas shares in Chinese enterprise held by foreign individuals. If relevant tax authorities promulgate implementation rules on the taxation of capital gains realized by individuals upon the sale or other disposition of the shares, individual holders of the shares may be required to pay capital gains tax.

Our investors in the U.S. who rely on our auditor’s audit reports currently do not have the benefit of PCAOB oversight.

As a company registered with the U.S. Securities and Exchange Commission, or the SEC, and traded publicly in the United States, our independent registered public accounting firm is required by the laws of the United States to be registered with the Public Company Accounting Oversight Board, or the PCAOB, and undergo regular inspections by the PCAOB to assess its compliance with the laws of the United States and professional standards. The PCAOB, however, is currently unable to inspect a registered public accounting firm’s audit work relating to a company’s operations in China where the documentation of such audit work is located in China. Accordingly, our independent registered public accounting firm’s audit of our operations in China is not subject to the PCAOB inspection.

15

Table of Contents

The PCAOB has conducted inspections of independent registered public accounting firms outside of China and has at times identified deficiencies in the audit procedures and quality control procedures of those accounting firms. Such deficiencies may be addressed in those accounting firms’ future inspection process to improve their audit quality. Due to the lack of PCAOB inspections of audit work undertaken in China, our investors do not have the benefit of the regular evaluation by PCAOB of the audit works, audit procedures and quality control procedures of our independent registered public accounting firm.

If additional remedial measures are imposed against four PRC-based accounting firms, including our independent registered public accounting firm, in administrative proceedings brought by the SEC, it could result in our financial statements being determined to not be in compliance with the requirements of the Securities Exchange Act of 1934.

In December 2012, the SEC instituted administrative proceedings against four PRC-based accounting firms, including our independent registered public accounting firm, alleging that these firms had violated U.S. securities laws and the SEC’s rules and regulations thereunder by failing to provide to the SEC the firms’ work papers related to their audits of certain PRC-based companies that are publicly traded in the United States. On January 22, 2014, an initial administrative law decision was issued, which determined that the four PRC-based accounting firms should be censured and barred from practicing before the SEC for a period of six months. The four PRC-based accounting firms appealed the initial administrative law decision to the SEC. The initial law decision is neither final nor legally effective unless and until it is endorsed by the full SEC. In February 2015, each of the four PRC-based accounting firms agreed to a censure and to pay a fine to the SEC to settle the dispute and avoid suspension of their ability to practice before the SEC. The settlement requires the firms to follow detailed procedures to provide the SEC with access to PRC-based firms’ audit documents via the CSRC.

We were not and are not the subject of any SEC investigations nor are we involved in the proceedings brought by the SEC against the accounting firms. If the firms do not follow these procedures or if there is a failure in the process between the SEC and the CSRC, the SEC could impose penalties such as suspensions or it could restart the administrative proceedings. If the accounting firms including our independent registered public accounting firm were denied, temporarily or permanently, the ability to practice before the SEC, and we are unable to find timely another registered public accounting firm which can audit and issue a report on our financial statements, our financial statements could be determined to not be in compliance with the requirements for financial statements of public companies registered under the Securities Exchange Act of 1934, as amended, or the Exchange Act. Such a determination could ultimately lead to the delisting of our common stock from the NYSE for CSA’s case or deregistration from the SEC, or both, which would substantially reduce or effectively terminate the trading of our common stock in the United States.

| ITEM 4. | INFORMATION ON THE COMPANY |

| A. | HISTORY AND DEVELOPMENT OF OUR COMPANY |

We were incorporated under PRC laws on March 25, 1995 as a joint stock company with limited liability under the name of China Southern Airlines Company Limited. The address of our principal place of business is 278 Ji Chang Road, Guangzhou, People’s Republic of China 510405. Our telephone number is +86 20 8612 4462 and our website is www.csair.com.

In July 1997, we issued 1,174,178,000 H Shares, par value RMB1.00 per share, and completed the listing of the H Shares on the Stock Exchange of Hong Kong Limited (the “Hong Kong Stock Exchange”) and the ADRs representing our H shares on the New York Stock Exchange.

On March 13, 2003, we obtained an approval certificate from the Ministry of Commerce to change to a permanent limited company with foreign investments and on October 17, 2003 obtained a business license for our new status, as a permanent limited company with foreign investments issued by the State Administration of Industry and Commerce of the People’s Republic of China.

In July 2003, we issued 1,000,000,000 A Shares, par value RMB1.00 per share, and completed the listing of the A shares on the Shanghai Stock Exchange.

Pursuant to a sale and purchase agreement dated November 12, 2004 between our Company, CSAH, China Northern Airlines (“CNA”) and Xinjiang Airlines (“XJA”), which was approved by our shareholders in an extraordinary general meeting held on December 31, 2004, we acquired the airline operations and certain related assets of CNA and XJA with effect from December 31, 2004 at a total consideration of RMB1,959 million.

16

Table of Contents

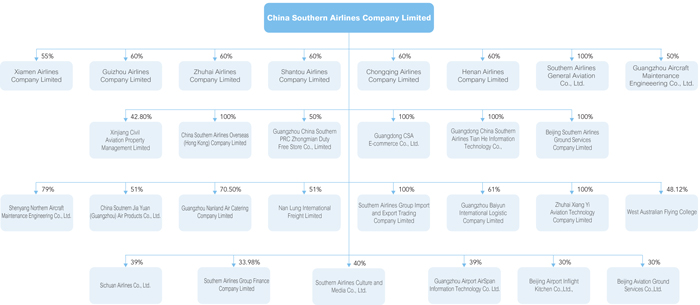

On May 30, 2007, we, together with an independent third party, established Chongqing Airlines Company Limited (“Chongqing Airlines”). As of December 31, 2012, our Company had transferred four aircraft to Chongqing Airlines as capital contribution. We own a total of 60% equity interest in Chongqing Airlines.

On August 14, 2007, we acquired a 51% equity interest in Nan Lung International Freight Limited beneficially owned by and registered in the name of Nan Lung Travel & Express (Hong Kong) Limited, and a 100% equity interest in China Southern Airlines Group Air Catering Company Limited, both a wholly owned subsidiary of CSAH, for a total consideration of RMB112 million.

In December 2008, we acquired a 26% equity interest in China Southern West Australian Flying College Pty Ltd. (“Flying College”) from CSAH, and Flying College became a 91% owned subsidiary of our Company.

In June 2009, we acquired a 50% equity interest in Beijing Southern Airlines Ground Services Company Limited (“Beijing Ground Service”) from the other shareholder, and Beijing Ground Service became a wholly-owned subsidiary of our Company.

On September 28, 2009, we entered into an agreement with CSAH to sell our 50% equity interest in MTU Maintenance Zhuhai Co., Ltd (“Zhuhai MTU”), a jointly controlled entity of our Company, to CSAH at a consideration of RMB 1,607,850,000. The transfer was completed in February 2010.

On June 2, 2010, a third party company injected capital to Flying College, which diluted our Company’s interest in Flying College from 91% to 48.12%. Flying College became a jointly controlled entity of our Company since then. The retained non-controlling equity interest in Flying College is re-measured to our fair value at the date when control was lost and a gain on deemed disposal of a subsidiary of RMB17 million was recorded in 2010.

In December 2010, we entered into an agreement with Xiamen Jianfa Group Co., Ltd. and Hebei Aviation Investment Group Corporation Limited (“Hebei Investment”), pursuant to which Hebei Investment agreed to inject a cash capital of RMB1,460 million into Xiamen Airlines Company Limited (“Xiamen Airlines”). In March 2011, the capital injection was received in full and our Company’s equity interest in Xiamen Airlines was diluted from 60% to 51%. Xiamen Airlines remains a subsidiary of our Company.

On June 29, 2012, Xiamen Airlines, a subsidiary of our Company and Southern Airlines Culture and Media Co., Ltd. (“SACM”) entered into an agreement, pursuant to which Xiamen Airlines agreed to sell and SACM agreed to purchase 51% equity interests in Xiamen Airlines Media Co., Ltd.(“XAMC”), at a consideration of approximately RMB43.12 million. Immediate prior to the transaction, XAMC was wholly owned by Xiamen Airlines and primarily engaged in providing advertising, corporate branding, publicity and exhibition services and was responsible for the overall brand building and publicity of Xiamen Airlines.

On September 24, 2012, we entered into a joint venture agreement with Henan Civil Aviation Development and Investment Co., Ltd. (“Henan Aviation Investment”) for the establishment of China Southern Airlines Henan Airlines Company Limited (“Henan Airlines”), a joint venture company with a total registered capital of RMB6 billion, which will be owned as 60% and 40% by our Company and Henan Aviation Investment, respectively. On September 28, 2013, Henan Airlines was established.

On October 13, 2014, Xiamen Airlines and Hebei Airlines Investment Group Company Limited (the “Hebei Airlines Investment”) entered into an agreement, pursuant to which Hebei Airlines Investment agreed to sell and Xiamen Airlines agreed to purchase 95.4% equity interests in Hebei Airlines at the consideration of RMB680 million. The acquisition was completed in December 2014.

On July 14, 2015, we and Xiamen Jianfa entered into an agreement, pursuant to which Xiamen Jianfa agreed to sell and we agreed to purchase 4% equity interests in Xiamen Airlines at the consideration of RMB586,666,670. The acquisition was completed in December 2015.

On February 2, 2016, we and CSAH entered into an agreement, pursuant to which CSAH agreed to sell and we agreed to purchase 100% equity interests in Southern Airlines (Group) Import And Export Trading Co. Ltd. at the consideration of RMB400,570,400. The acquisition was completed in August 2016.

On March 27, 2017, according to the authorisation under the general mandate approved by the 2015 annual general meeting and as approved by the Board, we entered into the Share Subscription Agreement with American Airlines, pursuant to which American Airlines has agreed to subscribe for 270,606,272 new H Shares of the Company (the “Subscription”), at the consideration of HK$1,553.28 million, representing a subscription price of HK$5.74 per share. The closing price of the H Shares as at the date of the Share Subscription Agreement is HK$5.49. The Subscription was completed on 10 August 2017.

17

Table of Contents

On May 18, 2017, we entered into the Joint Venture Agreement regarding Guangzhou Nanland Air Catering Company Limited with Hong Kong Sharpland Investments Ltd., Servair S.A and Hong Kong Ginkgo Group Company Limited, pursuant to which our Company made contribution into Guangzhou Nanland Air Catering Co., Ltd. in cash with an amount of RMB76,206,300 and by contributing the equity interests in a subsidiary with a valuation of RMB513,727,300. After the capital contribution, our Company held 70.5% equity interests in Guangzhou Nanland Air Catering Co., Ltd..