0001035443false12/312023Q100010354432023-01-012023-03-3100010354432023-04-14xbrli:shares00010354432023-03-31iso4217:USD00010354432022-12-310001035443are:IncomefromrentalsMember2023-01-012023-03-310001035443are:IncomefromrentalsMember2022-01-012022-03-310001035443us-gaap:ProductAndServiceOtherMember2023-01-012023-03-310001035443us-gaap:ProductAndServiceOtherMember2022-01-012022-03-3100010354432022-01-012022-03-31iso4217:USDxbrli:shares0001035443us-gaap:CommonStockMember2022-12-310001035443us-gaap:AdditionalPaidInCapitalMember2022-12-310001035443us-gaap:RetainedEarningsMember2022-12-310001035443us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-12-310001035443us-gaap:NoncontrollingInterestMember2022-12-310001035443are:RedeemableNoncontrollingInterestsMember2022-12-310001035443us-gaap:RetainedEarningsMember2023-01-012023-03-310001035443us-gaap:NoncontrollingInterestMember2023-01-012023-03-310001035443are:RedeemableNoncontrollingInterestsMember2023-01-012023-03-310001035443us-gaap:AccumulatedOtherComprehensiveIncomeMember2023-01-012023-03-310001035443us-gaap:AdditionalPaidInCapitalMember2023-01-012023-03-310001035443us-gaap:CommonStockMember2023-01-012023-03-310001035443us-gaap:CommonStockMember2023-03-310001035443us-gaap:AdditionalPaidInCapitalMember2023-03-310001035443us-gaap:RetainedEarningsMember2023-03-310001035443us-gaap:AccumulatedOtherComprehensiveIncomeMember2023-03-310001035443us-gaap:NoncontrollingInterestMember2023-03-310001035443are:RedeemableNoncontrollingInterestsMember2023-03-310001035443us-gaap:CommonStockMember2021-12-310001035443us-gaap:AdditionalPaidInCapitalMember2021-12-310001035443us-gaap:RetainedEarningsMember2021-12-310001035443us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-12-310001035443us-gaap:NoncontrollingInterestMember2021-12-3100010354432021-12-310001035443are:RedeemableNoncontrollingInterestsMember2021-12-310001035443us-gaap:RetainedEarningsMember2022-01-012022-03-310001035443us-gaap:NoncontrollingInterestMember2022-01-012022-03-310001035443are:RedeemableNoncontrollingInterestsMember2022-01-012022-03-310001035443us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-01-012022-03-310001035443us-gaap:AdditionalPaidInCapitalMember2022-01-012022-03-310001035443us-gaap:CommonStockMember2022-01-012022-03-310001035443us-gaap:CommonStockMember2022-03-310001035443us-gaap:AdditionalPaidInCapitalMember2022-03-310001035443us-gaap:RetainedEarningsMember2022-03-310001035443us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-03-310001035443us-gaap:NoncontrollingInterestMember2022-03-3100010354432022-03-310001035443are:RedeemableNoncontrollingInterestsMember2022-03-31are:propertyutr:sqft0001035443us-gaap:BuildingAndBuildingImprovementsMembersrt:MaximumMember2023-01-012023-03-310001035443us-gaap:LandImprovementsMembersrt:MaximumMember2023-01-012023-03-310001035443country:CA2023-03-310001035443country:CN2023-03-31xbrli:pure0001035443are:IncomefromrentalsMemberus-gaap:AccountingStandardsUpdate201409Member2023-01-012023-03-310001035443are:IncomefromrentalsMemberus-gaap:AccountingStandardsUpdate201409Member2022-01-012022-03-310001035443are:RevenuessubjecttootheraccountingguidanceMember2023-01-012023-03-310001035443srt:NorthAmericaMember2023-03-310001035443srt:NorthAmericaMember2022-12-310001035443srt:AsiaMember2023-03-310001035443srt:AsiaMember2022-12-310001035443are:FuturedevelopmentprojectsMembercountry:CA2023-03-310001035443are:ActiveDevelopmentRedevelopmentMembercountry:CA2023-03-310001035443country:CAare:OperatingwithfuturedevelopmentandredevelopmentMember2023-03-310001035443country:CA2023-01-012023-03-310001035443are:OthermarketsMember2023-03-310001035443are:FuturedevelopmentprojectsMemberare:OthermarketsMember2023-03-310001035443are:ActiveDevelopmentRedevelopmentMemberare:OthermarketsMember2023-03-310001035443are:OperatingwithfuturedevelopmentandredevelopmentMemberare:OthermarketsMember2023-03-310001035443are:OthermarketsMember2023-01-012023-03-310001035443are:FuturedevelopmentprojectsMember2022-03-310001035443are:ActiveDevelopmentRedevelopmentMember2022-03-310001035443are:OperatingwithfuturedevelopmentandredevelopmentMember2022-03-310001035443srt:NorthAmericaMember2022-01-012022-03-310001035443srt:NorthAmericaMember2023-01-012023-03-310001035443us-gaap:LeasesAcquiredInPlaceMember2023-03-310001035443are:AboveandBelowMarketLeasesMember2023-03-310001035443are:OperatingpropertiesMemberare:AboveandBelowMarketLeasesMember2023-01-012023-03-310001035443are:OperatingpropertiesMember2023-01-012023-03-310001035443are:OperatingpropertiesMemberus-gaap:LeasesAcquiredInPlaceMember2023-01-012023-03-310001035443are:A50And60BinneyStreetMemberare:AlexandriaMember2023-03-310001035443are:A75125BinneyStreetMemberare:AlexandriaMember2023-03-310001035443are:A100And225BinneyStreetAnd300ThirdStreetMemberare:AlexandriaMember2023-03-310001035443are:A99CoolidgeAvenueMemberare:AlexandriaMember2023-03-310001035443are:A15NeccoStreetMemberare:AlexandriaMember2023-03-310001035443are:OtherGreaterBostonMemberare:AlexandriaMember2023-03-310001035443are:AlexandriaCenterForScienceAndTechnologyMissionBayMemberare:AlexandriaMember2023-03-310001035443are:A1450OwensStreetMemberare:AlexandriaMember2023-03-310001035443are:A601611651681685And701GatewayBoulevardMemberare:AlexandriaMember2023-03-310001035443are:A751GatewayBoulevardMemberare:AlexandriaMember2023-03-310001035443are:A213EastGrandAvenueMemberare:AlexandriaMember2023-03-310001035443are:A500ForbesBoulevardMemberare:AlexandriaMember2023-03-310001035443are:AlexandriaCenterForLifeScienceMillbraeMemberare:AlexandriaMember2023-03-310001035443are:A3215MerryfieldRowMemberare:AlexandriaMember2023-03-310001035443are:CampusPointByAlexandriaMemberare:AlexandriaMember2023-03-310001035443are:A5200IlluminaWayMemberare:AlexandriaMember2023-03-310001035443are:A9625TowneCentreDriveMemberare:AlexandriaMember2023-03-310001035443are:SDTechbyAlexandriaMemberare:AlexandriaMember2023-03-310001035443are:PacificTechnologyParkMemberare:AlexandriaMember2023-03-310001035443are:SummersRidgeScienceParkMemberare:AlexandriaMember2023-03-310001035443are:A1201And1208EastlakeAvenueEastAnd199EastBlaineStreetMemberare:AlexandriaMember2023-03-310001035443are:A400DexterAvenueNorthMemberare:AlexandriaMember2023-03-310001035443are:A800MercerStreetMemberare:AlexandriaMember2023-03-310001035443are:A1655and1715ThirdStreetMember2023-03-310001035443are:A14011413ResearchBoulevardMember2023-03-310001035443are:A1450ResearchBoulevardMember2023-03-310001035443are:A101WestDickmanStreetMember2023-03-310001035443us-gaap:NoncontrollingInterestMemberare:A1450OwensStreetMemberare:AlexandriaMember2023-03-310001035443are:OtherGreaterBostonMemberare:DevelopmentEntitlementsAcquiredMember2023-03-310001035443are:OtherGreaterBostonMember2023-01-012023-03-310001035443are:OtherGreaterBostonMemberus-gaap:NoncontrollingInterestMemberare:AlexandriaMember2023-03-310001035443are:OtherGreaterBostonMemberare:FuturedevelopmentprojectsMember2023-03-310001035443are:OtherGreaterBostonMemberare:RedeemableNoncontrollingInterestsMember2023-01-012023-03-310001035443us-gaap:VariableInterestEntityPrimaryBeneficiaryMember2023-03-310001035443us-gaap:VariableInterestEntityPrimaryBeneficiaryMember2022-12-310001035443are:A1655and1715ThirdStreetMember2022-12-310001035443are:A1450ResearchBoulevardMember2022-12-310001035443are:A101WestDickmanStreetMember2022-12-310001035443are:OtherunconsolidatedrealestatejointventuresMember2023-03-310001035443are:OtherunconsolidatedrealestatejointventuresMember2022-12-310001035443are:SecuredDebtMaturingOn122324Memberare:A14011413ResearchBoulevardMember2023-01-012023-03-310001035443are:SecuredDebtMaturingOn122324Memberare:A14011413ResearchBoulevardMember2023-03-310001035443are:Secureddebtmaturingon31025Memberare:A1655and1715ThirdStreetMember2023-01-012023-03-310001035443are:Secureddebtmaturingon31025Memberare:A1655and1715ThirdStreetMember2023-03-310001035443are:SecuredDebtMaturingOn111026Memberare:A101WestDickmanStreetMember2023-01-012023-03-310001035443are:SecuredDebtMaturingOn111026Memberus-gaap:SecuredOvernightFinancingRateSofrOvernightIndexSwapRateMemberare:A101WestDickmanStreetMember2023-03-310001035443are:SecuredDebtMaturingOn111026Memberare:A101WestDickmanStreetMember2023-03-310001035443are:A1450ResearchBoulevardMemberare:SecuredDebtMaturingOn121026Member2023-01-012023-03-310001035443are:A1450ResearchBoulevardMemberare:SecuredDebtMaturingOn121026Memberus-gaap:SecuredOvernightFinancingRateSofrOvernightIndexSwapRateMember2023-03-310001035443are:A1450ResearchBoulevardMemberare:SecuredDebtMaturingOn121026Member2023-03-310001035443us-gaap:EquityMethodInvestmentNonconsolidatedInvesteeOrGroupOfInvesteesMember2023-03-310001035443us-gaap:SecuredOvernightFinancingRateSofrOvernightIndexSwapRateMember2023-01-012023-03-31are:directFinancingLeaseare:landParcel0001035443are:PurchaseOptionTermOneMember2023-01-012023-03-310001035443are:PurchaseOptionTermTwoMember2023-01-012023-03-310001035443are:PurchaseOptionTermThreeMember2023-01-012023-03-3100010354432017-10-012017-10-010001035443are:LandparcelssubjecttoleaseagreementthatcontainsapurchaseoptionMember2023-01-012023-03-310001035443srt:CumulativeEffectPeriodOfAdoptionAdjustmentMemberare:IncomefromrentalsMember2023-01-012023-03-310001035443srt:CumulativeEffectPeriodOfAdoptionAdjustmentMemberare:IncomefromrentalsMember2022-01-012022-03-310001035443are:GroundandOperatingLeasesMember2023-03-310001035443are:OperatingPropertyWithGroundLeaseMember2023-03-310001035443srt:MinimumMember2023-01-012023-03-310001035443srt:MaximumMember2023-01-012023-03-310001035443are:SanFranciscoBayAreaMember2022-07-012022-09-300001035443are:FundsheldinescrowrelatedtoconstructionprojectsandinvestingactivitiesMember2023-03-310001035443are:FundsheldinescrowrelatedtoconstructionprojectsandinvestingactivitiesMember2022-12-310001035443are:OtherrestrictedcashMember2023-03-310001035443are:OtherrestrictedcashMember2022-12-31are:investment0001035443are:LimitedpartnershipsMember2023-01-012023-03-310001035443are:InvestmentsinpubliclytradedcompaniesMember2023-03-310001035443are:LimitedpartnershipsMember2023-03-310001035443are:InvestmentsinprivatelyheldentitiesthatdonotreportNAVMemberare:EntitieswithobservablepricechangeMember2023-03-310001035443are:InvestmentsinprivatelyheldentitiesthatdonotreportNAVMemberare:EntitieswithoutobservablepricechangesMember2023-03-310001035443are:InvestmentsinpubliclytradedcompaniesMember2022-12-310001035443are:LimitedpartnershipsMember2022-12-310001035443are:InvestmentsinprivatelyheldentitiesthatdonotreportNAVMemberare:EntitieswithobservablepricechangeMember2022-12-310001035443are:InvestmentsinprivatelyheldentitiesthatdonotreportNAVMemberare:EntitieswithoutobservablepricechangesMember2022-12-310001035443are:InvestmentsinprivatelyheldentitiesthatdonotreportNAVMemberare:EntitieswithobservablepricechangeMember2023-01-012023-03-310001035443are:InvestmentsinprivatelyheldentitiesthatdonotreportNAVMemberare:EntitieswithobservablepricechangeMember2022-01-012022-03-310001035443are:TotalInvestmentsHeldMember2023-01-012023-03-310001035443are:TotalInvestmentsHeldMember2022-01-012022-03-310001035443us-gaap:EquityMethodInvestmentsMember2023-01-012023-03-31are:transfer0001035443are:InvestmentsinpubliclytradedcompaniesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:EstimateOfFairValueFairValueDisclosureMember2023-03-310001035443are:InvestmentsinpubliclytradedcompaniesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:FairValueInputsLevel1Member2023-03-310001035443are:InvestmentsinpubliclytradedcompaniesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:FairValueInputsLevel2Member2023-03-310001035443us-gaap:FairValueInputsLevel3Memberare:InvestmentsinpubliclytradedcompaniesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:EstimateOfFairValueFairValueDisclosureMember2023-03-310001035443are:InvestmentsinpubliclytradedcompaniesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:EstimateOfFairValueFairValueDisclosureMember2022-12-310001035443are:InvestmentsinpubliclytradedcompaniesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:FairValueInputsLevel1Member2022-12-310001035443are:InvestmentsinpubliclytradedcompaniesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:FairValueInputsLevel2Member2022-12-310001035443us-gaap:FairValueInputsLevel3Memberare:InvestmentsinpubliclytradedcompaniesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:EstimateOfFairValueFairValueDisclosureMember2022-12-310001035443are:InvestmentsinprivatelyheldentitiesthatdonotreportNAVMemberare:EntitieswithoutobservablepricechangesMemberus-gaap:FairValueMeasurementsNonrecurringMemberus-gaap:EstimateOfFairValueFairValueDisclosureMember2023-03-310001035443are:InvestmentsinprivatelyheldentitiesthatdonotreportNAVMemberare:EntitieswithoutobservablepricechangesMemberus-gaap:FairValueMeasurementsNonrecurringMemberus-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:FairValueInputsLevel1Member2023-03-310001035443are:InvestmentsinprivatelyheldentitiesthatdonotreportNAVMemberare:EntitieswithoutobservablepricechangesMemberus-gaap:FairValueMeasurementsNonrecurringMemberus-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:FairValueInputsLevel2Member2023-03-310001035443us-gaap:FairValueInputsLevel3Memberare:InvestmentsinprivatelyheldentitiesthatdonotreportNAVMemberare:EntitieswithoutobservablepricechangesMemberus-gaap:FairValueMeasurementsNonrecurringMemberus-gaap:EstimateOfFairValueFairValueDisclosureMember2023-03-310001035443are:InvestmentsinprivatelyheldentitiesthatdonotreportNAVMemberare:EntitieswithoutobservablepricechangesMemberus-gaap:FairValueMeasurementsNonrecurringMemberus-gaap:EstimateOfFairValueFairValueDisclosureMember2022-12-310001035443are:InvestmentsinprivatelyheldentitiesthatdonotreportNAVMemberare:EntitieswithoutobservablepricechangesMemberus-gaap:FairValueMeasurementsNonrecurringMemberus-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:FairValueInputsLevel1Member2022-12-310001035443are:InvestmentsinprivatelyheldentitiesthatdonotreportNAVMemberare:EntitieswithoutobservablepricechangesMemberus-gaap:FairValueMeasurementsNonrecurringMemberus-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:FairValueInputsLevel2Member2022-12-310001035443us-gaap:FairValueInputsLevel3Memberare:InvestmentsinprivatelyheldentitiesthatdonotreportNAVMemberare:EntitieswithoutobservablepricechangesMemberus-gaap:FairValueMeasurementsNonrecurringMemberus-gaap:EstimateOfFairValueFairValueDisclosureMember2022-12-310001035443us-gaap:CarryingReportedAmountFairValueDisclosureMember2023-03-310001035443us-gaap:FairValueMeasurementsNonrecurringMemberus-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:FairValueInputsLevel2Member2023-03-310001035443us-gaap:FairValueMeasurementsNonrecurringMemberus-gaap:EstimateOfFairValueFairValueDisclosureMember2023-03-310001035443us-gaap:CarryingReportedAmountFairValueDisclosureMemberare:A22BillionUnsecuredSeniorLineOfCreditMember2023-03-310001035443us-gaap:FairValueMeasurementsNonrecurringMemberus-gaap:EstimateOfFairValueFairValueDisclosureMemberare:A22BillionUnsecuredSeniorLineOfCreditMemberus-gaap:FairValueInputsLevel1Member2023-03-310001035443us-gaap:FairValueMeasurementsNonrecurringMemberus-gaap:EstimateOfFairValueFairValueDisclosureMemberare:A22BillionUnsecuredSeniorLineOfCreditMemberus-gaap:FairValueInputsLevel2Member2023-03-310001035443us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsNonrecurringMemberus-gaap:EstimateOfFairValueFairValueDisclosureMemberare:A22BillionUnsecuredSeniorLineOfCreditMember2023-03-310001035443us-gaap:FairValueMeasurementsNonrecurringMemberus-gaap:EstimateOfFairValueFairValueDisclosureMemberare:A22BillionUnsecuredSeniorLineOfCreditMember2023-03-310001035443us-gaap:CarryingReportedAmountFairValueDisclosureMemberus-gaap:CommercialPaperMember2023-03-310001035443us-gaap:FairValueMeasurementsNonrecurringMemberus-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:CommercialPaperMemberus-gaap:FairValueInputsLevel1Member2023-03-310001035443us-gaap:FairValueMeasurementsNonrecurringMemberus-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:CommercialPaperMemberus-gaap:FairValueInputsLevel2Member2023-03-310001035443us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsNonrecurringMemberus-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:CommercialPaperMember2023-03-310001035443us-gaap:FairValueMeasurementsNonrecurringMemberus-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:CommercialPaperMember2023-03-310001035443us-gaap:CarryingReportedAmountFairValueDisclosureMember2022-12-310001035443us-gaap:FairValueMeasurementsNonrecurringMemberus-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:FairValueInputsLevel2Member2022-12-310001035443us-gaap:FairValueMeasurementsNonrecurringMemberus-gaap:EstimateOfFairValueFairValueDisclosureMember2022-12-310001035443us-gaap:CarryingReportedAmountFairValueDisclosureMemberare:A22BillionUnsecuredSeniorLineOfCreditMember2022-12-310001035443us-gaap:FairValueMeasurementsNonrecurringMemberus-gaap:EstimateOfFairValueFairValueDisclosureMemberare:A22BillionUnsecuredSeniorLineOfCreditMemberus-gaap:FairValueInputsLevel1Member2022-12-310001035443us-gaap:FairValueMeasurementsNonrecurringMemberus-gaap:EstimateOfFairValueFairValueDisclosureMemberare:A22BillionUnsecuredSeniorLineOfCreditMemberus-gaap:FairValueInputsLevel2Member2022-12-310001035443us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsNonrecurringMemberus-gaap:EstimateOfFairValueFairValueDisclosureMemberare:A22BillionUnsecuredSeniorLineOfCreditMember2022-12-310001035443us-gaap:FairValueMeasurementsNonrecurringMemberus-gaap:EstimateOfFairValueFairValueDisclosureMemberare:A22BillionUnsecuredSeniorLineOfCreditMember2022-12-310001035443us-gaap:CarryingReportedAmountFairValueDisclosureMemberus-gaap:CommercialPaperMember2022-12-310001035443us-gaap:FairValueMeasurementsNonrecurringMemberus-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:CommercialPaperMemberus-gaap:FairValueInputsLevel1Member2022-12-310001035443us-gaap:FairValueMeasurementsNonrecurringMemberus-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:CommercialPaperMemberus-gaap:FairValueInputsLevel2Member2022-12-310001035443us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsNonrecurringMemberus-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:CommercialPaperMember2022-12-310001035443us-gaap:FairValueMeasurementsNonrecurringMemberus-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:CommercialPaperMember2022-12-310001035443are:SecuredNotesPayableMaturingOn111926Memberus-gaap:SecuredOvernightFinancingRateSofrOvernightIndexSwapRateMember2023-01-012023-03-310001035443are:SecuredNotesPayableMaturingOn111926Member2023-03-310001035443are:SecuredNotesPayableMaturingOn111926Member2023-01-012023-03-310001035443are:SecuredNotesPayableMaturingJuly12036Member2023-03-310001035443are:SecuredNotesPayableMaturingJuly12036Member2023-01-012023-03-310001035443us-gaap:SecuredDebtMember2023-03-310001035443us-gaap:CommercialPaperMemberus-gaap:LineOfCreditMember2023-03-310001035443us-gaap:CommercialPaperMemberus-gaap:LineOfCreditMember2023-01-012023-03-310001035443are:A3.45unsecuredseniornotespayableduein2025Member2023-03-310001035443are:A3.45unsecuredseniornotespayableduein2025Member2023-01-012023-03-310001035443are:A4.30UnsecuredSeniorNotesPayableMember2023-03-310001035443are:A4.30UnsecuredSeniorNotesPayableMember2023-01-012023-03-310001035443are:A3.80UnsecuredSeniorNotesPayableMember2023-03-310001035443are:A3.80UnsecuredSeniorNotesPayableMember2023-01-012023-03-310001035443are:A3.95UnsecuredSeniorNotesPayableMember2023-03-310001035443are:A3.95UnsecuredSeniorNotesPayableMember2023-01-012023-03-310001035443are:A3.95UnsecuredSeniorNotesPayableDuein2028Member2023-03-310001035443are:A3.95UnsecuredSeniorNotesPayableDuein2028Member2023-01-012023-03-310001035443are:UnsecuredSeniorNotesDueinJuly2029Member2023-03-310001035443are:UnsecuredSeniorNotesDueinJuly2029Member2023-01-012023-03-310001035443are:A2.75UnsecuredSeniorNotesPayableDue2029Member2023-03-310001035443are:A2.75UnsecuredSeniorNotesPayableDue2029Member2023-01-012023-03-310001035443are:A4.70UnsecuredSeniorNotesPayableMember2023-03-310001035443are:A4.70UnsecuredSeniorNotesPayableMember2023-01-012023-03-310001035443are:A4.90UnsecuredSeniorNotesPayableMember2023-03-310001035443are:A4.90UnsecuredSeniorNotesPayableMember2023-01-012023-03-310001035443are:A3.375UnsecuredSeniorNotesPayableMember2023-03-310001035443are:A3.375UnsecuredSeniorNotesPayableMember2023-01-012023-03-310001035443are:A200UnsecuredSeniorNotesPayableMember2023-03-310001035443are:A200UnsecuredSeniorNotesPayableMember2023-01-012023-03-310001035443are:A1875UnsecuredSeniorNotesPayableMember2023-03-310001035443are:A1875UnsecuredSeniorNotesPayableMember2023-01-012023-03-310001035443are:A295UnsecuredSeniorNotesPayableMember2023-03-310001035443are:A295UnsecuredSeniorNotesPayableMember2023-01-012023-03-310001035443are:A475UnsecuredSeniorNotesPayableMember2023-03-310001035443are:A475UnsecuredSeniorNotesPayableMember2023-01-012023-03-310001035443are:A4.85UnsecuredSeniorNotePayableMember2023-03-310001035443are:A4.85UnsecuredSeniorNotePayableMember2023-01-012023-03-310001035443are:A4.00UnsecuredSeniorNotesPayablesDue2050Member2023-03-310001035443are:A4.00UnsecuredSeniorNotesPayablesDue2050Member2023-01-012023-03-310001035443are:A300UnsecuredSeniorNotesPayableMember2023-03-310001035443are:A300UnsecuredSeniorNotesPayableMember2023-01-012023-03-310001035443are:A355UnsecuredSeniorNotesPayableMember2023-03-310001035443are:A355UnsecuredSeniorNotesPayableMember2023-01-012023-03-310001035443are:A515UnsecuredSeniorNotesPayableMember2023-03-310001035443are:A515UnsecuredSeniorNotesPayableMember2023-01-012023-03-310001035443us-gaap:UnsecuredDebtMember2023-03-310001035443are:SecuredNotesPayableMaturingOn111926Memberare:A99CoolidgeAvenueMember2023-03-310001035443us-gaap:SecuredDebtMember2023-01-012023-03-310001035443us-gaap:SeniorNotesMember2023-03-310001035443us-gaap:SeniorNotesMember2023-01-012023-03-310001035443us-gaap:LineOfCreditMember2023-03-310001035443us-gaap:CommercialPaperMember2023-03-310001035443us-gaap:CommercialPaperMember2023-01-012023-03-310001035443are:TotalIssuanceOfUnsecuredSeniorNotesInFeb2023Member2023-02-012023-02-280001035443are:TotalIssuanceOfUnsecuredSeniorNotesInFeb2023Member2023-02-280001035443us-gaap:SecuredOvernightFinancingRateSofrOvernightIndexSwapRateMemberus-gaap:LineOfCreditMember2023-01-012023-03-310001035443us-gaap:LineOfCreditMember2023-01-012023-03-310001035443us-gaap:LineOfCreditMember2022-09-220001035443us-gaap:SecuredOvernightFinancingRateSofrOvernightIndexSwapRateMemberus-gaap:LineOfCreditMember2022-01-012022-12-310001035443us-gaap:LineOfCreditMember2022-01-012022-12-310001035443srt:MinimumMemberus-gaap:CommercialPaperMember2023-01-012023-03-310001035443us-gaap:CommercialPaperMembersrt:MaximumMember2023-01-012023-03-310001035443are:AllForwardEquitySalesAgreementsOutstandingMember2023-03-310001035443are:AllForwardEquitySalesAgreementsOutstandingMember2023-01-012023-03-310001035443are:ATMCommonStockOfferingProgramEstablishedDecember2021Member2023-03-3100010354432022-05-010001035443are:NonCoreSubmarketMember2023-03-310001035443are:ChinaPropertiesMember2023-03-310001035443are:A15NeccoStreetMember2023-03-310001035443are:A15NeccoStreetMemberus-gaap:NoncontrollingInterestMemberare:ExistingPartnerMemberare:AlexandriaMember2023-03-310001035443us-gaap:NoncontrollingInterestMemberare:A15NeccoStreetMemberus-gaap:SubsequentEventMemberare:NewPartnerMemberare:AlexandriaMember2023-04-240001035443are:A15NeccoStreetMemberus-gaap:NoncontrollingInterestMemberus-gaap:SubsequentEventMemberare:AlexandriaMember2023-04-240001035443us-gaap:NoncontrollingInterestMemberare:A15NeccoStreetMemberare:ExistingPartnerMemberus-gaap:SubsequentEventMemberare:AlexandriaMember2023-04-240001035443are:A15NeccoStreetMemberus-gaap:SubsequentEventMember2023-04-242023-04-240001035443are:A15NeccoStreetMemberus-gaap:SubsequentEventMemberare:AlexandriaMember2023-04-240001035443are:A275GroveStreetMember2023-03-310001035443are:A275GroveStreetMember2023-01-012023-03-310001035443are:A275GroveStreetMemberus-gaap:SubsequentEventMember2023-04-242023-04-240001035443are:A275GroveStreetMemberus-gaap:SubsequentEventMember2023-04-24

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

☒ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES

EXCHANGE ACT OF 1934

For the quarterly period ended March 31, 2023

OR

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES

EXCHANGE ACT OF 1934

For the transition period from ____________ to ____________

Commission file number 1-12993

ALEXANDRIA REAL ESTATE EQUITIES, INC.

(Exact name of registrant as specified in its charter)

| | | | | | | | |

| Maryland | | 95-4502084 |

(State or other jurisdiction of

incorporation or organization) | | (I.R.S. Employer Identification Number) |

26 North Euclid Avenue, Pasadena, California 91101

(Address of principal executive offices) (Zip code)

(626) 578-0777

(Registrant’s telephone number, including area code)

N/A

(Former name, former address and former fiscal year, if changed since last report)

Securities registered pursuant to Section 12(b) of the Exchange Act:

| | | | | | | | |

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

| Common Stock, $0.01 par value per share | ARE | New York Stock Exchange |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | | | | |

| Large accelerated filer | ☒ | | Smaller reporting company | ☐ |

| Accelerated filer | ☐ | | Emerging growth company | ☐ |

| Non-accelerated filer | ☐ | | | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As of April 14, 2023, 173,013,623 shares of common stock, par value $0.01 per share, were outstanding.

TABLE OF CONTENTS

| | | | | | | | |

| | | Page |

| |

| | | |

| | |

| | | |

| | | |

| | | |

| Consolidated Financial Statements for the Three Months Ended March 31, 2023 and 2022: | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| | | |

| | |

| | | |

| | | |

| | | |

| | |

| | | |

| | |

| | | |

| | |

| | |

| |

| | | |

| | |

| | |

| | |

| | | |

| |

GLOSSARY

The following abbreviations or acronyms that may be used in this document shall have the adjacent meanings set forth below:

| | | | | |

| ASU | Accounting Standards Update |

| ATM | At the Market |

| CIP | Construction in Progress |

| EPS | Earnings per Share |

| ESG | Environmental, Social & Governance |

| FASB | Financial Accounting Standards Board |

| FDIC | Federal Deposit Insurance Corporation |

| FFO | Funds From Operations |

| GAAP | U.S. Generally Accepted Accounting Principles |

| IRS | Internal Revenue Service |

| JV | Joint Venture |

LEED® | Leadership in Energy and Environmental Design |

| Nareit | National Association of Real Estate Investment Trusts |

| NAV | Net Asset Value |

| NYSE | New York Stock Exchange |

| REIT | Real Estate Investment Trust |

| RSF | Rentable Square Feet/Foot |

| SEC | Securities and Exchange Commission |

| SF | Square Feet/Foot |

| SoDo | South of Downtown submarket of Seattle |

| SOFR | Secured Overnight Financing Rate |

| SoMa | South of Market submarket of the San Francisco Bay Area |

| U.S. | United States |

| VIE | Variable Interest Entity |

PART I – FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENTS (UNAUDITED)

Alexandria Real Estate Equities, Inc.

Consolidated Balance Sheets

(In thousands)

| | | | | | | | | | | |

| March 31, 2023 | | December 31, 2022 |

| (Unaudited) | | |

| Assets | | | |

Investments in real estate | $ | 30,889,395 | | | $ | 29,945,440 | |

Investments in unconsolidated real estate joint ventures | 38,355 | | | 38,435 | |

Cash and cash equivalents | 1,263,452 | | | 825,193 | |

Restricted cash | 34,932 | | | 32,782 | |

Tenant receivables | 8,197 | | | 7,614 | |

Deferred rent | 974,865 | | | 942,646 | |

Deferred leasing costs | 527,848 | | | 516,275 | |

Investments | 1,573,018 | | | 1,615,074 | |

Other assets | 1,602,403 | | | 1,599,940 | |

Total assets | $ | 36,912,465 | | | $ | 35,523,399 | |

| | | |

| Liabilities, Noncontrolling Interests, and Equity | | | |

Secured notes payable | $ | 73,645 | | | $ | 59,045 | |

Unsecured senior notes payable | 11,089,124 | | | 10,100,717 | |

Unsecured senior line of credit and commercial paper | 374,536 | | | — | |

Accounts payable, accrued expenses, and other liabilities | 2,479,047 | | | 2,471,259 | |

Dividends payable | 209,346 | | | 209,131 | |

Total liabilities | 14,225,698 | | | 12,840,152 | |

| | | |

Commitments and contingencies | | | |

| | | |

Redeemable noncontrolling interests | 44,862 | | | 9,612 | |

| | | |

Alexandria Real Estate Equities, Inc.’s stockholders’ equity: | | | |

Common stock | 1,709 | | | 1,707 | |

| Additional paid-in capital | 18,902,821 | | | 18,991,492 | |

| Accumulated other comprehensive loss | (20,536) | | | (20,812) | |

Alexandria Real Estate Equities, Inc.’s stockholders’ equity | 18,883,994 | | | 18,972,387 | |

Noncontrolling interests | 3,757,911 | | | 3,701,248 | |

Total equity | 22,641,905 | | | 22,673,635 | |

Total liabilities, noncontrolling interests, and equity | $ | 36,912,465 | | | $ | 35,523,399 | |

The accompanying notes are an integral part of these consolidated financial statements.

Alexandria Real Estate Equities, Inc.

Consolidated Statements of Operations

(In thousands, except per share amounts)

(Unaudited)

| | | | | | | | | | | | | | | |

| Three Months Ended March 31, | | |

| 2023 | | 2022 | | | | |

Revenues: | | | | | | | |

Income from rentals | $ | 687,949 | | | $ | 612,554 | | | | | |

Other income | 12,846 | | | 2,511 | | | | | |

Total revenues | 700,795 | | | 615,065 | | | | | |

| | | | | | | |

Expenses: | | | | | | | |

Rental operations | 206,933 | | | 181,328 | | | | | |

General and administrative | 48,196 | | | 40,931 | | | | | |

Interest | 13,754 | | | 29,440 | | | | | |

Depreciation and amortization | 265,302 | | | 240,659 | | | | | |

| | | | | | | |

| | | | | | | |

Total expenses | 534,185 | | | 492,358 | | | | | |

| | | | | | | |

| Equity in earnings of unconsolidated real estate joint ventures | 194 | | | 220 | | | | | |

| Investment loss | (45,111) | | | (240,319) | | | | | |

| | | | | | | |

| Net income (loss) | 121,693 | | | (117,392) | | | | | |

| Net income attributable to noncontrolling interests | (43,831) | | | (32,177) | | | | | |

| Net income (loss) attributable to Alexandria Real Estate Equities, Inc.’s stockholders | 77,862 | | | (149,569) | | | | | |

Net income attributable to unvested restricted stock awards | (2,606) | | | (2,081) | | | | | |

| Net income (loss) attributable to Alexandria Real Estate Equities, Inc.’s common stockholders | $ | 75,256 | | | $ | (151,650) | | | | | |

| | | | | | | |

| Net income (loss) per share attributable to Alexandria Real Estate Equities, Inc.’s common stockholders: | | | | | | | |

Basic | $ | 0.44 | | | $ | (0.96) | | | | | |

Diluted | $ | 0.44 | | | $ | (0.96) | | | | | |

The accompanying notes are an integral part of these consolidated financial statements.

Alexandria Real Estate Equities, Inc.

Consolidated Statements of Comprehensive Income

(In thousands)

(Unaudited)

| | | | | | | | | | | | | | | |

| Three Months Ended March 31, | | |

| 2023 | | 2022 | | | | |

| Net income (loss) | $ | 121,693 | | | $ | (117,392) | | | | | |

| Other comprehensive income | | | | | | | |

| Unrealized gains on foreign currency translation: | | | | | | | |

| Unrealized foreign currency translation gains arising during the period | 276 | | | 1,567 | | | | | |

| Unrealized gains on foreign currency translation, net | 276 | | | 1,567 | | | | | |

| | | | | | | |

| Total other comprehensive income | 276 | | | 1,567 | | | | | |

| Comprehensive income (loss) | 121,969 | | | (115,825) | | | | | |

| Less: comprehensive income attributable to noncontrolling interests | (43,831) | | | (32,177) | | | | | |

| Comprehensive income (loss) attributable to Alexandria Real Estate Equities, Inc.’s stockholders | $ | 78,138 | | | $ | (148,002) | | | | | |

The accompanying notes are an integral part of these consolidated financial statements.

Alexandria Real Estate Equities, Inc.

Consolidated Statement of Changes in Stockholders’ Equity and Noncontrolling Interests

(Dollars in thousands)

(Unaudited)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Alexandria Real Estate Equities, Inc.’s Stockholders’ Equity | | | | | | |

| | Number of

Common

Shares | | Common

Stock | | Additional

Paid-In Capital | | Retained

Earnings | | Accumulated Other Comprehensive Loss | | Noncontrolling

Interests | | Total

Equity | | Redeemable

Noncontrolling

Interests |

| Balance as of December 31, 2022 | | 170,748,395 | | | $ | 1,707 | | | $ | 18,991,492 | | | $ | — | | | $ | (20,812) | | | $ | 3,701,248 | | | $ | 22,673,635 | | | $ | 9,612 | |

| Net income | | — | | | — | | | — | | | 77,862 | | | — | | | 43,630 | | | 121,492 | | | 201 | |

| Total other comprehensive income | | — | | | — | | | — | | | — | | | 276 | | | — | | | 276 | | | — | |

| Contributions from and sales of noncontrolling interests | | — | | | — | | | 18,999 | | | — | | | — | | | 76,018 | | | 95,017 | | | 35,250 | |

| Distributions to and redemption of noncontrolling interests | | — | | | — | | | — | | | — | | | — | | | (62,985) | | | (62,985) | | | (201) | |

| | | | | | | | | | | | | | | | |

| Issuance pursuant to stock plan | | 194,586 | | | 2 | | | 35,782 | | | — | | | — | | | — | | | 35,784 | | | — | |

| Taxes related to net settlement of equity awards | | (83,277) | | | — | | | (11,968) | | | — | | | — | | | — | | | (11,968) | | | — | |

Dividends declared on common stock ($1.21 per share) | | — | | | — | | | — | | | (209,346) | | | — | | | — | | | (209,346) | | | — | |

| Reclassification of distributions in excess of earnings | | — | | | — | | | (131,484) | | | 131,484 | | | — | | | — | | | — | | | — | |

| Balance as of March 31, 2023 | | 170,859,704 | | | $ | 1,709 | | | $ | 18,902,821 | | | $ | — | | | $ | (20,536) | | | $ | 3,757,911 | | | $ | 22,641,905 | | | $ | 44,862 | |

The accompanying notes are an integral part of these consolidated financial statements.

Alexandria Real Estate Equities, Inc.

Consolidated Statement of Changes in Stockholders’ Equity and Noncontrolling Interests

(Dollars in thousands)

(Unaudited)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Alexandria Real Estate Equities, Inc.’s Stockholders’ Equity | | | | | | |

| | Number of

Common

Shares | | Common

Stock | | Additional

Paid-In Capital | | Retained

Earnings | | Accumulated Other Comprehensive Loss | | Noncontrolling

Interests | | Total

Equity | | Redeemable

Noncontrolling

Interests |

| Balance as of December 31, 2021 | | 158,043,880 | | | $ | 1,580 | | | $ | 16,195,256 | | | $ | — | | | $ | (7,294) | | | $ | 2,834,096 | | | $ | 19,023,638 | | | $ | 9,612 | |

| Net (loss) income | | — | | | — | | | — | | | (149,569) | | | — | | | 31,976 | | | (117,593) | | | 201 | |

| Total other comprehensive income | | — | | | — | | | — | | | — | | | 1,567 | | | — | | | 1,567 | | | — | |

| | | | | | | | | | | | | | | | |

| Contributions from and sales of noncontrolling interests | | — | | | — | | | 413,615 | | | — | | | — | | | 405,251 | | | 818,866 | | | — | |

| Distributions to and redemption of noncontrolling interests | | — | | | — | | | — | | | — | | | — | | | (30,300) | | | (30,300) | | | (201) | |

| Issuance of common stock | | 3,220,000 | | | 32 | | | 646,284 | | | — | | | — | | | — | | | 646,316 | | | — | |

| Issuance pursuant to stock plan | | 219,905 | | | 2 | | | 30,857 | | | — | | | — | | | — | | | 30,859 | | | — | |

| Taxes related to net settlement of equity awards | | (75,489) | | | — | | | (14,648) | | | — | | | — | | | — | | | (14,648) | | | — | |

Dividends declared on common stock ($1.15 per share) | | — | | | — | | | — | | | (187,701) | | | — | | | — | | | (187,701) | | | — | |

| Reclassification of distributions and net loss | | — | | | — | | | (337,270) | | | 337,270 | | | — | | | — | | | — | | | — | |

| Balance as of March 31, 2022 | | 161,408,296 | | | $ | 1,614 | | | $ | 16,934,094 | | | $ | — | | | $ | (5,727) | | | $ | 3,241,023 | | | $ | 20,171,004 | | | $ | 9,612 | |

The accompanying notes are an integral part of these consolidated financial statements.

| | | | | | | | | | | |

Alexandria Real Estate Equities, Inc. Consolidated Statements of Cash Flows (In thousands) (Unaudited)

|

| Three Months Ended March 31, |

| 2023 | | 2022 |

Operating Activities: | | | |

| Net income (loss) | $ | 121,693 | | | $ | (117,392) | |

| Adjustments to reconcile net income (loss) to net cash provided by operating activities: | | | |

| Depreciation and amortization | 265,302 | | | 240,659 | |

| Equity in earnings of unconsolidated real estate joint ventures | (194) | | | (220) | |

| Distributions of earnings from unconsolidated real estate joint ventures | 285 | | | 975 | |

| Amortization of loan fees | 3,639 | | | 3,103 | |

| Amortization of debt discounts (premiums) | 288 | | | (424) | |

| Amortization of acquired above- and below-market leases | (21,636) | | | (13,915) | |

| Deferred rent | (33,191) | | | (42,025) | |

| Stock compensation expense | 16,486 | | | 14,028 | |

| Investment loss | 45,111 | | | 240,319 | |

Changes in operating assets and liabilities: | | | |

| Tenant receivables | (582) | | | (191) | |

| Deferred leasing costs | (33,469) | | | (75,162) | |

| Other assets | (25,422) | | | (22,618) | |

| Accounts payable, accrued expenses, and other liabilities | (32,740) | | | (36,051) | |

| Net cash provided by operating activities | 305,570 | | | 191,086 | |

| | | |

Investing Activities: | | | |

| Additions to real estate | (873,366) | | | (666,364) | |

| Purchases of real estate | (177,543) | | | (1,903,800) | |

| Change in escrow deposits | 9,366 | | | 100,635 | |

| Investments in unconsolidated real estate joint ventures | (106) | | | (335) | |

| Return of capital from unconsolidated real estate joint ventures | — | | | 471 | |

| Additions to non-real estate investments | (47,401) | | | (64,247) | |

| Sales of and distributions from non-real estate investments | 49,385 | | | 44,842 | |

| Net cash used in investing activities | $ | (1,039,665) | | | $ | (2,488,798) | |

| | | | | | | | | | | |

Alexandria Real Estate Equities, Inc. Consolidated Statements of Cash Flows (In thousands) (Unaudited)

|

| Three Months Ended March 31, |

| 2023 | | 2022 |

Financing Activities: | | | |

| Borrowings from secured notes payable | $ | 14,428 | | | $ | 5,082 | |

| Repayments of borrowings from secured notes payable | — | | | (906) | |

| Proceeds from issuance of unsecured senior notes payable | 996,205 | | | 1,793,318 | |

| Borrowings from unsecured senior line of credit | 375,000 | | | 1,180,000 | |

| Repayments of borrowings from unsecured senior line of credit | (375,000) | | | (1,180,000) | |

| Proceeds from issuances under commercial paper program | 775,000 | | | 6,120,000 | |

| Repayments of borrowings under commercial paper program | (400,000) | | | (6,390,000) | |

| Payments of loan fees | (9,989) | | | (17,596) | |

| Taxes paid related to net settlement of equity awards | (7,854) | | | (8,906) | |

| Proceeds from issuance of common stock | — | | | 646,316 | |

| Dividends on common stock | (209,131) | | | (183,847) | |

| Contributions from and sales of noncontrolling interests | 79,337 | | | 819,610 | |

| Distributions to and purchases of noncontrolling interests | (63,186) | | | (30,501) | |

| Net cash provided by financing activities | 1,174,810 | | | 2,752,570 | |

| | | |

Effect of foreign exchange rate changes on cash and cash equivalents | (306) | | | 81 | |

| | | |

| Net increase in cash, cash equivalents, and restricted cash | 440,409 | | | 454,939 | |

Cash, cash equivalents, and restricted cash as of the beginning of period | 857,975 | | | 415,227 | |

Cash, cash equivalents, and restricted cash as of the end of period | $ | 1,298,384 | | | $ | 870,166 | |

| | | |

| Supplemental Disclosure and Non-Cash Investing and Financing Activities: | | | |

| Cash paid during the period for interest, net of interest capitalized | $ | 21,519 | | | $ | 22,550 | |

| Accrued construction for current-period additions to real estate | $ | 419,029 | | | $ | 300,713 | |

| Contribution of assets from real estate joint venture partner | $ | 33,250 | | | $ | — | |

| Issuance of noncontrolling interest to joint venture partner | $ | (33,250) | | | $ | — | |

| Right-of-use asset | $ | — | | | $ | 10,127 | |

| Lease liability | $ | — | | | $ | (10,127) | |

The accompanying notes are an integral part of these consolidated financial statements.

Alexandria Real Estate Equities, Inc.

Notes to Consolidated Financial Statements

(Unaudited)

1. ORGANIZATION AND BASIS OF PRESENTATION

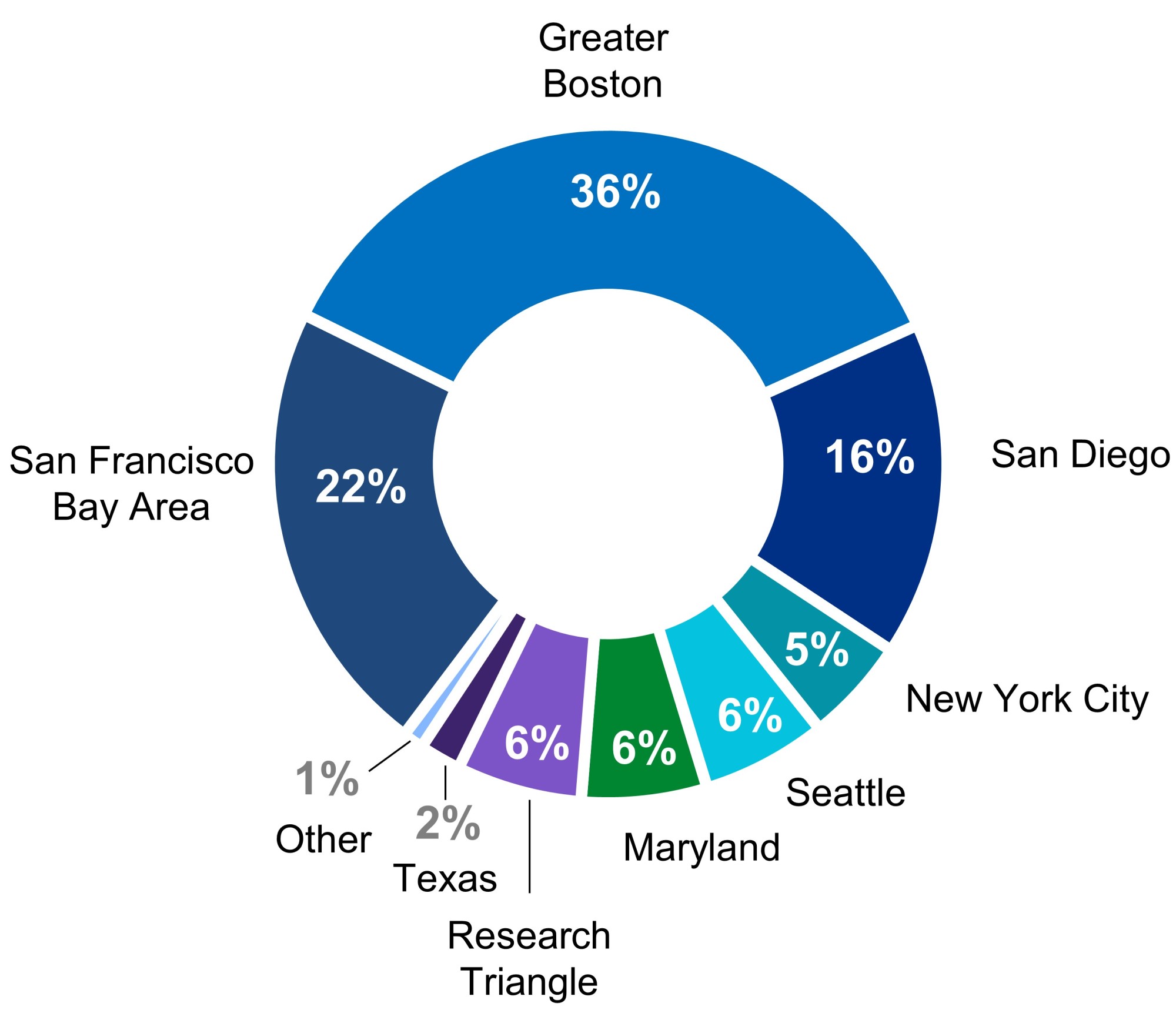

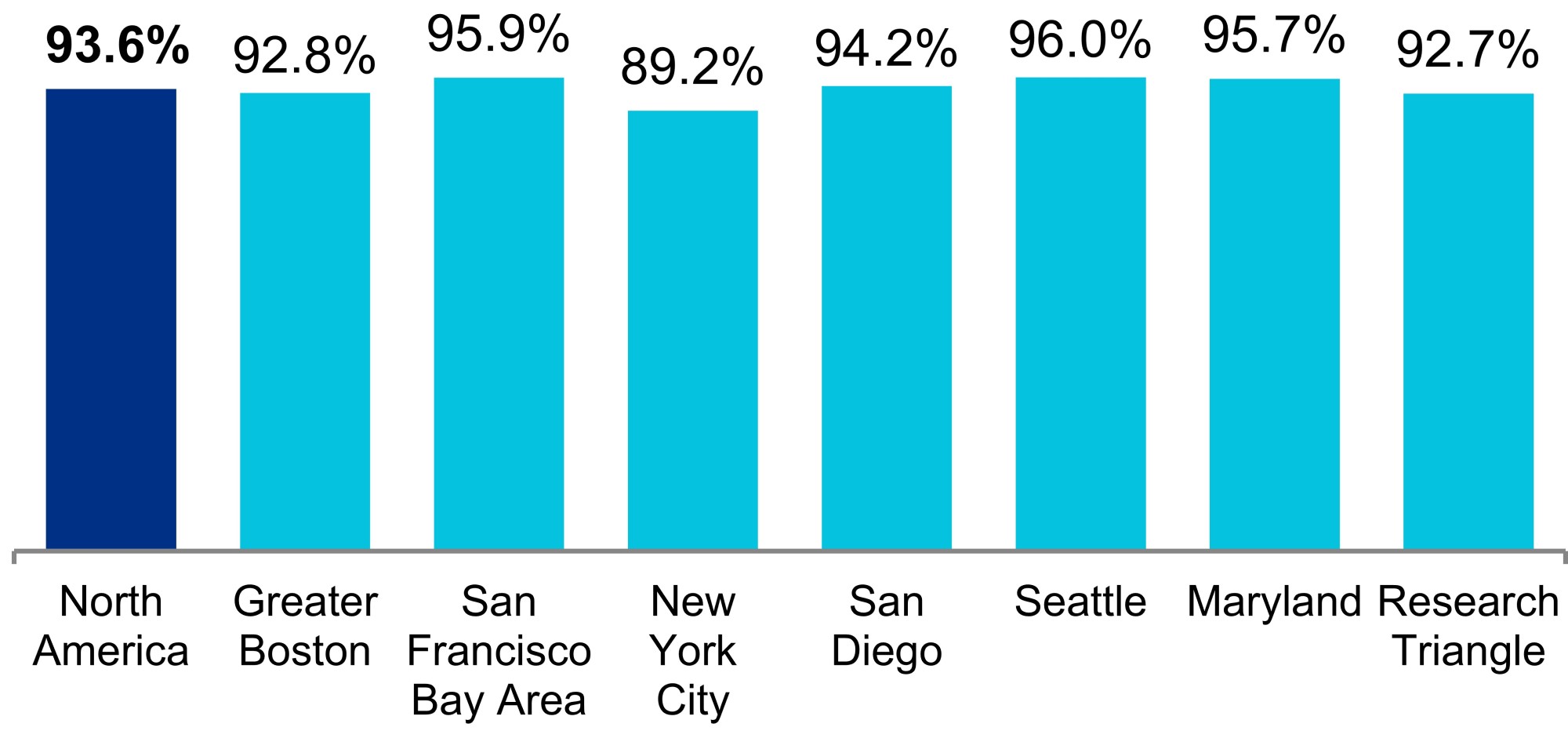

Alexandria Real Estate Equities, Inc. (NYSE:ARE), an S&P 500® life science REIT, is the pioneer of the life science real estate niche since its founding in 1994. Alexandria is the preeminent and longest-tenured owner, operator, and developer of collaborative life science, agtech, and advanced technology campuses in AAA innovation cluster locations, including Greater Boston, the San Francisco Bay Area, New York City, San Diego, Seattle, Maryland, and Research Triangle. With over 850 tenants, Alexandria has a total market capitalization of $33.0 billion and an asset base in North America of 75.6 million SF as of March 31, 2023. As used in this quarterly report on Form 10-Q, references to the “Company,” “Alexandria,” “ARE,” “we,” “us,” and “our” refer to Alexandria Real Estate Equities, Inc. and its consolidated subsidiaries. The accompanying unaudited consolidated financial statements include the accounts of Alexandria Real Estate Equities, Inc. and its consolidated subsidiaries. All significant intercompany balances and transactions have been eliminated.

We have prepared the accompanying interim consolidated financial statements in accordance with GAAP and in conformity with the rules and regulations of the SEC. In our opinion, these interim consolidated financial statements presented herein reflect all adjustments, of a normal recurring nature, that are necessary to fairly present the interim consolidated financial statements. The results of operations for the interim period are not necessarily indicative of the results that may be expected for the year ending December 31, 2023. These unaudited consolidated financial statements should be read in conjunction with the audited consolidated financial statements and the notes thereto included in our annual report on Form 10-K for the year ended December 31, 2022. Any references to our market capitalization, number or quality of buildings or tenants, quality of location, square footage, number of leases, or occupancy percentage, and any amounts derived from these values in these notes to consolidated financial statements are outside the scope of our independent registered public accounting firm’s review.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Consolidation

On an ongoing basis, as circumstances indicate the need for reconsideration, we evaluate each legal entity that is not wholly owned by us in accordance with the consolidation accounting guidance. Our evaluation considers all of our variable interests, including equity ownership, as well as fees paid to us for our involvement in the management of each partially owned entity. To fall within the scope of the consolidation guidance, an entity must meet both of the following criteria:

•The entity has a legal structure that has been established to conduct business activities and to hold assets; such entity can be in the form of a partnership, limited liability company, or corporation, among others; and

•We have a variable interest in the legal entity — i.e., variable interests that are contractual, such as equity ownership, or other financial interests that change with changes in the fair value of the entity’s net assets.

If an entity does not meet both criteria above, we apply other accounting literature, such as the cost or equity method of accounting. If an entity does meet both criteria above, we evaluate such entity for consolidation under either the variable interest model if the legal entity meets any of the following characteristics to qualify as a VIE, or under the voting model for all other legal entities that are not VIEs.

A legal entity is determined to be a VIE if it has any of the following three characteristics:

1)The entity does not have sufficient equity to finance its activities without additional subordinated financial support;

2)The entity is established with non-substantive voting rights (i.e., the entity deprives the majority economic interest holder(s) of voting rights); or

3)The equity holders, as a group, lack the characteristics of a controlling financial interest. Equity holders meet this criterion if they lack any of the following:

•The power, through voting rights or similar rights, to direct the activities of the entity that most significantly influence the entity’s economic performance, as evidenced by:

•Substantive participating rights in day-to-day management of the entity’s activities; or

•Substantive kick-out rights over the party responsible for significant decisions;

•The obligation to absorb the entity’s expected losses; or

•The right to receive the entity’s expected residual returns.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

Our real estate joint ventures consist of limited partnerships or limited liability companies. For an entity structured as a limited partnership or a limited liability company, our evaluation of whether the equity holders (equity partners other than the general partner or the managing member of a joint venture) lack the characteristics of a controlling financial interest includes the evaluation of whether the limited partners or non-managing members (the noncontrolling equity holders) lack both substantive participating rights and substantive kick-out rights, defined as follows:

•Participating rights provide the noncontrolling equity holders the ability to direct significant financial and operating decisions made in the ordinary course of business that most significantly influence the entity’s economic performance.

•Kick-out rights allow the noncontrolling equity holders to remove the general partner or managing member without cause.

If we conclude that any of the three characteristics of a VIE are met, including that the equity holders lack the characteristics of a controlling financial interest because they lack both substantive participating rights and substantive kick-out rights, we conclude that the entity is a VIE and evaluate it for consolidation under the variable interest model.

Variable interest model

If an entity is determined to be a VIE, we evaluate whether we are the primary beneficiary. The primary beneficiary analysis is a qualitative analysis based on power and benefits. We consolidate a VIE if we have both power and benefits — that is, (i) we have the power to direct the activities of a VIE that most significantly influence the VIE’s economic performance (power) and (ii) we have the obligation to absorb losses of or the right to receive benefits from the VIE that could potentially be significant to the VIE (benefits). We consolidate VIEs whenever we determine that we are the primary beneficiary. Refer to Note 4 – “Consolidated and unconsolidated real estate joint ventures” to our unaudited consolidated financial statements for information on specific joint ventures that qualify as VIEs. If we have a variable interest in a VIE but are not the primary beneficiary, we account for our investment using the equity method of accounting.

Voting model

If a legal entity fails to meet any of the three characteristics of a VIE (i.e., insufficiency of equity, existence of non-substantive voting rights, or lack of a controlling financial interest), we then evaluate such entity under the voting model. Under the voting model, we consolidate the entity if we determine that we, directly or indirectly, have greater than 50% of the voting shares and that other equity holders do not have substantive participating rights. Refer to Note 4 – “Consolidated and unconsolidated real estate joint ventures” to our unaudited consolidated financial statements for information on specific joint ventures that qualify for evaluation under the voting model.

Use of estimates

The preparation of consolidated financial statements in conformity with GAAP requires us to make estimates and assumptions that affect the reported amounts of assets, liabilities, and equity; the disclosure of contingent assets and liabilities as of the date of the consolidated financial statements; and the amounts of revenues and expenses during the reporting period. Actual results could materially differ from those estimates.

Investments in real estate

Evaluation of business combination or asset acquisition

We evaluate each acquisition of real estate or in-substance real estate (including equity interests in entities that predominantly hold real estate assets) to determine whether the integrated set of assets and activities acquired meets the definition of a business and needs to be accounted for as a business combination. An acquisition of an integrated set of assets and activities that does not meet the definition of a business is accounted for as an asset acquisition. If either of the following criteria is met, the integrated set of assets and activities acquired would not qualify as a business:

•Substantially all of the fair value of the gross assets acquired is concentrated in either a single identifiable asset or a group of similar identifiable assets; or

•The integrated set of assets and activities is lacking, at a minimum, an input and a substantive process that together significantly contribute to the ability to create outputs (i.e., revenue generated before and after the transaction).

An acquired process is considered substantive if:

•The process includes an organized workforce (or includes an acquired contract that provides access to an organized workforce) that is skilled, knowledgeable, and experienced in performing the process;

•The process cannot be replaced without significant cost, effort, or delay; or

•The process is considered unique or scarce.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

Generally, our acquisitions of real estate or in-substance real estate do not meet the definition of a business because substantially all of the fair value is concentrated in a single identifiable asset or group of similar identifiable assets (i.e., land, buildings, and related intangible assets) or because the acquisition does not include a substantive process in the form of an acquired workforce or an acquired contract that cannot be replaced without significant cost, effort, or delay. When evaluating acquired service or management contracts, we consider the nature of the services performed, the terms of the contract relative to similar arm’s-length contracts, and the availability of comparable vendors in evaluating whether the acquired contract constitutes a substantive process.

Recognition of real estate acquired

We evaluate each acquisition of real estate or in-substance real estate (including equity interests in entities that predominantly hold real estate assets) to determine whether the integrated set of assets and activities acquired meets the definition of a business and needs to be accounted for as a business combination. An acquisition of an integrated set of assets and activities that does not meet the definition of a business is accounted for as an asset acquisition.

For acquisitions of real estate or in-substance real estate that are accounted for as business combinations, we allocate the acquisition consideration (excluding acquisition costs) to the assets acquired, liabilities assumed, noncontrolling interests, and previously existing ownership interests at fair value as of the acquisition date. Assets include intangible assets such as tenant relationships, acquired in-place leases, and favorable intangibles associated with in-place leases in which we are the lessor. Liabilities include unfavorable intangibles associated with in-place leases in which we are the lessor. In addition, for acquired in-place finance or operating leases in which we are the lessee, acquisition consideration is allocated to lease liabilities and related right-of-use assets, adjusted to reflect favorable or unfavorable terms of the lease when compared with market terms. Any excess (deficit) of the consideration transferred relative to the fair value of the net assets acquired is accounted for as goodwill (bargain purchase gain). Acquisition costs related to business combinations are expensed as incurred.

Generally, we expect that acquisitions of real estate or in-substance real estate will not meet the definition of a business because substantially all of the fair value is concentrated in a single identifiable asset or group of similar identifiable assets (i.e., land, buildings, and related intangible assets). The accounting model for asset acquisitions is similar to the accounting model for business combinations, except that the acquisition consideration (including acquisition costs) is allocated to the individual assets acquired and liabilities assumed on a relative fair value basis. Any excess (deficit) of the consideration transferred relative to the sum of the fair value of the assets acquired and liabilities assumed is allocated to the individual assets and liabilities based on their relative fair values. As a result, asset acquisitions do not result in the recognition of goodwill or a bargain purchase gain. Incremental and external direct acquisition costs related to acquisitions of real estate or in-substance real estate (such as legal and other third-party services) are capitalized.

We exercise judgment to determine the key assumptions used to allocate the purchase price of real estate acquired among its components. The allocation of the consideration to the various components of properties acquired during the year can have an effect on our net income due to the useful depreciable and amortizable lives applicable to each component and the recognition of the related depreciation and amortization expense in our consolidated statements of operations. We apply judgment in utilizing available comparable market information to assess relative fair value. We assess the relative fair values of tangible and intangible assets and liabilities based on available comparable market information, including estimated replacement costs, rental rates, and recent market transactions. In addition, we may use estimated cash flow projections that utilize appropriate discount and capitalization rates. Estimates of future cash flows are based on a number of factors, including the historical operating results, known and anticipated trends, and market/economic conditions that may affect the property.

The value of tangible assets acquired is based upon our estimation of fair value on an “as if vacant” basis. The value of acquired in-place leases includes the estimated costs during the hypothetical lease-up period and other costs that would have been incurred in the execution of similar leases under the market conditions at the acquisition date of the acquired in-place lease. If there is a bargain fixed-rate renewal option for the period beyond the noncancelable lease term of an in-place lease, we evaluate intangible factors, such as the business conditions in the industry in which the lessee operates, the economic conditions in the area in which the property is located, and the ability of the lessee to sublease the property during the renewal term, in order to determine the likelihood that the lessee will renew. When we determine that there is reasonable assurance that such bargain purchase option will be exercised, we consider the option in determining the intangible value of such lease and its related amortization period. We also recognize the relative fair values of assets acquired, the liabilities assumed, and any noncontrolling interest in acquisitions of less than a 100% interest when the acquisition constitutes a change in control of the acquired entity.

Depreciation and amortization

The values allocated to buildings and building improvements, land improvements, tenant improvements, and equipment are depreciated on a straight-line basis. For buildings and building improvements, we depreciate using the shorter of the respective ground lease terms or their estimated useful lives, not to exceed 40 years. Land improvements are depreciated over their estimated useful lives, not to exceed 20 years. Tenant improvements are depreciated over their respective lease terms or estimated useful lives, and equipment is depreciated over the shorter of the lease term or its estimated useful life. The values of the right-of-use assets are amortized on a straight-line basis over the remaining terms of each related lease. The values of acquired in-place leases and

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

associated favorable intangibles (i.e., acquired above-market leases) are classified in other assets in our consolidated balance sheets and are amortized over the remaining terms of the related leases as a reduction of income from rentals in our consolidated statements of operations. The values of unfavorable intangibles (i.e., acquired below-market leases) associated with acquired in-place leases are classified in accounts payable, accrued expenses, and other liabilities in our consolidated balance sheets and are amortized over the remaining terms of the related leases as an increase in income from rentals in our consolidated statements of operations.

Capitalized project costs

We capitalize project costs, including pre-construction costs, interest, property taxes, insurance, and other costs directly related and essential to the development, redevelopment, pre-construction, or construction of a project. Capitalization of development, redevelopment, pre-construction, and construction costs is required while activities are ongoing to prepare an asset for its intended use. Fluctuations in our development, redevelopment, pre-construction, and construction activities could result in significant changes to total expenses and net income. Costs incurred after a project is substantially complete and ready for its intended use are expensed as incurred. Should development, redevelopment, pre-construction, or construction activity cease, interest, property taxes, insurance, and certain other costs would no longer be eligible for capitalization and would be expensed as incurred. Expenditures for repairs and maintenance are expensed as incurred.

Real estate sales

A property is classified as held for sale when all of the following criteria for a plan of sale have been met: (i) management, having the authority to approve the action, commits to a plan to sell the property; (ii) the property is available for immediate sale in its present condition, subject only to terms that are usual and customary; (iii) an active program to locate a buyer and other actions required to complete the plan to sell have been initiated; (iv) the sale of the property is probable and is expected to be completed within one year; (v) the property is being actively marketed for sale at a price that is reasonable in relation to its current fair value; and (vi) actions necessary to complete the plan of sale indicate that it is unlikely that significant changes to the plan will be made or that the plan will be withdrawn. Depreciation of assets ceases upon designation of a property as held for sale. For additional details, refer to Note 15 – “Assets classified as held for sale” to our unaudited consolidated financial statements.

If the disposal of a property represents a strategic shift that has (or will have) a major effect on our operations or financial results, such as (i) a major line of business, (ii) a major geographic area, (iii) a major equity method investment, or (iv) other major parts of an entity, then the operations of the property, including any interest expense directly attributable to it, are classified as discontinued operations in our consolidated statements of operations, and amounts for all prior periods presented are reclassified from continuing operations to discontinued operations. The disposal of an individual property generally will not represent a strategic shift and therefore will typically not meet the criteria for classification as a discontinued operation.

We recognize gains or losses on real estate sales in accordance with the accounting standard on the derecognition of nonfinancial assets arising from contracts with noncustomers. Our ordinary output activities consist of the leasing of space to our tenants in our operating properties, not the sales of real estate. Therefore, sales of real estate (in which we are the seller) qualify as contracts with noncustomers. In our transactions with noncustomers, we apply certain recognition and measurement principles consistent with our method of recognizing revenue arising from contracts with customers. Derecognition of the asset is based on the transfer of control. If a real estate sales contract includes our ongoing involvement with the property, then we evaluate each promised good or service under the contract to determine whether it represents a separate performance obligation, constitutes a guarantee, or prevents the transfer of control. If a good or service is considered a separate performance obligation, an allocated portion of the transaction price is recognized as revenue as we transfer the related good or service to the buyer.

The recognition of gain or loss on the sale of a partial interest also depends on whether we retain a controlling or noncontrolling interest in the property. If we retain a controlling interest in the property upon completion of the sale, we continue to reflect the asset at its book value, record a noncontrolling interest for the book value of the partial interest sold, and recognize additional paid-in capital for the difference between the consideration received and the partial interest at book value. Conversely, if we retain a noncontrolling interest upon completion of the sale of a partial interest of real estate, we recognize a gain or loss as if 100% of the asset were sold.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

Impairment of long-lived assets

Prior to and subsequent to the end of each quarter, we review current activities and changes in the business conditions of all of our long-lived assets to determine the existence of any triggering events or impairment indicators requiring an impairment analysis. If triggering events or impairment indicators are identified, we review an estimate of the future undiscounted cash flows, including, if necessary, a probability-weighted approach if multiple outcomes are under consideration.

Long-lived assets to be held and used, including our rental properties, CIP, land held for development, right-of-use assets related to operating leases in which we are the lessee, and intangibles, are individually evaluated for impairment when conditions exist that may indicate that the carrying amount of a long-lived asset may not be recoverable. The carrying amount of a long-lived asset to be held and used is not recoverable if it exceeds the sum of the undiscounted cash flows expected to result from the use and eventual disposition of the asset. Triggering events or impairment indicators for long-lived assets to be held and used are assessed by project and include significant fluctuations in estimated net operating income, occupancy changes, significant near-term lease expirations, current and historical operating and/or cash flow losses, construction costs, estimated completion dates, rental rates, and other market factors. We assess the expected undiscounted cash flows based upon numerous factors, including, but not limited to, construction costs, available market information, current and historical operating results, known trends, current market/economic conditions that may affect the asset, and our assumptions about the use of the asset, including, if necessary, a probability-weighted approach if multiple outcomes are under consideration.

Upon determination that an impairment has occurred, a write-down is recognized to reduce the carrying amount of the asset to its estimated fair value. If an impairment charge is not required to be recognized, the recognition of depreciation or amortization is adjusted prospectively, as necessary, to reduce the carrying amount of the asset to its estimated disposition value over the remaining period that the asset is expected to be held and used. We may adjust depreciation of properties that are expected to be disposed of or redeveloped prior to the end of their useful lives.

We use the held for sale impairment model for our properties classified as held for sale, which is different from the held and used impairment model. Under the held for sale impairment model, an impairment charge is recognized if the carrying amount of the long-lived asset classified as held for sale exceeds its fair value less cost to sell. Because of these two different models, it is possible for a long-lived asset previously classified as held and used to require the recognition of an impairment charge upon classification as held for sale.

International operations

In addition to operating properties in the U.S., we have 11 properties in Canada and one operating property in China. The functional currency for our subsidiaries operating in the U.S. is the U.S. dollar. The functional currencies for our foreign subsidiaries are the local currencies in each respective country. The assets and liabilities of our foreign subsidiaries are translated into U.S. dollars at the exchange rate in effect as of the financial statement date. Revenue and expense accounts of our foreign subsidiaries are translated using the weighted-average exchange rate for the periods presented. Gains or losses resulting from the translation are classified in accumulated other comprehensive income (loss) as a separate component of total equity and are excluded from net income (loss).

Whenever a foreign investment meets the criteria for classification as held for sale, we evaluate the recoverability of the investment under the held for sale impairment model. We may recognize an impairment charge if the carrying amount of the investment exceeds its fair value less cost to sell. In determining an investment’s carrying amount, we consider its net book value and any cumulative unrealized foreign currency translation adjustment related to the investment.

The appropriate amounts of foreign exchange rate gains or losses classified in accumulated other comprehensive income (loss) are reclassified to net income (loss) when realized upon the sale of our investment or upon the complete or substantially complete liquidation of our investment.

Investments

We hold investments in publicly traded companies and privately held entities primarily involved in the life science, agtech, and technology industries. As a REIT, we generally limit our ownership of each individual entity’s voting stock to less than 10%. We evaluate each investment to determine whether we have the ability to exercise significant influence, but not control, over an investee. We evaluate investments in which our ownership is equal to or greater than 20%, but less than or equal to 50%, of an investee’s voting stock with a presumption that we have this ability. For our investments in limited partnerships that maintain specific ownership accounts, we presume that such ability exists when our ownership interest exceeds 3% to 5%. In addition to our ownership interest, we consider whether we have a board seat or whether we participate in the policy-making process, among other criteria, to determine if we have the ability to exert significant influence, but not control, over an investee. If we determine that we have such ability, we account for the investment under the equity method of accounting, as described below.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

Investments accounted for under the equity method

Under the equity method of accounting, we initially recognize our investment at cost and subsequently adjust the carrying amount of the investment for our share of earnings or losses reported by the investee, distributions received, and other-than-temporary impairments. For more information about our investments accounted for under the equity method, refer to Note 7 – “Investments” to our unaudited consolidated financial statements.

Investments that do not qualify for the equity method of accounting

For investees over which we determine that we do not have the ability to exercise significant influence or control, we account for each investment depending on whether it is an investment in a (i) publicly traded company, (ii) privately held entity that reports NAV per share, or (iii) privately held entity that does not report NAV per share, as described below.

Investments in publicly traded companies

Our investments in publicly traded companies are classified as investments with readily determinable fair values and are presented at fair value in our consolidated balance sheets, with changes in fair value classified in investment income (loss) in our consolidated statements of operations. The fair values for our investments in publicly traded companies are determined based on sales prices or quotes available on securities exchanges.

Investments in privately held companies

Our investments in privately held entities without readily determinable fair values consist of (i) investments in privately held entities that report NAV per share and (ii) investments in privately held entities that do not report NAV per share. These investments are accounted for as follows:

Investments in privately held entities that report NAV per share

Investments in privately held entities that report NAV per share, such as our privately held investments in limited partnerships, are presented at fair value using NAV as a practical expedient, with changes in fair value classified in investment income (loss) in our consolidated statements of operations. We use NAV per share reported by limited partnerships generally without adjustment, unless we are aware of information indicating that the NAV reported by a limited partnership does not accurately reflect the fair value of the investment at our reporting date.

Investments in privately held entities that do not report NAV per share

Investments in privately held entities that do not report NAV per share are accounted for using a measurement alternative, under which these investments are measured at cost, adjusted for observable price changes and impairments, with changes classified in investment income (loss) in our consolidated statements of operations.

An observable price arises from an orderly transaction for an identical or similar investment of the same issuer, which is observed by an investor without expending undue cost and effort. Observable price changes result from, among other things, equity transactions of the same issuer executed during the reporting period, including subsequent equity offerings or other reported equity transactions related to the same issuer. To determine whether these transactions are indicative of an observable price change, we evaluate, among other factors, whether these transactions have similar rights and obligations, including voting rights, distribution preferences, and conversion rights to the investments we hold.

Impairment evaluation of equity method investments and investments in privately held entities that do not report NAV per share

We monitor equity method investments and investments in privately held entities that do not report NAV per share for new developments, including operating results, prospects and results of clinical trials, new product initiatives, new collaborative agreements, capital-raising events, and merger and acquisition activities. These investments are evaluated on the basis of a qualitative assessment for indicators of impairment by monitoring the presence of the following triggering events or impairment indicators:

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

(i)a significant deterioration in the earnings performance, credit rating, asset quality, or business prospects of the investee;

(ii)a significant adverse change in the regulatory, economic, or technological environment of the investee;

(iii)a significant adverse change in the general market condition, including the research and development of technology and products that the investee is bringing or attempting to bring to the market;

(iv)significant concerns about the investee’s ability to continue as a going concern; and/or

(v)a decision by investors to cease providing support or reduce their financial commitment to the investee.

If such indicators are present, we are required to estimate the investment’s fair value and immediately recognize an impairment charge in an amount equal to the investment’s carrying value in excess of its estimated fair value.

Investment income/loss recognition and classification

We recognize both realized and unrealized gains and losses in our consolidated statements of operations, classified in investment income (loss) in our consolidated statements of operations. Unrealized gains and losses represent:

(i)changes in fair value for investments in publicly traded companies;

(ii)changes in NAV for investments in privately held entities that report NAV per share;

(iii)observable price changes for investments in privately held entities that do not report NAV per share; and

(iv)our share of unrealized gains or losses reported by our equity method investees.

Realized gains and losses on our investments represent the difference between proceeds received upon disposition of investments and their historical or adjusted cost basis. For our equity method investments, realized gains and losses represent our share of realized gains or losses reported by the investee. Impairments are realized losses, which result in an adjusted cost basis, and represent charges to reduce the carrying values of investments in privately held entities that do not report NAV per share and equity method investments, if impairments are deemed other than temporary, to their estimated fair value.

Revenues

The table below provides details of our consolidated total revenues for the three months ended March 31, 2023 and 2022 (in thousands):

| | | | | | | | | | | | | | | | | | |

| | Three Months Ended March 31, | | |

| | 2023 | | 2022 | | | | |

| Income from rentals: | | | | | | | | |

| Revenues subject to the lease accounting standard: | | | | | | | | |

| Operating leases | | $ | 677,422 | | | $ | 603,513 | | | | | |

Direct financing and sales-type leases(1) | | 648 | | | 1,020 | | | | | |

| Revenues subject to the lease accounting standard | | 678,070 | | | 604,533 | | | | | |

| Revenues subject to the revenue recognition accounting standard | | 9,879 | | | 8,021 | | | | | |

| Income from rentals | | 687,949 | | | 612,554 | | | | | |

| Other income | | 12,846 | | | 2,511 | | | | | |

| Total revenues | | $ | 700,795 | | | $ | 615,065 | | | | | |