United States

Securities and Exchange Commission

Washington, D.C. 20549

Form 10-K

Annual Report Pursuant to Section 13 or 15(d) of the Securities Act of 1934

For the fiscal year ended December 31, 2015 Commission File Number 1-13145 | ||

Jones Lang LaSalle Incorporated

(Exact name of registrant as specified in its charter)

Maryland | 36-4150422 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

200 East Randolph Drive, Chicago, IL | 60601 | |

(Address of principal executive offices) | (Zip Code) | |

Registrant's telephone number, including area code: 312-782-5800 | ||

Securities registered pursuant to Section 12(b) of the Act: | ||

Title of each class | Name of each exchange on which registered | |

Common Stock ($.01 par value) | New York Stock Exchange | |

Securities registered pursuant to Section 12(g) of the Act: None | ||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [ X ] No [ ]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes [ ] No [ X ]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [ X ] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such period that the registrant was required to submit and post such files). Yes [ X ] No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer (as defined in Rule 12b-2 of the Exchange Act). Large accelerated filer [ X ] Accelerated filer [ ] Non-accelerated filer [ ]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes [ ] No [ X ]

The aggregate market value of the voting stock (common stock) held by non-affiliates of the registrant as of the close of business on July 1, 2015 was $7,705,853,898.

The number of shares outstanding of the registrant's common stock (par value $0.01) as of the close of business on February 22, 2016 was 45,085,160.

Portions of the Registrant's Proxy Statement for its 2016 Annual Meeting of Shareholders are incorporated by reference in Part III of this report.

TABLE OF CONTENTS | ||

Item 1. | Business | |

Item 1A. | Risk Factors | |

Item 2. | Properties | |

Item 3. | Legal Proceedings | |

Item 4. | Mine Safety Disclosures | |

Item 5. | Market for Registrant's Common Equity, Related Shareholder Matters and Issuer Purchase of Equity Securities | |

Item 6. | Selected Financial Data (Unaudited) | |

Item 7. | Management's Discussion and Analysis of Financial Conditions | |

Item 7A. | Quantitative and Qualitative Disclosures About Market Risks | |

Item 8. | Financial Statements and Supplementary Data | |

Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosures | |

Item 9A. | Controls and Procedures | |

Item 9B. | Other Information | |

Item 10. | Directors and Executive Officers of the Registrant | |

Item 11. | Executive Compensation | |

Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Shareholder Matters | |

Item 13. | Certain Relationships and Related Transactions | |

Item 14. | Principal Accountant Fees and Services | |

Item 15. | Exhibits and Financial Statement Schedules | |

Power of Attorney | ||

Signatures | ||

Exhibit Index | ||

International Integrated Reporting Council Cross Reference | ||

ITEM 1. BUSINESS

COMPANY OVERVIEW

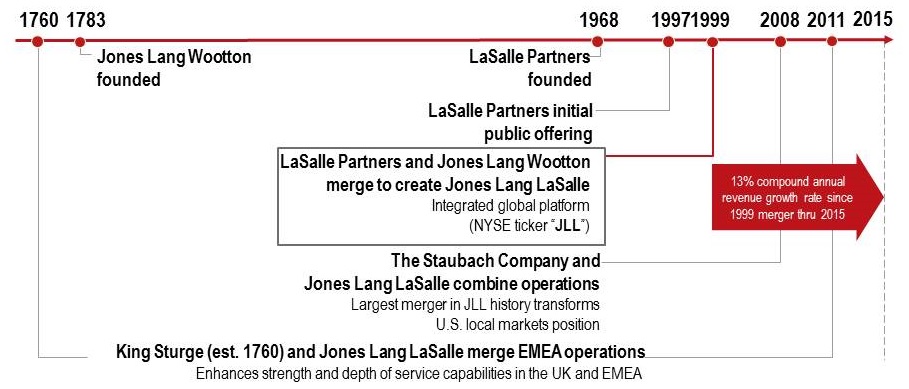

Jones Lang LaSalle Incorporated ("Jones Lang LaSalle," which we may refer to as "JLL," "we," "us," "our," the "Company" or the "Firm") was incorporated in 1997. Our common stock is listed on The New York Stock Exchange under the symbol "JLL."

We are a Fortune 500 financial and professional services firm specializing in real estate. We offer comprehensive integrated services on a local, regional, and global basis to owner, occupier, investor, and developer clients seeking increased value by owning, occupying, or investing in real estate. We have more than 280 corporate offices worldwide from which we provide services to clients in more than 80 countries. We have over 60,000 employees, including 32,700 employees whose costs our clients reimburse. Our issuer and senior unsecured ratings are investment grade: BBB+ (stable outlook) from Standard & Poor’s Ratings Services ("S&P") and Baa2 (positive outlook) from Moody’s Investors Service, Inc. ("Moody’s").

Over the ten years ended December 31, 2015, the fee revenue of the Firm has grown at a 14% compound annual growth rate. We have grown our business by expanding our client base and the range of our services and products, both organically and through a series of strategic acquisitions and mergers. Our extensive global platform and in-depth knowledge of local real estate markets enable us to serve as a single-source provider of solutions for the full spectrum of our clients' real estate needs. We began to establish this network of services across the globe through the 1999 merger of the Jones Lang Wootton companies ("JLW", founded in England in 1783) with LaSalle Partners Incorporated ("LaSalle Partners", founded in the United States in 1968).

We use JLL as our principal trading name. Jones Lang LaSalle Incorporated remains our legal name. JLL is a registered trademark in the countries in which we do business, as is our logo:

Using the shorter JLL name in the marketplace is a natural evolution of the firm's historically rich brand, recognizing that it is a truly global company located in multiple markets, with a wide range of expertise applied through many different client services. It also represents its adaptation to different communication styles in different countries, languages and channels, and especially the use of digital and online channels for marketing and communications.

JLL delivers an array of Real Estate Services ("RES") across three geographic business segments: (1) the Americas, (2) Europe, Middle East and Africa ("EMEA") and (3) Asia Pacific.

LaSalle Investment Management, which uses LaSalle as its principal trading name, is a wholly-owned member of the Jones Lang LaSalle Incorporated group and our fourth business segment. LaSalle is one of the world's largest and most diversified real estate investment management firms. Over the ten years ended December 31, 2015, the assets under management have grown from $30.0 million to $56.4 billion, a 6.5% compound annual growth rate. LaSalle is a registered trademark in the countries in which we conduct business, as is our logo:

In 2015, we generated record-setting fee revenue of $5.2 billion across our four business segments, a 17% increase over 2014 in local currency. We believe we remain well-positioned to take advantage of the opportunities in a consolidating industry and to navigate successfully the dynamic and challenging markets in which we compete worldwide.

We are proud to be a preferred provider of global real estate services, an employer of choice, a consistent winner of industry awards, and a valued partner to the largest and most successful companies and institutions in the global marketplace.

For discussion of our segment results, please see "Results of Operations" and "Market Risks" within Item 7, Management's Discussion and Analysis of Financial Condition and Results of Operations, as well as Note 3, Business Segments, in the Notes to Consolidated Financial Statements.

3

Awards

We won numerous awards with respect to 2015, reflecting the quality of the services we provide to our clients, the integrity of our people and our desirability as a place to work. As examples, we were named:

• | World’s Best Property Consultancy, International Property Awards Grand Final 2015 |

• | Best Consultancy in Asia, International Property Awards Grand Final 2015 |

• | Global Real Estate Company of the Year (LaSalle), Estates Gazette |

• | Core Property Manager of the Year (LaSalle), Professional Pensions |

• | Pan-European Property Manager of the Year (LaSalle), Professional Pensions |

• | Japan Firm of the Year (LaSalle), 2015 Global PERE Awards |

• | For the eighth consecutive year, one of the World's Most Ethical Companies, the Ethisphere Institute |

• | 100 Best Corporate Citizens (#20), CR Magazine |

• | For the seventh consecutive year, one of the Global Outsourcing 100 - International Association of Outsourcing Professionals |

• | World’s Most Admired Companies, Fortune Magazine |

• | 50 Out Front for Diversity Leadership: Best Places for Women & Diverse Managers to Work, Diversity MBA Magazine |

• | As having a perfect score on the Human Rights Campaign Foundation's 2015 Corporate Equality Index, a national benchmarking survey on corporate policies and practices related to LGBT workplace equality |

• | As a Winning "W" Company and were listed on the 2020 Honor Roll by the 2020 Women on Boards |

• | As having one of the Best Law Departments in the US real estate industry, by The Legal 500 |

• | One of the Best Places to Work by a number of local publications world-wide |

• | 2015 Energy Star Sustained Excellence Award by the U.S. Environmental Protection Agency |

• | Energy Star Climate Communications Award, U.S. Environmental Protection Agency |

• | Excellence in Global Corporate Governance, India Institute of Directors |

Services and Clientele

The broad range of real estate services we offer includes (in alphabetical order):

Agency Leasing | Project and Development Management / Construction |

Capital Markets | Property Management (Investors) |

Corporate Finance | Real Estate Investment Banking / Merchant Banking |

Energy and Sustainability Services | Research |

Facility Management Outsourcing (Occupiers) | Strategic Consulting and Advisory Services |

Investment Management | Tenant Representation |

Lease Administration | Transaction Management |

Logistics and Supply-Chain Management | Valuations |

Mortgage Origination and Servicing | Value Recovery and Receivership Services |

We offer these services locally, regionally and globally to real estate owners, occupiers, investors and developers for a variety of property types, including (in alphabetical order):

Critical Environments and Data Centers | Infrastructure Projects |

Cultural Facilities | Military Housing |

Educational Facilities | Office Properties |

Government Facilities | Residential Properties (Individual and Multifamily) |

Healthcare and Laboratory Facilities | Retail Properties and Shopping Malls |

Hotels and Hospitality Facilities | Sports Facilities |

Industrial and Warehouse Properties | Transportation Centers |

Individual regions and markets may focus on different property types to a greater or lesser extent depending on local requirements, market conditions and the strength of the business opportunities we perceive from time to time.

4

We work for a broad range of clients. They represent a wide variety of industries in markets throughout the world. Our clients vary greatly in size and complexity. They include for-profit and not-for-profit entities of all kinds, public-private partnerships, and governmental ("public sector") entities. Increasingly, we are also offering services to middle-market companies seeking to outsource real estate services. Through LaSalle, we invest for clients on a global basis in publicly traded real estate securities, private real estate assets, and debt obligations. As an example of the breadth and significance of our client base, we provide services to approximately half of the Fortune 500 companies and approximately 75% of the Fortune 100 companies.

We believe our market reach strengthens the long-term value of the enterprise in a number of ways, including by: (1) reducing the potential impact of episodic volatility or disruption in any specific region; (2) enhancing the expertise of our people through knowledge sharing among colleagues across the globe; and (3) allowing us to identify and react to emerging trends and risks quickly.

Distinguishing Attributes

The attributes that enhance our services and distinguish our Firm, some of which we discuss in more detail below under "Competitive Differentiators," include:

• | Our focus on client relationship management as a means to provide superior client service on an increasingly coordinated basis; |

• | Our integrated global services platform; |

• | The quality and worldwide reach of our industry-leading research function, enhanced by applications of technology and our ability to synthesize complex information into practical advice for clients; |

• | Our reputation for consistent and trustworthy service delivery worldwide, as the result of our creation of best practices and by the skills, experience, collaborative nature, and integrity of our people; |

• | Our ability to deliver innovative solutions and technology applications to assist our clients in maximizing the value of their real estate portfolios; |

• | Our local market knowledge; |

• | The strength of our brand and reputation; |

• | The strength of our financial position; |

• | Our high staff engagement levels; |

• | Our efforts to deliver the best possible returns for investment management clients; |

• | The quality of our internal governance and enterprise risk management; |

• | Our history of delivering strong investment performance for LaSalle clients; |

• | The management of our supply chain for the benefit of the project management, facilities and property management, and other services we provide to clients; and |

• | Our sustainability leadership agenda, which addresses the long-term financial, environmental and social risks and opportunities for ourselves and our clients. |

5

JLL History and Acquisition Activities

Prior to our incorporation in Maryland in April 1997 and our initial public offering (the "Offering") of 4,000,000 shares of common stock in July 1997, JLL conducted its real estate services and investment management businesses as LaSalle Partners Limited Partnership and LaSalle Partners Management Limited Partnership (collectively, the "Predecessor Partnerships"). Immediately prior to the Offering, the general and limited partners of the Predecessor Partnerships contributed all of their partnership interests in the Predecessor Partnerships in exchange for an aggregate of 12,200,000 shares of common stock.

In March 1999, LaSalle Partners merged its business with that of JLW and changed its name to Jones Lang LaSalle Incorporated. In connection with the merger, we issued 14,300,000 shares of common stock and paid cash consideration of $6.2 million.

Since 2005, we have completed more than 80 acquisitions as part of our global growth strategy. These strategic acquisitions have given us additional share in key geographical markets, expanded our capabilities in certain service areas, and further broadened the global platform we make available to our clients. These acquisitions have also increased our presence and product offering globally, and have included acquisitions in the following countries:

Australia | India | Portugal |

Brazil | Indonesia | Singapore |

Canada | Ireland | South Africa |

Dubai | Japan | Spain |

Finland | Malaysia | Sweden |

France | Netherlands | Turkey |

Germany | Philippines | United Kingdom |

Hong Kong | Poland | United States |

In January 2006, we acquired Spaulding & Slye, a privately held real estate services and investment company with 500 employees that significantly increased the Firm's market presence in New England and Washington, D.C.

In a multi-step acquisition starting in 2007, we acquired the former Trammell Crow Meghraj ("TCM"), one of the largest privately held real estate services companies in India. We have combined TCM's operations with our Indian operations and we now operate under the JLL brand name throughout India.

In May 2008, we acquired Kemper's Holding GmbH, making us the largest retail property advisor in Germany.

In July 2008, we acquired Staubach Holdings Inc. ("Staubach"), a U.S. real estate services firm specializing in tenant representation. Staubach, with 1,000 employees, significantly enhanced our presence in key markets across the United States and made us an industry leader in local, national and global tenant representation. The acquisition also established us as the market leader in public sector services and added scale to our industrial brokerage, investment sales, corporate finance and project and development services.

6

In May 2011, we completed the acquisition of King Sturge, a United Kingdom-based international property consultancy. The King Sturge acquisition, which extended our historical roots back to its founding in 1760, significantly enhanced the strength and depth of our service capabilities in the United Kingdom and in continental Europe, adding approximately 1,400 employees.

Acquisitions from 2012 through 2014

During the period from January 1, 2012 through December 31, 2014, we completed 19 new acquisitions. The entire list of the specific acquisitions is set forth in the About section of our public website.

Acquisitions During 2015

In 2015, we completed 20 new acquisitions that expanded our capabilities in key regional markets as follows:

Acquired Company | Country | Business |

Five D | Australia | Facilities management |

Propell National Valuers | Australia | Integrated valuations services |

HFM | Canada | Commissioning services |

CMM Projekt & Office Solutions | Germany | Design and fit-out services |

Guardian Property Asset Management | Ireland | Residential agency services |

Tansei Mall Management | Japan | Retail property management |

Neo-Świat | Poland | Design and fit-out services |

AGL | Sweden | Real estate financial advisory |

Nextport | Sweden | Tenant representation and relocation management |

AVM Partners | Turkey | Retail property management and leasing |

Avenue9 | United Kingdom | IT consulting for the hotels and hospitality sector |

Bluu | United Kingdom | Design and fit-out services |

CoR Advisors | United States | Smart-building consulting and solutions |

Corrigo | United States | Cloud-based facility management software and services |

Cresa South Florida | United States | Tenant representation |

Lodgetax | United States | Hotel real estate tax services and consulting |

Martin Potts & Associates | United States | Project and construction management services |

Oak Grove Capital | United States | Debt financing for multifamily and senior housing |

Shelter Bay Retail Group | United States | Retail property management |

Wilson Retail Group | United States | Retail brokerage and capital markets |

We will continue to consider acquisitions that we believe will strengthen our market positions, expand our service offerings, increase our profitability, and supplement our organic growth.

Value Drivers for Providing Superior Client Service and Prospering as a Sustainable Enterprise

Our mission is to deliver exceptional strategic fully-integrated services, best practices, and innovative solutions for real estate owners, occupiers, investors, and developers worldwide. We deliver a combination of services, expertise, and technology applications on an integrated global platform that we own (and do not franchise), the totality of which we believe distinguishes us from our competitors and contributes to service excellence and customer loyalty. While we face high-quality competition in individual markets, we believe the following attributes make us the best choice for clients seeking real estate and investment management services on a worldwide basis:

• | We have the size and scale of resources necessary to deliver the expertise of the Firm wherever clients need it; |

• | Our culture of client service, teamwork, and integrity means that we can marshal those resources to deliver the greatest possible value and results; |

• | Our "client first" and ethical orientation means that our people focus on how we can best provide what our clients need and want, with integrity and transparency; |

• | Our governance and enterprise risk management orientation means that we have built an enterprise that clients can rely on over the long-term; |

• | Our strong intellectual capital, our long-term approach to business, and our ability to anticipate, interpret, and respond to the trends influencing our industry sector mean that we are quick and nimble in adapting to new challenges and opportunities in a fast changing world and in helping our clients to do the same. |

7

In their totality, these aspects affirm our commitment to sustaining our business over the long term. We seek to successfully manage the financial, environmental and social risks and opportunities our complex organization faces, and help our clients do the same. Under the new title, Building A Better Tomorrow (sm), during 2016 we will be reorganizing our sustainability communications and strategy globally.

Global Governance Structure

To achieve our mission, we must establish and maintain an enterprise that will sustain itself over the long term for the benefit of all of our stakeholders: clients, shareholders, employees, suppliers and communities, among others. Accordingly, we have committed ourselves to effective corporate governance that reflects best practices and the highest level of business ethics. For a number of years, we have governed the organization through a highly coordinated framework within which decisions are deliberated and corporate authority is derived.

GLOBAL STRATEGIC PRIORITIES

To continue to create on-going value for our clients, shareholders, and employees, both from current and longer-term perspectives, we have identified five strategic priorities, which we call the G5. We have consistently used the G5 approach since 2005. Although we have grown significantly over the past decade, we believe we have a substantial opportunity to continue to grow and prosper by providing our core services within our key markets, whose potential remains large given the global magnitude of commercial and residential real estate, broadly defined. From time to time we may add adjacent services that are not part of our historical core functions, but we intend these to be opportunistic in nature and targeted to individual geographical locations and evolving business opportunities. For example, we successfully expanded the cross-border brokerage of high-end residential properties in London with the 2011 King Sturge merger, followed by the acquisition of W.A. Ellis during 2014 and Guardian in Dublin in 2015. We have expanded the Tetris-branded fit-out business we originally acquired in France and have been introducing it into other countries, including through acquisitions in Portugal in 2014 and in Poland, Germany, and the United Kingdom in 2015. In 2015, we enhanced our service offering for facility management clients by acquiring a cloud-based technology platform called Corrigo.

8

We regularly re-evaluate whether the G5 continue to be the right priorities for best driving the business forward toward the overall objective of on-going value creation.

G1: Build our Leading Local and Regional Service Operations

Our strength in local and regional markets contributes to the strength of our global service capabilities. Our financial performance also depends, in great part, on the business we source and execute locally from our more than 280 wholly-owned offices around the world. We continually seek to leverage our established business presence in the world's principal real estate markets to provide expanded and adjacent local and regional services without a proportionate increase in infrastructure costs. We believe these capabilities will continue to fuel our competitive advantage and make us more attractive to current and prospective clients, as well as to revenue-generating employees such as brokers and client relationship managers.

Metrics: During 2015, we completed approximately 35,500 transactions for landlord and tenant clients, a 6% increase over 2014, representing 1.1 billion square feet of space.

G2: Strengthen our Leading Position in Corporate Solutions

The accelerating trends of globalization, cost cutting, energy management and the outsourcing of real estate services by corporate occupiers support our decision to emphasize a truly global Corporate Solutions business that serves the comprehensive needs of corporate clients. This service delivery capability helps us create new client relationships, particularly as companies turn to outsourcing their real estate as a way to manage expenses and to implement sustainable practices. These services have proved to be counter-cyclical, as we have seen demand for them strengthen when the economy has weakened.

Metrics: During 2015, we provided corporate facility management services for 1.3 billion square feet of clients' real estate, a 17% increase from 2014. Over the same period, JLL had 137 new business wins, 75 expansions of existing relationships and 35 contract renewals.

G3: Capture the Leading Share of Global Capital Flows for Investment Sales

Our focus on further developing our ability to provide global Capital Markets services reflects the increasingly international nature of cross-border money flows into real estate and the global marketing of real estate assets. Our real estate investment banking capability helps provide capital and other financial solutions by which our clients can maximize the value of their real estate.

Metrics: During 2015, we provided capital markets services for $138 billion of client transactions, a 17% increase from 2014.

9

G4: Strengthen LaSalle Investment Management's Leadership Position

With its integrated global platform, LaSalle is well-positioned to serve institutional investors looking for attractive real estate investment opportunities around the globe. LaSalle also continues to develop its ability to serve individual retail investors, particularly in the U.S. and Japan. LaSalle develops and implements strategies based on a thorough understanding of investor objectives and knowledge of local market risks and rewards. We intend to continue to maintain strong offerings in core products to meet the demand from clients who seek lower risk investments in the most stable and mature real estate markets. In addition, we continue to strengthen our capabilities in value-add, opportunistic and debt strategies to meet the diverse range of our clients' objectives.

Metrics: At the end of 2015, LaSalle had assets under management of $56.4 billion, an increase of 5% over 2014, while raising $5.0 billion of capital.

G5: Connections: Differentiate and Sustain the Organization by Connecting Across the Firm and with Clients and other Stakeholders

Connecting. To create real value and new opportunities for our clients, shareholders, and employees, we regularly work to strengthen and fully leverage the links between our people, service lines, and geographies to better connect with our clients and put the Firm's global expertise and experience to work for them. This includes constantly striving to strengthen our data and analytics capabilities, and to leverage use of the Internet and emerging social media to gather, analyze, and disseminate information that will be useful to our clients, employees, vendors, and other constituencies. Linking our operations effectively to make service delivery more efficient not only serves client needs, it also contributes to our profitability and enhances our ability to identify and manage the enterprise risks inherent in our business.

Differentiating and Sustaining. We also recognize that the value we deliver to our clients, shareholders, employees, and the global community closely relates to our Firm's people, brand, ethics, and technology. As a professional services company, the focus on our people is paramount. Because our human capital contributes strongly to high-quality client service, this includes a focus on areas such as: employee satisfaction; health, safety and well-being; training and career development and rewards and recognition; and diversity and inclusion. Coupled with a strong brand and high ethical standards, our active role as good corporate citizens enables our long-lasting presence. Our use of technology to provide information to our clients and to improve the ability of our people play an undeniable role in maximizing our clients' real estate value, shaping our industry's response to global challenges such as market risk, climate change and urbanization. These values and culture help us embed sustainability principles throughout the enterprise and successfully differentiate us from our competition, therefore ensuring we continue our more than 250-year history.

Metrics: Our Employee Engagement Index, which measures the percentage of survey respondents reporting high levels of engagement with the Firm and their work reached 76% as measured in 2015, up 3 percentage points from 2012, the last time we completed a full survey. Substantially all of the results in the survey improved over 2012 and also were higher than the global norms reported by our independent survey provider.

From Google Analytics, we understand our website received over 20.5 million page views by more than 4.8 million visitors in 2015.

Future Development of the G5

We have committed resources to each of the G5 priorities in past years and expect to continue to do so in the future. This strategy has helped us weather economic downturns, continue to grow market share, expand our services by developing adjacent offerings, and take advantage of new opportunities.

Our strategic review has validated the continued potential for our G5 priorities to drive the long-term sustained growth of our firm and deliver real value to our clients. To derive the full advantage of that potential, we recognize the need to accelerate the development of the G5 to meet the challenges of our dynamic markets and the specific themes we have identified such as globalization and urbanization. We will do this by targeting our efforts and capital resources to:

• | Deploy innovative technology that allows our people to mine the depth of our intellectual property to provide the most sophisticated possible advice and service to our clients. |

Examples: HiRise (sm), Blackbird (sm) and RED systems bring digital capabilities for managing real estate needs directly to clients in multiple ways (all available on-line through our public website).

• | Apply best practices in human resources to supply our businesses with well-trained, engaged and diverse employees and create an overall culture that serves to retain our top talent. |

Examples: Develop and implement a new electronic learning management system by Human Resources for use globally.

10

• | Promote an updated and modern brand that fully leverages our digital capabilities and clearly reflects the breadth of our expertise, wisdom, governance and integrity. |

Examples: Adapting the JLL and LaSalle names and refreshing their logos; acquiring the rights to the dot jll (.jll) and dot lasalle (.lasalle) top-level domain names.

• | Establish and standardize tools and processes that make our operations highly productive and minimize losses from enterprise risk. |

Examples: Implementing significant new document management system for legal and other client documentation in our Corporate Solutions business.

By continuing to invest in the future based on how our strengths can support the needs of our clients, we intend to enhance our position as an industry leader. Although we have validated our fundamental business strategies, each of our businesses continually re-evaluates how it can best serve our clients as their needs change, as technologies and the application of technologies evolve, and as real estate markets, credit markets, economies, and political environments exhibit changes, which in each case may be dramatic and unpredictable.

STRATEGY 2020: OUR FUTURE ORIENTATION

During 2015, we continued to implement our Strategy 2020, which we first launched to identify specific business and operational strategies we believe will best drive the continued success of the G5 priorities over the longer term. They include:

• | Employing an investment philosophy and filters that are focused on growth that will best meet client needs and concentrate on the most lucrative potential services, markets and cities; |

• | Establishing charters for internal business boards with responsibility for promoting more inter-connected global approaches, where appropriate, to client services and delivery; |

• | Using technology, including emerging digital, Internet and social media capabilities, to provide information to clients to help them maximize the value of their real estate portfolios and to mine and apply our knowledge to improve the ability of our people to provide superior client services; |

• | Deploying additional tools and metrics that will make our people as productive and efficient as possible; |

• | Determining how best to marshal, train, recruit, motivate and retain the human resources that will have the skill sets, diversity and other abilities necessary to accomplish our strategic objectives; |

• | Continuing to develop our brand and reputation for high quality client service, integrity and intimate local and global market knowledge; |

• | Building our brand in digital and social media channels; and |

• | Continuing to promote best-in-class governance, compliance, enterprise risk management and professional standards to operate a sustainable organization capable of meeting the significant challenges and risks inherent in global markets and to minimize disruptions to, and distractions from, the accomplishment of our corporate mission. |

Viewed as complementary strategies, the G5 and Strategy 2020 work in combination to provide both short- and long-term paths to sustained success for our Firm.

As a professional services organization, the principal capitals we deploy are (1) human resources enabled by (2) intellectual property in the form of market knowledge, technology, innovation, and a reputation for quality, expertise, and integrity that is reflected by the strength of our brand, and (3) financial resources. Our Strategy 2020 review confirmed that the historical approach we have taken to our business should sustain us in the future. We believe there is ample room for growth within our core markets and competencies without having to resort to particularly different business lines to continue to grow and prosper as a business organization. We will, however, maintain an open mind about moving into adjacent businesses where local teams identify specific opportunities, as our clients and industry evolve, and as new technologies develop that could support our business.

We also believe that our historical approach to growth through a combination of organic development of talent and opportunistic acquisitions continues to be the best overall approach for us. Our business model has natural risk mitigation benefits derived from the diversity of our geographic presence, asset classes served, and complementary service lines. This diversity also provides revenue streams that have both short-term transactional and longer-term annuity characteristics.

During 2015, we continued to devote significant efforts and resources to implement our 2020 strategies and priorities through the deployment of cross-functional workstreams that have engaged our leadership globally. We expect these workstreams to continue for the foreseeable future and we have put a mechanism in place for both our Board of Directors and our Global Executive Board to monitor and influence their progress on a regular basis.

11

Our Strategy 2020 identified particular challenges we will need to confront to successfully achieve its goals:

• | In terms of our financial capital, we recognize the challenge of maintaining healthy short-term profit margins while continuing to invest in the further growth of the business. As there is constant fee pressure from our clients that is inherent in a competitive professional services environment, we need to continue to find new ways to increase the productivity of our people so that we can drive higher revenue per person. Additional productivity can be derived by improved application of technology, by continuous process improvements, and through increased staff well-being and training and development, among other techniques. |

Example: We now report revenues per professional in our quarterly operating reviews to senior management.

• | In terms of our human capital, we recognize that our investments in talent will continue to be a primary method of creating long-term value and that continuing business growth will necessitate the growth and increased flexibility and diversity of our workforce. This can be a challenge, particularly in emerging markets, where the available pool of talent does not necessarily have the skill sets we need. Consequently, we may need to establish our own training programs beyond what is typically required for companies in developed markets. Increased reliance on third-party suppliers may create challenges in terms of due diligence, performance management, and ensuring that third-party personnel have the same level of commitment and integrity as we demand from our own people. In developed markets, the challenge of growing a workforce with the requisite skill sets can be frustrated by the targeted efforts of competitors to hire away our people, including sometimes by offering above-market compensation. |

Example: We now report diversity statistics in our quarterly operating reviews to senior management.

• | In terms of our intellectual capital, we recognize the challenge of continuing to identify innovations through which we can provide increasingly valuable services to our clients, including as the result of developing, identifying, and successfully applying new technologies to our business processes. We also must confront the challenges inherent in managing and mining the significant data in our systems so that it can be made useful to our people and maximized in terms of our ability to analyze it in a sophisticated way for the benefit of our clients. As we develop our intellectual capital, we need to make sure our brand, and the awareness it generates in the marketplace, keeps pace with our capabilities and the messages we want associated with them in the minds of current and prospective clients, employees, and other third parties in the business community and society at large. |

Example: Our U.S. business runs an annual innovation competition to identify cutting-edge approaches that will benefit clients, which we then evaluate in terms of potential patent applications.

INTEGRATED REPORTING

Initially as a pilot company from 2012-2014 and now as a part of the business network of the International Integrated Reporting Council ("IIRC"), we support the general principles designed to promote communications and integrated thinking about how an organization's strategy, governance, and financial and non-financial performance lead to the creation of value over the short, medium and long term. This Annual Report on Form 10-K focuses on our business strategy and our financial performance, including an initial attempt to illustrate how being a sustainable enterprise is integral to our success. Our citizenship and sustainability efforts for ourselves and our clients are reflected primarily in our annual Global Sustainability Report.

Our governance and remuneration practices are reported primarily in the Proxy Statement for our Annual Meeting of Shareholders. The mechanisms we use to provide confidence to our clients with respect to our transparency and fair dealing are summarized in our Transparency Report, which we first published in 2013. The behaviors and standards we expect of our employees and of the suppliers we engage for our own firm and on behalf of clients are presented in our Code of Business Ethics and our Vendor Code of Conduct. Our Corporate Facts document is intended to provide an overall summary of the information we believe will be of primary interest to our different stakeholders.

We intend this Annual Report to satisfy the requirements of the International <IR> Framework issued by the IIRC in December, 2013 (www.theiirc.org). Following the Exhibit Index, we present a tie-out sheet that cross-references the requirements in the Framework and the locations of our responses within this Annual Report.

We have recently launched an electronic Integrated Report on our website which provides access to all of our information embedded in the documents discussed above through one access portal.

Responsibility for Integrated Reporting. The Finance and Legal Services functions of our Company are primarily responsible for the integrity of our integrated reporting efforts and acknowledge that we have applied a collaborative approach in the preparation and presentation of this report. To do so, we have also engaged the members of our Global Operating Board ("GOB"), which consists of the leaders of our corporate staff functions in addition to others and is described below in more detail, with respect to the preparation of the information presented in Items 1 (Business) and 1A (Risk Factors). In our collective opinion, this report is presented in accordance with the Framework. However, as our effort to comply with the Framework is done voluntarily, we disclaim any legal liability to the extent that this report is deemed to not comply with the Framework.

12

Alignment with the Integrated Reporting Framework. Building on the Strategy 2020 and as an important part of our aim to align more closely with the Integrated Reporting Framework, we began to identify the medium- to long-term global megatrends with the greatest potential to impact materially upon our business. To do this, we used the 'six capitals' model advocated by the International Integrated Reporting Council, namely financial, human, intellectual, manufactured, social, and natural capitals.

While we are most heavily dependent on the financial, human, and intellectual capitals to execute our own operations successfully, we identified significant trends with implications for our business across all six capitals. Furthermore, changes in the availability of all six capitals impact our clients’ businesses, and by extension, our service provision. An example in 2015 was the effect of significantly lower oil prices on the financial ability of energy-related companies to improve their real estate assets. Through internal consultation, we identified a number of trends as significant for our business in the medium to long term. All of these "Global Trends," which we are tracking and/or actively managing, are illustrated below. The "JLL Activities," which address these trends, are summarized in the table below primarily via a combination of references to (1) sections within Items 1 and 1A in this Annual Report on Form 10-K and (2) resources we publish on our website, where we discuss relevant points in more detail.

Type of Capital | Global Trends | JLL Activities |

Financial | Continued risk of financial crises | Maintaining our financial strength as a differentiator; Financial Risk Factors Enterprise Risk Management; Strategic Risk Factors |

Potential increase in disruptive market cycles | Enterprise Risk Management; Strategic Risk Factors; Financial Risk Factors | |

Shift towards emerging markets | G1: Build our Leading Local and Regional Service Operations Strategy 2020 focus on potential growth markets and cities | |

Regulatory reform in banking & other sectors | Enterprise Risk Management; Operational Risk Factors; Legal and Compliance Risk Factors | |

Growth increasingly dependent on productivity gains | Strategy 2020 focus on productivity | |

Global push against tax avoidance | Enterprise Risk Management; Strategic Risk Factors; Financial Risk Factors; Legal and Compliance Risk Factors | |

Human | Changing demographics affects workplace profiles | Enterprise Risk Management; Operational Risk Factors |

Growing importance of technology in the workplace | G5: Connections Strategy 2020 Internal HR programs for data & technology and social media | |

Evolving leadership needs | Leadership pipeline development program | |

Diversity is equated with "good business" | Strategy 2020 Global Sustainability Report 2014 (on our website) Diversity and Inclusion Report (on our website) | |

Intellectual | Increased risk of cyber-attacks and data theft | Enterprise Risk Management; Operational Risk Factors |

Intellectual capital becomes increasingly disseminated | Strategy 2020 focus on technology, digital and social media Enterprise Risk Management; Operational Risk Factors | |

Digital technology transforms how people live and work | Strategy 2020 focus on technology, digital and social media | |

Manufactured | Urbanization trends, including rapid urbanization and ‘megacities' | G1: Build our Leading Local and Regional Service Operations Strategy 2020 focus on potential growth markets and cities JLL Cities Research Centre (on our website) |

Changing levels of demand for different types of real estate | Strategy 2020 focus on most lucrative potential services JLL Research | |

Expansion of the global investable real estate universe | G3: Capture the Leading Share of Global Capital Flows for Investment Sales G4: Strengthen LaSalle Investment Management's Leadership Position | |

Social | Unprecedented levels of transparency | Code of Business Ethics and Corporate Sustainability Transparency Report 2014 (on our website) Enterprise Risk Management; Strategic Risk Factors |

Increasing political instability and conflict | Enterprise Risk Management; Strategic Risk Factors | |

Businesses need to demonstrate social contribution | Global Sustainability Report 2014 (on our website) | |

Natural | Increase in extreme weather events | Enterprise Risk Management; Strategic Risk Factors Global Sustainability & Cities Research |

Natural resources in increasingly short supply | Enterprise Risk Management; Operational Risk Factors Global Sustainability Report 2014 (on our website) | |

13

Our Materiality Process. In 2014, JLL identified its long-term risks and opportunities with a view to furthering our integrated reporting journey. This effort complemented our Enterprise Risk Management processes; enabled further engagement with internal executives; prioritized our long-term risks and opportunities to generate further business value based on the IIRC’s guidance; and will help us articulate how we are managing and taking advantage of long-term risks and opportunities in reports like this and in our sustainability reporting.

We used the ‘six capitals’ model from the IR Framework to identify and investigate a number of global trends with the potential to impact our business. These trends covered financial, human, manufactured, intellectual, social and natural capitals. This process helped us to identify where and how different trends interact with one another. Using this model, we created an initial list of 36 trends and their potential implications for JLL. We then undertook one-to-one engagements with around 30 executives across the firm from different disciplines and geographies to present the six capitals model; discuss the trends identified; and to understand, based on these trends, what the potential risks and opportunities are to JLL and how we are, or should be, responding to them. We were then able to develop a comprehensive qualitative analysis based on these internal engagements. Working with our Internal Audit team, we developed a quantitative analysis aligned with our existing risk management matrix. We scored the long-term trends according to likelihood and magnitude, taking account of potential impact on different areas of the business. The result of this scoring is the six capitals risks and opportunities materiality matrices, shown below, which allowed us to identify the most material long-term risks and opportunities for our company.

14

15

SUSTAINING OUR ENTERPRISE: A BUSINESS MODEL THAT COMBINES CAPITALS TO CREATE STAKEHOLDER VALUE

We have designed our business model to (1) create value for our clients, shareholders, and employees and (2) establish high-quality relationships with the suppliers we engage and the communities in which we operate. Our synergistic approach seeks to derive business benefits from the application and intersection primarily of human resources, financial capital, and intellectual capital and technology. Based on our intimate knowledge of local real estate and capital markets worldwide, as well as our investments in thought leadership and technology, we create value for clients by addressing their real estate needs as well as their broader business, strategic, operating, and longer-term sustainability goals. Given the increasingly global and interconnected marketplace in which many of our clients compete, our own capacity to deliver global solutions has also become more important to our business model.

We strive to create a healthy and dynamic balance between (1) activities that will produce short-term value and returns for our stakeholders through effective management of current transactions and business activities and (2) investments in people (such as new hires), acquisitions, technologies and systems designed to produce sustainable returns over the longer-term.

Our financial strength and our reputation for integrity, strong governance, and transparency, which we believe are among the strongest in the industry, give our clients confidence in our long-term ability to meet our obligations to them. It also positions us to be trusted extensions for the ways in which they seek to do business for the benefit of their own stakeholders. During 2015, we were included on the Ethisphere Institute's list of The World's Most Ethical Companies and we were listed as #20 on CR Magazine's list of the 100 Best Corporate Citizens.

The ability to create and deliver value to our clients drives our revenue and profits, which in turn allows us to invest in our business and our people, improving productivity and shareholder value. In doing so, we enable our people to advance their careers by taking on new and increased responsibilities within a dynamic environment as our business expands geographically, adds adjacent service offerings and develops new competencies. We are also increasingly able to develop and expand our relationships with suppliers of services to our own organization as well as to our clients, for whom we serve a significant intermediary role. By expanding employment both internally and to outsourced providers, we stimulate economically the locations in which we operate, and we increase the opportunities for those we directly or indirectly employ to engage in community services and other activities beneficial to society.

We apply our business model to the resources and capitals that we employ to provide services to assets owned or occupied by our clients. We provide these services through our own employees and, where necessary or appropriate in the case of property and facility management and project and development services, through the management of third-party contractors. The revenue and profits we earn from those efforts are divided between further investments in our business, employee compensation, and returns to our shareholders. We are increasingly focused on linking our business and sustainability strategies to promote the goal of creating long-term value for our shareholders, clients, employees, and the global community of which our firm is a part. These efforts help our clients manage their real estate more effectively and efficiently, promote employment globally, and create wealth for our shareholders and employees. In turn, they allow us to be an increasingly impactful member of, and positive force within, the communities in which we operate.

16

The following diagram summarizes how we create value for our shareholders and our broader stakeholders. It starts with the capital resources – or inputs – we need to do business. We use these resources to deliver services – or outputs – for our clients through a number of business activities we closely manage.

The resources we use are broadly comparable to many other professional services firms globally. What makes JLL unique is that we provide real value in a changing world: both through the implementation of our G5 business strategy and the medium-term Strategy 2020 to mitigate the impact of risks of future volatility on our business model.

Finally, there are outcomes of our business model, which can be both positive and negative. We realize that these outcomes will eventually become our resources once again, so our business model is designed in a way that keeps our impact low and our influence on quality resources high. Ultimately, this business model shows how we seek to derive long-term profit by the sustainable use of all resources.

17

BUSINESS SEGMENTS

We report our operations as four business segments. We manage our RES product offerings geographically as (1) the Americas, (2) EMEA and (3) Asia Pacific, and we manage our investment management business globally as (4) LaSalle.

There are significant risks inherent in conducting a global business. We describe these in detail below in Item 1A, Risk Factors. Information regarding revenue and operating income or loss, attributable to each of our segments, is included in “Segment Operating Results” within Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and within Note 3 of our Notes to Consolidated Financial Statements. Information concerning the identifiable assets of each of our business segments is also set forth in Note 3 of our Notes to Consolidated Financial Statements.

REAL ESTATE SERVICES: AMERICAS, EMEA AND ASIA PACIFIC

To address the needs of real estate owners and occupiers, we provide a full range of integrated property and facility management, project management, advisory and transaction services locally, regionally, and globally through our Americas, EMEA and Asia Pacific operating segments. We organize our RES in five major product categories:

• | Leasing; |

• | Capital Markets and Hotels; |

• | Property and Facility Management; |

• | Project and Development Services; and |

• | Advisory, Consulting and Other Services. |

Across these five broad RES categories, we leverage our deep real estate expertise and experience within the Firm to provide innovative solutions for our clients. For the year ended December 31, 2015, we derived our RES revenue from product categories and regional geographies as follows ($ in millions and showing change from 2014 in local currency):

For Property & Facility Management, Project & Development Services and total RES revenue, the table above shows "Fee Revenue," or revenue net of vendor and subcontract costs that are otherwise included both in revenue and expense ("gross contract costs") for reporting in accordance with U.S. generally accepted accounting principles. We believe that excluding gross contract costs from revenue in this presentation gives a more accurate picture of the revenue growth rates in these RES product categories.

18

RES Revenue Mix by Business Lines and Geographies

For the year ended December 31, 2015, our global total fee revenue of $4.8 million was generated as follows:

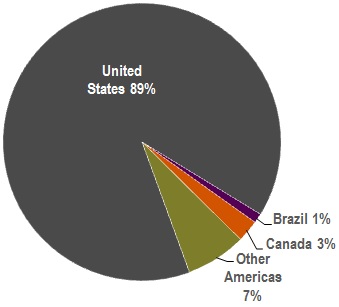

In the Americas, our total RES operating revenue for the year ended December 31, 2015, was derived from the following countries in the proportions indicated below:

19

In EMEA, our total RES operating revenue for the year ended December 31, 2015, was derived from the following countries in the proportions indicated below:

In Asia Pacific, our total RES operating revenue for the year ended December 31, 2015, was derived from the following countries in the proportions indicated below:

20

These product categories, and the services we provide within them, include:

1. Leasing Services

Agency Leasing Services executes marketing and leasing programs on behalf of investors, developers, property companies and public entities to secure tenants, and negotiate leases with terms that reflect our clients' best interests. In 2015, we completed approximately 18,100 agency leasing transactions representing 714 million square feet of space. We typically base our agency leasing fees on a percentage of the value of the lease revenue commitment for consummated leases, although in some cases they are based on a dollar amount per square foot leased.

Tenant Representation Services establishes strategic alliances with clients to deliver ongoing assistance to meet their real estate needs and to help them evaluate and execute transactions in line with their occupancy requirements. Tenant Representation Services is also an important component of our local market services. We assist clients by defining space requirements, identifying suitable alternatives, recommending appropriate occupancy solutions, negotiating lease and ownership terms with landlords and reducing real estate costs for clients through analyzing, structuring and negotiating business and economic incentives. We help our clients lower their real estate costs, minimize real estate occupancy risks, improve occupancy control and flexibility, and create more productive office environments. We employ a multi-disciplinary approach to develop occupancy strategies linked to our clients' core business objectives.

We determine Tenant Representation Services fees on a negotiated fee basis. In various markets, landlords may be responsible for paying them. Fees sometimes reflect performance measures related to targets that we and our clients establish prior to engagement or, in the case of strategic alliances, at future annual intervals. We use quantitative and qualitative measurements to assess performance relative to these goals, and we may be awarded incentive fees for superior performance. In 2015, we completed approximately 17,400 tenant representation transactions representing 426 million square feet of space.

2. Property and Facility Management

Property Management Services provides on-site management services to real estate owners for office, industrial, retail, multifamily residential and specialty properties. We seek to leverage our market share and buying power to deliver superior service and value to clients. Our goal is to enhance our clients' property values through aggressive day-to-day management. We may provide services through our own employees or through contracts with third-party providers. We focus on maintaining high levels of occupancy and tenant satisfaction while lowering property operating costs. During 2015, we provided on-site property management services for properties totaling approximately 2.7 billion square feet.

We typically provide property management services through an on-site general manager and staff. We support them with regional supervisory teams and central resources in such areas as training, technical and environmental services, accounting, marketing, and human resources. Our general managers are responsible for property management activities, client satisfaction and financial results. We do not compensate them with commissions, but rather with a combination of base salary and a performance bonus that is directly linked to results they produce for their clients. In some cases, management agreements provide for incentive compensation relating to operating expense reductions, gross revenue or occupancy objectives, or tenant satisfaction levels. Consistent with industry custom, management contract terms typically range from one to three years, although some contracts are terminable at will at any time following a short notice period, usually 30 to 120 days, as is typical in the industry.

Integrated Facility Management Services provides comprehensive portfolio and facility management services to corporations and institutions that outsource the management of the real estate they occupy. Facilities under management range from corporate headquarters to industrial complexes. During 2015, Integrated Facility Management Services managed approximately 1.3 billion square feet of real estate for its clients. Our target clients typically have large portfolios (usually over one million square feet) that offer significant opportunities to reduce costs and improve service delivery. The competitive trends of globalization, outsourcing, and offshoring have prompted many of these clients to demand consistent service delivery worldwide and a single point of contact from their real estate service providers. We generally develop performance measures to quantify the progress we make toward goals and objectives that we have mutually determined. Depending on client needs, our Integrated Facility Management Services units, either alone or partnering with other business units to benefit from their particular expertise or local market knowledge, provide services that include portfolio planning, property management, agency leasing, tenant representation, acquisition, finance, disposition, development management, energy and sustainability services, and land advisory services. We may provide services through our own employees or through contracts with third-party providers (as to which we may act in a principal capacity or which we may hire as an agent acting on behalf of our clients).

Our Integrated Facility Management Services units are compensated on the basis of negotiated fees that we typically structure to include a base fee and a performance bonus. We generally base performance bonus compensation on a quantitative evaluation of progress toward performance measures and regularly scheduled client satisfaction surveys. Integrated Facility Management Services agreements are typically three to five years in duration, although most contracts are terminable at will by the client upon a short notice period, usually 30 to 60 days, as is typical in the industry.

21

We also provide Lease Administration and Auditing Services, helping clients centralize their lease management processes. Whether clients have a small number of leases or a global portfolio, we assist them by reducing costs associated with incorrect lease charges, right-sizing their portfolios through lease options, identifying underutilized assets and ensuring regulatory compliance to mitigate risk.

In the United States, the United Kingdom and selected other countries, we provide Mobile Engineering Services to clients with large portfolios of sites or where we have multiple clients in proximity to each other. Rather than using multiple vendors to perform facility services, these companies hire JLL to provide HVAC, electrical and plumbing services, and general interior repair and maintenance. Our multi-disciplined mobile engineers serve numerous clients in a specified geographic area, performing multiple tasks in a single visit and taking ownership of the operational success of the sites they service. This service delivery model reduces clients' operating costs by bundling on-site services, leveraging resources across multiple accounts and reducing travel time between sites.

3. Project and Development Services

Project and Development Services provides a variety of services to tenants of leased space, owners in self-occupied buildings, and owners of real estate investments. These include conversion management, move management, construction management, and strategic occupancy planning services. Project and Development Services frequently manages relocation and build-out initiatives for clients of our Property Management Services, Integrated Facility Management Services, and Tenant Representation Services units. Project and Development Services also manages all aspects of development and renovation of commercial projects for our clients, serving as a general contractor in some cases. Additionally, we provide these services to public-sector clients, particularly to military and government entities and educational institutions, primarily in the United States, and to a limited but growing extent in other countries.

Our Project and Development Services business is generally compensated on the basis of negotiated fees. Client contracts are typically multi-year in duration and may govern a number of discrete projects, with individual projects being completed in less than one year.

In a growing number of countries, we provide fit-out and refurbishment services on a principal basis under the Tetris brand, which is an outgrowth of a previous acquisition we completed through our French business.

4. Capital Markets and Hotels

Capital Markets and Hotels Services includes property sales and acquisitions, real estate financings, private equity placements, portfolio advisory activities and corporate finance advice and execution. We provide these services with respect to substantially all types of properties. In the United States, we operate a multifamily lending and commercial loan servicing platform and for a number of years we have been a Freddie Mac Program Plus® Seller/Servicer. With our acquisition of Oak Grove Capital in 2015, we have added Fannie Mae and HUD/GNMA multifamily lending services capabilities. Real Estate Investment Banking Services includes sourcing capital, both in the form of equity and debt, derivatives structuring, and other traditional investment banking services designed to assist investor and corporate clients in maximizing the value of their real estate. To meet client demands for marketing real estate assets internationally and investing outside of their home markets, our Capital Markets Services teams combine local market knowledge with our access to global capital sources to provide superior execution in raising capital for real estate transactions. By researching, developing, and introducing innovative new financial products and strategies, Capital Markets Services is also integral to the business development efforts of our other businesses.

Clients typically compensate Capital Markets Services units on the basis of the value of transactions completed or securities placed. In certain circumstances, we receive retainer fees for portfolio advisory services. Real Estate Investment Banking fees are generally transaction-specific and conditioned upon the successful completion of the transaction.

We also deliver specialized Capital Markets Services for hotel and hospitality assets and portfolios on a global basis, including investment sales, mergers and acquisitions, and financing. We provide services to assets that span the hospitality spectrum: luxury properties; resorts; select service and budget hotels; golf courses; theme parks; casinos; spas; and pubs.

We provide Value Recovery Services to owners, investors and occupiers to help them analyze the impact of a possible financial downturn on their assets and identify solutions that allow them to respond decisively. In this area, we address the operational and occupancy needs of banks and insurance companies that are merging with or acquiring other institutions. We assist banks and insurance companies with challenged assets and liabilities on their balance sheets by providing valuations, asset management, loan servicing, and disposition services. We provide receivership services and special asset servicing capabilities to lenders, loan servicers, and financial institutions that need help managing defaulted real estate assets. In addition, we provide valuation, asset management, and disposition services to government entities to maximize the value of owned securities and assets acquired from failed financial institutions or from government relief programs. We also assist owners by identifying potentially distressed properties and the major occupiers who are facing challenges.

22

5. Advisory, Consulting and Other Services

Valuation Services provides clients with professional valuation services to help them determine market values for office, retail, industrial, and mixed-use properties. Such services may involve valuing a single property or a global portfolio of multiple property types. We conduct valuations, which typically involve commercial property, for a variety of purposes, including acquisitions, dispositions, debt and equity financings, mergers and acquisitions, securities offerings (including initial public offerings), and privatization initiatives. Clients include occupiers, investors, and financing sources from the public and private sectors. For the most part, our valuation specialists provide services outside of the United States. We usually negotiate compensation for valuation services based on the scale and complexity of each assignment, and our fees typically relate in part to the value of the underlying assets.

Consulting Services delivers innovative, results-driven real estate solutions that align strategically and tactically with clients' business objectives. We provide clients with specialized, value-added real estate consulting services in such areas as mergers and acquisitions, occupier portfolio strategy, workplace solutions, location advisory, financial optimization strategies, organizational strategy, and Six Sigma process solutions. Our professionals focus on translating global best practices into local real estate solutions, creating optimal financial and operational results for our clients.

We also provide Advisory Services for hotels, including hotel valuations and appraisals, acquisition advice, asset management, strategic planning, management contract negotiation, consulting, industry research and project and development services for asset types spanning the hospitality spectrum.

We typically negotiate compensation for Consulting Services based on work plans developed for advisory services that vary based on the scope and complexity of projects. For transaction services, we generally base compensation on the value of transactions that close.

We provide Energy and Sustainability Services to occupiers and investors to help them develop their corporate sustainability strategies, green their real estate portfolios, reduce their energy consumption and carbon footprint, upgrade building performance by managing Leadership in Energy and Environmental Design ("LEED") construction or retrofits and provide sustainable building operations management. We have more than 1,500 energy and sustainability accredited professionals. In 2014 alone, we documented $47 million in estimated energy savings for our U.S. clients and reduced their greenhouse gas emissions by 278,000 tons. Our sustainability teams worked on a total of 8,098 buildings in 2014.

We generally negotiate compensation for Energy and Sustainability Services for each assignment based on shared savings or the scale and complexity of the project.

LASALLE INVESTMENT MANAGEMENT

Our global real estate investment management business, operating under the brand name of LaSalle Investment Management, has three priorities:

• | Deliver superior investment performance; |

• | Develop and execute investment strategies that meet the specific investment objectives of our clients; and |

• | Deliver uniformly high levels of client service globally. |

We provide investment management services to institutional and retail investors, including high-net-worth individuals. We seek to establish and maintain relationships of trust with sophisticated investors who value our global platform and extensive local market knowledge. As of December 31, 2015, LaSalle managed $56.4 billion of private real estate assets, including debt and equity, and public real estate securities, making us one of the world's largest managers of institutional capital invested in real estate assets and securities.

LaSalle provides clients with a broad range of real estate investment products and services in the private and public capital markets. We design these products and services to meet the differing strategic, asset allocation, risk/return and liquidity requirements of clients. The range of investment solutions includes private investments in multiple real estate property types including office, retail, industrial, health care and multifamily residential, as well as investments in debt. We act either through commingled investment funds or single client account relationships ("separate accounts"). We also offer indirect public investments, primarily in publicly traded real estate investment trusts ("REITs") and other real estate equities.

23

The geographic distribution of LaSalle's assets under management is as follows ($ in billions):

Separate Accounts | $ | 32.4 | |

Commingled Funds | 11.2 | ||

Public Securities | 12.8 | ||

Total Assets under Management | $ | 56.4 | |

We believe the success of our investment management business comes from our strong investment performance, industry-leading research capabilities, experienced investment professionals, innovative investment strategies, global presence and coordinated platform, local market knowledge, and strong client focus. We maintain an extensive real estate research and strategy department whose dedicated professionals monitor real estate and capital market conditions around the world to enhance current investment decisions and identify future opportunities. Research and strategy is integrated throughout the investment management process from portfolio strategy formulation to property acquisition through ongoing asset management and disposition. In addition to drawing on public sources for information, LaSalle's research department utilizes the extensive local presence of JLL professionals throughout the world to gather and share proprietary insight into local market conditions.

The investment and capital origination activities of our investment management business have become increasingly global. We have invested in direct real estate assets in 18 countries around the globe, as well as in public real estate companies traded on all major stock exchanges. We expect that cross-border investment management activities, both fund raising and investing, will continue to grow.

Private Investments in Real Estate Properties (Separate Accounts and Commingled Funds)

In serving our investment management clients, LaSalle is responsible for the acquisition, financing, leasing, management, and divestiture of real estate investments across a broad range of real estate property types. LaSalle launched its first institutional investment fund in 1979 and currently has a series of commingled investment funds, including eight funds that invest in assets in the Americas, ten funds that invest in assets located in Europe and six funds that invest in assets in Asia Pacific. LaSalle also maintains separate account relationships with investors for whom we manage private real estate investments.

LaSalle is the advisor to Jones Lang LaSalle Income Property Trust, Inc. ("JLL IPT"), a non-listed real estate investment trust launched in 2012 that gives suitable individual investors access to a growing portfolio of diversified commercial real estate investments. As of December 31, 2015, JLL IPT had $1.1 billion in assets under management. In 2015, JLL IPT raised over $400 million.

As of December 31, 2015, LaSalle had approximately $43.6 billion in assets under management in commingled funds and separate accounts.

24

Some investors prefer to partner with investment managers willing to co-invest their own funds to more closely align the interests of the investor and the investment manager. We believe that our ability to co-invest alongside the investments of our clients' funds will continue to be an important factor in maintaining and continually improving our competitive position. We believe our co-investment strategy strengthens our ability to raise capital for new real estate investments and real estate funds. As of December 31, 2015, we had a total of $311.5 million of co-investments in real estate ventures, the majority of which are included in LaSalle's $56.4 billion of assets under management.

We may engage in merchant banking activities in appropriate circumstances. These may involve making investments of the Firm's capital or providing loan capital to acquire properties in order to seed investment management funds before they are offered to clients.

LaSalle conducts its operations with teams of professionals dedicated to achieving specific client objectives. Each investment team functions as an entrepreneurial group managing an investment's entire life cycle and is directly accountable for performance. Regional investment committees, whose members have specialized knowledge applicable to underlying investment strategies, oversee all separate accounts and funds and must approve all investment decisions. This proven approach builds trust and alignment with our clients' investment objectives.