As filed with the Securities and Exchange Commission on July 9, 2020

Registration No. 333-238863

==================================================================================

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM N-14

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

PRE-EFFECTIVE AMENDMENT NO. 1

POST-EFFECTIVE AMENDMENT NO.____

MADISON FUNDS

(Exact Name of Registrant as Specified in Charter)

c/o Madison Asset Management, LLC

550 Science Drive, Madison, Wisconsin 53711

(Address of Principal Executive Offices)

(608) 274-0300

(Registrant's Telephone Number)

Steven J. Fredricks

Chief Legal Officer and Chief Compliance Officer

Madison Asset Management, LLC

550 Science Drive

Madison, Wisconsin 53711

(Name and Address of Agent for Service)

With copies to:

Pamela M. Krill, Esq.

Godfrey & Kahn, S.C.

One East Main Street, Suite 500

Madison, Wisconsin 53703

Approximate Date of Proposed Public Offering: As soon as practicable after the Registration Statement becomes effective under the Securities Act of 1933.

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such dates as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

No filing fee is due because the Registrant has previously registered an indefinite number of shares under the Securities Act of 1933 pursuant to Section 24(f) under the Investment Company Act of 1940.

Title of Securities Being Registered.............................................Class A and Y Shares of the Madison Dividend

Income Fund, no par value per share, of the Registrant

==================================================================================

MADISON FUNDS®

LARGE CAP VALUE FUND

550 Science Drive

Madison, Wisconsin 53711

July 9, 2020

Dear Shareholder:

The Board of Trustees of Madison Funds (the “Trust”) is asking shareholders of the Madison Large Cap Value Fund (the “Acquired Fund”), a series of the Trust, to approve the acquisition of the assets and liabilities of the Acquired Fund by the Madison Dividend Income Fund (the “Acquiring Fund” which, together with the Acquired Fund, are collectively referred to as the “Funds”), also a series of the Trust, pursuant to the terms and conditions of an agreement and plan of reorganization and liquidation (the “Reorganization”). For this purpose, you are invited to a Special Meeting of Shareholders of the Acquired Fund (the “Meeting”) to be held on September 2, 2020.

The Reorganization is described in more detail in the attached Combined Proxy Statement/Prospectus. You should review the Combined Proxy Statement/Prospectus carefully and retain it for future reference. If the shareholders of the Acquired Fund approve the Reorganization, it is expected to be completed on or about September 14, 2020.

The Acquired Fund has similar investment objectives, investment strategies and investment policies as the Acquiring Fund. In addition, while the Acquiring Fund has a higher investment advisory fee than the Acquired Fund, the overall expense ratio for the Acquiring Fund is lower than that of the Acquired Fund. The Acquired Fund’s portfolio managers - John Brown and Drew Justman - are also the portfolio managers of the Acquiring Fund. The Reorganization is expected to be tax-free to the Acquired Fund’s shareholders for federal income tax purposes. We anticipate that the Reorganization will result in benefits to the shareholders of the Acquired Fund as discussed more fully in the Combined Proxy Statement/Prospectus.

The Board of Trustees has given careful consideration to the Reorganization and has concluded that it is in the best interests of the Funds and the interests of shareholders of the Funds will not be diluted as a result of the Reorganization. The Board unanimously recommends that you vote “FOR” the Reorganization.

If the Reorganization is approved by shareholders of the Acquired Fund, each shareholder holding Class A shares of the Acquired Fund will receive Class A shares of the Acquiring Fund, and each shareholder holding Class Y shares of the Acquired Fund will receive Class Y shares of the Acquiring Fund. These shares will have an aggregate net asset value (“NAV”) equal to the aggregate NAV of the shareholder’s shares of the Acquired Fund. The Acquired Fund would then be liquidated and terminated as a series of the Trust. Shareholders of the Acquired Fund will not be assessed any sales charges or other individual shareholder fees in connection with the Reorganization.

Special Notice to shareholders of Class B shares: Because the Acquiring Fund does not offer Class B shares, prior to the Reorganization, on or about August 20, 2020, all Class B shares of the Acquired Fund will be automatically converted to Class A shares of the Acquired Fund. Since your money remains invested in the same fund, the conversion from Class B to Class A shares is not a taxable event. In addition, if applicable, no contingent deferred sales charges will be assessed on this one-time conversion.

We welcome your attendance at the Meeting. If you are unable to attend, we encourage you to authorize proxies to cast your votes. No matter how many shares you own, your vote is important.

Sincerely,

/s/ Patrick F. Ryan

Patrick F. Ryan

President

MADISON FUNDS®

LARGE CAP VALUE FUND

550 Science Drive

Madison, Wisconsin 53711

NOTICE OF SPECIAL MEETING OF SHAREHOLDERS

to be held September 2, 2020

To the Shareholders of the Large Cap Value Fund:

NOTICE IS HEREBY GIVEN that a Special Meeting of Shareholders (the “Meeting”) of the Large Cap Value Fund (the “Acquired Fund”), a series of Madison Funds (the “Trust”), is to be held at 10:00 a.m. Central time on September 2, 2020, at the offices of Madison Asset Management, LLC located at 550 Science Drive, Madison, Wisconsin 53711.

At the Meeting you will be asked to consider and approve the following proposals:

1. | To approve an Agreement and Plan of Reorganization and Liquidation (the “Plan”) providing for the acquisition of all of the assets and the assumption of all of the liabilities of the Acquired Fund in exchange for shares of beneficial interest of the Dividend Income Fund (the “Acquiring Fund”), a series of Madison Funds, followed by the liquidation of the Acquired Fund; and |

2. | To transact such other business as may properly come before the Meeting or any adjournments or postponements thereof. |

Record owners of shares of the Acquired Fund as of the close of business on June 15, 2020, are entitled to vote at the Meeting or any adjournments or postponements thereof. If you attend the Meeting, you may vote your shares in person. If you do not attend the Meeting, you may vote by proxy by completing, signing and returning the enclosed proxy card by mail in the envelope provided, or by following the instructions on the proxy card to vote by telephone or the Internet.

Your vote is important. If you have any questions, please contact the Trust’s proxy agent, Computershare Fund Services toll-free at (866) 956-7277 for additional information.

By order of the Board of Trustees

Sincerely,

/s/ Holly S. Baggot

Holly S. Baggot

Secretary of Madison Funds

July 9, 2020

IMPORTANT -- WE URGE YOU TO SIGN AND DATE THE ENCLOSED PROXY CARD AND RETURN IT IN THE ENCLOSED ADDRESSED ENVELOPE, WHICH REQUIRES NO POSTAGE AND IS INTENDED FOR YOUR CONVENIENCE. YOU ALSO MAY VOTE BY TELEPHONE OR BY INTERNET USING THE INSTRUCTIONS ON YOUR PROXY CARD. YOUR PROMPT VOTE MAY SAVE THE FUND THE NECESSITY OF FURTHER SOLICITATIONS TO ENSURE A QUORUM AT THE MEETING. IF YOU CAN ATTEND THE MEETING AND WISH TO VOTE YOUR SHARES IN PERSON AT THAT TIME, YOU WILL BE ABLE TO DO SO.

(This page intentionally left blank)

MADISON FUNDS®

LARGE CAP VALUE FUND

550 Science Drive

Madison, Wisconsin 53711

QUESTIONS AND ANSWERS

July 9, 2020

The following questions and answers provide an overview of key features of the proposed reorganization and of the information contained in the attached Combined Proxy Statement/Prospectus (the “Proxy Statement/Prospectus”). Please review the full Proxy Statement/Prospectus before casting your vote.

1. | What is this document and why was it sent to you? |

The attached Proxy Statement/Prospectus provides you with information about the proposed acquisition of the Large Cap Value Fund (the “Acquired Fund”), a series of Madison Funds (the “Trust”), by the Dividend Income Fund (the “Acquiring Fund”, and, together with the Acquired Fund, the “Funds”), also a series of Madison Funds (the “Reorganization”). The purposes of the Proxy Statement/Prospectus are to (1) solicit votes from shareholders of the Acquired Fund to approve the Reorganization, as described in the Agreement and Plan of Reorganization and Liquidation, included as Exhibit A hereto (the “Plan”), and (2) provide information regarding the shares of the Acquiring Fund.

The Proxy Statement/Prospectus contains information that shareholders of the Acquired Fund should know before voting on the Reorganization. The Proxy Statement/Prospectus should be retained for future reference.

2. | Why is the Reorganization being proposed now? |

Madison Asset Management, LLC (“Madison”), the investment adviser of the Funds, has recently completed a strategic review of the offerings by the Trust and concluded that, in its current state, the Acquired Fund will not likely grow, making it cost prohibitive to continue to operate as a standalone fund. Because the Acquired Fund and the Acquiring Fund have similar investment objectives, investment strategies and investment policies, substantially similar risk profiles and the same portfolio management team, as well as the fact that both Funds occupy the same “Large Value” space in Morningstar® ratings, Madison recommended the Reorganization to the Board of Trustees of the Trust (the “Board”). Madison believes that optimizing its equity fund lineup, while still offering breadth and depth across asset classes, will make it easier for shareholders to differentiate funds and may increase the combined Fund’s prospects for increased sales and economies of scale. In addition, Madison believes that the Reorganization represents the most effective use of investment resources and creates an environment with the best opportunity for successful long-term investing on behalf of shareholders.

3. | What is the purpose of the Reorganization? |

The purpose of the Reorganization is to transfer the assets of the Acquired Fund into the Acquiring Fund. As discussed in the Proxy Statement/Prospectus, after carefully considering the recommendation of Madison, the Board concluded that the Acquired Fund’s participation in the Reorganization would be in the best interests of the Acquired

i

Fund and its shareholders, and approved the submission of the Plan to shareholders of the Acquired Fund for approval. In reaching this conclusion, the Board considered, among other factors, the expectation that the Acquired Fund and its shareholders will not recognize any taxable gain or loss in the Reorganization and that shareholders of the Acquired Fund would benefit from becoming shareholders of the Acquiring Fund, which has:

• | The same portfolio managers as the Acquired Fund; |

• | Similar investment objectives, investment strategies and investment policies as the Acquired Fund; |

• | Lower overall expenses, on a per class basis, than the Acquired Fund; and |

• | The same adviser and distributor which are committed to facilitate the future growth of the larger, combined Fund. |

The Reorganization will not occur unless the Plan is approved by shareholders of the Acquired Fund. The Board unanimously recommends that you vote “FOR” the Plan.

4. | How will the proposed Reorganization work? |

Subject to the approval of the shareholders of the Acquired Fund, the Plan provides for:

• | The transfer of all of the assets of the Class A shares of the Acquired Fund in exchange for shares of beneficial interest of Class A shares of the Acquiring Fund, and the transfer of all of the assets of the Class Y shares of the Acquired Fund in exchange for shares of beneficial interest of Class Y shares of the Acquiring Fund, and the assumption by the Acquiring Fund of all of the liabilities of the Acquired Fund; |

• | That, prior to the “Exchange Date” as defined in the Plan of Reorganization, the Acquired Fund shall convert all of the existing Class B shares to Class A shares of the Acquired Fund; |

• | The distribution of the Acquiring Fund shares received by the Acquired Fund from the Acquiring Fund to shareholders of the Acquired Fund; and |

• | The complete termination and liquidation of the Acquired Fund. |

Upon consummation of the Reorganization, Class A shareholders of the Acquired Fund will become shareholders of Class A shares of the Acquiring Fund, and Class Y shareholders of the Acquired Fund will become shareholders of Class Y shares of the Acquiring Fund. As a result, each former Class A shareholder will hold Acquiring Fund Class A shares with an aggregate net asset value (“NAV”) equal to the aggregate NAV of the shareholder’s Acquired Fund Class A shares, and each former Class Y shareholder will hold Acquiring Fund Class Y shares with an aggregate NAV equal to the aggregate NAV of the shareholder’s Acquired Fund Class Y shares. Please refer to the Proxy Statement/Prospectus for a detailed explanation of the Reorganization. If the Plan is approved by the Acquired Fund’s shareholders at the Special Meeting of Shareholders (the “Meeting”), the Reorganization is expected to occur on or about September 14, 2020 (the “Effective Date”).

5. | Who is eligible to vote on the Reorganization? |

Shareholders of record of the Acquired Fund at the close of business on June 15, 2020 (the “Record Date”), are entitled to notice of, and to vote at, the Meeting or any adjournment or postponement thereof. If you held Acquired Fund shares on the Record Date, you have the right to vote even if you later sold your shares. Each shareholder is entitled to one vote for each dollar of net asset value standing in such shareholder’s name on the books

ii

of the Acquired Fund as of the Record Date. As of the Record Date, the Acquired Fund had 4,740,667.078 shares outstanding with an aggregate net asset value of $52,094,663.54. Shares represented by properly executed proxies, unless the proxies are revoked before or at the Meeting, will be voted according to shareholders’ instructions. If you sign and return a proxy but do not fill in a vote, your shares will be voted “FOR” the Plan. If any other business properly comes before the Meeting, your shares will be voted at the discretion of the persons named as proxies.

6. | How will the Reorganization affect me as a shareholder of the Acquired Fund? |

Each Class A shareholder of the Acquired Fund will become a shareholder of Class A shares of the Acquiring Fund, and each Class Y shareholder of the Acquired Fund will become a shareholder of the Class Y shares of the Acquiring Fund. The shares of the Acquiring Fund that an Acquired Fund shareholder receives will have a total NAV equal to the total NAV of the shares held by such shareholder in the Acquired Fund as of the Effective Date of the Reorganization. In addition, prior to consummation of the Reorganization, on or about August 20, 2020, each issued and outstanding Class B share of the Acquired Fund will be converted into Class A shares of the Acquired Fund.

7. | Who manages the Acquiring Fund? |

The investment adviser to the Acquiring Fund is Madison. Madison also serves as investment adviser to the Acquired Fund. The same portfolio management team that manages the Acquired Fund - John Brown and Drew Justman - also manage the Acquiring Fund.

8. | How will the Reorganization affect the advisory fees and expenses? |

The Reorganization will result in a change in the advisory fee rate of the Acquired Fund, as the investment advisory fee of the Acquired Fund, which is an annual rate of 0.55% of the Acquired Fund’s average daily net assets, is lower than the investment advisory fee of the Acquiring Fund, which is an annual rate of 0.70% of the Acquired Fund’s average daily net assets. Nevertheless, the Acquiring Fund has lower overall expenses than the Acquired Fund, which will benefit Acquired Fund shareholders.

9. | What happens if shareholders do not approve the Plan? |

If shareholders do not approve the Plan, the Reorganization will not occur and the Board will consider other options for the Acquired Fund, including liquidation.

10. | Is consummation of the Reorganization subject to any conditions (in addition to shareholder approval)? |

In addition to shareholder approval, the Reorganization is subject to a number of customary conditions to close, including the receipt of a tax opinion from counsel to the Funds to the effect that the Reorganization is expected to be tax-free for federal income tax purposes and the effectiveness of the registration statement of which this Proxy Statement/Prospectus is a part.

11. | Who is paying for expenses of the Reorganization? |

Madison is paying for the costs and expenses related to the Reorganization, including the repositioning costs and expenses described under the heading “Costs of the Reorganization” below.

iii

12. | Who do I call if I have questions about the Meeting or the Reorganization? |

If you have any questions about the Reorganization or the proxy card, please call the Trust’s proxy agent, Computershare Fund Services toll-free at (866) 956-7277.

13. | Where may I find additional information regarding the Acquired Fund and the Acquiring Fund? |

Additional information relating to the Acquired Fund and the Acquiring Fund has been filed with the U.S. Securities and Exchange Commission (“SEC”) and can be found in the following documents:

• | The Statement of Additional Information dated July 9, 2020 that has been filed with the SEC in connection with this Proxy Statement/Prospectus and is incorporated into this Proxy Statement/Prospectus by reference (the “Reorganization SAI”); |

• | The Annual Report to Shareholders of the Funds, which contains audited financial statements for the fiscal year ended October 31, 2019, which is incorporated into this Proxy Statement/Prospectus by reference; and |

• | The Semi-Annual Report to Shareholders of the Funds, which contains unaudited financial statements for the six-month period ended April 30, 2020, which is incorporated into this Proxy Statement/Prospectus by reference; |

• | The Prospectus and Statement of Additional Information (“SAI”) of the Funds, dated June 1, 2020, which are incorporated into this Proxy Statement/Prospectus by reference. |

Copies of the Funds’ Annual Report to Shareholders, Semi-Annual Report to Shareholders and Prospectus and SAI are available, along with the Proxy Statement/Prospectus and Reorganization SAI, upon request, without charge, by writing to the address or calling the telephone number listed below.

By mail Madison Funds, P.O. Box 219083, Kansas City, MO 64121-9083

By phone: (800) 877-6089

All of this additional information is also available in documents filed with the SEC. You may view or obtain these documents from the SEC:

In person: at the SEC’s Public Reference Room located at 100 F Street, N.E.,

Washington, DC 20549

By phone: 1-202-551-8090 (for information on the operations of the Public

Reference Room only)

By mail: Public Reference Branch, Officer of Consumer Affairs and Information

Services, Securities and Exchange Commission, Washington, DC

20549-1520 (duplicating fee required)

By email: publicinfo@sec.gov (duplicating fee required)

By Internet: www.sec.gov

Other Important Things to Note:

• | You may lose money by investing in the Funds. |

• | The SEC has not approved or disapproved these securities or passed upon the adequacy of the Proxy Statement/Prospectus. Any representation to the contrary is a criminal offense. |

iv

COMBINED PROXY STATEMENT/PROSPECTUS

RELATING TO THE ACQUISITION OF

MADISON LARGE CAP VALUE FUND,

a series of Madison Funds

BY

MADISON DIVIDEND INCOME FUND,

a series of Madison Funds

Managed by:

Madison Asset Management, LLC

550 Science Drive

Madison, Wisconsin 53711

(800) 877-6089

July 9, 2020

This Combined Proxy Statement and Prospectus (the “Proxy Statement/Prospectus”) is being sent to you in connection with the solicitation of proxies by the Board of Trustees of Madison Funds (the “Trust”) for use at a Special Meeting of Shareholders (the “Meeting”) of the Large Cap Value Fund, a series of the Trust (the “Acquired Fund”), managed by Madison Asset Management, LLC (“Madison”), at the offices of Madison located at 550 Science Drive, Madison, Wisconsin 53711.

At the Meeting, you will be asked to consider and approve the following proposals:

1. | To approve an Agreement and Plan of Reorganization and Liquidation (the “Plan”) providing for the acquisition of all of the assets and the assumption of all of the liabilities of the Acquired Fund in exchange for shares of beneficial interest of the Madison Dividend Income Fund (the “Acquiring Fund” and together with the Acquired Fund, the “Funds”), a series of Madison Funds, followed by the liquidation of the Acquired Fund (the “Reorganization”); and |

2. | To transact such other business as may properly come before the Meeting or any adjournments or postponements thereof. |

Each Fund is a series of the Trust, an open-end management investment company registered with the U.S. Securities and Exchange Commission (the “SEC”) and organized as a Delaware statutory trust. The investment objective of the Acquiring Fund is to seek to produce current income while providing an opportunity for capital appreciation, and the investment objective of the Acquired Fund is to seek long-term capital growth, with income as a secondary consideration.

This Proxy Statement/Prospectus sets forth the basic information you should know before voting on the proposal. You should read it and keep it for future reference. Additional information relating to the Acquiring Fund and this Proxy Statement/Prospectus is set forth in the Statement of Additional Information to this Proxy Statement/Prospectus dated July 9, 2020 (the “Reorganization SAI”), which is incorporated by reference into this Proxy Statement/Prospectus. Additional information about the Acquiring Fund has been filed with the SEC and is available upon request and without charge by writing to the Acquiring Fund or by calling (800) 877-6089. The Acquired Fund expects that this Proxy Statement/Prospectus will be mailed to shareholders on or about July 17, 2020.

THE SEC HAS NOT APPROVED OR DISAPPROVED THESE SECURITIES NOR HAS IT PASSED ON THE ACCURACY OR ADEQUACY OF THIS PROXY STATEMENT/PROSPECTUS. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

(This page intentionally left blank)

TABLE OF CONTENTS

(This page intentionally left blank)

APPROVAL OF AGREEMENT AND PLAN OF REORGANIZATION AND LIQUIDATION

On May 21, 2020, the Board of Trustees of the Trust (the “Board”) approved the Plan. Subject to the approval of the shareholders of the Acquired Fund, the Plan provides for:

• | The transfer of all of the assets of the Class A shares of the Acquired Fund in exchange for shares of beneficial interest of Class A shares of the Acquiring Fund, and the transfer of all of the assets of the Class Y shares of the Acquired Fund in exchange for shares of beneficial interest of Class Y shares of the Acquiring Fund, and the assumption by the Acquiring Fund of all of the liabilities of the Acquired Fund; |

• | That, prior to the “Exchange Date” as defined in the Plan of Reorganization, the Acquired Fund shall convert all of the existing Class B shares to Class A shares of the Acquired Fund; |

• | The distribution of the Acquiring Fund shares received by the Acquired Fund from the Acquiring Fund to shareholders of the Acquired Fund; and |

• | The complete termination and liquidation of the Acquired Fund. |

Class A shareholders of the Acquired Fund will become shareholders of Class A shares of the Acquiring Fund, and Class Y shareholders of the Acquired Fund will become shareholders of Class Y shares of the Acquiring Fund. Immediately after the Reorganization, each former Class A shareholder will hold Acquiring Fund Class A shares, and each former Class Y shareholder will hold Acquiring Fund Class Y shares, with an aggregate net asset value (“NAV”) equal to the aggregate NAV of the shareholder’s Acquired Fund Class A and Class Y shares, respectively. Prior to the Reorganization, on or about August 20, 2020, the Class B shares of the Acquired Fund will be converted to Class A shares of the Acquired Fund. There will be no effect on the Class B shareholders as a result of the conversion and no contingent deferred sales charges will be assessed. The Funds expect that shareholders of the Acquired Fund will recognize no gain or loss for federal income tax purposes in connection with the Reorganization. If approved by shareholders of the Acquired Fund, consummation of the Reorganization is expected to occur on or about September 14, 2020 (the “Effective Date”).

The shareholders of the Acquired Fund must approve the Plan in order for the Reorganization to occur. Approval of the Plan requires the affirmative vote of a “majority of the outstanding voting securities” of the Acquired Fund, as that term is defined under the Investment Company Act of 1940, as amended (the “1940 Act”). The Reorganization does not require approval of the shareholders of the Acquiring Fund.

A quorum for the transaction of business by shareholders of the Acquired Fund at the Meeting will consist of the presence in person or by proxy of the holders of at least 20% of the shares of the Acquired Fund outstanding at the close of business on June 15, 2020 (the “Record Date”).

Based on its consideration of, among other factors, the anticipated tax-free nature of the Reorganization and the benefits expected to be received by shareholders of the Acquired Fund in becoming shareholders of the Acquiring Fund, the Board has determined that the Reorganization is in the best interests of the Funds and the interests of shareholders of the Funds will not be diluted as a result of the Reorganization. Accordingly, the Board unanimously recommends that shareholders vote “FOR” the Plan.

For a more complete discussion of the factors considered by the Board in approving the Reorganization, see “Information about the Reorganization-Reasons for the Reorganization.”

1

SUMMARY

Introduction. The following summary highlights differences between the Funds. This summary is not complete and does not contain all of the information that you should consider before voting on the Plan. This summary is qualified in its entirety by reference to the additional information contained elsewhere in this Proxy Statement/Prospectus and the Plan, a form of which is attached to this Proxy Statement/Prospectus as Appendix A. Shareholders should read this entire Proxy Statement/Prospectus carefully. For more complete information, please read the Funds’ Prospectus. This Proxy Statement/Prospectus, the accompanying Notice of the Special Meeting of Shareholders and the enclosed Proxy Card are being mailed to shareholders of the Acquired Fund on or about July 17, 2020.

Comparison of Investment Advisory Fees. The Funds are party to the same investment advisory agreement with Madison; however, the Funds pay different advisory fees. The Acquired Fund’s annual advisory fee rate is 0.55% of the Acquired Fund’s average daily net assets, and the Acquiring Fund’s annual advisory fee rate is 0.70% of the Acquiring Fund’s average daily net assets, in each case accrued daily and paid monthly. The advisory fee rate for both Funds is reduced by 0.05% when Fund assets reach $500 million and by another 0.05% when Fund assets reach $1 billion.

Comparison of Expenses. While the Acquiring Fund has a higher annual advisory fee rate than the Acquired Fund, the Acquiring Fund’s overall expense ratio is lower than that of the Acquired Fund, as illustrated in the fee table, below.

Fee Table. The purpose of the fee table below is to assist an investor in understanding the various costs and expenses that a shareholder bears directly and indirectly from an investment in the Funds. You may pay other fees, such as brokerage commissions and other fees to financial intermediaries, which are not reflected in the table and example below. You may qualify for Class A sales charge discounts if you and your immediate family invest, or agree to invest in the future, at least $25,000 in Madison Funds. More information about these and other discounts is available from your financial professional and can also be found in Appendix B of this Proxy Statement/Prospectus. The fee table shown below is based on actual Fund expenses incurred for the fiscal year ended October 31, 2019 (adjusted to account for contractual advisory and service fee changes since that time). The table also reflects the pro forma combined fees for the Acquiring Fund after giving effect to the Reorganization.

2

Acquired Fund - Large Cap Value Fund (Current) | Acquiring Fund - Dividend Income Fund (Current) | Acquiring Fund - Dividend Income Fund (Pro Forma Combined) | |||||

Shareholder Fees (fees paid directly from your investment) | Class A | Class B1 | Class Y | Class A | Class Y | Class A | Class Y |

Maximum sales charge (load) imposed on purchases (as a percentage of offering price) | 5.75% | None | None | 5.75% | None | 5.75% | None |

Maximum deferred sales charge (load) (as a percentage of amount redeemed) | None | 4.50%2 | None | None | None | None | None |

Redemption fee within 30 days of purchase (as a percentage of amount redeemed) | None | None | None | None | None | None | None |

Annual Fund Operating Expenses (expenses you pay each year as a percentage of the value of your investment) | Class A | Class B | Class Y | Class A | Class Y | Class A | Class Y |

Management fees | 0.55% | 0.55% | 0.55% | 0.70% | 0.70% | 0.70% | 0.70% |

Distribution and/or service (12b-1) fees | 0.25% | 1.00% | None | 0.25% | None | 0.25% | None |

Other expenses | 0.36% | 0.36% | 0.36% | 0.20% | 0.20% | 0.20% | 0.20% |

Total annual fund operating expenses | 1.16% | 1.91% | 0.91% | 1.15% | 0.90% | 1.15% | 0.90% |

1Class B shares of the Large Cap Value Fund will be exchanged for Class A shares of the Large Cap Value Fund prior to the Reorganization, on or about August 20, 2020.

2 The CDSC is reduced after 12 months and eliminated after six years following purchase.

Expense Example. The following example is intended to help you compare the cost of investing in each Fund with the cost of investing in other mutual funds. The example assumes you invest $10,000 in each Fund for the time periods indicated and then redeem your shares at the end of the period. The example also assumes that your investment has a 5% return each year and that each Fund’s total annual fund operating expenses (as set forth above) remain the same. Although your actual costs may be higher or lower, based on these assumptions, your costs would be:

Redemption/No Redemption | ||||

Fund/Class | Year 1 | Year 3 | Year 5 | Year 10 |

Acquired Fund/Class A (current) | $ 686 | $ 922 | $1,177 | $1,903 |

Acquiring Fund/Class A (current) | 685 | 919 | 1,172 | 1,892 |

Acquiring Fund/Class A (pro forma) | 685 | 919 | 1,172 | 1,892 |

Acquired Fund/Class Y (current) | 93 | 290 | 504 | 1,120 |

Acquiring Fund/Class Y (current) | 92 | 287 | 498 | 1,108 |

Acquiring Fund/Class Y (pro forma) | 92 | 287 | 498 | 1,108 |

3

Redemption | No Redemption | |||||||

Fund/Class | Year 1 | Year 3 | Year 5 | Year 10 | Year 1 | Year 3 | Year 5 | Year 10 |

Acquired Fund/Class B (current)1 | $644 | $950 | $1,232 | $2,038 | $194 | $600 | $1,032 | $2,038 |

Acquiring Fund/Class B (current) | N/A | N/A | N/A | N/A | N/A | N/A | N/A | N/A |

1Class B shares of the Large Cap Value Fund will be exchanged for Class A shares of the Large Cap Value Fund prior to the Reorganization, on or about August 20, 2020.

Comparison of Portfolio Turnover. Each Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. Those costs, which are not reflected in annual fund operating expenses or in the expense example, affect a Fund’s performance. During the fiscal year ended October 31, 2019, each Fund’s portfolio turnover rate was the following percentage of the average value of the Fund’s portfolio:

Fund | Percentage of the Average Value of the Fund’s Portfolio |

Acquired Fund | 71% |

Acquiring Fund | 28% |

Performance Comparison. The bar chart and table shown below provide some indication of the risks of investing in the Funds. The bar chart shows how each Fund’s performance results have varied from year to year, and the table shows how each Fund’s average annual returns for the one-year, five-year and ten-year periods compare to those of a broad measure of market performance. The Funds’ past performance (before and after taxes) does not necessarily indicate how the Funds will perform in the future. Updated performance information current to the most recent month end is available at no cost by visiting www.madisonfunds.com or by calling 1-800-877-6089.

Acquired Fund - Large Cap Value Fund

Calendar Year Total Returns for Class A Shares

(Returns do not reflect sales charges and would be lower if they did.)

Highest/Lowest quarter end results during this period were: | ||||

Highest: | 4Q 2011 | 13.33 | % | |

Lowest: | 4Q 2018 | -17.69 | % | |

4

Average Annual Total Returns

For periods ended December 31, 2019

1 Year | 5 Years | 10 Years | ||||

Class A Shares - Return Before Taxes | 17.23 | % | 5.04 | % | 9.02 | % |

Return After Taxes on Distributions | 16.28 | % | 2.32 | % | 7.14 | % |

Return After Taxes on Distributions and Sale of Fund Shares | 10.88 | % | 3.42 | % | 7.04 | % |

Class B Shares - Return before Taxes | 19.00 | % | 5.26 | % | 9.01 | % |

Class Y Shares - Return before Taxes | 24.70 | % | 6.56 | % | 9.94 | % |

Russell 1000® Value Index (reflects no deduction for sales charges, account fees, expenses or taxes) | 26.54 | % | 8.29 | % | 11.80 | % |

After-tax returns are calculated using the highest historical individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown, and after-tax returns shown are not relevant to investors who hold their Fund shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts. After-tax returns are shown only for Class A shares and will vary for other share classes. Returns after taxes on distributions and sale of Fund shares may be higher than other returns for the same period due to the tax benefit of realizing a capital loss on the sale of Fund shares.

Acquiring Fund - Dividend Income Fund

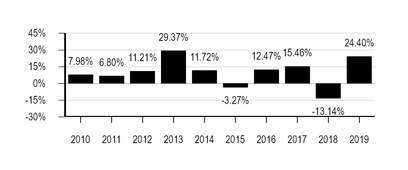

Calendar Year Total Returns for Class Y Shares

Highest/Lowest quarter end results during this period were: | ||||

Highest: | 1Q 2013 | 12.47 | % | |

Lowest: | 3Q 2011 | -7.99 | % | |

5

Average Annual Total Returns

For periods ended December 31, 2019

1 Year | 5 Years | 10 Years | |||

Class Y Shares - Return Before Taxes | 25.16% | 10.97 | % | 11.28 | % |

Return After Taxes on Distributions | 24.00% | 9.43 | % | 10.02 | % |

Return After Taxes on Distributions and Sale of Fund Shares | 15.69% | 8.42 | % | 9.08 | % |

Class A Shares - Return Before Tax | * | * | * | ||

S&P 500® Index (reflects no deduction for sales charges, account fees, expenses or taxes) | 31.49% | 11.70 | % | 13.56 | % |

Russell 1000® Value Index (reflects no deduction for sales charges, account fees, expenses or taxes) | 26.54% | 8.29 | % | 11.80 | % |

Lipper Equity Income Funds Index (reflects no deduction for sales charges, account fees, expenses or taxes) | 26.38% | 8.80 | % | 11.20 | % |

* The Class A shares commenced operations until June 1, 2020, therefore, performance information is not available. Class A shares would have substantially similar returns as Class Y shares because the shares are invested in the same portfolio of securities and the annual returns would differ only to the extent that the share classes do not have the same expenses.

After-tax returns are calculated using the highest historical individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown, and after-tax returns shown are not relevant to investors who hold their Fund shares through tax-deferred arrangements such as 401(k) plans or individual retirement accounts. After-tax returns are shown only for Class Y shares and will vary for other share classes. Returns after taxes on distributions and sale of Fund shares may be higher than other returns for the same period due to the tax benefit of realizing a capital loss on the sale of Fund shares

The performance history of the Acquiring Fund will survive consummation of the Reorganization. Please remember that past performance (both before and after taxes) is no guarantee of the results the Funds may achieve in the future. Future returns may be higher or lower than the returns achieved in the past.

Comparison of Investment Objectives and Strategies. The investment objective of the Acquired Fund is to seek long-term capital growth, with income as a secondary consideration, and the investment objective of the Acquiring Fund is to seek to produce current income while providing an opportunity for capital appreciation. Accordingly, the investment objective of each Fund is similar in that both Funds seek capital appreciation as well as current income. The Acquired Fund emphasizes capital appreciation, with current income as a secondary objective, while the Acquiring Fund emphasizes current income at the same time looking for opportunities for capital growth.

To attempt to achieve its investment objective, the Acquired Fund will, under normal market conditions, maintain at least 80% of its net assets (including borrowings for investment purposes) in large cap stocks (generally, stocks with a market capitalization of the companies represented in the Russell 1000® Value Index -- as of the most recent reconstitution date, the low end of the range of market capitalizations included in this index was $1.71 billion). The Acquired Fund follows what is known as a “value” approach, which generally means that the Fund’s portfolio managers seek to invest in stocks at prices below their perceived intrinsic value as estimated based on fundamental analysis of the issuing company and its prospects. By investing in value stocks, the Acquired Fund attempts to limit the downside risk over time but may also produce smaller gains than

6

other stock funds if their intrinsic values are not realized by the market or if growth-oriented investments are favored by investors. The Acquired Fund will diversify its holdings among various industries and among companies within those industries. The Acquired Fund may invest up to 25% of its assets in foreign securities, including American Depositary Receipts (“ADRs”) and emerging market securities, and may invest in exchange traded funds (“ETFs”) that are registered investment companies. As a non-principal investment strategy, the Acquired Fund may also invest in warrants, convertible securities, preferred stocks and debt securities (including non-investment grade debt securities). The Acquired Fund generally holds 25-60 individual securities in its portfolio at any given time. The Acquired Fund typically sells a stock when the fundamental expectations for buying it no longer apply, the price exceeds its intrinsic value or other stocks appear more attractively priced relative to their intrinsic values.

The Acquiring Fund seeks to achieve its investment objective by investing in equity securities of companies with a market capitalization of over $1 billion (similar to the Acquired Fund) and a history of paying dividends, with the ability to increase dividends over time. Under normal market conditions, at least 80% of the Acquiring Fund’s net assets (including borrowings for investment purposes) will be invested in dividend paying equity securities. The Acquiring Fund’s portfolio managers, who are the same persons managing the Acquired Fund’s portfolio, will identify investment opportunities by screening for companies that generally have the following characteristics: (i) a dividend yield of at least 100% of the market dividend yield (for this purpose, the “market” is the S&P 500); (ii) a strong balance sheet; (iii) a dividend that has been maintained and which is likely to increase; (iv) trade on the high side of the company’s historical relative dividend yield, due to issues which the portfolio managers view as temporary; and (v) other compelling valuation characteristics. Under normal market conditions, the Acquiring Fund expects to be fully invested in equity securities, but will maintain the flexibility to hold up to 20% of its assets in investment grade fixed income securities when warranted. Additionally, the Acquiring Fund may write (sell) covered call options against equity holdings, not to exceed 25% of its equity holdings. Like the Acquired Fund, the Acquiring Fund may also invest up to 25% of its common stock allocation in foreign securities (including ADRs and emerging market securities). To the extent invested in common stocks, the Acquiring Fund generally invests in 30-60 companies at any given time. This focused approach to investing, which is used in the management of both Funds, reflects Madison’s belief that your money should be invested in Madison's top investment ideas, and that focusing on Madison’s best investment ideas is the best way to achieve a Fund’s investment objective.

The portfolio managers for the Acquiring Fund follow a rigorous three-step process when evaluating companies which considers (1) the business model, (2) the management team, and (3) the valuation of each potential investment. When evaluating the business model, the team looks for sustainable competitive advantages, metrics that demonstrate relatively high levels of profitability, stable and growing earnings, and a solid balance sheet. When assessing management, the team evaluates its operational and capital allocation track records and the nature of its accounting practices. The final step in the process is assessing the proper valuation for the company. The portfolio management team strives to purchase securities trading at a discount to their intrinsic value as determined by discounted cash flows modeling and additional valuation methodologies. Often, the team finds companies that clear the business model and management team hurdles, but not the valuation hurdle. Those companies are monitored for inclusion at a later date when the price may be more appropriate. The team seeks to avoid the downside risks associated with overpriced securities. The portfolio managers may sell stocks for a number of reasons, including: (i) the price target they have set for stock has been

7

achieved, (ii) the fundamental business prospects for the company have materially changed, or (iii) the team finds a more attractive alternative. In addition, with regard to dividend paying stocks in particular, the team may sell a stock that has reduced its dividend to a level that brings the yield on the stock to below the market (S&P 500) dividend yield, but only if the reduction in dividend appears to the team to be a symptom of fundamental difficulties with the company that are other than temporary in nature.

Each Fund’s investment strategy reflects Madison's general “Participate and Protect®” investment philosophy. Madison’s expectation is that investors in the Funds will participate in market appreciation during bull markets and experience something less than full participation during bear markets compared with investors in portfolios holding more speculative and volatile securities; therefore, this investment philosophy is intended to represent a conservative investment strategy. There is no assurance that Madison’s expectations regarding this investment strategy will be realized. In addition, although each Fund expects to pursue its investment objective utilizing its principal investment strategies regardless of market conditions, each Fund may invest up to 100% in money market instruments. To the extent a Fund engages in this temporary defensive position, the Fund’s ability to achieve its investment objective may be diminished.

In their management of the Acquiring Fund, the portfolio managers of the Acquiring Fund, who are the same as the portfolio managers of the Acquired Fund, intend to follow the same investment strategies utilized in managing the Acquiring Fund, as described above.

Comparison of Fundamental and Non-Fundamental Investment Policies.

Fundamental Policies. Fundamental investment policies are policies that, under the 1940 Act, may not be changed without a shareholder vote. The 1940 Act requires a fund to disclose whether it has certain policies relating to, for example, borrowing money or issuing senior securities, and that these policies be fundamental. The Acquiring Fund has the same fundamental policies as the Acquired Fund. In addition to the fundamental policies listed below, the investment objective of both Funds is a fundamental investment policy which cannot be changed without shareholder approval.

Fundamental Policies | |

Acquired Fund | Acquiring Fund |

1. The Fund will not, with respect to 75% of its total assets, purchase securities of an issuer (other than the U.S. Government, its agencies or instrumentalities), if (i) such purchase would cause more than 5% of the Fund’s total assets taken at market value to be invested in the securities of such issuer or (ii) such purchase would at the time result in more than 10% of the outstanding voting securities of such issuer being held by the Fund. | 1. Same. |

2. The Fund will not invest 25% or more of its total assets in the securities of one or more issuers conducting their principal business activities in the same industry (excluding the U.S. Government or any of its agencies or instrumentalities). | 2. Same. |

8

Fundamental Policies | |

Acquired Fund | Acquiring Fund |

3. The Fund will not borrow money, except that it may (i) borrow from any lender for temporary purposes in amounts not in excess of 5% of its total assets and (ii) borrow from banks in any amount for any purpose, provided that immediately after borrowing from a bank, the fund’s aggregate borrowings from any source do not exceed 33 1/3% of the Fund’s total assets (including the amount borrowed). If, after borrowing from a bank, the Fund’s aggregate borrowings later exceed 33 1/3% of the Fund’s total assets, the Fund will, within three days after exceeding such limit (not including Sundays or holidays), reduce the amount of its borrowings to meet the limitation. The Fund may make additional investments while it has borrowings outstanding, and the Fund may make other borrowings to the extent permitted by applicable law. | 3. Same. |

4. The Fund may not make loans, except through (i) the purchase of debt obligations in accordance with the Fund’s investment objective and policies, (ii) repurchase agreements with banks, brokers, dealers and other financial institutions, and (iii) loans of securities as permitted by applicable law. | 4. Same. |

5. The Fund may not underwrite securities issued by others, except to the extent that the sale of portfolio securities by the Fund may be deemed to be an underwriting. | 5. Same. |

6. The Fund may not purchase, hold or deal in real estate, although it may purchase and sell securities that are secured by real estate or interests therein, securities of real estate investment trusts and mortgage-related securities and may hold and sell real estate acquired by the Fund as a result of the ownership of securities. | 6. Same. |

7. The Fund may not invest in commodities or commodity contracts, except that the Fund may invest in currency, and financial instruments and contracts that are commodities or commodity contracts. | 7. Same. |

8. The Fund may not issue senior securities to the extent such issuance would violate applicable law. | 8. Same. |

Non-Fundamental Policies. Non-fundamental investment policies may be changed by the Board of Trustees of the Funds without a shareholder vote. The Acquiring Fund has the same non-fundamental policies as the Acquired Fund.

Non-Fundamental Policies | |

Acquired Fund | Acquiring Fund |

1. The Fund will not sell securities short or maintain a short position, except for short sales against the box. | 1. Same. |

2. The Fund will not purchase illiquid securities if more than 15% of the total assets of the Fund, taken at market value, would be invested in such securities. | 2. Same. |

9

Comparison of Principal Risks. The principal risks of the Acquiring Fund are substantially the same as those of the Acquired Fund. A description of each of these risks is provided below.

Principal Risks | |

Acquired Fund | Acquiring Fund |

Equity Risk. The Fund is subject to equity risk. Equity risk is the risk that securities held by the Fund will fluctuate in value due to general market or economic conditions, perceptions regarding the industries in which the issuers of securities held by the Fund participate, and the particular circumstances and performance of particular companies whose securities the Fund holds. In addition, while broad market measures of common stocks have historically generated higher average returns than fixed income securities, common stocks have also experienced significantly more volatility in those returns. | Same. |

Value Investing Risk. The Fund primarily invests in “value” oriented stocks which may help limit the risk of negative portfolio returns. However, these “value” stocks are subject to the risk that their perceived intrinsic values may never be realized by the market, and to the risk that, although the stock is believed to be undervalued, it is actually appropriately priced or overpriced due to unanticipated problems associated with the issuer or industry. | Similar. Because the Acquiring Fund invests in both growth and value stocks, it is subject to risks from both styles of investing, as follows: Growth and Value Risks. Stocks with growth characteristics can experience sharp price declines as a result of earnings disappointments, even small ones. Stocks with value characteristics carry the risk that investors will not recognize their intrinsic value for a long time or that they are actually appropriately priced at a low level. Because the Fund generally follows a strategy of holding stocks with both growth and value characteristics, any particular stock’s share price may be negatively affected by either set of risks. |

Capital Gain Realization Risks to Taxpaying Shareholders. Because of the focused nature of the Fund’s portfolio, the Fund is susceptible to capital gain realization. In other words, when the Fund is successful in achieving its investment objective, portfolio turnover may generate more capital gains per share than funds that hold greater numbers of individual securities. The Fund’s sale of just a few positions will represent a larger percentage of the Fund’s assets compared with, say, a fund that has hundreds of securities positions. | Same. |

10

Principal Risks | |

Acquired Fund | Acquiring Fund |

ETF Risks. The main risks of investing in ETFs are the same as investing in a portfolio of equity securities comprising the index on which the ETF is based, although lack of liquidity in an ETF could result in it being more volatile than the securities comprising the index. Additionally, the market prices of ETFs will fluctuate in accordance with both changes in the market value of their underlying portfolio securities and due to supply and demand for the instruments on the exchanges on which they are traded (which may result in their trading at a discount or premium to their net asset values.) Index-based ETF investments may not replicate exactly the performance of their specific index because of transaction costs and because of the temporary unavailability of certain component securities of the index. | No similar risk. |

Foreign Security and Emerging Market Risk. Investments in foreign securities, including investments in ADRs and emerging market securities, involve risks relating to currency fluctuations and to political, social and economic developments abroad, as well as risks resulting from differences between the regulations to which U.S. and foreign issuers and markets are subject. These risks may be greater in emerging markets. The investment markets of emerging countries are generally more volatile than markets of developed countries with more mature economies. | Same. |

Depository Receipt Risk. Depository receipts, such as ADRs, global depository receipts (“GDRs”), and European depository receipts (“EDRs”), may be issued in sponsored or un-sponsored programs. In a sponsored program, a security issuer has made arrangements to have its securities traded in the form of depository receipts. In an un-sponsored program, the issuer may not be directly involved in the creation of the program. Depository receipts involve many of the same risks as direct investments in foreign securities. These risks include, but are not limited to: fluctuations in currency exchange rates, which are affected by international balances of payments and other financial conditions; government interventions; and speculation. With respect to certain foreign countries, there is the possibility of expropriation or nationalization of assets, confiscatory taxation, political and social upheaval, and economic instability. Investments in depository receipts that are traded over the counter may also be subject to liquidity risk. | Same. |

Market Risk. The share price of the Fund reflects the value of the securities it holds. If a security’s price falls, the share price of the Fund will go down (unless another security’s price rises by an offsetting amount). If the Fund’s share price falls below the price you paid for your shares, you could lose money when you redeem your shares. | Same. |

11

Principal Risks | |

Acquired Fund | Acquiring Fund |

No similar risk. | Special Risks Associated with Dividend Paying Stocks. Raising interest rates have the potential to hurt the value and/or price of higher dividend yielding stocks more so than the overall market. In addition, higher dividend yielding stocks may go through periods of underperformance as a group versus the broader market. |

No similar risk. | Option Risk. There are several risks associated with transactions in options on securities, as follows: There are significant differences between the securities and options markets that could result in an imperfect correlation between these markets, causing a given transaction not to achieve its objectives. As the writer of a covered call option, the Fund forgoes, during the option’s life, the opportunity to profit from increases in the market value of the security covering the call option above the sum of the premium and the strike price of the call, but has retained the risk of loss should the price of the underlying security decline. The writer of an option has no control over the time when it may be required to fulfill its obligation as a writer of the option. Once an option writer has received an exercise notice, it may not be able to effect a closing purchase transaction in order to terminate its obligation under the option and must then deliver the underlying security at the exercise price. There can be no assurance that a liquid market will exist when the Fund seeks to close out an option position. If the Fund is unable to close out a covered call option that it wrote on a security, it would not be able to sell the underlying security unless the option expired without exercise. |

12

Principal Risks | |

Acquired Fund | Acquiring Fund |

No similar risk. | Interest Rate Risk. To the extent the Fund invests in fixed income securities (i.e., bonds), the Fund will be subject to interest rate risk, which is the risk that the value of your investment will fluctuate with changes in interest rates. Typically, a rise in interest rates causes a decline in the market value of income-bearing securities. When interest rates rise, bond prices fall; generally, the longer a bond’s maturity, the more sensitive it is to this risk. |

Federal Income Tax Consequences. The Funds expect that the Reorganization will constitute a “reorganization” within the meaning of Section 368 of the Internal Revenue Code of 1986, as amended (the “Code”), with substantially the following results: no gain or loss will be recognized by the Acquired Fund or its shareholders as a result of the Reorganization. The aggregate tax basis of the shares of the Acquiring Fund received by a shareholder of the Acquired Fund (including any fractional shares to which the shareholder may be entitled) will be the same as the aggregate tax basis of the shareholder’s shares of the Acquired Fund. The holding period of the shares of the Acquiring Fund received by a shareholder of the Acquired Fund (including any fractional share to which the shareholder may be entitled) will include the holding period of the shares of the Acquired Fund held by the shareholder, provided that such shares are held as capital assets by the shareholder of the Acquired Fund at the time of the Reorganization. The holding period and tax basis of each asset of the Acquired Fund in the hands of the Acquiring Fund as a result of the Reorganization will generally be the same as the holding period and tax basis of each such asset in the hands of the Acquired Fund prior to the Reorganization. It is a condition to the closing of the Reorganization that both the Acquired Fund and Acquiring Fund receive an opinion of Godfrey & Kahn, S.C. confirming these consequences, as further discussed below under “Information About the Reorganization-Federal Income Tax Consequences.” An opinion of counsel is not binding on the Internal Revenue Service.

Additional tax considerations are discussed under the section on “Information about the Reorganization-Federal Income Tax Consequences.”

Distributor; Rule 12b-1 Service Plan. MFD Distributor, LLC (“MFD”) is the Funds’ distributor. MFD’s principal business address is 550 Science Drive, Madison, Wisconsin 53711. MFD is a wholly-owned subsidiary of MIH and an affiliate of Madison. The Board of Trustees has adopted a Rule 12b-1 plan with respect to each Fund’s Class A shares pursuant to which the Funds pay for shareholder services at an aggregate annual rate of 0.25% of each Fund’s daily net assets attributable to the Class A shares. The Board of Trustees has also adopted a Rule 12b-1 plan with respect to the Acquired Fund’s Class B shares pursuant to which the Acquired Fund pays for shareholder services at an aggregate annual rate of 0.25% and distribution at an aggregate annual rate of 0.75%, in each case, based on the Fund’s daily net assets attributable to the Class B shares. For more information, please see Appendix B.

13

Other Service Providers. Deloitte & Touche LLP serves as the Funds’ independent registered accounting firm; State Street Bank & Trust Company services as the Funds’ sub-administrator, fund accountant, custodian and securities lending agent; and DST Asset Manager Solutions, Inc. serves as the Funds’ transfer agent.

Comparison of Purchase, Exchange and Redemption Procedures. The purchase, exchange redemption procedures of the Acquired Fund and the Acquiring Fund are exactly the same. While Class A shares of both Funds are subject to a front-end sales load, Class Y shares of both Funds are not. In addition, shares of both Funds are redeemed at a price equal to the NAV next determined after the redemption request is accepted in good order by the Funds. The Funds do not impose any redemption fees or contingent deferred sales charges on Class A or Class Y shares. As previously noted, the Acquiring Fund does not offer Class B shares, although the Acquired Fund does offer such share class. As a result, prior to consummation of the Reorganization, on or about August 20, 2020, Class B shares of the Acquired Fund will be converted into Class A shares of the Acquired Fund. Currently, Class B shares may not be purchased or acquired, except by exchange from Class B shares of another Madison Fund or through dividend and/or capital gains reinvestments. Class B shares do not impose a front-end sales charge that is deducted from your initial investment, but they do impose a contingent deferred sales charge (CDSC), which you pay if you sell your shares within a certain number of years. The CDSC gets smaller each year and eventually is eliminated after several years. Selling Class B shares during the period in which the CDSC applies can significantly diminish the overall return on your investment, especially when coupled with the higher annual expenses charged when you hold Class B shares. For more information, please see Appendix B.

14

INFORMATION ABOUT THE REORGANIZATION

Introduction. This Proxy Statement/Prospectus is provided to you to solicit your proxy for exercise at the Meeting to approve the Reorganization of the assets and assumption of the liabilities of the Acquired Fund by the Acquiring Fund and the subsequent liquidation and dissolution of the Acquired Fund. The Meeting will be held at 550 Science Drive, Madison, Wisconsin 53711, at 10:00 a.m. Central time on September 2, 2020. This Proxy Statement/Prospectus, the accompanying Notice of Special Meeting of Shareholders and the enclosed Proxy Card are being mailed to shareholders of the Acquired Fund on or about July 17, 2020.

Description of the Plan. The Reorganization is expected to be consummated as of the Effective Date. Under the Plan, the Acquired Fund will transfer all of its assets to the Acquiring Fund and, in exchange, the Acquiring Fund will assume all the Acquired Fund’s liabilities and will issue Class A and Class Y shares of the Acquiring Fund (the “Reorganization Shares”) to the Acquired Fund. The value of the Acquired Fund’s assets, as well as the number of Reorganization Shares to be issued to the Acquired Fund, will be determined in accordance with the Plan. The Reorganization Shares to be issued will have an aggregate NAV equal to the aggregate value of the assets received from the Acquired Fund, less the aggregate liabilities assumed by the Acquiring Fund in the Reorganization. Because the Acquiring Fund does not offer Class B shares, prior to the Reorganization, on or about August 20, 2020, all Class B shares of the Acquired Fund will be automatically converted to Class A shares of the Acquired Fund. There will be no effect on the Class B shareholders as a result of the conversion and no contingent deferred sales charges will be assessed. The Reorganization Shares will immediately be distributed to Acquired Fund shareholders in proportion to their holdings of Class A and Class Y shares of the Acquired Fund, in liquidation of the Acquired Fund. As a result, Class A shareholders of the Acquired Fund will become Class A shareholders of the Acquiring Fund, and Class Y shareholders of the Acquired Fund will become Class Y shareholders of the Acquiring Fund. The NAV of the Funds will be computed as of the close of regular trading on the New York Stock Exchange on the day prior to the Effective Date (the “Valuation Time”).

Following the distribution of the Reorganization Shares of the Acquiring Fund in full liquidation of the Acquired Fund, the Acquired Fund will wind up its affairs, cease operations and dissolve as soon as is reasonably practicable after the Reorganization. If the shareholders do not approve the Plan, the Board will consider alternative options for the Acquired Fund, including liquidation.

The projected expenses of the Reorganization, including printing and proxy solicitation expenses, legal and accounting costs, are estimated to be approximately $68,593. Not included in this estimate are portfolio repositioning costs of approximately $5,000. All such costs and expenses will be borne by Madison, not the Funds.

The Acquired Fund plans to sell approximately 4-5 securities representing 10% of the Acquired Fund’s portfolio prior to consummation of the Reorganization. In this regard, Madison expects to sell primarily mining related stocks and real estate investment trust (REIT) holdings. These positions are expected to be sold because they are not included within the Acquiring Fund’s investment model. The sale of these securities will generate gains of approximately $1.9 million, but even after realizing these gains, the Acquired Fund currently does not have a capital gain distribution requirement prior to consummation of the Reorganization as it has year-to-date net losses as of the date hereof of approximately $2.7 million. Madison expects that the Acquired Fund will have a small amount of net investment income to distribute (approximately $323,000). The Acquired

15

Fund will incur approximately $5,000 of portfolio repositioning costs in connection with the Reorganization, which will be reimbursed by Madison.

If the Plan is approved, the Reorganization will be consummated on the Effective Date and is conditioned upon satisfying the terms of the Plan. Under applicable legal and regulatory requirements, none of the Acquired Fund’s shareholders will be entitled to exercise objecting shareholders' appraisal rights (i.e., to demand the fair value of their shares in connection with the Reorganization). Therefore, shareholders will be bound by the terms of the Plan. However, any shareholder of the Acquired Fund may redeem his or her shares prior to the Effective Date.

Completion of the Reorganization is subject to certain conditions set forth in the Plan. The Plan may be amended by the Board, and may also be terminated by the Board if circumstances should develop that, in the opinion of the Board, make proceeding with the Reorganization inadvisable. The form of the Plan is attached as Appendix A.

Reasons for the Reorganization. At a meeting of the Board held on May 21, 2020 (the “Board Meeting”), Madison recommended that the Board approve and recommend to Acquired Fund shareholders for their approval the proposed Plan. At the Board Meeting, the Board reviewed detailed information provided by Madison, and considered, among other things, the factors discussed below, in light of their fiduciary duties under federal and state law. After careful consideration, the Board, including all trustees who are not “interested persons” of the Funds, with the advice and assistance of independent counsel, approved the Plan and the Reorganization, and recommended that the shareholders of the Acquired Fund vote in favor of the Reorganization by approving the Plan.

In approving and recommending the proposed Plan, the Board considered, among other things:

• | The terms of the Reorganization, including the anticipated tax-free nature of the transaction for the Acquired Fund and its shareholders; |

• | That the portfolio managers of the Acquired Fund are the same persons managing the Acquiring Fund’s portfolio, thereby resulting in continuity of investment management for the combined Fund; |

• | That the Funds’ have similar investment objectives, strategies and policies; |

• | That the Funds have similar risk profiles and while their portfolio holdings differ somewhat, both Funds concentrate their investments in securities having similar characteristics; |

• | That, despite the higher investment advisory fee charged to the Acquiring Fund, the overall expense ratios for the Acquiring Fund’s Class A and Class Y shares are lower than those of the Acquired Fund’s Class A and Class Y shares, respectively; |

• | That Madison and the distributor of the Madison Funds are committed to facilitate the future growth of the larger, combined Fund; |

• | That the Reorganization will not result in the dilution of shareholders’ interests; |

• | That the Funds will not bear the costs of the Reorganization; and |

• | Other alternatives to the Reorganization, including liquidation (which would impose transaction and other costs and would not be tax-free). |

Based on the foregoing and additional information presented at the Board Meeting, the Board determined that the Reorganization and the Plan would be in the best interests of the Funds and the interests of shareholders of the Funds will not be diluted as a result of the Reorganization. The Board concluded that the advantages associated with proceeding with the Reorganization outweighed any disadvantages that they identified as part of their review (e.g., the higher investment advisory fee for the Acquiring Fund).

16

The Board approved the Plan, subject to approval by shareholders of the Acquired Fund, and the solicitation of the shareholders of the Acquired Fund to vote “FOR” the approval of the Plan.

Description of the Securities to be Issued. The Declaration of Trust of the Trust permits the Board of Trustees to issue an unlimited number of shares of beneficial interest of each series within the Trust with no par value per share. Each Fund is a series of the Trust which offers two share classes: Class A and Class Y. The Acquired Fund also offers Class B shares, however, those shares will be converted to Class A shares of the Acquired Fund prior to consummation of the Reorganization. Under the Plan, the Acquiring Fund will issue Class A and Class Y shares for distribution to the Acquired Fund shareholders in exchange for their Class A and Class Y shares, respectively. The Class A and Class Y shares of the Acquiring Fund are identical in all respects to the Class A and Class Y shares of the Acquired Fund.

On any matter submitted to a vote of the shareholders, each shareholder shall be entitled to one vote for each dollar of net asset value standing in such shareholder’s name on the books of each Fund and class of which such shareholder owns shares which are entitled to vote on the matter. Each share of beneficial interest of each Fund shares equally in dividends and distributions when and if declared by the Fund and in the Fund’s net assets upon liquidation. All shares, when issued, are fully paid and nonassessable. The shares do not entitle the holder thereof to preference, preemptive, appraisal, conversion or exchange rights, except as the Board of Trustees may determine. Shareholders of each Fund vote, as a series of the Trust, to change, among other things, a fundamental policy of the Fund and to approve the Fund’s investment advisory contract. The Funds are not required to hold annual meetings of shareholders but will hold special meetings of shareholders when, in the judgment of the Board of Trustees, it is necessary or desirable to submit matters for a shareholder vote.

Dividends and Other Distributions. On or before the Valuation Time, the Acquired Fund may make one or distributions to shareholders. Such distributions generally will be taxable as ordinary income or capital gains to shareholders that hold their shares of the Acquired Fund in a taxable account.

Share Certificates. The Acquiring Fund will not issue certificates representing Acquiring Fund shares generally or in connection with the Reorganization. Instead, ownership of the Acquiring Fund’s shares will be shown on the books of the Acquiring Fund's transfer agent. If you currently hold certificates representing shares of the Acquired Fund, it is not necessary to surrender the certificates.

Federal Income Tax Consequences. The Reorganization is expected to qualify for federal income tax purposes as a tax-free reorganization under Section 368(a) of the Code, and thus is not expected to result in the recognition of gain or loss by either the Acquired Fund or its shareholders. As a condition to the closing of the Reorganization, subject to certain stated assumptions contained therein, the Acquired Fund and the Acquiring Fund will receive an opinion from Godfrey & Kahn, S.C. substantially to the effect that, for United States federal income tax purposes:

• | The transfer of all of the assets and liabilities of the Acquired Fund to the Acquiring Fund in exchange for Reorganization Shares and the distribution to the Acquired Fund shareholders of the Reorganization Shares will constitute a “reorganization” within the meaning of Section 368(a) of the Code, and the Acquired Fund and the Acquiring Fund will each be a “party to a reorganization” within the meaning of Section 368(b) of the Code; |

17

• | No gain or loss will be recognized by the Acquiring Fund upon its receipt of the assets of the Acquired Fund solely in exchange for the Reorganization Shares and the assumption by the Acquiring Fund of all of the liabilities of the Acquired Fund; |

• | No gain or loss will be recognized by the Acquired Fund upon the transfer of all of its assets to the Acquiring Fund solely in exchange for the Reorganization Shares and the assumption by the Acquiring Fund of all of the liabilities of the Acquired Fund; |

• | No gain or loss will be recognized by the Acquired Fund upon the distribution of the Reorganization Shares to the Acquired Fund shareholders in exchange for their shares of the Acquired Fund in complete liquidation of the Acquired Fund; |

• | No gain or loss will be recognized by the shareholders of the Acquired Fund upon the receipt of the Reorganization Shares solely in exchange for their shares of the Acquired Fund as part of the Reorganization; |

• | The aggregate adjusted tax basis of the Reorganization Shares received by a shareholder of the Acquired Fund will be the same as the aggregate adjusted tax basis of the shares of the Acquired Fund exchanged therefor by such shareholder; |

• | The holding period of the Reorganization Shares received by a shareholder of the Acquired Fund will include the holding period during which the shares of the Acquired Fund exchanged therefor were held by such shareholder, provided that at the time of the exchange, the shares of the Acquired Fund were held as a capital asset in the hands of such Acquired Fund shareholder; |

• | The aggregate tax basis of the assets of the Acquired Fund in the hands of the Acquiring Fund will be the same as the aggregate tax basis of such assets immediately prior to the transfer thereof; |

• | The holding period of each asset of the Acquired Fund in the hands of the Acquiring Fund will include the respective holding period of such assets in the hands of the Acquired Fund immediately prior to the transfer thereof; and |

• | The Acquiring Fund will succeed to and take into account the items of the Acquired Fund described in Section 381(c) of the Code, subject to any applicable conditions and limitations specified in Sections 381, 382, 383, and 384 of the Code and the regulations thereunder. |

This opinion may contain limitations that Godfrey & Kahn, S.C. deems appropriate and will be based on customary assumptions and representations that Godfrey & Kahn, S.C. reasonably requests. This opinion of counsel will not be binding on the Internal Revenue Service or a court and there is no assurance that the Internal Revenue Service or a court will not take a view contrary to those expressed in the opinion.

The ability of the Acquiring Fund to use any capital loss carryforwards of the Acquired Fund to offset future gains will be limited as a direct result of the Reorganization.

Shareholders of the Acquired Fund are encouraged to consult their tax advisers regarding the effect, if any, of the Reorganization in light of their individual circumstances. Because the foregoing only relates to the federal income tax consequences of the Reorganization, those shareholders also should consult their tax advisers as to state and local tax consequences, if any, of the Reorganization.

18

Capitalization Information. The following table shows the capitalization of each of the Funds as of April 30, 2020, and on a pro forma combined basis, giving effect to the acquisition of the assets and liabilities of the Acquired Fund by the Acquiring Fund at net asset value as of April 30, 2020:

Share Class | Acquired Fund | Acquiring Fund | Pro Forma Adjustments | Acquired Fund Pro Forma Combined | ||||||||

Class A: | ||||||||||||

Net Assets | $ | 48,415,933 | — | $ | 1,510,378 | $ | 49,926,311 | |||||

Shares Outstanding1 | 4,493,542 | — | 140,239 | 4,633,781 | ||||||||

Net Asset Value per Share | $ | 10.77 | — | — | $ | 10.77 | ||||||

Class B2: | ||||||||||||

Net Assets | $ | 1,510,378 | — | $ | (1,510,378 | ) | — | |||||

Shares Outstanding1 | 144,391 | — | (144,391 | ) | — | |||||||

Net Asset Value per Share | $ | 10.46 | — | — | — | |||||||

Class Y: | ||||||||||||

Net Assets | $ | 1,487,728 | $ | 193,797,254 | — | $ | 195,284,982 | |||||

Shares Outstanding1 | 138,549 | 7,994,958 | (77,174 | ) | 8,056,333 | |||||||

Net Asset Value per Share | $ | 10.74 | $ | 24.24 | — | $ | 24.24 | |||||