UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

(Mark One)

ACT OF 1934

For the fiscal year ended December 31 , 2020

or

ACT OF 1934

For the transition period from to

Commission file number 001-13251

(Exact Name of Registrant as Specified in Its Charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||||||||||

| (Address of principal executive offices) | (Zip Code) | ||||||||||

(302 ) 451-0200

(Registrant’s Telephone Number, Including Area Code)

(Former name, former address and former fiscal year, if changed since last report)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

par value $.20 per share | ||||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☑ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ☐ No ☑

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☑ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

| ☑ | Accelerated filer | ☐ | |||||||||||||||

| Non-accelerated filer | ☐ | (Do not check if a smaller reporting company) | Smaller reporting company | ||||||||||||||

| Emerging growth company | |||||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☑

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☑

The aggregate market value of voting common stock held by non-affiliates of the Registrant as of June 30, 2020 was $2.6 billion (based on closing sale price of $7.03 per share as reported for the NASDAQ Global Select Market).

As of January 31, 2021, there were 363,671,446 shares of common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

SLM CORPORATION

TABLE OF CONTENTS

| Page Number | ||||||||

| PART I | ||||||||

| Item 1. | ||||||||

| Item 1A. | ||||||||

| Item 1B. | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| PART II | ||||||||

| Item 5. | ||||||||

| Item 6. | ||||||||

| Item 7. | ||||||||

| Item 7A. | ||||||||

| Item 8. | ||||||||

| Item 9. | ||||||||

| Item 9A. | ||||||||

| Item 9B. | ||||||||

| PART III. | ||||||||

| Item 10. | ||||||||

| Item 11. | ||||||||

| Item 12. | ||||||||

| Item 13. | ||||||||

| Item 14. | ||||||||

| PART IV | ||||||||

| Item 15. | ||||||||

FORWARD-LOOKING AND CAUTIONARY STATEMENTS

References in this Annual Report on Form 10-K to “we,” “us,” “our,” “Sallie Mae,” “SLM” and the “Company” refer to SLM Corporation and its subsidiaries, except as otherwise indicated or unless the context otherwise requires.

This Annual Report on Form 10-K contains “forward-looking” statements and information based on management’s current expectations as of the date of this report. Statements that are not historical facts, including statements about our beliefs, opinions, or expectations and statements that assume or are dependent upon future events, are forward-looking statements. This includes, but is not limited to: statements regarding future developments surrounding COVID-19 or any other pandemic, including, without limitation, statements regarding the potential impact of COVID-19 or any other pandemic on the Company’s business, results of operations, financial condition, and/or cash flows; our expectation and ability to pay a quarterly cash dividend on our common stock in the future, subject to the determination by our Board of Directors, and based on an evaluation of our earnings, financial condition and requirements, business conditions, capital allocation determinations, and other factors, risks, and uncertainties; the Company’s 2021 guidance; the Company’s three-year horizon outlook; the Company’s expectation and ability to execute loan sales and share repurchases; the Company’s projections regarding originations, net charge-offs, non-interest expenses, earnings, balance sheet position, and other metrics; and any estimates related to accounting standard changes. Forward-looking statements are subject to risks, uncertainties, assumptions, and other factors that may cause actual results to be materially different from those reflected in such forward-looking statements. These factors include, among others, the risks and uncertainties set forth in Item 1A. “Risk Factors” and elsewhere in this Annual Report on Form 10-K and subsequent filings with the Securities and Exchange Commission (“SEC”); the societal, business, and legislative/regulatory impact of pandemics and other public heath crises; increases in financing costs; limits on liquidity; increases in costs associated with compliance with laws and regulations; failure to comply with consumer protection, banking, and other laws; changes in accounting standards and the impact of related changes in significant accounting estimates, including any regarding the measurement of our allowance for credit losses and the related provision expense; any adverse outcomes in any significant litigation to which we are a party; credit risk associated with our exposure to third-parties, including counterparties to our derivative transactions; and changes in the terms of education loans and the educational credit marketplace (including changes resulting from new laws and the implementation of existing laws). We could also be affected by, among other things: changes in our funding costs and availability; reductions to our credit ratings; cybersecurity incidents, cyberattacks, and other failures or breaches of our operating systems or infrastructure, including those of third-party vendors; damage to our reputation; risks associated with restructuring initiatives, including failures to successfully implement cost-cutting programs and the adverse effects of such initiatives on our business; changes in the demand for educational financing or in financing preferences of lenders, educational institutions, students, and their families; changes in law and regulations with respect to the student lending business and financial institutions generally; changes in banking rules and regulations, including increased capital requirements; increased competition from banks and other consumer lenders; the creditworthiness of our customers; changes in the general interest rate environment, including the rate relationships among relevant money-market instruments and those of our earning assets versus our funding arrangements; rates of prepayment on the loans that we own; changes in general economic conditions and our ability to successfully effectuate any acquisitions; and other strategic initiatives. The preparation of our consolidated financial statements also requires us to make certain estimates and assumptions, including estimates and assumptions about future events. These estimates or assumptions may prove to be incorrect. All forward-looking statements contained in this Annual Report on Form 10-K are qualified by these cautionary statements and are made only as of the date of this report. We do not undertake any obligation to update or revise these forward-looking statements to conform such statements to actual results or changes in our expectations.

1

AVAILABLE INFORMATION

Our website address is www.salliemae.com. Copies of our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q and Current Reports on Form 8-K, as well as any amendments to those reports, and our Proxy Statements and any significant investor presentations, are available free of charge through our website as soon as reasonably practicable after they are electronically filed with, or furnished to, the SEC. The SEC maintains a website at www.sec.gov that contains all such filed or furnished reports and other information. In addition, copies of our Board Governance Guidelines, Code of Business Conduct (which includes the code of ethics applicable to our Principal Executive Officer, Principal Financial Officer and Principal Accounting Officer) and the governing charters for each committee of our Board of Directors are available free of charge on our website, as well as in print, to any stockholder upon request. We intend to disclose any amendments to or waivers of our Code of Business Conduct (to the extent applicable to our Principal Executive Officer, Principal Financial Officer or Principal Accounting Officer) by posting such information on our website. Information contained or referenced on our website is not incorporated by reference into and does not form a part of this Annual Report on Form 10-K.

2

PART I.

Item 1. Business

Our Company Mission

SLM Corporation, more commonly known as Sallie Mae, is the premier financial brand in higher education. Our mission is to power confidence as students begin their unique journey. We simplify the college planning process by providing tools, resources, and information to help students and families make informed decisions and to improve access and support college completion through our scholarship programs and responsible financing options.

We believe education, in all forms, is the foundation for success, an equalizer of opportunities, and a proven pathway to economic mobility. Higher education increases lifetime wages and enables economic mobility. For example, data from the U.S. Bureau of Labor and Statistics confirms those with bachelor’s degrees earn 66 percent more than those with a high school diploma.1 Those with advanced degrees earn an even greater percentage than those with a high school diploma.1 This effect is multigenerational, as children of parents who are college educated are more likely to earn a bachelor’s degree than students whose parents did not go to college. Most would agree our society prospers and becomes more economically inclusive when each of its members is provided access to post-secondary education.2 Education represents a transformative investment in one’s future that yields our country’s next nurses, teachers, engineers, business leaders, and more.

Our History

While the Sallie Mae name has existed for more than 40 years, the company that operates as Sallie Mae today, SLM Corporation, was formed in late 2013 and includes its wholly-owned subsidiary, Sallie Mae Bank, an industrial bank established in 2005 (the “Bank”). On April 30, 2014, we legally separated (the “Spin-Off”) from another public company that is now named Navient Corporation (“Navient”), which is in the education loan management, servicing, asset recovery, and consolidation loan business. Navient retained all assets and liabilities generated prior to the Spin-Off other than those explicitly retained by us pursuant to the Separation and Distribution Agreement (as hereinafter defined) executed in connection with the Spin-Off. We are a consumer banking business and did not retain any assets or liabilities generated prior to the Spin-Off other than those explicitly retained by us pursuant to the Separation and Distribution Agreement. We sometimes refer to the company that existed prior to the Spin-Off as “pre-Spin-Off SLM.”

The Bank was formed in 2005 to fund and originate Private Education Loans (as hereinafter defined) on behalf of pre-Spin-Off SLM. While the Bank first originated Private Education Loans in February 2006, pre-Spin-Off SLM continued to purchase a portion of its Private Education Loans from third-party lending partners through mid-2009. With some minor exceptions, the Bank became the sole originator of Private Education Loans for pre-Spin-Off SLM beginning with the 2009-2010 academic year, the first academic year following the launch of the Bank’s Smart Option Student Loan program in mid-2009.

Our principal executive offices are located at 300 Continental Drive, Newark, Delaware 19713. Additionally, we have offices in New Castle, Delaware; Salt Lake City, Utah; Indianapolis, Indiana; Newton, Massachusetts; and Sterling, Virginia. Our telephone number is (302) 451-0200.

______________________

1 https://www.bls.gov/careeroutlook/2020/data-on-display/education-pays.htm

2 https://research.collegeboard.org/trends/education-pays

3

Our Business

Our business is focused and aligned to strategic imperatives that set the foundation for our continued success. These imperatives include: increasing the profitability and growth of our core business, continuing to build and advance a strong brand among our customers, helping policymakers better understand the student lending marketplace and our role in it, allocating capital and returning it to shareholders when appropriate, and fostering a true mission- and performance-led culture.

In 2020, we developed a new organizational structure to better align to these focused strategic imperatives, which resulted in reduced costs and improved operating efficiencies. For further information on these new imperatives, see Part II, Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations — 2020 Strategic Imperatives and Corporate Restructuring,” in this annual report on Form 10-K.

Private Education Loans

Our primary business is to originate and service high-quality Private Education Loans. “Private Education Loans” are education loans for students or their families that are not made, insured or guaranteed by any state or federal government. We also offer a range of deposit products insured by the Federal Deposit Insurance Corporation (the “FDIC”). In 2020, more than 420,000 families chose us as their Private Education Loan provider, more than any other private student loan lender. We originated $5.3 billion of Private Education Loans, a decrease of 5 percent from the year ended December 31, 2019, with the decrease largely due to the COVID-19 pandemic. As of December 31, 2020, we had $18.4 billion of Private Education Loans held for investment, net, outstanding.

The Private Education Loans we make to students and families serve primarily to bridge the gap between the cost of higher education and the amount funded through financial aid, federal loans and student and families’ resources. We also extend Private Education Loans as an alternative to similar federal education loan products where we believe our rates are competitive.

Our primary Private Education Loan product is the Smart Option Student Loan, which emphasizes in-school payment features that can produce shorter terms and reduce customers’ total finance charges. Customers generally elect one of three Smart Option repayment types at the time of loan origination. The first two, Interest Only and Fixed Payment options, require monthly payments while the student is in school and during the grace period thereafter, and accounted for approximately half of the Private Education Loans the Bank originated during 2020. The third repayment option is the more traditional deferred Private Education Loan product where customers are not required to make payments while the student is in school and during the grace period after separation from school. (The grace period for a Smart Option Student Loan generally runs for six months after the borrower separates from school, but can run for up to 36 months for a small subset of graduate loans.) Lower interest rates on the Interest Only and Fixed Payment options encourage customers to elect those options, which help customers reduce their total loan cost compared with the traditional deferred option loan. Making payments while in school helps customers become accustomed to making on-time regular loan payments. We offer both variable-rate and fixed-rate loans.

We also offer six loan products for specific graduate programs of study. These include the Sallie Mae Law School Loan, the Sallie Mae MBA Loan, the Sallie Mae Health Professions Graduate Loan, the Sallie Mae Medical School Loan, the Sallie Mae Dental School Loan, and the Sallie Mae Graduate School Loan. These products were designed to address the specific needs of graduate students, such as extended grace periods for medical students.

We regularly review and update the terms of our Private Education Loan products. Our Private Education Loans include important protections for the family, including loan forgiveness in case of death or permanent disability of the student borrower, a free, quarterly FICO score benefit to students and cosigners and, for borrowers with a Smart Option Student Loan, on-line tutoring services to help students succeed in school.

As a holder of Private Education Loans, we bear the full credit risk of the customers. We manage this risk by underwriting and pricing based on customized credit scoring criteria and the addition of qualified cosigners. For Private Education Loans originated during the year ended December 31, 2020, our average FICO scores (representing the higher credit scores of the cosigners or borrowers) at the time of original approval were 749, and approximately 86.0 percent of those loans were cosigned. In addition, we require school certification of both the need for, and the amount of, every Private Education Loan we originate (to prevent unnecessary borrowing beyond a school’s cost of attendance), and we disburse the loan proceeds directly to the higher education institutions to ensure loan proceeds are applied directly to the student’s education expenses.

The core of our marketing strategy is to promote our products on campuses through financial aid offices as well as through online and direct marketing to students and families. Our on-campus efforts with approximately 2,400 higher education institutions are led by our sales force, the largest in the industry, which has become a trusted resource for financial aid offices.

4

Our loans are high credit quality and the overwhelming majority of our customers manage their payments with great success. Private Education Loans in repayment include loans on which customers are making interest only or fixed payments, as well as loans that have entered full principal and interest repayment status after any applicable grace period. At December 31, 2020, 2.8 percent of Private Education Loans (held for investment) in repayment were greater than 30 days delinquent, and Private Education Loans (held for investment) in forbearance were 4.3 percent of loans in repayment and forbearance. In 2020, net charge-offs as a percentage of average loans in repayment were 1.17 percent.

Sallie Mae Bank

The Bank, which is regulated by the Utah Department of Financial Institutions (the “UDFI”), the FDIC, and the Consumer Financial Protection Bureau (the “CFPB”), offers traditional savings products, such as high-yield savings accounts, money market accounts, and certificates of deposit (“CDs”), originates Private Education Loans, and manages a loan portfolio that also includes loans insured or guaranteed under the previously existing Federal Family Education Loan Program (“FFELP Loans”) and credit card loans (“Credit Cards”). At December 31, 2020, the Bank had total assets of $30.3 billion, including $18.4 billion of Private Education Loans (held for investment), net, $735 million of FFELP Loans (held for investment), net, $11 million of Credit Cards (held for investment), net, and total deposits of $23.2 billion.

Our ability to obtain deposit funding and offer competitive interest rates on deposits will be necessary to sustain our Private Education Loan and other originations. Our ability to obtain such funding is dependent, in part, on the capital levels of the Bank and its compliance with other applicable regulatory requirements. At the time of this filing, there are no regulatory restrictions on our ability to obtain deposit funding or the interest rates we offer other than those restrictions generally applicable to all FDIC-insured banks of similar charter and size. We maintained our diversified funding base by raising $1.3 billion in term funding collateralized by pools of Private Education Loans in the long-term asset-backed securities (“ABS”) market in 2020. This brought our total ABS funding outstanding at December 31, 2020 to $4.5 billion, or 24 percent of our total Private Education Loans held for investment portfolio. We plan to continue to use ABS funding, market conditions permitting. This helps us better match-fund our assets and avoids excessive reliance on deposit funding.

See the subsection titled “Regulation of Sallie Mae Bank” under “Supervision and Regulation” for additional details about the Bank.

Credit Cards

We offer three types of credit cards, each uniquely designed to promote and reward financial responsibility, including a card that offers a cash back bonus that cardholders can apply to pay down a student loan. At December 31, 2020, we had $11 million of Credit Cards, net, outstanding in our held for investment portfolio.

SmartyPig

Our SmartyPig™ product is a free, FDIC-insured, online, goal-based savings account that helps consumers save for long- and short-term goals. Its tiered interest rates reward consumers for growing their savings.

Personal Loans and Upromise

In the fourth quarter of 2019, we discontinued originations of our unsecured personal loans used for non-educational purposes (“Personal Loans”) and did not originate or purchase any Personal Loans in 2020. In the third quarter of 2020, we sold our entire Personal Loan portfolio to focus our capital and attention on the core education loan business.

As part of our efforts to focus and align to our core business, on May 31, 2020, we also sold our Upromise Inc. subsidiary, which operated a free to join rewards program.

5

Our Lending Philosophy

Sallie Mae is committed to lending responsibly and encourages responsible borrowing by advising students and families to follow this three-step approach to paying for college:

Start with money you won’t have to pay back. Supplement your college savings and income by maximizing scholarships, grants, and work-study.

Explore federal student loans. Explore federal student loan options by completing the Free Application for Federal Student Aid (“FAFSA”).

Consider a responsible private student loan. Fill the gap between your available resources and the cost of college.

The best interests of our customers are front-and-center and integral to our responsible lending philosophy. We reward financial responsibility, emphasize building good credit, and provide flexible repayment terms to help customers manage and eliminate debt. We also embed customer protections in our products. To ensure applicants borrow only what they need to cover their school’s cost of attendance, we actively engage with schools and require school certification before we disburse a Private Education Loan. To help applicants understand their loan and its terms, we provide multiple, customized disclosures explaining the applicant’s starting interest rate, the interest rate during the life of the loan, and the loan’s total cost under the available repayment options. Our Private Education Loans feature (i) no origination fees and no prepayment penalties, (ii) interest rate reductions for those who enroll in and make monthly payments through auto debit, (iii) free access to quarterly FICO credit scores to help customers monitor their credit health, (iv) a choice of repayment options, and (v) a choice of either variable or fixed interest rates. Beginning in 2017, all newly-originated Private Education Loans for undergraduate students included the benefit of free access to study services at an online third-party vendor to assist students in advancing their education.

Our Approach to Assisting Students and Families Borrowing and Repaying Private Education Loans

Half of our Private Education Loan customers elect an in-school repayment option. By making in-school payments, customers learn to establish good repayment patterns, reduce their total loan cost, and graduate with less debt. We send monthly communications to customers while they are in school, even if they have no monthly payments scheduled, to keep them informed and encourage them to reduce the amount they will owe when they leave school.

Some customers transitioning from school to the work force may require more time before they are financially capable of making full payments of principal and interest. Sallie Mae created a Graduated Repayment Program (the “GRP”) to assist borrowers with additional payment flexibility, allowing customers to make interest-only payments instead of full principal and interest payments for a period of 12 months if they elect within a specified time frame to participate in the GRP. The time frame for electing to participate in the GRP begins six months before expiration of a borrower’s grace period and extends until 12 months after the expiration of the grace period. The 12-month interest only payments under the GRP begin upon expiration of a borrower’s grace period or election of the GRP, whichever is later.

Our experience has taught us the successful transition from school to full principal and interest repayment status involves making and carrying out a financial plan. As customers approach the principal and interest repayment period on their loans, Sallie Mae engages with them and communicates what to expect during the transition. In addition, SallieMae.com provides educational content for customers on how to organize loans, set up a monthly budget, and understand repayment obligations. Examples are provided to help explain how payments are applied and allocated, and see how the accrued interest on alternative repayment programs could affect the cost of customers’ loans. The site also provides important information on benefits available to service men and women under the Servicemembers Civil Relief Act (the “SCRA”).

After graduation, a customer may apply for the cosigner to be released from the loan. This option is available after 12 principal and interest payments are made and the student borrower adequately meets our credit requirements. In the event of a cosigner’s death, the student borrower automatically continues as the sole individual on the loan with the same terms.

If a customer’s account becomes delinquent, our collections centers work with the customer and/or the cosigner to understand their ability to make ongoing payments. If the customer is in financial hardship, we work with the customer and/or cosigner and identify any available alternative arrangements designed to reduce monthly payment obligations. These can include extended repayment schedules, temporary interest rate reductions and, if appropriate, short-term hardship forbearance (which typically is retroactive and granted by our collections department), suited to their individual circumstances and ability to make payments. Currently, our servicing centers generally also grant prospective forbearance if a borrower who is current requests it for increments of up to three months at a time, for up to 12 months. When we grant forbearance, we counsel customers on the effect forbearance will have on their loan balance. See Part II, Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations — Financial Condition — Allowance for Credit Losses — Use of

6

Forbearance and Rate Modifications as a Private Education Loan Collection Tool” for additional information about planned changes to our credit administration practices.

COVID-19 Response

We are accommodating to customers who face special circumstances or have trouble making loan payments. Like many Americans, some of our customers faced unforeseen challenges due to the pandemic of respiratory disease caused by the coronavirus 2019 or COVID-19 (“COVID-19”). In response, we took significant steps to provide relief to assist those customers. On March 10, 2020, we proactively posted assistance information on our web site and communicated to all Sallie Mae customers, including cosigners, to inform them assistance was available. We enhanced the functionality of our chat, automated phone system, mobile app, and website features to help all our customers manage their accounts, make or postpone payments, and request hardship relief. Customers may contact us in whatever way is most convenient for them.

Historically we have utilized disaster forbearance for material events, including hurricanes, wildfires, and floods. Disaster forbearance defers payments for as many as 90 days upon enrollment. In accordance with regulatory guidance that encourages lenders to work constructively with customers who have been impacted by COVID-19, we invoked this same disaster forbearance program to assist our customers through COVID-19 and offered this program across our operations, including through mobile and self-service channels such as chat and interactive voice response (“IVR”) to address initial high volumes at the onset of the pandemic. We have since returned to a policy of interacting with 100 percent of these customers through our customer care and collections personnel. Customers requesting a disaster forbearance or an extension of a disaster forbearance are required to speak with our customer care and collections personnel. The first wave of disaster forbearance was granted primarily in 90-day increments. As these forbearances ended in late second quarter and early third quarter, we reduced the disaster forbearance to one-month increments and implemented additional discussions between our servicing agents and borrowers to encourage borrowers/cosigners to enter repayment. Customers who receive a disaster forbearance do not progress in delinquency and are not assessed late fees or other fees. During a disaster forbearance, a customer’s credit file will continue to reflect the status of the loan as it was immediately prior to granting the disaster forbearance. During the period of the disaster forbearance, interest continues to accrue, but is not capitalized to the loan balance after the loan returns to repayment status. If the financial hardship extends beyond 90 days, additional assistance is available for eligible customers. For example, for borrowers exiting disaster forbearance and not eligible for GRP, we may allow them to make interest only payments for 12 months before reverting to full principal and interest payments. As of December 31, 2020, $44.2 million of Private Education Loans held for investment were in disaster forbearance status. For further information on the impact of COVID-19 on the Company, see Part II, Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations — Impact of COVID-19 on Sallie Mae,” in this annual report on Form 10-K.

Customer Service

We perform the origination, servicing and collections activities for all of our Private Education Loans in the United States with dedicated representatives assisting customers with various needs, including the military personnel customers who may be eligible for military benefits. We expect the Bank or affiliates of the Bank to retain servicing of all Private Education Loans the Bank originates, regardless of whether the loans are held, sold or securitized.

Over the past few years, we have implemented several improvements in our ability to interact with our loan customers, including:

•an integrated platform that allows customers and servicing agents to simultaneously access the same systems in real time interaction;

•an on-line chat function for customer service;

•a mobile application accessible through smart phones and the Apple watch; and

•initiation of customer surveys to gain feedback on areas for improvement within our servicing function.

These and other enhancements have contributed to streamlined originations and servicing processes, increased customer self-services rates, and improved customer satisfaction in all channels. The Company maintains an A+ rating with the Better Business Bureau.

Customer Success

We continue to adapt our business to best serve the needs of families who see us as a trusted advisor and partner. We are strongly invested in our customers’ success. Of total customers, 98 percent of loans in repayment are in good standing.

Our College Planning Calculator helps families set college savings goals, projects the full costs of a college degree, and estimates future student loan payments and the annual starting salary level needed to keep payments manageable.

7

Scholarship Search, our free online scholarship database, is home to more than 6 million scholarships collectively worth over $30 billion. For academic year (“AY”) 2019-2020, more than 24,000 students reported receiving at least one scholarship via our database, covering more than $67 million in college costs. Our Scholarship Search for Graduate Students includes access to approximately 1 million graduate school scholarships with an aggregate value of more than $1 billion.

In 2019, we unveiled a new, one-stop college-planning destination — Sallie Mae’s Paying for College Resource — created with, and for, high school educators and counselors. The Sallie Mae Paying for College Resource provides access to free, online college planning tools, short educational videos on financial aid, and other valuable information to help guide students and their families through the planning for college process.

In 2020, to raise awareness about the importance of completing the FAFSA and to simplify the process, we partnered with Embark, the leading provider of admissions software for schools and universities, to provide a free online tool to help families file the FAFSA. The tool reduces the average time it takes to complete the FAFSA from 55 minutes to less than 20 minutes.

8

Key Drivers of Private Education Loan Market Growth

The size of the Private Education Loan market is based primarily on three factors: college enrollment levels, the costs of attending college, and the availability of funds from the federal government to pay for a college education. The amounts students and their families can contribute toward college costs and the availability of scholarships and institutional grants are also important. If the cost of education increases at a pace exceeding the sum of family income, savings, federal lending, and scholarships, more students and families can be expected to rely on Private Education Loans. If enrollment levels or college costs decline, or the availability of federal education loans, grants or subsidies and scholarships significantly increases, Private Education Loan demand could decrease.

We focus primarily on students attending public and private not-for-profit four-year degree granting institutions. We lend to some students attending two-year and for-profit schools. Due to the low cost of two-year programs, federal grant and loan programs are typically sufficient for the funding needs of these students. Approximately 11 percent or $583 million of our 2020 Private Education Loan originations were for students attending for-profit schools. The for-profit schools where we continue to do business are primarily focused on career training and health care fields. We expect students who attend and complete programs at for-profit schools to support the same repayment performance as students who attend and graduate from public and private not-for-profit four-year degree granting institutions.

Our competitors1 in the Private Education Loan market include large banks such as Discover Bank, Citizens Financial Group, Inc. and PNC Bank, as well as a number of smaller specialty finance companies and members of the Education Finance Council. We compete based on our products, originations capability, price, and customer service.

Enrollment

We expect modest enrollment growth over the next several years.

Enrollment at Four-Year Degree Granting Institutions2

(in millions)

•According to the U.S. Department of Education’s projections released in December 2019, the high school graduate population is projected to remain relatively flat from 2020 to 2029.2

______________________

1Source: MeasureOne Q3 2020 Private Student Loan Report, November 2020. www.measureone.com.

2Source: U.S. Department of Education, National Center for Education Statistics, Projections of Education Statistics to 2029 (NCES, December 2019), Enrollment in Postsecondary Institutions (NCES, December 2019). These are the most recent sources available to us for this information.

9

Tuition Rates

•Average published tuition and fees (exclusive of room and board) at four-year public and private not-for-profit institutions increased at compound annual growth rates of 1.8 percent and 2.4 percent, respectively, from AYs 2016-2017 through 2020-2021. Average published tuition and fees at public and private four-year not-for-profit institutions grew 2.3 percent and 3.4 percent, respectively, between AYs 2018-2019 and 2019-2020 and 1.1 percent and 2.1 percent, respectively, between AYs 2019-2020 and 2020-2021.3 Tuition and fees are likely to continue to grow at the more modest rates of recent years.

Published Tuition and Fees3

(Dollars in actuals)

______

3 Source: The College Board-Trends in College Pricing 2020. © 2020 The College Board. www.collegeboard.org. The College Board restates its data annually, which may cause previously reported results to vary.

10

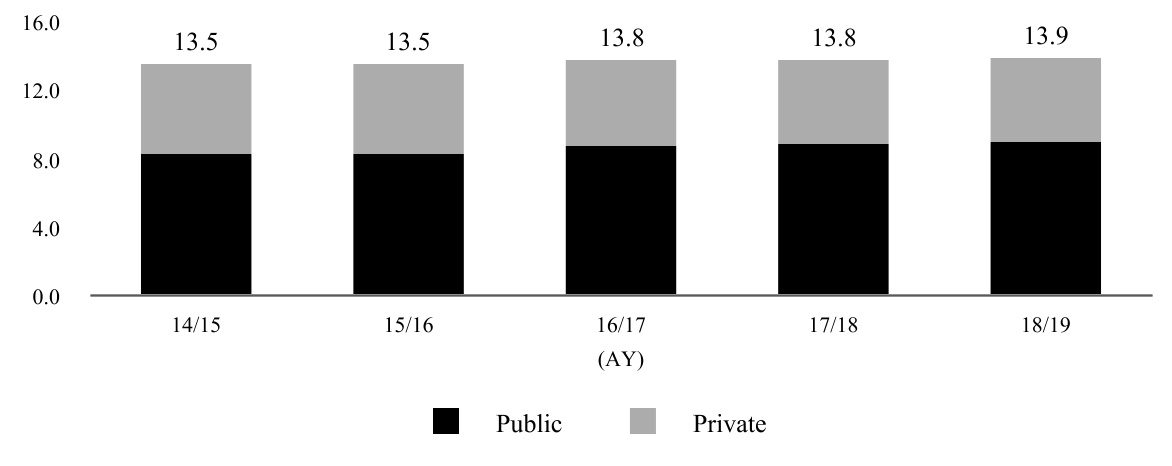

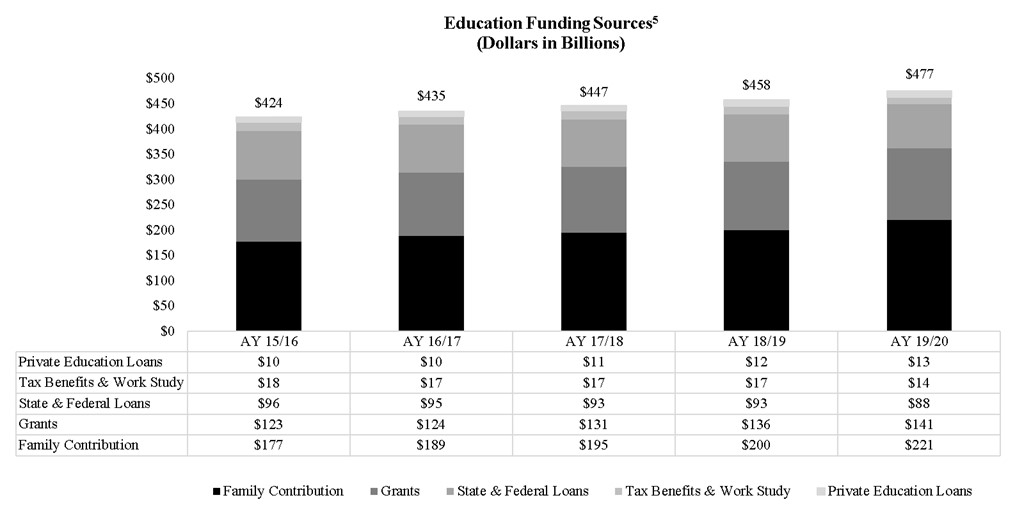

Sources of Funding

Private Education Loan originations increased to an estimated $13 billion in AY 2019-2020, up 10 percent over the previous year.4

_______

4 Source: The College Board-Trends in Student Aid 2016. © 2016 The College Board. www.collegeboard.org and The College Board-Trends in Student Aid 2020. © 2020 The College Board. www.collegeboard.org. MeasureOne www.measureone.com. Funding sources in current dollars and include federal and private loan data. 2020 Private Education Loan market assumptions use The College Board-Trends in Student Aid 2016© 2016 trends and College Board-Trends in Student Aid 2020 © 2020 data, and MeaureOne report. Other sources for the size of the Private Education Loan market exist and may cite the size of the market differently. The College Board restates its data annually, which may cause previously reported results to vary. We changed our source of participants in this 2020 annual report, removing our internal estimates for Private Education Loans made by smaller lenders, and relying solely on publicly available sources for market estimates, because we believe it provides a more appropriate basis for comparison of the performance of our business.

11

•We estimate total spending on higher education was $477 billion in AY 2019-2020, up from $424 billion in AY 2015-2016. Private Education Loan originations increased to an estimated $13 billion in AY 2019-2020, up 10 percent over the previous year and represent just 2.7 percent of total spending on higher education. Modest growth in total spending can lead to meaningful increases in Private Education Loans in the absence of growth in other sources of funding. .5

•Over the AYs 2015-2019 period, increases in total spending have been absorbed primarily through increased family contributions. If household finances continue to improve, we would expect this trend to continue.

_________________________

5 Source: Total post-secondary education spending is estimated by Sallie Mae determining the full-time equivalents for both graduates and undergraduates and multiplying by the estimated total per person cost of attendance for each school type. In doing so, we utilize information from the U.S. Department of Education, National Center for Education Statistics, Projections of Education Statistics to 2027 (NCES 2020, October 2020), The Integrated Postsecondary Education Data System (IPEDS), College Board -Trends in Student Aid 2016. © 2016 The College Board, www.collegeboard.org, College Board -Trends in Student Aid 2020. © 2020 The College Board, www.collegeboard.org, College Board -Trends in Student Pricing 2020. © 2020 The College Board, www.collegeboard.org, National Student Clearinghouse - Term Enrollment Estimates, and Company analysis. 2019 Private Education Loan market assumptions use The College Board-Trends in Student Aid 2016 © 2016 trends and College Board-Trends in Student Aid 2020 © 2020 data. Other sources for these data points also exist publicly and may vary from our computed estimates. NCES, IPEDS, and College Board restate their data annually, which may cause previous reports to vary. We have also recalculated figures in our Company analysis to standardize all costs of attendance to dollars not adjusted for inflation. This has a minimal impact on historically-stated numbers. | ||

12

Supervision and Regulation

Overview

We are subject to extensive regulation, examination and supervision by various federal, state and local authorities. The more significant aspects of the laws and regulations that apply to us and our subsidiaries are described below. These descriptions are qualified in their entirety by reference to the full text of the applicable statutes, legislation, regulations and policies, as they may be amended, and as interpreted and applied, by federal, state and local agencies.

The Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (the “Dodd-Frank Act”) was adopted to reform and strengthen regulation and supervision of the U.S. financial services industry. It contains comprehensive provisions to govern the practices and oversight of financial institutions and other participants in the financial markets. It mandates significant regulations, additional requirements and oversight on almost every aspect of the U.S. financial services industry, including increased capital and liquidity requirements, limits on leverage and enhanced supervisory authority. It requires the issuance of many regulations, which will take effect over several years.

Additionally, states are taking an increased interest in directly regulating the conduct and practices of student loan servicers. Some states recently have enacted legislation creating specialized offices within state government to oversee the student loan servicing industry operating within those states, as well as to set minimum standards governing the practices of student loan servicers. This represents a significant change from the past in which states generally did not issue laws and regulations tailored specifically to the student loan servicing industry.

Consumer Protection Laws and Regulations

Our origination, servicing, first-party collection and deposit taking activities subject us to federal and state consumer protection, privacy and related laws and regulations. Some of the more significant laws and regulations that are applicable to our business include:

•various state and federal laws governing unfair, deceptive or abusive acts or practices;

•various state laws and regulations imposing specific, mandated standards and requirements on the conduct and practices of student loan servicers;

•the federal Truth-In-Lending Act and Regulation Z, which govern disclosures of credit terms to consumer borrowers;

•the Fair Credit Reporting Act and Regulation V, which govern the use and provision of information to consumer reporting agencies;

•the Equal Credit Opportunity Act and Regulation B, which prohibit creditor practices that discriminate on the basis of race, religion and other prohibited factors in extending credit;

•the SCRA, which applies to all debts incurred prior to commencement of active military service (including education loans) and limits the amount of interest, including fees, that may be charged;

•the Truth in Savings Act and Regulation DD, which mandate certain disclosures related to consumer deposit accounts;

•the Expedited Funds Availability Act, Check Clearing for the 21st Century Act and Regulation CC issued by the Federal Reserve Bank (“FRB”), which relate to the availability of deposit funds to consumers;

•the Right to Financial Privacy Act, which imposes a duty to maintain the confidentiality of consumer financial records and prescribes procedures for complying with federal government requests for and subpoenas of financial records;

•the Electronic Funds Transfer Act and Regulation E, which govern automated transfers of funds and consumers’ rights related thereto;

•the Telephone Consumer Protection Act, which governs communication methods that may be used to contact customers;

•the Gramm-Leach-Bliley Act, which governs the ability of financial institutions to disclose nonpublic information about consumers to non-affiliated third-parties; and

•the California Consumer Privacy Act, which governs transparency and disclosure obligations regarding personal information of residents of the State of California.

13

Consumer Financial Protection Bureau

The CFPB has broad authority to promulgate regulations under federal consumer financial protection laws and to directly or indirectly enforce those laws, including providing regulatory oversight of the Private Education Loan industry, and to examine financial institutions for compliance. It is authorized to collect fines and order consumer restitution in the event of violations, engage in consumer financial education, track consumer complaints, request data and promote the availability of financial services to underserved consumers and communities. It has authority to prevent unfair, deceptive or abusive acts and practices by issuing regulations or by using its enforcement authority without first issuing regulations. The CFPB has been active in its supervision, examination and enforcement of financial services companies, notably bringing enforcement actions, imposing fines and mandating large refunds to customers of several large banking institutions. The CFPB is the Bank’s primary consumer compliance supervisor with compliance examination authority and primary consumer protection enforcement authority. The UDFI and FDIC remain the prudential regulatory authorities with respect to the Bank’s financial strength.

The Private Education Loan Ombudsman within the CFPB is authorized to receive and attempt to informally resolve inquiries about Private Education Loans. The Private Education Loan Ombudsman is required by law to report to Congress annually on the trends and issues identified through this process. The CFPB continues to take an active interest in the student loan industry, undertaking a number of initiatives related to the Private Education Loan market and student loan servicing. In early February 2020, the CFPB entered into a Memorandum of Understanding with the U.S. Department of Education (the “CFPB/DOE MOU”) in order to better serve student loan borrowers. Under the agreement, the agencies will share complaint information from borrowers and meet quarterly to discuss, among other things, the nature of complaints received and available information about the resolution of complaints.

Regulation of Sallie Mae Bank

The Bank was chartered in 2005 and is a Utah industrial bank regulated by the FDIC, the UDFI and the CFPB. We are not a bank holding company under the Bank Holding Company Act and therefore are not subject to the federal regulations applicable to bank holding companies. However, we and our non-bank subsidiaries are subject to regulation and oversight as institution-affiliated parties. The following discussion sets forth some of the elements of the bank regulatory framework applicable to us, the Bank and our other non-bank subsidiaries.

General

The Bank is currently subject to prudential regulation and examination by the FDIC and the UDFI, and consumer compliance regulation and examination by the CFPB. Numerous other federal and state laws and regulations govern almost all aspects of the operations of the Bank and, to some degree, our operations and those of our non-bank subsidiaries as institution-affiliated parties.

Actions by Federal and State Regulators

Under federal and state laws and regulations pertaining to the safety and soundness of insured depository institutions, the UDFI and the FDIC have the authority to compel or restrict certain actions of the Bank if it is determined to lack sufficient capital or other resources, or is otherwise operating in a manner deemed to be inconsistent with safe and sound banking practices. Under this authority, the Bank’s regulators can require it to enter into informal or formal supervisory agreements, including board resolutions, memoranda of understanding, written agreements and consent or cease and desist orders, pursuant to which the Bank would be required to take identified corrective actions to address cited concerns and refrain from taking certain actions.

14

Enforcement Powers of Regulators

As “institution-affiliated parties” of the Bank, we, our non-bank subsidiaries and our management, employees, agents, independent contractors and consultants are subject to potential civil and criminal penalties for violations of law, regulations or written orders of a government agency. Violations can include failure to timely file required reports, filing false or misleading information or submitting inaccurate reports. Civil penalties may be as high as $1,000,000 per day for such violations, and criminal penalties for some financial institution crimes may include imprisonment for 20 years. Regulators have flexibility to commence enforcement actions against institutions and institution-affiliated parties, and the FDIC has the authority to terminate deposit insurance. When issued by a banking agency, cease and desist and similar orders may, among other things, require affirmative action to correct any harm resulting from a violation or practice, including by compelling restitution, reimbursement, indemnifications or guarantees against loss. A financial institution may also be ordered to restrict its growth, dispose of certain assets, rescind agreements or contracts, or take other actions determined to be appropriate by the ordering agency. The federal banking regulators also may remove a director or officer from an insured depository institution (or bar them from the industry) if a violation is willful or reckless.

In May 2014, the Bank received a Civil Investigative Demand (“CID”) from the CFPB as part of the CFPB’s separate investigation relating to customer complaints, fees and charges assessed in connection with the servicing of student loans and related collection practices of pre-Spin-Off SLM by entities now subsidiaries of Navient during a time period prior to the Spin-Off (the “CFPB Investigation”). Two state attorneys general also provided the Bank identical CIDs and other state attorneys general have become involved in the inquiry over time (collectively, the “Multi-State Investigation”). To the extent requested, the Bank has been cooperating fully with the CFPB and the attorneys general conducting the Multi-State Investigation. Given the timeframe covered by the CIDs, the CFPB Investigation and the Multi-State Investigation, and the focus on practices and procedures previously conducted by Navient and its servicing subsidiaries prior to the Spin-Off, Navient is leading the response to these investigations. Consequently, we have no basis from which to estimate either the duration or ultimate outcome of these investigations.

With regard to the CFPB Investigation, we note that on January 18, 2017, the CFPB filed a complaint in federal court in Pennsylvania against Navient, along with its subsidiaries, Navient Solutions, Inc. and Pioneer Credit Recovery, Inc. The complaint alleges these Navient entities, among other things, engaged in deceptive practices with respect to their historic servicing and debt collection practices. Neither SLM, the Bank, nor any of their current subsidiaries are named in, or otherwise a party to, the lawsuit and are not alleged to have engaged in any wrongdoing. The CFPB’s complaint asserts Navient’s assumption of these liabilities pursuant to the Separation and Distribution Agreement entered into by the Company and Navient in connection with the Spin-Off (the “Separation and Distribution Agreement”).

On January 18, 2017, the Illinois Attorney General filed a lawsuit in Illinois state court against Navient - its subsidiaries Navient Solutions, Inc., Pioneer Credit Recovery, Inc., and General Revenue Corporation - and the Bank arising out of the Multi-State Investigation. On March 20, 2017, the Bank moved to dismiss the Illinois Attorney General action as to the Bank, arguing, among other things, the complaint failed to allege with sufficient particularity or specificity how the Bank was responsible for any of the alleged conduct, most of which predated the Bank’s existence. On July 10, 2018, the Court granted the Bank’s motion to dismiss without prejudice. On August 7, 2018, the Illinois Attorney General filed a First Amended Complaint and, on October 9, 2018, the Bank again moved to dismiss the action based on grounds similar to those raised in its March 20, 2017 motion. The Illinois Attorney General filed its response on November 21, 2018, and the Bank filed its reply on December 10, 2018. Oral argument on the motion took place on January 9, 2019. The Court took the motion under advisement.

To date, four other state attorneys general (California, Washington, Pennsylvania, and New Jersey) have filed suits against Navient and one or more of its current subsidiaries arising out of the Multi-State Investigation. Neither SLM, the Bank, nor any of their current subsidiaries are named in, or otherwise a party to, the California, Washington, Pennsylvania, or New Jersey lawsuits, and no claims are asserted against them. Each complaint asserts in its own fashion that Navient assumed responsibility under the Separation and Distribution Agreement for the alleged conduct in the complaints prior to the Spin-Off. On September 24, 2018, the Washington Attorney General served a third-party subpoena on the Bank calling for the production of certain records. The Bank has responded to the subpoena.

Additional lawsuits may arise from the Multi-State Investigation which may or may not name the Company, the Bank or any of their current subsidiaries as parties to these suits. Pursuant to the terms of the Separation and Distribution Agreement, and as contemplated by the structure of the Spin-Off, Navient is legally obligated to indemnify the Bank against all claims, actions, damages, losses or expenses that may arise from the conduct of all activities of pre-Spin-Off SLM occurring prior to the Spin-Off, except for certain liabilities related to the conduct of the pre-Spin-Off consumer banking business that were specifically assumed by the Bank (and as to which the Bank is obligated to indemnify Navient). Navient has acknowledged its indemnification obligations under the Separation and Distribution Agreement, in connection with the Multi-State Investigation

15

and the related lawsuits in which the Bank has been named as a party. Navient has informed the Bank, however, that it believes that the Bank may be responsible to indemnify Navient against certain potential liabilities arising from the above-described lawsuits under the Separation and Distribution Agreement and/or a separate loan servicing agreement between the parties, and has suggested that the parties defer further discussion regarding indemnification obligations, and reimbursement of ongoing legal costs, in connection with the lawsuits until the lawsuits are resolved. The Bank disagrees with Navient’s position and the Bank has reiterated to Navient that Navient is responsible for promptly indemnifying the Bank against all liabilities arising out of the conduct of pre-Spin-Off SLM that are at issue in the Multi-State Investigation and in the above-described lawsuits.

Standards for Safety and Soundness

The Federal Deposit Insurance Act requires the federal banking regulatory agencies such as the FDIC to prescribe, by regulation or guidance, operational and managerial standards for all insured depository institutions, such as the Bank, relating to internal controls, information systems and audit systems, loan documentation, credit underwriting, interest rate risk exposure, and asset quality. The agencies also must prescribe standards for earnings and stock valuation, as well as standards for compensation, fees and benefits. The federal banking regulators have implemented these required standards through regulations and interagency guidance designed to identify and address problems at insured depository institutions before capital becomes impaired. Under the regulations, if a regulator determines a bank fails to meet any prescribed standards, the regulator may require the bank to submit an acceptable plan to achieve compliance, consistent with deadlines for the submission and review of such safety and soundness compliance plans.

Dividends and Share Repurchase Programs

The Bank is chartered under the laws of the State of Utah and its deposits are insured by the FDIC. The Bank’s ability to pay dividends is subject to the laws of Utah and the regulations of the FDIC. Generally, under Utah’s industrial bank laws and regulations as well as FDIC regulations, the Bank may pay dividends to the Company from its net profits without regulatory approval if, following the payment of the dividend, the Bank’s capital and surplus would not be impaired.

The Company pays quarterly cash dividends on its outstanding Floating-Rate Non-Cumulative Preferred Stock, Series B (the “Series B Preferred Stock”) when, as, and if declared by its Board of Directors, in the Board’s discretion. In January 2019, the Company initiated a new policy to pay a regular, quarterly cash dividend on its common stock as well, beginning in the first quarter of 2019, and its Board of Directors approved a common stock share repurchase program.

Common stock dividend declarations are subject to determination by, and the discretion of, the Company’s Board of Directors. The Company may change its common stock dividend policy at any time.

The January 23, 2019 share repurchase program (the “2019 Share Repurchase Program”), which was effective upon announcement and expired on January 22, 2021, permitted the Company to repurchase from time to time shares of its common stock up to an aggregate repurchase price not to exceed $200 million. We have utilized all capacity under the 2019 Share Repurchase Program, having repurchased 17 million shares of common stock for $167 million for the year ended December 31, 2019 and 3 million shares of common stock for $33 million in the year ended December 31, 2020.

The January 22, 2020 share repurchase program (the “2020 Share Repurchase Program”), which was effective upon announcement and expires on January 21, 2022, permits the Company to repurchase shares of its common stock from time to time up to an aggregate repurchase price not to exceed $600 million.

Under the authority of the 2020 Share Repurchase Program, on March 10, 2020, we entered into an accelerated share repurchase agreement (“ASR”) with a third-party financial institution under which we paid $525 million for an upfront delivery of our common stock and a forward agreement. On March 11, 2020, the third-party financial institution delivered to us approximately 44.9 million shares. The final total actual number of shares of common stock delivered to us pursuant to the forward agreement was based upon the Rule 10b-18 volume-weighted average price at which the shares of our common stock traded during the regular trading sessions on the NASDAQ Global Select Market during the term of the ASR. The transactions are accounted for as equity transactions and are included in treasury stock when the shares are received, at which time there is an immediate reduction in the weighted average common shares calculation for basic and diluted earnings per share. On January 26, 2021, we completed the ASR and upon final settlement on January 28, 2021, we received an additional 13 million shares. In total, we repurchased 58 million shares under the ASR at an average price per share of $9.01. For additional information, see Notes to Consolidated Financial Statements, Note 25, “Subsequent Events.”

16

In October 2020, we initiated a cash tender offer to purchase up to 2,000,000 shares of our Series B Preferred Stock. On November 30, 2020, we accepted for purchase 1,489,304 shares of the Series B Preferred Stock at a purchase price of $45 per share plus an amount equal to accrued and unpaid dividends, for an aggregate purchase price of approximately $68 million.

On January 27, 2021, the Company announced a new share repurchase program (the “2021 Share Repurchase Program”), which was effective upon announcement and expires on January 26, 2023, and permits the Company to repurchase shares of its common stock from time to time up to an aggregate repurchase price not to exceed $1.25 billion.

On February 2, 2021, we announced the commencement of a tender offer (the “Tender Offer”) to purchase up to $1 billion in aggregate purchase price of our outstanding shares of common stock, par value $0.20 per share (the “Securities”) or such lesser aggregate purchase price of Securities as are properly tendered and not properly withdrawn, at a single per-Security price not greater than $15.00 nor less than $13.10 per share to the seller in cash, less any applicable withholding taxes and without interest. The Tender Offer may be amended from time to time, and will expire, upon the terms and conditions described in the relevant Tender Offer materials filed with the SEC. The results of the Tender Offer will be reflected in the Company’s financial results for the first fiscal quarter of 2021.

Repurchases under the programs may occur from time to time and through a variety of methods, including tender offers, open market repurchases, repurchases effected through Rule 10b5-1 trading plans, negotiated block purchases, accelerated share repurchase programs, or other similar transactions. The timing and volume of any repurchases under the 2020 Share Repurchase Program and the 2021 Share Repurchase Program will be subject to market conditions, and there can be no guarantee that the Company will repurchase up to the limit of the programs or at all.

We expect that the Bank will pay dividends to the Company as may be necessary to enable the Company to pay any declared dividends on its Series B Preferred Stock and common stock and to consummate any common share repurchases by the Company under the share repurchase programs. The Bank declared $579 million and $254 million in dividends for the years ended December 31, 2020 and 2019, respectively, with the proceeds primarily used to fund the 2019 and 2020 Share Repurchase Programs and stock dividends. The Bank paid no dividends on its common stock for the year ended December 31, 2018.

Regulatory Capital Requirements

The Bank is subject to various regulatory capital requirements administered by the FDIC and the UDFI. Failure to meet minimum capital requirements can initiate certain mandatory and possibly additional discretionary actions by regulators that, if undertaken, could have a material adverse effect on our business, results of operations and financial position. Under the FDIC’s regulations implementing the Basel III capital framework (“U.S. Basel III”) and the regulatory framework for prompt corrective action, the Bank must meet specific capital standards that involve quantitative measures of its assets, liabilities and certain off-balance sheet items as calculated under regulatory accounting practices. The Bank’s capital amounts and its classification under the prompt corrective action framework are also subject to qualitative judgments by the regulators about components of capital, risk weightings and other factors.

The Bank is subject to the following minimum capital ratios under U.S. Basel III: a Common Equity Tier 1 risk-based capital ratio of 4.5 percent, a Tier 1 risk-based capital ratio of 6.0 percent, a Total risk-based capital ratio of 8.0 percent, and a Tier 1 leverage ratio of 4.0 percent. In addition, the Bank is subject to a Common Equity Tier 1 capital conservation buffer of greater than 2.5 percent. Failure to maintain the buffer will result in restrictions on the Bank’s ability to make capital distributions, including the payment of dividends, and to pay discretionary bonuses to executive officers. Including the buffer, the Bank is required to maintain the following capital ratios under U.S. Basel III in order to avoid such restrictions: a Common Equity Tier 1 risk-based capital ratio of greater than 7.0 percent, a Tier 1 risk-based capital ratio of greater than 8.5 percent and a Total risk-based capital ratio of greater than 10.5 percent.

To qualify as “well capitalized” under the prompt corrective action framework for insured depository institutions, the Bank must maintain a Common Equity Tier 1 risk-based capital ratio of at least 6.5 percent, a Tier 1 risk-based capital ratio of at least 8.0 percent, a Total risk-based capital ratio of at least 10.0 percent, and a Tier 1 leverage ratio of at least 5.0 percent.

On August 26, 2020, the FDIC and other federal banking agencies published a final rule that provides those banking organizations that adopt CECL (as hereinafter defined) during the 2020 calendar year with the option to delay for two years, and then phase in over the following three years, the effects on regulatory capital of CECL relative to the incurred loss methodology. We have elected to use this option. The final rule is substantially similar to an interim final rule issued on March 27, 2020. Under this final rule, because we have elected to use the deferral option, the regulatory capital impact of our transition adjustments recorded on January 1, 2020 from the adoption of CECL will be deferred for two years. In addition, from January 1, 2020 through the end of the two-year deferral period, 25 percent of the ongoing impact of CECL on our allowance for credit

17

losses, retained earnings, and average total consolidated assets, each as reported for regulatory capital purposes, will be added to the deferred transition amounts (“adjusted transition amounts”) and deferred for the two-year period. At the conclusion of the two-year period (i.e., beginning January 1, 2022), the adjusted transition amounts will be phased in for regulatory capital purposes at a rate of 25 percent per year, with the phased-in amounts included in regulatory capital at the beginning of each year. Our January 1, 2020 CECL transition amounts increased the allowance for credit losses by $1.1 billion, increased the liability representing our off-balance sheet exposure for unfunded commitments by $116 million, and increased our deferred tax asset by $306 million, resulting in a cumulative effect adjustment that reduced retained earnings by $953 million. This transition adjustment was inclusive of qualitative adjustments incorporated into our CECL allowance as necessary, to address any limitations in the models used.

Stress Testing Requirements

The Dodd-Frank Act as enacted imposed stress testing requirements on banking organizations with total consolidated assets, averaged over the four most recent consecutive quarters, of more than $10 billion. The Bank completed its third annual stress test (using the scenarios provided by the FDIC) with the January 1, 2018 stress testing cycle. As a result of the passage of the Economic Growth, Regulatory Relief, and Consumer Protection Act, signed into law on May 24, 2018, the Bank became exempt from formally filing and publishing the results. However, under regulatory guidance, the Bank still conducts annual capital stress tests, the results of which it presents to its prudential regulators - the FDIC and the UDFI - for their review. The Bank also conducts quarterly liquidity stress tests to evaluate the adequacy of its liquidity sources under various stress scenarios and provides the results to its Board of Directors. These scenarios are submitted to the Bank’s prudential regulators at their request.

Deposit Insurance and Assessments

Deposits at the Bank are insured up to the applicable legal limits by the FDIC - administered Deposit Insurance Fund (the “DIF”), which is funded primarily by quarterly assessments on insured banks. An insured bank’s assessment is calculated by multiplying its assessment rate by its assessment base. A bank’s assessment base and assessment rate are determined each quarter.

The Bank’s insurance assessment base currently is its average consolidated total assets minus its average tangible equity during the assessment period. The Bank’s assessment rate is determined by the FDIC using a number of factors, including the results of supervisory evaluations, the Bank’s capital ratios and its financial condition, as well as the risk posed by the Bank to the DIF. Assessment rates for insured banks also are subject to adjustment depending on a number of factors, including significant holdings of brokered deposits in certain instances and the issuance or holding of certain types of debt.

Deposits

With respect to brokered deposits, an insured depository institution must be well capitalized under the prompt corrective action framework in order to accept, renew or roll over such deposits without FDIC clearance. An adequately capitalized insured depository institution must obtain a waiver from the FDIC to accept, renew or roll over brokered deposits. Undercapitalized insured depository institutions generally may not accept, renew or roll over brokered deposits. For more information on the Bank’s deposits, see Part II, Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations — Key Financial Measures — Funding Sources.”

Regulatory Examinations

The Bank currently undergoes regular on-site examinations by the Bank’s regulators, who examine for adherence to a range of legal and regulatory compliance responsibilities. A regulator conducting an examination has complete access to the books and records of the examined institution. The results of the examination are confidential. The cost of examinations may be assessed against the examined institution as the agency deems necessary or appropriate.

Source of Strength

Under the Dodd-Frank Act, we are required to serve as a source of financial strength to the Bank and to commit resources to support the Bank in circumstances when we might not do so absent the statutory requirement. Any loan by us to the Bank would be subordinate in right of payment to depositors and to certain other indebtedness of the Bank.

18

Community Reinvestment Act

The Community Reinvestment Act (the “CRA”) requires the FDIC to evaluate the record of the Bank in meeting the credit needs of its local community, including low- and moderate-income neighborhoods. These evaluations are considered in evaluating mergers, acquisitions and applications to open a branch or facility. Failure to adequately meet these criteria could result in additional requirements and limitations on the Bank. The Bank has received a CRA rating of Outstanding.

Privacy Laws

The federal banking regulators, as required by the Gramm-Leach-Bliley Act (“GLBA”), have adopted regulations that limit the ability of banks and other financial institutions to disclose nonpublic information about consumers to nonaffiliated third-parties. Financial institutions are required to disclose to consumers their policies for collecting and protecting confidential customer information. Customers generally may prevent financial institutions from sharing nonpublic personal financial information with nonaffiliated third-parties, with some exceptions, such as the processing of transactions requested by the consumer. Financial institutions generally may not disclose certain consumer or account information to any nonaffiliated third-party for use in telemarketing, direct mail marketing or other marketing. The privacy regulations also restrict information sharing among affiliates for marketing purposes and govern the use and provision of information to consumer reporting agencies. Federal and state banking agencies have prescribed standards for maintaining the security and confidentiality of consumer information, and the Bank is subject to such standards, as well as certain federal and state laws or standards for notifying consumers in the event of a security breach. In addition, we must comply with increasingly complex and rigorous data privacy and data security laws and regulatory standards enacted to protect business and personal data. These laws impose additional obligations on companies regarding the handling of personal data and provide certain individual privacy rights to persons whose data is stored. Any failure to comply with these laws and regulatory standards could subject us to legal and reputational risk. For example, California passed the California Consumer Privacy Act (the “CCPA”), which became effective on January 1, 2020, and applies to for-profit businesses that conduct business in California and meet certain revenue or data collection thresholds. The CCPA contains several exemptions, including an exemption applicable to information that is collected, processed, sold or disclosed pursuant to the GLBA. However, the definition of personal information is expanded under the CCPA to apply to certain data beyond the scope of the GLBA exemption. Misuse of or failure to secure certain personal information could result in violation of data privacy laws and regulations, proceedings against the Company by governmental entities or others, damage to our reputation and credibility and could negatively affect our business, financial condition, and results of operations. If other states in the U.S. adopt similar laws or if a comprehensive federal data privacy law is enacted, we may expend considerable additional resources to meet these requirements and the overall risk to the Company could incrementally increase depending upon the reach and application of any such laws.

State Regulation of Student Loan Servicers

In certain states, laws regulating the conduct of student loan servicers may apply to and impact the servicing practices of the Bank. While these state laws vary in content, they generally include components relating to licensure and oversight by state authorities and the creation of specialized student loan ombudsman offices to oversee the student loan industry operating within these states. These laws may also include requirements pertaining to payment processing, customer communications, the handling of customer inquiries and complaints, information concerning loan repayment options and access to borrower account records, among other requirements. Notably, these laws often include provisions for enforcement of alleged violations by state regulators as well as private litigation by aggrieved consumers.

Other Sources of Regulation

Many other aspects of our businesses are subject to federal and state regulation and administrative oversight. Some of the most significant of these are described below.

Oversight of Derivatives

Title VII of the Dodd-Frank Act requires all standardized derivatives, including most interest rate swaps, to be submitted for clearing to central intermediaries to reduce counterparty risk. Two of the central intermediaries we use are the Chicago Mercantile Exchange (the “CME”) and the London Clearing House (the “LCH”). All variation margin payments on derivatives cleared through the CME and LCH are required to be accounted for as legal settlement. As of December 31, 2020, $8.2 billion notional of our derivative contracts were cleared on the CME and $0.4 billion were cleared on the LCH. The derivative contracts cleared through the CME and the LCH represent 95.3 percent and 4.7 percent, respectively, of our total notional derivative contracts of $8.6 billion at December 31, 2020. Our exposure is limited to the value of the derivative contracts in a

19

gain position less any collateral held and plus any collateral posted. When there is a net negative exposure, we consider our exposure to the counterparty to be zero.

Credit Risk Retention