Exhibit 99.1

Oriental Financial Group to Acquire BBVA’s Puerto Rico Operations

| • | Creates Market Leading Bank that is Strongly Capitalized, Locally Controlled and Totally Focused on Puerto Rico |

| • | Transforms Oriental with Bigger Branch Network, Larger and More Diversified Loan Portfolio, Greater Core Deposit Funding, Expanded Customer Base |

| • | Projected to be Highly Accretive to Earnings Per Share |

| • | Initial Tranche of $84 Million in Capital Raised to Support the Transaction |

| • | Conference Call Today at 9:00 AM ET |

SAN JUAN, Puerto Rico, June 28, 2012 – Oriental Financial Group Inc. (NYSE: OFG) and Banco Bilbao Vizcaya Argentaria, S.A. (NYSE: BBVA) today announced the signing of a definitive agreement for Oriental to acquire BBVA’s Puerto Rico operations for $500 million in cash, approximately a 3% premium to tangible book value. Closing of the transaction, which is subject to customary regulatory approvals, is targeted for before year end 2012.

In connection with the acquisition, Oriental announced that it has raised, in a private placement with institutional investors, $84 million of 8.75% non-cumulative convertible perpetual preferred stock, with a conversion price of $11.77, as a first step in raising an estimated $150 million in Tier 1 capital. Oriental intends to use its own excess capital to fund the balance of the purchase price.

CEO’s Comment

“We are very pleased to announce this transaction, which combines two of the healthiest banks on the Island to create a market leading bank that is strongly capitalized, locally controlled and totally focused on serving the needs of Puerto Rico businesses and consumers,” said José Rafael Fernández, President, Chief Executive Officer and Vice Chairman of the Board of Oriental.

“At the same time, by acquiring BBVA Puerto Rico, we will achieve our long time goal of transforming Oriental into a bank with a bigger branch network, a larger and more diversified loan portfolio, greater core deposit funding, expanded customer base, and a smaller investment securities portfolio.”

“BBVA PR has a strong franchise that is highly complementary to Oriental’s. It also has an experienced, highly capable management team and staff that will fit perfectly with Oriental’s service and advisory oriented culture.”

“For Puerto Rico, we believe this transaction further increases the strength of the local banking industry. It is well timed, as the Puerto Rico economy has stabilized and the fiscal situation has continued to improve.”

“For Oriental, we believe this transaction offers the best way to efficiently use our excess capital to enhance our financial performance, franchise and shareholder value. By replacing securities and borrowings with loans and deposits, it creates a unique opportunity to transform our balance sheet and significantly improve earnings predictability.”

“Ultimately, combining two healthy institutions will enable Oriental to continue to gain strength and leadership in the Puerto Rico market. The acquisition reaffirms our strong faith in Puerto Rico’s future and Oriental’s commitment to play an instrumental role in it,” Mr. Fernández concluded.

Oriental’s most recent acquisition was in 2010 when it successfully purchased and integrated Eurobank’s assets and liabilities in Puerto Rico from the Federal Deposit Insurance Corporation.

The Oriental-BBVA PR Combination

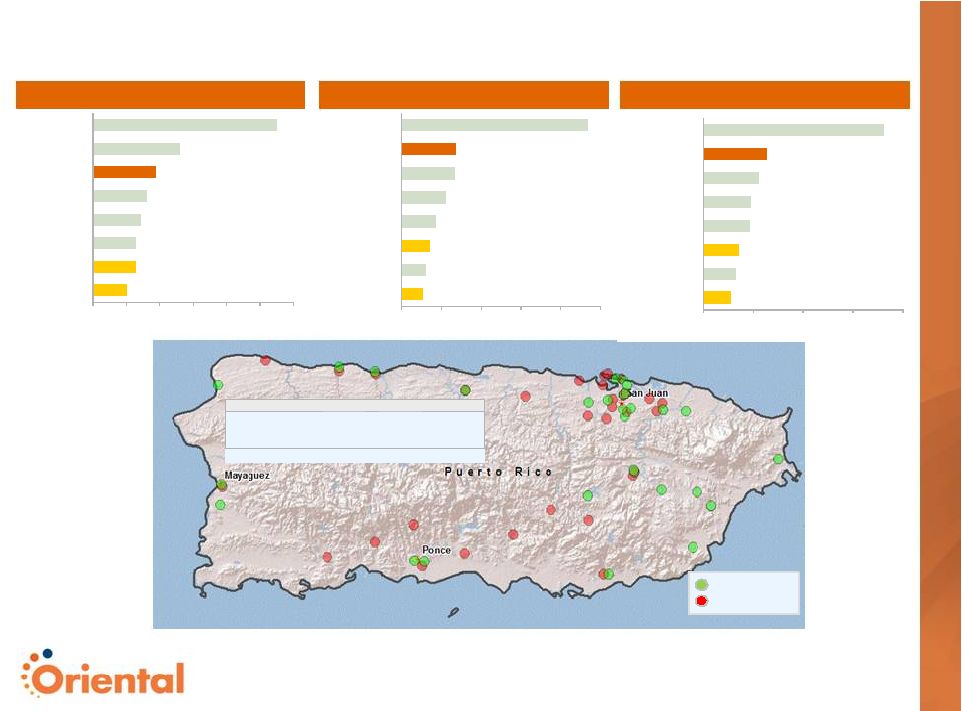

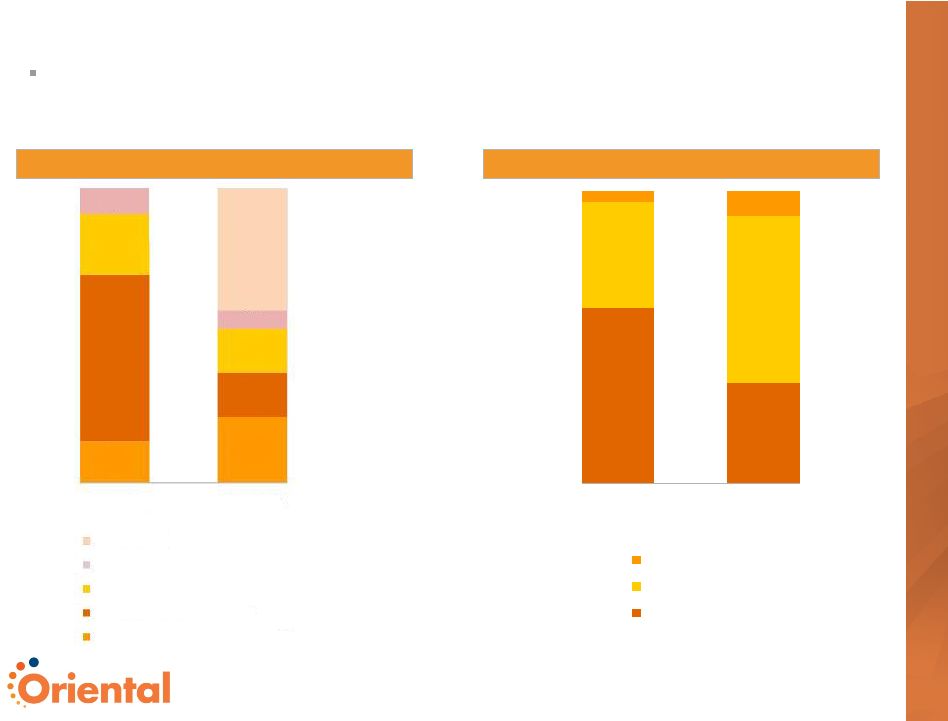

Upon consummation of the acquisition, Oriental will be the second largest bank in Puerto Rico in terms of branches and core deposit funding, and the third largest in terms of assets. The resulting loan portfolio will be approximately a third each in commercial loans, residential mortgages, and consumer loans and leases, while the resulting securities portfolio will represent less than 40% of total earning assets.

As of March 31, 2012, BBVA PR had approximately $5.2 billion in assets, $3.7 billion in loans, $3.3 billion in deposits, 36 branches, and approximately 950 employees, which would add to Oriental’s $6.5 billion in assets, $1.7 billion in loans, $2.3 billion in deposits, 28 branches and approximately 720 employees, also as of March 31, 2012. BBVA PR has strong franchises in commercial and corporate banking, auto lending, retail banking, residential mortgage lending, insurance and wealth management.

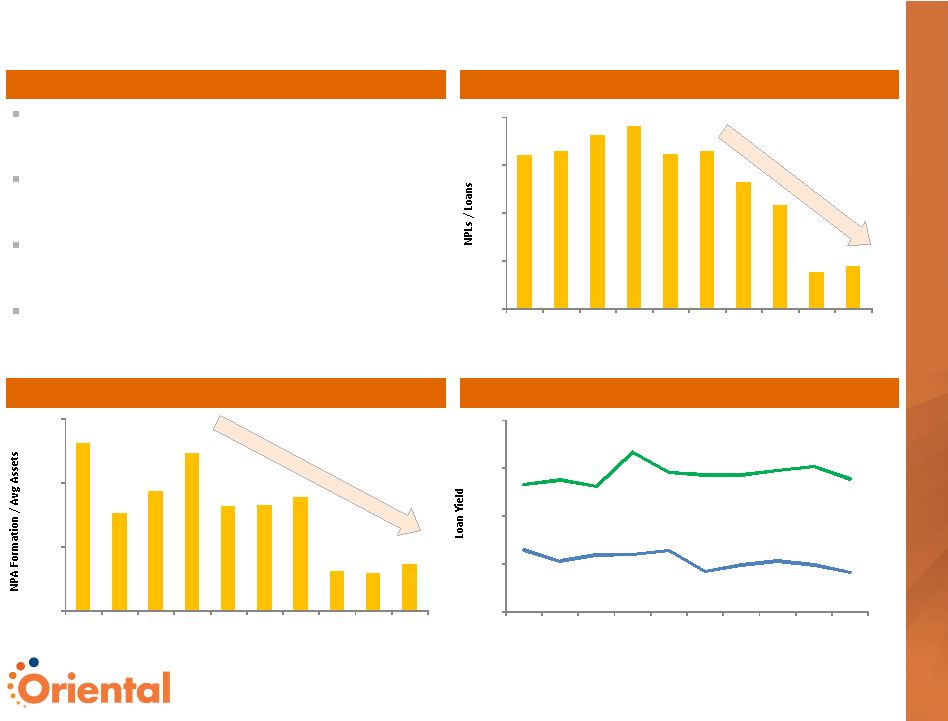

The loan portfolio being acquired positively reflects BBVA PR having aggressively addressed problem assets. Non-performing loans have significantly declined and stabilized, non-performing asset formation also has declined significantly, and BBVA PR exhibits higher loan yields versus peers. As a result of additional credit marks that will be taken as part of the closing, Oriental anticipates having the highest levels of asset quality in the Puerto Rico market.

Financial Highlights

The financial impact of the transaction is expected to be decidedly positive for Oriental. Based on current estimates, the acquisition (including the related capital raise described below) would be approximately 35% accretive to earnings per share in 2013 on a pro forma basis and approximately 52% in 2014. The projected annual cost savings are expected to be about 20% of BBVA PR’s non-interest expenses, approximately half of which are expected to be realized in 2013. Oriental expects to incur certain one-time restructuring charges of approximately $40 million in 2013 in connection with the transaction. While tangible book value per share is expected to be diluted approximately 23% at the close, it is anticipated to be earned back in less than two years, based on the combined company’s earnings.

Oriental has developed a financing plan designed to minimize shareholder dilution and maximize EPS accretion. The Company plans to finance the transaction through (i) $350 million of cash on the balance sheet, (ii) the previously mentioned private placement of $84 million in non-cumulative convertible perpetual preferred stock that is expected to close on July 3, 2012, subject only to customary closing conditions, and (iii) approximately $65-$70 million currently expected to be raised in approximately equal amounts of non-convertible perpetual preferred and common equity.

In addition, to reduce capital requirements and further strategic goals, Oriental plans to delever, at or prior to closing, approximately $1.3 billion of its investment securities portfolio and approximately $450 million of the BBVA PR investment securities portfolio, including the settlement of the related repurchase agreement funding at both Oriental and BBVA PR.

Additional Information

The acquisition has been approved by Oriental’s Board of Directors.

2

Oriental has been providing updates on the acquisition, including details on capital raise, pro forma financials, risk management and its plans for integration, throughout the process to the Federal Reserve Bank of New York and the Federal Deposit Insurance Corporation. Oriental also has advised the Office of the Commissioner of Financial Institutions of the Commonwealth of Puerto Rico about the proposed acquisition. The acquisition is subject to approval by the Board of Governors of the Federal Reserve System, the FDIC and the Commissioner of Financial Institutions, as well as other customary conditions.

Jefferies & Company, Inc. acted as financial advisor for Oriental, delivered a fairness opinion to the Oriental Board, and acted as sole placement agent on the convertible preferred offering. Cleary Gottlieb Steen & Hamilton LLP and McConnell Valdés LLC acted as legal advisors for Oriental.

For more information regarding BBVA PR, the impact of the transaction on a pro forma basis and the key assumptions underlying the pro forma analysis, please see the investor presentation being furnished as an exhibit to our Current Report on Form 8-K filed with the Securities and Exchange Commission today.

Conference Call

A conference call to discuss this announcement and related matters will be held today, Thursday, June 28, 2012, at 9:00 AM Eastern and Puerto Rico Time. The call will be accessible live via a webcast on Oriental’s Investor Relations website at www.orientalfg.com or at http://services.choruscall.com/links/ofg120628.html. A webcast replay will be available shortly thereafter. Access the webcast link in advance to download any necessary software.

Legal Notes

The 8.75% non-cumulative convertible perpetual preferred stock was offered and sold in private transactions and has not been and will not be registered under the Securities Act of 1933, as amended and may not be offered or sold in the United States absent registration or an applicable exemption from registration requirements.

This press release does not constitute an offer to sell or solicitation of an offer to purchase any security, nor shall there be any sale of securities in any state or jurisdiction in which such offer, solicitation or purchase would be unlawful prior to the registration or qualification under the securities laws of any such jurisdiction.

About Oriental Financial Group

Oriental Financial Group Inc. is a diversified financial holding company that operates under U.S. and Puerto Rico banking laws and regulations, principally through its two subsidiaries, Oriental Bank and Trust and Oriental Financial Services. Now in its 48th year in business, Oriental provides a full range of commercial, consumer and mortgage banking services, as well as financial planning, trust, insurance, investment brokerage and investment banking services, primarily in Puerto Rico, through 28 financial centers. Investor information about Oriental can be found at www.orientalfg.com.

Forward-Looking Statements

The information included in this document contains certain forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These statements are based on management’s current expectations and involve certain risks and uncertainties that may cause actual results to differ materially from those expressed in forward-looking statements.

3

Factors that might cause such a difference include, but are not limited to (i) the ability to receive and timing of necessary regulatory approvals to consummate the acquisition, (ii) difficulties in combining the operations of BBVA PR; (iii) the amounts by which our assumptions related to the acquisition, including future financing, fail to approximate actual results; (iv) the rate of declining growth in the economy and employment levels, as well as general business and economic conditions; (v) changes in interest rates, as well as the magnitude of such changes; (vi) the fiscal and monetary policies of the federal government and its agencies; (vii) changes in federal bank regulatory and supervisory policies, including required levels of capital; (viii) the relative strength or weakness of the consumer and commercial credit sectors and of the real estate market in Puerto Rico; (ix) the performance of the stock and bond markets; (x) competition in the financial services industry; (xi) possible legislative, tax or regulatory changes; and (xii) difficulties in combining the operations of any other acquired entity.

For a discussion of such factors and certain risks and uncertainties to which Oriental is subject, see Oriental’s annual report on Form 10-K for the year ended December 31, 2011, as well as its other filings with the U.S. Securities and Exchange Commission. Other than to the extent required by applicable law, including the requirements of applicable securities laws, Oriental assumes no obligation to update any forward-looking statements to reflect occurrences or unanticipated events or circumstances after the date of such statements.

# # #

Contacts:

Puerto Rico: Alexandra Lopez (allopez@orientalfg.com), Oriental Financial Group Inc., (787) 522-6970

U.S.: Steven Anreder (steven.anreder@anreder.com) and Gary Fishman (gary.fishman@anreder.com), Anreder & Company, (212) 532-3232

4