UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934. | |

For the quarterly period ended June 30, 2020

or

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934. | |

For the transition period from to

Commission File Number: 001-34139

(Exact name of registrant as specified in its charter)

Federally chartered | ||||||||||||||

corporation | ||||||||||||||

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | (Address of principal executive offices) | (Zip Code) | (Registrant’s telephone number, including area code) | ||||||||||

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

None | N/A | N/A |

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ☒ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

☒ | Accelerated filer | ☐ | ||||

Non-accelerated filer | ☐ | Smaller reporting company | ||||

Emerging growth company | ||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As of July 14, 2020, there were 650,059,292 shares of the registrant’s common stock outstanding.

Table of Contents |

Table of Contents

Page | |

MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | |

n Introduction | |

n Market Conditions and Economic Indicators | |

n Consolidated Results of Operations | |

n Consolidated Balance Sheets Analysis | |

n Our Business Segments | |

n Risk Management | |

l Credit Risk | |

l Operational Risk | |

l Market Risk | |

n Liquidity and Capital Resources | |

n Off-Balance Sheet Arrangements | |

n Critical Accounting Policies and Estimates | |

n Conservatorship and Related Matters | |

n Regulation and Supervision | |

n Forward-Looking Statements | |

FINANCIAL STATEMENTS | |

OTHER INFORMATION | |

CONTROLS AND PROCEDURES | |

EXHIBIT INDEX | |

SIGNATURES | |

FORM 10-Q INDEX | |

Freddie Mac 2Q 2020 Form 10-Q | i | |

Table of Contents |

MD&A TABLE INDEX

Table | Description | Page |

1 | Summary of Condensed Consolidated Statements of Comprehensive Income (Loss) | |

2 | Components of Net Interest Income | |

3 | Analysis of Net Interest Yield | |

4 | Components of Guarantee Fee Income | |

5 | Components of Investment Gains (Losses), Net | |

6 | Components of Mortgage Loans Gains (Losses) | |

7 | Components of Investment Securities Gains (Losses) | |

8 | Components of Debt Gains (Losses) | |

9 | Components of Derivative Gains (Losses) | |

10 | Components of Benefit (Provision) for Credit Losses | |

11 | Summarized Condensed Consolidated Balance Sheets | |

12 | Single-Family Guarantee Segment Financial Results | |

13 | Multifamily Portfolio and Market Support | |

14 | Multifamily Segment Financial Results | |

15 | Capital Markets Segment Financial Results | |

16 | Capital Markets Segment Interest Rate-Related and Market Spread-Related Fair Value Changes, Net of Tax | |

17 | Single-Family New Business Activity | |

18 | Single-Family Credit Guarantee Portfolio CRT Issuance | |

19 | Single-Family Credit Guarantee Portfolio Credit Enhancement Coverage Outstanding | |

20 | Credit-Enhanced and Non-Credit-Enhanced Loans in Our Single-Family Credit Guarantee Portfolio | |

21 | Credit Enhancement Coverage by Year of Origination | |

22 | Details of Single-Family Credit Enhancement Expenses and Recoveries | |

23 | Reduction in Conservatorship Credit Capital as a Result of Certain CRT Transactions | |

24 | Single-Family Allowance for Credit Losses Activity | |

25 | Single-Family Credit Guarantee Portfolio Credit Performance Metrics | |

26 | Single-Family TDR and Non-Accrual Loans | |

27 | Single-Family TDR Loan Activity | |

28 | Single-Family Loans in Forbearance by Payment Status | |

29 | Credit Quality Characteristics of Our Single-Family Credit Guarantee Portfolio | |

30 | Credit Quality Characteristics of Our Single-Family Loans in Forbearance | |

31 | Single-Family Credit Guarantee Portfolio Attribute Combinations for Higher Risk Loans | |

32 | Alt-A Loans in Our Single-Family Credit Guarantee Portfolio | |

33 | Concentration of Credit Risk of Our Single-Family Credit Guarantee Portfolio | |

34 | Single-Family Loans in Forbearance Activity | |

35 | Single-Family REO Activity | |

36 | Current Credit Quality of Multifamily Loans Under a Forbearance Program | |

37 | Credit-Enhanced and Non-Credit-Enhanced Loans Underlying Our Multifamily Mortgage Portfolio | |

38 | Level of Subordination Outstanding | |

39 | Credit Quality of Our Multifamily Mortgage Portfolio Without Credit Enhancement | |

40 | Single-Family Credit Guarantee Portfolio Non-Depository Servicers | |

41 | Single-Family Mortgage Insurers | |

42 | PVS-YC and PVS-L Results Assuming Shifts of the LIBOR Yield Curve | |

43 | Duration Gap and PVS Results | |

44 | PVS-L Results Before Derivatives and After Derivatives | |

45 | Earnings Sensitivity to Changes in Interest Rates | |

46 | Liquidity Sources | |

Freddie Mac 2Q 2020 Form 10-Q | ii | |

Table of Contents |

Table | Description | Page |

47 | Other Investments Portfolio | |

48 | Funding Sources | |

49 | Other Debt Activity | |

50 | Activity for Debt Securities of Consolidated Trusts Held by Third Parties | |

51 | Net Worth Activity | |

52 | Return on Conservatorship Capital | |

53 | Mortgage-Related Investments Portfolio Details | |

54 | Current and Proposed 2021 Affordable Housing Goal Benchmark Levels | |

Freddie Mac 2Q 2020 Form 10-Q | iii | |

Management's Discussion and Analysis | Introduction | |

Management's Discussion and Analysis of Financial Condition and Results of Operations

This Quarterly Report on Form 10-Q includes forward-looking statements that are based on current expectations, including the effects the COVID-19 pandemic and the actions taken in response may have on our liquidity, business activities, financial condition, and results of operations, and are subject to significant risks and uncertainties. These forward-looking statements are made as of the date of this Form 10-Q. We undertake no obligation to update any forward-looking statement to reflect events or circumstances after the date of this Form 10-Q. Actual results might differ significantly from those described in or implied by such statements due to various factors and uncertainties, including those described in the Forward-Looking Statements section of this Form 10-Q, the Other Information - Risk Factors section of our Form 10-Q for the quarter ended March 31, 2020 and the Business, Forward-Looking Statements, and Risk Factors sections of our Annual Report on Form 10-K for the year ended December 31, 2019, or 2019 Annual Report.

Throughout this Form 10-Q, we use certain acronyms and terms that are defined in the Glossary of our 2019 Annual Report.

You should read the following MD&A in conjunction with our 2019 Annual Report and our condensed consolidated financial statements and accompanying notes for the three and six months ended June 30, 2020 included in Financial Statements.

INTRODUCTION

Freddie Mac is a GSE chartered by Congress in 1970. Our public mission is to provide liquidity, stability, and affordability to the U.S. housing market. We do this primarily by purchasing residential mortgage loans originated by lenders. In most instances, we package these loans into guaranteed mortgage-related securities, which are sold in the global capital markets and transfer interest-rate and liquidity risks to third-party investors. In addition, we transfer mortgage credit risk exposure to third-party investors through our credit risk transfer programs, which include securities- and insurance-based offerings. We also invest in mortgage loans and mortgage-related securities. We do not originate loans or lend money directly to mortgage borrowers.

We support the U.S. housing market and the overall economy by enabling America's families to access mortgage loan funding with better terms and by providing consistent liquidity to the multifamily mortgage market. We have helped many distressed borrowers keep their homes or avoid foreclosure. We are working with FHFA, our customers, and the industry to build a better housing finance system for the nation.

COVID-19 Pandemic Response Efforts

During 2Q 2020, the COVID-19 pandemic continued to evolve both globally and domestically with significant adverse effects on populations and economies. We remain focused on serving our mission and the crucial role we play in the U.S. housing finance system while supporting the health and safety of our communities, customers, and staff. We continue to actively monitor the situation and make decisions based on guidance from national, state, and local governments and public health authorities, including the U.S. Centers for Disease Control and Prevention (CDC).

Our business continuity plans have enabled us to continue fulfilling our mission while protecting our staff and community. Our senior leaders and Crisis Management Team (CMT), consisting of representatives from across the company, are meeting regularly, closely monitoring the situation, and providing frequent updates to our Board of Directors, our staff, and FHFA. While more than 95% of our staff continue to work remotely, our CMT has developed a framework focused on returning our staff to the office in a phased approach. The framework is predicated on several external and internal factors and will allow staff to return to the office in an organized manner, while not compromising their health, safety, and well-being. For example, we have implemented a number of measures that include daily temperature checks and required face coverings for all staff on-site. In addition, a number of new protocols have been established to adhere to best practices, including deep cleaning protocols, an upgraded air-filtration system, reduced touch points and foot traffic, and visitor restrictions. A number of facilities, such as cafeterias and fitness centers, will be unavailable in the early stages of re-entry.

Providing Assistance to Homeowners and Supporting the Single-Family Mortgage Market

We remain focused on making sure homeowners with Freddie Mac-owned mortgages who are directly or indirectly affected by the COVID-19 pandemic are able to stay in their homes during this challenging time. We have announced a number of mortgage-relief options for borrowers affected by the COVID-19 pandemic, including providing up to 12 months of mortgage forbearance during which a borrower’s payments are temporarily reduced or suspended. We have also established a foreclosure and eviction moratorium for homeowners with Freddie Mac-owned single-family mortgages, which FHFA recently instructed us to extend until at least August 31, 2020. In addition, we have introduced a number of temporary measures to help provide sellers with the clarity and flexibility to continue to lend in a prudent and responsible manner and to expedite loan closings and help keep homebuyers, sellers, and appraisers safe during the COVID-19 pandemic. We recently extended the

Freddie Mac 2Q 2020 Form 10-Q | 1 | |

Management's Discussion and Analysis | Introduction | |

application date window for these measures to August 31, 2020 and also expanded certain of these measures.

As of June 30, 2020, 3.75% of loans in our single-family credit guarantee portfolio, based on loan count, were delinquent and in forbearance. All information included in this Form 10-Q related to single-family loans in forbearance is based on information reported to us by our servicers. For the purpose of reporting delinquency rates, we report single-family loans in forbearance as delinquent during the forbearance period to the extent that payments are past due based on the loan's original contractual terms, irrespective of the forbearance agreement. Single-family servicers are not required to report forbearance information to us if the borrower continues to make payments during the forbearance period and remains in current status. As a result, our forbearance data is limited to loans in forbearance that are past due based on the loan’s original contractual terms and does not include loans that are in forbearance where borrowers have continued to make payments during the forbearance period and remain in current status. For this reason, our reported forbearance rates may be lower than single-family forbearance rates reported by other industry participants, which generally report forbearance rates that include all loans in forbearance, including loans where the borrower has continued to make payments during the forbearance period and remain in current status. Effective October 1, 2020, we are requiring servicers to report to us all alternatives to foreclosure, which include forbearance plans on all mortgages, including those that are not delinquent. For additional information on our support of the single-family mortgage market during the COVID-19 pandemic, see MD&A - Risk Management - Credit Risk - Single-Family Mortgage Credit Risk.

Providing Assistance to Renters and Multifamily Borrowers and Supporting the Multifamily Mortgage Market

We have also provided support to the multifamily mortgage market, including by offering multifamily borrowers mortgage forbearance with the condition that they suspend all evictions during the forbearance period for renters unable to pay rent. Under our forbearance program, multifamily borrowers with a fully performing loan as of February 1, 2020 can defer their loan payments for up to 90 days by showing hardship as a consequence of the COVID-19 pandemic and by gaining lender approval. In June 2020, in coordination with FHFA, we announced several supplemental forbearance relief options to assist borrowers with a forbearance plan in place and who continue to be materially affected by the COVID-19 pandemic. These supplemental relief options extend most of the original tenant protections and provide increased flexibility to tenants, allowing the repayment of past due rent over time and not in a lump sum.

As of June 30, 2020, 2.43% of the loans in our multifamily mortgage portfolio, based on UPB, were in forbearance, approximately 83.5% of which are included in securitizations with credit enhancement provided by subordination. We report multifamily loans in forbearance as current as long as the borrower is in compliance with the forbearance agreement, including the agreed upon repayment plan. Loans in forbearance are therefore not included in our multifamily delinquency rates if the borrower is in compliance with the forbearance agreement. For additional information on our support of the multifamily mortgage market during the COVID-19 pandemic, see MD&A - Risk Management - Credit Risk - Multifamily Mortgage Credit Risk.

Business Outlook

We expect the COVID-19 pandemic to have an adverse effect on our business for the remainder of 2020 and into 2021, and perhaps beyond. The duration and continued severity of the COVID-19 pandemic will determine the extent of the effect on our business. The impact the pandemic has had on the economy is unprecedented, and as a result, our economic and business forecasts are more uncertain than usual, and there are significant downside risks.

The housing market, however, is one segment of the economy that has shown signs of recovery, with purchase applications increasing significantly since early 2Q 2020 and mortgage interest rates remaining at record lows. We expect the low mortgage rate environment, which led to a significant increase in mortgage refinance activity in the first half of 2020, to continue and result in high levels of mortgage refinance activity during the second half of 2020, before declining in 2021. However, due to the impact of the COVID-19 pandemic, we expect full-year home sales to fall in 2020 and then begin to rebound in 2021. While house prices increased at a solid pace during 1Q 2020, we expect full-year house price growth to slow in 2020 and 2021.

We also anticipate that supply and demand in the multifamily housing market will be affected over the next year or two due to the COVID-19 pandemic, which could flow through to multifamily fundamentals. The lack of ability to move and form new households, as well as economic uncertainty for renter households, will make it difficult to fill vacancies. As people sheltered in place, the number of lease renewals increased, partially offsetting the lack of new tenants moving in. We expect new completions to slow due to the COVID-19 pandemic, which should limit new supply. The multifamily sector entered the COVID-19 pandemic on solid ground, with below historical average vacancy rates and above average rent growth. The higher unemployment rate resulting from the COVID-19 pandemic will cause some renters to face financial hardships. Federal interventions from enhanced unemployment benefits and other forms of direct relief for the multifamily mortgage market helped lessen the impact of the COVID-19 pandemic on the multifamily sector in 2Q 2020. Many of those benefits are set to expire by the end of July, and without additional support, and if the unemployment rate remains elevated, there could be a greater impact to the multifamily sector in future periods. Multifamily delinquency rates could increase in the near term due to the effects of the COVID-19 pandemic. However, we currently do not expect to experience significant credit losses given our risk transfer business model. For additional information on market and macroeconomic indicators that can affect our business and financial results, see Market Conditions and Economic Indicators.

Freddie Mac 2Q 2020 Form 10-Q | 2 | |

Management's Discussion and Analysis | Introduction | |

Our allowance for credit losses increased significantly during YTD 2020, and we expect single-family serious delinquency rates and the volume of loss mitigation activity to remain elevated as a result of the COVID-19 pandemic and the forbearance programs we have announced. While we expect that the actions we have taken to support the mortgage markets as a result of the COVID-19 pandemic will improve borrower outcomes, these actions may not be as successful as we hope. In addition, we expect these actions may continue to negatively affect our financial condition and results of operations, perhaps significantly. The ultimate success of these programs will depend on the duration and severity of the economic downturn. In addition, our counterparty credit risk level has increased, particularly with respect to non-depository institutions and credit enhancement providers, as a result of financial strains and liquidity pressures on our counterparties due to the COVID-19 pandemic. For additional information, see MD&A - Risk Management - Credit Risk.

While we continued to successfully transfer multifamily credit risk throughout 2Q 2020, our single-family CRT issuance amounts declined significantly during 2Q 2020 due to the volatility in the CRT markets driven by the impact of the COVID-19 pandemic. However, single-family CRT markets recovered substantially by the end of 2Q 2020 and demonstrated an ability to support new issuances, and we successfully executed new single-family CRT offerings in early 3Q 2020. While CRT remains a critical component of our business strategy, and we intend to continue to pursue our existing CRT strategies under the current capital framework, it is uncertain if there will be adequate demand for our single-family CRT transactions during the COVID-19 pandemic and shortly thereafter based on its potential effect on mortgage performance.

Our debt funding needs may increase as we expect to advance significant amounts to cover principal and interest payments to security holders for loans in forbearance and to purchase delinquent loans from securities after borrowers exit forbearance plans. Therefore, our less liquid assets in our mortgage-related investments portfolio are likely to increase in future periods.

Business Results

Consolidated Financial Results

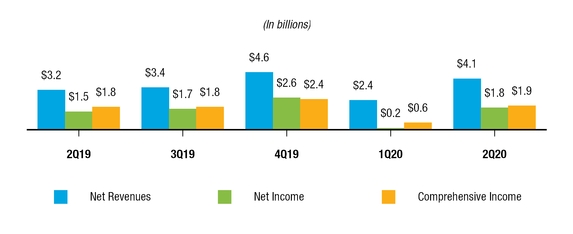

Net Revenues, Net Income, and Comprehensive Income

n | Comprehensive income was $1.9 billion for 2Q 2020, an increase of $0.1 billion, or 6%, from 2Q 2019, driven by higher net revenues, partially offset by higher expected credit losses due to the COVID-19 pandemic. |

n | Net revenues increased $0.9 billion compared to 2Q 2019, primarily due to higher guarantee fee income and higher investment gains (losses), net. |

Freddie Mac 2Q 2020 Form 10-Q | 3 | |

Management's Discussion and Analysis | Introduction | |

Total Equity

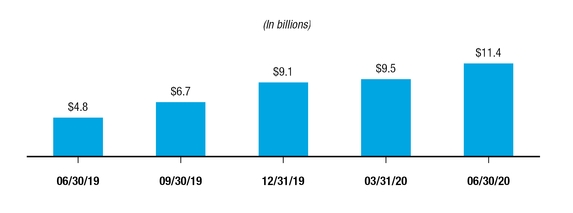

n | Total equity was $11.4 billion as of June 30, 2020, up from $9.1 billion as of December 31, 2019. |

n | Pursuant to the September 2019 Letter Agreement, the liquidation preference of the senior preferred stock increased from $81.8 billion on March 31, 2020 to $82.2 billion on June 30, 2020 based on the $0.4 billion increase in our Net Worth Amount during 1Q 2020, and will increase to $84.1 billion on September 30, 2020 based on the $1.9 billion increase in our Net Worth Amount during 2Q 2020. |

Housing Market Support

Housing Market Support

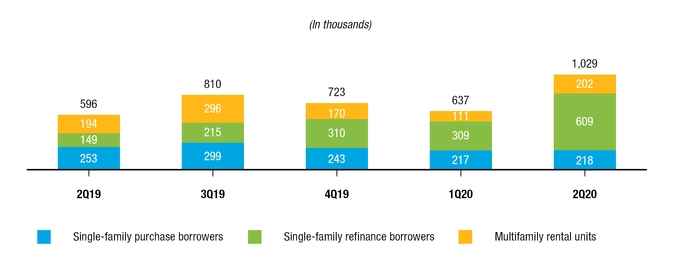

We support the U.S. housing market by executing our Charter Mission to ensure credit availability for new and refinanced single-family mortgages as well as for rental housing. We provided $253.5 billion in liquidity to the mortgage market in 2Q 2020, which enabled the financing of 1.0 million home purchases, refinancings, or rental units. Single-family refinance activity increased significantly during 2Q 2020, as borrowers took advantage of record low mortgage interest rates. In addition, multifamily new business activity increased during 2Q 2020, due to strong demand for multifamily loan products given the low interest-rate environment.

Freddie Mac 2Q 2020 Form 10-Q | 4 | |

Management's Discussion and Analysis | Introduction | |

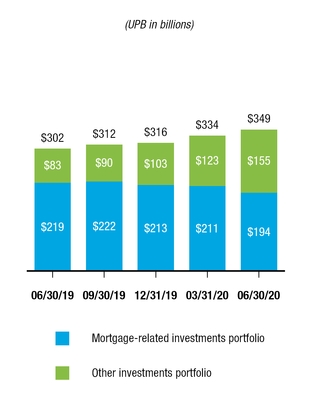

Portfolio Balances

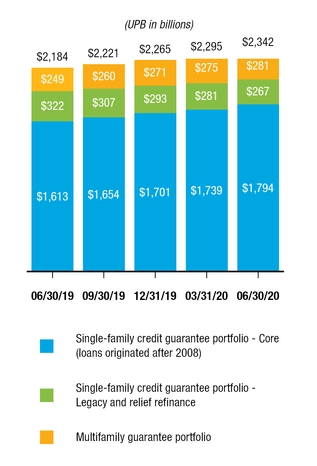

n | Our total guarantee portfolio grew $158 billion, or 7%, from June 30, 2019 to June 30, 2020, driven by a 7% increase in our single-family credit guarantee portfolio and a 13% increase in our multifamily guarantee portfolio. |

l | The growth in our single-family credit guarantee portfolio continued in 2Q 2020 driven by an increase in U.S. single-family mortgage debt outstanding and a higher GSE share of the total market. Additionally, continued house price appreciation contributed to new business acquisitions having a higher average loan size compared to older vintages that continued to run off. |

l | The growth in our multifamily guarantee portfolio also continued in 2Q 2020, primarily driven by strong loan purchase and securitization activity attributable to strong demand for multifamily loan products. |

n | Our total investments portfolio at June 30, 2020 increased compared to June 30, 2019, primarily due to an increase in our other investments portfolio driven by higher near-term cash needs for a higher expected single-family cash loan purchase forecast, coupled with upcoming debt maturities and anticipated calls of other debt. In addition, our custodial trust account balance increased due to higher loan prepayments. In February 2019, FHFA directed us to maintain the mortgage-related investments portfolio at or below $225 billion at all times. |

Freddie Mac 2Q 2020 Form 10-Q | 5 | |

Management's Discussion and Analysis | Introduction | |

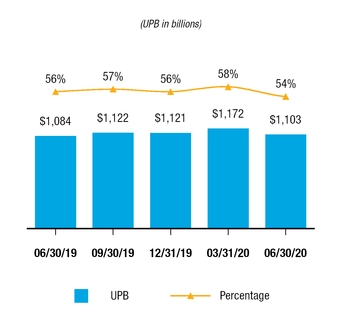

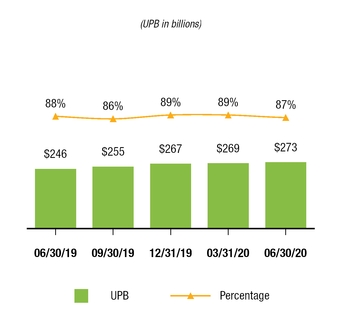

Credit Risk Transfer

Multifamily Mortgage Portfolio with Credit Enhancement

In addition to transferring interest-rate and liquidity risk to third-party investors through our securitization activities, we have developed innovative CRT programs that distribute mortgage credit risk to third-party investors and have transformed our business model from one where we buy and hold credit risk to one where we buy and transfer a portion of such credit risk. Our programmatic offerings regularly transfer a portion of the credit risk primarily on recently acquired loans, with the percentage of our single-family credit guarantee portfolio and the percentage of our multifamily mortgage portfolio covered by credit enhancements at 54% and 87%, respectively, as of June 30, 2020. For additional information, see COVID-19 Pandemic Response Efforts - Business Outlook. See MD&A - Our Business Segments - Single-Family Guarantee - Products and Activities and MD&A - Our Business Segments - Multifamily - Products and Activities in our 2019 Annual Report for additional information on our credit enhancements.

FHFA Re-Proposed Capital Rule for the Enterprises

On May 20, 2020, FHFA issued a notice of proposed rulemaking for a new Enterprise Regulatory Capital Framework for Freddie Mac and Fannie Mae. This proposed rule is a re-proposal of the Enterprise Capital Rule published by FHFA in July 2018. FHFA is seeking comments on the re-proposed capital rule through August 31, 2020. The re-proposed capital rule, if adopted, would significantly increase our capital requirements and could affect our business strategies, perhaps significantly. For additional information regarding the re-proposed capital rule, see MD&A - Regulation and Supervision - Legislative and Regulatory Developments - FHFA Re-Proposed Capital Rule for the Enterprises.

Conservatorship and Government Support for Our Business

Since September 2008, we have been operating in conservatorship, with FHFA as our Conservator. The conservatorship and related matters significantly affect our management, business activities, financial condition, and results of operations. Our future is uncertain, and the conservatorship has no specified termination date. We do not know what changes may occur to our business model during or following conservatorship, including whether we will continue to exist.

In connection with our entry into conservatorship, we entered into the Purchase Agreement with Treasury, under which we issued Treasury both senior preferred stock and a warrant to purchase common stock. Our Purchase Agreement with Treasury and the terms of the senior preferred stock also affect our business activities and are critical to keeping us solvent and avoiding the appointment of a receiver by FHFA under statutory mandatory receivership provisions. We believe that the support provided by Treasury pursuant to the Purchase Agreement currently enables us to have adequate liquidity to conduct normal business activities.

Freddie Mac 2Q 2020 Form 10-Q | 6 | |

Management's Discussion and Analysis | Introduction | |

Treasury, as the holder of the senior preferred stock, is entitled to receive cumulative quarterly cash dividends, when, as, and if declared by the Conservator, acting as successor to the rights, titles, powers, and privileges of our Board of Directors. The dividends we have paid to Treasury on the senior preferred stock have been declared by, and paid at the direction of, the Conservator.

Under the August 2012 amendment to the Purchase Agreement, our cash dividend requirement each quarter is the amount, if any, by which our Net Worth Amount at the end of the immediately preceding fiscal quarter, less the applicable Capital Reserve Amount, exceeds zero. Pursuant to the September 2019 Letter Agreement, the Capital Reserve Amount is $20.0 billion. If for any reason we were not to pay our dividend requirement on the senior preferred stock in full in any future period, the unpaid amount would be added to the liquidation preference and our applicable Capital Reserve Amount would thereafter be zero. This would not affect our ability to draw funds from Treasury under the Purchase Agreement.

The September 2019 Letter Agreement also provides that the liquidation preference of the senior preferred stock will be increased, at the end of each fiscal quarter, beginning on September 30, 2019, by an amount equal to the increase in the Net Worth Amount, if any, during the immediately prior fiscal quarter, until the liquidation preference has increased by $17.0 billion. See Note 2 for more information about our Purchase Agreement with Treasury.

Under the September 2019 Letter Agreement, Freddie Mac and Treasury agreed to negotiate and execute an amendment to the Purchase Agreement that further enhances taxpayer protections by adopting covenants broadly consistent with recommendations for administrative reform contained in Treasury's September 2019 Housing Reform Plan. For more information regarding Treasury's Plan, see MD&A - Regulation and Supervision - Legislative and Regulatory Developments - Treasury Housing Reform Plan in our 2019 Annual Report.

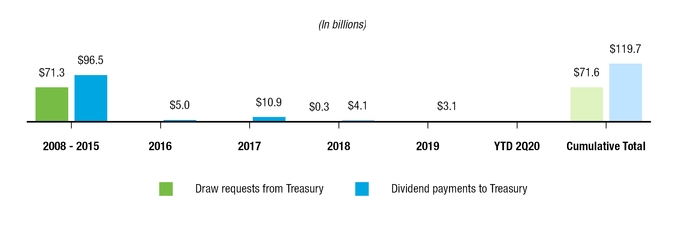

Draw Requests From and Dividend Payments to Treasury

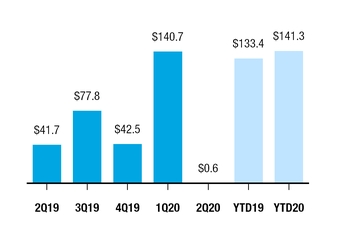

At June 30, 2020, our assets exceeded our liabilities under GAAP; therefore, no draw is being requested from Treasury under the Purchase Agreement. In addition, because our Net Worth Amount did not exceed the applicable Capital Reserve Amount of $20.0 billion, we did not declare or pay a dividend to Treasury on the senior preferred stock during the three months ended March 31, 2020 and June 30, 2020. The amount of available funding remaining under the Purchase Agreement was $140.2 billion at June 30, 2020 and will be reduced by any future draws.

The graph below shows our cumulative draw requests from Treasury and cumulative dividend payments to Treasury. The Treasury draw request amounts reflect the total draws requested based on our quarterly net deficits for the periods presented. Draw requests are funded in the quarter subsequent to any net deficit. The dividend payment amounts reflect the total dividend payments made to Treasury as required by the Purchase Agreement for the periods presented. Dividend payments are currently based on the prior quarter's Net Worth Amount. Under the Purchase Agreement, the payment of dividends does not reduce the outstanding liquidation preference of the senior preferred stock. For more information on the conservatorship and government support for our business, see MD&A - Conservatorship and Related Matters and Note 2 in our 2019 Annual Report.

Draw Requests From and Dividend Payments To Treasury

Freddie Mac 2Q 2020 Form 10-Q | 7 | |

Management's Discussion and Analysis | Market Conditions and Economic Indicators | |

MARKET CONDITIONS AND ECONOMIC INDICATORS

The following graphs and related discussions present certain market and macroeconomic indicators that can significantly affect our business and financial results.

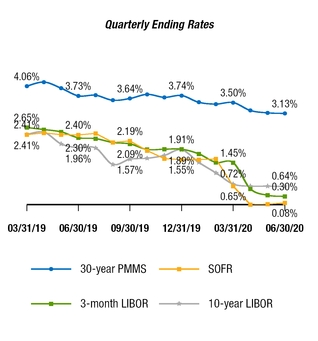

Interest Rates(1)

(1) 30-year PMMS interest rates are as of the last week in each quarter. SOFR interest rates are 30-day average rates.

n | The 30-year Primary Mortgage Market Survey (PMMS) interest rate is indicative of what a consumer could expect to be offered on a first-lien prime conventional conforming home purchase mortgage with an LTV of 80%. Increases (decreases) in the PMMS rate typically result in decreases (increases) in refinancing activity and originations. |

n | Changes in the 10-year LIBOR interest rate and other benchmark rates can significantly affect the fair value of our financial instruments. We have elected hedge accounting for certain assets and liabilities in an effort to reduce GAAP earnings variability attributable to changes in benchmark interest rates. |

n | Changes in the 3-month LIBOR rate affect the interest earned on our short-term investments and interest expense on our short-term funding. |

n | SOFR is a benchmark rate for secured overnight dollar denominated financing identified by certain banking regulators and market participants as a potential replacement for LIBOR. |

n | Interest rates continued to decline and remained at or near record lows during 2Q 2020. |

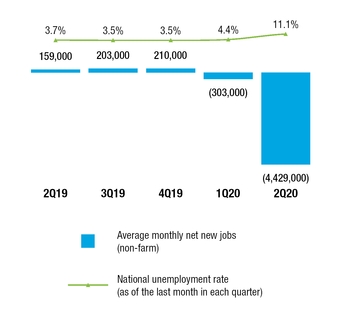

Unemployment Rate and Monthly Net New Jobs

n | Changes in the national unemployment rate can affect several market factors, including the demand for both single-family and multifamily housing and the level of loan delinquencies. |

n | In response to the COVID-19 pandemic, many state and local governments enacted measures designed to curb the spread of COVID-19 that have severely curtailed economic activity and significantly increased unemployment levels, which may take an extended period of time to recover. |

Freddie Mac 2Q 2020 Form 10-Q | 8 | |

Management's Discussion and Analysis | Market Conditions and Economic Indicators | |

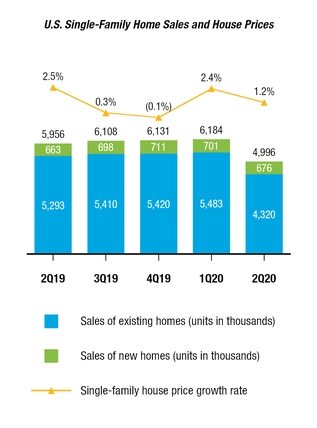

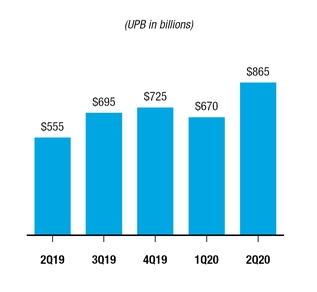

Single-Family Housing and Mortgage Market Conditions

Sources: National Association of Realtors, U.S. Census Bureau, and Freddie Mac House Price Index.

Sources: National Association of Realtors, U.S. Census Bureau, and Freddie Mac House Price Index.U.S. Single-Family Mortgage Originations

Source: Inside Mortgage Finance.

n | Changes in house prices affect the amount of equity that borrowers have in their homes. Borrowers with less equity typically have higher delinquency rates. As house prices decline, the severity of losses we incur on defaulted loans that we hold or guarantee increases because the amount we can recover from the property securing the loan decreases. |

n | Single-family house prices increased 1.2% during 2Q 2020, compared to an increase of 2.5% during 2Q 2019. We expect full-year house price growth to slow in 2020 and 2021. The full effect of the COVID-19 pandemic on house prices is uncertain and dependent on the pandemic's economic impact and the pace of economic recovery. |

n | For full-year 2020, we expect a decline in U.S. single-family home purchase volume, while the low mortgage interest rate environment has led to a significant increase in refinance originations. Freddie Mac's single-family loan purchase volumes generally follow a similar trend. |

n | U.S. single-family mortgage origination volume increased to $865 billion in 2Q 2020 from $555 billion in 2Q 2019, driven by higher refinance volume as a result of lower average mortgage interest rates in recent quarters. |

n | We expect the low mortgage rate environment to continue and result in high levels of refinance activity during the second half of 2020, before declining in 2021. |

Freddie Mac 2Q 2020 Form 10-Q | 9 | |

Management's Discussion and Analysis | Market Conditions and Economic Indicators | |

Multifamily Housing and Mortgage Market Conditions

Source: Reis.

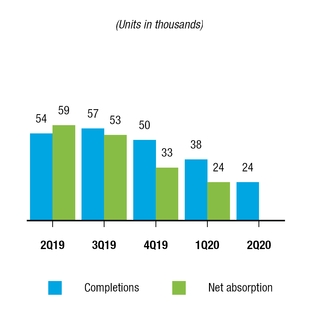

Source: Reis. Apartment Completions and Net Absorption

Source: Reis. 2Q 2020 net absorption data is not yet available.

n | Completions in 2Q 2020 totaled nearly 24,000 units, one of the lowest levels over the past several years, due to the COVID-19 pandemic slowing construction. Despite low absorptions, the vacancy rate remained unchanged from 1Q 2020 at 4.8% nationally. This rate is below the long-term average vacancy rate of 5.4% dating back to 2000, but it is anticipated to rise as COVID-19 relief programs expire. |

n | Effective rent (i.e., the average rent paid by the tenant over the term of the lease, adjusted for concessions by the landlord and costs borne by the tenant) decreased by 0.4% in 2Q 2020, the first decline since 2009. Annual rents increased 1.5% but are expected to decline given the weakening macroeconomy and labor market. |

n | Both supply and demand for rental housing will be affected over the next year or two due to the COVID-19 pandemic, which will flow through to multifamily fundamentals. The lack of ability to move and form new households, as well as economic uncertainty for renter households, will make it difficult to fill vacancies. As people sheltered in place, the number of lease renewals increased, partially offsetting the lack of new tenants moving in. Also, new completions are expected to slow, which should limit new supply. |

n | The multifamily sector entered the COVID-19 pandemic on solid ground, with below historical average vacancy rates and above average rent growth. The higher unemployment rate will cause some tenants to face financial hardships. Federal interventions from enhanced unemployment benefits and other forms of direct relief helped lessen the impact of the COVID-19 pandemic on the multifamily sector in the second quarter of 2020. However, as many of those benefits are set to expire by the end of July 2020, without additional support, and if the unemployment rate remains elevated, there could be a greater impact to the multifamily sector in future periods. |

Freddie Mac 2Q 2020 Form 10-Q | 10 | |

Management's Discussion and Analysis | Market Conditions and Economic Indicators | |

Mortgage Debt Outstanding

Single-Family Mortgage Debt Outstanding

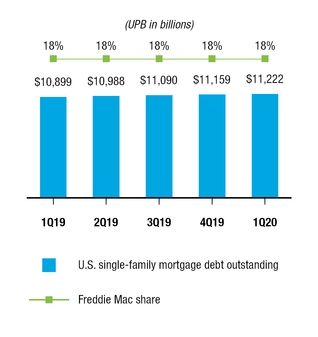

Source: Federal Reserve Financial Accounts of the United States of America.

Multifamily Mortgage Debt Outstanding  Source: Federal Reserve Financial Accounts of the United States of America. 2Q 2020 U.S. multifamily mortgage debt outstanding data is not yet available.

Source: Federal Reserve Financial Accounts of the United States of America. 2Q 2020 U.S. multifamily mortgage debt outstanding data is not yet available.

Source: Federal Reserve Financial Accounts of the United States of America. 2Q 2020 U.S. multifamily mortgage debt outstanding data is not yet available.n | During 2Q 2020, the single-family mortgage market grew primarily driven by house price appreciation. However, the length and severity of the economic downturn caused by the COVID-19 pandemic, and its impact on the housing market, is subject to significant uncertainty. |

n | Up until March 2020, multifamily market fundamentals were driven by a healthy job market, population growth, high propensity to rent among young adults, and rising single-family house prices. Since then, the effects of the COVID-19 pandemic have slowed the economy significantly, which we believe could negatively affect the multifamily mortgage market during the remainder of 2020. |

Freddie Mac 2Q 2020 Form 10-Q | 11 | |

Management's Discussion and Analysis | Market Conditions and Economic Indicators | |

Delinquency Rates

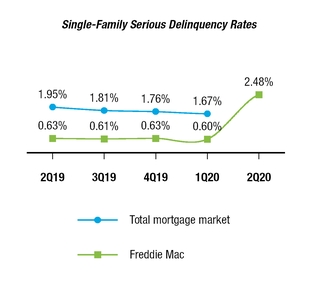

Source: National Delinquency Survey from the Mortgage Bankers Association. 2Q 2020 total mortgage market rate is not yet available.

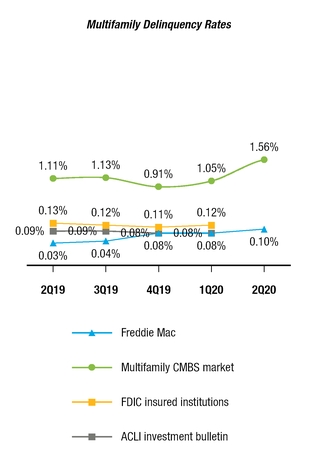

Source: Freddie Mac, FDIC Quarterly Banking Profile, Intex Solutions, Inc., and Wells Fargo Securities (Multifamily CMBS market, excluding REOs), American Council of Life Insurers (ACLI). The 2Q 2020 delinquency rates for FDIC insured institutions and ACLI investment bulletin are not yet available.

Source: Freddie Mac, FDIC Quarterly Banking Profile, Intex Solutions, Inc., and Wells Fargo Securities (Multifamily CMBS market, excluding REOs), American Council of Life Insurers (ACLI). The 2Q 2020 delinquency rates for FDIC insured institutions and ACLI investment bulletin are not yet available.n | Our single-family serious delinquency rates are based on the number of loans in our single-family guarantee portfolio that are past due as reported to us by our servicers. |

n | We report single-family loans in forbearance as delinquent during the forbearance period to the extent that payments are past due based on the loan's original contractual terms, irrespective of the forbearance agreement. |

n | Our single-family serious delinquency rate was higher as of June 30, 2020 compared to June 30, 2019 driven by an increase in loans in forbearance due to the COVID-19 pandemic. However, 52% of the seriously delinquent loans at June 30, 2020 were covered by credit enhancements designed to reduce our credit risk exposure. |

n | We expect our single-family serious delinquency rate to remain elevated as a result of the COVID-19 pandemic and the forbearance programs we are offering in response. |

n | Our 2Q 2020 multifamily delinquency rate remained low compared to other market participants, ending the quarter at 10 basis points, primarily due to our prior-approval underwriting approach. We report multifamily loans in forbearance as current as long as the borrower is in compliance with the forbearance agreement, including the agreed upon repayment plan. Loans in forbearance are therefore not included in our multifamily delinquency rates if the borrower is in compliance with the forbearance agreement. See Risk Management - Credit Risk - Multifamily Mortgage Credit Risk for additional information on our delinquency and forbearance rates. |

n | Multifamily delinquency rates could increase in the near term due to the effects of the COVID-19 pandemic. However, we currently do not expect to experience significant credit losses given our risk transfer business model. |

Freddie Mac 2Q 2020 Form 10-Q | 12 | |

Management's Discussion and Analysis | Consolidated Results of Operations | |

CONSOLIDATED RESULTS OF OPERATIONS

You should read this discussion of our consolidated results of operations in conjunction with our condensed consolidated financial statements and accompanying notes.

On January 1, 2020, we adopted CECL, which changed our methodology for accounting for credit losses on financial assets measured at amortized cost, off-balance sheet credit exposures, and investments in debt securities classified as available-for-sale. See Note 1 for additional information on our adoption of CECL. See Note 4, Note 5, Note 6, and Note 7 for additional information on the changes in our significant accounting policies as a result of our adoption of CECL.

The table below compares our summarized consolidated results of operations. Certain prior period amounts have been revised to conform to the current period presentation. See Note 1 in our 2019 Annual Report for additional information.

Table 1 - Summary of Condensed Consolidated Statements of Comprehensive Income (Loss)

Change | Change | |||||||||||||||||||||||||

(Dollars in millions) | 2Q 2020 | 2Q 2019 | $ | % | YTD 2020 | YTD 2019 | $ | % | ||||||||||||||||||

Net interest income | $2,876 | $2,927 | ($51 | ) | (2 | )% | $5,661 | $6,080 | ($419 | ) | (7 | )% | ||||||||||||||

Guarantee fee income | 469 | 280 | 189 | 68 | 846 | 570 | 276 | 48 | ||||||||||||||||||

Investment gains (losses), net | 670 | (138 | ) | 808 | 586 | (165 | ) | (651 | ) | 486 | 75 | |||||||||||||||

Other income (loss) | 134 | 143 | (9 | ) | (6 | ) | 229 | 126 | 103 | 82 | ||||||||||||||||

Net revenues | 4,149 | 3,212 | 937 | 29 | 6,571 | 6,125 | 446 | 7 | ||||||||||||||||||

Benefit (provision) for credit losses | (705 | ) | 160 | (865 | ) | (541 | ) | (1,938 | ) | 295 | (2,233 | ) | (757 | ) | ||||||||||||

Credit enhancement expense | (233 | ) | (177 | ) | (56 | ) | (32 | ) | (464 | ) | (339 | ) | (125 | ) | (37 | ) | ||||||||||

Expected credit enhancement recoveries | 221 | 38 | 183 | 482 | 688 | 42 | 646 | 1,538 | ||||||||||||||||||

REO operations expense | (14 | ) | (81 | ) | 67 | 83 | (99 | ) | (114 | ) | 15 | 13 | ||||||||||||||

Credit-related expense | (731 | ) | (60 | ) | (671 | ) | (1,118 | ) | (1,813 | ) | (116 | ) | (1,697 | ) | (1,463 | ) | ||||||||||

Administrative expense | (601 | ) | (619 | ) | 18 | 3 | (1,188 | ) | (1,197 | ) | 9 | 1 | ||||||||||||||

Temporary Payroll Tax Cut Continuation Act of 2011 expense | (442 | ) | (399 | ) | (43 | ) | (11 | ) | (874 | ) | (789 | ) | (85 | ) | (11 | ) | ||||||||||

Other expense | (140 | ) | (236 | ) | 96 | 41 | (243 | ) | (360 | ) | 117 | 33 | ||||||||||||||

Operating expense | (1,183 | ) | (1,254 | ) | 71 | 6 | (2,305 | ) | (2,346 | ) | 41 | 2 | ||||||||||||||

Income (loss) before income tax (expense) benefit | 2,235 | 1,898 | 337 | 18 | 2,453 | 3,663 | (1,210 | ) | (33 | ) | ||||||||||||||||

Income tax (expense) benefit | (458 | ) | (392 | ) | (66 | ) | (17 | ) | (503 | ) | (750 | ) | 247 | 33 | ||||||||||||

Net income (loss) | 1,777 | 1,506 | 271 | 18 | 1,950 | 2,913 | (963 | ) | (33 | ) | ||||||||||||||||

Total other comprehensive income (loss), net of taxes and reclassification adjustments | 161 | 320 | (159 | ) | (50 | ) | 610 | 578 | 32 | 6 | ||||||||||||||||

Comprehensive income (loss) | $1,938 | $1,826 | $112 | 6 | % | $2,560 | $3,491 | ($931 | ) | (27 | )% | |||||||||||||||

Freddie Mac 2Q 2020 Form 10-Q | 13 | |

Management's Discussion and Analysis | Consolidated Results of Operations | |

Net Revenues

Net Interest Income

The table below presents the components of net interest income.

Table 2 - Components of Net Interest Income

Change | Change | |||||||||||||||||||||||||

(Dollars in millions) | 2Q 2020 | 2Q 2019 | $ | % | YTD 2020 | YTD 2019 | $ | % | ||||||||||||||||||

Guarantee portfolio net interest income: | ||||||||||||||||||||||||||

Contractual net interest income | $1,054 | $904 | $150 | 17 | % | $2,179 | $1,808 | $371 | 21 | % | ||||||||||||||||

Net interest income related to the Temporary Payroll Tax Cut Continuation Act of 2011 | 454 | 389 | 65 | 17 | 883 | 767 | 116 | 15 | ||||||||||||||||||

Amortization | 748 | 475 | 273 | 57 | 1,300 | 957 | 343 | 36 | ||||||||||||||||||

Total guarantee portfolio net interest income | 2,256 | 1,768 | 488 | 28 | 4,362 | 3,532 | 830 | 23 | ||||||||||||||||||

Investments portfolio net interest income: | ||||||||||||||||||||||||||

Contractual net interest income | 1,460 | 1,603 | (143 | ) | (9 | ) | 2,893 | 3,139 | (246 | ) | (8 | ) | ||||||||||||||

Amortization | (178 | ) | (142 | ) | (36 | ) | (25 | ) | (342 | ) | (270 | ) | (72 | ) | (27 | ) | ||||||||||

Interest expense related to CRT debt | (187 | ) | (289 | ) | 102 | 35 | (427 | ) | (576 | ) | 149 | 26 | ||||||||||||||

Total investments portfolio net interest income | 1,095 | 1,172 | (77 | ) | (7 | ) | 2,124 | 2,293 | (169 | ) | (7 | ) | ||||||||||||||

Income (expense) from hedge accounting | (475 | ) | (13 | ) | (462 | ) | (3,554 | ) | (825 | ) | 255 | (1,080 | ) | (424 | ) | |||||||||||

Net interest income | $2,876 | $2,927 | ($51 | ) | (2 | )% | $5,661 | $6,080 | ($419 | ) | (7 | )% | ||||||||||||||

Key Drivers:

n | Guarantee portfolio contractual net interest income |

l | 2Q 2020 vs. 2Q 2019 and YTD 2020 vs. YTD 2019 - Increased primarily due to a higher contractual guarantee fee rate coupled with the continued growth of the core single-family loan portfolio. |

n | Guarantee portfolio amortization |

l | 2Q 2020 vs. 2Q 2019 and YTD 2020 vs. YTD 2019 - Increased primarily due to income from upfront fees due to an increase in the liquidation rate, partially offset by higher loan premium amortization. |

n | Investments portfolio contractual net interest income |

l | 2Q 2020 vs. 2Q 2019 and YTD 2020 vs. YTD 2019 - Decreased primarily due to the lower interest rate environment, coupled with a change in our investment mix as the other investments portfolio represented a larger percentage of our total investments portfolio. |

n | Investments portfolio amortization |

l | 2Q 2020 vs. 2Q 2019 and YTD 2020 vs. YTD 2019 - Expense increased primarily due to the change in our investment mix as the other investments portfolio represented a larger percentage of our total investments portfolio. |

n | Interest expense related to CRT debt |

l | 2Q 2020 vs. 2Q 2019 and YTD 2020 vs. YTD 2019 - Decreased primarily due to a decline in volume as we no longer issue STACR debt notes on a regular basis. |

n | Income (expense) from hedge accounting |

l | 2Q 2020 vs. 2Q 2019 - Expense increased primarily due to amortization of hedge accounting related basis adjustments, partially offset by a favorable earnings mismatch and higher income related to accruals of periodic cash settlements on derivatives in hedging relationships. |

l | YTD 2020 vs. YTD 2019 - Shifted to expense primarily due to amortization of hedge accounting related basis adjustments and an unfavorable earnings mismatch, partially offset by higher income related to accruals of periodic cash settlements on derivatives in hedging relationships. |

Freddie Mac 2Q 2020 Form 10-Q | 14 | |

Management's Discussion and Analysis | Consolidated Results of Operations | |

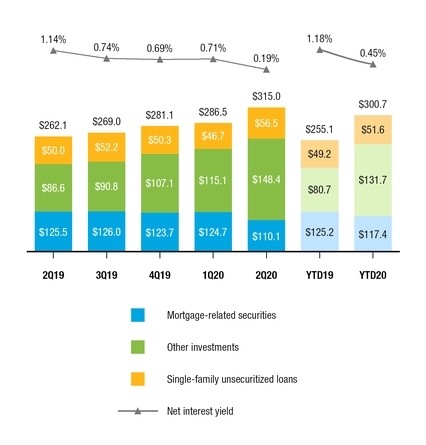

Net Interest Yield Analysis

The tables below present an analysis of interest-earning assets and interest-bearing liabilities.

Table 3 - Analysis of Net Interest Yield

2Q 2020 | 2Q 2019 | |||||||||||||||||

(Dollars in millions) | Average Balance | Interest Income (Expense) | Average Rate | Average Balance | Interest Income (Expense) | Average Rate | ||||||||||||

Interest-earning assets: | ||||||||||||||||||

Cash and cash equivalents | $18,656 | $3 | 0.06 | % | $8,406 | $46 | 2.16 | % | ||||||||||

Securities purchased under agreements to resell | 95,243 | 30 | 0.13 | 55,731 | 350 | 2.52 | ||||||||||||

Secured lending | 4,574 | 20 | 1.83 | 2,325 | 24 | 4.09 | ||||||||||||

Mortgage-related securities: | ||||||||||||||||||

Mortgage-related securities | 115,903 | 1,225 | 4.23 | 133,551 | 1,472 | 4.41 | ||||||||||||

Extinguishment of debt securities of consolidated trusts held by Freddie Mac | (72,835 | ) | (672 | ) | (3.69 | ) | (87,156 | ) | (909 | ) | (4.17 | ) | ||||||

Total mortgage-related securities, net | 43,068 | 553 | 5.14 | 46,395 | 563 | 4.85 | ||||||||||||

Non-mortgage-related securities | 31,632 | 84 | 1.05 | 20,928 | 121 | 2.31 | ||||||||||||

Loans held by consolidated trusts(1) | 1,992,498 | 14,260 | 2.86 | 1,868,648 | 16,377 | 3.51 | ||||||||||||

Loans held by Freddie Mac(1) | 88,112 | 766 | 3.48 | 86,716 | 981 | 4.53 | ||||||||||||

Total interest-earning assets | 2,273,783 | 15,716 | 2.76 | 2,089,149 | 18,462 | 3.53 | ||||||||||||

Interest-bearing liabilities: | ||||||||||||||||||

Debt securities of consolidated trusts including those held by Freddie Mac | 2,024,487 | (12,647 | ) | (2.50 | ) | 1,894,064 | (14,605 | ) | (3.08 | ) | ||||||||

Extinguishment of debt securities of consolidated trusts held by Freddie Mac | (72,836 | ) | 672 | 3.69 | (87,156 | ) | 909 | 4.17 | ||||||||||

Total debt securities of consolidated trusts held by third parties | 1,951,651 | (11,975 | ) | (2.45 | ) | 1,806,908 | (13,696 | ) | (3.03 | ) | ||||||||

Other debt: | ||||||||||||||||||

Short-term debt | 101,989 | (130 | ) | (0.51 | ) | 78,057 | (484 | ) | (2.46 | ) | ||||||||

Long-term debt | 195,573 | (735 | ) | (1.50 | ) | 198,009 | (1,355 | ) | (2.73 | ) | ||||||||

Total other debt | 297,562 | (865 | ) | (1.16 | ) | 276,066 | (1,839 | ) | (2.65 | ) | ||||||||

Total interest-bearing liabilities | 2,249,213 | (12,840 | ) | (2.28 | ) | 2,082,974 | (15,535 | ) | (2.98 | ) | ||||||||

Impact of net non-interest-bearing funding | 24,570 | — | 0.02 | 6,175 | — | 0.01 | ||||||||||||

Total funding of interest-earning assets | 2,273,783 | (12,840 | ) | (2.26 | ) | 2,089,149 | (15,535 | ) | (2.97 | ) | ||||||||

Net interest income/yield | $2,876 | 0.50 | % | $2,927 | 0.56 | % | ||||||||||||

(1) | Loan fees, primarily consisting of amortization of upfront fees, included in interest income were $1.2 billion and $749 million for loans held by consolidated trusts and $20 million and $23 million for loans held by Freddie Mac during 2Q 2020 and 2Q 2019, respectively. |

Freddie Mac 2Q 2020 Form 10-Q | 15 | |

Management's Discussion and Analysis | Consolidated Results of Operations | |

YTD 2020 | YTD 2019 | |||||||||||||||||

(Dollars in millions) | Average Balance | Interest Income (Expense) | Average Rate | Average Balance | Interest Income (Expense) | Average Rate | ||||||||||||

Interest-earning assets: | ||||||||||||||||||

Cash and cash equivalents | $15,444 | $24 | 0.31 | % | $7,756 | $84 | 2.15 | % | ||||||||||

Securities purchased under agreements to resell | 83,767 | 291 | 0.69 | 51,478 | 647 | 2.51 | ||||||||||||

Secured lending | 4,127 | 46 | 2.22 | 1,946 | 40 | 4.09 | ||||||||||||

Mortgage-related securities: | ||||||||||||||||||

Mortgage-related securities | 123,312 | 2,583 | 4.19 | 133,738 | 2,933 | 4.39 | ||||||||||||

Extinguishment of debt securities of consolidated trusts held by Freddie Mac | (79,278 | ) | (1,501 | ) | (3.79 | ) | (85,933 | ) | (1,804 | ) | (4.20 | ) | ||||||

Total mortgage-related securities, net | 44,034 | 1,082 | 4.92 | 47,805 | 1,129 | 4.72 | ||||||||||||

Non-mortgage-related securities | 30,124 | 207 | 1.37 | 20,168 | 244 | 2.42 | ||||||||||||

Loans held by consolidated trusts(1) | 1,978,555 | 30,117 | 3.04 | 1,858,254 | 33,354 | 3.59 | ||||||||||||

Loans held by Freddie Mac(1) | 83,259 | 1,541 | 3.70 | 87,934 | 1,950 | 4.44 | ||||||||||||

Total interest-earning assets | 2,239,310 | 33,308 | 2.97 | 2,075,341 | 37,448 | 3.61 | ||||||||||||

Interest-bearing liabilities: | ||||||||||||||||||

Debt securities of consolidated trusts including those held by Freddie Mac | 2,005,837 | (26,923 | ) | (2.68 | ) | 1,882,956 | (29,481 | ) | (3.13 | ) | ||||||||

Extinguishment of debt securities of consolidated trusts held by Freddie Mac | (79,278 | ) | 1,501 | 3.79 | (85,933 | ) | 1,804 | 4.20 | ||||||||||

Total debt securities of consolidated trusts held by third parties | 1,926,559 | (25,422 | ) | (2.64 | ) | 1,797,023 | (27,677 | ) | (3.08 | ) | ||||||||

Other debt: | ||||||||||||||||||

Short-term debt | 110,605 | (560 | ) | (1.00 | ) | 74,125 | (920 | ) | (2.47 | ) | ||||||||

Long-term debt | 183,022 | (1,665 | ) | (1.81 | ) | 198,973 | (2,771 | ) | (2.78 | ) | ||||||||

Total other debt | 293,627 | (2,225 | ) | (1.51 | ) | 273,098 | (3,691 | ) | (2.70 | ) | ||||||||

Total interest-bearing liabilities | 2,220,186 | (27,647 | ) | (2.49 | ) | 2,070,121 | (31,368 | ) | (3.03 | ) | ||||||||

Impact of net non-interest-bearing funding | 19,124 | — | 0.02 | 5,220 | — | 0.01 | ||||||||||||

Total funding of interest-earning assets | 2,239,310 | (27,647 | ) | (2.47 | ) | 2,075,341 | (31,368 | ) | (3.02 | ) | ||||||||

Net interest income/yield | $5,661 | 0.50 | % | $6,080 | 0.59 | % | ||||||||||||

(1) | Loan fees, primarily consisting of amortization of upfront fees, included in interest income were $2.0 billion and $1.3 billion for loans held by consolidated trusts and $41 million and $39 million for loans held by Freddie Mac during YTD 2020 and YTD 2019, respectively. |

Guarantee Fee Income

The table below presents the components of guarantee fee income.

Table 4 - Components of Guarantee Fee Income

Change | Change | |||||||||||||||||||||||||

(Dollars in millions) | 2Q 2020 | 2Q 2019 | $ | % | YTD 2020 | YTD 2019 | $ | % | ||||||||||||||||||

Contractual guarantee fees | $245 | $222 | $23 | 10 | % | $485 | $439 | $46 | 10 | % | ||||||||||||||||

Guarantee obligation amortization | 254 | 195 | 59 | 30 | 474 | 387 | 87 | 22 | ||||||||||||||||||

Guarantee asset fair value changes | (30 | ) | (137 | ) | 107 | 78 | (113 | ) | (256 | ) | 143 | 56 | ||||||||||||||

Guarantee fee income | $469 | $280 | $189 | 68 | % | $846 | $570 | $276 | 48 | % | ||||||||||||||||

Key Drivers:

n | 2Q 2020 vs. 2Q 2019 and YTD 2020 vs. YTD 2019 - Increased primarily driven by lower fair value losses on our multifamily guarantee asset coupled with continued growth in our multifamily guarantee portfolio. |

Freddie Mac 2Q 2020 Form 10-Q | 16 | |

Management's Discussion and Analysis | Consolidated Results of Operations | |

Investment Gains (Losses), Net

The table below presents the components of investment gains (losses), net.

Table 5 - Components of Investment Gains (Losses), Net

Change | Change | |||||||||||||||||||||||||

(Dollars in millions) | 2Q 2020 | 2Q 2019 | $ | % | YTD 2020 | YTD 2019 | $ | % | ||||||||||||||||||

Mortgage loans gains (losses) | $1,046 | $1,544 | ($498 | ) | (32 | )% | $2,218 | $2,478 | ($260 | ) | (10 | )% | ||||||||||||||

Investment securities gains (losses) | 65 | 358 | (293 | ) | (82 | ) | 1,120 | 502 | 618 | 123 | ||||||||||||||||

Debt gains (losses) | 60 | 49 | 11 | 22 | 760 | 64 | 696 | 1,088 | ||||||||||||||||||

Derivative gains (losses) | (501 | ) | (2,089 | ) | 1,588 | 76 | (4,263 | ) | (3,695 | ) | (568 | ) | (15 | ) | ||||||||||||

Investment gains (losses), net | $670 | ($138 | ) | $808 | 586 | % | ($165 | ) | ($651 | ) | $486 | 75 | % | |||||||||||||

Mortgage Loans Gains (Losses)

The table below presents the components of mortgage loans gains (losses).

Table 6 - Components of Mortgage Loans Gains (Losses)

Change | Change | |||||||||||||||||||||||||

(Dollars in millions) | 2Q 2020 | 2Q 2019 | $ | % | YTD 2020 | YTD 2019 | $ | % | ||||||||||||||||||

Gains (losses) on certain multifamily loan purchase commitments | $650 | $613 | $37 | 6 | % | $1,182 | $1,003 | $179 | 18 | % | ||||||||||||||||

Gains (losses) on mortgage loans: | ||||||||||||||||||||||||||

Single-family | 103 | 453 | (350 | ) | (77 | ) | 81 | 656 | (575 | ) | (88 | ) | ||||||||||||||

Multifamily | 293 | 478 | (185 | ) | (39 | ) | 955 | 819 | 136 | 17 | ||||||||||||||||

Total gains (losses) on mortgage loans | 396 | 931 | (535 | ) | (57 | ) | 1,036 | 1,475 | (439 | ) | (30 | ) | ||||||||||||||

Mortgage loans gains (losses) | $1,046 | $1,544 | ($498 | ) | (32 | )% | $2,218 | $2,478 | ($260 | ) | (10 | )% | ||||||||||||||

Key Drivers:

n | 2Q 2020 vs. 2Q 2019 - Decreased primarily due to a lower volume of sales of single-family held-for-sale loans and lower interest rate-related fair value gains, partially offset by gains due to higher quoted spreads in our multifamily business resulting in higher margins on new loan commitments, as well as spread tightening on multifamily loans and commitments. |

n | YTD 2020 vs. YTD 2019 - Decreased primarily due to spread widening on multifamily loans and commitments, a lower volume of sales of single-family held-for-sale loans, and lower-of-cost-or-fair-value losses on single-family held-for-sale loans, partially offset by gains due to higher quoted spreads in our multifamily business resulting in higher margins on new loan commitments. |

Investment Securities Gains (Losses)

The table below presents the components of investment securities gains (losses).

Table 7 - Components of Investment Securities Gains (Losses)

Change | Change | |||||||||||||||||||||||||

(Dollars in millions) | 2Q 2020 | 2Q 2019 | $ | % | YTD 2020 | YTD 2019 | $ | % | ||||||||||||||||||

Realized gains (losses) on sales of available-for-sale securities | $7 | $33 | ($26 | ) | (79 | )% | $17 | $67 | ($50 | ) | (75 | )% | ||||||||||||||

Realized and unrealized gains (losses) on trading securities | 84 | 358 | (274 | ) | (77 | ) | 1,153 | 497 | 656 | 132 | ||||||||||||||||

Other | (26 | ) | (33 | ) | 7 | 21 | (50 | ) | (62 | ) | 12 | 19 | ||||||||||||||

Investment securities gains (losses) | $65 | $358 | ($293 | ) | (82 | )% | $1,120 | $502 | $618 | 123 | % | |||||||||||||||

Freddie Mac 2Q 2020 Form 10-Q | 17 | |

Management's Discussion and Analysis | Consolidated Results of Operations | |

Key Drivers:

n | 2Q 2020 vs. 2Q 2019 - Decreased primarily due to lower gains on trading securities as long-term interest rates declined less in 2Q 2020 compared to 2Q 2019. |

n | YTD 2020 vs. YTD 2019 - Increased primarily due to higher gains on trading securities from the decline in long-term interest rates as a result of the significant market volatility caused by the COVID-19 pandemic. |

Debt Gains (Losses)

The table below presents the components of debt gains (losses).

Table 8 - Components of Debt Gains (Losses)

Change | Change | |||||||||||||||||||||||||

(Dollars in millions) | 2Q 2020 | 2Q 2019 | $ | % | YTD 2020 | YTD 2019 | $ | % | ||||||||||||||||||

Fair value changes: | ||||||||||||||||||||||||||

Debt securities of consolidated trusts | ($1 | ) | ($2 | ) | $1 | 50 | % | $3 | ($4 | ) | $7 | 175 | % | |||||||||||||

Other debt | (69 | ) | 69 | (138 | ) | (200 | ) | 479 | 67 | 412 | 615 | |||||||||||||||

Total fair value changes | (70 | ) | 67 | (137 | ) | (204 | ) | 482 | 63 | 419 | 665 | |||||||||||||||

Gains (losses) on extinguishment of debt: | ||||||||||||||||||||||||||

Debt securities of consolidated trusts | 35 | (42 | ) | 77 | 183 | 39 | (49 | ) | 88 | 180 | ||||||||||||||||

Other debt | 95 | 24 | 71 | 296 | 239 | 50 | 189 | 378 | ||||||||||||||||||

Total gains (losses) on extinguishment of debt | 130 | (18 | ) | 148 | 822 | 278 | 1 | 277 | 27,700 | |||||||||||||||||

Debt gains (losses) | $60 | $49 | $11 | 22 | % | $760 | $64 | $696 | 1,088 | % | ||||||||||||||||

Key Drivers:

n | 2Q 2020 vs. 2Q 2019 - Remained relatively flat as gains on extinguishments of debt were mostly offset by fair value losses as a result of spread tightening on STACR debt notes for which we elected the fair value option. |

n | YTD 2020 vs. YTD 2019 - Increased primarily due to fair value gains on STACR debt notes for which we elected the fair value option as a result of spread widening caused by the significant market volatility related to the COVID-19 pandemic, coupled with an increase in gains on extinguishments of debt due to an increase in call volume. |

Derivative Gains (Losses)

The table below presents the components of derivative gains (losses).

Table 9 - Components of Derivative Gains (Losses)

Change | Change | |||||||||||||||||||||||||

(Dollars in millions) | 2Q 2020 | 2Q 2019 | $ | % | YTD 2020 | YTD 2019 | $ | % | ||||||||||||||||||

Fair value changes: | ||||||||||||||||||||||||||

Interest-rate swaps | $1,000 | ($1,709 | ) | $2,709 | 159 | % | ($3,863 | ) | ($2,756 | ) | ($1,107 | ) | (40 | )% | ||||||||||||

Option-based derivatives | (705 | ) | 648 | (1,353 | ) | (209 | ) | 3,517 | 461 | 3,056 | 663 | |||||||||||||||

Futures | (120 | ) | (779 | ) | 659 | 85 | (2,448 | ) | (1,021 | ) | (1,427 | ) | (140 | ) | ||||||||||||

Commitments | (396 | ) | (216 | ) | (180 | ) | (83 | ) | (1,122 | ) | (312 | ) | (810 | ) | (260 | ) | ||||||||||

CRT-related derivatives | 43 | 2 | 41 | 2,050 | 121 | 1 | 120 | 12,000 | ||||||||||||||||||

Other | 6 | 7 | (1 | ) | (14 | ) | 37 | 28 | 9 | 32 | ||||||||||||||||

Total fair value changes | (172 | ) | (2,047 | ) | 1,875 | 92 | (3,758 | ) | (3,599 | ) | (159 | ) | (4 | ) | ||||||||||||

Accrual of periodic cash settlements | (329 | ) | (42 | ) | (287 | ) | (683 | ) | (505 | ) | (96 | ) | (409 | ) | (426 | ) | ||||||||||

Derivative gains (losses) | ($501 | ) | ($2,089 | ) | $1,588 | 76 | % | ($4,263 | ) | ($3,695 | ) | ($568 | ) | (15 | )% | |||||||||||

Key Drivers:

n | 2Q 2020 vs. 2Q 2019 - Long-term interest rates declined less in 2Q 2020 compared to 2Q 2019 which resulted in lower fair value losses on pay-fixed interest rate swaps and futures, as well as on certain option-based derivatives, partially offset by lower fair value gains on receive-fixed swaps. |

Freddie Mac 2Q 2020 Form 10-Q | 18 | |

Management's Discussion and Analysis | Consolidated Results of Operations | |

n | YTD 2020 vs. YTD 2019 - The decline in long-term interest rates during YTD 2020 resulted in higher fair value losses on pay-fixed interest rate swaps, forward commitments to issue mortgage-related securities, and futures, partially offset by fair value gains on receive-fixed swaps and certain option-based derivatives. These interest rate-related derivative losses offset the interest rate-related gains on our mortgage loans and investment securities. |

Credit-Related Expense

Benefit (Provision) for Credit Losses

Our provision for credit losses relates primarily to single-family loans held-for-investment and can vary substantially from period to period based on a number of factors, such as changes in actual and forecasted house prices and interest rates, borrower prepayments and delinquency rates, events such as natural disasters or pandemics, the type and volume of our loss mitigation and foreclosure activity, government assistance provided to borrowers, and redesignation of loans between held-for-investment and held-for-sale. Our estimate of expected credit losses is particularly sensitive to changes in forecasted house price growth rates, which affect both the probability and severity of expected credit losses, and changes in forecasted interest rates, as lower (higher) interest rates typically result in higher (lower) expected prepayments and a shorter (longer) estimated loan life, and therefore lower (higher) expected credit losses. See Critical Accounting Policies and Estimates for additional information.

The table below presents the components of benefit (provision) for credit losses.

Table 10 - Components of Benefit (Provision) for Credit Losses

Change | Change | |||||||||||||||||||||||||

(Dollars in millions) | 2Q 2020 | 2Q 2019 | $ | % | YTD 2020 | YTD 2019 | $ | % | ||||||||||||||||||

Benefit (provision) for credit losses: | ||||||||||||||||||||||||||

Single-family | ($624 | ) | $161 | ($785 | ) | (488 | )% | ($1,790 | ) | $297 | ($2,087 | ) | (703 | )% | ||||||||||||

Multifamily | (81 | ) | (1 | ) | (80 | ) | (8,000 | ) | (148 | ) | (2 | ) | (146 | ) | (7,300 | ) | ||||||||||

Benefit (provision) for credit losses | ($705 | ) | $160 | ($865 | ) | (541 | )% | ($1,938 | ) | $295 | ($2,233 | ) | (757 | )% | ||||||||||||

Key Drivers:

n | Single-family |

l | 2Q 2020 vs. 2Q 2019 and YTD 2020 vs. YTD 2019 - Shifted to a provision primarily due to higher expected credit losses as a result of the negative economic effects of the COVID-19 pandemic. The higher expected credit losses during YTD 2020 were primarily driven by the following factors: |

– | Expected credit losses related to COVID-19 relief programs - Our provision for credit losses in YTD 2020 required significant management judgment to estimate the impact of COVID-19-related forbearance and relief programs on our expected credit losses. These judgments included estimates of the number of loans that will receive forbearance, the likely exit paths for loans in forbearance, and the number of loans where forbearance will be unsuccessful and the borrower will ultimately default. These factors resulted in a significant increase in our provision for credit losses for YTD 2020, with the majority of the increase occurring in 1Q 2020. In total, we have increased our allowance for credit losses for single-family mortgage loans held-for-investment by $2.1 billion as a result of the forbearance plans related to the COVID-19 pandemic. |

– | Changes in forecasted house price growth rates - The overall effect of forecasted house price changes on our provision for credit losses for YTD 2020 was relatively minor, with an increase in provision in 1Q 2020 being largely offset by the improvement in 2Q 2020. |

– | Declines in forecasted interest rates - The effect of the significant declines in mortgage interest rates during YTD 2020 partially offset the increase in the provision for credit losses as a result of the COVID-19 pandemic. |

n | Multifamily |

l | 2Q 2020 vs. 2Q 2019 and YTD 2020 vs. YTD 2019 - Increase in provision due to higher expected credit losses as a result of the negative economic effects of the COVID-19 pandemic. |

The decline in economic activity caused by the COVID-19 pandemic, and the corresponding government response, is unprecedented, and as a result, our estimate of expected credit losses is subject to significant uncertainty. See MD&A - Risk Management - Credit Risk for additional information.

Freddie Mac 2Q 2020 Form 10-Q | 19 | |

Management's Discussion and Analysis | Consolidated Results of Operations | |

Credit Enhancement Expense

Key Drivers:

n | 2Q 2020 vs. 2Q 2019 and YTD 2020 vs. YTD 2019 - Increased primarily due to higher outstanding volumes of CRT transactions. |

Expected Credit Enhancement Recoveries

Key Drivers:

n | 2Q 2020 vs. 2Q 2019 and YTD 2020 vs. YTD 2019 - Increase in expected recoveries from freestanding credit enhancements as a result of the corresponding increase in expected credit losses due to the COVID-19 pandemic. |

Other Comprehensive Income (Loss)

Key Drivers:

n | 2Q 2020 vs. 2Q 2019 - Decrease of $0.2 billion primarily driven by lower fair value gains on available-for-sale securities due to a smaller decline in long-term interest rates in 2Q 2020 compared to 2Q 2019. |

n | YTD 2020 vs. YTD 2019 - Remained relatively flat. |

Freddie Mac 2Q 2020 Form 10-Q | 20 | |

Management's Discussion and Analysis | Consolidated Balance Sheets Analysis | |

CONSOLIDATED BALANCE SHEETS ANALYSIS

The table below compares our summarized condensed consolidated balance sheets.

Beginning January 1, 2020, we elected to offset payables related to securities sold under agreements to repurchase against receivables related to securities purchased under agreements to resell when such amounts meet the conditions for balance sheet offsetting. Prior period amounts have been reclassified to conform to the current presentation. See Note 1 and Note 10 in this Form 10-Q for additional information.

Table 11 - Summarized Condensed Consolidated Balance Sheets

Change | |||||||||||||

(Dollars in millions) | June 30, 2020 | December 31, 2019 | $ | % | |||||||||

Assets: | |||||||||||||

Cash and cash equivalents | $7,605 | $5,189 | $2,416 | 47 | % | ||||||||

Securities purchased under agreements to resell | 100,525 | 56,271 | 44,254 | 79 | |||||||||

Subtotal | 108,130 | 61,460 | 46,670 | 76 | |||||||||

Investment securities, at fair value | 77,902 | 75,711 | 2,191 | 3 | |||||||||

Mortgage loans, net | 2,100,640 | 2,020,200 | 80,440 | 4 | |||||||||

Accrued interest receivable, net | 7,132 | 6,848 | 284 | 4 | |||||||||

Derivative assets, net | 1,402 | 844 | 558 | 66 | |||||||||

Deferred tax assets, net | 5,698 | 5,918 | (220 | ) | (4 | ) | |||||||

Other assets | 34,751 | 22,799 | 11,952 | 52 | |||||||||

Total assets | $2,335,655 | $2,193,780 | $141,875 | 6 | % | ||||||||

Liabilities and Equity: | |||||||||||||

Liabilities: | |||||||||||||

Accrued interest payable | $6,246 | $6,559 | ($313 | ) | (5 | )% | |||||||

Debt | 2,308,301 | 2,169,685 | 138,616 | 6 | |||||||||

Derivative liabilities, net | 839 | 372 | 467 | 126 | |||||||||

Other liabilities | 8,827 | 8,042 | 785 | 10 | |||||||||

Total liabilities | 2,324,213 | 2,184,658 | 139,555 | 6 | |||||||||

Total equity | 11,442 | 9,122 | 2,320 | 25 | |||||||||

Total liabilities and equity | $2,335,655 | $2,193,780 | $141,875 | 6 | % | ||||||||

Key Drivers:

As of June 30, 2020 compared to December 31, 2019:

n | Cash and cash equivalents and securities purchased under agreements to resell increased on a combined basis primarily due to higher near-term cash needs for upcoming debt maturities and anticipated calls of other debt and a higher expected single-family cash loan purchase forecast. In addition, our custodial trust account balance increased due to higher loan prepayments. |

n Derivative assets, net and derivative liabilities, net increased primarily due to significant changes in the fair value of forward commitments to purchase and sell mortgage loans and mortgage-related securities.

n Other assets increased primarily due to higher servicer receivables driven by an increase in mortgage loan payoffs reported but not yet remitted at the end of 2Q 2020.

Freddie Mac 2Q 2020 Form 10-Q | 21 | |

Management's Discussion and Analysis | Our Business Segments | Segment Earnings | |

OUR BUSINESS SEGMENTS

We have three reportable segments, which are based on the way we manage our business.

n | Single-Family Guarantee - Reflects results from our purchase, securitization, and guarantee of single-family loans and the management of single-family mortgage credit risk. |

n | Multifamily - Reflects results from our purchase, sale, securitization, and guarantee of multifamily loans and securities, our investments in those loans and securities, and the management of multifamily mortgage credit risk and market risk. |

n | Capital Markets - Reflects results from managing our mortgage-related investments portfolio (excluding Multifamily segment investments, single-family seriously delinquent loans, and the credit risk of single-family performing and reperforming loans), single-family securitization activities, and treasury function, which includes interest-rate risk management for the company. |

Certain activities that are not part of a reportable segment, such as material corporate-level activities that are infrequent in nature and based on decisions outside the control of the management of our reportable segments, are included in the All Other category.

Segment Earnings

We present Segment Earnings by reclassifying certain credit guarantee-related activities and investment-related activities between various line items on our GAAP condensed consolidated statements of comprehensive income (loss) and allocating certain revenues and expenses to our three reportable segments. For more information on our segment reclassifications, see Note 13.

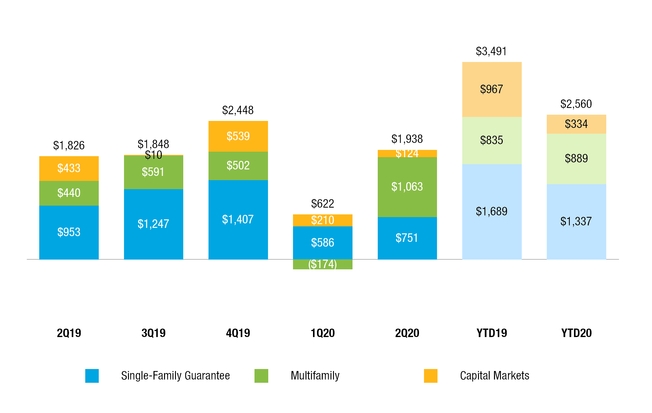

Segment Comprehensive Income (Loss)

The graph below shows our comprehensive income (loss) by segment.

(In millions)

Freddie Mac 2Q 2020 Form 10-Q | 22 | |

Management's Discussion and Analysis | Our Business Segments | Single-Family Guarantee |

Single-Family Guarantee

Business Results

The following tables, graphs, and related discussion present the business results of our Single-family Guarantee segment.

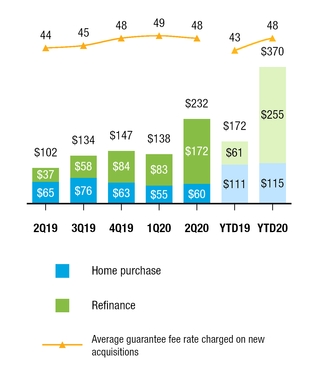

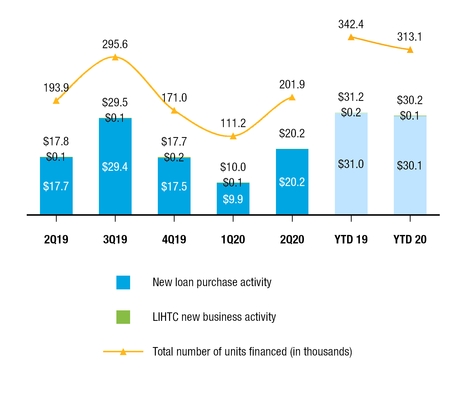

New Business Activity

UPB of Single-Family Loan Purchases and Guarantees by Loan Purpose and Average Guarantee Fee Rate (1) Charged on New Acquisitions

(UPB in billions, guarantee fee in bps)

(1) Guarantee fee excludes legislated 10 basis point increase.

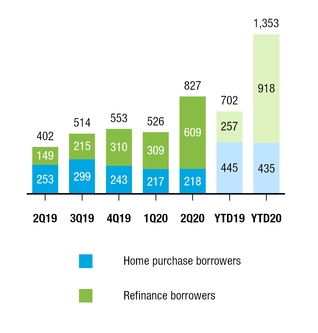

(1) Guarantee fee excludes legislated 10 basis point increase.Number of Families Helped to Own a Home

(In thousands)

2Q 2020 vs. 2Q 2019 and YTD 2020 vs. YTD 2019

n | Our loan purchase and guarantee activity increased, primarily due to higher refinance activity driven by the declining average mortgage interest rates in recent quarters. |

n | The average guarantee fee rate charged on new acquisitions increased, primarily due to an increase in contractual guarantee fees and an enhancement in our estimation methodology related to recognition of buy-up fees in 2Q 2019. |

n | Home sales fell in 2Q 2020 as a result of the COVID-19 pandemic. The housing market, however, has shown signs of recovery, with purchase applications increasing significantly since early 2Q 2020 and mortgage rates at record lows. The low mortgage rate environment, which led to a significant increase in mortgage refinance activity in the first half of 2020, is expected to continue and result in high levels of mortgage refinance activity for full-year 2020, before declining in 2021. However, due to the impact of the COVID-19 pandemic, we expect full-year home sales to fall in 2020 and then begin to rebound in 2021. While house prices increased at a solid pace during 1Q 2020, full-year house price growth is expected to slow in 2020 and 2021. |

Freddie Mac 2Q 2020 Form 10-Q | 23 | |

Management's Discussion and Analysis | Our Business Segments | Single-Family Guarantee |

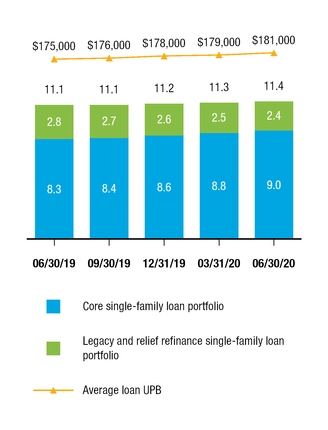

Single-Family Credit Guarantee Portfolio

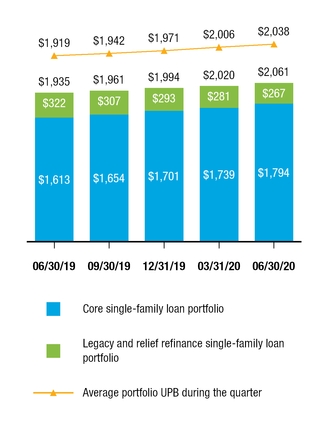

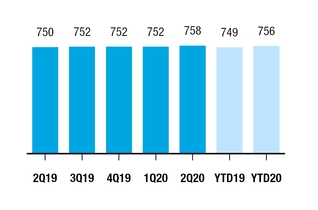

Single-Family Credit Guarantee Portfolio Single-Family Loans

(UPB in billions) (Loan count in millions)

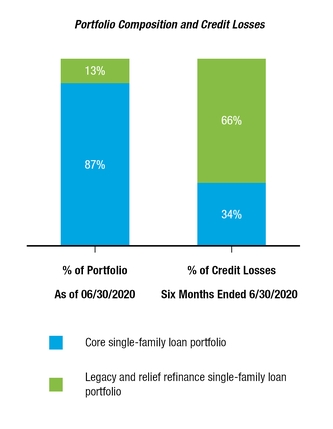

n | The single-family credit guarantee portfolio increased at an annualized rate of approximately 7% between December 31, 2019 and June 30, 2020, driven by an increase in U.S. single-family mortgage debt outstanding and a higher GSE share of the total market. Additionally, continued house price appreciation contributed to new business acquisitions having a higher average loan size compared to older vintages that continued to run off. |

n | As we continued to purchase new loans, our core single-family loan portfolio grew to 87% of the single-family credit guarantee portfolio at June 30, 2020, compared to 85% at December 31, 2019. Our legacy and relief refinance single-family loan portfolio, which generally has a lower credit profile, continued to run off, declining to 13% of the single-family credit guarantee portfolio at June 30, 2020, compared to 15% at December 31, 2019. |