Use these links to rapidly review the document

TABLE OF CONTENTS

EURAMAX HOLDINGS, INC. AND SUBSIDIARIES INDEX TO FINANCIAL STATEMENTS

As filed with the Securities and Exchange Commission on December 9, 2011

Registration No. 333-176561

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 3

TO

FORM S-4

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

EURAMAX INTERNATIONAL, INC.

and the Guarantor Registrants Listed in the Table Below

(Exact name of registrant as specified in its charter)

| Delaware (State or other jurisdiction of incorporation or organization) |

3444 (Primary Standard Industrial Classification Code Number) |

04-3818543 (I.R.S. Employer Identification Number) |

5445 Triangle Parkway, Suite 350

Norcross, GA 30092

(770) 449-7066

(Address, including zip code, and telephone number,

including area code, of registrant's principal executive offices)

R. Scott Vansant

Vice President, Secretary and Chief Financial Officer

5445 Triangle Parkway, Suite 350

Norcross, GA 30092

(770) 449-7066

(Name, address, including zip code,

and telephone number, including area code, of agent for service)

Copies of all communications to:

Michael A. Levitt, Esq.

Fried, Frank, Harris, Shriver &

Jacobson LLP

One New York Plaza

New York, New York 10004

(212) 859-8000

Approximate date of commencement of proposed exchange offer:

As soon as practicable after the effective date of this registration statement.

If the securities being registered on this Form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer o | Accelerated filer o | Non-accelerated filer ý (Do not check if a smaller reporting company) |

Smaller reporting company o |

If applicable, place an X in the box to designate the appropriate rule provision relied upon in conducting this transaction:

Exchange Act Rule 13e-4(i) (Cross-Border Issuer Tender Offer) o

Exchange Act Rule 14d01(d) (Cross-Border Third-Party Tender Offer) o

CALCULATION OF REGISTRATION FEE

|

||||||||

| Title of each class of securities to be registered |

Amount to be registered |

Proposed maximum offering price per Note |

Proposed maximum aggregate offering price |

Amount of registration fee |

||||

|---|---|---|---|---|---|---|---|---|

91/2% Senior Secured Notes due 2016 |

$375,000,000 | 100% | $375,000,000(1) | $43,537.50(2) | ||||

Guarantees of 91/2% Senior Secured Notes due 2016 |

$375,000,000 | — | — | (3) | ||||

|

||||||||

- (1)

- Estimated

solely for the purposes of calculating the registration fee pursuant to Rule 457(f) under the Securities Act of 1933, as amended (the

"Securities Act").

- (2)

- Previously

paid.

- (3)

- Pursuant to Rule 457(n) of the Securities Act, no separate filing fee is required for the guarantees.

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

TABLE OF ADDITIONAL REGISTRANT GUARANTORS

Exact Name of Registrant Guarantor as Specified in its Charter(1) |

State or Other Jurisdiction of Incorporation or Organization |

Primary Standard Industrial Classification Code Number |

I.R.S. Employer Identification Number |

||||||

|---|---|---|---|---|---|---|---|---|---|

Amerimax Building Products, Inc. |

Delaware | 3444 | 75-2670496 | ||||||

Amerimax Fabricated Products, Inc. |

Delaware | 3444 | 58-2260346 | ||||||

Amerimax Finance Company, Inc. |

Delaware | 6719 | 52-2237169 | ||||||

Amerimax Home Products, Inc. |

Delaware | 3444 | 23-2860729 | ||||||

Amerimax Richmond Company |

Indiana | 6719 | 35-1995557 | ||||||

Amerimax UK, Inc. |

Delaware | 6719 | 52-1994016 | ||||||

AMP Commercial, Inc. |

Delaware | 6719 | 20-2208994 | ||||||

Berger Building Products, Inc. |

Pennsylvania | 3444 | 23-0403055 | ||||||

Berger Holdings, Ltd. |

Pennsylvania | 3444 | 23-2160077 | ||||||

Euramax Holdings, Inc. |

Delaware | 3444 | 58-2502320 | ||||||

Fabral Holdings, Inc. |

Delaware | 6719 | 34-1787702 | ||||||

Fabral, Inc. |

Delaware | 3444 | 58-1374624 | ||||||

- (1)

- The address for each of the additional registrant guarantors is c/o Euramax International, Inc., 5445 Triangle Parkway, Suite 350, Norcross, Georgia 30092.

The information in this prospectus is not complete and may be changed. We may not sell these securities or consummate the exchange offer until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell or exchange these securities and it is not soliciting an offer to acquire or exchange these securities in any jurisdiction where the offer, sale or exchange is not permitted.

SUBJECT TO COMPLETION, DATED DECEMBER 9, 2011

Prospectus

Euramax International, Inc.

Exchange Offer for

$375,000,000 91/2% Senior Secured Notes due 2016

and

Guarantees of 91/2% Senior Secured Notes due 2016

The Exchange Offer:

- •

- We are offering to exchange up to $375,000,000 of our new 91/2% Senior Secured Notes due 2016, which we

refer to as the exchange notes, and related guarantees, for up to $375,000,000 of our outstanding 91/2% Senior Secured Notes due 2016, which we refer to as the outstanding notes, and

related guarantees.

- •

- The exchange offer will expire at 12:00 midnight, New York City time

on , 2011, unless we extend it.

We do not currently intend to extend the expiration date.

- •

- You may withdraw tenders of outstanding notes and related guarantees at any time prior to the expiration date of the

exchange offer.

- •

- We will not receive any cash proceeds from the exchange offer.

The Exchange Notes and Related Guarantees:

- •

- We are offering exchange notes and related guarantees to satisfy certain obligations under the registration rights

agreement entered into in connection with the private offering of the outstanding notes.

- •

- The exchange notes and related guarantees will represent the same debt as the outstanding notes and related guarantees and

we will issue the exchange notes and related guarantees under the same indenture as the outstanding notes and related guarantees.

- •

- The exchange notes and related guarantees are substantially identical to the outstanding notes and related guarantees,

except that the exchange notes and related guarantees have been registered under the federal securities laws, are not subject to transfer restrictions and are not entitled to certain registration

rights relating to the outstanding notes and related guarantees.

- •

- The exchange notes will be guaranteed by Euramax Holdings, Inc., our direct parent, and all of our material domestic

subsidiaries, and such guarantees will be joint and several, and full and unconditional.

- •

- There is no existing public market for the outstanding notes and related guarantees or the exchange notes and related

guarantees.

- •

- We do not intend to list the exchange notes and related guarantees on any securities exchange or seek approval for quotation through any automated trading system.

Broker-dealers receiving exchange notes and related guarantees in exchange for outstanding notes and related guarantees acquired for their own account through market-making or other trading activities must acknowledge that they will deliver this prospectus in any resale of the exchange notes. The letter of transmittal states that by so acknowledging and by delivering a prospectus, a broker-dealer will not be deemed to admit that it is an "underwriter" within the meaning of the Securities Act. This prospectus, as it may be amended or supplemented from time to time, may be used by a broker-dealer in connection with resales of the exchange notes received in exchange for outstanding notes that were acquired by such broker-dealer as a result of market-making activities or other trading activities. We have agreed that, for a period of 90 days after the expiration date of the exchange offer, we will make this prospectus available to any broker-dealer for use in connection with any such resale. See "Plan of Distribution."

You should consider carefully the "Risk Factors" beginning on page 20 of this prospectus before participating in the exchange offer.

Neither the Securities and Exchange Commission, nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this prospectus is , 2011.

You should rely only on the information contained in this prospectus and any applicable prospectus supplement or amendment. We have not authorized any person to provide you with any additional or different information. This prospectus is not an offer to sell, nor is it an offer to buy, these securities in any state where the offer or sale is not permitted. The information in this prospectus is complete and accurate as of the date on the front cover of this prospectus, but our business, prospects, financial condition or results of operations may have changed since that date.

i

The terms "Euramax," "Company," "we," "our" and "us" refer to Euramax International, Inc. and all of its consolidated subsidiaries, except as the context otherwise requires. We provide the consolidated financial statements of Euramax Holdings, Inc., our parent company, in this prospectus. Euramax Holdings is a guarantor of the outstanding notes and will be a guarantor of the exchange notes, has no material assets other than the stock of its subsidiaries, and conducts all of its operations through Euramax International, Inc., the issuer of the exchange notes, and its subsidiaries. The term "you" generally refers to a prospective purchaser of the exchange notes.

References to "euros," "Euros" or "€" are to the lawful currency of the European Monetary Union and references to "U.S. dollars," "dollars" or "$" are to the lawful currency of the United States.

INDUSTRY, RANKING AND MARKET DATA

Market and industry data included in this prospectus, including all market share and market size data and our position and the positions of our competitors within these markets, are based on estimates derived from our management's knowledge and experience in the markets in which we operate, as well as information obtained from internal research and surveys, our customers, distributors, suppliers, trade and business organizations and other contacts in the markets in which we operate. Data regarding market position and market share within our industry is intended to provide general guidance, and market share data is subject to change. In addition, customer preferences can and do change. Also, the discussion herein regarding our various markets is based on our views regarding the end markets for our products, which products may be either part of larger overall markets or markets that include other types of products.

ii

This summary highlights significant aspects of our business and this offering. This summary is not complete and does not contain all of the information you should consider before making your investment decision. You should carefully read this entire prospectus, including the risks described under the heading "Risk Factors" and our consolidated financial statements and related notes included elsewhere in this prospectus, before making an investment decision. This summary contains forward-looking statements that involve risks and uncertainties. Our actual results may differ significantly from the results discussed in the forward-looking statements as a result of certain factors, including those set forth in the sections entitled "Risk Factors" and "Cautionary Statement Regarding Forward-Looking Statements."

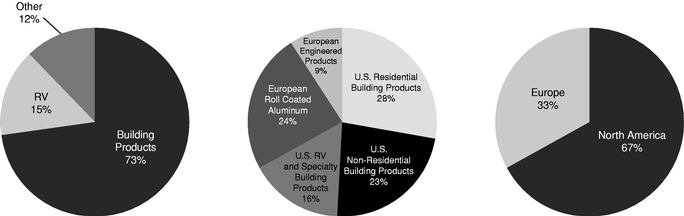

We are a leading international producer of metal and vinyl products sold to the residential repair and remodel, non-residential construction and recreational vehicle (RV) markets primarily in North America and Europe. We are a leader in several niche product categories, including preformed roof-drainage products sold in the U.S., metal roofing and siding for wood frame construction in the U.S., and aluminum siding for towable RVs in the U.S. and Europe. Sales to the building products and RV markets accounted for approximately 73% and 15% of our 2010 net sales, respectively.

Our customers are located predominantly throughout North America and Europe and include distributors, contractors and home improvement retailers, as well as RV, transportation and other original equipment manufacturers, or OEMs. We have extensive in-house manufacturing and distribution capabilities for our more than 10,000 unique products and operate through a network consisting of 40 facilities, including 32 located in the U.S., two in Canada and six in Europe. We have over 50 years of experience manufacturing building products and RV exterior components, including our time as a division of our former parent, Alumax Inc., or Alumax, a fully integrated aluminum producer acquired by Alcoa Inc. in 1998. We have operated as an independent company since 1996 when our division was acquired in a management-led buyout.

The following charts show our net sales by end market, business segment and geography during the year ended December 31, 2010:

| Net Sales by End Market | Net Sales by Business Segment | Net Sales by Geography | ||

|

||||

Our Business Segments

We manage our business and serve our customers through five reportable segments differentiated by market, product type and geography. Our structure and business model trace their roots to our history as a downstream producer of aluminum products and have evolved in response to customer

1

demand for products made from materials other than aluminum and in pursuit of growth opportunities in different end markets and geographies. Today we offer a full complement of products responsive to the demands of the markets we serve and produced from various materials, including aluminum, steel, copper, vinyl and fiberglass.

Our five reportable segments are described below:

U.S. Residential Building Products

Our U.S. Residential Building Products segment utilizes aluminum, steel, copper and vinyl to produce residential roof drainage products, including preformed gutters, downspouts, elbows, soffit, drip edge, fascia, flashing, snow guards and related accessories. These products are used primarily for the repair, replacement or enhancement of residential roof drainage systems. We sell these products to home improvement retailers, lumber yards, distributors and contractors from nine manufacturing and distribution facilities located in North America.

This segment accounted for $244.5 million, or 28%, of our net sales in 2010. In 2010 we were the leading manufacturer of preformed metal gutters sold in North America by unit volumes. Further, we believe that we are the only North American supplier that produces preformed roof drainage systems from each of the four most common gutter materials: aluminum, steel, copper and vinyl. Demand for products we sell through this segment generally increases in periods following significant weather events including hurricanes, severe winter weather, and excessive rain.

U.S. Non-Residential Building Products

Our U.S. Non-Residential Building Products segment utilizes light gauge steel and aluminum coil to produce exterior building components, including roofing and siding panels, ridge caps, flashing, trim, soffit and other accessories. We sell these products to builders, contractors, lumber yards and home improvement retailers from 11 manufacturing and distribution facilities located in the U.S. These products are predominantly used in the construction of a wide variety of small scale non-residential, agricultural and industrial building types on either wood or metal frames.

This segment accounted for $203.4 million, or 23%, of our net sales in 2010. We believe that we are the second largest supplier of steel roofing and siding utilized for wood frame construction in the U.S. by revenues and believe that we have the largest market share of steel roofing and siding supplied to the Northeastern U.S. wood frame market by sales volume.

U.S. RV and Specialty Building Products

Our U.S. RV and Specialty Building Products segment utilizes various materials, including aluminum coil, steel coil and fiberglass to create exterior components for the towable RV, cargo and manufactured housing markets. These products include sidewall components, siding, doors and trim. We also produce specialty made-to-order vinyl replacement windows and aluminum patio and awning components sold primarily to home improvement contractors in the Western U.S. Our vinyl windows and patio and awning products are high-end replacement and remodel products that carry strong brand recognition in the regional markets where they are sold. This segment operates from 13 manufacturing and distribution facilities located in the U.S.

This segment accounted for $146.1 million, or 16%, of our net sales in 2010. We estimate that we sold at least 50% of the aluminum sidewalls and 26% of the doors used in the production of towable RVs in the United States in 2010. In addition, we believe that we are the only supplier of aluminum sidewalls in the U.S. with in-house coil coating capabilities. After declining in 2008 and 2009, the towable RV market grew 42% in 2010 according to the Recreation Vehicle Industry Association, or RVIA.

2

European Roll Coated Aluminum

Our European Roll Coated Aluminum segment uses a roll coating process to apply paint to bare aluminum coil and, to a lesser extent, bare steel coil in order to produce specialty coated coil, which we also process into specialty coated sheets and panels. We sell these products to building panel manufacturers, contractors and UK "holiday home," RV and transportation OEMs that sell to customers throughout Europe and in parts of Asia. Our customers use our specialty coated metal products to manufacture, among other things, RV sidewalls, commercial roofing panels, interior ceiling panels, and liner panels for shipping containers. We produce and distribute these roll coated products from one facility in the Netherlands and one facility in the UK.

This segment accounted for $210.5 million, or 24%, of our net sales in 2010. We estimate that we sold at least 85% of the aluminum sidewall material used in the production of RVs in Europe in 2010.

European Engineered Products

Our European Engineered Products segment utilizes aluminum and vinyl extrusions to produce residential windows, doors and shower enclosures. These products are sold to home improvement retailers, distributors and factory-built "holiday home" builders in the UK. We also produce windows used in the operator compartments of heavy equipment, components sold to suppliers to automotive OEMs in Western Europe and RV doors. We produce and distribute these engineered products from two facilities in France and two facilities in the UK and have developed extensive in-house manufacturing capabilities, including powder coating, glass cutting, anodizing and glass toughening.

This segment accounted for $79.2 million, or 9%, of our net sales in 2010. We believe that we are the largest supplier of residential vinyl windows to the UK home improvement and holiday home markets by revenues.

Our End Markets

Through our five business segments we serve two primary end markets—Building Products and Recreational Vehicle Products. We believe our geographic network, broad product portfolio and customization capabilities allow us to effectively meet the diverse requirements of our customers within our end markets. These primary end markets are discussed below:

Building Products

Our net sales to the Residential Building Products end market in 2010 were $331.2 million, or 38% of our net sales, of which approximately 88% were from North America and approximately 12% were from Europe. We supply roof drainage components, vinyl windows, patio components, roofing and siding panels and other related products to the Residential Building Products market. Our roof drainage products are typically used for repair, remodel or replacement projects which are driven by wear and tear and weather damage. Roof drainage repair projects are often low cost and non-discretionary in nature. We believe that over 95% of our sales to this end market are derived from repair and remodel activity, with demand typically driven by turnover and aging of housing stock, consumer sentiment, availability of home equity and consumer financing and, in the case of our vinyl window products, consumer interest in energy efficiency.

Our net sales to the Non-Residential Building Products end market in 2010 were $312.7 million, or 35% of our net sales, of which approximately 65% were from the U.S. and Canada and approximately 35% were from Europe. Our non-residential building products are typically used in new construction and include, in the U.S., light gauge steel and aluminum roofing and siding panels, trim and hardware and, in Europe, the Middle East and Asia, roll coated aluminum coil and sheet. In the U.S. and Canada, our products are used in a variety of building applications including barns, smaller commercial

3

buildings, storage sheds, schools, churches, shopping centers, parking garages, pavilions, boat docks and carports. Demand for these products varies according to end use and project scale, with smaller projects driven by consumer confidence and the availability of consumer credit and farm or rural applications driven by the strength of agricultural markets. Outside the U.S. and Canada, our specialty coated aluminum coil is used by customers who produce interior and exterior panels for roofs, ceilings, and siding used in larger commercial construction projects. Demand for these products is generally tied to commercial construction activity throughout Europe, the Middle East and Asia.

Recreational Vehicle Products

Our net sales to the Recreational Vehicle Products end market in 2010 were $135.5 million, or 15% of our net sales, of which approximately 42% were from the U.S. and approximately 58% were from Europe. We supply aluminum siding, doors and accessories for RVs in both the U.S. and Europe. This end market is comprised of two distinct RV products: motorhomes and towables. Motorhomes are generally larger, motorized vehicles and towables are lower-cost units towed by automobiles or light trucks. The majority of our sales to this end market are within the towable segment, which comprises the majority of global RV industry unit shipments, and includes sales to substantially all major towable RV OEMs in both the U.S. and Europe. We believe we are the number one supplier of aluminum siding for towable RVs in the combined U.S. and European markets by unit volumes.

Other Products

Our net sales of Other Products in 2010 were $104.3 million, or 12% of our net sales, of which approximately 40% were from the U.S. and Canada and approximately 60% were from Europe. In addition to serving our two primary end markets, we have taken advantage of our available manufacturing capacity and leveraged our materials expertise to develop and sell new products into other markets. These include various metal-based products, such as micro-car frames, heavy equipment operator compartments, utility trailer sidewalls, automobile sunroofs and windows for buses and trains.

The following competitive strengths have contributed to our success and are critical to maintaining the market positions that we enjoy and to achieving our plans for future growth:

Well positioned leader in rebounding end markets. We maintain leading market positions in a number of niche markets which we believe are likely to rebound following a severe cyclical downturn. These positions include:

- •

- #1 position by unit volumes in preformed residential gutters sold in the United States.

- •

- #1 position by revenues in metal roofing and siding for wood frame construction in the Northeast United States.

- •

- #1 position by unit volumes in aluminum siding for towable RV exteriors in the United States.

- •

- #1 position by unit volumes in aluminum siding and roofing for towable RVs in Europe.

- •

- #1 position by unit volumes in steel exterior panels for manufactured housing in the United States.

- •

- #1 position by revenues in vinyl windows and doors for the UK holiday home and home center markets.

Our total net sales derived from these #1 positions were $335.8 million in 2010, or 38% of our total net sales. We believe our leading market positions position us to grow sales and improve our

4

profitability amid a period of anticipated recovery in the residential repair and remodel, non-residential construction and RV markets.

Fabrication capabilities specifically tailored for niche markets. Our manufacturing capabilities are critical to maintaining our strong position in several niche markets for our products. We are able to procure bare metal and paint it to our customers' specifications. These integrated metal coil coating capabilities provide us with a competitive advantage in the home improvement retail and RV industries as an integrated low-cost supplier of metal products with the ability to meet the demanding delivery requirements of customers in these industries. We believe we are also the only supplier who manufactures roof drainage components from each of the four most common gutter materials: aluminum, steel, copper and vinyl. In Europe, our 103" wide aluminum coating line in the Netherlands is one of only two such lines in the world that coat metal in excess of 100" wide.

Strong, established customer relationships. We have maintained long-standing relationships with our major customers across our end markets and, to many, we are a critical supplier. Our top ten accounts include customers from each of our five business segments, have been customers of ours for more than 15 years on average, and include The Home Depot® and Lowe's®, the two largest home improvement retailers in the United States, each of whom have been our customer for over 25 years. In addition, since 2005, the year-over-year retention rate of our top 100 customers has averaged over 97%. The depth and longevity of our customer relationships provide a foundation for recurring revenues and an outlet for the introduction of new products.

More efficient, lower cost business. Since the third quarter of 2008 we have worked to operate a more efficient, lower cost business. Recent improvements reflect the results of our ongoing initiatives to centralize certain management controls, rationalize our operating structure and implement best practices to improve our manufacturing culture. Specific initiatives include:

- •

- Facility rationalization. Between January 2008 and

September 2011, we closed 31 facilities representing approximately 28.2% of our square footage devoted to manufacturing and distribution. These closures eliminated redundant and less profitable or

unprofitable facilities while reducing supervisory and administrative personnel. In closing these facilities, we endeavored to and believe we did retain a significant portion of the profitable

business previously served by these closed facilities. We believe we have enhanced the overall productivity potential of our facilities and will be able to support the peak volumes that existed prior

to these closures.

- •

- Centralized lean manufacturing deployment. Beginning in

June 2008, we centralized the implementation and execution of our lean manufacturing initiatives and related integrated sales and operational planning. As a result, we have achieved significant

reductions in inventory, improved our efficiency and strengthened customer service at many of our facilities. We expect to continue to benefit from greater efficiencies incrementally as we implement

these best practices across our global platform.

- •

- Information technology deployment. We have deployed a

market leading enterprise resource planning, or ERP, system in our U.S. Non-Residential Building Products segment, our U.S. Residential Building Products segment and our corporate offices.

We expect to deploy this system in our remaining U.S. segment within the next two years. Our new ERP system enables us to better support our manufacturing and selling processes by providing critical

information related to product cost, supply chain status and customer profitability.

- •

- Improved freight and logistics productivity. We have undertaken a significant number of initiatives to improve our freight and logistics productivity and reduce our shipping costs, including outsourcing routes, implementing load optimization software, changing our driver compensation

5

- •

- Non-metal procurement cost management. Under our procurement cost reduction initiatives, in 2010 we reduced our non-metal procurement costs by more than $3.8 million.

structure and adding on-board GPS systems to track productivity and manage mileage-based compensation within our captive shipping fleet.

As a result of these and other initiatives, we have a more favorable cost structure than we did prior to 2008. For example, we estimate that we increased our net sales per employee by 7.3% for the year ended December 31, 2010 compared to the year ended December 28, 2007. We also estimate that we reduced our selling and general expenses (excluding depreciation) as a percentage of sales volume by 2% in the year ended December 31, 2010 as compared to the year ended December 28, 2007. These improvements were achieved despite a 23% reduction in net sales volume during the same period. We believe that these improvements have made us more competitive and have positioned us to improve our operating margins when key end markets recover.

Significant diversification across products, materials, customers, end markets and geography. We produce and deliver over 10,000 unique products, utilizing aluminum, steel, copper, vinyl and fiberglass, through a multi-channel distribution network that serves customers across multiple end markets and geographies. Our customer base is highly diverse, with our top ten customers accounting for less than 31% and no single customer accounting for more than 12% of our total 2010 net sales. Further, our top ten customers include customers from each of our five segments. Our sales are also diversified geographically, with 67% of our 2010 net sales originating in the U.S. and Canada, and the remainder originating in the UK, the Netherlands and France. This diversity has helped to offset the cyclicality that is experienced in some of the markets we serve, while allowing us to address profitable growth opportunities as they arise in different product lines, end markets and geographies.

Committed and experienced management team. We have an experienced management team led by our chief executive officer Mitchell B. Lewis and chief financial officer R. Scott Vansant. Messrs. Lewis and Vansant each have approximately 20 years of industry experience with us and our predecessor and have effectively led us through various industry cycles, economic conditions and capital and ownership structures.

Our strategy is to leverage the strengths and experience that have provided us leading market positions to grow our business beyond our current product offerings and the customers and geographic markets we currently serve. In addition, we will endeavor to improve our capabilities and profitability through process improvement initiatives and further cost reductions.

Capture growth related to anticipated market recovery. We intend to capitalize on the anticipated recovery in the residential repair and remodel, non-residential construction and RV markets. We believe that our leading market positions, well-established customer relationships, broad product portfolio, national distribution capabilities and low cost manufacturing platform provide us with a competitive advantage over other suppliers.

Continue to focus on operational leverage. We believe that we have created significant operating leverage within our current manufacturing platform that will provide substantially greater earnings potential in a rising volume environment. We intend to continue to improve our cost structure through incremental lean manufacturing deployment, improved supply chain management, reduced freight and procurement costs, incremental facility rationalization, and implementation of best practices throughout our organization. We also intend to continue to integrate new information technologies across our business, which we expect will further enhance our management capabilities, improve our data quality and enable further integration of our businesses.

6

Drive growth through business development initiatives. We have instituted a series of business development initiatives that we believe will position us to achieve profitable organic growth. As part of our planning process, we task each segment to broaden its geographic presence and product offering. Our efficient and adaptable manufacturing and distribution platform, as well as our existing channel partners and industry relationships, have well positioned us to develop and profitably commercialize new products as well as modify existing products to respond to new and expanding markets, particularly when our markets continue to recover. As part of our efforts, we have instituted an incentive compensation structure that specifically rewards business development efforts among key managers.

- •

- Expand into new geographic markets. Our efficient and

adaptable manufacturing and distribution platform, as well as our established channel partners and industry relationships, have well positioned us to identify and selectively act on growth

opportunities in new geographic markets. The versatility of our product line allows us to modify already successful products for use in other geographic areas both in the United States and abroad. For

example, we plan to grow our sales of roof drainage products in Canada and to the distributor channels outside the Northeastern U.S. Internationally, we have increased our sales representation in

emerging markets where our manufacturing and distribution expertise can be leveraged profitably.

- •

- Increase sales to new customers. We plan to continue

identifying and developing new market opportunities for our products. Opportunities include selling to government entities (including the military) or to government contractors, and increasing

penetration of all building materials sales channels with our full product line.

- •

- Develop innovative new products. We plan to continue engaging in research and development of new products and leveraging our existing customer relationships to distribute these products. Examples include our successful introduction of a new solid gutter cover in the United States as well as roll coated aluminum coil offerings with unique graphics capabilities for architectural applications.

Maintain focus on free cash flow generation and deleveraging. Since 2008, centralization of many procurement functions and implementation of operational planning processes have enhanced our capabilities for managing working capital. In addition, while capital expenditures have historically averaged approximately 1% of net sales, reductions in the number of facilities we operate has further reduced capital spending necessary to maintain equipment and productive capacity while also reducing operating costs. We expect to continue to develop our capabilities for working capital management and to maintain low levels of maintenance capital expenditures. Our focus on these initiatives reflects our intention of generating free cash flow available for debt reduction and deleveraging.

Risks Relating to Our Business

We face certain risks that could materially affect our business, financial condition, results of operations and prospects. You should carefully consider the risks and uncertainties summarized below, the risks described under "Risk Factors," the other information contained in this prospectus and our consolidated financial statements and the related notes. Some of the more significant challenges and risks we face include the following:

- •

- our susceptibility to cyclical fluctuations in the end markets we serve, declines in U.S., European and global general

economic conditions and the stability of our end markets;

- •

- our ability to maintain positive relations with our key customers and the risk to our business if we lose business from or

terminate relationships with our major customers;

- •

- the cost and availability of raw materials used in our products, particularly aluminum and steel, and our ability to pass through increases in these costs to our customers;

7

- •

- our reliance on unique fabrication techniques and risks associated with manufacturing processes;

- •

- our dependence on information technology in our operations, including our new ERP system;

- •

- the highly competitive nature of our business;

- •

- risks arising from the international scope of our business;

- •

- our substantial indebtedness; and

- •

- restrictions contained in our debt agreements which may limit our flexibility in operating our business.

Euramax International, Inc. is a corporation formed under the laws of the State of Delaware. Our headquarters and principal executive offices are located at 5445 Triangle Parkway, Suite 350, Norcross, Georgia 30092 and our telephone number is (770) 449-7066. We are the wholly-owned operating subsidiary of Euramax Holdings, Inc. Our website address is www.euramax.com. Our website and the information contained therein or connected thereto is not incorporated into this prospectus or the registration statement of which this prospectus forms a part, and you should not rely on any such information in making your decision whether to purchase the exchange notes.

The Euramax logo, "Flex-A-SpoutTM" and other trademarks or service marks of Euramax appearing in this prospectus are the property of Euramax. This prospectus contains additional trade names, trademarks and service marks of other companies, which are the property of their respective owners.

We operate on a 52 or 53 week fiscal year ending on the last Friday in December. Our fiscal years consisted of 53 weeks for the year ended December 31, 2010 and 52 weeks for the years ended December 25, 2009 and December 26, 2008. Fiscal years are referred to in this prospectus according to the closest calendar year. For example, 2009 refers to the fiscal year ended December 25, 2009 and 2010 refers to the fiscal year ended December 31, 2010. Additionally, our interim reporting is based on a 13 week quarterly closing calendar with a fiscal year-end on the last Friday in the month of December. For example, the nine month period ended September 30, 2011 includes 39 weeks compared to 40 weeks for the nine month period ended October 1, 2010.

8

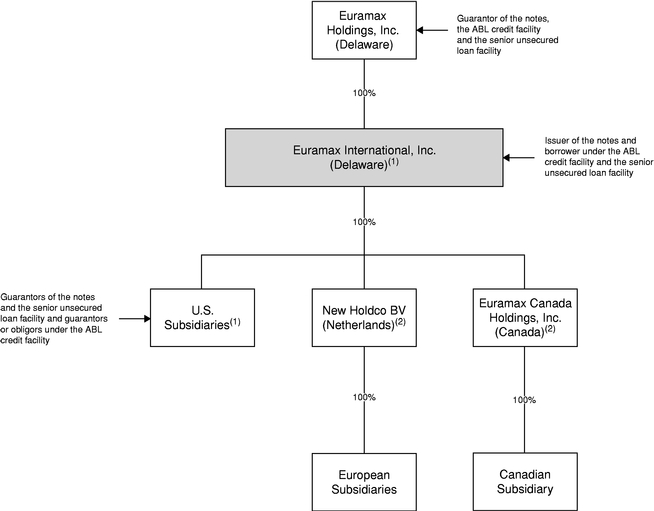

The following chart illustrates our organizational structure:

- (1)

- The

collateral securing the outstanding notes (and which will secure the exchange notes) includes the assets of these entities and pledges of the capital

stock of these entities.

- (2)

- The collateral securing the outstanding notes (and which will secure the exchange notes) includes pledges of 65% of the voting capital stock and 100% of any non-voting capital stock of these entities.

9

The following summary contains basic information about the exchange offer and the exchange notes. It does not contain all the information that is important to you. For a more complete understanding of the exchange notes, please refer to the sections of this prospectus entitled "The Exchange Offer" and "Description of Exchange Notes."

On March 18, 2011, we issued $375.0 million in aggregate principal amount of our 91/2% senior secured notes due 2016, which we refer to as the outstanding notes, in a private offering to a group of initial purchasers in reliance on exemptions from, or in transactions not subject to, the registration requirements of the Securities Act and applicable state securities laws. We entered into a registration rights agreement with the initial purchasers in the private offering in which we agreed, among other things, to file the registration statement of which this prospectus forms a part and to complete an exchange offer for the outstanding notes. The following is a summary of the exchange offer.

Exchange Notes |

$375.0 million aggregate principal amount of 91/2% senior secured notes due 2016, which we refer to as the "exchange notes." We refer to the exchange notes and the outstanding notes collectively as the "notes." | |

|

The terms of the exchange notes are substantially identical to the terms of the outstanding notes, except that the transfer restrictions, registration rights and provisions for additional interest relating to the outstanding notes do not apply to the exchange notes. |

|

The Exchange Offer |

We are offering exchange notes in exchange for a like principal amount of our outstanding notes. You may tender your outstanding notes for exchange notes by following the procedures described under the heading "The Exchange Offer." |

|

Expiration Date; Withdrawal |

The exchange offer will expire at 12:00 midnight, New York City time, on , 2011, unless we extend it. You may withdraw any outstanding notes that you tender for exchange at any time prior to the expiration of this exchange offer. See "The Exchange Offer—Terms of the Exchange Offer" for a more complete description of the tender and withdrawal period. |

|

Conditions to the Exchange Offer |

The exchange offer is not subject to any conditions, other than that (i) the exchange offer does not violate applicable law or any applicable interpretation of the staff of the SEC, (ii) no action or proceeding shall have been instituted or threatened in any court or by any governmental agency which might materially impair the ability of the Company to proceed with the exchange offer, and no material adverse development shall have occurred in any existing action or proceeding with respect to the Company, and (iii) all governmental approvals which the Company deems necessary for the consummation of the exchange offer shall have been obtained. |

10

|

The exchange offer is not conditioned upon any minimum aggregate principal amount of outstanding notes being tendered in the exchange. |

|

Procedures for Tendering Outstanding Notes |

To participate in this exchange offer, you must properly complete and duly execute a letter of transmittal, which accompanies this prospectus, and transmit it, along with all other documents required by such letter of transmittal, to the exchange agent on or before the expiration date at the address provided on the cover page of the letter of transmittal. |

|

|

In the alternative, you can tender your outstanding notes by book-entry delivery following the procedures described in this prospectus, whereby you will agree to be bound by the letter of transmittal and we may enforce the letter of transmittal against you. |

|

|

If a holder of outstanding notes desires to tender such notes and the holder's outstanding notes are not immediately available, or time will not permit the holder's outstanding notes or other required documents to reach the exchange agent before the expiration date, or the procedure for book-entry transfer cannot be completed on a timely basis, a tender may be effected pursuant to the guaranteed delivery procedures described in this prospectus. See "The Exchange Offer—How to Tender Outstanding Notes for Exchange." |

|

Material United States Federal Tax Considerations |

Your exchange of outstanding notes for exchange notes to be issued in the exchange offer will not result in any gain or loss to you for U.S. federal income tax purposes. See "Material United States Federal Tax Considerations" for a summary of U.S. federal income and estate tax consequences associated with the exchange of outstanding notes for the exchange notes and the purchase, ownership and disposition of those exchange notes. |

|

Use of Proceeds |

We will not receive any cash proceeds from the exchange offer. |

|

Consequences of Failure to Exchange Your Outstanding Notes |

Outstanding notes not exchanged in the exchange offer will continue to be subject to the restrictions on transfer that are described in the legend on the outstanding notes. In general, you may offer or sell your outstanding notes only if they are registered under, or offered or sold under an exemption from, the Securities Act and applicable state securities laws. Except as required by the registration rights agreement, we do not currently intend to register the outstanding notes under the Securities Act. If your outstanding notes are not tendered and accepted in the exchange offer, it may become more difficult for you to sell or transfer your outstanding notes. |

11

Resales of the Exchange Notes |

Based on interpretations of the staff of the SEC, we believe that you may offer for sale, resell or otherwise transfer the exchange notes that we issue in the exchange offer without complying with the registration and prospectus delivery requirements of the Securities Act if: |

|

|

• you are not a broker-dealer tendering notes acquired directly from us; |

|

|

• you acquire the exchange notes issued in the exchange offer in the ordinary course of your business; |

|

|

• you are not participating, do not intend to participate, and have no arrangement or undertaking with anyone to participate, in the distribution of the exchange notes issued to you in the exchange offer; and |

|

|

• you are not an "affiliate" of our company, as that term is defined in Rule 405 of the Securities Act. |

|

|

If any of these conditions are not satisfied and you transfer any exchange notes issued to you in the exchange offer without delivering a proper prospectus or without qualifying for a registration exemption, you may incur liability under the Securities Act. We will not be responsible for, or indemnify you against, any liability you incur. |

|

|

Any broker-dealer that acquires exchange notes in the exchange offer for its own account in exchange for outstanding notes which it acquired through market-making or other trading activities must acknowledge that it will deliver this prospectus when it resells or transfers any exchange notes issued in the exchange offer. See "Plan of Distribution" for a description of the prospectus delivery obligations of broker-dealers. |

|

Acceptance of Outstanding Notes and Delivery of Exchange Notes |

Subject to the satisfaction or waiver of the conditions to the exchange offer, we will accept for exchange any and all outstanding notes properly tendered prior to the expiration of the exchange offer. We will complete the exchange offer and issue the exchange notes promptly after the expiration of the exchange offer. |

|

Exchange Agent |

Wells Fargo Bank, National Association, the trustee under the indenture governing the notes, is serving as exchange agent in connection with the exchange offer. The address and telephone number of the exchange agent are set forth under the heading "The Exchange Offer—The Exchange Agent." |

12

The summary below describes the principal terms of the exchange notes. Certain of the terms and conditions described below are subject to important limitations and exceptions. A more detailed description of the terms and conditions of the exchange notes is set forth in "Description of Exchange Notes."

The exchange offer applies to the $375.0 million aggregate principal amount of the outstanding notes outstanding as of the date hereof. The form and terms of the exchange notes will be identical in all respects to the form and the terms of the outstanding notes except that the exchange notes:

- •

- will have been registered under the Securities Act;

- •

- will not be subject to restrictions on transfer under the Securities Act;

- •

- will not be entitled to the registration rights that apply to the outstanding notes; and

- •

- will not be subject to the additional interest provisions relating to the outstanding notes.

The exchange notes evidence the same debt as the outstanding notes exchanged for the exchange notes and will be entitled to the benefits of the same indenture under which the outstanding notes were issued. The indenture is governed by New York law.

Issuer |

Euramax International, Inc. | |

Notes Offered |

$375.0 million aggregate principal amount of 91/2% senior secured notes due 2016. |

|

Maturity |

April 1, 2016. |

|

Interest Rate |

The exchange notes will accrue interest at the rate of 91/2% per annum. |

|

Interest Payment Dates |

April 1 and October 1 of each year. |

|

Collateral |

The exchange notes and the guarantees thereof will be our and the guarantors' senior secured obligations. The exchange notes and the related guarantees will be secured, subject to certain exceptions, by a first priority lien on (i) substantially all of our and the guarantors' assets (other than inventory and accounts receivable and related assets, which assets secure our ABL Credit Facility on a first priority basis) and (ii) all of our capital stock and the capital stock owned by us or a guarantor and 65% of the voting capital stock and 100% of any non-voting capital stock of foreign restricted subsidiaries directly owned by us or a guarantor (the "notes collateral"), and a second priority lien on our and the guarantors' inventory and accounts receivable and related assets (the "ABL collateral"). |

|

Ranking |

The exchange notes and related guarantees will rank: |

|

|

• equal in right of payment with all of our and the guarantors' existing and future unsecured and unsubordinated indebtedness, including our senior unsecured loan facility, and effectively senior to such indebtedness to the extent of the value of the collateral securing the exchange notes; |

13

|

• effectively equal in right of payment with our and the guarantors' obligations that are secured by first priority liens on the notes collateral, to the extent of the value of such collateral, or assets; |

|

|

• effectively junior in right of payment to our and the guarantors' obligations under our ABL Credit Facility and any other obligations that are secured by first priority liens on the ABL collateral or that are secured by a lien on assets that are not part of the collateral securing the exchange notes, in each case, to the extent of the value of such collateral or assets; |

|

|

• structurally subordinated to all existing and future indebtedness and other liabilities (including trade payables) of our subsidiaries that are not guarantors; and |

|

|

• senior in right of payment to all of our and the guarantors' future subordinated indebtedness. As of September 30, 2011, we had $375.0 million outstanding under the notes, approximately $25.3 million drawn (and availability of $42.6 million) under our $70.0 million ABL Credit Facility, and $122.7 million outstanding under our Senior Unsecured Loan Facility. In addition, our subsidiaries that are not guarantors had approximately $63.0 million of total liabilities outstanding (including trade payables). As of and for the nine months ended September 30, 2011, our subsidiaries that are not guarantors had $333.1 million of our assets and generated $273.4 million of our net sales (including $264.4 million of sales to external customers). |

|

|

For more information, see "Description of Exchange Notes—Collateral." |

|

Guarantees |

The payment of principal, premium, if any, and interest on the exchange notes will be fully and unconditionally guaranteed, jointly and severally, on a senior secured basis by Euramax Holdings, our direct parent, and all of our material domestic subsidiaries. The guarantees may be released under certain circumstances. Our foreign subsidiaries will not guarantee the exchange notes. |

|

Optional Redemption |

We may redeem the exchange notes at any time on or after April 1, 2013 at the redemption prices described under the heading "Description of Exchange Notes—Optional Redemption," plus accrued and unpaid interest, if any, to the date of redemption. We may also redeem the greater of (i) $37.5 million and (ii) up to 10% of the aggregate principal amount of the exchange notes at any time and from time to time, prior to April 1, 2013, but not more than once in any twelve-month period, at a price equal to 103% of the principal amount of the exchange notes redeemed. |

14

|

Additionally, we may redeem all or part of the exchange notes at any time prior to April 1, 2013 at a redemption price equal to 100% of the principal amount of exchange notes redeemed, plus a "make whole" premium, and accrued and unpaid interest, if any, to the date of redemption. |

|

|

For more information, see "Description of Exchange Notes—Optional Redemption." |

|

Optional Redemption After Equity Offerings |

At any time before April 1, 2013, we may redeem up to 35% of the aggregate principal amount of the exchange notes issued with the net proceeds of certain equity offerings, so long as: |

|

|

• we redeem the notes within 90 days of completing the equity offering; and |

|

|

• at least 55% of the aggregate principal amount of the notes remains outstanding afterwards. |

|

Change of Control Offer |

If a change of control occurs, we must give holders of the exchange notes the opportunity to sell us their exchange notes at 101% of their face amount, plus accrued and unpaid interest. For more information, see "Description of Exchange Notes—Repurchase at the Option of Holders—Change of Control." |

|

Asset Sale Proceeds |

If we or our subsidiaries engage in asset sales, we generally must either invest the net cash proceeds from such asset sales in our business within a specific period of time, prepay our or the guarantors' secured debt or senior debt of non-guarantor subsidiaries or make an offer to purchase a principal amount of the exchange notes with the excess net cash proceeds. The purchase price of the exchange notes will be 100% of their principal amount plus accrued and unpaid interest, if any. For more information, see "Description of Exchange Notes—Repurchase at the Option of Holders—Asset Sales." |

|

Covenants |

The indenture governing the exchange notes contains covenants limiting our and our restricted subsidiaries' ability to: |

|

|

• incur additional indebtedness or issue certain preferred shares; |

|

|

• create liens on certain assets; |

|

|

• pay dividends or make other equity distributions; |

|

|

• purchase or redeem capital stock; |

|

|

• make certain investments; |

|

|

• sell assets; |

|

|

• agree to any restrictions on the ability of restricted subsidiaries to make payments to us; |

15

|

• consolidate, merge, sell or otherwise dispose of all or substantially all of our assets; |

|

|

• engage in transactions with affiliates; and |

|

|

• designate our restricted subsidiaries as unrestricted subsidiaries. |

|

|

These covenants are subject to a number of important limitations and exceptions. For more information, see "Description of Exchange Notes—Certain Covenants." |

|

No Public Market |

The exchange notes will be new securities for which there is currently no market. Accordingly, we cannot assure that a liquid market for the exchange notes will develop or be maintained. |

|

Use of Proceeds |

We will not receive any cash proceeds from the exchange offer. |

|

Governing Law |

The indenture and the exchange notes will be governed by the laws of the State of New York without regard to conflict of laws principles thereof. |

|

Risk Factors |

See "Risk Factors" and the other information in this prospectus for a discussion of the factors you should carefully consider before deciding to invest in the exchange notes. |

For additional information regarding the exchange notes, see the "Description of Exchange Notes" section of this prospectus.

16

SUMMARY HISTORICAL CONSOLIDATED FINANCIAL DATA

The following table sets forth our summary historical consolidated financial data as of and for the periods indicated. The financial data for the fiscal years ended December 31, 2010, December 25, 2009, December 26, 2008 and December 28, 2007 are derived from our consolidated financial statements which have been audited by Ernst & Young LLP, independent registered public accounting firm. The financial data for the fiscal year ended December 29, 2006 and the nine months ended September 30, 2011 and October 1, 2010 has been derived from our unaudited consolidated financial statements. The unaudited consolidated financial information set forth below has been prepared on the same basis as our audited consolidated financial statements and includes all adjustments, consisting of normal recurring adjustments, that we consider necessary for a fair presentation of our financial position and operating results for such periods. The financial data set forth in this table are not necessarily indicative of our future results of operations and should be read in conjunction with our consolidated financial statements and related notes included elsewhere in this prospectus and the information under "Selected Consolidated Financial Data" and "Management's Discussion and Analysis of Financial Condition and Results of Operations."

| |

As of and for the | ||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

Nine months ended September 30, 2011(1) |

Nine months ended October 1, 2010(1) |

Year ended December 31, 2010(1) |

Year ended December 25, 2009(1) |

Year ended December 26, 2008(1) |

Year ended December 28, 2007(1) |

Year ended December 29, 2006(1) |

||||||||||||||||

| |

(Unaudited) |

(Unaudited) |

|

|

|

|

(Unaudited) |

||||||||||||||||

| |

(in thousands) |

||||||||||||||||||||||

Statements of Operations Data: |

|||||||||||||||||||||||

Net sales |

$ | 714,017 | $ | 671,985 | $ | 883,700 | $ | 812,055 | $ | 1,173,493 | $ | 1,245,631 | $ | 1,140,417 | |||||||||

Cost of goods sold (excluding depreciation and amortization) |

596,488 | 551,631 | 732,451 | 675,126 | 1,009,392 | 1,052,838 | 941,426 | ||||||||||||||||

Gross profit |

117,529 | 120,354 | 151,249 | 136,929 | 164,101 | 192,793 | 198,991 | ||||||||||||||||

Selling and general (excluding depreciation and amortization) |

75,108 | 71,512 | 93,581 | 90,603 | 110,608 | 101,189 | 90,793 | ||||||||||||||||

Multiemployer pension withdrawal expense |

1,200 | — | — | — | — | — | — | ||||||||||||||||

Depreciation and amortization |

28,064 | 27,159 | 38,700 | 39,721 | 55,348 | 57,590 | 52,689 | ||||||||||||||||

Debt restructuring and forbearance expenses |

— | — | — | 14,506 | 3,798 | — | — | ||||||||||||||||

Goodwill and other impairments |

— | — | — | 3,516 | 401,376 | — | — | ||||||||||||||||

Income (loss) from operations |

13,157 | 21,683 | 18,968 | (11,417 | ) | (407,029 | ) | 34,014 | 55,509 | ||||||||||||||

Interest expense |

(42,122 | ) | (53,896 | ) | (68,333 | ) | (84,204 | ) | (109,527 | ) | (84,923 | ) | (74,675 | ) | |||||||||

Gain on extinguishment of debt |

— | — | — | 8,723 | — | — | — | ||||||||||||||||

Other income (loss), net |

(8,912 | ) | (2,183 | ) | (3,484 | ) | 1,303 | (22,716 | ) | 5,143 | 11,949 | ||||||||||||

Loss from continuing operations before income taxes |

(37,877 | ) | (34,396 | ) | (52,849 | ) | (85,595 | ) | (539,272 | ) | (45,766 | ) | (7,217 | ) | |||||||||

Provision (benefit) for income taxes |

(375 | ) | (7,547 | ) | (14,461 | ) | (1,297 | ) | (61,078 | ) | (2,529 | ) | (3,374 | ) | |||||||||

Loss from continuing operations |

(37,502 | ) | (26,849 | ) | (38,388 | ) | (84,298 | ) | (478,194 | ) | (43,237 | ) | (3,843 | ) | |||||||||

Loss from discontinued operations, net of tax |

— | (116 | ) | (152 | ) | (1,330 | ) | (22,413 | ) | (6,194 | ) | (1,830 | ) | ||||||||||

Net loss |

$ | (37,502 | ) | $ | (26,965 | ) | $ | (38,540 | ) | $ | (85,628 | ) | $ | (500,607 | ) | $ | (49,431 | ) | $ | (5,673 | ) | ||

Other Financial Data: |

|||||||||||||||||||||||

Net cash flow provided by (used in): |

|||||||||||||||||||||||

Operating activities |

$ | 1,625 | $ | (26,763 | ) | $ | 4,133 | $ | 59,482 | $ | (16,455 | ) | $ | 74,916 | $ | (12,639 | ) | ||||||

Investing activities |

(8,302 | ) | (5,890 | ) | (9,482 | ) | (2,026 | ) | (6,784 | ) | (50,076 | ) | (65,901 | ) | |||||||||

Financing activities |

(2,565 | ) | (20,475 | ) | (37,046 | ) | (35,929 | ) | 59,598 | (27,893 | ) | 45,645 | |||||||||||

Capital expenditures |

(8,382 | ) | (8,122 | ) | (12,165 | ) | (4,351 | ) | (14,824 | ) | (21,255 | ) | (25,048 | ) | |||||||||

Adjusted EBITDA(2) |

51,116 | 53,603 | 69,281 | 57,544 | 68,291 | 101,685 | 115,403 | ||||||||||||||||

Balance Sheet Data: |

|||||||||||||||||||||||

Cash and cash equivalents |

$ | 16,587 | $ | 15,192 | $ | 24,902 | $ | 69,944 | $ | 48,658 | $ | 8,272 | $ | 16,425 | |||||||||

Working capital(3) |

115,761 | 133,716 | 120,476 | 163,393 | 167,849 | 138,828 | 217,296 | ||||||||||||||||

Total assets |

706,576 | 720,554 | 666,890 | 758,626 | 841,966 | 1,423,648 | 1,440,062 | ||||||||||||||||

Total debt, including current portion |

522,960 | 518,056 | 503,169 | 525,319 | 884,740 | 812,401 | 807,849 | ||||||||||||||||

Total shareholders' equity (deficit) |

(22,797 | ) | 20,093 | 9,831 | 47,060 | (259,282 | ) | 273,771 | 320,245 | ||||||||||||||

- (1)

- Our

fiscal year ends on the last Friday in December of each calendar year. Each of our fiscal years presented is based on a 52 week period, except

that our fiscal year ended December 31, 2010 includes 53 weeks. Additionally, our interim reporting is based on a 13 week quarterly closing calendar with a fiscal

year-end on the last Friday in the month of December. The nine month period ended September 30, 2011 includes 39 weeks compared to 40 weeks for the nine month period

ended October 1, 2010.

- (2)

- Adjusted EBITDA is defined as net loss plus (i) benefit for income taxes, (ii) interest expense and (iii) depreciation and amortization, as further adjusted to exclude the effects of certain income and expense items that management believes make it more difficult to assess the

17

Company's actual operating performance. We have calculated Adjusted EBITDA herein pursuant to the definition of Adjusted EBITDA in the indenture, the Senior Unsecured Loan Facility and the ABL Credit Facility.

We believe Adjusted EBITDA is helpful to investors and our management in highlighting trends because Adjusted EBITDA excludes the results of certain decisions of operating management that can differ significantly from company to company depending on long-term strategic decisions regarding capital structure, the tax jurisdictions in which companies operate and capital investments. We believe that excluding items such as goodwill and asset impairment charges, restructuring charges, gain on extinguishment of debt and the other charges specified below helps investors compare our operating performance with our results in prior periods. We believe it is appropriate to exclude these items as they are not related to ongoing operating performance and, therefore, limit comparability between periods and between us and similar companies. Management compensates for the limitations of using non-GAAP financial measures by using them to supplement GAAP results to provide a more complete understanding of the factors and trends affecting the business than GAAP results alone.

We also believe Adjusted EBITDA is useful to investors because it is frequently used by securities analysts, investors and other interested parties in the evaluation of companies in our industry. We understand that investors use Adjusted EBITDA, among other things, to assess our period-to-period operating performance and to gain insight into the manner in which management analyzes operating performance. In addition, we believe that Adjusted EBITDA is useful in evaluating our operating performance compared to that of other companies in our industry because the calculation of Adjusted EBITDA generally eliminates the effects of financing and income taxes and the accounting effects of capital spending and acquisitions, which items may vary for different companies for reasons unrelated to overall operating performance. Using several measures to evaluate the business allows us and investors to assess our relative performance against our competitors and ultimately monitor our capacity to generate returns for our stockholders.

Although

we believe that Adjusted EBITDA can make an evaluation of our operating performance more consistent because it removes items that do not reflect our core operations, other companies, even in

the same industry, may define Adjusted EBITDA differently than we do. Because not all companies use identical calculations, our presentation of Adjusted EBITDA may not be comparable to similarly

titled measures of other companies. As a result, it may be difficult to use Adjusted EBITDA or similarly named non-GAAP measures that other companies may use to compare the performance of

those companies to our performance. We do not, and investors should not, place undue reliance on Adjusted EBITDA as a measure of operating performance. Adjusted EBITDA is not a measure of financial

performance under accounting principles generally accepted in the U.S., and should not be considered an alternative to net income as a measure of operating performance or cash flows from operating,

investing and financing activities as a measure of liquidity. In addition, Adjusted EBITDA is not intended to be a measure of free cash flow available for management's discretionary use, as it does

not consider certain cash requirements such as interest payments, tax payments and other debt service requirements.

A reconciliation of net income (loss) to Adjusted EBITDA is as follows:

| |

Nine months ended September 30, 2011(1) |

Nine months ended October 1, 2010(1) |

Year ended December 31, 2010 |

Year ended December 25, 2009 |

Year ended December 26, 2008 |

Year ended December 28, 2007 |

Year ended December 29, 2006 |

|||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

(in thousands) |

|||||||||||||||||||||

Net loss |

$ | (37,502 | ) | $ | (26,965 | ) | $ | (38,540 | ) | $ | (85,628 | ) | $ | (500,607 | ) | $ | (49,431 | ) | $ | (5,673 | ) | |

Add: |

||||||||||||||||||||||

Provision (benefit) for income taxes |

(375 | ) | (7,547 | ) | (14,461 | ) | (1,297 | ) | (61,078 | ) | (2,529 | ) | (3,374 | ) | ||||||||

Interest expense |

42,122 | 53,896 | 68,333 | 84,204 | 109,527 | 84,923 | 74,675 | |||||||||||||||

Depreciation and amortization(a) |

28,572 | 27,644 | 39,348 | 41,347 | 57,689 | 60,116 | 55,009 | |||||||||||||||

Adjustments: |

||||||||||||||||||||||

Goodwill and other impairments |

— | — | — | 3,516 | 401,376 | — | — | |||||||||||||||

Other (income) loss, net(b) |

8,912 | 2,183 | 3,484 | (1,303 | ) | 22,716 | (5,143 | ) | (11,949 | ) | ||||||||||||

Debt offering and refinancing fees(c) |

2,513 | — | — | — | — | — | — | |||||||||||||||

Debt restructuring and forbearance expenses(d) |

— | — | — | 14,506 | 4,234 | 1,206 | 169 | |||||||||||||||

Gain on extinguishment of debt(e) |

— | — | — | (8,723 | ) | — | — | — | ||||||||||||||

Loss from discontinued operations, net of tax |

— | 116 | 152 | 1,330 | 22,413 | 6,194 | 1,830 | |||||||||||||||

Stock compensation expense |

1,960 | 1,748 | 2,334 | 2,885 | 925 | 1,107 | 1,261 | |||||||||||||||

Long term incentive plan |

905 | — | — | — | — | — | — | |||||||||||||||

Multiemployer pension withdrawal expense |

1,200 | — | — | — | — | — | — | |||||||||||||||

Severance, relocation and one-time compensation costs |

2,233 | 65 | 2,656 | 3,113 | 4,681 | — | 905 | |||||||||||||||

Facility closures, relocation and optimization costs |

576 | 752 | 2,144 | 188 | 1,673 | 4,184 | — | |||||||||||||||

Non-recurring consulting,legal and professional fees |

— | 1,711 | 2,122 | 3,406 | 4,742 | 226 | — | |||||||||||||||

Non-recurring gains and losses |

— | — | 1,709 | — | — | 832 | — | |||||||||||||||

Plant start up costs |

— | — | — | — | — | — | 2,550 | |||||||||||||||

Adjusted EBITDA |

$ | 51,116 | $ | 53,603 | $ | 69,281 | $ | 57,544 | $ | 68,291 | $ | 101,685 | $ | 115,403 | ||||||||

- (a)

- Includes

amortization attributable to royalty payments under a five-year minimum purchase agreement entered into in connection with our

acquisition of a product line in 2005, which is being recognized in net sales.

- (b)

- Other (income) loss for the nine months ended September 30, 2011 include translation losses on intercompany obligations of $7.4 million and a $1.5 million loss on extinguishment of the First Lien Credit Facility.

18

- (c)

- Debt

offering and refinancing fees include indirect tax consulting and legal fees related to the Company's debt offering and other financing transactions

and certain legal and professional fees incurred for capital market activities.

- (d)

- Debt

restructuring, acquisition and forbearance expenses include, for the years ended December 26, 2008 and December 25, 2009, expenses

associated with a series of forbearance and limited waiver agreements in place from November 10, 2008 to June 29, 2009 with our then-existing lenders. See "Management's

Discussion and Analysis of Financial Condition and Results of Operations—History."

- (e)

- Represents the gain recognized in connection with our June 2009 debt restructuring, in which lenders cancelled 100% of amounts owed under our then-existing Second Lien Credit Agreement consisting of principal and accrued interest of $191 million and $12 million, respectively, in exchange for 100% of our issued and outstanding shares of common stock. See "Management's Discussion and Analysis of Financial Condition and Results of Operations—History."

Adjusted EBITDA for annual periods is adjusted to give pro forma effect to acquisitions, dispositions, refinancings, restructurings and operating changes that occurred in the prior four quarters. For the year ended December 31, 2010, these pro forma amounts included approximately (i) $2,419,000 of "severance, relocation and one-time compensation costs," (ii) $1,153,000 of "facility closures, relocation and optimization costs," (iii) $411,000 of "non-recurring consulting, legal and professional fees," and (iv) $1,709,000 of "non-recurring gains and losses." Such pro forma adjustments are not made in our interim periods.

- (3)

- We define working capital as current assets less current liabilities.

19

You should carefully consider the risk factors set forth below as well as the other information contained in this prospectus before making an investment decision. Any of the following risks could materially adversely affect our business, financial condition, results of operations prospects or cash flows. In such a case, you may lose all or part of your original investment in the exchange notes. The risks described below are not the only risks facing us. Additional risks and uncertainties not currently known to us may also materially and adversely affect our business, financial condition or results of operations.

Demand for our products is cyclical, and reduced demand in our end markets is likely to adversely affect our profitability and cash flow.

Demand for many of our products is cyclical in nature. Because the ultimate end users of our products are most typically individuals electing whether to make discretionary expenditures, our results are affected by various macroeconomic trends which affect consumer confidence and access to financing. Sales of our residential building products for repair, remodel and replacement applications depend upon the availability of home equity and consumer financing, low interest rates, the turnover and aging of housing stock, wear and tear, weather damage and consumer sentiment. Expenditures in the broader U.S. residential repair and remodel industry declined substantially between 2007 and 2009 due to adverse changes in many of these factors. Sales of our non-residential building products are affected by consumer confidence, interest rates, consumer disposable income, the strength of agricultural markets, consumer access to affordable financing and commercial construction trends. Demand for our RV products is driven by trends in disposable income, interest rates and general economic conditions, as well as demographic trends relating to consumers in the 55 through 74 year old age group, who constitute a significant source of demand for RV products. For example, the U.S. towable RV market suffered a 32.9% decline in shipments in 2008 and a 30.1% decline in 2009 but experienced a 46.2% increase in 2010 due to changes in certain of these economic factors. Adverse trends in these and other cyclical factors are likely to materially reduce demand for and sales of our products. Moreover, simultaneous declines in multiple end markets, such as those we experienced in 2008 and 2009, could have a material adverse effect on our business, financial condition, results of operations, prospects and cash flows.

Our business, financial condition, results of operations, prospects and cash flows have been and in the future may be materially and adversely affected by U.S., European and global general economic conditions.

Many aspects of our business, including demand for our products and the pricing and availability of raw materials, are affected by global general economic conditions and, specifically, economic conditions in the U.S. and Europe. General economic conditions and predictions regarding future economic conditions also affect our business strategies, and a decrease in demand for our products or other adverse effects resulting from an economic downturn affecting our geographic end markets may cause us to fail to achieve our anticipated financial results. General economic factors beyond our control that affect our business and end-markets include interest rates, inflation, deflation, consumer credit availability, consumer debt levels, consumer confidence, employment levels, business confidence levels, housing markets, energy costs, tax rates and policy, unemployment rates, commencement or escalation of war or hostilities, the threat or possibility of war, terrorism or other global or national unrest, political or financial instability, and other matters that influence spending by our customers and in our end markets. Increasing volatility in financial markets may cause these factors to change with a greater degree of frequency or increase in magnitude.

Beginning in the fall of 2008 and continuing through 2009 and into 2010, the global economy entered a financial crisis and severe global recession, which materially and adversely impacted our