UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2013

— OR —

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Commission File Number 1-12833

Energy Future Holdings Corp.

(Exact name of registrant as specified in its charter)

Texas | 46-2488810 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

1601 Bryan Street, Dallas, TX 75201-3411 | (214) 812-4600 | |

(Address of principal executive offices) (Zip Code) | (Registrant's telephone number, including area code) | |

__________________________________________________________________________

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class | Name of Each Exchange on Which Registered | |

9.75% Senior Notes due 2019 | New York Stock Exchange | |

Securities registered pursuant to Section 12(g) of the Act: None

__________________________________________________________________________

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer o Accelerated filer o Non-Accelerated filer x (Do not check if a smaller reporting company)

Smaller reporting company o

Indicate by check mark if the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

At April 29, 2014, there were 1,669,861,383 shares of common stock, without par value, outstanding of Energy Future Holdings Corp. (substantially all of which were owned by Texas Energy Future Holdings Limited Partnership, Energy Future Holdings Corp.’s parent holding company, and none of which is publicly traded).

________________________________________________________________________________

DOCUMENTS INCORPORATED BY REFERENCE

None

TABLE OF CONTENTS

PAGE | ||

Items 1. and 2. | ||

Item 1A. | ||

Item 1B. | ||

Item 3. | ||

Item 4. | ||

Item 5. | ||

Item 6. | ||

Item 7. | ||

Item 7A. | ||

Item 8. | ||

Item 9. | ||

Item 9A. | ||

Item 9B. | ||

Item 10. | ||

Item 11. | ||

Item 12. | ||

Item 13. | ||

Item 14. | ||

Item 15. | ||

Energy Future Holdings Corp.'s (EFH Corp.) annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and any amendments to those reports are made available to the public, free of charge, on the EFH Corp. website at http://www.energyfutureholdings.com, as soon as reasonably practicable after they have been filed with or furnished to the Securities and Exchange Commission. The information on EFH Corp.'s website shall not be deemed a part of, or incorporated by reference into, this annual report on Form 10-K. The representations and warranties contained in any agreement that we have filed as an exhibit to this annual report on Form 10-K or that we have or may publicly file in the future may contain representations and warranties made by and to the parties thereto at specific dates. Such representations and warranties may be subject to exceptions and qualifications contained in separate disclosure schedules, may represent the parties' risk allocation in the particular transaction, or may be qualified by materiality standards that differ from what may be viewed as material for securities law purposes.

This annual report on Form 10-K and other Securities and Exchange Commission filings of EFH Corp. and its subsidiaries occasionally make references to EFH Corp. (or "we," "our," "us" or "the company"), EFCH, EFIH, TCEH, TXU Energy, Luminant, Oncor Holdings or Oncor when describing actions, rights or obligations of their respective subsidiaries. These references reflect the fact that the subsidiaries are consolidated with, or otherwise reflected in, their respective parent company's financial statements for financial reporting purposes. However, these references should not be interpreted to imply that the parent company is actually undertaking the action or has the rights or obligations of the relevant subsidiary company or vice versa.

i

GLOSSARY

When the following terms and abbreviations appear in the text of this report, they have the meanings indicated below.

Adjusted EBITDA | Adjusted EBITDA means EBITDA adjusted to exclude noncash items, unusual items and other adjustments allowable under certain of our debt arrangements. See the definition of EBITDA below. Adjusted EBITDA and EBITDA are not recognized terms under US GAAP and, thus, are non-GAAP financial measures. We are providing Adjusted EBITDA in this Form 10-K (see reconciliations in Exhibits 99(b), 99(c) and 99(d)) solely because of the important role that Adjusted EBITDA plays in respect of certain covenants contained in our debt arrangements. We do not intend for Adjusted EBITDA (or EBITDA) to be an alternative to net income as a measure of operating performance or an alternative to cash flows from operating activities as a measure of liquidity or an alternative to any other measure of financial performance presented in accordance with US GAAP. Additionally, we do not intend for Adjusted EBITDA (or EBITDA) to be used as a measure of free cash flow available for management's discretionary use, as the measure excludes certain cash requirements such as interest payments, tax payments and other debt service requirements. Because not all companies use identical calculations, our presentation of Adjusted EBITDA (and EBITDA) may not be comparable to similarly titled measures of other companies. | |

ancillary services | Refers to services necessary to support the transmission of energy and maintain reliable operations for the entire transmission system. These services include monitoring and providing for various types of reserve generation to ensure adequate electricity supply and system reliability. | |

Bankruptcy Filing | Voluntary petitions for relief under Chapter 11 of the US Bankruptcy Code (Bankruptcy Code) in the US Bankruptcy Court for the District of Delaware (Bankruptcy Court) filed on April 29, 2014 by the Debtors. | |

CAIR | Clean Air Interstate Rule | |

CFTC | US Commodity Futures Trading Commission | |

CO2 | carbon dioxide | |

CPNPC | Refers to Comanche Peak Nuclear Power Company LLC, which was formed by subsidiaries of TCEH (holding an 88% equity interest) and Mitsubishi Heavy Industries Ltd. (MHI) (holding a 12% equity interest) for the purpose of developing two new nuclear generation units and obtaining a combined operating license from the NRC for the units. | |

Competitive Electric segment | the EFH Corp. business segment that consists principally of TCEH | |

Consenting Creditors | Means collectively, (i) certain lenders or investment advisors or managers of discretionary accounts (Consenting TCEH First Lien Lenders) that hold claims under the TCEH Senior Secured Facilities; (ii) certain holders (Consenting TCEH First Lien Noteholders and together with the Consenting TCEH First Lien Lenders, the Consenting TCEH First Lien Creditors) of TCEH Senior Secured Notes; (iii) certain holders (Consenting EFIH First Lien Noteholders) of the EFIH 6.875% Notes and the EFIH 10% Notes (EFIH First Lien Notes); (iv) certain holders (Consenting EFIH Second Lien Noteholders) of the EFIH 11% Notes and the EFIH 11.75% Notes (EFIH Second Lien Notes); (v) certain holders (Consenting EFIH Unsecured Noteholders) of the EFIH Toggle Notes; and certain holders (the Consenting EFH Corp. Unsecured Noteholders) of the EFH Corp. 5.55% Series P Senior Notes due 2014, the EFH Corp. 6.50% Series Q Senior Notes due 2024, EFH Corp. 6.55% Series R Senior Notes due 2034, the EFH Corp. 11.250%/12.00% Senior Toggle Notes due 2017, the EFH Corp. 10.875% Senior Notes due 2017, the EFH Corp. 9.75% Fixed Senior Notes due 2019, and the EFH Corp. 10% Fixed Senior Notes due 2020 (EFH Unsecured Notes). | |

CREZ | Competitive Renewable Energy Zone | |

CSAPR | the final Cross-State Air Pollution Rule issued by the EPA in July 2011, vacated by the US Court of Appeals for the District of Columbia Circuit in August 2012 and remanded by the US Supreme Court to the D.C. Circuit Court for further proceedings consistent with the US Supreme Court's opinion (see Note 11 to Financial Statements) | |

DIP Facilities | Refers, collectively, to TCEH's and EFIH's proposed debtor-in-possession financing. See Note 10 to Financial Statements. | |

Debtors | EFH Corp. and the substantial majority of its direct and indirect subsidiaries, including EFIH, EFCH and TCEH but excluding the Oncor Ring-Fenced Entities | |

D.C. Circuit Court | US Court of Appeals for the District of Columbia Circuit | |

ii

DOE | US Department of Energy | |

EBITDA | earnings (net income) before interest expense, income taxes, depreciation and amortization | |

EFCH | Energy Future Competitive Holdings Company LLC, a direct, wholly owned subsidiary of EFH Corp. and the direct parent of TCEH, and/or its subsidiaries, depending on context | |

EFH Corp. | Energy Future Holdings Corp., a holding company, and/or its subsidiaries, depending on context, whose major subsidiaries include TCEH and Oncor | |

EFIH | Energy Future Intermediate Holding Company LLC, a direct, wholly owned subsidiary of EFH Corp. and the direct parent of Oncor Holdings | |

EFIH Debtors | EFIH and EFIH Finance | |

EFIH Finance | EFIH Finance Inc., a direct, wholly owned subsidiary of EFIH, formed for the sole purpose of serving as co-issuer with EFIH of certain debt securities | |

EFIH Notes | Refers, collectively, to EFIH's and EFIH Finance's 6.875% Senior Secured Notes with a maturity date of August 15, 2017 (EFIH 6.875% Notes), 10.000% Senior Secured Notes with a maturity date of December 1, 2020 (EFIH 10% Notes), 11% Senior Secured Second Lien Notes with a maturity date of October 1, 2021 (EFIH 11% Notes), 11.75% Senior Secured Second Lien Notes with a maturity date of March 1, 2022 (EFIH 11.75% Notes), 11.25%/12.25% Senior Toggle Notes with a maturity date of December 1, 2018 (EFIH Toggle Notes) and 9.75% Senior Notes with a maturity date of October 15, 2019 (EFIH 9.75% Notes). | |

EFIH Second Lien DIP Facility | Refers, collectively, to the facility that includes the EFIH Second Lien DIP Notes. | |

EPA | US Environmental Protection Agency | |

ERCOT | Electric Reliability Council of Texas, Inc., the independent system operator and the regional coordinator of various electricity systems within Texas | |

ERISA | Employee Retirement Income Security Act of 1974, as amended | |

FERC | US Federal Energy Regulatory Commission | |

Fifth Circuit Court | US Court of Appeals for the Fifth Circuit | |

GAAP | generally accepted accounting principles | |

GHG | greenhouse gas | |

GWh | gigawatt-hours | |

ICE | the IntercontinentalExchange, a commodity exchange | |

IRS | US Internal Revenue Service | |

kWh | kilowatt-hours | |

LIBOR | London Interbank Offered Rate, an interest rate at which banks can borrow funds, in marketable size, from other banks in the London interbank market | |

Luminant | subsidiaries of TCEH engaged in competitive market activities consisting of electricity generation and wholesale energy sales and purchases as well as commodity risk management and trading activities, all largely in Texas | |

market heat rate | Heat rate is a measure of the efficiency of converting a fuel source to electricity. Market heat rate is the implied relationship between wholesale electricity prices and natural gas prices and is calculated by dividing the wholesale market price of electricity, which is based on the price offer of the marginal supplier in ERCOT (generally natural gas plants), by the market price of natural gas. Forward wholesale electricity market price quotes in ERCOT are generally limited to two or three years; accordingly, forward market heat rates are generally limited to the same time period. Forecasted market heat rates for time periods for which market price quotes are not available are based on fundamental economic factors and forecasts, including electricity supply, demand growth, capital costs associated with new construction of generation supply, transmission development and other factors. | |

iii

MATS | the Mercury and Air Toxics Standard established by the EPA | |

Merger | The transaction referred to in the Agreement and Plan of Merger, dated February 25, 2007, under which Texas Holdings agreed to acquire EFH Corp., which was completed on October 10, 2007. | |

MMBtu | million British thermal units | |

Moody's | Moody's Investors Services, Inc. | |

MW | megawatts | |

MWh | megawatt-hours | |

NERC | North American Electric Reliability Corporation | |

NOX | nitrogen oxides | |

NRC | US Nuclear Regulatory Commission | |

NYMEX | the New York Mercantile Exchange, a physical commodity futures exchange | |

Oncor | Oncor Electric Delivery Company LLC, a direct, majority-owned subsidiary of Oncor Holdings and an indirect subsidiary of EFH Corp., and/or its consolidated bankruptcy-remote financing subsidiary, Oncor Electric Delivery Transition Bond Company LLC, depending on context, that is engaged in regulated electricity transmission and distribution activities | |

Oncor Holdings | Oncor Electric Delivery Holdings Company LLC, a direct, wholly owned subsidiary of EFIH and the direct majority owner of Oncor, and/or its subsidiaries, depending on context | |

Oncor Ring-Fenced Entities | Oncor Holdings and its direct and indirect subsidiaries, including Oncor | |

Oncor Tax Sharing Agreement | Federal and State Income Tax Allocation Agreement among EFH Corp., Oncor Holdings, Oncor and Texas Transmission | |

OPEB | other postretirement employee benefits | |

PUCT | Public Utility Commission of Texas | |

PURA | Texas Public Utility Regulatory Act | |

purchase accounting | The purchase method of accounting for a business combination as prescribed by US GAAP, whereby the cost or "purchase price" of a business combination, including the amount paid for the equity and direct transaction costs are allocated to identifiable assets and liabilities (including intangible assets) based upon their fair values. The excess of the purchase price over the fair values of assets and liabilities is recorded as goodwill. | |

Regulated Delivery segment | the EFH Corp. business segment that consists primarily of our investment in Oncor | |

REP | retail electric provider | |

RCT | Railroad Commission of Texas, which among other things, has oversight of lignite mining activity in Texas | |

S&P | Standard & Poor's Ratings Services, a division of the McGraw-Hill Companies Inc. (a credit rating agency) | |

SEC | US Securities and Exchange Commission | |

Securities Act | Securities Act of 1933, as amended | |

SG&A | selling, general and administrative | |

SO2 | sulfur dioxide | |

Sponsor Group | Refers, collectively, to certain investment funds affiliated with Kohlberg Kravis Roberts & Co. L.P., TPG Global, LLC (together with its affiliates, TPG) and GS Capital Partners, an affiliate of Goldman, Sachs & Co., that have an ownership interest in Texas Holdings. | |

iv

TCEH | Texas Competitive Electric Holdings Company LLC, a direct, wholly owned subsidiary of EFCH and an indirect subsidiary of EFH Corp., and/or its subsidiaries, depending on context, that are engaged in electricity generation and wholesale and retail energy markets activities, and whose major subsidiaries include Luminant and TXU Energy | |

TCEH Debtors | TCEH and its subsidiaries that are Debtors in the Chapter 11 Cases | |

TCEH Demand Notes | Refers to certain loans from TCEH to EFH Corp. in the form of demand notes to finance EFH Corp. debt principal and interest payments and, until April 2011, other general corporate purposes of EFH Corp. that were guaranteed on a senior unsecured basis by EFCH and EFIH and were settled by EFH Corp. in January 2013. | |

TCEH Finance | TCEH Finance, Inc., a direct, wholly owned subsidiary of TCEH, formed for the sole purpose of serving as co-issuer with TCEH of certain debt securities | |

TCEH Senior Notes | Refers, collectively, to TCEH's and TCEH Finance's 10.25% Senior Notes with a maturity date of November 1, 2015 and 10.25% Senior Notes with a maturity date of November 1, 2015, Series B (collectively, TCEH 10.25% Notes) and TCEH's and TCEH Finance's 10.50%/11.25% Senior Toggle Notes with a maturity date of November 1, 2016 (TCEH Toggle Notes). | |

TCEH Senior Secured Facilities | Refers, collectively, to the TCEH Term Loan Facilities, TCEH Revolving Credit Facility and TCEH Letter of Credit Facility. See Note 10 to Financial Statements for details of these facilities. | |

TCEH Senior Secured Notes | TCEH's and TCEH Finance's 11.5% Senior Secured Notes with a maturity date of October 1, 2020 | |

TCEH Senior Secured Second Lien Notes | Refers, collectively, to TCEH's and TCEH Finance's 15% Senior Secured Second Lien Notes with a maturity date of April 1, 2021 and TCEH's and TCEH Finance's 15% Senior Secured Second Lien Notes with a maturity date of April 1, 2021, Series B. | |

TCEQ | Texas Commission on Environmental Quality | |

Texas Holdings | Texas Energy Future Holdings Limited Partnership, a limited partnership controlled by the Sponsor Group, that owns substantially all of the common stock of EFH Corp. | |

Texas Holdings Group | Texas Holdings and its direct and indirect subsidiaries other than the Oncor Ring-Fenced Entities | |

Texas Transmission | Texas Transmission Investment LLC, a limited liability company that owns a 19.75% equity interest in Oncor and is not affiliated with EFH Corp., any of EFH Corp.'s subsidiaries or any member of the Sponsor Group | |

TRE | Texas Reliability Entity, Inc., an independent organization that develops reliability standards for the ERCOT region and monitors and enforces compliance with NERC standards and ERCOT protocols | |

TXU Energy | TXU Energy Retail Company LLC, a direct, wholly owned subsidiary of TCEH that is a REP in competitive areas of ERCOT and is engaged in the retail sale of electricity to residential and business customers | |

US | United States of America | |

VIE | variable interest entity | |

v

PART I.

Items 1. and 2. BUSINESS AND PROPERTIES

References in this report to "we," "our," "us" and "the company" are to EFH Corp. and/or its subsidiaries, as apparent in the context. See "Glossary" for descriptions of major subsidiaries and other defined terms.

EFH Corp. Business and Strategy

As described more fully below under "Filing under Chapter 11 of the United States Bankruptcy Code," on April 29, 2014 (the Petition Date), EFH Corp. and the substantial majority of its direct and indirect subsidiaries, including EFIH, EFCH and TCEH but excluding the Oncor Ring-Fenced Entities, (the Debtors) filed voluntary petitions for relief (the Bankruptcy Filing) under Chapter 11 of the United States Bankruptcy Code (the Bankruptcy Code) in the United States Bankruptcy Court for the District of Delaware (the Bankruptcy Court). During the pendency of the Bankruptcy Filing (the Chapter 11 Cases), the Debtors will operate their businesses as "debtors-in-possession" under the jurisdiction of the Bankruptcy Court and in accordance with the applicable provisions of the Bankruptcy Code. We intend to conduct our business operations in the normal course and maintain our focus on achieving excellence in customer service and meeting the needs of electricity consumers in Texas.

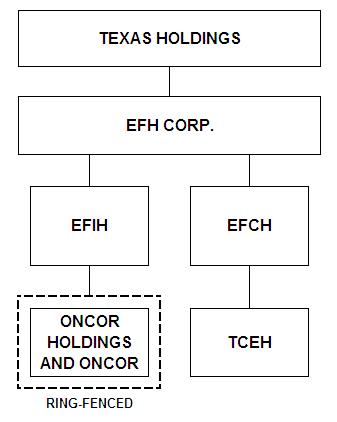

We are a Dallas, Texas-based energy company with a portfolio of competitive and regulated energy businesses in Texas. EFH Corp. is a holding company conducting its operations principally through its TCEH and Oncor subsidiaries. Collectively with its operating subsidiaries, EFH Corp. is the largest generator, retailer and distributor of electricity in Texas. Immediately below is an organization chart of the key subsidiaries discussed in this report.

Texas Holdings, which is controlled by the Sponsor Group, owns substantially all of the common stock of EFH Corp.

EFCH and EFIH are wholly owned by EFH Corp. TCEH is wholly owned by EFCH. EFIH indirectly holds an approximate 80% equity interest in Oncor.

EFCH's principal asset is its investment in TCEH. EFCH is a guarantor of a significant portion of TCEH's debt and $60 million principal amount of EFH Corp.'s debt.

TCEH, through its subsidiaries, is engaged in competitive electricity market activities largely in Texas, including electricity generation, wholesale energy sales and purchases, commodity risk management and trading activities, and retail electricity sales.

TCEH owns 15,427 MW of generation capacity in Texas, which consists of lignite/coal, nuclear and natural gas fueled generation facilities and accounts for approximately 18% of the generation capacity in our market. TCEH is also one of the largest purchasers of wind-generated electricity in Texas and the US. TCEH provides competitive electricity and related services to 1.7 million retail electricity customers in Texas.

1

EFIH's principal asset consists of its investment in Oncor Holdings, the principal asset of which is an 80% equity interest in Oncor. EFIH is also a guarantor of $60 million principal amount of EFH Corp.'s debt.

Oncor is engaged in regulated electricity transmission and distribution operations in Texas that are primarily regulated by the PUCT and, in certain instances, the FERC. Oncor provides transmission and distribution services to REPs, which sell electricity to residential and business consumers, as well as transmission services to electricity distribution companies, cooperatives and municipalities. Oncor operates the largest transmission and distribution system in Texas, delivering electricity to more than 3.2 million homes and businesses and operating more than 120,000 miles of transmission and distribution lines. A significant portion of Oncor's revenues represent fees for services provided to TCEH's retail sales operations. Revenues from services provided to TCEH represented 27% and 29% of Oncor's total reported consolidated revenues for the years ended December 31, 2013 and 2012, respectively.

EFH Corp. and Oncor have implemented certain structural and operational "ring-fencing" measures based on commitments made by Texas Holdings and Oncor to the PUCT to further enhance the credit quality of Oncor Holdings and Oncor. These measures serve to mitigate Oncor's and Oncor Holdings' credit exposure to the Texas Holdings Group with the intent to minimize the risk that a court would order any of the assets and liabilities of the Oncor Ring-Fenced Entities to be substantively consolidated with the assets and liabilities of any member of the Texas Holdings Group in the event any such member were to become a debtor in a bankruptcy case. Accordingly, EFH Corp. and EFIH do not control and do not consolidate Oncor Holdings and Oncor for financial reporting purposes. See Notes 1 and 3 to Financial Statements for a description of the material features of these ring-fencing measures.

At December 31, 2013, we had approximately 9,000 full-time employees (including approximately 3,420 at Oncor). Approximately 2,710 employees are under collective bargaining agreements (including approximately 690 at Oncor).

Filing under Chapter 11 of the United States Bankruptcy Code

On April 29, 2014, EFH Corp. and the substantial majority of its direct and indirect subsidiaries, including EFIH, EFCH and TCEH but excluding the Oncor Ring-Fenced Entities, filed voluntary petitions for relief under Chapter 11 of the United States Bankruptcy Code in the United States Bankruptcy Court for the District of Delaware. During the pendency of the Bankruptcy Filing, the Debtors will operate their businesses as "debtors-in-possession" under the jurisdiction of the Bankruptcy Court and in accordance with the applicable provisions of the Bankruptcy Code.

The Bankruptcy Filing resulted primarily from the adverse effects on EFH Corp.'s competitive businesses of lower wholesale electricity prices in ERCOT driven by the sustained decline in natural gas prices since mid-2008. Further, the remaining natural gas hedges that TCEH entered into when forward market prices of natural gas were significantly higher than current prices mature in 2014. These market conditions challenged the profitability and operating cash flows of EFH Corp.'s competitive businesses and resulted in the inability to support their significant interest payments and debt maturities, including the remaining debt obligations due in 2014, and to refinance and/or extend the maturities of their outstanding debt. These liquidity matters raised substantial doubt about our ability to continue as a going concern without a restructuring of the debt.

In consideration of the liquidity matters discussed above, the report of our independent registered public accounting firm that accompanies our audited consolidated financial statements for the year ended December 31, 2013 included in this annual report contains an explanatory paragraph regarding the substantial doubt about our ability to continue as a going concern.

In 2013, we began to engage in discussions with certain creditors with respect to proposed changes to our capital structure, including the possibility of a consensual, prepackaged restructuring transaction. Because of the recent constructive nature of these discussions, TCEH elected not to make interest payments due in April 2014 totaling $123 million on certain debt obligations. Under the terms of the debt obligations that apply to the substantial majority of the missed interest payments, the lenders had the right to accelerate the payment of the debt if TCEH had not cured the default after an applicable grace period. In consideration of the additional time required to evaluate the effects of events related to the creditor discussions, including potential changes to our capital structure, on the financial statements and disclosures included in EFH Corp.'s, EFCH's and EFIH's Annual Reports on Form 10-K for the year ended December 31, 2013, the companies did not file their Annual Reports on Form 10-K for the year ended December 31, 2013 with the SEC by April 15, 2014, the date when the reports were required to be filed (including an allowed extension), and instead filed those Annual Reports on April 30, 2014. In anticipation of the Bankruptcy Filing, on April 29, 2014, the Debtors entered into a Restructuring Support and Lock-Up Agreement (the Restructuring Support and Lock-Up Agreement) with various stakeholders in order to effect an agreed upon restructuring of the Debtors through a pre-arranged Chapter 11 plan of reorganization (the Restructuring Plan).

2

Restructuring Support and Lock-Up Agreement

General

In anticipation of the Bankruptcy Filing, on April 29, 2014, the Debtors, Texas Holdings and its general partner Texas Energy Future Capital Holdings LLC (TEF and, together with Texas Holdings, the Consenting Interest Holders) and the Consenting Creditors entered into the Restructuring Support and Lock-Up Agreement in order to effect an agreed upon restructuring of the Debtors through the Restructuring Plan.

Pursuant to the Restructuring Support and Lock-Up Agreement, the Consenting Interest Holders and Consenting Creditors agreed, subject to the terms and conditions contained in the Restructuring Support and Lock-Up Agreement, to support the Debtors’ proposed financial restructuring (the Restructuring Transactions), and further agreed to limit certain transfers of any ownership (including any beneficial ownership) in the equity interests of or claims held against the Debtors, including any such interests or claims acquired after executing the Restructuring Support and Lock-Up Agreement.

Material Restructuring Terms

The Restructuring Support and Lock-Up Agreement along with the accompanying term sheet sets forth the material terms of the Restructuring Transactions pursuant to which, in general:

TCEH First Lien Secured Claims

As a result of the Restructuring Transactions, holders of TCEH first lien secured claims will receive, among other things, their pro rata share of (i)100% of the equity of TCEH consummated through a tax-free spin (in accordance with the Private Letter Ruling described below) in connection with TCEH's emergence from bankruptcy (Reorganized TCEH) and (ii) all of the net cash from the proceeds of the issuance of new long-term secured debt of Reorganized TCEH.

TCEH Unsecured Claims

As a result of the Restructuring Transactions, holders of general unsecured claims against EFCH, TCEH and its subsidiaries (including TCEH first lien deficiency claims, TCEH second lien claims and TCEH unsecured note claims) will receive their pro rata share of the unencumbered assets of TCEH.

EFIH First Lien Settlement

Certain holders of EFIH 6.875% Notes and EFIH 10% Notes (such holders, the EFIH First Lien Note Parties) have agreed to voluntary settlements with respect to EFIH's and EFIH Finance's obligations under the EFIH First Lien Notes held by the EFIH First Lien Note Parties. Under the terms of the settlement, each EFIH First Lien Note Party has agreed to accept as payment in full of any claims arising out of its EFIH First Lien Notes an amount of loans under the EFIH First Lien DIP Facility (as discussed in Note 10 to Financial Statements) equal to the greater of (a) 105% of the principal amount on the EFIH First Lien Notes plus 101% of the accrued and unpaid interest at the non-default rate on such principal (which amount will be deemed to include the original issue discount) and (b) 104% of the principal amount of, plus accrued and unpaid interest at the non-default rate on, the EFIH First Lien Notes, in each case held by such EFIH First Lien Note Party. In addition, in the case of (b) above, each EFIH First Lien Note Party will be entitled to original issue discount paid in accordance with the EFIH First Lien Facility. No EFIH First Lien Note Party will receive any other fees, including commitment fees, paid in respect of the EFIH First Lien DIP Facility (such settlement, the EFIH First Lien Settlement).

During the early portion of the Chapter 11 Cases, EFIH expects to:

• | solicit agreement to, and participation in, the EFIH First Lien Settlement from holders of the remaining outstanding EFIH First Lien Notes, other than the EFIH First Lien Note Parties (the EFIH First Lien Settlement Solicitation), and |

• | initiate litigation to obtain entry of an order from the Bankruptcy Court disallowing the claims of holders of EFIH First Lien Notes not a party to the EFIH First Lien Settlement (Non-Settling EFIH First Lien Note Holders) derived from or based upon make-whole or other similar payment provisions under the EFIH First Lien Notes. |

3

Following the completion of the EFIH First Lien Settlement Solicitation, Non-Settling EFIH First Lien Note Holders will receive their pro rata share of cash from the proceeds of the EFIH First Lien DIP Facility in an amount equal to the principal plus accrued and unpaid interest through the closing of the EFIH First Lien DIP Facility, at the non-default rate of such holder's claim (not including any premiums, fees, or claims relating to the repayment of the EFIH First Lien Notes).

EFIH Second Lien Settlement

Certain holders of EFIH 11% Notes and EFIH 11.75% Notes (such holders, the EFIH Second Lien Note Parties) have agreed to voluntary settlements with respect to EFIH's and EFIH Finance's obligations under the EFIH Second Lien Notes held by the EFIH Second Lien Note Parties. Under the terms of the settlement, each EFIH Second Lien Note Party has agreed to accept as payment in full of any claims arising out of its EFIH Second Lien Notes, its pro rata share of an amount in cash equal to (i) 100% of the principal of, plus accrued but unpaid interest at the non-default rate on, EFIH Second Lien Notes held by such EFIH Second Lien Party plus (ii) 50% of the aggregate amount of any claim derived from or based upon make-whole or other similar provisions under the EFIH 11% Notes or EFIH 11.75% Notes (such settlement, the EFIH Second Lien Settlement).

As part of the EFIH Second Lien Settlement, a significant EFIH Second Lien Note Party, but not other EFIH Second Lien Note Parties, will have the right to receive up to $500 million of its payment under the EFIH Second Lien Settlement in the form of loans under the EFIH First Lien DIP Facility. In addition, such EFIH Second Lien Note Party will be entitled to its pro rata share of interest and original issue discount paid in respect of the EFIH First Lien DIP Facility and a 1.75% commitment fee.

During the early portion of the Chapter 11 Cases, EFIH expects to:

• | solicit agreement to, and participation in, the EFIH Second Lien Settlement from holders of the remaining outstanding EFIH Second Lien Notes, other than the EFIH Second Lien Note Parties (the EFIH Second Lien Settlement Solicitation), and |

• | initiate litigation to obtain entry of an order from the Bankruptcy Court disallowing the claims of holders of EFIH Second Lien Notes not a party to the EFIH Second Lien Settlement (Non-Settling EFIH Second Lien Note Holders) derived from or based upon make-whole or other similar payment provisions under the EFIH Second Lien Notes. |

Following the completion of the EFIH Second Lien Settlement Solicitation, Non-Settling EFIH Second Lien Note Holders will receive their pro rata share of cash from the proceeds of the EFIH Second Lien DIP Facility (as described below) in an amount equal to the principal plus accrued and unpaid interest through the closing of the EFIH Second Lien DIP Facility, at the non-default rate of such holder’s claim (not including any premiums, fees, or claims relating to the repayment of the EFIH Second Lien Notes).

EFIH Second Lien DIP Notes Offering

During the early portion of the Chapter 11 Cases, EFIH and EFIH Finance expect to offer (the EFIH Second Lien DIP Notes Offering) to all holders as of a specified record date of EFIH Unsecured Notes the right to purchase up to its pro rata percentage of $1.73 billion aggregate principal amount of 8% Mandatorily Convertible Second Lien Subordinated Secured DIP Financing Tranche A-1 Notes due 2016 (EFIH Second Lien DIP Tranche A-1 Notes). Concurrently with the EFIH Second Lien DIP Notes Offering, EFIH and EFIH Finance will also offer (the concurrent offering) to a significant EFIH Second Lien Note Party the right to purchase up to $170 million aggregate principal amount of 8% Mandatorily Convertible Second Lien Subordinated Secured DIP Financing Tranche A-3 Notes due 2016 (EFIH Second Lien DIP Tranche A-3 Notes). If such significant EFIH Second Lien Note Party elects to participate in the offering, EFIH will pay such party $11.3 million. To the extent the Backstop Parties are required to purchase any notes in the offering pursuant to the terms of the Commitment Letter (as described below), such notes will be 8% Mandatorily Convertible Second Lien Subordinated Secured DIP Financing Tranche A-2 Notes due 2016 (EFIH Second Lien DIP Tranche A-2 Notes). The EFIH Second Lien DIP Tranche A-1 Notes, the EFIH Second Lien DIP Tranche A-2 Notes and the EFIH Second Lien DIP Tranche A-3 Notes are expected to have the same terms and conditions (other than (i) the ability to trade as a single tranche, (ii) the EFIH Second Lien Tranche A-1 Notes will trade together with the corresponding EFIH Unsecured Notes and (iii) the EFIH Second Lien Tranche A-2 Notes and EFIH Second Lien Tranche A-3 Notes will not trade together with any other notes).

4

Backstop Commitment

In connection with the execution of the Restructuring Support and Lock-Up Agreement, certain holders of the EFIH Unsecured Notes (the Backstop Parties) have entered into a commitment letter with EFH Corp. and EFIH, dated April 29, 2014 (the Commitment Letter), pursuant to which such holders have committed, severally and not jointly, up to $2.0 billion in available funds (the Backstop Commitment) to purchase EFIH Second Lien DIP Notes. Any EFIH Second Lien DIP Notes not sold in the EFIH Second Lien DIP Notes Offering and the concurrent offering (unpurchased notes) will be purchased by the Backstop Parties, pro rata in proportion to their respective share of the Backstop Commitment. If any Backstop Party fails to satisfy its obligation to purchase its pro rata share of the unpurchased notes, the other Backstop Parties would have the right, but not the obligation, to purchase such unpurchased notes. The obligations under the Commitment Letter are not subject to the approval of the Oncor TSA Amendment (as described below) by the Bankruptcy Court.

Under the Commitment Letter and in consideration of the Backstop Commitment, EFIH agreed to pay the Backstop Parties a commitment fee consisting of (i) a $10 million execution fee that was paid to the Backstop Parties concurrently with the execution of the Commitment Letter, (ii) a $10 million approval fee to be paid within five days of the issuance of an order by the Bankruptcy Court authorizing the EFIH First Lien Settlement, the EFIH Second Lien Settlement, and the performance by EFH Corp. and EFIH under the Commitment Letter, (iii) a $20 million funding fee to be paid concurrently with the consummation of the EFIH Second Lien DIP Notes Offering to holders of EFIH Unsecured Notes and the concurrent offering and (iv) a fee equal to $100 million payable in the form of Non-Interest Bearing Mandatorily Convertible Second Lien Subordinated Secured DIP Financing Tranche B Notes due 2016 (EFIH Second Lien DIP Tranche B Notes and, together with the EFIH Second Lien DIP Tranche A-1 Notes, the EFIH Second Lien DIP Tranche A-2 Notes and the EFIH Second Lien DIP Tranche A-3 Notes, the EFIH Second Lien DIP Notes) to be paid concurrently with the consummation of the EFIH Second Lien DIP Notes Offering to holders of EFIH Unsecured Notes and the concurrent offering. Other than with respect to the requirement not to pay interest and related mechanics and not trading together with any other debt, the EFIH Second Lien DIP Tranche B Notes are expected to have the same terms and conditions as the EFIH Second Lien DIP Tranche A-1 Notes, the EFIH Second Lien DIP Tranche A-2 Notes and the EFIH Second Lien DIP Tranche A-3 Notes.

In the event the EFIH Second Lien DIP Notes are repaid in cash prior to the effective date of the plan of reorganization (Effective Date), EFIH agreed to pay the Backstop Parties a termination fee of $380 million. In addition, if the EFIH Second Lien DIP Notes Offering is not consummated at the option of EFIH, EFIH agreed to pay the Backstop Parties a break-up fee of $60 million.

EFIH Unsecured Claims and EFH Corp. Unsecured Claims

On the Effective Date, all of the EFIH Unsecured Notes and EFH Corp. Unsecured Notes will be canceled. In full satisfaction of the claims under the EFIH Unsecured Notes and the EFH Corp. Unsecured Notes, (i) each holder of EFIH Unsecured Notes will receive its pro rata share of 98.0% of the equity interests of newly reorganized EFH Corp. (Reorganized EFH Corp.) (subject to dilution by the Equity Conversion as described below) and (ii) each holder of EFH Corp. Unsecured Notes will receive its pro rata share of 1.0% of the equity interests of Reorganized EFH Corp. (subject to dilution by the Equity Conversion).

Holders of the EFH Corp. Unsecured Notes will also receive on the Effective Date their pro rata share of either (A) if the Oncor TSA Amendment (described below) has then been approved, (1) $55 million in cash from EFIH, provided, however, that if the Oncor tax payments received by EFIH under the Oncor TSA Amendment through the Effective Date are less than 80% of projected amounts, the $55 million payment will be reduced on a dollar for dollar basis by the amount of such shortfall, and (2) cash on hand at EFH Corp. (not including the settlement payment in clause (1) hereof); or (B) if the Oncor TSA Amendment has not then been approved, all assets of EFH Corp., including cash on hand but excluding the equity interests in EFIH.

EFH Corp. Equity Interests

On the Effective Date, all of the equity interests in EFH Corp. (EFH Corp. Interests) will be canceled. In full satisfaction of the claims under the EFH Corp. Interests, each holder of EFH Corp. Interests will receive its pro rata share of 1.0% of the equity interests of Reorganized EFH Corp. (subject to dilution by the Equity Conversion).

Equity Conversion

On the Effective Date, the EFIH Second Lien DIP Notes will automatically convert (Equity Conversion) on a pro rata basis into approximately 64% of the equity interests of Reorganized EFH Corp.

5

Oncor TSA Amendment

The Restructuring Support and Lock-Up Agreement provides that the Debtors will request authority from the Bankruptcy Court to amend, or otherwise assign the right to payments under, the Oncor Tax Sharing Agreement (the Oncor TSA Amendment) to provide that any payment required to be made to EFH Corp. under the Oncor Tax Sharing Agreement after March 31, 2014, will instead be made to EFIH. Any tax payments received by EFH Corp. before the Bankruptcy Court enters or denies an order authorizing the Oncor TSA Amendment will be deposited by EFH Corp. into a segregated account until the earlier of (i) the date the Bankruptcy Court enters the order authorizing the Oncor TSA Amendment, in which case such amounts will be remitted to EFIH, or (ii) the date the Bankruptcy Court denies authorization of the Oncor TSA Amendment, in which case such amounts will be remitted to EFH Corp.

The Oncor TSA Amendment will automatically terminate and be of no further force and effect in the event that the Commitment Letter is terminated by the Backstop Parties; provided, however, that any amounts that were paid to EFIH in accordance with the Oncor TSA Amendment before its termination will be retained by EFIH if the Commitment Letter terminates or the EFIH Second Lien DIP Facility is not fully funded in accordance with its terms (i.e., except as a result of a breach by the Backstop Parties). Neither EFH Corp. nor EFIH will have the right to terminate or modify the Oncor TSA Amendment during the Chapter 11 Cases if the EFIH Second Lien DIP Facility is consummated.

If the Bankruptcy Court has not approved the Oncor TSA Amendment within 90 days after the Petition Date, the interest rate on the EFIH Second Lien DIP Tranche A-1 Notes, EFIH Second Lien DIP Tranche A-2 Notes and EFIH Second Lien DIP Tranche A-3 Notes will increase by 4.0% with such additional interest to be paid-in-kind (compounded quarterly) until such approval is received from the Bankruptcy Court. If the Bankruptcy Court has not approved the Oncor TSA Amendment by May 1, 2015, each holder of EFIH Second Lien DIP Notes will receive additional EFIH Second Lien DIP Notes equal to 10.0% of the amount of EFIH Second Lien DIP Notes held by such holder.

Private Letter Ruling

The Restructuring Support and Lock-Up Agreement provides that EFH Corp. will file a request with the IRS for a private letter ruling (Private Letter Ruling) that, among other things, will provide (a) that (i) the transfer by TCEH of all of its assets and its ordinary course operating liabilities to Reorganized TCEH, (ii) the transfer by the Debtors to Reorganized TCEH of certain operating assets and liabilities that are reasonably necessary to the operation of Reorganized TCEH and (iii) the distribution by TCEH of (A) the equity it holds in Reorganized TCEH and (B) the cash proceeds TCEH receives from Reorganized TCEH to the holders of TCEH First Lien Claims will qualify as a "reorganization" within the meaning of Sections 368(a)(1)(G) , 355 and 356 of the Code and (b) for certain other rulings under Sections 368(a)(1)(G) and 355 of the Code.

Conditions Precedent to Restructuring Transactions

The Restructuring Support and Lock-Up Agreement provides that the consummation of the Restructuring Transactions is subject to the satisfaction or waiver (if applicable) of various conditions, including, among other things:

• | the consummation of the debtor-in-possession financing transactions and settlements described above; |

• | holders of certain EFH Unsecured Notes shall have received not less than 37.15% in value for their respective claims under the plan of reorganization; |

• | immediately following the distribution by TCEH described above under the heading "Private Letter Ruling", the aggregate tax basis, for federal income tax purposes, of the assets held by Reorganized TCEH will be equal to a specified minimum amount of aggregate tax basis, and the step-up in aggregate tax basis will be no less than $2.1 billion; |

• | the receipt of requisite regulatory approvals; |

• | the receipt of the Private Letter Ruling, and |

• | the receipt of requisite orders from the Bankruptcy Court. |

6

Termination

The Restructuring Support and Lock-Up Agreement may be terminated upon the occurrence and continuation of certain events described in the Restructuring Support and Lock-Up Agreement.

For additional discussion of the Bankruptcy Filing and its effects, see Item 7, "Management's Discussion and Analysis of Financial Condition and Results of Operations – Significant Activities and Events and Items Influencing Future Performance – Filing under Chapter 11 of the United States Bankruptcy Code" and Item 1A, "Risk Factors – Risks Related to Filing under Chapter 11 of the United States Bankruptcy Code." See Note 10 to Financial Statements for discussion of the DIP Facilities.

EFH Corp.'s Market

We operate primarily within the ERCOT market. This market represents approximately 85% of the electricity consumption in Texas. ERCOT is the regional reliability coordinating organization for member electricity systems in Texas and the Independent System Operator of the interconnected transmission grid for those systems. ERCOT's membership consists of more than 300 corporate and associate members, including electric cooperatives, municipal power agencies, independent generators, independent power marketers, investor-owned utilities, REPs and consumers.

The ERCOT market operates under reliability standards set by the NERC. The PUCT has primary jurisdiction over the ERCOT market to ensure adequacy and reliability of power supply across Texas' main interconnected transmission grid. ERCOT is responsible for scheduling power on the grid and maintaining reliable operations of the electricity supply system in the market. Its responsibilities include centralized dispatch of the power pool and ensuring that electricity production and delivery are accurately accounted for among the generation resources and wholesale buyers and sellers. ERCOT also serves as agent for procuring ancillary services for those members who elect not to provide their own ancillary services.

Oncor, along with other owners of transmission and distribution facilities in Texas, assists ERCOT in its operations. Oncor has planning, design, construction, operation and maintenance responsibility for the portion of the transmission grid and for the load-serving substations it owns, primarily within its certificated distribution service area. Oncor participates with ERCOT and other ERCOT utilities in obtaining regulatory approvals and planning, designing and constructing new transmission lines in order to remove existing constraints and interconnect generation on the ERCOT transmission grid. The new transmission lines are necessary to meet reliability needs, support renewable energy production and increase bulk power transfer capability.

Installed generation capacity in the ERCOT market for the year 2013 totaled approximately 84,500 MW, including approximately 2,000 MW mothballed (idled) capacity and more than 11,500 MW of wind and other resources that may not be available coincident with system need. Texas has more installed wind generation capacity than any other state in the US. In 2013, ERCOT's hourly demand peaked at 67,245 MW as compared to peak demand of 66,548 MW in 2012. Of ERCOT's total installed capacity, approximately 59% is natural gas fueled generation, approximately 28% is lignite/coal and nuclear fueled generation and approximately 13% is wind and other renewable resources.

The ERCOT market has limited interconnections to other markets in the US and Mexico, which currently limits potential imports into and exports out of the ERCOT market to 1,106 MW of generation capacity (or approximately 2% of peak demand). In addition, wholesale transactions within the ERCOT market are generally not subject to regulation by the FERC.

Natural gas fueled generation is the predominant electricity capacity resource (approximately 59%) in the ERCOT market and accounted for approximately 41% of the electricity produced in the ERCOT market in 2013. Because of the significant amount of natural gas fueled capacity and the ability of such facilities to more readily increase or decrease production when compared to nuclear and lignite/coal fueled generation, marginal demand for electricity in ERCOT is usually met by natural gas fueled facilities. As a result, wholesale electricity prices in ERCOT have generally moved with natural gas prices.

7

EFH Corp.'s Strategies

Each of our businesses focuses its operations on key safety, reliability, economic and environmental drivers for that business, as described below:

• | TCEH focuses on optimizing and developing its generation fleet to safely provide reliable electricity supply in a cost-effective manner and in consideration of environmental impacts, hedging its commodity price and volume exposure and providing high quality service and innovative energy products to retail and wholesale customers. |

• | Oncor focuses on delivering electricity in a safe and reliable manner, minimizing service interruptions and investing in its transmission and distribution infrastructure to maintain its system, serve its growing customer base with a modernized grid and support renewable energy production. |

Other elements of our strategies include:

• | Increase value from existing business lines. We strive for top-tier performance across our operations in terms of safety, reliability, cost and customer service. In establishing strategic objectives, we incorporate the following core operating principles: |

• | Safety: Placing the safety of communities, customers and employees first; |

• | Environmental Stewardship: Continuing to make strategic and operational improvements that lead to cleaner air, land and water; |

• | Customer Focus: Delivering products and superior service to help customers more effectively manage their use of electricity; |

• | Community Focus: Being an integral part of the communities in which we live, work and serve; |

• | Operational Excellence: Incorporating continuous improvement and financial discipline in all aspects of the business to achieve top-tier results that maximize the value of the company for stakeholders, including operating world-class facilities that produce and deliver safe and dependable electricity at affordable prices, and |

• | Performance-Driven Culture: Fostering a strong values- and performance-based culture designed to attract, develop and retain best-in-class talent. |

• | Drive and support growth of the ERCOT market. We expect to pursue growth opportunities across our existing business lines, including: |

• | Pursuing generation development opportunities to help meet ERCOT's growing electricity needs over the longer term from a diverse range of energy sources such as natural gas, nuclear and renewable energy. |

• | Working with ERCOT and other market participants to develop policies and protocols that provide appropriate pricing signals that incent the development of new generation to meet growing electricity demand in the ERCOT market. |

• | Profitably increasing the number of retail customers served throughout the competitive ERCOT market areas by delivering superior value through high quality customer service and innovative energy products, including leading energy efficiency initiatives and service offerings. |

• | Investing in transmission and distribution and constructing new transmission and distribution facilities to meet the needs of the growing Texas market. |

• | Manage exposure to wholesale electricity price volatility. We actively manage our exposure to wholesale electricity prices in ERCOT through contracts for physical delivery of electricity, exchange traded and over-the-counter financial contracts, ERCOT day-ahead market transactions and bilateral contracts with other wholesale market participants, including other generators and end-use customers. These hedging activities include shorter-term agreements, longer-term electricity sales contracts and forward sales of natural gas. The historical relationship between natural gas prices and wholesale electricity prices in the ERCOT market has provided us an opportunity to manage our exposure to variability of wholesale electricity prices through natural gas hedging activities. For discussion of natural gas hedging activities, see Item 7, "Management's Discussion and Analysis of Financial Condition and Results of Operations – Significant Activities and Events and Items Influencing Future Performance – Natural Gas Hedging Program." |

8

• | Pursue new environmental initiatives. We are committed to continue to operate in compliance with all environmental laws, rules and regulations and to reduce our impact on the environment. EFH Corp.'s Sustainable Energy Advisory Board advises us in our pursuit of technology development opportunities that reduce our impact on the environment while balancing the need to help address the energy requirements of Texas. The Sustainable Energy Advisory Board is comprised of individuals who represent the following interests, among others: environmental conservation, labor unions, customers, economic development in Texas and technology/reliability standards. See "Environmental Regulations and Related Considerations" below for discussion of actions we are taking to reduce emissions from our generation facilities and our investments in energy efficiency and related initiatives. |

Seasonality

Our revenues and results of operations are subject to seasonality, weather conditions and other electricity usage drivers, with revenues being highest in the summer.

9

Operating Segments

We have aligned and report our business activities as two operating segments: the Competitive Electric segment, consisting largely of TCEH and its subsidiaries, and the Regulated Delivery segment, consisting largely of our investment in Oncor. See Note 18 to Financial Statements for additional financial information for the segments.

Competitive Electric Segment

Key activities, including management of risks related to commodity price and availability, as well as electricity sourcing for our retail and wholesale customers, are performed on an integrated basis. This integration strategy, the execution of which is discussed below in describing the activities of our wholesale operations, is a key consideration in our operating segment determination. For purposes of market identity and operational accountability, our operations are grouped and identified as Luminant, which is engaged in electricity generation and wholesale markets activities, and TXU Energy, which is engaged in retail electricity sales activities. These activities are conducted through separate legal entities.

Luminant — Luminant's existing electricity production fleet consists of 40 generation units in Texas, all of which are owned, with total installed nameplate generating capacity as shown in the table below:

Fuel Type | Installed Nameplate Capacity (MW) | Number of Plant Sites | Number of Units | |||||

Nuclear | 2,300 | 1 | 2 | |||||

Lignite/coal | 8,017 | 5 | 12 | |||||

Natural gas (a) | 5,110 | 8 | 26 | |||||

Total | 15,427 | 14 | 40 | |||||

___________

(a) | Includes 1,655 MW representing four units mothballed and not currently available for dispatch. See "Natural Gas Fueled Generation Operations" below. |

The generation units are located primarily on owned land. Nuclear and lignite/coal fueled units are generally scheduled to run at capacity except for periods of scheduled maintenance activities; however, we reduce production from certain lignite/coal fueled generation units, referred to as economic backdown, during periods when wholesale electricity market prices are less than the unit's variable production costs. In addition, we have implemented seasonal suspensions of operations of certain lignite/coal fueled generation units because of the low wholesale electricity price environment. The natural gas fueled generation units supplement the nuclear and lignite/coal fueled generation capacity in meeting consumption in peak demand periods as production from certain of these units, particularly combustion-turbine units, can be more readily ramped up or down as demand warrants.

Nuclear Generation Operations — Luminant operates two nuclear generation units at the Comanche Peak plant site, each of which is designed for a capacity of 1,150 MW. Comanche Peak's Unit 1 and Unit 2 went into commercial operation in 1990 and 1993, respectively, and are generally operated at full capacity. Refueling (nuclear fuel assembly replacement) outages for each unit are scheduled to occur every eighteen months during the spring or fall off-peak demand periods. Every three years, the refueling cycle results in the refueling of both units during the same year, which will occur in 2014 and last occurred in 2011. While one unit is undergoing a refueling outage, the remaining unit is intended to operate at full capacity. During a refueling outage, other maintenance, modification and testing activities are completed that cannot be accomplished when the unit is in operation. Over the last three years the refueling outage period per unit has ranged from 22 to 29 days. The Comanche Peak facility operated at a capacity factor of 101.7%, 98.5% and 95.7% in 2013, 2012 and 2011, respectively.

Luminant has contracts in place for all of its uranium and nuclear fuel conversion, enrichment and fabrication services for 2014. For the period of 2015 through 2019, Luminant has contracts in place for the acquisition of approximately 66% of its uranium requirements and 81% of its nuclear fuel conversion services requirements. In addition, Luminant has contracts in place for all of its nuclear fuel enrichment services through 2019, as well as all of its nuclear fuel fabrication services through 2018. Luminant does not anticipate any significant difficulties in acquiring uranium and contracting for associated conversion and enrichment services in the foreseeable future.

10

The nuclear industry has developed ways to store used nuclear fuel on site at nuclear generation facilities, primarily through the use of dry cask storage, since there are no facilities for reprocessing or disposal of used nuclear fuel currently in operation in the US. Luminant stores its used nuclear fuel on-site in storage pools or dry cask storage facilities and believes its on-site used nuclear fuel storage capability is sufficient for the foreseeable future.

The Comanche Peak nuclear generation units have an estimated useful life of 60 years from the date of commercial operation. Therefore, assuming that Luminant receives 20-year license extensions, similar to what has been granted by the NRC to several other commercial generation reactors over the past several years, decommissioning activities would be scheduled to begin in 2050 for Comanche Peak Unit 1 and 2053 for Unit 2 and common facilities. Decommissioning costs will be paid from a decommissioning trust that, pursuant to Texas law, is intended to be fully funded from Oncor's customers through an ongoing delivery surcharge. (See Note 19 to Financial Statements for discussion of the decommissioning trust fund.) Under applicable law, the Bankruptcy Filing is not expected to have any effect on the collection of such surcharge or the ongoing viability of the decommissioning trust.

Nuclear insurance provisions are discussed in Note 11 to Financial Statements.

Nuclear Generation Development — In 2008, we filed a combined operating license application with the NRC for two new nuclear generation units, each with approximately 1,700 MW (gross capacity), at our existing Comanche Peak nuclear plant site. In connection with the filing of the application, in 2009, subsidiaries of TCEH and Mitsubishi Heavy Industries Ltd. (MHI) formed a joint venture, Comanche Peak Nuclear Power Company LLC (CPNPC), to further the development of the two new nuclear generation units using MHI's US-Advanced Pressurized Water Reactor (US-APWR) technology. The TCEH subsidiary owns an 88% interest in CPNPC, and an MHI subsidiary owns a 12% interest.

In the fourth quarter 2013, MHI notified us and the NRC of its plans to refocus MHI's US resources on the restart of 24 nuclear reactors in Japan and thus reduce its support of review activities related to the NRC's Design Certification of MHI's US-APWR technology. As a result, Luminant has notified the NRC of its intent to suspend all reviews associated with the combined operating license application by March 31, 2014. Luminant does not intend to withdraw the license application at this time. MHI expressed to the NRC its continuing commitment to obtaining an NRC design certification for its technology. Luminant has filed a loan guarantee application with the DOE for financing the proposed units prior to commencement of construction and expects to continue to update the application in accordance with the loan solicitation guidelines. See Note 8 to Financial Statements for discussion of impairment of the joint venture's assets.

Lignite/Coal Fueled Generation Operations — Luminant's lignite/coal fueled generation fleet capacity totals 8,017 MW and consists of the Big Brown (2 units), Monticello (3 units), Martin Lake (3 units), Oak Grove (2 units) and Sandow (2 units) plant sites. Maintenance outages at these units are scheduled during seasonal off-peak demand periods. Over the last three years, the total annual scheduled and unscheduled outages per unit averaged 40 days in duration. Luminant's lignite/coal fueled generation fleet operated at a capacity factor of 74.1% in 2013, 70.0% in 2012 and 83.5% in 2011. This performance reflects increased economic backdown of the units and the seasonal suspension of operations of certain units as discussed above.

Luminant is the seventh-largest coal miner in the US and the largest lignite coal miner in Texas. Luminant's mining activity supports generation at its lignite/coal fueled units. Approximately 68% of the fuel used at Luminant's lignite/coal fueled generation units in 2013 was supplied from surface-minable lignite reserves dedicated to our generation plants, which are located adjacent to the reserves. Luminant owns or has under lease an estimated 715 million tons of lignite reserves dedicated to our generation plants, including an undivided interest in approximately 175 million tons of lignite reserves that provide fuel for the Sandow facility. Luminant also owns or has under lease approximately 85 million tons of reserves not currently dedicated to specific generation plants. In 2013, Luminant recovered approximately 29 million tons of lignite to fuel its generation plants. Luminant utilizes owned and/or leased equipment to remove the overburden and recover the lignite.

Luminant's lignite mining operations include extensive reclamation activities that return the land to productive uses such as wildlife habitats, commercial timberland and pasture land. In 2013, Luminant reclaimed more than 2,300 acres of land. In addition, Luminant planted 1.5 million trees in 2013, the majority of which were part of the reclamation effort.

Luminant meets its fuel requirements for its Big Brown, Monticello and Martin Lake generation units by blending lignite with western coal from the Powder River Basin in Wyoming. The coal is purchased from multiple suppliers under contracts of various lengths and is transported from the Powder River Basin to Luminant's generation plants by railcar. Based on its current planned usage, Luminant believes that it has sufficient lignite reserves for the foreseeable future and has contracted the majority of its anticipated western coal requirements and all of the related transportation through 2014.

11

See "Environmental Regulations and Related Considerations – Sulfur Dioxide, Nitrogen Oxide and Mercury Air Emissions" for discussion of potential effects of recent EPA rules on future operations of our generation units.

Natural Gas Fueled Generation Operations — Luminant owns a fleet of 26 natural gas fueled generation units, of which 11 are steam generation units totaling 4,135 MW of capacity and 15 are combustion turbine generation units totaling 975 MW of capacity. Of the steam generation units, four units representing 1,655 MW of capacity are currently mothballed (idled). The natural gas fueled units predominantly serve as peaking units that can be ramped up or down to balance electricity supply and demand.

Natural Gas Fueled Generation Development — In August 2013, the TCEQ granted air permits to Luminant to build two natural gas combustion turbine generation units totaling 420 MW to 460 MW at its existing DeCordova generation facility. In February 2014, the TCEQ granted air permits to Luminant to build two natural gas combustion turbine generation units totaling 420 MW to 460 MW at its existing Tradinghouse generation facility. In January 2014, Luminant filed an air permit application with the TCEQ to build a combined cycle natural gas turbine generation unit totaling 730 MW to 810 MW at its existing Eagle Mountain generation facility. In February 2014, Luminant filed an air permit application with the TCEQ to build two natural gas combustion turbine generation units totaling 420 MW to 460 MW at its existing Lake Creek generation facility. While we believe current market conditions do not provide adequate economic returns for the development or construction of these facilities, we believe additional generation resources will be needed to support future electricity demand growth and reliability in the ERCOT market. See "Management's Discussion and Analysis of Financial Condition and Results of Operations – Significant Activities and Events and Items Influencing Future Performance – Recent PUCT/ERCOT Actions" for discussion of recent actions by the PUCT and ERCOT related to generation resource adequacy.

Wholesale Operations — Luminant's wholesale operations play a pivotal role in our Competitive Electric segment portfolio by optimally dispatching the generation fleet, procuring fuels for the generation fleet, sourcing all of TXU Energy's electricity requirements and managing commodity risk for the retail and wholesale electricity sales operations.

Our electricity price exposure is managed across the complementary generation, wholesale and retail operations on an integrated portfolio basis. Under this approach, Luminant's wholesale operations manage the risks of imbalances between generation supply and sales load, as well as exposures to natural gas price movements and market heat rate changes (variations in the relationships between natural gas prices and wholesale electricity prices), through wholesale market activities that include physical purchases and sales and transacting in financial instruments.

Luminant's wholesale operations provide TXU Energy and other retail and wholesale customers with electricity-related services to meet their demands and the operating requirements of ERCOT. In consideration of electricity generation resource availability and consumer demand levels that can be highly variable, as well as opportunities to meet longer-term objectives of larger wholesale market participants, Luminant buys and sells electricity in short-term transactions and executes longer-term forward electricity purchase and sales agreements. Luminant is also one of the largest purchasers of wind-generated electricity in Texas and the US with approximately 700 MW of existing wind power under contract.

Fuel price exposure, primarily relating to Powder River Basin coal, natural gas, uranium and fuel oil, as well as fuel transportation costs, is managed primarily through short- and long-term contracts for physical delivery of fuel as well as financial contracts.

In its hedging activities, Luminant enters into contracts for the physical delivery of electricity and fuel commodities, exchange traded and over-the-counter financial contracts and bilateral contracts with other wholesale market participants, including generators and end-use customers. A significant element of these activities involves natural gas hedging, described above under "EFH Corp.'s Strategies," designed to reduce exposure to changes in future electricity prices due to changes in the price of natural gas, principally utilizing natural gas-related financial instruments.

The wholesale operations also dispatch Luminant's available generation capacity. These dispatching activities include economic backdown of lignite/coal fueled units and ramping up and down of natural gas fueled units as market conditions warrant. Luminant's dispatching activities are performed on a centrally managed real-time basis optimizing operational activities across the fleet and interfacing with various wholesale market channels. In addition, the wholesale operations manage the fuel procurement requirements for Luminant's fossil fuel and nuclear generation facilities.

Luminant's wholesale operations include electricity and natural gas trading and third-party energy management activities. Natural gas transactions include direct purchases from natural gas producers, transportation agreements, storage leases and commercial retail sales. Luminant currently manages approximately 10.5 billion cubic feet of natural gas storage capacity.

12

Luminant's wholesale operations manage exposure to wholesale commodity and credit-related risk within established transactional risk management policies, limits and controls. These policies, limits and controls have been structured so that they are practical in application and consistent with stated business objectives. Risk management processes include capturing transaction data, monitoring transaction types and notional limits, reviewing and managing credit risk, performing and validating valuations and reporting exposures on a daily basis using risk management information systems designed to support a large transactional portfolio. A risk management forum meets regularly to ensure that business practices comply with approved transactional limits, commodities, instruments, exchanges and markets. Transactional risks are monitored to ensure limits comply with the established risk policy. Risk management also includes a disciplinary program to address any violations of the risk management policies and periodic reviews of these policies to ensure they are responsive to changing market and business conditions.

TXU Energy — TXU Energy serves 1.7 million residential and commercial retail electricity customers in Texas. Approximately 69% of our reported retail revenues in 2013 represented sales to residential customers. Texas is one of the fastest growing states in the nation with a diverse economy and, as a result, has attracted a number of competitors into the retail electricity market; consequently, competition is robust. TXU Energy, as an active participant in this competitive market, provides retail electric service to all areas of the ERCOT market now open to competition, including the Dallas/Fort Worth, Houston, Corpus Christi, and lower Rio Grande Valley areas of Texas and holds an approximately 26% and 19% share of the residential and business customers in ERCOT, respectively. TXU Energy competitively markets its services to add new customers and retain its existing customer base, as well as opportunistically acquire customers from other REPs. There are more than 100 REPs certified to compete within the ERCOT region. Based upon data published by the PUCT, at September 30, 2013, approximately 62% of residential customers and 69% of small commercial customers in competitive areas of ERCOT are served by REPs not affiliated with the pre-competition utility. TXU Energy is a REP affiliated with a pre-competition utility, considering EFH Corp.'s history prior to the deregulation of the Texas market.

TXU Energy's strategy focuses on providing its customers with high quality customer service and creating new products and services to meet customer needs; accordingly, customer care enhancements are implemented on an ongoing basis to continually improve customer satisfaction. TXU Energy offers a wide range of residential products to meet varying customer needs and has invested more than $100 million in energy efficiency initiatives since the Merger as part of a program to offer customers a broad set of innovative energy products and services.

Regulation — Luminant is an exempt wholesale generator under the Energy Policy Act of 2005 and is subject to the jurisdiction of the NRC with respect to its nuclear generation units. NRC regulations govern the granting of licenses for the construction and operation of nuclear fueled generation facilities and subject such facilities to continuing review and regulation. In addition, Luminant is subject to the jurisdiction of the RCT's oversight of its lignite mining and reclamation operations.

Luminant is also subject to the jurisdiction of the PUCT's oversight of the competitive ERCOT wholesale electricity market. PUCT rules establish a framework for and robust oversight of wholesale power pricing and market behavior. Luminant is also subject to the requirements of the ERCOT Nodal Protocols as well as reliability standards adopted and enforced by the TRE and the NERC, including NERC critical infrastructure protection (CIP) standards. Luminant is also subject to the authority of the CFTC as it continues to implement rules and provide oversight vested in the agency by the Wall Street Reform and Consumer Protection Act of 2010, particularly Title VII, which deals with over-the-counter derivative markets.

TXU Energy is a licensed REP under the Texas Electric Choice Act and is subject to the jurisdiction of the PUCT with respect to provision of electricity service in ERCOT. PUCT rules govern the granting of licenses for REPs, including oversight but not setting of retail prices. TXU Energy is also subject to the requirements of the ERCOT Nodal Protocols as well as reliability standards adopted and enforced by the TRE and the NERC, including NERC CIP standards.

13

Regulated Delivery Segment

The Regulated Delivery segment consists largely of our investment in Oncor. Oncor is a regulated electricity transmission and distribution company that provides the service of delivering electricity safely, reliably and economically to end-use consumers through its electrical systems, as well as providing transmission grid connections to merchant generation facilities and interconnections to other transmission grids in Texas. Oncor's service territory comprises 91 counties and over 400 incorporated municipalities, including Dallas/Fort Worth and surrounding suburbs, as well as Waco, Wichita Falls, Odessa, Midland, Tyler and Killeen. Oncor's transmission and distribution assets are located principally in the north-central, eastern and western parts of Texas. Most of Oncor's power lines have been constructed over lands of others pursuant to easements or along public highways, streets and rights-of-way as permitted by law. Oncor's transmission and distribution rates are regulated by the PUCT.

Oncor is not a seller of electricity, nor does it purchase electricity for resale. It provides transmission services to electricity distribution companies, cooperatives and municipalities. It provides distribution services to REPs, including subsidiaries of TCEH, which sell electricity to residential, business and other consumers. Oncor is also subject to the requirements of the ERCOT Nodal Protocols as well as reliability standards adopted and enforced by the TRE and the NERC, including NERC CIP standards.

Performance — Oncor achieved or exceeded market performance protocols in 12 out of 14 PUCT market metrics in 2013. These metrics measure the success of transmission and distribution companies in facilitating customer transactions in the competitive Texas electricity market.