Exhibit 99.1

For Further Information:

Simulations Plus, Inc.

42505 10th Street West

Lancaster, CA 93534-7059

| CONTACT: | |

| Simulations Plus Investor Relations | Hayden IR |

| Ms. Renee Bouche | Mr. Cameron Donahue |

| 661-723-7723 | 651-653-1854 |

| renee@simulations-plus.com | cameron@haydenir.com |

For Immediate Release:

July 14, 2016

Simulations Plus Reports Third Quarter FY2016 Financial Results

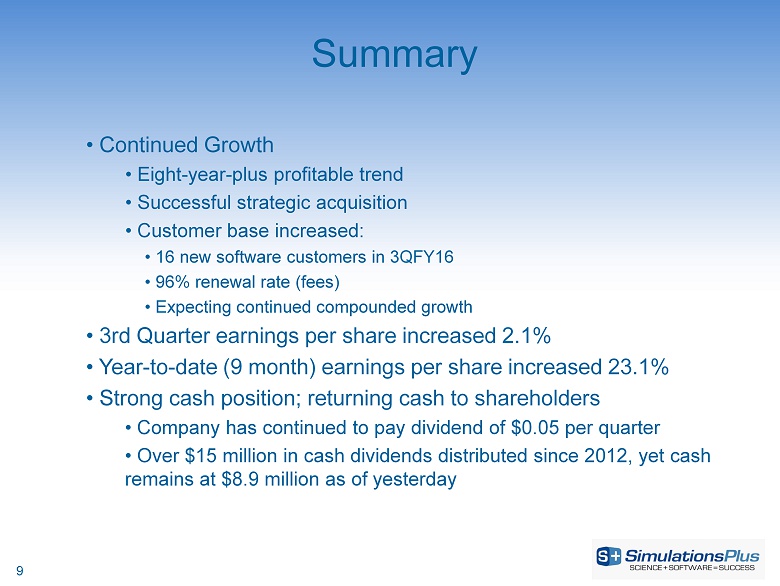

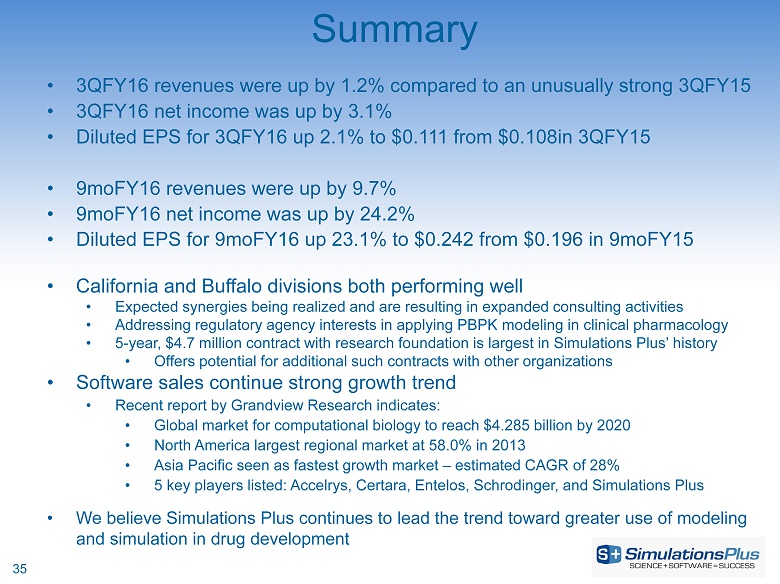

Record quarterly revenue, 9moFY16 diluted EPS increased 23% to a record $0.242 from $0.196

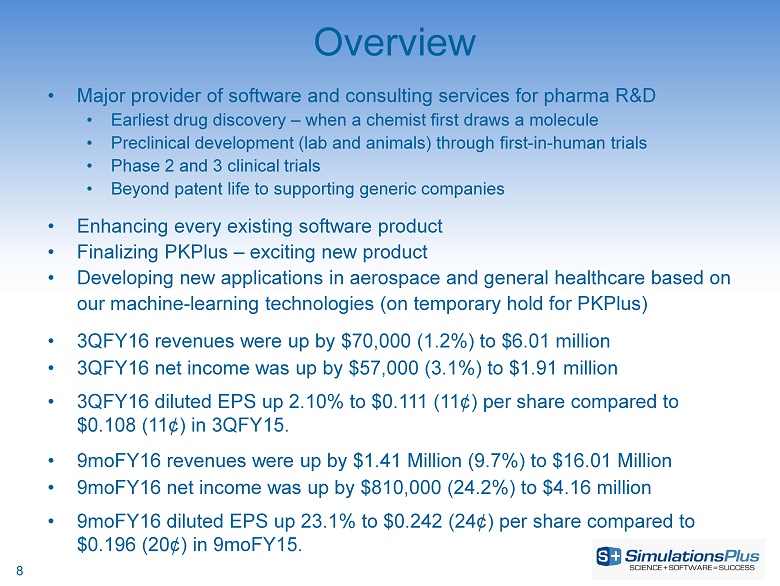

LANCASTER, CA, July 14, 2016 – Simulations Plus, Inc. (NASDAQ: SLP), the premier provider of simulation and modeling software and consulting services for pharmaceutical discovery and development from the earliest discovery through all phases of clinical trials, today reported financial results for its third quarter of fiscal year 2016 (3QFY16) and the first nine months of fiscal year 2016 (9moFY16), the period ended May 31, 2016.

3QFY16 highlights compared with 3QFY15:

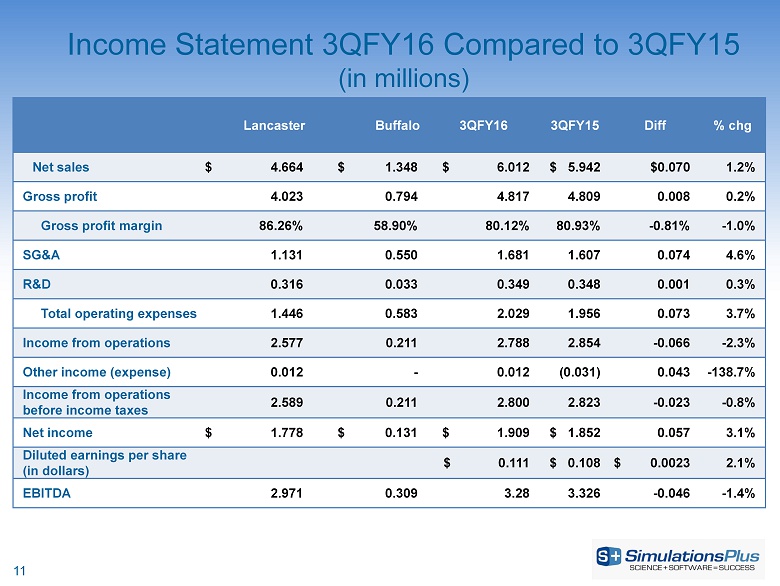

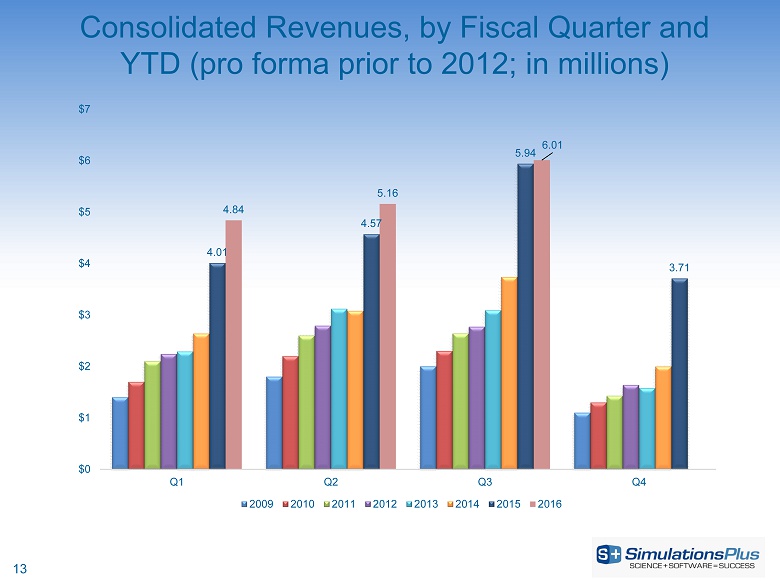

| · | Net revenues increased 1.2% to $6.01 million, an increase of $70,000 from $5.94 million |

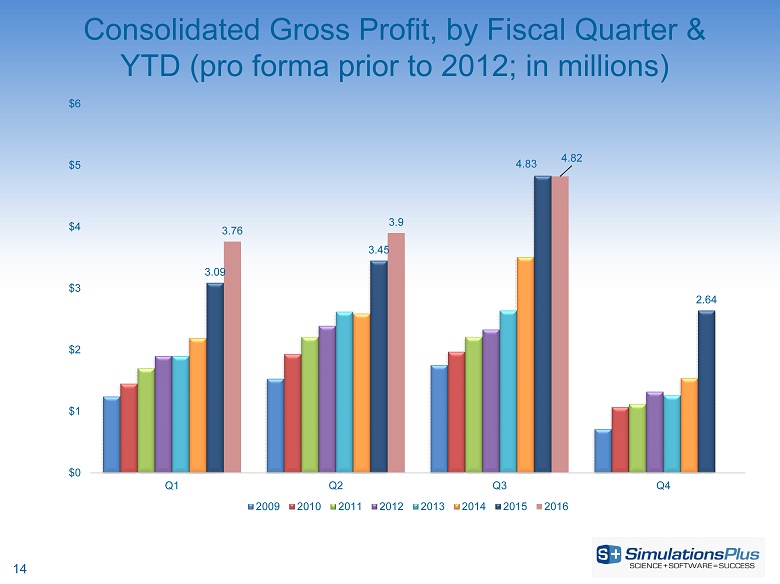

| · | Gross profit was up 0.2% to $4.82 million, an increase of $8,000 from $4.81 million |

| · | SG&A was $1.68 million, an increase of 4.6% or $73,000 from $1.61 million |

| · | R&D expenditures were $617,000, an increase of $23,000, or 3.8% over $594,000 |

| o | In 3QFY16, $269,000 was capitalized and $348,000 was expensed |

| o | In 3QFY15, $246,000 was capitalized and $348,000 was expensed |

| · | Income before taxes decreased 0.8% to $2.80 million, a decrease of $22,000 from $2.82 million |

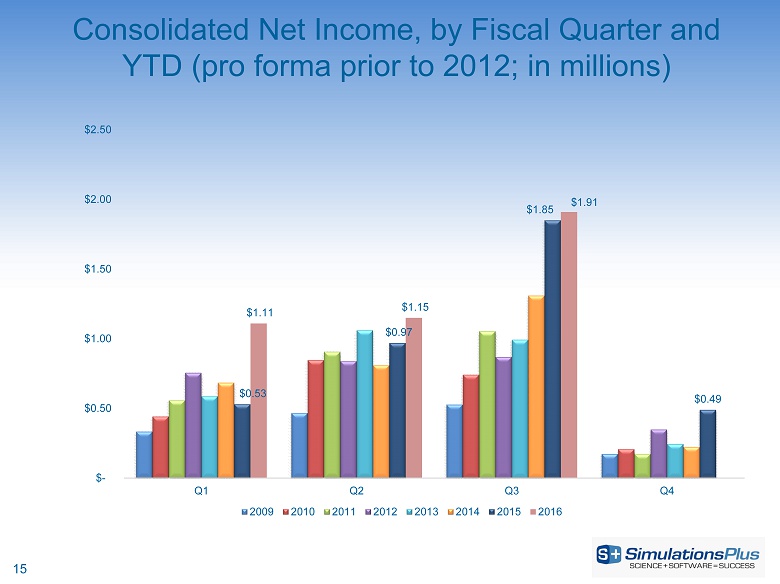

| · | Net income increased 3.1% to $1.91 million, an increase of $57,000 from $1.85 million |

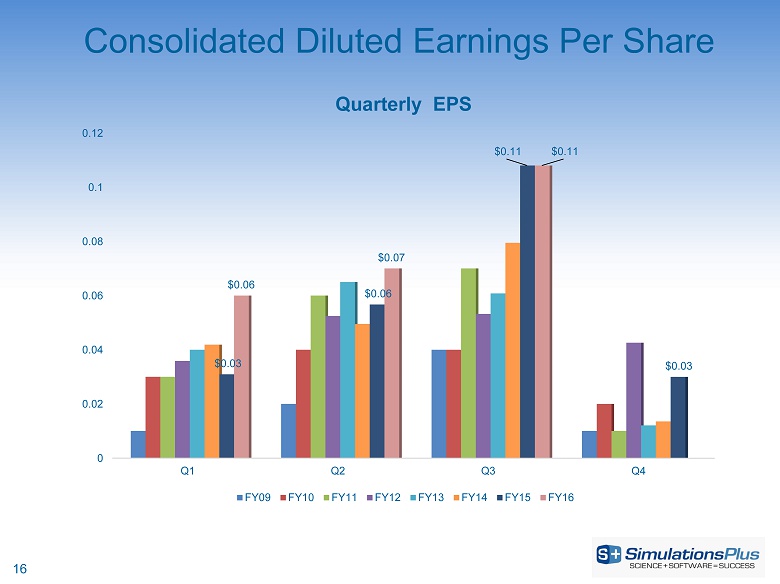

| · | Diluted earnings per share increased 2.1% to $0.111 from $0.108 |

9moFY16 highlights compared with 9moFY15:

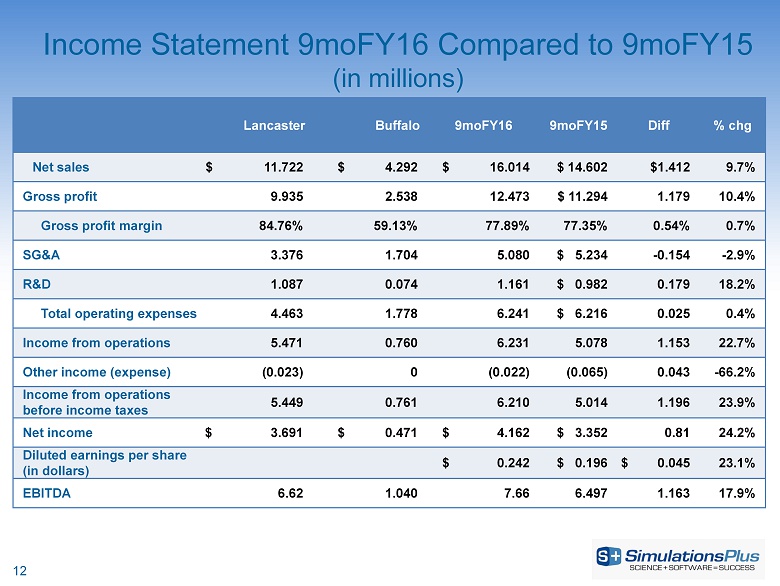

| · | Net revenues increased 9.7% to $16.01 million, an increase of $1.41 million from $14.60 million |

| · | Gross profit was up 10.4% to $12.47 million, an increase of $1.18 million from $11.29 million |

| · | SG&A was $5.08 million, a decrease of $154,000, or 2.9%, from $5.23 million |

| · | R&D expenditures were $1.974 million, an increase of $17,000, or 0.9% over $1.957 million |

| o | For 9moFY16, $814,000 was capitalized and $1.16 million was expensed |

| o | For 9moFY15, $976,000 was capitalized and $982,000 was expensed |

| · | Income before taxes increased 23.9% to $6.21 million, an increase of $1.2 million from $5.01 million |

| · | Net income increased 24.2% to $4.16 million, an increase of $810,000 from $3.35 million |

| · | Diluted earnings per share increased 23.1% to $0.242 from $0.196 |

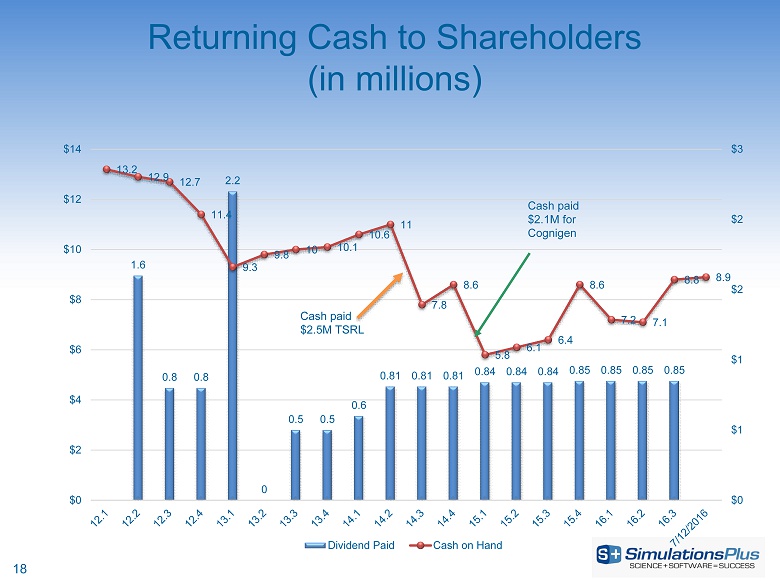

John Kneisel, chief financial officer of Simulations Plus, said: “The Company continues to produce record financial results, with year-to-date sales up nearly 10% and net income increased by 24%, speaking to our operational efficiency and demonstrating the leverage inherent in our business model. The Company’s strong cash position enables continuing investment in software products while being able to reward shareholders by providing continuing quarterly dividends. As always, such distributions are at the discretion of the Board of Directors.”

| 1 |

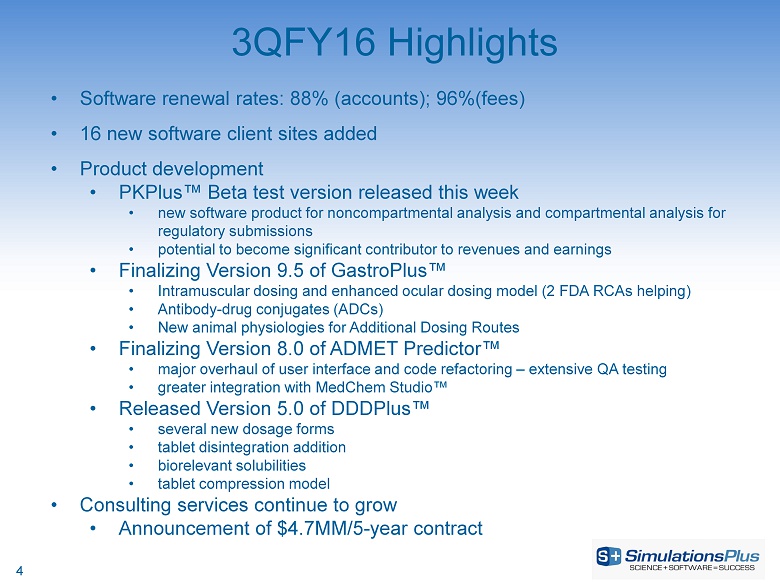

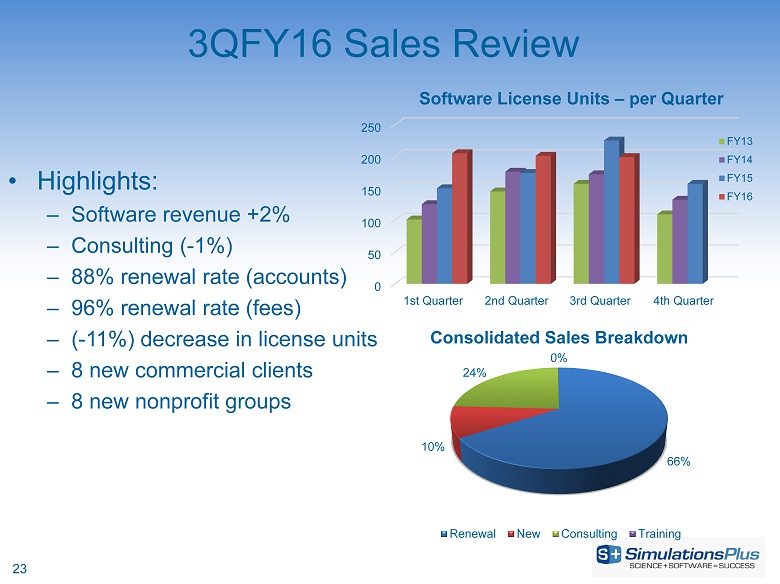

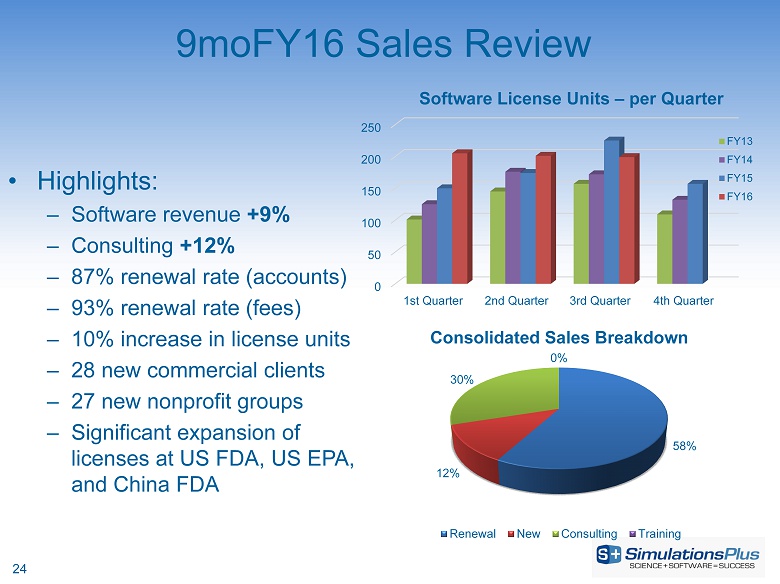

John DiBella, vice president for marketing and sales of Simulations Plus, said: “While revenue growth for 3QFY16 was lower than our historical averages, it is compared with an exceptionally strong third quarter in FY15. We executed on several fronts and achieved the highest quarter in our history for both revenues and earnings. Software renewal rates exceeded 88% (accounts) and 96% (fees) for the quarter, and we added 16 new clients, with several coming from India. The first nine months of FY2016 have shown strong growth trends in both software and consulting services revenue, and along with the imminent release of our new PKPlus™ software, we have a full pipeline of new contracts keeping our experts busy as we move towards FY2017. We believe our aggressive marketing and training programs, coupled with positive underlying sales fundamentals, set us up nicely to end FY2016 on a strong note.”

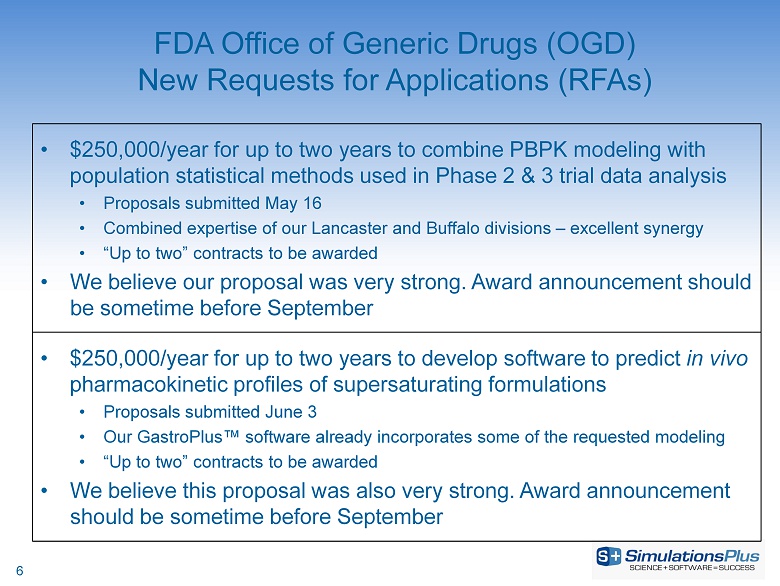

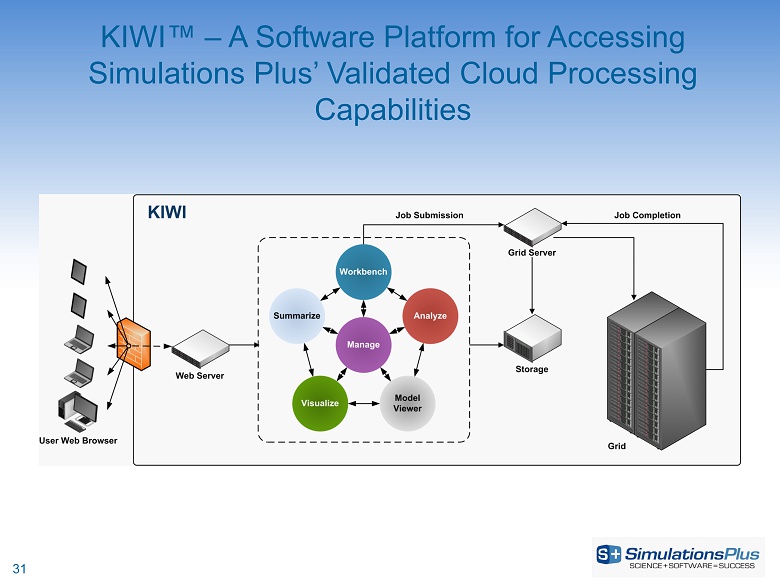

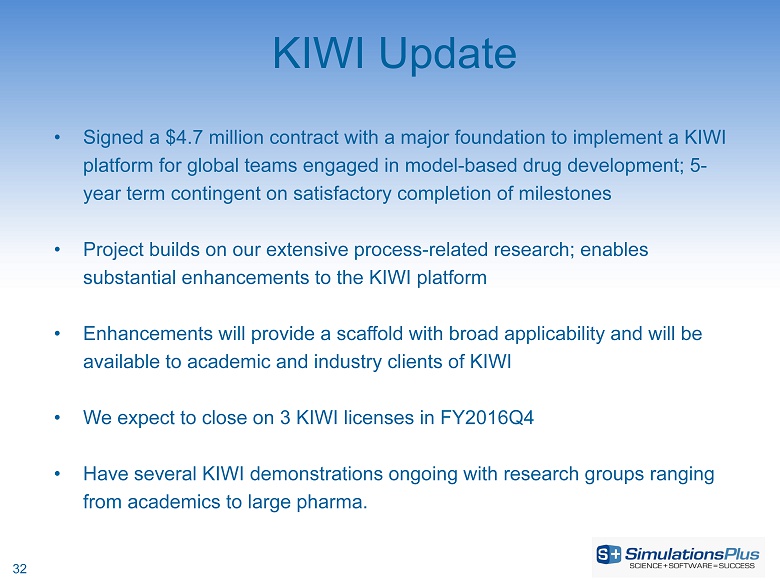

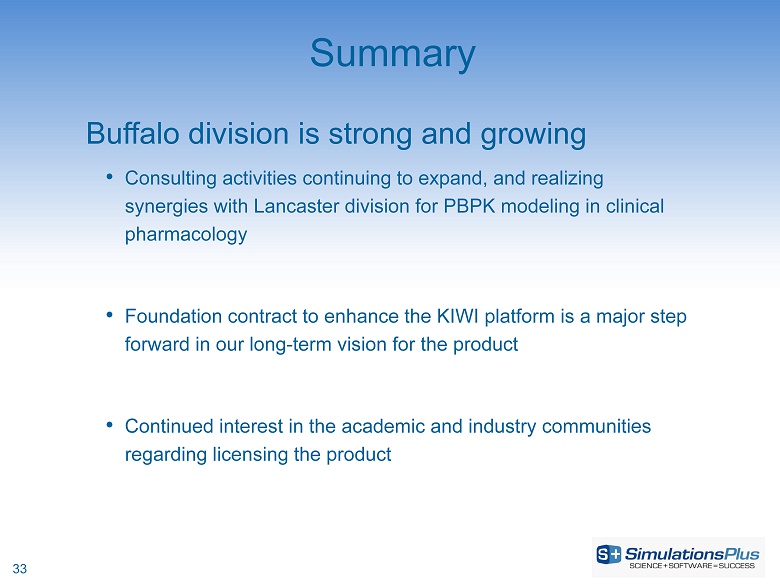

Ted Grasela, president of Simulations Plus, added: “The recently announced 5-year, $4.7 million contract to expand and further develop the KIWI™ software platform for a major research foundation is expected to add significantly to the revenue growth of our Buffalo division. We believe this effort, which is based on our secure in-house computing cloud, has the potential to lead to additional opportunities for such services, both with this foundation and with pharmaceutical companies and other research organizations around the world. In addition, we are now routinely providing physiologically based pharmacokinetics (PBPK) analysis to clinical pharmacology groups as we have realized the expected synergies between our Lancaster and Buffalo divisions.”

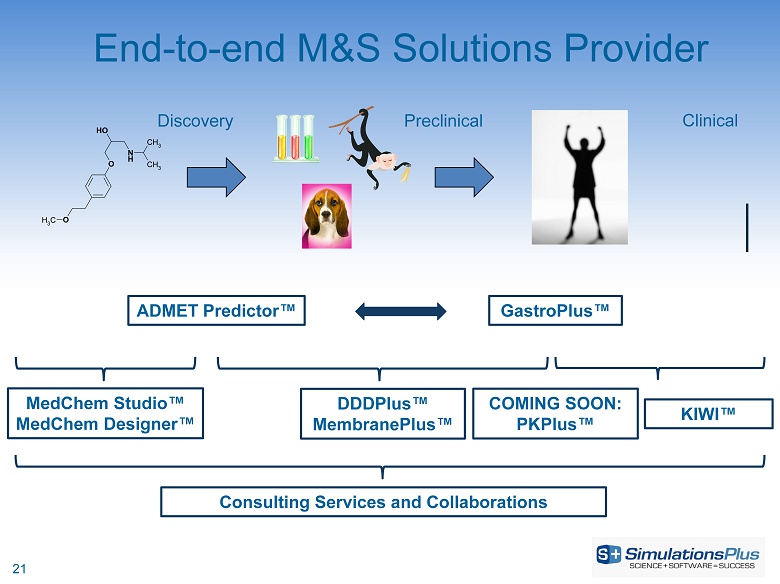

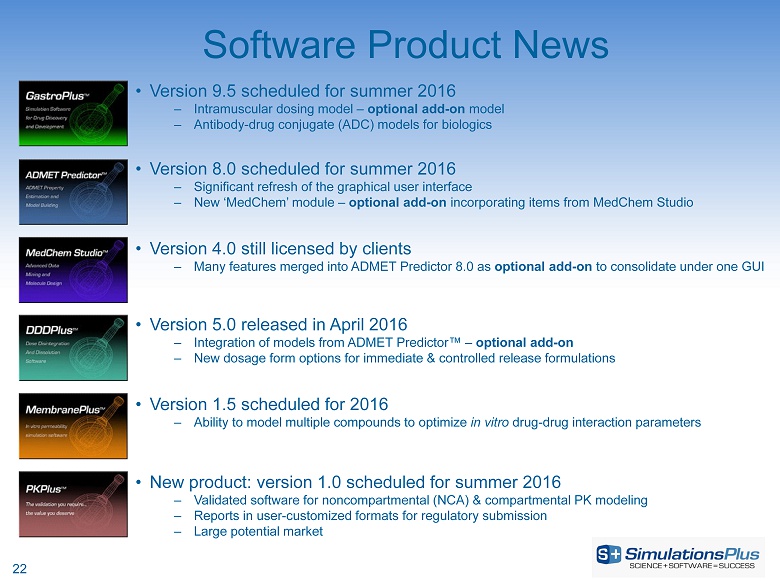

Walt Woltosz, chairman and chief executive officer of Simulations Plus, concluded: “This month marks the 20th anniversary of Simulations Plus. Driving the evolution of the pharmaceutical industry over the past two decades from minimal use of simulation and modeling to widespread adoption by industry and regulatory agencies has been very satisfying. As John DiBella noted, our nine-month results demonstrate excellent continued revenues and earnings growth. Now we are beginning to perform on our five-year contract and expecting the release of our newest software product, PKPlus™, along with updates to GastroPlus™ and ADMET Predictor™, all in the fourth fiscal quarter. We’re excited about these developments and expect them to contribute to a strong finish to FY2016.”

Investor Conference Call

The Company will host a conference call on July 14, 2016, at 4:15 p.m. Eastern Time. All interested parties are invited to join the call by registering at this link. On registering, you will receive a confirmation e-mail with instructions for joining the call. Please dial in five to ten minutes prior to the scheduled start time. For listen-only mode, you may dial (213) 929-4232, and enter access code 790-046-526.

About Simulations Plus, Inc.

Simulations Plus, Inc. is a premier developer of drug discovery and development software as well as a leading provider of both preclinical and clinical pharmacometric consulting services for regulatory submissions. The company is a global leader focused on improving the ways scientists use knowledge and data to predict the properties and outcomes of pharmaceutical and biotechnology agents. Our software is licensed to and used in the conduct of drug research by major pharmaceutical and biotechnology companies and regulatory agencies worldwide. Our innovations in integrating new and existing science in medicinal chemistry, computational chemistry, pharmaceutical science, biology, and physiology into our software have made us the leading software provider for physiologically based pharmacokinetic modeling and simulation. For more information, visit our website at www.simulations-plus.com.

Follow Us on Twitter

Safe Harbor Statement Under the Private Securities Litigation Reform Act of 1995 – With the exception of historical information, the matters discussed in this press release are forward-looking statements that involve a number of risks and uncertainties. Words like “believe,” “expect” and “anticipate” mean that these are our best estimates as of this writing, but that there can be no assurances that expected or anticipated results or events will actually take place, so our actual future results could differ significantly from those statements. Factors that could cause or contribute to such differences include, but are not limited to: our ability to maintain our competitive advantages, acceptance of new software and improved versions of our existing software by our customers, the general economics of the pharmaceutical industry, our ability to finance growth, our ability to continue to attract and retain highly qualified technical staff, our ability to identify and close acquisitions on terms favorable to the Company, and a sustainable market. Further information on our risk factors is contained in our quarterly and annual reports as filed with the U.S. Securities and Exchange Commission.

| 2 |

SIMULATIONS PLUS, INC.

CONDENSED CONSOLIDATED BALANCE SHEETS

As of

| (Unaudited) | (Audited) | |||||||

| May 31, | August 31, | |||||||

| ASSETS | ||||||||

| 2016 | 2015 | |||||||

| Current assets | ||||||||

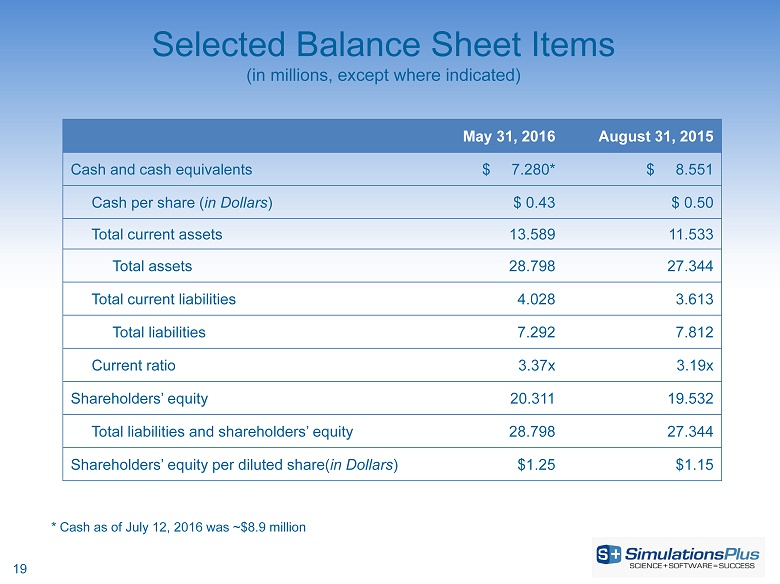

| Cash and cash equivalents | $ | 7,279,683 | $ | 8,551,275 | ||||

| Accounts receivable, net of allowance for doubtful accounts of $0 | 4,582,573 | 1,593,707 | ||||||

| Revenues in excess of billings | 1,039,897 | 795,125 | ||||||

| Prepaid income taxes | 108,690 | – | ||||||

| Prepaid expenses and other current assets | 288,164 | 381,718 | ||||||

| Deferred income taxes | 289,835 | 210,972 | ||||||

| Total current assets | 13,588,842 | 11,532,797 | ||||||

| Long-term assets | ||||||||

| Capitalized computer software development costs, net of accumulated amortization of $8,368,000 and $7,632,421 | 3,878,342 | 3,798,339 | ||||||

| Property and equipment, net | 297,385 | 413,510 | ||||||

| Intellectual property, net of accumulated amortization of $1,256,875 and $801,250 | 4,818,125 | 5,273,750 | ||||||

| Other intangible assets net of accumulated amortization of $258,125 and $147,500 | 1,391,875 | 1,502,500 | ||||||

| Goodwill | 4,789,248 | 4,789,248 | ||||||

| Other assets | 34,082 | 34,082 | ||||||

| Total assets | $ | 28,797,899 | $ | 27,344,226 | ||||

| LIABILITIES AND SHAREHOLDERS' EQUITY | ||||||||

| Current liabilities | ||||||||

| Accounts payable | $ | 184,996 | $ | 209,407 | ||||

| Accrued payroll and other expenses | 510,792 | 429,580 | ||||||

| Accrued bonuses to officers | 90,750 | 121,000 | ||||||

| Income taxes payable | – | 43,602 | ||||||

| Other current liabilities | 13,239 | 19,859 | ||||||

| Current portion - Contracts payable | 2,854,404 | 2,604,404 | ||||||

| Billings in excess of revenues | 112,445 | 106,534 | ||||||

| Deferred revenue | 261,266 | 78,945 | ||||||

| Total current liabilities | 4,027,892 | 3,613,331 | ||||||

| Long-term liabilities | ||||||||

| Deferred income taxes | 3,264,372 | 3,190,419 | ||||||

| Payments due under Contracts payable | – | 1,000,000 | ||||||

| Other long-term liabilities | – | 8,274 | ||||||

| Total liabilities | $ | 7,292,264 | $ | 7,812,024 | ||||

| Commitments and contingencies | ||||||||

| Shareholders' equity | ||||||||

| Preferred stock, $0.001 par value 10,000,000 shares authorized no shares issued and outstanding | $ | – | $ | – | ||||

| Common stock, $0.001 par value 50,000,000 shares authorized 17,032,364 and 16,943,001 shares issued and outstanding | 5,504 | 5,414 | ||||||

| Additional paid-in capital | 10,078,647 | 9,714,290 | ||||||

| Retained earnings | 11,421,484 | 9,812,498 | ||||||

| Total shareholders' equity | $ | 21,505,635 | $ | 19,532,202 | ||||

| Total liabilities and shareholders' equity | $ | 28,797,899 | $ | 27,344,226 | ||||

| 3 |

SIMULATIONS PLUS, INC.

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

For the three and nine months ended May 31,

| Three months ended | Nine months ended | |||||||||||||||

| (Unaudited) | (Unaudited) | |||||||||||||||

| 2016 | 2015 | 2016 | 2015 | |||||||||||||

| Net Revenues | $ | 6,012,193 | $ | 5,942,082 | $ | 16,014,539 | $ | 14,602,464 | ||||||||

| Cost of revenues | 1,194,815 | 1,132,695 | 3,541,903 | 3,308,277 | ||||||||||||

| Gross margin | 4,817,378 | 4,809,387 | 12,472,636 | 11,294,187 | ||||||||||||

| Operating expenses | ||||||||||||||||

| Selling, general, and administrative | 1,680,707 | 1,607,317 | 5,079,985 | 5,234,311 | ||||||||||||

| Research and development | 348,427 | 348,285 | 1,161,124 | 981,633 | ||||||||||||

| Total operating expenses | 2,029,134 | 1,955,602 | 6,241,109 | 6,215,944 | ||||||||||||

| Income from operations | 2,788,244 | 2,853,785 | 6,231,527 | 5,078,243 | ||||||||||||

| Other income (expense) | ||||||||||||||||

| Interest income | 4,553 | 4,391 | 13,507 | 13,394 | ||||||||||||

| Gain(loss) on currency exchange | 7,733 | (35,632 | ) | (35,490 | ) | (78,107 | ) | |||||||||

| Total other income (expense) | 12,286 | (31,241 | ) | (21,983 | ) | (64,713 | ) | |||||||||

| Income from operations before provision for income taxes | 2,800,530 | 2,822,544 | 6,209,544 | 5,013,530 | ||||||||||||

| Provision for income taxes | (891,191 | ) | (970,122 | ) | (2,048,383 | ) | (1,661,972 | ) | ||||||||

| Net Income | $ | 1,909,339 | $ | 1,852,422 | $ | 4,161,161 | $ | 3,351,558 | ||||||||

| Earnings per share | ||||||||||||||||

| Basic | $ | 0.11 | $ | 0.11 | $ | 0.24 | $ | 0.20 | ||||||||

| Diluted | $ | 0.11 | $ | 0.11 | $ | 0.24 | $ | 0.20 | ||||||||

| Weighted-average common shares outstanding | ||||||||||||||||

| Basic | 17,028,634 | 16,862,128 | 17,000,228 | 16,847,191 | ||||||||||||

| Diluted | 17,227,540 | 17,073,155 | 17,219,835 | 17,070,334 | ||||||||||||

| 4 |