ITEM 1A. RISK FACTORS

Many factors may have an effect on our business, results of operations, financial condition and cash flows. We are subject to various risks resulting from changing economic, environmental, political, industry, business and financial conditions. The factors, as may be exacerbated by the impact of the COVID-19 pandemic, described below represent our principal risks.

Global and National Risks Related to our Business

Our industry, as well as the industries of many of our customers and suppliers upon whom we are dependent, is affected by domestic and global economic factors including periods of slower than anticipated economic growth and the risk of a recession.

Our financial results are substantially dependent not only upon overall economic conditions in the United States and globally, including North America, Europe and in Asia, but also as they may affect one or more of the industries upon which we depend for the sale of our products. Global or domestic actions or conditions, including political actions, trade policies or restrictions, such as the United States-Mexico-Canada Agreement (USMCA), changes in tax laws, terrorism, natural disasters, or pandemics, epidemics, widespread illness or other health issues, such as COVID-19, could result in changing economic conditions in the United States and globally, disruptions to or slowdowns in our business or our global or domestic industry, or those of our customers or suppliers upon whom we are dependent. Additionally, periods of slower than anticipated economic growth could reduce customer confidence and adversely affect demand for our products and further adversely affect our business, results of operations, financial condition and cash flows. Metals industries have historically been vulnerable to significant declines in consumption and product pricing during periods of economic downturn or continued uncertainty, including the pace of domestic non-residential construction activity.

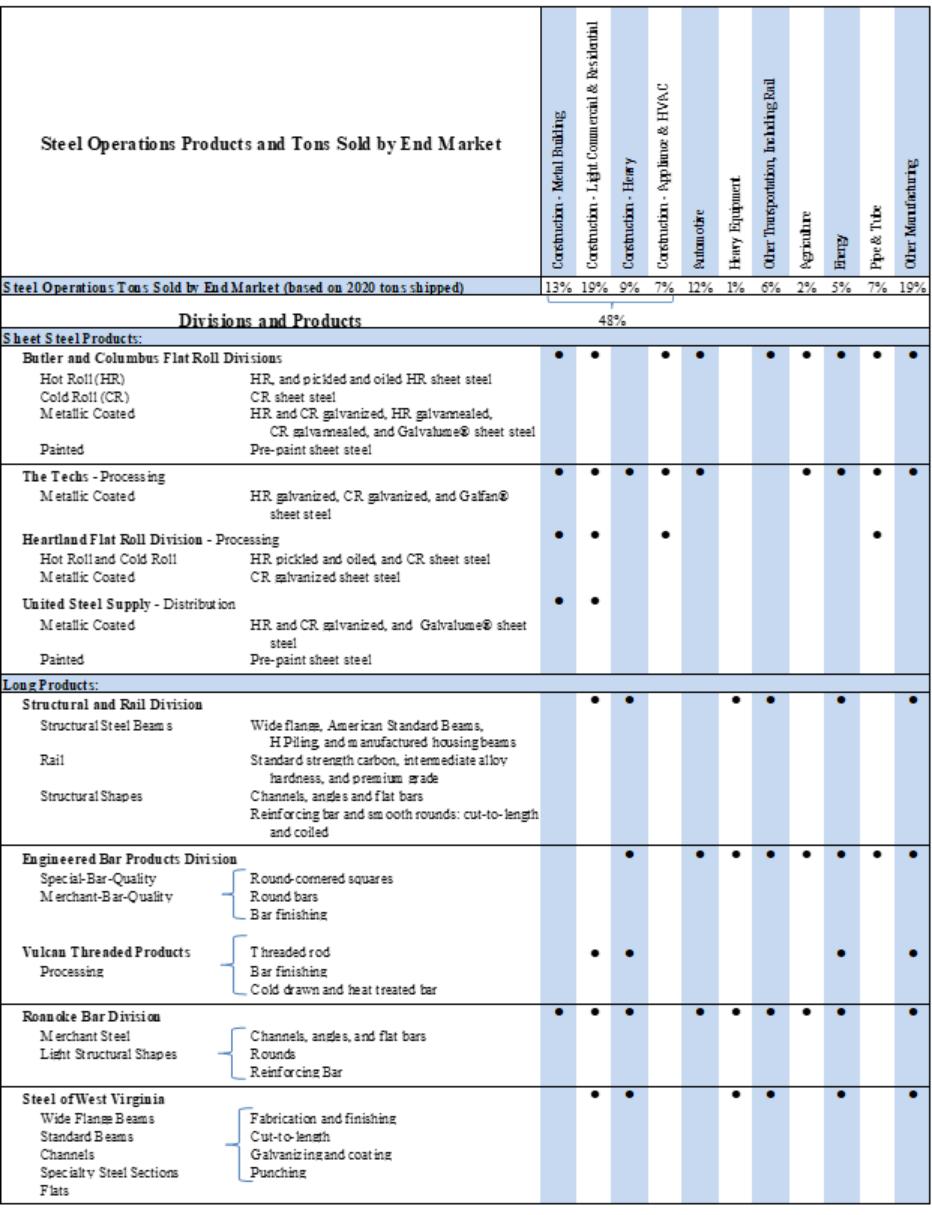

Our business is also dependent upon certain industries, such as construction, automotive, manufacturing, transportation, heavy and agriculture equipment, and pipe and tube (including OCTG) markets, and these industries are also cyclical in nature. Therefore, these industries may experience their own fluctuations in demand for our products based on such things as economic conditions, raw material and energy costs, consumer demand and infrastructure funding decisions by governments. Many of these factors are beyond our control. As a result of volatility in our industry or in the industries we serve, we may have difficulty increasing or maintaining our level of sales or profitability. A downturn in our industry or the industries we serve may adversely affect our business, results of operations, financial condition and cash flows.

A prospective decline in consumer and business confidence and spending, which is often coupled with reductions in the availability of credit or increased cost of credit, as well as volatility in the capital and credit markets, may adversely affect the business and economic environment in which we operate and the profitability of our business. We are also exposed to risks associated with the creditworthiness of our customers and suppliers. If the availability of credit to fund or support the continuation and expansion of our customers’ business operations is curtailed or if the cost of that credit is increased, the resulting inability of our customers or of their customers to either access credit or absorb the increased cost of that credit may adversely affect our business by reducing our sales or by increasing our exposure to losses from uncollectible customer accounts. A disruption of the credit markets could also result in financial instability of some of our customers and suppliers. The consequences of such adverse effects could include the interruption of production at the facilities of our customers, the reduction, delay or cancellation of customer orders, delays or interruptions of the supply of raw materials we purchase, and bankruptcy of customers, suppliers or other creditors. Any of these events may adversely affect our business, results of operations, financial condition and cash flows.

Global steelmaking overcapacity and imports of steel into the United States have adversely affected, and may continue to adversely affect, United States steel prices, which, together with increased scrap prices, may adversely affect our business, results of operations, financial condition and cash flows.

Global steelmaking capacity currently exceeds global consumption of steel products, which adversely affects United States and global steel prices. Such excess capacity sometimes results in steel manufacturers in certain countries exporting steel and steel products, including pre-fabricated long product steel, at prices that are lower than prevailing domestic prices, and sometimes at or below their cost of production. Excessive imports of steel and steel products, including pre-fabricated steel, into the United States, have exerted, and may continue to exert, downward pressure on United States steel and steel products prices, which adversely affects our business, results of operations, financial condition and cash flows. Fluctuations in the value of the dollar can also affect imports, as strong United States dollar makes imported products less expensive, potentially resulting in more imports of steel products into the United States by our foreign competitors. Furthermore, anticipated additional domestic steel capacity could increase this global overcapacity. This, in turn, may also increase domestic demand for ferrous scrap. Our results of operations, financial condition and cash flows are driven primarily from the metal spread achieved from the price we sell steel and steel products compared to the price of our metallic raw materials, including scrap. During prolonged periods of steel and steel products overcapacity, leading to lower selling prices, combined with high demand for scrap and raw materials, leading to higher buying prices, our metal spreads could be compressed, which may adversely affect our business, results of operations, financial condition and cash flows.