Exhibit 99.1

|

FOR IMMEDIATE RELEASE |

|

Friday July 22, 2011 |

|

(All amounts in U.S. dollars. |

|

|

|

Per share information based on diluted |

|

|

|

shares outstanding unless noted otherwise). |

|

|

CELESTICA ANNOUNCES SECOND QUARTER FINANCIAL RESULTS

Second Quarter 2011 Summary

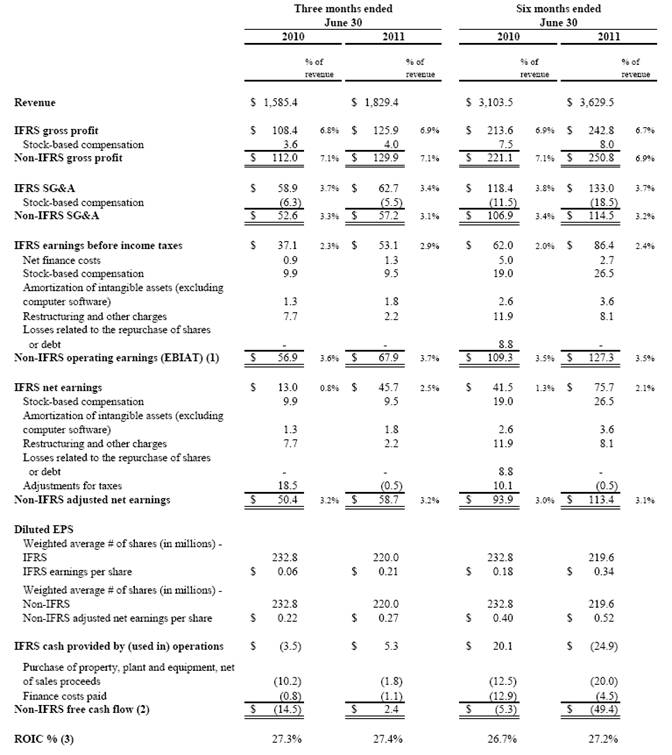

· Revenue of $1.83 billion, compared to $1.59 billion for the same period last year

· IFRS net earnings of $45.7 million, or $0.21 per share, compared to IFRS net earnings of $13.0 million, or $0.06 per share, last year

· Non-IFRS adjusted net earnings of $0.27 per share, compared to $0.22 per share last year

· Non-IFRS return on invested capital of 27.4%, compared to 27.3% last year

· Non-IFRS operating margin of 3.7%, compared to 3.6% last year

· Third quarter of 2011 guidance: revenue of $1.725 billion to $1.875 billion, adjusted net earnings per share of $0.23 to $0.29.

TORONTO, Canada - Celestica Inc. (NYSE, TSX: CLS), a global leader in the delivery of end-to-end product lifecycle solutions, today announced financial results for the second quarter ended June 30, 2011.

Second Quarter Results

Revenue for the quarter was $1.83 billion, compared to $1.59 billion in the second quarter of 2010. IFRS net earnings were $45.7 million, or $0.21 per share, compared to IFRS net earnings of $13.0 million, or $0.06 per share, for the same period last year. IFRS net earnings for the second quarter of 2011 included the following recurring items, which together resulted in a $0.06 per share (pre-tax) charge: stock-based compensation, amortization of intangible assets (excluding computer software) and restructuring charges. This aggregate (pre-tax) charge was within the range provided on April 21, 2011 of between $0.05 to $0.08 per share.

Adjusted net earnings for the quarter were $58.7 million, or $0.27 per share, compared to $50.4 million, or $0.22 per share, for the same period last year. The term adjusted net earnings is a non-IFRS measure defined as net earnings before stock-based compensation, amortization of intangible assets (excluding computer software), restructuring and other charges, and gains or losses related to the repurchase of shares or debt, net of tax adjustments. Detailed IFRS financial statements and supplementary information related to adjusted net earnings and other non-IFRS measures appear at the end of this press release.

For the six months ended June 30, 2011, revenue was $3.63 billion, compared to $3.10 billion for the same period in 2010. IFRS net earnings were $75.7 million, or $0.34 per share, compared to $41.5 million, or $0.18 per share, for the same period last year. Adjusted net earnings for the six months ended June 30, 2011 were $113.4 million, or $0.52 per share, compared to $93.9 million, or $0.40 per share, for the same period in 2010.

Second Quarter Results Compared to Guidance

The company’s revenue of $1.83 billion and adjusted net earnings of $0.27 per share for the second quarter of 2011 were within the company’s published guidance range, announced on April 21, 2011, of revenue of $1.75 billion to $1.90 billion and adjusted net earnings per share of $0.22 to $0.28.

more….

“Celestica had strong financial results in the second quarter as we delivered robust margin expansion and we achieved 15% year-over-year revenue growth,” said Craig Muhlhauser, President and Chief Executive Officer, Celestica. “New business awards from 2010 are contributing to our revenue growth and operating margins are benefiting from a favorable revenue mix and higher operating efficiencies from recently ramped programs.”

“We anticipate the current global economic environment will drive continued volatility in customer demand. Despite this environment, Celestica remains focused on providing industry-leading flexibility and operational performance to support our customers’ success and delivering on our 2011 revenue growth, operating margin and ROIC targets.”

End Markets by Quarter

The following table sets forth revenue by end market as a percentage of total revenue for the periods indicated:

|

|

|

2010 |

|

2011 |

| |||||||||||||||||

|

|

|

First |

|

Second |

|

Third |

|

Fourth |

|

Full |

|

First |

|

Second |

| |||||||

|

Consumer |

|

28 |

% |

26 |

% |

24 |

% |

24 |

% |

25 |

% |

26 |

% |

25 |

% | |||||||

|

Enterprise Communications |

|

22 |

% |

24 |

% |

25 |

% |

24 |

% |

24 |

% |

25 |

% |

25 |

% | |||||||

|

Telecommunications |

|

14 |

% |

13 |

% |

14 |

% |

12 |

% |

13 |

% |

11 |

% |

9 |

% | |||||||

|

Storage |

|

14 |

% |

12 |

% |

12 |

% |

12 |

% |

12 |

% |

12 |

% |

11 |

% | |||||||

|

Servers |

|

12 |

% |

14 |

% |

13 |

% |

17 |

% |

14 |

% |

15 |

% |

17 |

% | |||||||

|

Industrial, Aerospace and Defense, Healthcare and Green Technology |

|

10 |

% |

11 |

% |

12 |

% |

11 |

% |

12 |

% |

11 |

% |

13 |

% | |||||||

|

Revenue (in millions) |

|

$ |

1,518.1 |

|

$ |

1,585.4 |

|

$ |

1,546.5 |

|

$ |

1,876.1 |

|

$ |

6,526.1 |

|

$ |

1,800.1 |

|

$ |

1,829.4 |

|

Third Quarter of 2011 Outlook

For the third quarter ending September 30, 2011, the company anticipates revenue to be in the range of $1.725 billion to $1.875 billion, and adjusted net earnings per share to be in the range of $0.23 to $0.29. The company expects a negative $0.05 to $0.07 per share (pre-tax) aggregate impact on an IFRS basis for the following recurring items: stock-based compensation, amortization of intangible assets (excluding computer software) and restructuring charges.

Second Quarter Webcast

Management will host its second quarter results conference call today at 8:00 a.m. Eastern. The webcast can be accessed at www.celestica.com.

IFRS Reporting Commenced in 2011

Celestica has reported its financial results in accordance with International Financial Reporting Standards (IFRS), as required for public companies in Canada. The comparative financial information has been restated to reflect the adoption of IFRS, with effect from January 1, 2010. Periods prior to January 1, 2010 will not be presented under IFRS. The company has included a reconciliation between IFRS and the amounts previously reported under Canadian generally accepted accounting standards (GAAP) in the attached interim financial statements.

Although Celestica was required to transition to IFRS, its major North American competitors will continue to report financial results under U.S. GAAP. IFRS did not significantly impact the company’s non-IFRS financial metrics, which the company presents to enable investors to compare Celestica’s financial results with those of its major North American peer group.

Supplementary Information

In addition to disclosing detailed results in accordance with IFRS, Celestica provides supplementary non-IFRS measures to consider in evaluating the company’s operating performance. See Schedule 1.

Management uses adjusted net earnings and other non-IFRS measures to assess operating performance and the effective use and allocation of resources; to provide more meaningful period-to-period comparisons of operating results; to enhance investors’ understanding of the core operating results of Celestica’s business; and to set management incentive targets.

About Celestica

Celestica is dedicated to delivering end-to-end product lifecycle solutions to drive our customers’ success. Through our simplified global operations network and information technology platform, we are solid partners who deliver informed, flexible solutions that enable our customers to succeed in the markets they serve. Committed to providing a truly differentiated customer experience, our agile and adaptive employees share a proud history of demonstrated expertise and creativity that provides our customers with the ability to overcome any challenge.

For further information on Celestica, visit its website at http://www.celestica.com. The company’s security filings can also be accessed at http://www.sedar.com and http://www.sec.gov.

Safe Harbor and Fair Disclosure Statement

This news release contains forward-looking statements related to our future growth, trends in our industry, our financial or operational results including our quarterly earnings and revenue guidance, the impact of program wins or losses and acquisitions on our financial results and working capital requirements, anticipated expenses, capital expenditures, benefits or payments, our financial or operational performance, our expected tax outcomes, our cash flows and financial targets and the effect of the global economic environment on customer demand. Such forward-looking statements are predictive in nature and may be based on current expectations, forecasts or assumptions involving risks and uncertainties that could cause actual outcomes and results to differ materially from the forward-looking statements themselves. Such forward-looking statements may, without limitation, be preceded by, followed by, or include words such as “believes”, “expects”, “anticipates”, “estimates”, “intends”, “plans”, or similar expressions, or may employ such future or conditional verbs as “may”, “will”, “should” or “would”, or may otherwise be indicated as forward-looking statements by grammatical construction, phrasing or context. For those statements, we claim the protection of the safe harbor for forward-looking statements contained in the U.S. Private Securities Litigation Reform Act of 1995, and in any applicable Canadian securities legislation. Forward-looking statements are not guarantees of future performance. You should understand that the following important factors could affect our future results and could cause those results to differ materially from those expressed in such forward-looking statements: the effects of price competition and other business and competitive factors generally affecting the electronics manufacturing services (EMS) industry, including changes in the trend for outsourcing; our dependence on a limited number of customers and end markets; variability of operating results among periods; the challenges of effectively managing our operations and our working capital performance, including responding to significant changes in demand from our customers; the challenges of managing inflation, including rising energy and labor costs; our inability to retain or expand our business due to execution problems relating to the ramping of new programs, completing our restructuring activities or integrating our acquisitions; the delays in the delivery and/or general availability of various components and materials used in our manufacturing process; disruptions to our operations, or those of our customers, component suppliers, or our logistics partners, resulting from world or local events such as the recent natural disasters in Japan, political instability or labor and social unrest; our dependence on industries affected by rapid technological change; our ability to successfully manage our international operations; increasing income taxes and our ability to successfully defend tax audits or meet the conditions of tax incentives; the challenge of managing our financial exposures to foreign currency volatility; and the risk of potential non-performance by counterparties, including but not limited to financial institutions, customers and suppliers. These and other risks and uncertainties, as well as other information related to the company, are discussed in the Company’s various public filings at www.sedar.com and www.sec.gov, including our Annual Report on Form 20-F and subsequent reports on Form 6-K filed with the U.S. Securities and Exchange Commission and our Annual Information Form filed with the Canadian securities regulators. Forward-looking statements are provided for the purpose of providing information about management’s current expectations and plans relating to the future. Readers are cautioned that such information may not be appropriate for other purposes. Except as required by applicable law, we disclaim any intention or obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

Our revenue and earnings guidance, as contained in this press release, is based on various assumptions which management believes are reasonable under the current circumstances, but may prove to be inaccurate, and many of which involve factors that are beyond the control of the Company. The material assumptions may include the following: forecasts from our customers, which range from 30 to 90 days and can fluctuate significantly in terms of volume and mix of products or services; the timing, execution of, and investments associated with ramping new business; the success in the marketplace of our customers’ products, general economic and market conditions; currency exchange rates; pricing and competition; anticipated customer demand; supplier performance and pricing; commodity, labor, energy and transportation costs; operational and financial matters; and technological developments. These assumptions and estimates are based on management’s current views with respect to current plans and events, and are and will be subject to the risks and uncertainties referred to above. It is Celestica’s policy that revenue and earnings guidance is effective on the date given, and will only be updated through a public announcement.

|

Contacts: |

|

|

|

Laurie Flanagan |

|

Paul Carpino |

|

Celestica Communications |

|

Celestica Investor Relations |

|

(416) 448-2200 |

|

(416) 448-2211 |

|

media@celestica.com |

|

clsir@celestica.com |

Schedule 1

Supplementary Non-IFRS Measures

Our non-IFRS measures include gross profit, gross margin (gross profit as a percentage of revenue), selling, general and administrative expenses (SG&A), SG&A as a percentage of revenue, operating earnings (EBIAT), operating margin (EBIAT as a percentage of revenue), adjusted net earnings, adjusted net earnings per share, return on invested capital (ROIC), free cash flow, cash cycle days and inventory turns. In calculating these non-IFRS financial measures, management excludes the following items, as applicable: stock-based compensation, amortization of intangible assets (excluding computer software), restructuring and other charges (most significantly restructuring charges), the write-down of goodwill and long-lived assets, and gains or losses related to the repurchase of shares or debt, net of tax adjustments and significant deferred tax write-offs or recoveries.

These non-IFRS measures do not have any standardized meaning prescribed by IFRS and are not necessarily comparable to similar measures presented by other companies using IFRS, or our North American competitors who report under U.S. GAAP and use non-U.S. GAAP measures to describe similar operating metrics. Non-IFRS measures are not measures of performance under IFRS and should not be considered in isolation or as a substitute for any standardized measure under IFRS. The most significant limitation to management’s use of non-IFRS financial measures is that the charges and expenses excluded from the non-IFRS measures are nonetheless charges that are recognized under IFRS and that have an economic impact on the company. Management compensates for these limitations primarily by issuing IFRS results to show a complete picture of the company’s performance, and reconciling non-IFRS results back to IFRS, unless there are no comparable IFRS measures.

The economic substance of these exclusions and management’s rationale for excluding these from non-IFRS financial measures is provided below:

Stock-based compensation, which represents the estimated fair value of stock options and restricted stock units granted to employees, is excluded because grant activities vary significantly from quarter-to-quarter in both quantity and fair value. In addition, excluding this expense allows us to better compare core operating results with those of our competitors who also generally exclude stock-based compensation from their core operating results, who may have different granting patterns and types of equity awards, and who may use different option valuation assumptions than we do, including those competitors who use U.S. GAAP and non-U.S. GAAP measures to present similar metrics.

Amortization charges (excluding computer software) consist of non-cash charges against intangible assets that are impacted by the timing and magnitude of acquired businesses. Amortization of intangibles varies among competitors, and we believe that excluding these charges permits a better comparison of core operating results with those of our competitors who also generally exclude amortization charges.

Restructuring and other charges, which consist primarily of employee severance, lease termination and facility exit costs associated with closing and consolidating manufacturing facilities, reductions in infrastructure and acquisition-related transaction costs, are excluded because such charges are not directly related to ongoing operating results and do not reflect expected future operating expenses after completion of these activities. We believe that excluding these charges permits a better comparison of our core operating results with those of our competitors who also generally exclude these costs in assessing operating performance.

Impairment charges, which consist of non-cash charges against goodwill and long-lived assets, result primarily when the carrying value of these assets exceeds their fair value. These charges are excluded because they are generally non-recurring. In addition, our competitors may record impairment charges at different times and excluding these charges permits a better comparison of our core operating results with those of our competitors who also generally exclude these charges in assessing operating performance.

Gains or losses related to the repurchase of shares or debt are excluded as these gains or losses do not impact core operating performance and vary significantly among our competitors who also generally exclude these charges in assessing operating performance.

Significant deferred tax write-offs or recoveries are excluded as these write-offs or recoveries do not impact core operating performance and vary significantly among our competitors who also generally exclude these charges in assessing operating performance.

The following table sets forth, for the periods indicated, a reconciliation of IFRS to non-IFRS measures (in millions, except per share amounts):

(1) EBIAT is defined as earnings before interest, amortization and income taxes. EBIAT also excludes stock-based compensation, restructuring and other charges, gains or losses related to the repurchase of shares or debt, and impairment charges.

(2) Management uses free cash flow as a measure, in addition to cash flow from operations, to assess operational cash flow performance. We believe free cash flow provides another level of transparency to our liquidity as it represents cash generated from or used in operating activities after the purchase of capital equipment and property (net of proceeds from sale of certain surplus equipment and property) and finance costs paid.

(3) Management uses ROIC as a measure to assess the effectiveness of the invested capital it uses to build products or provide services to its customers. Our ROIC measure includes operating margin, working capital management and asset utilization. ROIC is calculated by dividing EBIAT by average net invested capital. Net invested capital consists of total assets less cash, accounts payable, accrued and other current liabilities and provisions, and income taxes payable. We use a two-point average to calculate average net invested capital for the quarter and a three-point average to calculate average net invested capital for the six-month period. There is no comparable measure under IFRS.

The following table sets forth, for the periods indicated, our calculation of ROIC % (in millions, except ROIC%):

GUIDANCE SUMMARY

|

|

|

Q2 11 Guidance |

|

Q2 11 Actual |

|

Q3 11 Guidance(4) |

|

|

Revenue |

|

$1.75B - $1.90B |

|

$1.83B |

|

$1.725B - $1.875B |

|

|

Adjusted net EPS |

|

$0.22 - $0.28 |

|

$0.27 |

|

$0.23 - $0.29 |

|

(4) We expect a negative $0.05 to $0.07 per share (pre-tax) aggregate impact on an IFRS basis for the following recurring items: stock-based compensation, amortization of intangible assets (excluding computer software) and restructuring charges.

CELESTICA INC.

CONSOLIDATED BALANCE SHEET

(in millions of U.S. dollars)

(unaudited)

|

|

|

January 1 |

|

December 31 |

|

June 30 |

| |||

|

|

|

2010 |

|

2010 |

|

2011 |

| |||

|

Assets |

|

|

|

|

|

|

| |||

|

Current assets: |

|

|

|

|

|

|

| |||

|

Cash and cash equivalents (note 11) |

|

$ |

937.7 |

|

$ |

632.8 |

|

$ |

552.6 |

|

|

Accounts receivable |

|

828.1 |

|

945.1 |

|

824.5 |

| |||

|

Inventories (note 6) |

|

676.1 |

|

845.7 |

|

1,010.8 |

| |||

|

Income taxes receivable |

|

21.2 |

|

15.6 |

|

15.6 |

| |||

|

Assets classified as held-for-sale |

|

22.8 |

|

35.5 |

|

33.9 |

| |||

|

Other current assets |

|

74.5 |

|

87.0 |

|

84.4 |

| |||

|

Total current assets |

|

2,560.4 |

|

2,561.7 |

|

2,521.8 |

| |||

|

|

|

|

|

|

|

|

| |||

|

Property, plant and equipment |

|

371.5 |

|

332.2 |

|

330.9 |

| |||

|

Goodwill |

|

— |

|

14.6 |

|

46.5 |

| |||

|

Intangible assets |

|

33.1 |

|

33.6 |

|

41.2 |

| |||

|

Deferred income taxes |

|

25.1 |

|

41.9 |

|

44.7 |

| |||

|

Other non-current assets |

|

31.7 |

|

29.9 |

|

35.5 |

| |||

|

Total assets |

|

$ |

3,021.8 |

|

$ |

3,013.9 |

|

$ |

3,020.6 |

|

|

|

|

|

|

|

|

|

| |||

|

Liabilities and Equity |

|

|

|

|

|

|

| |||

|

Current liabilities: |

|

|

|

|

|

|

| |||

|

Borrowings under credit facilities (note 7(a)) |

|

$ |

— |

|

$ |

— |

|

$ |

45.0 |

|

|

Accounts payable |

|

927.1 |

|

1,176.2 |

|

1,089.9 |

| |||

|

Accrued and other current liabilities |

|

261.1 |

|

279.1 |

|

235.2 |

| |||

|

Income taxes payable |

|

38.0 |

|

55.4 |

|

48.3 |

| |||

|

Current portion of provisions |

|

72.1 |

|

41.9 |

|

43.9 |

| |||

|

Current portion of long-term debt (note 7(b)) |

|

222.8 |

|

— |

|

— |

| |||

|

Total current liabilities |

|

1,521.1 |

|

1,552.6 |

|

1,462.3 |

| |||

|

|

|

|

|

|

|

|

| |||

|

Retirement benefit obligations |

|

116.0 |

|

129.3 |

|

126.3 |

| |||

|

Provisions and other non-current liabilities |

|

7.1 |

|

12.9 |

|

11.4 |

| |||

|

Deferred income taxes |

|

31.9 |

|

36.2 |

|

36.1 |

| |||

|

Total liabilities |

|

1,676.1 |

|

1,731.0 |

|

1,636.1 |

| |||

|

|

|

|

|

|

|

|

| |||

|

Equity: |

|

|

|

|

|

|

| |||

|

Capital stock (note 8) |

|

3,591.2 |

|

3,329.4 |

|

3,347.4 |

| |||

|

Treasury stock |

|

(0.4 |

) |

(15.9 |

) |

(9.1 |

) | |||

|

Contributed surplus |

|

222.7 |

|

360.9 |

|

362.5 |

| |||

|

Deficit |

|

(2,476.7 |

) |

(2,403.8 |

) |

(2,328.1 |

) | |||

|

Accumulated other comprehensive income |

|

8.9 |

|

12.3 |

|

11.8 |

| |||

|

Total equity |

|

1,345.7 |

|

1,282.9 |

|

1,384.5 |

| |||

|

Total liabilities and equity |

|

$ |

3,021.8 |

|

$ |

3,013.9 |

|

$ |

3,020.6 |

|

Contingencies (note 12).

The accompanying notes are an integral part of these unaudited interim consolidated financial statements.

CELESTICA INC.

CONSOLIDATED STATEMENT OF OPERATIONS

(in millions of U.S. dollars, except per share amounts)

(unaudited)

|

|

|

Three months ended |

|

Six months ended |

| ||||||||

|

|

|

2010 |

|

2011 |

|

2010 |

|

2011 |

| ||||

|

Revenue |

|

$ |

1,585.4 |

|

$ |

1,829.4 |

|

$ |

3,103.5 |

|

$ |

3,629.5 |

|

|

Cost of sales |

|

1,477.0 |

|

1,703.5 |

|

2,889.9 |

|

3,386.7 |

| ||||

|

Gross profit |

|

108.4 |

|

125.9 |

|

213.6 |

|

242.8 |

| ||||

|

Selling, general and administrative expenses (SG&A) |

|

58.9 |

|

62.7 |

|

118.4 |

|

133.0 |

| ||||

|

Research and development |

|

— |

|

3.0 |

|

— |

|

5.2 |

| ||||

|

Amortization of intangible assets |

|

3.8 |

|

3.6 |

|

7.5 |

|

7.4 |

| ||||

|

Other charges (note 9) |

|

7.7 |

|

2.2 |

|

20.7 |

|

8.1 |

| ||||

|

Earnings from operations |

|

38.0 |

|

54.4 |

|

67.0 |

|

89.1 |

| ||||

|

Finance costs, net |

|

0.9 |

|

1.3 |

|

5.0 |

|

2.7 |

| ||||

|

Earnings before income taxes |

|

37.1 |

|

53.1 |

|

62.0 |

|

86.4 |

| ||||

|

Income tax expense (recovery) (note 10): |

|

|

|

|

|

|

|

|

| ||||

|

Current |

|

19.9 |

|

8.4 |

|

23.0 |

|

13.2 |

| ||||

|

Deferred |

|

4.2 |

|

(1.0 |

) |

(2.5 |

) |

(2.5 |

) | ||||

|

|

|

24.1 |

|

7.4 |

|

20.5 |

|

10.7 |

| ||||

|

Net earnings for the period |

|

$ |

13.0 |

|

$ |

45.7 |

|

$ |

41.5 |

|

$ |

75.7 |

|

|

|

|

|

|

|

|

|

|

|

| ||||

|

Basic earnings per share |

|

$ |

0.06 |

|

$ |

0.21 |

|

$ |

0.18 |

|

$ |

0.35 |

|

|

|

|

|

|

|

|

|

|

|

| ||||

|

Diluted earnings per share |

|

$ |

0.06 |

|

$ |

0.21 |

|

$ |

0.18 |

|

$ |

0.34 |

|

|

|

|

|

|

|

|

|

|

|

| ||||

|

Shares used in computing per share amounts (in millions): |

|

|

|

|

|

|

|

|

| ||||

|

Basic |

|

230.3 |

|

216.6 |

|

230.1 |

|

216.0 |

| ||||

|

Diluted |

|

232.8 |

|

220.0 |

|

232.8 |

|

219.6 |

| ||||

The accompanying notes are an integral part of these unaudited interim consolidated financial statements.

CELESTICA INC.

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME

(in millions of U.S. dollars)

(unaudited)

|

|

|

Three months ended |

|

Six months ended |

| ||||||||

|

|

|

2010 |

|

2011 |

|

2010 |

|

2011 |

| ||||

|

Net earnings for the period |

|

$ |

13.0 |

|

$ |

45.7 |

|

$ |

41.5 |

|

$ |

75.7 |

|

|

Other comprehensive income (loss), net of tax: |

|

|

|

|

|

|

|

|

| ||||

|

Currency translation differences for foreign operations |

|

(1.3 |

) |

1.9 |

|

(3.3 |

) |

5.2 |

| ||||

|

Change from derivatives designated as hedges |

|

(9.7 |

) |

(5.5 |

) |

(5.9 |

) |

(5.7 |

) | ||||

|

Total comprehensive income for the period |

|

$ |

2.0 |

|

$ |

42.1 |

|

$ |

32.3 |

|

$ |

75.2 |

|

The accompanying notes are an integral part of these unaudited interim consolidated financial statements.

CELESTICA INC.

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY

(in millions of U.S. dollars)

(unaudited)

|

|

|

Capital stock |

|

Treasury |

|

Contributed |

|

Deficit |

|

Accumulated |

| |||||

|

Balance — January 1, 2010 |

|

$ |

3,591.2 |

|

$ |

(0.4 |

) |

$ |

222.7 |

|

$ |

(2,476.7 |

) |

$ |

8.9 |

|

|

Issuance of capital stock |

|

5.8 |

|

— |

|

— |

|

— |

|

— |

| |||||

|

Purchase of treasury stock |

|

— |

|

(15.1 |

) |

— |

|

— |

|

— |

| |||||

|

Stock-based compensation |

|

— |

|

2.4 |

|

11.6 |

|

— |

|

— |

| |||||

|

Other |

|

— |

|

— |

|

(0.1 |

) |

— |

|

— |

| |||||

|

Net earnings for the period |

|

— |

|

— |

|

— |

|

41.5 |

|

— |

| |||||

|

Currency translation differences for foreign operations |

|

— |

|

— |

|

— |

|

— |

|

(3.3 |

) | |||||

|

Change from derivatives designated as hedges |

|

— |

|

— |

|

— |

|

— |

|

(5.9 |

) | |||||

|

Balance — June 30, 2010 |

|

$ |

3,597.0 |

|

$ |

(13.1 |

) |

$ |

234.2 |

|

$ |

(2,435.2 |

) |

$ |

(0.3 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

|

Balance — January 1, 2011 |

|

$ |

3,329.4 |

|

$ |

(15.9 |

) |

$ |

360.9 |

|

$ |

(2,403.8 |

) |

$ |

12.3 |

|

|

Issuance of capital stock |

|

18.0 |

|

— |

|

(6.5 |

) |

— |

|

— |

| |||||

|

Purchase of treasury stock |

|

— |

|

(9.3 |

) |

— |

|

— |

|

— |

| |||||

|

Stock-based compensation |

|

— |

|

16.1 |

|

7.5 |

|

— |

|

— |

| |||||

|

Other |

|

— |

|

— |

|

0.6 |

|

— |

|

— |

| |||||

|

Net earnings for the period |

|

— |

|

— |

|

— |

|

75.7 |

|

— |

| |||||

|

Currency translation differences for foreign operations |

|

— |

|

— |

|

— |

|

— |

|

5.2 |

| |||||

|

Change from derivatives designated as hedges |

|

— |

|

— |

|

— |

|

— |

|

(5.7 |

) | |||||

|

Balance — June 30, 2011 |

|

$ |

3,347.4 |

|

$ |

(9.1 |

) |

$ |

362.5 |

|

$ |

(2,328.1 |

) |

$ |

11.8 |

|

(a) Accumulated other comprehensive income (loss) is net of tax.

The accompanying notes are an integral part of these unaudited interim consolidated financial statements.

CELESTICA INC.

CONSOLIDATED STATEMENT OF CASH FLOWS

(in millions of U.S. dollars)

(unaudited)

|

|

|

Three months ended |

|

Six months ended |

| ||||||||

|

|

|

2010 |

|

2011 |

|

2010 |

|

2011 |

| ||||

|

Cash provided by (used in): |

|

|

|

|

|

|

|

|

| ||||

|

|

|

|

|

|

|

|

|

|

| ||||

|

Operating activities: |

|

|

|

|

|

|

|

|

| ||||

|

Net earnings for the period |

|

$ |

13.0 |

|

$ |

45.7 |

|

$ |

41.5 |

|

$ |

75.7 |

|

|

Adjustments for items not affecting cash: |

|

|

|

|

|

|

|

|

| ||||

|

Depreciation and amortization |

|

22.6 |

|

19.7 |

|

44.8 |

|

38.8 |

| ||||

|

Equity-settled stock-based compensation |

|

9.9 |

|

9.5 |

|

15.7 |

|

23.5 |

| ||||

|

Other charges (recovery) |

|

0.5 |

|

(3.6 |

) |

8.0 |

|

(3.7 |

) | ||||

|

Finance costs, net |

|

0.9 |

|

1.3 |

|

5.0 |

|

2.7 |

| ||||

|

Income tax expense |

|

24.1 |

|

7.4 |

|

20.5 |

|

10.7 |

| ||||

|

Other |

|

(5.1 |

) |

(6.5 |

) |

(7.6 |

) |

(4.9 |

) | ||||

|

Changes in non-cash working capital items: |

|

|

|

|

|

|

|

|

| ||||

|

Accounts receivable |

|

10.7 |

|

29.5 |

|

39.6 |

|

133.0 |

| ||||

|

Inventories |

|

47.5 |

|

8.1 |

|

(0.2 |

) |

(127.5 |

) | ||||

|

Other current assets |

|

(5.2 |

) |

(10.6 |

) |

1.5 |

|

(3.4 |

) | ||||

|

Accounts payable, accrued and other current liabilities and provisions |

|

(117.9 |

) |

(79.1 |

) |

(143.2 |

) |

(149.0 |

) | ||||

|

Non-cash working capital changes |

|

(64.9 |

) |

(52.1 |

) |

(102.3 |

) |

(146.9 |

) | ||||

|

Net income taxes paid |

|

(4.5 |

) |

(16.1 |

) |

(5.5 |

) |

(20.8 |

) | ||||

|

Net cash provided by (used in) operating activities |

|

(3.5 |

) |

5.3 |

|

20.1 |

|

(24.9 |

) | ||||

|

|

|

|

|

|

|

|

|

|

| ||||

|

Investing activities: |

|

|

|

|

|

|

|

|

| ||||

|

Acquisitions, net of cash acquired (note 4) |

|

— |

|

(78.0 |

) |

(5.0 |

) |

(78.0 |

) | ||||

|

Purchase of computer software and property, plant and equipment |

|

(11.9 |

) |

(9.9 |

) |

(19.5 |

) |

(28.5 |

) | ||||

|

Proceeds from sale of assets |

|

1.7 |

|

8.1 |

|

7.0 |

|

8.5 |

| ||||

|

Other |

|

0.5 |

|

— |

|

0.2 |

|

— |

| ||||

|

Net cash used in investing activities |

|

(9.7 |

) |

(79.8 |

) |

(17.3 |

) |

(98.0 |

) | ||||

|

|

|

|

|

|

|

|

|

|

| ||||

|

Financing activities: |

|

|

|

|

|

|

|

|

| ||||

|

Net borrowings under credit facilities (note 7(a)) |

|

— |

|

45.0 |

|

— |

|

45.0 |

| ||||

|

Repurchase of Senior Subordinated Notes (Notes) (note 7(b)) |

|

— |

|

— |

|

(231.6 |

) |

— |

| ||||

|

Issuance of capital stock (note 8) |

|

0.5 |

|

0.8 |

|

4.0 |

|

11.5 |

| ||||

|

Purchase of treasury stock (note 8) |

|

(14.1 |

) |

(1.6 |

) |

(15.1 |

) |

(9.3 |

) | ||||

|

Finance costs paid |

|

(0.8 |

) |

(1.1 |

) |

(12.9 |

) |

(4.5 |

) | ||||

|

Other |

|

(0.7 |

) |

— |

|

(1.0 |

) |

— |

| ||||

|

Net cash provided by (used in) financing activities |

|

(15.1 |

) |

43.1 |

|

(256.6 |

) |

42.7 |

| ||||

|

|

|

|

|

|

|

|

|

|

| ||||

|

Net decrease in cash and cash equivalents |

|

(28.3 |

) |

(31.4 |

) |

(253.8 |

) |

(80.2 |

) | ||||

|

Cash and cash equivalents, beginning of period |

|

712.2 |

|

584.0 |

|

937.7 |

|

632.8 |

| ||||

|

Cash and cash equivalents, end of period |

|

$ |

683.9 |

|

$ |

552.6 |

|

$ |

683.9 |

|

$ |

552.6 |

|

The accompanying notes are an integral part of these unaudited interim consolidated financial statements.

CELESTICA INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(in millions of U.S. dollars, except per share amounts)

(unaudited)

1. REPORTING ENTITY

Celestica Inc. (Celestica) is incorporated in Canada with its corporate headquarters located at 844 Don Mills Road, Toronto, Ontario, M3C 1V7. Celestica is a publicly listed company on the Toronto Stock Exchange (TSX) and the New York Stock Exchange (NYSE).

Celestica provides end-to-end product lifecycle solutions on a global basis to original equipment manufacturers (OEMs) and service providers in the consumer, communications, enterprise computing, industrial, aerospace and defense, healthcare and green technology markets. Our product lifecycle solutions include a full range of services to our customers including design, manufacturing, engineering, complex mechanical and systems integration, order fulfillment, logistics and after-market services.

2. BASIS OF PREPARATION AND SIGNIFICANT ACCOUNTING POLICIES

Statement of compliance:

These unaudited interim consolidated financial statements have been prepared in accordance with International Accounting Standard (IAS) 34, Interim Financial Reporting as issued by the International Accounting Standards Board (IASB) and accounting policies we adopted in accordance with International Financial Reporting Standards (IFRS).

Our unaudited interim consolidated financial statements are prepared in accordance with IFRS and its interpretations adopted by the IASB, including IFRS 1, First-time Adoption of International Financial Reporting Standards. We have elected January 1, 2010 as the date of transition to IFRS (Transition Date). Previously, we prepared our consolidated financial statements in accordance with generally accepted accounting principles in Canada (GAAP). GAAP differs in some policies from IFRS. In accordance with the transition rules, we have retroactively applied IFRS to our comparative data for 2010.

These unaudited interim consolidated financial statements should be read in conjunction with our 2010 annual consolidated financial statements prepared in accordance with GAAP and with our IFRS accounting policies, transition disclosures and selected annual disclosures in notes 2, 3 and 12, respectively, of our unaudited interim consolidated financial statements for the three months ended March 31, 2011.

In note 3, we have presented reconciliations and descriptions of the effect of our transition from GAAP to IFRS on our equity, net earnings (loss) and comprehensive income (loss) for the 2010 comparative periods.

The unaudited interim consolidated financial statements were authorized for issuance by the Board of Directors on July 21, 2011.

Functional and presentation currency:

These unaudited interim consolidated financial statements are presented in U.S. dollars, which is also our functional currency. All financial information presented in U.S. dollars (except per share amounts) has been rounded to the nearest million.

Use of estimates and judgments:

The preparation of financial statements in conformity with IFRS requires management to make judgments, estimates and assumptions that affect the application of accounting policies and the reported amounts of assets and liabilities, revenue and expenses and the related disclosures of contingent assets and liabilities. Actual results could differ

CELESTICA INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(in millions of U.S. dollars, except per share amounts)

(unaudited)

materially from these estimates and assumptions. We review our estimates and underlying assumptions on an ongoing basis. Revisions are recognized in the period in which the estimates are revised and may impact future periods as well.

We have applied significant estimates and assumptions to our valuations against inventory and income taxes, to the amount and timing of restructuring charges or recoveries, to the measurement of the recoverable amount of our cash generating units (CGU), and to valuing our financial instruments, pension costs, stock-based payments, provisions and contingencies. These unaudited interim consolidated financial statements are based upon accounting policies and estimates consistent with those used and described in note 2 of our unaudited interim consolidated financial statements for the three months ended March 31, 2011.

3. TRANSITION TO IFRS

We adopted IFRS on January 1, 2011. We have applied IFRS retroactively to our comparative data as of January 1, 2010, the Transition Date.

RECONCILIATION OF GAAP TO IFRS:

The following tables set forth, for the periods indicated, a reconciliation from GAAP to IFRS, of our equity, net earnings (loss) and comprehensive income (loss):

|

|

|

|

|

January 1 |

|

June 30 |

|

December 31 |

| |||

|

Reconciliation of equity: |

|

Notes |

|

2010 |

|

2010 |

|

2010 |

| |||

|

|

|

|

|

|

|

|

|

|

| |||

|

Equity in accordance with GAAP |

|

|

|

$ |

1,475.8 |

|

$ |

1,491.7 |

|

$ |

1,421.3 |

|

|

Employee benefits |

|

a |

|

(130.4 |

) |

(125.4 |

) |

(152.4 |

) | |||

|

Restructuring provision |

|

b |

|

(1.3 |

) |

14.2 |

|

9.8 |

| |||

|

Income taxes |

|

c |

|

1.6 |

|

2.3 |

|

5.6 |

| |||

|

Business combinations |

|

d |

|

— |

|

(0.4 |

) |

(1.0 |

) | |||

|

Other |

|

|

|

— |

|

0.2 |

|

(0.4 |

) | |||

|

Equity in accordance with IFRS |

|

|

|

$ |

1,345.7 |

|

$ |

1,382.6 |

|

$ |

1,282.9 |

|

|

|

|

|

|

Three months |

|

Six months |

|

Year ended |

| |||

|

Reconciliation of net earnings (loss): |

|

Notes |

|

2010 |

|

2010 |

|

2010 |

| |||

|

|

|

|

|

|

|

|

|

|

| |||

|

Net earnings (loss) in accordance with GAAP |

|

|

|

$ |

(6.1 |

) |

$ |

19.8 |

|

$ |

80.8 |

|

|

Employee benefits (includes related foreign exchange) |

|

a |

|

2.8 |

|

5.0 |

|

6.7 |

| |||

|

Restructuring provision |

|

b |

|

15.4 |

|

15.5 |

|

11.1 |

| |||

|

Income taxes |

|

c |

|

(0.1 |

) |

0.7 |

|

3.6 |

| |||

|

Business combinations |

|

d |

|

— |

|

(0.4 |

) |

(1.0 |

) | |||

|

Stock-based compensation |

|

f |

|

0.8 |

|

0.7 |

|

0.4 |

| |||

|

Other |

|

|

|

0.2 |

|

0.2 |

|

(0.4 |

) | |||

|

IFRS adjustments to net earnings (loss) |

|

|

|

19.1 |

|

21.7 |

|

20.4 |

| |||

|

Net earnings in accordance with IFRS |

|

|

|

$ |

13.0 |

|

$ |

41.5 |

|

$ |

101.2 |

|

CELESTICA INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(in millions of U.S. dollars, except per share amounts)

(unaudited)

|

|

|

|

|

Three months |

|

Six months |

|

Year ended |

| |||

|

Reconciliation of comprehensive income (loss): |

|

Notes |

|

2010 |

|

2010 |

|

2010 |

| |||

|

|

|

|

|

|

|

|

|

|

| |||

|

Comprehensive income (loss) in accordance with GAAP |

|

|

|

$ |

(17.1 |

) |

$ |

10.6 |

|

$ |

84.2 |

|

|

IFRS adjustments to net earnings (loss) as above |

|

|

|

19.1 |

|

21.7 |

|

20.4 |

| |||

|

Actuarial losses on pension plans, net of tax |

|

a |

|

— |

|

— |

|

(28.3 |

) | |||

|

Comprehensive income in accordance with IFRS |

|

|

|

$ |

2.0 |

|

$ |

32.3 |

|

$ |

76.3 |

|

Transitional adjustments:

(a) Employee benefits and actuarial losses on pension plans:

In accordance with GAAP, actuarial gains and losses arising from defined benefit and post-retirement benefit plans were deferred and amortized to operations over time using the corridor approach. Under IFRS, we elected to recognize all cumulative actuarial gains or losses deferred under GAAP through deficit at the Transition Date. At December 31, 2009, we had $140.3 of unrecognized actuarial losses under GAAP. Under GAAP, prior service costs or credits were deferred and amortized to operations over the remaining service period or life expectancy. Under IFRS, we recognized vested prior service credits deferred under GAAP through deficit at the Transition Date. At December 31, 2009, we had $9.9 of unrecognized vested prior service credits under GAAP.

At December 31, 2009, the balance of our pension asset and pension obligations under GAAP were $104.4 and $75.4, respectively. Compared to GAAP, the IFRS pension-related transitional adjustments had the following effect on the consolidated balance sheet:

|

|

|

January 1 |

|

June 30 |

|

December 31 |

| |||

|

|

|

2010 |

|

2010 |

|

2010 |

| |||

|

Decrease in pension asset (included in other non-current assets) |

|

$ |

89.8 |

|

$ |

92.7 |

|

$ |

104.3 |

|

|

Increase in retirement benefit obligations |

|

40.6 |

|

32.7 |

|

48.1 |

| |||

|

|

|

$ |

130.4 |

|

$ |

125.4 |

|

$ |

152.4 |

|

Employee benefit expense for the three and six months ended June 30, 2010 and the year ended December 31, 2010 was lower under IFRS compared to GAAP by $2.8, $5.0 and $6.7 (including the impact of related foreign exchange), respectively, as the employee benefit expense under IFRS excludes the impact of the above actuarial losses and vested prior service credits that we recorded directly through deficit on the Transition Date. Under IFRS, we elected to recognize actuarial gains and losses incurred after the Transition Date of $28.3 ($28.7 less $0.4 of taxes) through OCI and deficit for the year ended December 31, 2010.

(b) Restructuring provision:

In accordance with GAAP, we discounted significant restructuring provisions using the discount rate at the time of initial measurement and we recorded no adjustments to reflect subsequent changes in discount rates. Under IFRS, we remeasure our provisions each reporting period using the current period pre-tax discount rates. On the Transition Date, we increased the restructuring provision liability by $1.3 to reflect the impact of then current discount rates. For the three and six months ended June 30, 2010 and the year ended December 31, 2010, IFRS net earnings were higher than GAAP net earnings by $0.2, $0.3 and $0.4, respectively, to reflect changes in discount rates during the period. In addition, IFRS defers the recognition of restructuring charges until the plans are implemented or announced to employees. Under GAAP, our restructuring charges included $15.2 and $10.7 for actions not yet announced at June 30, 2010 and December 31, 2010, respectively, which we reversed under IFRS. The majority of the June 30, 2010 restructuring charges were announced and recognized in the second half of 2010 and the majority

CELESTICA INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(in millions of U.S. dollars, except per share amounts)

(unaudited)

of the December 31, 2010 charges were announced and recognized during the first half of 2011. There were no restructuring adjustments related to unannounced actions at the Transition Date. Our restructuring provision at January 1, 2010 was $45.3 (December 31, 2010 — $20.0) under IFRS.

(c) Income taxes:

Under IFRS, we recognized net deferred income tax assets for temporary differences arising from inter-company transfers of property and equipment and to reflect the tax effect of revaluing foreign currency denominated non-monetary balances, which were not required under GAAP. We also recorded the deferred income tax effects of the other IFRS adjustments.

(d) Business combinations:

Under IFRS, acquisition-related transaction costs are expensed as incurred. As a result of transaction costs associated with our two acquisitions in 2010, IFRS net earnings for the three and six months ended June 30, 2010 and the year ended December 31, 2010 were lower than GAAP net earnings by nil, $0.4 and $1.0, respectively. Under GAAP, these costs were capitalized as part of the purchase price allocation. IFRS also requires that obligations for contingent consideration be recorded at fair value at the acquisition date. Under GAAP, contingent consideration is only recorded when the amounts are reasonably estimable and the outcome is certain. For one acquisition in 2010, we recorded additional goodwill of $4.5 under IFRS, with a corresponding increase to other non-current provisions on the acquisition date. Subsequent changes in the fair value of the contingent consideration from the date of acquisition to the settlement date are generally recorded in the consolidated statement of operations. At December 31, 2010, the fair value of the contingent consideration increased to $4.6 due to changes in foreign exchange rates.

(e) Cumulative currency translation adjustment:

Under IFRS, we elected to clear our cumulative currency translation balance to zero through equity on the Transition Date. We eliminated $46.9 of cumulative currency translation gains from OCI and reduced our deficit upon transition to IFRS. Total equity was not affected.

Other adjustments and reclassifications:

(f) Stock-based compensation:

Under GAAP, each grant was treated as a single arrangement and compensation expense was determined at the time of grant and amortized over the vesting period, generally three to four years, on a straight-line basis. IFRS requires a separate calculation of compensation expense for awards that vest in installments. Under IFRS, compensation expense differs from GAAP based on the changing fair values used for each installment and the timing of recognizing compensation expense. Generally this results in accelerated expense recognition under IFRS. On the Transition Date, we recognized additional compensation expense of $11.7 which increased our deficit with a corresponding offset to contributed surplus. Total equity was not affected. Under IFRS as compared to GAAP, stock-based compensation expense for the three and six months ended June 30, 2010 and year ended December 31, 2010 decreased by $0.8, $0.7 and $0.4, respectively.

(g) Assets held-for-sale:

Under IFRS, we classified assets held-for-sale separately on the consolidated balance sheet. Under GAAP, assets held-for-sale were included with property, plant and equipment and long-term assets on the consolidated balance sheet. On the Transition Date, we reclassified assets held-for-sale of $22.8 to a separate line item. Total equity was not affected by this reclassification. At December 31, 2010, we had $35.5 in assets held-for-sale.

CELESTICA INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(in millions of U.S. dollars, except per share amounts)

(unaudited)

Cash flow:

The adoption of IFRS did not significantly impact our cash flows compared to GAAP. Under IFRS, we reclassified $0.8 and $12.9 of finance costs paid from operating activities to financing activities for the three and six months ended June 30, 2010, respectively ($15.0 — year ended December 31, 2010). These costs were primarily for interest paid on our Notes prior to redemption in March 2010. There were no changes to overall net cash flows.

4. ACQUISITIONS

In June 2011, we acquired the semiconductor equipment contract manufacturing operations of Brooks Automation, Inc. (Brooks). We acquired certain assets located in Portland, Oregon and the shares of China-based Brooks Automation Limited. The operations specialize in manufacturing complex mechanical equipment and providing systems integration services to some of the world’s largest semiconductor equipment manufacturers.

The purchase price was $78.0, net of cash acquired, which we financed from cash on hand and $45.0 from our revolving credit facility. Details of the preliminary purchase price allocation, using estimated fair values, are as follows:

|

Current assets, net of cash acquired |

|

$ |

50.2 |

|

|

Capital and other long-term assets |

|

1.5 |

| |

|

Customer intangible assets |

|

12.5 |

| |

|

Goodwill |

|

30.9 |

| |

|

Current liabilities |

|

(17.1 |

) | |

|

|

|

$ |

78.0 |

|

The fair values for certain assets, such as our customer intangible assets, are preliminary as we are in the process of obtaining third-party valuations. Our purchase price allocation is subject to adjustment in the period we obtain these valuations. Through this acquisition, we have an established entry into the semiconductor capital equipment market, added capabilities to and diversified our industrial service offering, and acquired an experienced design and engineering workforce we can leverage with our existing customers. We expect that approximately one-third of the goodwill will be tax deductible. The purchase price is subject to a working capital adjustment that, when determined, will be reflected as an adjustment to goodwill. We expensed $0.5 in acquisition-related transaction costs during the quarter through other charges. This acquisition did not have a significant impact on our consolidated results of operations for the quarter ended June 30, 2011.

Pro forma disclosure: Revenue and earnings for the combined companies for the current reporting period would not have been materially different had the acquisition occurred at the beginning of the year.

In January 2010, we acquired Scotland-based Invec Solutions Limited (Invec) for a cash purchase price of $5.0.

CELESTICA INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(in millions of U.S. dollars, except per share amounts)

(unaudited)

5. SEGMENT AND CUSTOMER REPORTING

End markets:

The following table indicates revenue by end market as a percentage of total revenue. Our revenue fluctuates from period-to-period depending on numerous factors, including but not limited to: seasonality of business, the mix and complexity of the products or services we provide, the level of business and program wins or losses from new, existing and disengaging customers, the phasing in or out of programs, and changes in customer demand. We expect that the pace of technological change, the frequency of OEMs transferring business among EMS competitors and the constantly changing dynamics of the global economy will also continue to impact our business from period-to-period.

|

|

|

Three months ended |

|

Six months ended |

| ||||

|

|

|

2010 |

|

2011 |

|

2010 |

|

2011 |

|

|

Consumer |

|

26 |

% |

25 |

% |

27 |

% |

25 |

% |

|

Enterprise Communications |

|

24 |

% |

25 |

% |

23 |

% |

25 |

% |

|

Servers |

|

14 |

% |

17 |

% |

13 |

% |

16 |

% |

|

Storage |

|

12 |

% |

11 |

% |

13 |

% |

12 |

% |

|

Telecommunications |

|

13 |

% |

9 |

% |

13 |

% |

10 |

% |

|

Industrial, Aerospace and Defense, Healthcare and Green Technology |

|

11 |

% |

13 |

% |

11 |

% |

12 |

% |

Customers:

For both the second quarter and first half of 2011, three customers represented more than 10% of total revenue (second quarter and first half of 2010 — two customers and one customer, respectively). Our largest customer, Research In Motion, accounted for 19% of total revenue for the second quarter of 2011 (year ended December 31, 2010 — 20%).

6. INVENTORIES

During the second quarter and first half of 2011, we recorded a net inventory provision through cost of sales of $2.0 and $5.7, respectively, to reflect changes in the value of our inventory to net realizable value. During the second quarter and first half of 2010, we recorded a net inventory valuation reversal through cost of sales of $3.0 and $5.2, respectively, primarily to reflect realized gains on the disposition of inventory previously written down.

7. CREDIT FACILITIES AND LONG-TERM DEBT

(a) Credit facilities:

In January 2011, we renewed our revolving credit facility on generally similar terms and conditions, and increased the size of the facility from $200.0 to $400.0 with a maturity of January 2015. We are required to comply with certain restrictive covenants including those relating to debt incurrence, the sale of assets, a change of control and certain financial covenants related to indebtedness, interest coverage and liquidity. We pledged certain assets, including the shares of certain North American subsidiaries, as security for borrowings under this facility.

Borrowings under this facility bear interest at LIBOR plus a margin. At June 30, 2011, $45.0 of borrowings were outstanding under this facility bearing interest at 2.2%. Each draw under the facility bears interest based on LIBOR plus a margin for the term of the draw (which is generally less than 90 days). We were in compliance with all covenants at June 30, 2011. Commitment fees for the first half of 2011 were $1.0.

CELESTICA INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(in millions of U.S. dollars, except per share amounts)

(unaudited)

We also have uncommitted bank overdraft facilities available for intraday and overnight operating requirements which total $70.0 at June 30, 2011. There were no borrowings outstanding under these overdraft facilities at June 30, 2011.

During any period, we may borrow and repay amounts under these facilities. The amounts we borrow and repay can vary significantly from month-to-month depending upon our working capital and other cash requirements.

(b) Senior Subordinated Notes:

In March 2010, we paid $231.6 to repurchase the remaining outstanding Notes and recognized a loss of $8.8 in other charges. We redeemed all of our outstanding Notes prior to March 31, 2010. There were no Notes outstanding at June 30, 2011.

8. CAPITAL STOCK

In July 2010, we filed a Normal Course Issuer Bid (NCIB) with the TSX to repurchase, at our discretion, until August 2, 2011 up to 18.0 million subordinate voting shares on the open market or as otherwise permitted, subject to normal terms and limitations of such bids. The total number of subordinate voting shares we may repurchase for cancellation under the NCIB is reduced by the number of subordinate voting shares purchased for our employee equity-based incentive programs (totaling 1.9 million from the NCIB’s commencement). During the first half of 2011, we did not repurchase any subordinate voting shares for cancellation under the NCIB. As of June 30, 2011, we had repurchased and cancelled a total of 16.1 million subordinate voting shares at a weighted average price of $8.75 per share under the NCIB since its commencement. At June 30, 2011, we have completed all repurchases under the NCIB.

From time-to-time, we pay cash for the purchase of subordinate voting shares in the open market by a trustee to satisfy the delivery of subordinate voting shares to employees upon vesting of share unit awards under our long-term incentive plans. During the second quarter and first half of 2011, we paid $1.6 and $9.3, respectively, for the trustee to purchase 0.1 million and 0.8 million subordinate voting shares, respectively, in the open market. At June 30, 2011, the trustee held 0.8 million subordinate voting shares, with an ascribed value of $9.1, for delivery under these plans. We classify these shares for accounting purposes as treasury stock until they are delivered to employees pursuant to the awards. At June 30, 2010, the trustee held 1.4 million subordinate voting shares with an ascribed value of $13.1.

We elected to cash-settle certain awards vesting in the first quarters of 2010 and 2011 due to limitations in the number of subordinate voting shares we could purchase in the open market as a result of terms in our Notes and our share buy-back program. Cash-settled awards are accounted for as liabilities and remeasured based on our share price at each reporting date until the settlement date, with a corresponding charge to compensation expense. We recorded additional compensation expense to reflect the mark-to-market adjustment on these cash-settled awards of $2.7 in the first quarter of 2011 (first quarter of 2010 — $2.2).

CELESTICA INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(in millions of U.S. dollars, except per share amounts)

(unaudited)

The following table outlines the activity for stock-based awards for the first half of 2011:

|

Number of awards (in millions) |

|

Options |

|

RSUs |

|

PSUs (i) |

| |||

|

|

|

|

|

|

|

|

| |||

|

Outstanding at December 31, 2010 |

|

10.5 |

|

4.8 |

|

7.7 |

| |||

|

Granted (i) |

|

0.9 |

|

2.1 |

|

2.1 |

| |||

|

Exercised (ii) |

|

(1.9 |

) |

(2.0 |

) |

(1.8 |

) | |||

|

Forfeited/expired |

|

(0.5 |

) |

(0.2 |

) |

(0.4 |

) | |||

|

Outstanding at June 30, 2011 |

|

9.0 |

|

4.7 |

|

7.6 |

| |||

|

|

|

|

|

|

|

|

| |||

|

The weighted-average grant date fair value of options and share units awarded: |

|

$ |

4.86 |

|

$ |

9.98 |

|

$ |

13.75 |

|

(i) During the first quarter of 2011, we granted 2.1 million PSUs that vest based on the achievement of a market performance condition based on Total Shareholder Return (TSR). See note 2(m) of our March 31, 2011 unaudited interim consolidated financial statements for a description of TSR. We estimated the grant date fair value of these PSUs using a Monte Carlo simulation model. We expect to settle these awards with subordinate voting shares purchased in the open market.

(ii) During the first half of 2011, we received cash proceeds of $11.5 relating to the exercise of stock options.

Total stock-based compensation expense, including the mark-to-market and plan adjustments, was $9.5 and $26.5, respectively, for the second quarter and first half of 2011 (second quarter and first half of 2010 — $9.9 and $19.0, respectively). During the first quarter of 2011, we amended the retirement eligibility clauses in our long-term incentive plans which accelerated our recognition of the related compensation expense of $4.8.

9. OTHER CHARGES

|

|

|

Three months ended |

|

Six months ended |

| ||||||||

|

|

|

2010 |

|

2011 |

|

2010 |

|

2011 |

| ||||

|

|

|

|

|

|

|

|

|

|

| ||||

|

Restructuring (a) |

|

$ |

7.7 |

|

$ |

1.7 |

|

$ |

13.9 |

|

$ |

7.6 |

|

|

Loss on repurchase of Notes (note 7(b)) |

|

— |

|

— |

|

8.8 |

|

— |

| ||||

|

Other (b) |

|

— |

|

0.5 |

|

(2.0 |

) |

0.5 |

| ||||

|

|

|

$ |

7.7 |

|

$ |

2.2 |

|

$ |

20.7 |

|

$ |

8.1 |

|

(a) Restructuring:

Our restructuring actions included consolidating facilities and reducing our workforce. The restructuring charges for the second quarter and first half of 2011 were comprised of $5.3 and $11.3, respectively, for primarily employee termination costs, offset partially by recoveries of $3.6 and $3.7, respectively, representing the gain on sale of vacated properties and surplus equipment. During the second quarter and first half of 2011, we paid employee termination costs and lease payments totaling $5.1 and $10.1, respectively. At June 30, 2011, the restructuring provision consists of the following:

|

Employee termination costs |

|

$ |

9.0 |

|

|

Lease and other contractual obligations, including accretion |

|

11.8 |

| |

|

Facility exit costs and other |

|

0.7 |

| |

|

|

|

$ |

21.5 |

|

CELESTICA INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(in millions of U.S. dollars, except per share amounts)

(unaudited)

(b) Other:

Includes realized recoveries on certain assets that were previously written down through other charges and acquisition-related transaction costs.

10. INCOME TAXES

Our effective tax rate can vary significantly quarter-to-quarter for various reasons, including the mix and volume of business in lower tax jurisdictions within Europe and Asia, in jurisdictions with tax holidays and incentives, and in jurisdictions for which no deferred income tax assets have been recognized because management believed it was not probable that future taxable profit would be available against which tax losses and deductible temporary differences could be utilized. Our effective tax rate can also vary due to the impact of foreign exchange fluctuations and changes in our provisions related to tax uncertainties.

During the second quarter of 2011, we formally settled the tax audits related to the years 1999 through 2008 of one of our Hong Kong subsidiaries for the amounts previously accrued. During the second quarter of 2010, we recorded an adjustment relating to these tax audits which had the effect of increasing the effective tax rate for the three and six months ended June 30, 2010.

11. FINANCIAL INSTRUMENTS AND RISK MANAGEMENT

Our financial assets are comprised primarily of cash and cash equivalents, accounts receivable and derivatives used for hedging purposes. Our financial liabilities are comprised primarily of accounts payable, certain accrued and other liabilities and provisions, as well as derivatives. The majority of our financial liabilities are recorded at amortized costs except for derivatives. Our term deposits are classified as held-to-maturity and our short-term investments in money market funds are recorded at fair value, with changes recognized through our consolidated statement of operations.

Cash and cash equivalents are comprised of the following:

|

|

|

January 1 |

|

December 31 |

|

June 30 |

| |||

|

|

|

2010 |

|

2010 |

|

2011 |

| |||

|

|

|

|

|

|

|

|

| |||

|

Cash (i) |

|

$ |

259.8 |

|

$ |

242.6 |

|

$ |

221.8 |

|

|

Cash equivalents (i) |

|

677.9 |

|

390.2 |

|

330.8 |

| |||

|

|

|

$ |

937.7 |

|

$ |

632.8 |

|

$ |

552.6 |

|

(i) Our current portfolio consists of bank deposits and certain money market funds that hold primarily U.S. government securities. The majority of our cash and cash equivalents are held with financial institutions each of which had at June 30, 2011 a Standard and Poor’s rating of A-1 or above.

Currency risk:

Due to the global nature of our operations, we are exposed to exchange rate fluctuations on our financial instruments denominated in various currencies. The majority of our currency risk is driven by the operational costs incurred in local currencies by our subsidiaries. We manage our currency risk through our hedging program using forecasts of future cash flows and balance sheet exposures denominated in foreign currencies.

Our major currency exposures at June 30, 2011 are summarized in U.S. dollar equivalents in the following table. We have included in this table only those items that we classify as financial assets or liabilities and which were denominated in non-functional currencies. In accordance with the financial instruments standard, we have excluded

CELESTICA INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(in millions of U.S. dollars, except per share amounts)

(unaudited)

items such as pension and post-employment benefits and income taxes. The local currency amounts have been converted to U.S. dollar equivalents using the spot rates at June 30, 2011.

|

|

|

Chinese |

|

Malaysia |

|

Thai |

|

Canadian |

|

Mexican |

| |||||

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

|

Cash and cash equivalents |

|

$ |

24.7 |

|

$ |

1.0 |

|

$ |

1.0 |

|

$ |

4.7 |

|

$ |

2.2 |

|

|

Accounts receivable |

|

19.4 |

|

— |

|

— |

|

— |

|

— |

| |||||

|

Other financial assets |

|

2.1 |

|

0.6 |

|

1.1 |

|

— |

|

0.1 |

| |||||

|

Accounts payable and certain accrued and other liabilities |

|

(27.7 |

) |

(13.2 |

) |

(18.0 |

) |

(27.1 |

) |

(15.8 |

) | |||||

|

Net financial assets (liabilities) |

|

$ |

18.5 |

|

$ |

(11.6 |

) |

$ |

(15.9 |

) |

$ |

(22.4 |

) |

$ |

(13.5 |

) |

Foreign currency risk sensitivity analysis:

At June 30, 2011, a one-percentage point strengthening or weakening of the following currencies against the U.S. dollar for our financial instruments denominated in non-functional currencies is summarized in the following table. The financial instruments impacted by a change in exchange rates include our exposures to the above financial assets or liabilities denominated in non-functional currencies and our foreign exchange forward contracts.

|

|

|

Chinese |

|

Malaysia |

|

Thai |

|

Canadian |

|

Mexican |

| |||||

|

1% Strengthening |

|

|

|

|

|

|