Moderator: Jeffrey Coats

11-05-14/2:00 p.m. ET

Confirmation # 23506766

Page 1

AUTOBYTEL INC.

Moderator: Jeffrey Coats

November 5, 2014

2:00 p.m. ET

|

Operator:

|

Good day, ladies and gentlemen, and welcome to the Autobytel Announces 2014 Third Quarter Financial Results. At this time, all participants are in a listen-only mode. Later, we will conduct the question-and-answer session, and instructions will follow at that time.

|

|

|

If anyone should require assistance during the conference, please press star then zero on your touch-tone telephone.

|

|

|

As a reminder this conference is being recorded.

|

|

|

I would like to introduce your host for today’s conference, Mr. Roger Pondel, Investor Relations of Autobytel. Sir, you may begin.

|

|

Roger Pondel:

|

Thank you, operator, and hello everyone. Welcome to Autobytel’s 2014 third quarter earnings conference call. Presenting today are Jeff Coats, President and Chief Executive Officer, and Curt DeWalt, Senior Vice President and Chief Financial Officer.

|

|

|

Before I introduce Jeff, I remind you that during today’s call, including the question-and-answer session, any projections and forward-looking statements made regarding future events or Autobytel’s future financial performance are covered by the Safe Harbor statements contained in today’s press release, the slides accompanying this presentation and the company’s public filings with the SEC. Actual events may differ materially from those forward-looking statements.

|

|

|

Specifically, please refer to the company’s Form 10-Q for the period ended September 30, 2014, which was filed just prior to this call, as well as other filings made from time-to-time by Autobytel with the SEC. These filings identify factors that could cause results to differ materially from those forward-looking statements.

|

|

|

There are slides included with today’s presentation to help illustrate some of the points being made and discussed during the call. The slides can be accessed by clicking on the link in today’s press release or by visiting Autobytel’s website at www.autobytel.com, and when there, go to Investor Relations and then click on Events & Presentations.

|

AUTOBYTEL INC.

Moderator: Jeffrey Coats

11-05-14/2:00 p.m. ET

Confirmation # 23506766

Page 2

|

|

Please also note that during this call and/or in accompanying slides, management will be discussing EBITDA, adjusted EBITDA, adjusted EBITDA per diluted share, non-GAAP income, and non-GAAP EPS, which are non-GAAP financial measures as defined by SEC Regulation G. Reconciliations of these non-GAAP financial measures to the most directly comparable GAAP measures are included in today’s press release and/or in the slides which are posted on the company’s website.

And with that, I will now turn the call over to Jeff. Jeff?

|

|

Jeffrey Coats:

|

Thank you, Roger. Good afternoon, everyone. Before I discuss our successful third quarter results, I’m going to take a step back to highlight how far Autobytel has come since December 2008, when the new management team took over:

|

|

·

|

I’ll start with profitability. Autobytel was only profitable in 2 of the 13 years that the company was in operation before I joined as CEO in December 2008, and those two years were 2003 and 2004. However, since 2008 (a year during which the company loss $80 million), the company has generated a profit in four of the last six years from 2011 through today.

|

|

·

|

Likewise, we have generated positive cash flow in four of the last six years from 2011 through today, we have produced more than $18 million in cash flow from operations.

|

|

·

|

We’ve had a successful history of acquisitions, most notably with Cyber Ventures in 2010. This transformative transaction resulted in higher dealer close rates, higher lead volumes delivered and higher margins. It also cemented Autobytel’s position as the largest automotive lead provider in the United States and the largest wholesale provider in the country.

|

|

·

|

Since 2008, internally-generated leads have grown from just 3% of our total lead supply to about 70% today. In addition, we’ve gone from delivering 3 million leads to our customers in 2009 to approximately 6.5 million this year. Concurrently, we’ve driven gross margin expansion from less than 30% to approximately 40%.

|

From pretty much every operational and financial measure, we are much stronger today with solid prospects to help us continue growing into the future.

|

|

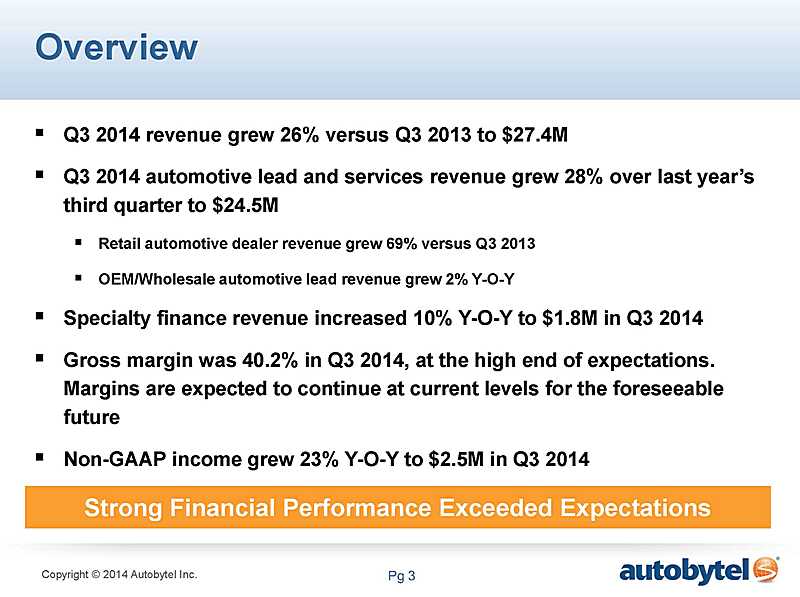

Now, I’ll discuss our strong third quarter financial performance. Year-over-year revenue growth of more than 26%, gross margins greater than 40% and solid profitability, exceeded our expectations.

|

AUTOBYTEL INC.

Moderator: Jeffrey Coats

11-05-14/2:00 p.m. ET

Confirmation # 23506766

Page 3

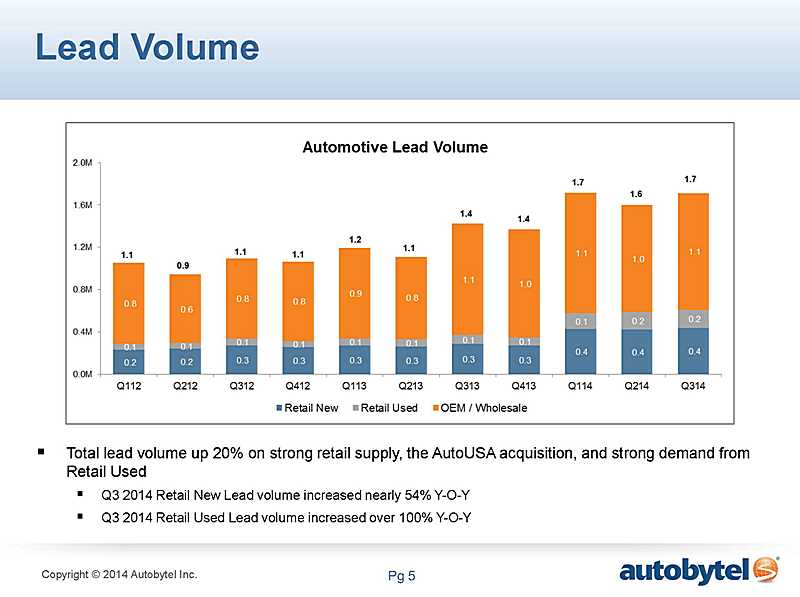

Our core leads business strengthened, while AutoUSA continued to be a meaningful contributor, resulting in total lead volume growth of 20%.

|

|

Retail new car lead volume increased 54% and retail used car lead volume more than doubled. As we continue to focus our energies on providing our customers with the highest quality and highest converting leads possible, in innovative, value-added products and services, we were enthusiastic about our continued success and about future growth opportunities.

|

|

|

After Curt’s financial review of the quarter, I will update you on our progress.

|

|

Curt DeWalt:

|

Thank you, Jeff.

|

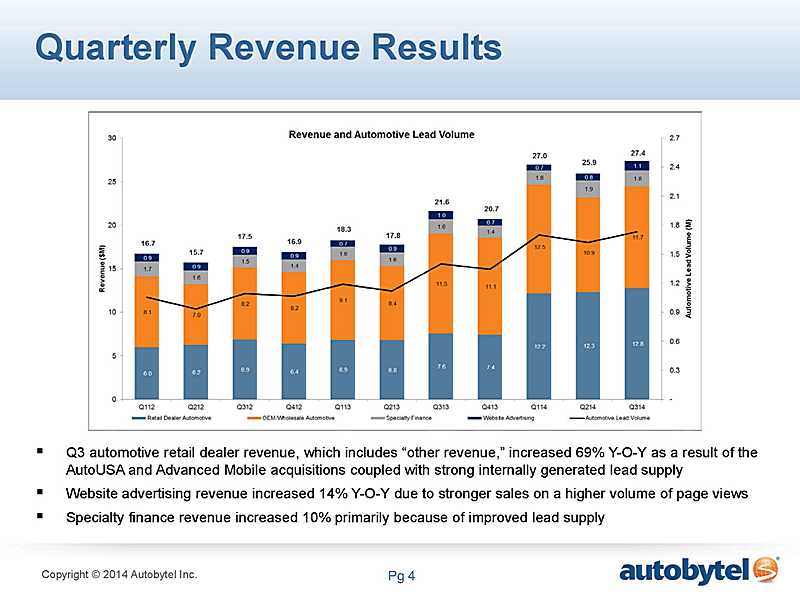

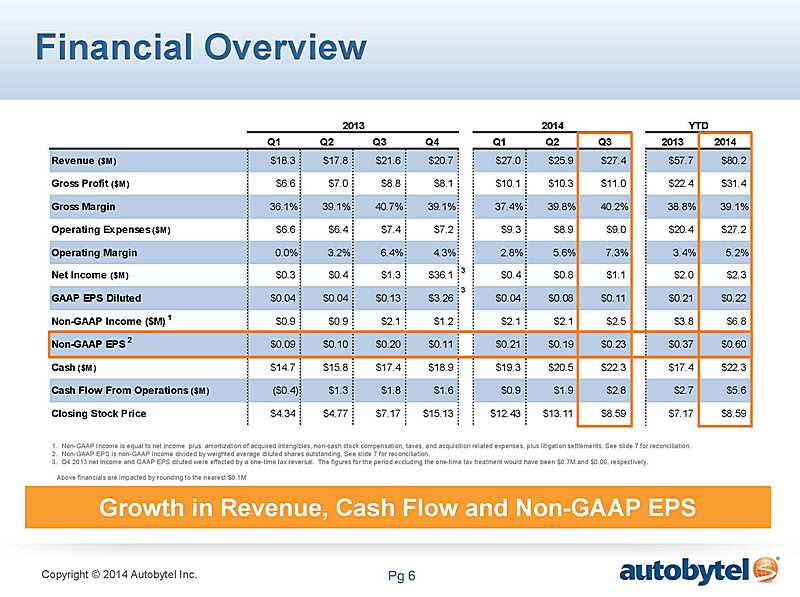

On Slide 4, you can see the total revenues increased to $27.4 million for the third quarter of 2014, up from $21.6 million last year. Revenues from automotive leads and services grew 28% over last year’s third quarter. Retail channel sales rose 69%, and wholesale channel sales increased 2%. Retail channels benefited from our acquisitions of AutoUSA and Advanced Mobile, strong internally-generated lead supply and increases in our average selling price.

|

|

Advertising revenues were $1.1 million for the third quarter of 2014, up more than 43% on a sequential basis and more than 14% compared with last year, as we continued to optimize our relationship with Jumpstart, and generated a higher volume of page views. Page views have almost doubled versus the third quarter of 2013.

|

|

|

The reason for the increase in page views is two-fold. First, we generated an increase in traffic a primary driver of which was Google’s Panda released in May, which was designed to help boost quality content sites like Autobytel.com. Second, page views per visit increased as a result of our continued optimization of content to provide users with a more engaging experience on our sites, demonstrating the effectiveness of our ongoing content and video investments.

|

|

|

Moving now to Slide 5, you will see that we delivered approximately 1.7 million automotive leads during the 2014 third quarter, a 20% increase over last year. 64% of the leads were delivered to the wholesale channel customers, with the remaining 36% to retail channel customers. Our used car leads business continued to grow with more than a 100% increase in leads delivered in the third quarter of 2014, versus last year.

|

|

|

We delivered a 104,000 specialty finance leads during the 2014 third quarter, up from 88,000 in the corresponding period a year ago, reflecting continuing efforts to ease supply constraints. Specialty finance lead revenue grew to $1.8 million for the third quarter of 2014, from $1.6 million last year.

|

AUTOBYTEL INC.

Moderator: Jeffrey Coats

11-05-14/2:00 p.m. ET

Confirmation # 23506766

Page 4

|

|

On Slide 6, you’ll note an approximate 25% improvement in gross profit, which grew to $11.0 million for the 2014 third quarter, from $8.8 million last year. Gross margin was 40.2% of total revenues for the 2014 third quarter, compared with 39.8% of total revenues for the 2014 second quarter, and 40.7% one year ago. The sequential improvement continues to reflect the delivery of a higher percentage of internally-generated leads being delivered to previous AutoUSA dealers, and improved lead pricing from our outside suppliers for these dealers. We expect margins to remain in a similar range for the foreseeable future.

|

|

|

Total operating expenses were $9.0 million or 32.9% of total revenues, for the 2014 third quarter, compared with $7.4 million or 34.3% of total revenues for the same quarter last year. The majority of the dollar increase related to sales and marketing expenses associated with the acquisitions of AutoUSA and Advanced Mobile, as well as activities related to SaleMove program.

|

|

|

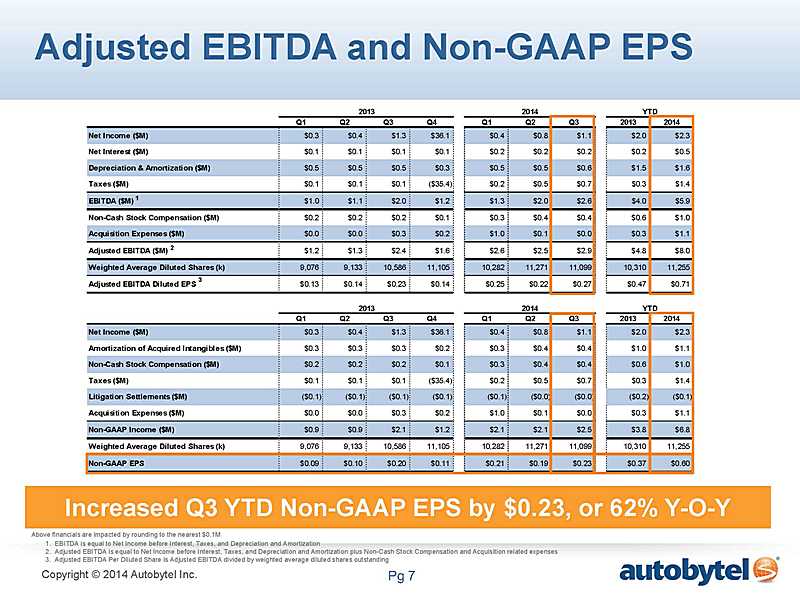

As you’ll see on Slide 7, non-cash stock-based compensation totaled $370,000, compared with $182,000 in the 2013 third quarter. The increase resulted from additional grants, as well as a higher share price versus last year, and the related Black-Scholes values used for expensing.

|

|

|

Depreciation and amortization was $575,000, versus $467,000 last year. The increase primarily related to AutoUSA and Advanced Mobile acquisitions.

|

Net income was $1.1 million, or $0.11 per diluted share, compared with $1.3 million, or $0.13 per diluted share, for last year’s third quarter. There were approximately 5% more diluted weighted average shares outstanding during the third quarter of 2014, compared with last year.

|

|

The change in diluted shares outstanding reflects an increase in Autobytel’s common stock price, as well as the company’s Cyber Ventures acquisition-related warrants being included in the diluted share calculation, as a result of the stock price increase. The diluted share calculation is also influenced quarter-to-quarter by the interplay between net income and interest expense on acquisition-related convertible debt.

|

|

|

As you’re aware, we now have a higher effective tax rate provision for book purposes than we’ve had in the past. This is the result of a valuation allowance reversal on our deferred tax assets at the end of last year. However, this increase will not impact cash, due to the utilization of NOL tax credits.

|

We are including non-GAAP financial information to help investors better understand Autobytel’s financial performance, given this higher tax rate provision and recent acquisitions. Also on Slide 7 you’ll see that non-GAAP income, which adds back amortization on acquired intangibles, non-cash stock-based compensation, acquisition costs, litigation settlements and income taxes, increased to $2.5 million, or $0.23 per diluted share, up from $2.1 million, or $0.20 per diluted share, one year ago.

AUTOBYTEL INC.

Moderator: Jeffrey Coats

11-05-14/2:00 p.m. ET

Confirmation # 23506766

Page 5

We’ve included calculation of non-GAAP income and non-GAAP EPS for the first and second quarters of this year to provide you with a more complete picture and for comparative purposes.

Our cash and cash equivalents balance grew to $22.3 million at September 30, 2014, up from $18.9 million at the end of 2013, and from $20.5 million at the end of the second quarter.

|

|

Cash provided by operations for the 2014 third quarter was $2.8 million, compared with $1.8 million in the prior year quarter. For the year-to-date period, cash provided by operations was $5.6 million, versus $2.7 million for the same period last year.

|

Detailed year-to-date financial results are available in the press release we issued earlier today, and in the Form 10-Q for the third quarter, filed prior to this call.

|

|

Now, I’ll turn the call back to Jeff.

|

|

Jeffrey Coats:

|

Thanks, Curt.

|

As I said earlier, we are enthusiastic about the growth opportunities ahead and are pleased with our results this quarter, particularly the fact that we’ve grown year-to-date non-GAAP EPS by $0.23, or $3 million, to $0.60 per diluted share.

However, there seems to be some continuing confusion in the investment community about our purchase of AutoUSA, so I’d like to spend the new few minutes reiterating the many benefits we have gained, and will continue to gain, as a result of the acquisition.

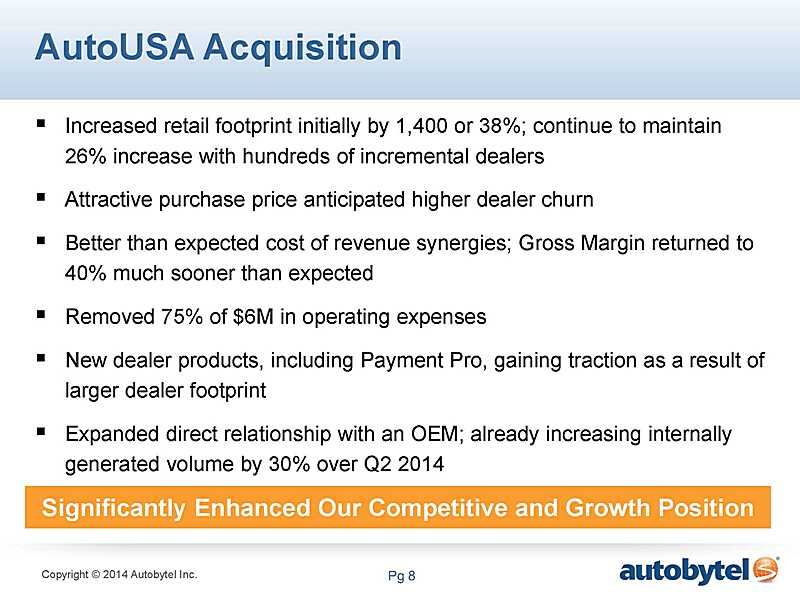

Slide 8 provides a summary of these benefits.

To start, our retail footprint has grown substantially with the addition of hundreds of incremental new dealer customers. This gives us an expanded base through which to sell not only our high quality leads, but our newer value added products, like SaleMove and Autobytel Mobile, especially our TextShield product.

|

|

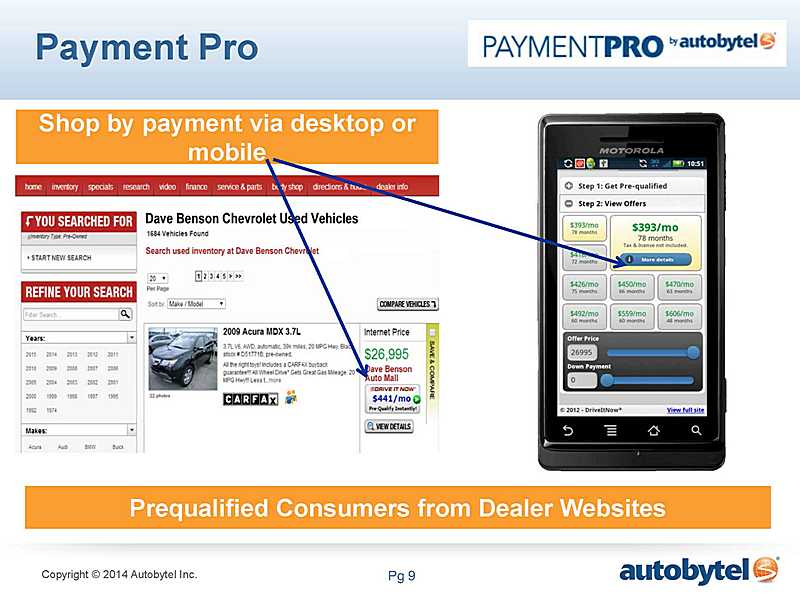

Second, as you can see on Slide 9, we’ve added a new dealer product, Payment Pro, which is gaining traction. Payment Pro provides a dealer with the ability to display online the actual monthly payment a consumer will pay for a car in the dealers inventory. This is especially timely since the majority of consumers shop for cars based on monthly payments.

|

AUTOBYTEL INC.

Moderator: Jeffrey Coats

11-05-14/2:00 p.m. ET

Confirmation # 23506766

Page 6

|

|

Next, we augmented our OEM network by expanding our direct relationship with a major automotive manufacturer that changed lead technology providers and re-launched its corporate lead program in the second quarter using Autobytel’s organic leads as a primary lead supplier.

|

|

|

This increase was largely offset by a reduction in volume of purchase leads that AutoUSA previously supplied to this OEM directly, which we discussed last quarter.

|

|

|

We have been working to improve the volumes and profitability of this program and believe that our volumes will continue to grow. In fact, in the third quarter, our organic volume to this OEM increased by more than 30% compared with the second quarter, and we believe that moving forward we will remain one of the largest suppliers to this OEM.

|

|

|

With the AutoUSA business now fully integrated, and after removing 75% of its $6.0 million in operating expenses, we can unequivocally say that the transaction has been positive for Autobytel.

|

When we purchased the company for $11 million in cash and notes in January, we knew there would be some work to do to make sure AutoUSA was running as efficiently and profitably as possible. We also were fully cognizant that their revenue was declining due to higher than average dealer churn, and we knew there would be inter-company eliminations since we were supplying leads to them before the acquisition.

|

|

Even at the current annual revenue run rate of approximately $16 million, we paid what we believe was a very attractive price based on the synergies we realized and the value we continue to drive as a result of the acquisition.

|

I’ll say it again, because it bears repeating… AutoUSA significantly enhanced our competitive position and created a more solid platform from which we can continue to grow.

|

|

Our core leads business continues to show strength, which is a testament to our focus on providing high quality leads that convert to sales and a higher return on investment for our customers.

|

|

|

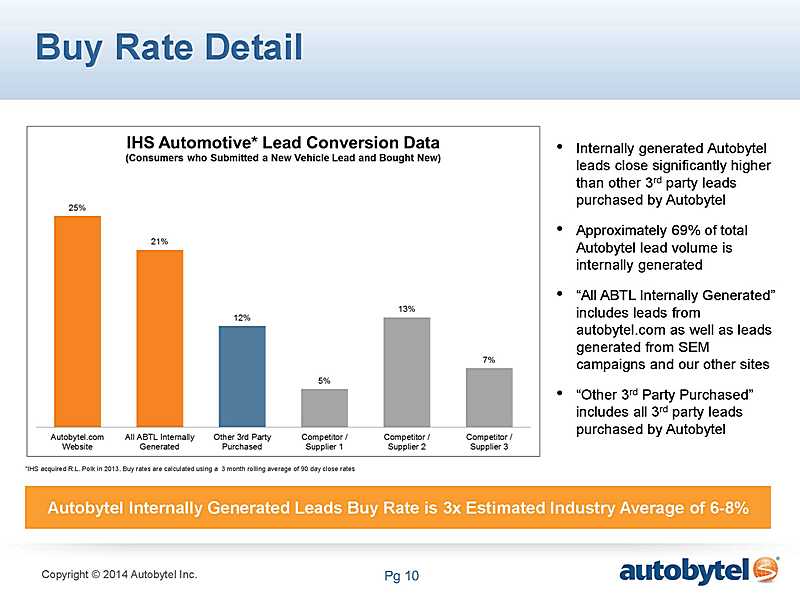

As you can see on Slide 10, and as validated by IHS Automotive, the leads we generate from autobytel.com currently have a buy rate, on average, of approximately 25%, meaning that of 100 new vehicle leads delivered to dealers, 25 of these consumers will purchase a new vehicle within 90 days.

|

AUTOBYTEL INC.

Moderator: Jeffrey Coats

11-05-14/2:00 p.m. ET

Confirmation # 23506766

Page 7

|

|

All leads internally-generated by Autobytel currently have a buy rate of approximately 21%. This is three times better than the estimated average for our industry. We believe this is a direct result of our ability to generate the substantial majority of our leads internally.

|

|

|

The conversion rates, or lead closing percentages, that an individual dealer will achieve will vary based primarily on the strength of processes and procedures within the dealership that are in place to manage communications and follow-up with consumers.

It is important to note that even these high buy rates are conservative because not all sales can be matched since many consumers buy outside of the 90-day measurement window, buy a used car instead or register a vehicle under a different name than from the original lead submission. Only direct match registrations are included in the buy rate data. The data illustrates that Autobytel automotive leads deliver in-market buyers to dealers and manufacturers and continue to be a proven method for dealers and manufacturers to sell more vehicles.

|

|

|

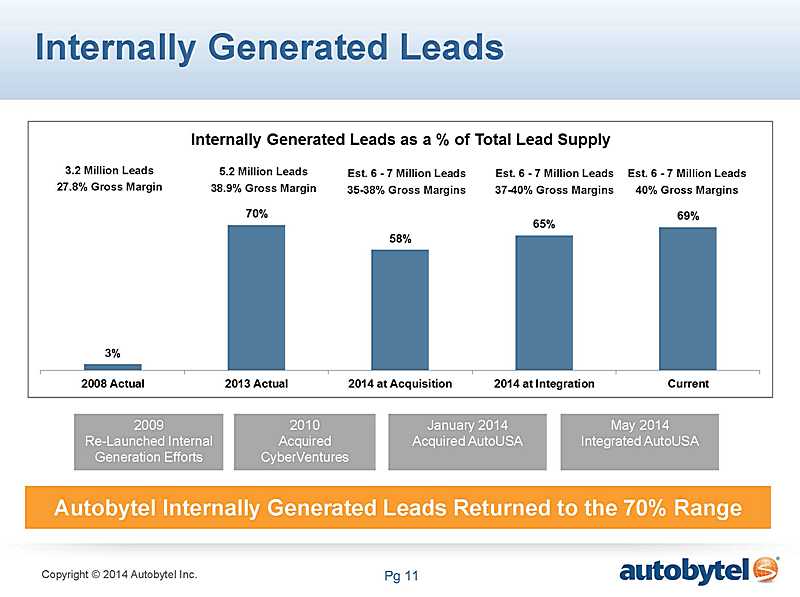

As you will see on Slide 11, we have grown the number of leads Autobytel generates internally from 3% six years ago to nearly 70% today. Our ability to generate leads internally has had a meaningful impact on several areas of our business.

|

|

|

First, we have been able to substantially enhance the quality of the leads we deliver to customers. This, in turn, has enabled us to solidify customer relationships, sell more leads and command higher marketplace pricing. Next, because it is less expensive to internally generate leads than to buy them from other third-party providers, we can generate higher margins. Slide 11 also shows the significant progress we’ve made in expanding margins as our internally-generated lead volume has increased.

|

|

|

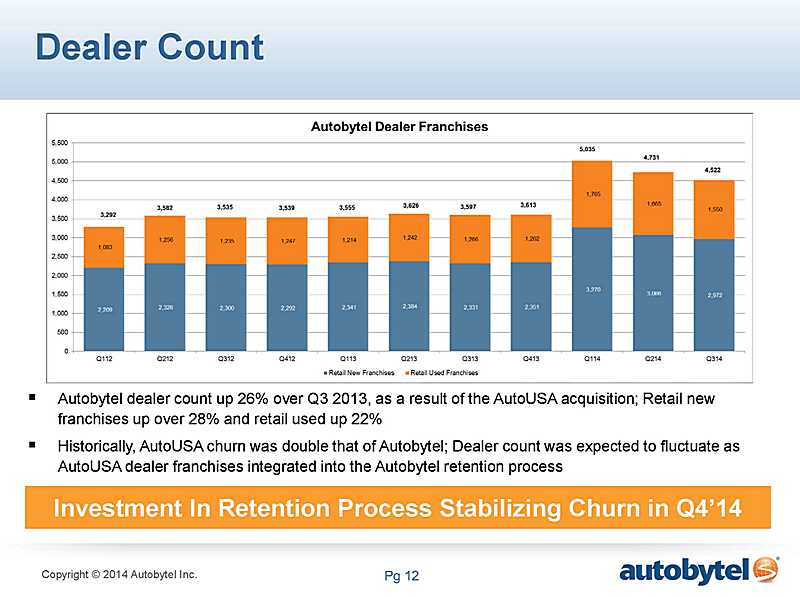

Dealer count, which is shown on Slide 12, stood at more than 4,500 franchises at the end of September, up 26% from last year’s third quarter, but down from 4,700 at the end of the second quarter as a result of AutoUSA’s higher-than-average churn. As I mentioned, our business plan anticipated this decline along with the commensurate decline in retail revenue. By expanding our dealer retention staff and improving our retention processes, we are starting to see positive results, and believe that churn is beginning to stabilize during the fourth quarter.

|

|

|

The quality and sales conversion of our leads is one of the reasons we are confident with this statement. Third-party leads have been the industry standard for many years. Autobytel’s high quality leads specifically were the gold standard in the early years of the automotive internet and are now once again being acknowledged as the gold standard.

|

AUTOBYTEL INC.

Moderator: Jeffrey Coats

11-05-14/2:00 p.m. ET

Confirmation # 23506766

Page 8

|

|

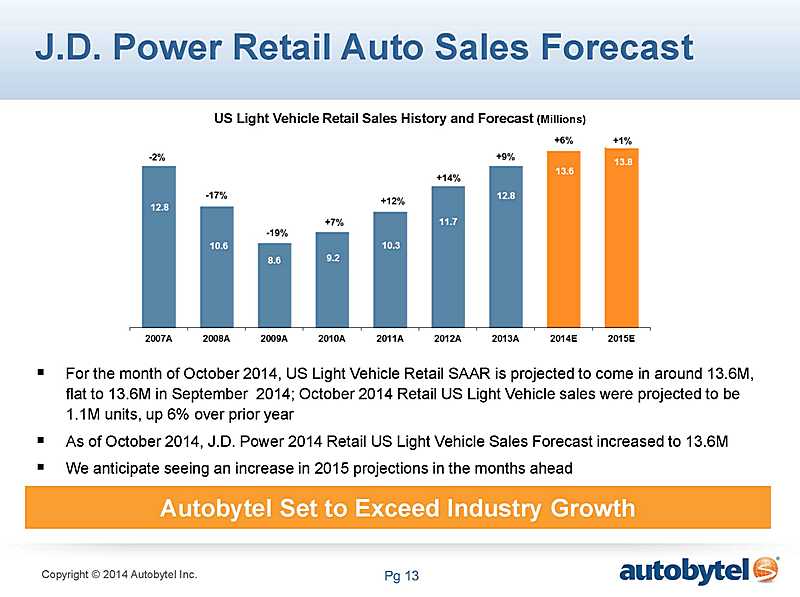

As with any other industry, though, from time-to-time, new products and services are introduced that temporarily take the focus away from lead generation as the best and most profitable way to sell cars to in-market buyers. During these periods, dealers may decide to pull back on their lead programs to test these new approaches, but anecdotally we know that a significant number of dealers tend to return to purchasing high quality leads after comparing the ROI they receive from other forms of marketing. As you can see on Slide 13, although the automotive market remains healthy, current automotive sales forecasts shows slower growth for 2015. The October retail seasonally adjusted annual run rate, or SAAR, was expected to be 13.6 million units, which is flat from September.

|

|

|

Retail U.S. light vehicle sales were projected to grow 6% in October, compared with the prior year. If sales slow in 2015, as currently forecast, we believe dealers will turn to the highest ROI activity available to sell more cars… and that’s third-party leads. Autobytel has been acknowledged as the highest quality provider of these leads, so we expect to benefit as a result.

|

|

|

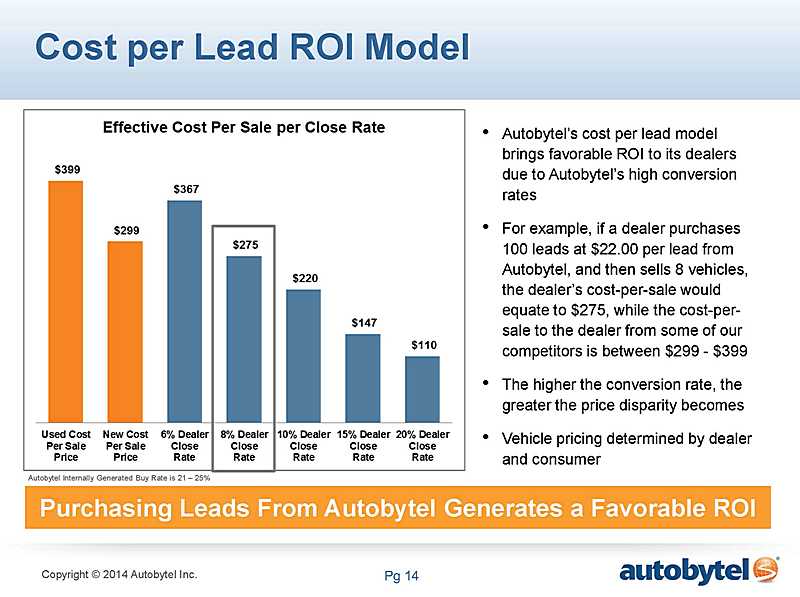

I won’t discuss it in detail because we’ve shown this slide in the past, but you can clearly see on Slide 14 that Autobytel’s cost-per-lead model delivers highly favorable ROI to our dealers compared with other models in the marketplace. We hear from time to time again from our dealers and OEMs that third-party leads continue to be one of the most efficient and highest ROI ways to sell cars. We currently have relationships with 31 automotive manufacturers, including all mainstream OEMs with the exception of one luxury brand that has yet to launch a lead program. Demonstrating how important third-party leads are to OEMs, over the past three years several major OEMs, including two major Japanese manufacturers, launched corporate lead programs for the first time. Others have completely re-launched their programs, and six have changed business rules, pricing or coverage in order to be able to purchase more of Autobytel’s high quality, organic leads.

|

|

|

We would argue this is evidence that third-party leads have neither lost favor nor gone out of style.

|

The bottom line is that our success is built on the quality and sales conversion rates of our leads. We are committed to doing whatever necessary to maintain that focus.

As I discussed earlier, in addition to enhancing the quality and volume of the leads we deliver to customers, we are focused on providing them with innovative products and services to help them sell more cars. While still relatively small, the revenue associated with each of these products is growing, and we’re pleased with their early performance.

AUTOBYTEL INC.

Moderator: Jeffrey Coats

11-05-14/2:00 p.m. ET

Confirmation # 23506766

Page 9

Autobytel Mobile, which is shown on Slide 7, continues to be well-accepted in the marketplace. By giving dealers and OEMs a compliant way to communicate with consumers via text using our TextShield platform, we are providing new sales opportunities for them.

SaleMove, which is shown on Slide 18, is helping dealers improve the online car shopping experience for their customers. Autobytel is providing the tools necessary to capture the opportunities being created as online shopping becomes increasingly popular with in-market car buyers.

|

|

You’ll also recall that we made a strategic investment of 16% about a year ago in AutoWeb, whose platform enables specialized targeting to high-intent online car shoppers while allowing advertisers to optimize their campaigns efficiently. AutoWeb is generating better than expected top line growth, with first year revenues exceeding its internal plan by more than 100%. Additionally, AutoWeb is contributing increasing profit through multiple revenue streams directly to Autobytel. With 66 employees throughout the Americas, AutoWeb is continuing to invest in growth. In fact, they are currently raising additional capital at a substantially higher valuation, and I would remind you that we have an option to purchase an additional approximately 10% of the company at the original valuation. We plan to share more about this relationship in the coming quarters.

|

Based on current business trends, the solid automotive market and anticipated typically seasonality, we expect 2014 fourth quarter revenue growth in the range of 23.5% to 27.5% over the 2013 fourth quarter. We also expect 2014 fourth quarter non-GAAP EPS to be in the range of $0.12 to $0.15 based on 11.1 million diluted average weighted shares outstanding. As you may have seen, we filed with the SEC a pre-effective amendment to our shelf registration statement on Form S-3 requesting that it be declared effective next Monday or as soon as possible thereafter. Let me state clearly once again that we have no current plans to raise capital under the S-3 but believe it is prudent corporate finance planning to have it in place.

I’d also like to remind everyone that our Board of Directors recently approved an increase in Autobytel’s stock buy-back authorization from $2.0 million to $3.0 million. It is the company’s intention to begin purchasing shares under this authorization when our trading window opens next week. Of course, the timing and actual number of shares repurchased depends on a number of factors and is at the company’s sole discretion. It is also my intention personally to purchase stock in the open market after our trading window opens.

We plan to drive long-term growth through a variety of initiatives, as shown on Slide 20. Our primary focus, as always, is on providing value to all of our customers, which we believe will ultimately translate to enhanced value for our shareholders.

AUTOBYTEL INC.

Moderator: Jeffrey Coats

11-05-14/2:00 p.m. ET

Confirmation # 23506766

Page 10

I hope that you can tell that we are as upbeat as ever about our business, our industry and our future opportunities.

Operator, we’re now ready to take questions.

|

Operator:

|

Ladies and gentlemen, if you have a question at this time, please press star then the number one key on your touch-tone telephone. If your question has been answered or you wish to remove yourself from the queue, please press the pound key.

|

Our first question comes from the line of Eric Martinuzzi from Lake Street Capital. Sir, your line is open.

Eric Martinuzzi: Thanks. Congratulations on the strong performance in Q3. My question has to do with the adjusted EPS. First of all, thank you for providing that to us. It does help, kind of, given apples to apples of Autobytel versus the other public comps out there. I wanted to understand, in 2013 what was the full-year adjusted EPS? If I look at, I think, it’s Slide 6 or 7, it looks like $0.49 or $0.50. What was the full year 2013?

|

Curt DeWalt:

|

One moment. $0.64.

|

|

Eric Martinuzzi:

|

OK, so that’s $0.64 a year ago, and then you said that through the nine months this year the adjusted EPS number was $0.60 through the nine months?

|

|

Curt DeWalt:

|

I’m sorry. The full year was $0.64. For the first nine months it was $0.47.

|

|

Eric Martinuzzi:

|

No. I’m talking about – my second question was through the nine months 2014?

|

|

Curt DeWalt:

|

Yes. It was $0.47 versus $0.71.

|

|

|

Eric Martinuzzi: $0.47 and $0.71. OK. What I was trying to get at is if you hit your $0.12 to $0.15 for Q4 that would put us at what for FY14 for adjusted EPS?

|

|

Curt DeWalt:

|

Well, it’s going to be a slightly different calculation. The adjusted EBITDA and the adjusted non-GAAP EPS, we’ve got slightly different components in the calculation there.

|

|

Eric Martinuzzi:

|

I never mentioned EBITDA. I’m just talking adjusted EPS. What I’m thinking here is last year you did $0.49, $0.50, and if you hit your guided range for 2014, you’ll be doing $0.72 to $0.75. So, that’s where I was headed.

|

AUTOBYTEL INC.

Moderator: Jeffrey Coats

11-05-14/2:00 p.m. ET

Confirmation # 23506766

Page 11

|

Curt DeWalt:

|

That’s correct.

|

|

Eric Martinuzzi:

|

Okay. All right, so just further example at least on an annual basis of the adjusted EPS growth. Okay, and then stepping away from that, I wanted to talk a little bit more about, on Slide 8, you talked about the expanded direct relationship with an OEM.

|

|

|

Could you revisit that and maybe go a layer deeper because one of the issues with AutoUSA in Q2 was, what I thought was the end of a relationship with the hope that it might be renewed, and here it looks like that is in fact happening, but was the last bullet on Slide 8.

|

|

Jeffrey Coats:

|

Sure. So, we already had a small direct relationship with that manufacturer. A lot of the volume that we were selling of leads for that manufacturer, we were in fact selling to AutoUSA, and AutoUSA was selling them on to that manufacturer at a higher price. So, we were both achieving a higher price under that particular program that AutoUSA had in place directly with that manufacturer.

|

|

|

That manufacturer made a decision to recast their program. They hired a new lead technology company to manage it for them. They decided to focus on buying a higher quality level of leads as part of what they were doing. So, what ended up happening is we actually lost the volume of purchased leads that AutoUSA had been buying from other third-party providers and then selling to that manufacturer.

|

|

|

So today, we sell them a higher volume of our higher quality internally-generated. We continued to do some of that during Q2, and that volume expanded as we said earlier by approximately 30% during Q3, and we would anticipate additional increases in volume as we continue to work closely with that manufacturer to help them sell more cars because they’re certainly interested in achieving a higher volume as long as we can maintain the quality, which, of course, we always do.

|

|

Eric Martinuzzi:

|

Okay, and then last question from me – you responded recently to a letter from an investor talking about some actions they would like you take as far as pursuing a different path than an independent path. I understand both sides of the argument. Are any of these actions here, recently – you’re talking about the expanded buy-back plan. You’re talking about you purchasing in the open market. Is any of that being driven as kind of a defensive maneuver here, or are these steps that you would have been taking anyhow?

|

|

Jeffrey Coats:

|

No. We were already planning to increase the buy-back. In fact, we had already begun the discussion at the Board level around increasing the buy-back. The other things they were talking about, I mean obviously, it’s a new investor. We think that they don’t completely understand our company based on some of the information in the letter that they sent.

|

AUTOBYTEL INC.

Moderator: Jeffrey Coats

11-05-14/2:00 p.m. ET

Confirmation # 23506766

Page 12

|

|

I think the fact that the company has now been profitable for four years in a row, that we are again the largest lead provider to the automotive industry in the United States, that we’re selling the highest quality leads, that we do business with all of the major manufacturers, that we’re the largest supplier to many of the manufacturers, that we’ve continued to increase our gross margin, that we’ve continued to increase our profitability, is testament of the fact that the company is operating effectively and appropriately.

|

|

|

In the long run, I think no one would argue that it may make sense for this company to be part of a larger organization, but we don’t believe that now is the time for that.

|

|

Eric Martinuzzi:

|

Okay. Thank you.

|

|

Operator:

|

Thank you. Our next question comes from the line of Sameet Sinha of B. Riley. Your line is open.

|

|

Sameet Sinha:

|

Yes. Thank you very much. So, just picking up from the previous question about this letter – your response to the investor’s letter. Can you talk about, in detail, about some of these new initiatives in Advanced Mobile and Car Move… and, of course, it’s good to see the traction with Jumpstart media, but how big could each of these be, and kind of, what’s the go-to-market strategy? Are there any gating factors? If you can provide a little more insight there, that would be helpful, and then I have a follow-up question.

|

|

Jeffrey Coats:

|

Sameet, we’ve had many conversations about these topics. When we bought Advanced Mobile a year ago we began preparing those products for roll-out to a larger number of dealers and for conversations with manufacturers. We have signed on quite a few dealers. We are in discussions and a pilot with a manufacturer about a larger roll-out of a program that would get us many more dealers on the program more quickly.

|

|

|

The roll-out has been a little slower than we initially anticipated, but that was really primarily a function of the AutoUSA acquisition and the focus that that took for the salespeople as part of trying to make sure that we had our arms around as many of the dealers as possible through that. So, it did slow us down a little bit from that standpoint.

|

|

|

SaleMove, we have a pilot going with a major manufacturer currently. We expect that pilot to be rolled out on a national basis. As we have more information and we’re allowed to talk about it, we’ll be happy to do that. We’re also signing on more dealers on that product as well. The revenue for both of those product lines are beginning to scale, again albeit a little bit more slowly than we had initially anticipated, but they are beginning to grow nicely.

|

AUTOBYTEL INC.

Moderator: Jeffrey Coats

11-05-14/2:00 p.m. ET

Confirmation # 23506766

Page 13

|

|

We are, in fact, getting our arms around the dealer churn that we faced as a result of the AutoUSA acquisition. I think this has been an interesting year. We have comments from people like Mike Jackson related to third-party leads and the TrueCar IPO and a lot of focus on that. A lot of focus on more dealers wanting to try to generate traffic to their own websites and generate leads from their websites as part of doing that. Of course, that’s a natural thing for people to want to do.

|

|

|

However, for most organizations that takes a relatively extended amount of time, and it’s pretty expense and doesn’t really generate a very good ROI for quite a while.

|

|

|

So, we tend to think, and we see already, we’re beginning to see some benefits from this that, in fact, dealers will come back to third-party leads because third-party leads are, in fact, their best and highest return on investment for what they’re getting. Whether it’s $20, $25 or even $30 for a lead – it’s a great return for a dealer.

|

|

|

And as we’ve highlighted in the past, we do not get between the dealer and their customer when it comes to negotiating price. So, we hear anecdotally quite often from our dealer customers that they maintain a higher gross on the vehicles they sell from Autobytel leads than they do from certain other kinds of marketing activities.

|

|

|

So, we believe 2015 will be a good year for us. Automotive sales… We think the analysts will probably increase their numbers a little bit as we move into 2015 in terms of overall growth rate.

|

So, we continue to think that that’s going to be a good year for us because as car sales do slow down a little bit from the higher levels coming out of the recession, dealers will focus again on their highest return on investment and one of the quickest things they can do, which is to turn to the third-party lead providers and turn up the volume again.

|

|

We’ve built our reputation for quality. We’re maintaining our reputation for quality, and we are known more and more for that in our marketplace.

|

|

Sameet Sinha:

|

Thanks. It was interesting to see that Edmunds had also acquired a similar mobile product a couple of weeks back, so, obviously, your buy was well in advance of that.

|

|

|

My second question. So, there were a couple of big OEM hold-outs in the last couple of years, and then you probably had a better relationship with one of them through AutoUSA. When these relationships tend to come on board, do they tend to scale very quickly, or is it kind of a slow test – test and draw kind of relationships that you have?

|

AUTOBYTEL INC.

Moderator: Jeffrey Coats

11-05-14/2:00 p.m. ET

Confirmation # 23506766

Page 14

|

|

And what are your thoughts, I mean – will you be able to close some of these relationships in the next few quarters, or are there some structural impediments to getting these additional OEMs?

|

|

Jeffrey Coats:

|

To answer the first part of your question, it really kind of depends upon the manufacturer and how they’re doing what they’re doing, but I think as you will have noted as a couple of the new major programs have come online, one beginning last year in the summer, and one beginning in essentially early 2012, they did scale pretty quickly.

|

Generally, what happens is they assign a volume target to each of the providers in their programs and they kind of cap you out once you hit that volume target. The same was true for us when these new programs started, but the difference for us has been as the manufacturers begin to scale and they see the results of their close rate information and they see that they’re generally selling a higher number of cars from the leads that we’re providing, they tend to open up the volume to us, and I think you will recall as we’ve spoken in the past, today for all of the largest manufacturer programs in the United States, Autobytel actually is uncapped for all of those programs, and they take as many leads from a volume standpoint as we can generate and send to them on a monthly basis. Of course, it’s incumbent upon us to maintain our high close rates, which is how we will continue to maintain those volumes.

|

|

So, it starts off a little slowly but tends to open up very fast and goes well. There are some manufacturers, there are a couple that we have discussed that have smaller programs. We believe that we will see one of those opportunities begin to open up more for us as we move into 2015 and will provide some nice scale growth opportunities for us during 2015, similarly, on a par with some of the largest programs.

|

|

Sameet Sinha:

|

Okay. My final question – kind of taking a step back, as you’ve seen the industry evolve, I mean lead generation obviously has been one of the older internet advertising, fast marketing products out there and it continues to grow quite nicely for the auto industry. What about the other media vehicles that have emerged that are gaining traction as a source of auto leads or just to sell automobiles?

|

|

Jeffrey Coats:

|

People who help dealers manage their own SEM activities, companies who help dealers with their own SEO activities, the website providers like Cobalt and Dealer.com provide some of these services as they provide the website services, but there are a lot of other smaller companies that manage that as well.

|

AUTOBYTEL INC.

Moderator: Jeffrey Coats

11-05-14/2:00 p.m. ET

Confirmation # 23506766

Page 15

|

|

Over the long-term, those are probably reasonable strategies for dealers, but in the short-term it’s extremely (inaudible), and it takes it a while to scale, and the return on investment is really not great, and in addition, you can’t -- it’s not just good enough to get traffic to a dealer’s website. A dealer’s website has to be set up in order to generate a lead, and not all dealer websites are effectively set up to help a consumer get through and provide a lead to a dealer, so, I mean, we see it in our conversations with the manufacturers and with many of the thousands of dealers that are on our program who are big believers in buying leads, that, in fact, continuing to buy leads in the price ranges that have been -- that we’ve been talking about – are a great return on investment for dealers, and we expect to see our dealer volumes as well as our manufacturer volumes continue to grow as we move into 2015.

|

|

Operator:

|

Thank you. Our next question comes from the line of Ed Woo of Ascendiant Capital. Sir, your line is open.

|

|

Ed Woo:

|

Thanks for taking my question. I had a question about the guidance for the fourth quarter and maybe as we are starting to looking past that, but how much of the growth in revenue is a result of AutoUSA, and how much if it is organic growth?

|

|

Curt DeWalt:

|

You know, again, Ed, when we said this quarter, now that we’ve integrated AutoUSA completely into Autobytel we really don’t break out or bifurcate the two businesses any longer, so for us it’s one consolidated operation, and the numbers you’re seeing is the result of that.

|

|

Ed Woo:

|

Okay, and then you mentioned that slowing growth in auto sales possibly next year to be a headwind. Do you think there might be any other headwinds into (inaudible) the anniversary of the AutoUSA acquisition?

|

|

Jeffrey Coats:

|

Actually, I did not say that slowing auto sales next year would be a headwind. I said it would be a tailwind because we will actually benefit if auto sales slow somewhat because again one of the most timely, cost effective things that a dealer can do as sales slowdown a little bit, is turn to their lead provider to increase the volume that we sell to them, so we do not view that as a negative at all. In fact, the company historically has considered itself somewhat countercyclical. As sales slowdown, dealers tend to turn up the lead volume, which we see during the course of the year as well. If things are slowing down a little bit or a dealer is not hitting a target they want to hit, we’ll get a phone call that they want to increase the volume, so we don’t view that at all as a headwind.

|

AUTOBYTEL INC.

Moderator: Jeffrey Coats

11-05-14/2:00 p.m. ET

Confirmation # 23506766

Page 16

Other issues – don’t really currently see anything. Financing is back full bore, that’s very important. I do think some of the CFPB Consumer Financial Protection Bureau investigations into subprime financing and some of the other stuff that they’re doing may, in fact, curtail some of the lower quality financing that’s available in the market, which could be an issue, but don’t really see that becoming an issue in the short-term.

|

Ed Woo:

|

Well, my apologies for getting that incorrect, but thank you for answering my question, and good luck guys.

|

|

Jeffrey Coats:

|

Thank you.

|

|

Operator:

|

Thank you. At this time, I’m showing no further questions. I would like to turn the call back over to Jeffrey Coats for closing remarks.

|

|

Jeffrey Coats:

|

Thank you. Thanks everybody for joining us today. We look forward to speaking with many of you at the upcoming LD Micro Conference in Los Angeles at the beginning of next month. Thanks for your support. Good bye.

|

|

Operator:

|

Ladies and gentlemen, thank you for your participation in today’s conference. This concludes the program. You may now disconnect. Everyone have a great day.

|