UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-07751

Nuveen Multistate Trust IV

(Exact name of registrant as specified in charter)

Nuveen Investments

333 West Wacker Drive, Chicago, IL 60606

(Address of principal executive offices) (Zip code)

Kevin J. McCarthy

Nuveen Investments

333 West Wacker Drive

Chicago, IL 60606

(Name and address of agent for service)

Registrant’s telephone number, including area code: (312) 917-7700

Date of fiscal year end: May 31

Date of reporting period: May 31, 2013

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policy making roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. ss.3507.

ITEM 1. REPORTS TO STOCKHOLDERS.

Mutual Funds

Nuveen Municipal Bond Funds

Dependable, tax-free income because it’s not what you earn, it’s what you keep.®

Annual Report

May 31, 2013

| Share Class / Ticker Symbol | ||||||||

| Fund Name | Class A | Class B | Class C | Class I | ||||

| Nuveen Kansas Municipal Bond Fund |

FKSTX | — | FCKSX | FRKSX | ||||

| Nuveen Kentucky Municipal Bond Fund |

FKYTX | FKYBX | FKYCX | FKYRX | ||||

| Nuveen Michigan Municipal Bond Fund |

FMITX | — | FLMCX | NMMIX | ||||

| Nuveen Missouri Municipal Bond Fund |

FMOTX | FMMBX | FMOCX | FMMRX | ||||

| Nuveen Ohio Municipal Bond Fund |

FOHTX | FOHBX | FOHCX | NXOHX | ||||

| Nuveen Wisconsin Municipal Bond Fund |

FWIAX | — | FWICX | FWIRX | ||||

LIFE IS COMPLEX.

Nuveen makes things e-simple.

It only takes a minute to sign up for e-Reports. Once enrolled, you’ll receive an e-mail as soon as your Nuveen Fund information is ready. No more waiting for delivery by regular mail. Just click on the link within the e-mail to see the report and save it on your computer if you wish.

Free e-Reports right to your e-mail!

www.investordelivery.com

If you receive your Nuveen Fund distributions and statements from your financial advisor or brokerage account.

OR

www.nuveen.com/accountaccess

If you receive your Nuveen Fund distributions and statements directly from Nuveen.

| Must be preceded by or accompanied by a prospectus. | NOT FDIC INSURED | MAY LOSE VALUE | NO BANK GUARANTEE |

| 4 | ||||

| 5 | ||||

| 15 | ||||

| 28 | ||||

| 30 | ||||

| 32 | ||||

| 34 | ||||

| 35 | ||||

| 86 | ||||

| 87 | ||||

| 88 | ||||

| 92 | ||||

| 104 | ||||

| 115 | ||||

| 119 | ||||

| 126 | ||||

| 127 | ||||

Letter to Shareholders

| 4 | Nuveen Investments |

Portfolio managers Daniel Close, CFA, Steven Hlavin and Chris Drahn review economic and market conditions, key investment strategies, and the performance of the Nuveen Kansas Municipal Bond Fund, Nuveen Kentucky Municipal Bond Fund, Nuveen Michigan Municipal Bond Fund, Nuveen Missouri Municipal Bond Fund, Nuveen Ohio Municipal Bond Fund and Nuveen Wisconsin Municipal Bond Fund. Dan has managed the Kentucky, Michigan and Ohio Funds since 2007, Steve has managed the Kansas and Wisconsin Funds since 2011 and Chris has managed the Missouri Fund since 2011.

What factors affected the U.S. economy and the national municipal bond market during the twelve-month period ending May 31, 2013?

During this reporting period, the U.S. economy’s progress toward recovery from recession continued at a moderate pace. The Federal Reserve (Fed) maintained its efforts to improve the overall economic environment by holding the benchmark fed funds rate at the record low level of zero to 0.25% that it established in December 2008. The Fed also continued its monthly purchases of $40 billion of mortgage-backed securities and $45 billion of longer-term Treasury securities in an open-ended effort to bolster growth. However, at its June 2013 meeting (subsequent to the end of this reporting period), the Central Bank indicated that downside risks to the economy had diminished since the fall of 2012. Although the Fed made no changes to its highly accommodative monetary policies at the June meeting, Chairman Bernanke’s remarks afterward indicated the Central Bank could slow the pace of its bond buying program later this year if the economy continues to improve.

As measured by gross domestic product (GDP), the U.S. economy grew at an annualized rate of 1.8% in the first quarter of 2013, compared with 0.4% for the fourth quarter of 2012, continuing the pattern of positive economic growth for the 15th consecutive quarter. The Consumer Price Index (CPI) rose 1.4% year-over-year as of May 2013, while the core CPI (which excludes food and energy) increased 1.7% during the period, staying within the Fed’s unofficial objective of 2.0% or lower for this inflation measure. Meanwhile, labor market conditions continued to slowly show signs of improvement, although unemployment remained above the Central Bank’s 6.5% target. As of May 2013, the national unemployment rate was 7.6%, down from 8.2% a year ago. The housing market, long a major weak spot in the U.S. economic recovery, also delivered some good news as the average home price in the S&P/Case-Shiller Index of 20 major metropolitan areas rose 12.1% for the twelve months ended April 2013 (most recent data available at the time this report was prepared). This marked the largest twelve-month percentage gain for the index since 2006.

However, the outlook for the U.S. economy continued to be clouded by uncertainty about global financial markets and the outcome of the “fiscal cliff.” The tax consequences of the fiscal cliff situation, which had been scheduled to become effective in January 2013, were averted through a last minute deal that raised payroll taxes, but left in place a number of tax breaks. However, lawmakers postponed and then failed to reach a resolution on $1.2 trillion in spending cuts intended to address the federal budget deficit. As a result, automatic spending cuts (or sequestration) affecting both defense and non-defense programs (excluding Social Security and Medicaid) took effect March 1, 2013, with potential implications for U.S. economic growth over the next decade. In late March, Congress passed legislation that established

Certain statements in this report are forward-looking statements. Discussions of specific investments are for illustration only and are not intended as recommendations of individual investments. The forward-looking statements and other views expressed herein are those of the portfolio managers as of the date of this report. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements and the views expressed herein are subject to change at any time, due to numerous market and other factors. The Funds disclaim any obligation to update publicly or revise any forward-looking statements or views expressed herein.

Ratings shown are the highest rating given by one of the following national rating agencies: Standard & Poor’s, Moody’s Investors Service, Inc. or Fitch, Inc. Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below investment grade ratings. Certain bonds backed by U.S. Government or agency securities are regarded as having an implied rating equal to the rating of such securities. Holdings designated N/R are not rated by these national rating agencies.

| Nuveen Investments | 5 |

federal funding levels for the remainder of fiscal 2013, which ends on September 30, preventing a federal government shutdown. The proposed federal budget for fiscal 2014 remains under debate.

Municipal bond prices generally rallied nationally during this period, as strong demand and tight supply combined to create favorable market conditions for municipal bonds. However, the market also encountered some additional volatility generated by the political environment, particularly the fiscal cliff at the end of 2012 and the approach of federal tax season. Although the total volume of tax-exempt supply improved over that of the same period a year earlier, the issuance pattern remained light compared with long-term historical trends and new money issuance was relatively flat. This supply/demand dynamic served as a key driver of performance. At the state level, state governments in aggregate appeared to have made good progress in dealing with budget issues. On the revenue side, state tax collections have grown for 13 straight quarters, exceeding pre-recession levels beginning in September 2011, while on the expense side, the states made headway in cutting and controlling costs. The current low level of municipal issuance reflects the current political distaste for additional borrowing by state and local governments facing fiscal constraints and the prevalent atmosphere of municipal budget austerity. During this period, we continued to see municipal yields remain relatively low. Borrowers seeking to take advantage of the low rate environment sparked an increase in refunding activity, with approximately 50% of municipal paper issued by borrowers that were calling existing debt and refinancing at lower rates.

Over the twelve months ended May 31, 2013, municipal bond issuance nationwide totaled $376 billion, an increase of 5.2% over the issuance for the twelve-month period ended May 31, 2012. As previously mentioned, the majority of this supply was attributable to refunding issues, rather than new money issuance. During this reporting period, demand for municipal bonds remained very strong, especially from individual investors, but also from mutual funds, banks and insurance companies.

How were the economic and market conditions in Kansas, Kentucky, Michigan, Missouri, Ohio and Wisconsin during this reporting period?

Kansas has been slowly recovering from the recent economic recession. In 2011, the state’s economy expanded at a rate of 0.5%, compared with the national growth rate of 1.5%, ranking Kansas 35th in terms of GDP growth by state. Private industry in the state continued to add jobs and indications were that these employment gains were permanent. As of May 2013, the Kansas unemployment rate stood at 5.7%. Recent employment gains have been led by professional and business services, manufacturing, and education and health services, the state’s largest private sectors. According to Moody’s, manufacturing was expected to be key to Kansas’s long term recovery, with hiring projected to accelerate in this high wage industry. Agricultural products were also expected to bolster the Kansas economy. Kansas ranks among the top ten states in the nation in agricultural production, with strong price support for two of its major crops, soy and corn. On the fiscal front, the Kansas state budget for fiscal 2013, which was introduced in January 2012 and enacted in June 2012, fully funded or increased funding for essential services, while holding state general fund expenditures below fiscal 2012 levels. While the 2013 budget closed a $500 million gap, it also included a package of income tax cuts projected to reduce state revenues by $3.7 billion over the next five years. The budget also called for adding $465 million in reserves to the state general fund, which had been largely depleted by the end of fiscal 2013. As of May 2013, Kansas general obligation bonds continued to carry ratings of Aa2 and a negative outlook, and AA and stable outlook from Moody’s and S&P, respectively. For the twelve months ending May 31, 2013, municipal issuance in Kansas totaled $3.4 billion, representing a 22.5% year-over-year increase.

After showing promise in 2011, Kentucky’s economic recovery slowed in 2012. In 2012, the Commonwealth’s economy posted growth of 1.4%, compared with the national growth rate of 2.5%, ranking Kentucky 33th in terms of GDP growth by state and below average among its peers in the southeast. Kentucky’s unemployment levels typically trend higher than the nation, but have recently improved, moving closer in line with the rest of the country. As of May 2013 unemployment had dropped to 8.1% from 8.3% the prior year. This is at least in part due to the state’s manufacturing

| 6 | Nuveen Investments |

sector, which is proportionally higher than the nation. Resident income indices have historically compared poorly with median per capita income at only 82% of the nation. Positively, Kentucky did not fall any further behind during the recent recession and the state reports personal income rose 1.3% during the last year. According to Moody’s, Kentucky’s low cost of doing business and highly affordable housing should continue to provide support for economic expansion. Kentucky’s biennial budget for fiscal 2013 and 2014 is structurally imbalanced and revenue projections for fiscal 2013 have been revised down slightly to 2.1% from 2.4%. Budget revisions for 2014 will be necessary. The Commonwealth has depleted reserve levels which have been at 3% or less of revenues since fiscal 2008, closing fiscal 2012 with a General Fund balance of $95.1 million, or just 1.1% of revenues. Though the state does not have any outstanding general obligation debt, as of June 2013, the state’s implied general obligation rating was Aa3 and AA- by Moody’s and S&P, respectively. The state typically issues annual appropriation debt, which is rated a notch lower at Aa3 and A+, by Moody’s and S&P, respectively, with negative outlooks. Debt levels are moderately high in relation to the Commonwealth’s economic base. Net tax supported debt per capita is above average at $1,998 and 5.9% of personal income, above the Moody’s medians of $1,074 and 2.8%, respectively. For the twelve months ending May 31, 2013, Kentucky issued $3.0 billion in municipal bonds, representing a 13.7% decline from the twelve months ended May 31, 2012.

After struggling to emerge from recession over the past few years, Michigan’s economy has continued to slowly improve driven in part by a recovering auto industry. Strong growth in domestic auto sales in 2012 bolstered Michigan’s recovery, with vehicle sales continuing the positive trend of the past three years. Overall, Michigan continued to rely heavily on manufacturing, which represented 13% of employment in the state, compared with 9% nationally. As of May 2013, Michigan’s unemployment rate was 8.4%, its best reading since August 2008, but still remains above the national average of 7.6%. Over the past seven years, housing prices have declined dramatically in most of central and eastern Michigan and the inventory of foreclosed homes remained elevated in many of the state’s hardest hit metropolitan areas, including Detroit, Warren and Flint. According to the S&P/Case-Shiller Index of 20 major metropolitan areas, housing prices in Detroit rose 19.8% over the twelve months ended April 2013 (most recent data available at the time this report was prepared). For fiscal 2013, Michigan’s $48.2 billion budget was structurally balanced and did not require major expenditure cuts or borrowing. Modest operating surpluses over the past two years have been used to replenish the state’s depleted rainy day fund, and Michigan projected its budget stabilization fund balance will reach approximately $600 million by the close of fiscal 2015. During the past two fiscal years, the state’s improved financial and cash position eliminated the need for cash flow borrowing. For fiscal 2014, the state’s $49 billion budget provides additional transportation funding, revenue sharing for local governments, and increased funding for K-12 education. Increased transportation spending is expected to help construction spending and payrolls. As of June 2013, Moody’s and S&P rated Michigan general obligation (GO) debt at Aa2 and AA, respectively, with positive outlooks. For the twelve months ended May 31, 2013, Michigan issued $9.3 billion in municipal bonds, a decrease of 15.9% from the twelve months ended May 31, 2012.

For 2012, the national recovery of 2.5% continued to outpace Missouri’s state GDP growth of 2.0%, ranking Missouri’s growth 26th among all states. Continued job losses in the government sector were offset by employment growth in transportation, leisure and hospitality, and education and health services sectors. As of May 2013, Missouri’s seasonally adjusted unemployment rate was 6.8%. Missouri’s overexposure to defense related manufacturing jobs continues to cause a drag on the state’s recovery, but efforts to transition part of the state economy away from traditional defense related manufacturing jobs into the development of biotechnology and alternative energy industries should help diversify the economy. Governor Nixon’s priority to expand exports experienced a slight step backwards with exports falling 1.4% in 2012 compared to 2011, but increases in exports to Mexico helped offset declines in exports to Canada and China. For fiscal 2014, the $25 billion Missouri state budget, which was introduced in January 2013 and sent to the Governor for approval in May 2013, focused on Medicaid expansion, job creation, increased K-12 education funding, and increased higher education funding. The Governor’s budget, which contained no new taxes, also called for eliminating 190 additional state jobs, bringing total reductions to 4,500 since 2009 and resulting in the smallest state

| Nuveen Investments | 7 |

workforce since 1997. As of May 2013, Moody’s and S&P rated Missouri general obligation debt at Aaa and AAA, respectively, with stable outlooks. During the twelve months ended May 31, 2013, municipal issuance in Missouri totaled $6.2 billion, a 33.5% increase from the twelve months ended May 31, 2012.

After weathering difficult years during the recession, the Ohio economy has shown signs of growth, although it continued to lag some aspects of the national recovery. Ohio’s education and health services industry remained the largest source of employment in the state and this sector along with manufacturing and professional and business services continued to be leaders in adding jobs during this period. In manufacturing, Ohio’s auto industry recently made capital investments to support future production, which in turn should benefit the state’s steel industry. Steel manufacturing also has been supported by the emerging energy industry in eastern Ohio, including the extraction of natural gas and oil from the Utica and Marcellus shale formations. In 2012, Ohio’s economy grew at a rate of 2.2%, compared with the national growth rate of 2.5% for 2012, ranking Ohio 20th in terms of GDP growth by state. As of May 2013, the state’s unemployment rate was 7.0%, and below the national rate of 7.6%. Boosted by gains in income and sales taxes, state tax revenues are up 11% through the first 10 months of fiscal 2013 on a year-over-year basis. The proposed biennial state budget for fiscal 2014-2015 included several changes to Ohio’s tax code: a tax cut for small businesses, a reduction in personal income tax rates and a lower sales tax on services, with some of the resultant revenue losses offset by increased taxes on oil and gas drilling. As of May 2013, Moody’s and S&P rated Ohio GO debt at Aa1 and AA+, respectively, with stable outlooks. For the twelve months ended May 31, 2013, municipal issuance in Ohio totaled $12.5 billion, an increase of 21% compared with the twelve months ended May 31, 2012.

Wisconsin’s economy has slowed in comparison to initial post-recession growth primarily due to a slowdown in the service sector, but has been exacerbated by a limited ability to trade agricultural goods. Low water levels resulting from the 2012 drought limited barge traffic through the beginning of 2013 and then heavy rains in April 2013 caused flooding, again slowing down barge traffic. Favorably, manufacturing has held up reasonably well and has buoyed Wisconsin’s economy. In 2012, the state’s economy expanded at a rate of 1.5%, compared with the national growth rate of 2.5%, ranking Wisconsin 32nd in terms of GDP growth by state. Hiring across sectors has been relatively weak in 2013, though a positive sign is that personal income indices continue to climb. As of May 2013, the Wisconsin jobless rate was 7.0%, up from 6.8% in the prior year. According to Moody’s, the state was expected to see further gains in manufacturing, benefiting from growth in Wisconsin’s largest trading partner, Canada, which provides the market for one-third of the state’s exports. Wisconsin enacted a two-year budget for fiscal 2012 and 2013, which closed a budget shortfall through reductions in spending for education, the University of Wisconsin system, Medicaid and state aid to local governments. The state now projects that fiscal 2013 will close with a budget surplus, adding to the General Fund reserves and beginning to fund the long-ago depleted rainy day fund. As of May 2013, Wisconsin’s general obligation debt carried ratings of Aa2 from Moody’s and AA from S&P with stable outlooks. For the twelve months ended May 31, 2013, Wisconsin issued $6.4 billion of municipal bonds, an increase of 8.9% from the twelve-month period ended May 31, 2012.

How did the Funds perform during the twelve-month reporting period ended May 31, 2013?

The tables in the Fund Performance, Expense and Leverage Ratios section of this report provide Class A Share total returns for the Funds for the one-year, five-year and ten-year periods ending May 31, 2013. The tables also compare these returns to each Fund’s benchmark index and its appropriate Lipper classification average.

During the twelve-month period, the Class A Shares at net asset value (NAV) of the Michigan, Missouri and Ohio Funds outperformed the S&P Municipal Bond Index, while the Class A Shares at NAV of the Kansas, Kentucky and Wisconsin Funds underperformed this performance measure. Kansas and Missouri outperformed their respective state index, while Kentucky, Michigan, Ohio and Wisconsin underperformed their respective state index. All six Funds outpaced their respective Lipper classification average.

| 8 | Nuveen Investments |

As was mentioned during the last reporting period, we will be discussing the Funds’ performance relative to the S&P Municipal Bond Index, and will no longer be using S&P state specific indexes as secondary benchmarks. While the S&P Municipal Bond Index does not reflect the Funds’ geographic concentration, it broadly reflects the Funds’ strategies and we believe it provides an appropriate performance comparison for shareholders. State specific indexes generally provide a less useful basis of comparison since they may not be investable due to sector/issuer and security concentrations and they may be volatile over time due to the limited size and issuance patterns.

What strategies were used to manage the Funds during the reporting period? How did these strategies influence performance?

All of the Funds continued to employ the same fundamental investment strategies and tactics long relied upon by the Funds’ sub-adviser, Nuveen Asset Management. Our municipal bond portfolios are managed with a value-oriented approach and close input from Nuveen Asset Management’s research team. Below we highlight the specific factors influencing each Fund’s investment strategy, as well as how we managed each portfolio in light of recent market conditions.

Nuveen Kansas and Wisconsin Municipal Bond Funds

The Nuveen Kansas Municipal Bond Fund trailed the S&P Municipal Bond Index during the twelve-month period. The Fund’s overweighting in local general obligation (GO) debt was one factor behind the relative underperformance. Compared with the national municipal bond market, Kansas features a relatively high amount of GO debt, mainly local school district bonds, which tended to underperform during the period. The Fund was also hampered by its overweighting in the utility bond sector, which also failed to keep pace with the market. In contrast, the Fund benefited from its overweighting in the strong performing health care sector.

Meanwhile, our credit quality positioning had a particularly favorable impact on performance. Going into the reporting period, we had structured the Fund to take advantage of narrowing credit spreads, meaning that investors were willing to accept a steadily smaller income premium to compensate them for buying riskier bonds. Compared to the index, the Fund had more exposure to lower investment grade bonds rated A and BBB and, when appropriate, below investment grade and non-rated bonds. We were also underweighted in the AAA-rating tier, representing the highest quality bonds available. Our stance was very helpful, as securities with lower credit ratings substantially outperformed their higher quality counterparts.

The Fund was also well positioned from a duration and yield curve standpoint. Specifically, we were overweight in longer duration bonds, which captured more of the favorable effects of declining interest rates during the period.

Trading activity was relatively light. Our purchases, which took place in both the new issue and secondary municipal bond markets, were financed largely with the proceeds of bond calls and a healthy but manageable level of new shareholder inflows. When possible, we favored lower rated issues with sound underlying credit quality. Many of our purchases came from the intermediate part of the yield curve. As the period progressed, we believed this segment provided better value for shareholders than longer-dated bonds, which had already rallied to a greater extent.

Our transactions included several purchases each of utility and dedicated sales tax bonds. We added lower rated securities that we believed offered attractive yields at a reasonable level of credit risk. To a lesser extent, we bought health care and local school district bonds, the latter of which formed a large part of the Kansas municipal bond market. One particularly noteworthy health care purchase during the period was A-rated bonds for the Mercy Regional Health Center in Manhattan, Kansas. These securities had been under represented in the portfolio and we believed they provided good relative value.

Our limited selling activity involved exchanging certain Puerto Rico holdings for others that better fit our management objectives. (Bonds issued by Puerto Rico and other U.S. territories are generally fully tax exempt for investors in all 50

| Nuveen Investments | 9 |

states.) These trades entailed moving into higher coupon bonds issued by Puerto Rico entities that we believed were less affected by the territory’s well publicized credit problems, and which we believed offered good long term prospects.

Similar to the Kansas Fund, the Wisconsin Fund underperformed the S&P Municipal Bond Index during the period. On the positive side, the portfolio’s duration and yield curve positioning proved helpful. The Fund was underweighted in bonds with shorter durations while overweight in longer dated issues, which benefited the most as interest rates declined.

In addition, the Fund was well situated to take advantage of the rally among lower rated bonds, as investors’ willingness to take on more credit risk translated into rising bond prices among lower quality securities. We were overweight in A-rated, BBB-rated and non-rated bonds, three categories that outperformed the market and underweight in lagging AA-rated issues, which further lifted the Fund’s results.

Meanwhile, the Fund’s sector positioning provided a mixed performance impact, shaped largely by the idiosyncrasies of the Wisconsin municipal bond market. Compared to the national market, for example, this portfolio was materially underweighted in GO debt. GO bonds are subject to Wisconsin state income tax, and when considered along with the low incremental yield associated with the securities, generally made them unattractive to us. During the reporting period, our lesser exposure to this category was helpful, as these issues underperformed. The state’s hospital bonds generally are state-income taxable as well, but the Fund was overweight in this sector compared with the national municipal bond market. We owned various hospital bonds that, in our view, offered sufficient relative value to compensate for the tax liability. As the health care category outperformed during the period, this allocation further added to the Fund’s results. On the other hand, dedicated sales-tax bonds are generally exempt from Wisconsin state taxes, and the Fund was overweight in this category. These issues failed to keep pace with the overall market, however, which hampered our results relative to the index.

The Wisconsin Fund experienced a modest amount of bond calls during the period. These proceeds, combined with bond maturities and new shareholder inflows, provided the cash proceeds we needed to finance our purchases, which can be divided into four main categories. First, we took advantage of opportunities to add to existing Wisconsin holdings, supplementing positions we liked at attractive prices. Second, we diversified the Fund’s territorial exposure by adding bonds issued by Guam and Virgin Islands entities. Like all territorial bonds, these are generally fully tax-exempt for U.S. investors. Our few bond sales during the period focused on restructuring the portfolio’s allocation to Puerto Rico issues, exchanging certain Puerto Rico holdings for others we believed offered more favorable characteristics. Third, we purchased new Wisconsin tax-exempt debt when we believed that doing so would enable us to achieve our management objectives. Two notable examples during the period included student housing bonds issued by Platteville Redevelopment Authority for the University of Wisconsin and tax increment financing bonds issued for Glendale Community Development Authority. Finally, we bought in-state or out-of-state debt that, though taxable for Wisconsin residents, represented especially good value, in our view. When looking out-of-state, we favored relatively liquid, lower rated bonds issued to fund large projects, choosing those securities with the potential to provide a particularly compelling risk/reward balance. With these four approaches, we were successful in essentially maintaining the Fund’s balance between Wisconsin taxable and tax-exempt securities in the portfolio.

Nuveen Kentucky, Michigan and Ohio Municipal Bond Funds

The Nuveen Kentucky Municipal Bond Fund trailed the S&P Municipal Bond Index during the twelve-month period. The Fund’s credit quality positioning was a primary factor behind its relative underperformance. Compared with the national municipal bond market, Kentucky is host to many high quality issuers and, therefore, has a much smaller proportion of bonds with credit ratings below investment grade. Given the lack of available opportunities among low-quality Kentucky bonds and our associated underweighting in them, the Fund did not fully benefit from the relative outperformance of these bonds as investors sought out higher yielding municipal debt. The Fund’s relative underweighting in the highest quality issues, those AAA-rated securities helped relative performance.

| 10 | Nuveen Investments |

The Fund’s sector positioning had a mixed effect on relative performance. Compared to the national market, this portfolio was overweight in health care debt, one of the market’s best-performing groups during the period given investors’ appetite for higher yielding segments. In contrast, our relative overweighting in pre-refunded bonds curtailed results. Pre-refunded securities, which are very high quality and tend to be low in duration, were among the worst performing Kentucky bonds, owing to their very high credit quality and low duration, two characteristics that investors generally eschewed during the period.

Duration and yield curve positioning were favorable. The Fund’s duration (meaning its sensitivity to changes in interest rates) was modestly longer than that of our benchmark index. This stance proved beneficial as interest rates declined throughout the bulk of the twelve month period. Additionally, our yield curve positioning, expressed through our emphasis on longer duration bonds and underweighting in shorter maturity securities, was helpful because longer term bonds outpaced their shorter term counterparts.

The significant amount of new shareholder cash coming into the portfolio, coupled with the calls (early redemptions) of some of our holdings, provided us with the proceeds we needed to make new purchases. Amid concern about a possible limitation to the tax-exempt status of municipal bonds, the municipal market hit an air pocket in the December 2012 and January 2013 time frame, affording us ample opportunities to purchase attractively priced bonds.

Our new portfolio additions during the period were spread among the health care, housing, water and sewer, and dedicated tax sectors, most of which had intermediate or long durations.

The Nuveen Michigan Fund outperformed the S&P Municipal Bond Index during the twelve-month period. On the positive side, the portfolio’s yield curve and credit quality positioning were helpful. The Fund was underweighted in bonds with shorter durations while overweight in longer dated issues, which benefited the most as interest rates declined.

In terms of credit quality positioning, the Fund benefited from the strong relative performance of lower rated bonds, which rallied strongly due to investors’ appetite for more credit risk and higher yields. We were overweight in bonds with credit ratings below investment grade, a category that outperformed the market and underweight in lagging AAA-rated issues, which further boosted the Fund’s results.

Meanwhile, the Fund’s sector positioning provided a mixed performance impact. Our overweighting in tobacco securities, another beneficiary of investor demand for higher yielding debt, was helpful. In contrast, the Fund’s overweighting in pre-refunded securities, some of the highest rated and lower duration issues in the marketplace, detracted from relative results, since both of those structural characteristics remained out of favor throughout much of the reporting period.

The Michigan Fund experienced a modest and manageable amount of bond calls, providing the proceeds we needed to finance our purchases. Most notably, we initiated or added to positions that we felt were unduly punished by their association with the City of Detroit. Specifically, we augmented our position in Detroit water/sewer bonds, purchasing these securities at what we believed were good values, especially given their comparatively short durations and backing by municipal bond insurer MBIA. Furthermore, we did not believe that these securities would be part of a bankruptcy proceeding. We also added to our position in Detroit Wayne County Stadium Authority (Comerica Park), and a limited tax GO bond for Wayne County, because we believed the securities had been unduly tainted by Detroit’s woes, and they offered compelling value and carried Assured Guaranteed insurance. Other transactions included purchases of some GO bonds issued by school districts in Southeast Michigan and electric utility bonds. Our limited bond sales involved exchanging certain tobacco-related securities for others that better fit our management objectives. These trades allowed us to diversify more equally between the two vintages of tobacco bonds available in the Michigan municipal marketplace.

| Nuveen Investments | 11 |

Subsequent to the close of this reporting period, on July 18, 2013, the City of Detroit filed for Chapter 9 in federal bankruptcy court. Detroit, burdened by decades of population loss, changes in the auto manufacturing industry and significant tax base deterioration, has been under severe financial stress for an extended period. Detroit’s bankruptcy filing will likely be a lengthy one given the complexity of its debt portfolio, number of creditors, numerous unions and significant legal questions that must be addressed. It is not yet clear how this bankruptcy will impact the actual creditworthiness, or the market’s perception of that creditworthiness, of other municipalities in Michigan.

The Nuveen Ohio Municipal Bond Fund outperformed the S&P Municipal Bond Index during the reporting period, primarily due to our duration and yield curve positioning. Specifically, we were overweight in longer duration bonds, which captured more of the favorable effects of declining interest rates during the period.

Relative results due to credit quality positioning were positive. The Fund’s overweighting in securities rated below investment grade proved helpful, while its underweighting in securities rated AAA was also positive. The lower a bond’s rating, the more likely it was to outperform the market, as investors gravitated toward bonds with higher yields.

Our sector selection also generated uneven relative results. An overweighting in pre-refunded bonds hurt, given their very short maturities and high underlying credit quality, two structural characteristics that investors generally avoided. In contrast, an overweighting in health care bonds, one of the chief beneficiaries of investors’ thirst for relatively high yielding securities, was a plus as the group outpaced the market overall. Elsewhere, our modest exposure to inverse floating rate securities (inverse floaters) was beneficial, because many of our holdings in such securities were longer duration.

The purchases we made during the period were funded primarily by new money received into the portfolio, either resulting from bond calls or new shareholder inflows. To keep the Fund fully invested, we looked to a variety of sectors for new additions, including airport, corporate-backed industrial development revenue, local school district GO and health care categories. One notable addition was the “JobsOhio Beverage System” bonds, which are backed by dedicated liquor taxes, which we consider a particularly stable income stream available in the Ohio market.

Nuveen Missouri Municipal Bond Fund

The Missouri Fund’s outperformance of the S&P Municipal Bond Index was driven in large part by favorable duration positioning (meaning its sensitivity to interest rate changes) and yield curve allocation. With respect to the latter, the Fund was somewhat overweight in bonds with longer maturities, which proved helpful, given that those securities generally outperformed shorter- and intermediate-dated issues during the reporting period.

The Fund’s credit quality stance also added value on a relative basis. In particular, the Fund was overweight in bonds with lower credit ratings, especially BBB-rated and non-rated issues. Due to low interest rates, investors favored lower-rated securities for their greater income potential and were willing to accept a steadily smaller income premium in exchange for buying these riskier bonds. Similarly, the Fund’s relative underweighting in the highest quality bonds rated AAA and AA helped relative performance as these securities failed to keep pace with their lower-rated counterparts.

Also adding to results was an overweighting in the health care sector, which fared well. However, that favorable impact was offset by having less exposure than the index to corporate-backed industrial development revenue securities. Because many of the issuers in this sector have lower credit ratings, and/or trade with a premium yield, these bonds tended to do well during the period, and our smaller exposure limited the Fund’s upside. Another disappointment was the portfolio’s slight overweighting in pre-refunded bonds, which are very high quality, short duration issues and therefore did not keep pace in a market favoring bonds with a higher income component. The Fund’s exposure to Puerto Rico securities modestly hurt results, as credit related challenges weighed on bonds issued in the territory.

We did not make significant changes to the Fund’s overall structure over the course of the reporting period. The Fund typically maintains some exposure to lower rated bonds because of both their income advantage over higher rated bonds and because we believe they often provide opportunities to realize relative value for our shareholders. While new

| 12 | Nuveen Investments |

purchases were made across a diversified set of sectors and reflected a range of credit rating categories from AAA to non-rated, we generally sought to maintain allocations to bonds with lower credit ratings. Funds were utilized from the proceeds of bond calls and maturities and new investment inflows, as well as the occasional sale of securities for which we believed we could get particularly good prices.

Throughout the period, we generally maintained the Fund’s desired level of interest-rate sensitivity with a duration that was slightly longer than that of the S&P index, and we mostly bought bonds with maturities ranging from 12 to 30 years. For most of the twelve-month period, there was very strong demand for the market’s longest bonds, which were often the highest yield bonds available. As a result, we occasionally found ourselves buying shorter dated paper until better value could be uncovered in longer bonds.

An Update Regarding Puerto Rico

Shareholders also should be aware of issues impacting some of the Funds’ non-state holdings. In December 2012, Moody’s down-graded Puerto Rico general obligation (GO) bonds to Baa3 from Baa1 based on Puerto Rico’s ongoing economic problems, unfunded pension liabilities, elevated debt levels and structural budget gaps. In addition, during July 2012, bonds issued by the Puerto Rico Sales Tax Financing Corporation (COFINA) also were downgraded by Moody’s to Aa3 from Aa2. The downgrade of the COFINA bonds was due mainly to the performance of Puerto Rico’s economy and its impact on the projected growth of sales tax revenues. In addition, the COFINA bonds were able to maintain a higher rating than the GOs because, unlike the revenue streams supporting some Puerto Rican issues, the sales taxes supporting the COFINA bonds cannot be diverted and used to support the commonwealth’s GO bonds. All of these Funds have some exposure to Puerto Rico bonds, the majority of which are the dedicated sales tax bonds issued by COFINA, and minimal exposure to Puerto Rico GOs.

During the reporting period, Puerto Rico paper generally underperformed the market as whole. Because most of our holdings were the COFINA bonds, the overall impact on performance was minimal. As we continue to emphasize Puerto Rico’s stronger credits, we view the COFINA bonds as potentially long-term holdings and note that the commonwealth recently introduced various sales tax initiatives aimed at improving future collections.

Risk Considerations

Mutual fund investing involves risk; principal loss is possible. Debt or fixed income securities such as those held by the Funds, are subject to market risk, credit risk, interest rate risk, call risk, state concentration risk, tax risk, and income risk. As interest rates rise, bond prices fall. Credit risk refers to an issuers ability to make interest and principal payments when due. Below investment grade or high yield debt securities are subject to liquidity risk and heightened credit risk. The Funds’ use of inverse floaters creates effective leverage. Leverage involves the risk that the Funds could lose more than its original investment and also increases the Funds’ exposure to volatility and interest rate risk.

Dividend Information

Each Fund seeks to pay dividends at a rate that reflects the past and projected performance of the Fund. To permit a Fund to maintain a more stable monthly dividend, the Fund may pay dividends at a rate that may be more or less than the amount of net investment income actually earned by the Fund during the period. If the Fund has cumulatively earned more than it has paid in dividends, it will hold the excess in reserve as undistributed net investment income (UNII) as part of the Fund’s net asset value. Conversely, if the Fund has cumulatively paid in dividends more than it has earned, the excess will constitute negative UNII that will likewise be reflected in the Fund’s net asset value. Each Fund will, over time, pay all its net investment income as dividends to shareholders. As of May 31, 2013, all six Funds had positive UNII balances for tax purposes. Kentucky had a negative UNII balance while Kansas, Michigan, Missouri, Ohio and Wisconsin had positive UNII balances for financial reporting purposes.

| Nuveen Investments | 13 |

[THIS PAGE INTENTIONALLY LEFT BLANK]

| 14 | Nuveen Investments |

Fund Performance, Expense and Effective Leverage Ratios

The Fund Performance and Expense Ratios for each Fund are shown on the following twelve pages.

Returns quoted represent past performance, which is no guarantee of future results. Current performance may be higher or lower than the performance shown. Investment returns and principal value will fluctuate so that when shares are redeemed, they may be worth more or less than their original cost. Returns without sales charges would be lower if the sales charge were included. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Income is generally exempt from regular federal income taxes. Some income may be subject to state and local income taxes and to the federal alternative minimum tax. Capital gains, if any, are subject to tax.

Returns may reflect a contractual agreement between certain Funds and the investment adviser to waive certain fees and expenses; see Notes to Financial Statements, Footnote 7 — Management Fees and Other Transactions with Affiliates for more information. In addition, returns may reflect a voluntary expense limitation by the Funds’ investment adviser that may be modified or discontinued at any time without notice. For the most recent month-end performance visit www.nuveen.com or call (800) 257-8787.

Returns reflect differences in sales charges and expenses, which are primarily differences in distribution and service fees. Fund returns assume reinvestment of dividends and capital gains.

Comparative index and Lipper return information is provided for the Funds’ Class A Shares at net asset value (NAV) only.

The expense ratios shown reflect the Funds’ total operating expenses (before fee waivers and/or expense reimbursements, if any) as shown in the Funds’ most recent prospectus. The expense ratios include management fees and other fees and expenses.

Leverage is created whenever a Fund has investment exposure (both reward and/or risk) equivalent to more than 100% of the investment capital. The effective leverage ratio shown is the amount of investment exposure created either through borrowings or indirectly through inverse floaters, divided by the assets invested, including those assets that were purchased with the proceeds of the leverage, or referenced by the levered instrument.

| Nuveen Investments | 15 |

Fund Performance, Expense and Effective Leverage Ratios (continued)

Nuveen Kansas Municipal Bond Fund

Refer to the first page of this Fund Performance and Expense Ratios section for further explanation of the information included within this page.

Fund Performance

Average Annual Total Returns as of May 31, 2013

| Average Annual | ||||||||||||

| 1-Year | 5-Year | 10-Year | ||||||||||

| Class A Shares at NAV |

3.13% | 5.91% | 4.53% | |||||||||

| Class A Shares at maximum Offering Price |

-1.19% | 5.01% | 4.09% | |||||||||

| S&P Municipal Bond Index* |

3.62% | 5.71% | 4.80% | |||||||||

| S&P Municipal Bond Kansas Index* |

3.09% | 5.89% | 4.80% | |||||||||

| Lipper Other States Municipal Debt Funds Classification Average* |

2.41% | 4.64% | 3.80% | |||||||||

| Class C Shares |

2.50% | 5.32% | 3.96% | |||||||||

| Class I Shares |

3.34% | 6.14% | 4.74% | |||||||||

Average Annual Total Returns as of June 30, 2013 (Most Recent Calendar Quarter)

| Average Annual | ||||||||||||

| 1-Year | 5-Year | 10-Year | ||||||||||

| Class A Shares at NAV |

-0.43% | 5.38% | 4.24% | |||||||||

| Class A Shares at maximum Offering Price |

-4.61% | 4.48% | 3.79% | |||||||||

| Class C Shares |

-0.87% | 4.80% | 3.68% | |||||||||

| Class I Shares |

-0.13% | 5.60% | 4.45% | |||||||||

Class A Shares have a maximum 4.20% sales charge (Offering Price). Class A Share purchases of $1 million or more are sold at net asset value without an up-front sales charge but may be subject to a contingent deferred sales charge (CDSC), also known as a back-end sales charge, if redeemed within eighteen months of purchase. Class C Shares have a 1% CDSC for redemptions within less than twelve months, which is not reflected in the one-year total return. Class I Shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors.

Expense Ratios as of Most Recent Prospectus

| Expense Ratios |

||||

| Class A Shares |

0.85% | |||

| Class C Shares |

1.39% | |||

| Class I Shares |

0.64% | |||

Effective Leverage Ratio as of May 31, 2013

| Effective Leverage Ratio |

5.55% |

| * | Refer to the Glossary of Terms Used in this Report for definitions. Indexes and Lipper averages are not available for direct investment. |

| 16 | Nuveen Investments |

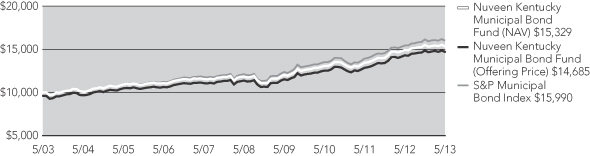

Growth of an Assumed $10,000 Investment as of May 31, 2013 – Class A Shares

The graphs do not reflect the deduction of taxes, such as state and local income taxes or capital gains taxes, that a shareholder may pay on Fund distributions or the redemption of Fund shares.

| Nuveen Investments | 17 |

Fund Performance, Expense and Effective Leverage Ratios (continued)

Nuveen Kentucky Municipal Bond Fund

Refer to the first page of this Fund Performance and Expense Ratios section for further explanation of the information included within this page.

Fund Performance

Average Annual Total Returns as of May 31, 2013

| Average Annual | ||||||||||||

| 1-Year | 5-Year | 10-Year | ||||||||||

| Class A Shares at NAV |

2.78% | 5.27% | 4.39% | |||||||||

| Class A Shares at maximum Offering Price |

-1.53% | 4.37% | 3.94% | |||||||||

| S&P Municipal Bond Index* |

3.62% | 5.71% | 4.80% | |||||||||

| S&P Municipal Bond Kentucky Index* |

3.64% | 6.11% | 4.49% | |||||||||

| Lipper Other States Municipal Debt Funds Classification Average* |

2.41% | 4.64% | 3.80% | |||||||||

| Class B Shares w/o CDSC |

2.03% | 4.48% | 3.77% | |||||||||

| Class B Shares w/CDSC |

-1.93% | 4.31% | 3.77% | |||||||||

| Class C Shares |

2.16% | 4.66% | 3.81% | |||||||||

| Class I Shares |

3.00% | 5.46% | 4.60% | |||||||||

Average Annual Total Returns as of June 30, 2013 (Most Recent Calendar Quarter)

| Average Annual | ||||||||||||

| 1-Year | 5-Year | 10-Year | ||||||||||

| Class A Shares at NAV |

-0.26% | 4.79% | 4.06% | |||||||||

| Class A Shares at maximum Offering Price |

-4.47% | 3.89% | 3.62% | |||||||||

| Class B Shares w/o CDSC |

-0.99% | 4.01% | 3.43% | |||||||||

| Class B Shares w/CDSC |

-4.83% | 3.84% | 3.43% | |||||||||

| Class C Shares |

-0.78% | 4.23% | 3.49% | |||||||||

| Class I Shares |

-0.05% | 5.00% | 4.27% | |||||||||

Class A Shares have a maximum 4.20% sales charge (Offering Price). Class A Share purchases of $1 million or more are sold at net asset value without an up-front sales charge but may be subject to a contingent deferred sales charge (CDSC), also known as a back-end sales charge, if redeemed within eighteen months of purchase. Class B Shares have a CDSC that begins at 5% for redemptions during the first year and declines periodically until after six years when the charge becomes 0%. Class B Shares automatically convert to Class A Shares eight years after purchase. Class C Shares have a 1% CDSC for redemptions within less than twelve months, which is not reflected in the one-year total return. Class I Shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors.

Expense Ratios as of Most Recent Prospectus

| Expense Ratios |

||||

| Class A Shares |

0.79% | |||

| Class B Shares |

1.54% | |||

| Class C Shares |

1.34% | |||

| Class I Shares |

0.59% | |||

Effective Leverage Ratio as of May 31, 2013

| Effective Leverage Ratio |

5.71% |

| * | Refer to the Glossary of Terms Used in this Report for definitions. Indexes and Lipper averages are not available for direct investment. |

| 18 | Nuveen Investments |

Growth of an Assumed $10,000 Investment as of May 31, 2013 – Class A Shares

The graphs do not reflect the deduction of taxes, such as state and local income taxes or capital gains taxes, that a shareholder may pay on Fund distributions or the redemption of Fund shares.

| Nuveen Investments | 19 |

Fund Performance, Expense and Effective Leverage Ratios (continued)

Nuveen Michigan Municipal Bond Fund

Refer to the first page of this Fund Performance and Expense Ratios section for further explanation of the information included within this page.

Fund Performance

Average Annual Total Returns as of May 31, 2013

| Average Annual | ||||||||||||

| 1-Year | 5-Year | 10-Year | ||||||||||

| Class A Shares at NAV |

3.85% | 5.31% | 4.28% | |||||||||

| Class A Shares at maximum Offering Price |

-0.55% | 4.41% | 3.84% | |||||||||

| S&P Municipal Bond Index* |

3.62% | 5.71% | 4.80% | |||||||||

| S&P Municipal Bond Michigan Index* |

4.28% | 5.75% | 4.76% | |||||||||

| Lipper Michigan Municipal Debt Funds Classification Average* |

2.96% | 4.20% | 3.76% | |||||||||

| Class C Shares |

3.33% | 4.73% | 3.72% | |||||||||

| Class I Shares |

4.15% | 5.53% | 4.50% | |||||||||

Average Annual Total Returns as of June 30, 2013 (Most Recent Calendar Quarter)

| Average Annual | ||||||||||||

| 1-Year | 5-Year | 10-Year | ||||||||||

| Class A Shares at NAV |

0.50% | 4.88% | 4.03% | |||||||||

| Class A Shares at maximum Offering Price |

-3.69% | 3.99% | 3.58% | |||||||||

| Class C Shares |

-0.11% | 4.29% | 3.45% | |||||||||

| Class I Shares |

0.61% | 5.08% | 4.22% | |||||||||

Class A Shares have a maximum 4.20% sales charge (Offering Price). Class A Share purchases of $1 million or more are sold at net asset value without an up-front sales charge but may be subject to a contingent deferred sales charge (CDSC), also known as a back-end sales charge, if redeemed within eighteen months of purchase. Class C Shares have a 1% CDSC for redemptions within less than twelve months, which is not reflected in the one-year total return. Class I Shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors.

Expense Ratios as of Most Recent Prospectus

| Expense Ratios |

||||

| Class A Shares |

0.83% | |||

| Class C Shares |

1.37% | |||

| Class I Shares |

0.62% | |||

Effective Leverage Ratio as of May 31, 2013

| Effective Leverage Ratio |

2.95% |

| * | Refer to the Glossary of Terms Used in this Report for definitions. Indexes and Lipper averages are not available for direct investment. |

| 20 | Nuveen Investments |

Growth of an Assumed $10,000 Investment as of May 31, 2013 – Class A Shares

The graphs do not reflect the deduction of taxes, such as state and local income taxes or capital gains taxes, that a shareholder may pay on Fund distributions or the redemption of Fund shares.

| Nuveen Investments | 21 |

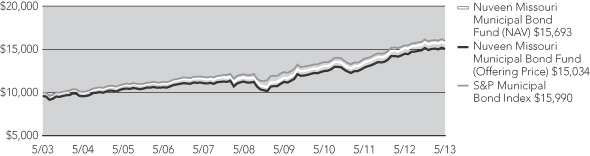

Fund Performance, Expense and Effective Leverage Ratios (continued)

Nuveen Missouri Municipal Bond Fund

Refer to the first page of this Fund Performance and Expense Ratios section for further explanation of the information included within this page.

Fund Performance

Average Annual Total Returns as of May 31, 2013

| Average Annual | ||||||||||||

| 1-Year | 5-Year | 10-Year | ||||||||||

| Class A Shares at NAV |

4.01% | 5.95% | 4.62% | |||||||||

| Class A Shares at maximum Offering Price |

-0.32% | 5.05% | 4.17% | |||||||||

| S&P Municipal Bond Index* |

3.62% | 5.71% | 4.80% | |||||||||

| S&P Municipal Bond Missouri Index* |

3.36% | 5.74% | 4.87% | |||||||||

| Lipper Other States Municipal Debt Funds Classification Average* |

2.41% | 4.64% | 3.80% | |||||||||

| Class B Shares w/o CDSC |

3.35% | 5.20% | 4.01% | |||||||||

| Class B Shares w/CDSC |

-0.65% | 5.03% | 4.01% | |||||||||

| Class C Shares |

3.39% | 5.37% | 4.05% | |||||||||

| Class I Shares |

4.14% | 6.16% | 4.82% | |||||||||

Average Annual Total Returns as of June 30, 2013 (Most Recent Calendar Quarter)

| Average Annual | ||||||||||||

| 1-Year | 5-Year | 10-Year | ||||||||||

| Class A Shares at NAV |

0.55% | 5.46% | 4.32% | |||||||||

| Class A Shares at maximum Offering Price |

-3.66% | 4.57% | 3.88% | |||||||||

| Class B Shares w/o CDSC |

-0.09% | 4.69% | 3.70% | |||||||||

| Class B Shares w/CDSC |

-3.96% | 4.52% | 3.70% | |||||||||

| Class C Shares |

0.03% | 4.89% | 3.75% | |||||||||

| Class I Shares |

0.76% | 5.66% | 4.53% | |||||||||

Class A Shares have a maximum 4.20% sales charge (Offering Price). Class A Share purchases of $1 million or more are sold at net asset value without an up-front sales charge but may be subject to a contingent deferred sales charge (CDSC), also known as a back-end sales charge, if redeemed within eighteen months of purchase. Class B Shares have a CDSC that begins at 5% for redemptions during the first year and declines periodically until after six years when the charge becomes 0%. Class B Shares automatically convert to Class A Shares eight years after purchase. Class C Shares have a 1% CDSC for redemptions within less than twelve months, which is not reflected in the one-year total return. Class I Shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors.

Expense Ratios as of Most Recent Prospectus

| Expense Ratios |

||||

| Class A Shares |

0.82% | |||

| Class B Shares |

1.56% | |||

| Class C Shares |

1.37% | |||

| Class I Shares |

0.62% | |||

Effective Leverage Ratio as of May 31, 2013

| Effective Leverage Ratio |

0.47% |

| * | Refer to the Glossary of Terms Used in this Report for definitions. Indexes and Lipper averages are not available for direct investment. |

| 22 | Nuveen Investments |

Growth of an Assumed $10,000 Investment as of May 31, 2013 – Class A Shares

The graphs do not reflect the deduction of taxes, such as state and local income taxes or capital gains taxes, that a shareholder may pay on Fund distributions or the redemption of Fund shares.

| Nuveen Investments | 23 |

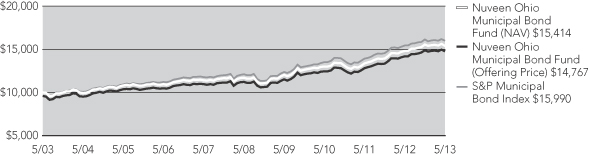

Fund Performance, Expense and Effective Leverage Ratios (continued)

Nuveen Ohio Municipal Bond Fund

Refer to the first page of this Fund Performance and Expense Ratios section for further explanation of the information included within this page.

Fund Performance

Average Annual Total Returns as of May 31, 2013

| Average Annual | ||||||||||||

| 1-Year | 5-Year | 10-Year | ||||||||||

| Class A Shares at NAV |

4.16% | 5.67% | 4.44% | |||||||||

| Class A Shares at maximum Offering Price |

-0.19% | 4.77% | 3.99% | |||||||||

| S&P Municipal Bond Index* |

3.62% | 5.71% | 4.80% | |||||||||

| S&P Municipal Bond Ohio Index* |

5.91% | 5.79% | 4.63% | |||||||||

| Lipper Ohio Municipal Debt Funds Classification Average* |

2.93% | 4.58% | 3.73% | |||||||||

| Class B Shares w/o CDSC |

3.33% | 4.87% | 3.82% | |||||||||

| Class B Shares w/CDSC |

-0.67% | 4.70% | 3.82% | |||||||||

| Class C Shares |

3.60% | 5.08% | 3.87% | |||||||||

| Class I Shares |

4.38% | 5.87% | 4.65% | |||||||||

Average Annual Total Returns as of June 30, 2013 (Most Recent Calendar Quarter)

| Average Annual | ||||||||||||

| 1-Year | 5-Year | 10-Year | ||||||||||

| Class A Shares at NAV |

0.33% | 5.09% | 4.13% | |||||||||

| Class A Shares at maximum Offering Price |

3.87% | 4.19% | 3.68% | |||||||||

| Class B Shares w/o CDSC |

-0.49% | 4.30% | 3.51% | |||||||||

| Class B Shares w/CDSC |

-4.35% | 4.13% | 3.51% | |||||||||

| Class C Shares |

-0.23% | 4.50% | 3.56% | |||||||||

| Class I Shares |

0.53% | 5.29% | 4.33% | |||||||||

Class A Shares have a maximum 4.20% sales charge (Offering Price). Class A Share purchases of $1 million or more are sold at net asset value without an up-front sales charge but may be subject to a contingent deferred sales charge (CDSC), also known as a back-end sales charge, if redeemed within eighteen months of purchase. Class B Shares have a CDSC that begins at 5% for redemptions during the first year and declines periodically until after six years when the charge becomes 0%. Class B Shares automatically convert to Class A Shares eight years after purchase. Class C Shares have a 1% CDSC for redemptions within less than twelve months, which is not reflected in the one-year total return. Class I Shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors.

Expense Ratios as of Most Recent Prospectus

| Expense Ratios |

||||

| Class A Shares |

0.81% | |||

| Class B Shares |

1.56% | |||

| Class C Shares |

1.36% | |||

| Class I Shares |

0.61% | |||

Effective Leverage Ratio as of May 31, 2013

| Effective Leverage Ratio |

8.53% |

| * | Refer to the Glossary of Terms Used in this Report for definitions. Indexes and Lipper averages are not available for direct investment. |

| 24 | Nuveen Investments |

Growth of an Assumed $10,000 Investment as of May 31, 2013 – Class A Shares

The graphs do not reflect the deduction of taxes, such as state and local income taxes or capital gains taxes, that a shareholder may pay on Fund distributions or the redemption of Fund shares.

| Nuveen Investments | 25 |

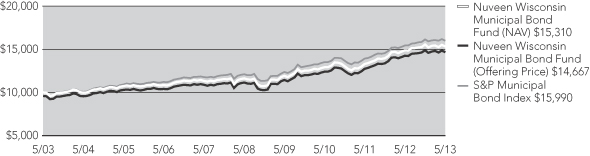

Fund Performance, Expense and Effective Leverage Ratios (continued)

Nuveen Wisconsin Municipal Bond Fund

Refer to the first page of this Fund Performance and Expense Ratios section for further explanation of the information included within this page.

Fund Performance

Average Annual Total Returns as of May 31, 2013

| Average Annual | ||||||||||||

| 1-Year | 5-Year | 10-Year | ||||||||||

| Class A Shares at NAV |

2.94% | 5.66% | 4.37% | |||||||||

| Class A Shares at maximum Offering Price |

-1.42% | 4.76% | 3.92% | |||||||||

| S&P Municipal Bond Index* |

3.62% | 5.71% | 4.80% | |||||||||

| S&P Municipal Bond Wisconsin Index* |

3.16% | 5.95% | 5.31% | |||||||||

| Lipper Other States Municipal Debt Funds Classification Average* |

2.41% | 4.64% | 3.80% | |||||||||

| Class C Shares |

2.39% | 5.07% | 3.80% | |||||||||

| Class I Shares |

3.15% | 5.86% | 4.57% | |||||||||

Average Annual Total Returns as of June 30, 2013 (Most Recent Calendar Quarter)

| Average Annual | ||||||||||||

| 1-Year | 5-Year | 10-Year | ||||||||||

| Class A Shares at NAV |

-1.37% | 4.95% | 3.96% | |||||||||

| Class A Shares at maximum Offering Price |

-5.48% | 4.05% | 3.51% | |||||||||

| Class C Shares |

-1.90% | 4.37% | 3.39% | |||||||||

| Class I Shares |

-1.16% | 5.16% | 4.15% | |||||||||

Class A Shares have a maximum 4.20% sales charge (Offering Price). Class A Share purchases of $1 million or more are sold at net asset value without an up-front sales charge but may be subject to a contingent deferred sales charge (CDSC), also known as a back-end sales charge, if redeemed within eighteen months of purchase. Class C Shares have a 1% CDSC for redemptions within less than twelve months, which is not reflected in the one-year total return. Class I Shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors.

Expense Ratios as of Most Recent Prospectus

| Expense Ratios |

||||

| Class A Shares |

0.86% | |||

| Class C Shares |

1.40% | |||

| Class I Shares |

0.65% | |||

Effective Leverage Ratio as of May 31, 2013

| Effective Leverage Ratio |

3.03% |

| * | Refer to the Glossary of Terms Used in this Report for definitions. Indexes and Lipper averages are not available for direct investment. |

| 26 | Nuveen Investments |

Growth of an Assumed $10,000 Investment as of May 31, 2013 – Class A Shares

The graphs do not reflect the deduction of taxes, such as state and local income taxes or capital gains taxes, that a shareholder may pay on Fund distributions or the redemption of Fund shares.

| Nuveen Investments | 27 |

Dividend Yield is the most recent dividend per share (annualized) divided by the offering price per share.

The SEC 30-Day Yield is a standardized measure of a Fund’s yield that accounts for the future amortization of premiums or discounts of bonds held in the Fund’s portfolio. The SEC 30-Day Yield is computed under an SEC standardized formula and is based on the maximum offer price per share. Dividend Yield may differ from the SEC 30-Day Yield because the Fund may be paying out more or less than it is earning and it may not include the effect of amortization of bond premium.

The Taxable-Equivalent Yield represents the yield that must be earned on a fully taxable investment in order to equal the yield of the Fund on an after-tax basis at a specified tax rate. With respect to investments that generate qualified dividend income that is taxable at a maximum rate of 15%, the Taxable-Equivalent Yield is lower.

Nuveen Kansas Municipal Bond Fund

| Dividend Yield |

SEC 30-Day Yield |

Taxable- Equivalent Yield1 |

||||||||||

| Class A Shares5 |

3.27% | 2.30% | 3.36% | |||||||||

| Class C Shares |

2.88% | 1.85% | 2.70% | |||||||||

| Class I Shares |

3.61% | 2.60% | 3.80% | |||||||||

Nuveen Kentucky Municipal Bond Fund

| Dividend Yield |

SEC 30-Day Yield |

Taxable- Equivalent Yield2 |

||||||||||

| Class A Shares5 |

3.41% | 1.91% | 2.82% | |||||||||

| Class B Shares |

2.82% | 1.24% | 1.83% | |||||||||

| Class C Shares |

3.03% | 1.44% | 2.13% | |||||||||

| Class I Shares |

3.77% | 2.19% | 3.23% | |||||||||

Nuveen Michigan Municipal Bond Fund

| Dividend Yield |

SEC 30-Day Yield |

Taxable- Equivalent Yield3 |

||||||||||

| Class A Shares5 |

3.66% | 1.85% | 2.69% | |||||||||

| Class C Shares |

3.27% | 1.38% | 2.00% | |||||||||

| Class I Shares |

4.03% | 2.13% | 3.09% | |||||||||

Nuveen Missouri Municipal Bond Fund

| Dividend Yield |

SEC 30-Day Yield |

Taxable- Equivalent Yield4 |

||||||||||

| Class A Shares5 |

3.65% | 2.34% | 3.46% | |||||||||

| Class B Shares |

3.07% | 1.69% | 2.50% | |||||||||

| Class C Shares |

3.29% | 1.89% | 2.79% | |||||||||

| Class I Shares |

4.02% | 2.65% | 3.91% | |||||||||

| 1 | TheTaxable-Equivalent Yield is based on the Fund’s SEC 30-Day Yield on the indicated date and a combined federal and state income tax rate of 31.5%. |

| 2 | TheTaxable-Equivalent Yield is based on the Fund’s SEC 30-Day Yield on the indicated date and a combined federal and state income tax rate of 32.3%. |

| 3 | TheTaxable-Equivalent Yield is based on the Fund’s SEC 30-Day Yield on the indicated date and a combined federal and state income tax rate of 31.1%. |

| 4 | TheTaxable-Equivalent Yield is based on the Fund’s SEC 30-Day Yield on the indicated date and a combined federal and state income tax rate of 32.3%. |

| 5 | The SEC Yield for Class A shares quoted in the table reflects the maximum sales load. Investors paying a reduced load because of volume discounts, investors paying no load because they qualify for one of the several exclusions from the load, and existing shareholders who previously paid a load but would like to know the SEC Yield applicable to their shares on a going-forward basis, should understand that the SEC Yield effectively applicable to them would be higher than the figure quoted in the table. |

| 28 | Nuveen Investments |

| Nuveen Investments | 29 |

Nuveen Ohio Municipal Bond Fund

| Dividend Yield |

SEC 30-Day Yield |

Taxable- Equivalent Yield1 |

||||||||||

| Class A Shares3 |

3.73% | 2.01% | 2.95% | |||||||||

| Class B Shares |

3.13% | 1.34% | 1.97% | |||||||||

| Class C Shares |

3.34% | 1.55% | 2.28% | |||||||||

| Class I Shares |

4.11% | 2.30% | 3.38% | |||||||||

Nuveen Wisconsin Municipal Bond Fund

| Dividend Yield |

SEC 30-Day Yield |

Taxable- Equivalent Yield2 |

||||||||||

| Class A Shares3 |

3.39% | 2.40% | 3.58% | |||||||||

| Class C Shares |

2.99% | 1.95% | 2.91% | |||||||||

| Class I Shares |

3.75% | 2.71% | 4.04% | |||||||||

| 1 | The Taxable-Equivalent Yield is based on the Fund’s SEC 30-Day Yield on the indicated date and a combined federal and state income tax rate of 31.9%. |

| 2 | The Taxable-Equivalent Yield is based on the Fund’s SEC 30-Day Yield on the indicated date and a combined federal and state income tax rate of 32.9%. |

| 3 | The SEC Yield for Class A shares quoted in the table reflects the maximum sales load. Investors paying a reduced load because of volume discounts, investors paying no load because they qualify for one of the several exclusions from the load, and existing shareholders who previously paid a load but would like to know the SEC Yield applicable to their shares on a going-forward basis, should understand that the SEC Yield effectively applicable to them would be higher than the figure quoted in the table. |

Holding Summaries as of May 31, 2013

This data relates to the securities held in each Fund’s portfolio of investments. It should not be construed as a measure of performance for the Fund itself.

Ratings shown are the highest rating given by one of the following national rating agencies: Standard & Poor’s Group, Moody’s Investors Service, Inc. or Fitch, Inc. Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below investment grade ratings. Certain bonds backed by U.S. Government or agency securities are regarded as having an implied rating equal to the rating of such securities. Holdings designated N/R are not rated by these national rating agencies.

| 1 | Holdings are subject to change. |

| 2 | Percentages may not add to 100% due to the exclusion of Other Assets Less Liabilities from the table. |

| 3 | As a percentage of total investment exposure. |

| 4 | As a percentage of total investments. |

| 30 | Nuveen Investments |

| 1 | Holdings are subject to change. |

| 2 | Percentages may not add to 100% due to the exclusion of Other Assets Less Liabilities from the table. |

| 3 | As a percentage of total investment exposure. |

| 4 | As a percentage of total investments. |

| Nuveen Investments | 31 |

As a shareholder of one or more of the Funds, you incur two types of costs: (1) transaction costs, including up-front and back-end sales charges (loads) or redemption fees, where applicable; and (2) ongoing costs, including management fees; distribution and service (12b-1) fees, where applicable; and other Fund expenses. The Examples below are intended to help you understand your ongoing costs (in dollars) of investing in the Funds and to compare these costs with the ongoing costs of investing in other mutual funds.

The Examples below are based on an investment of $1,000 invested at the beginning of the period and held through the period.

The information under “Actual Performance,” together with the amount you invested, allows you to estimate actual expenses incurred over the reporting period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.60) and multiply the result by the cost shown for your share class, in the row entitled “Expenses Incurred During Period” to estimate the expenses incurred on your account during this period.

The information under “Hypothetical Performance,” provides information about hypothetical account values and hypothetical expenses based on the respective Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expense you incurred for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the tables are meant to highlight your ongoing costs only and do not reflect any transaction costs. Therefore, the hypothetical information is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds or share classes. In addition, if these transaction costs were included, your costs would have been higher.

Nuveen Kansas Municipal Bond Fund

| Hypothetical Performance | ||||||||||||||||||||||||||

| Actual Performance | (5% annualized return before expenses) | |||||||||||||||||||||||||

| A Shares | C Shares | I Shares | A Shares | C Shares | I Shares | |||||||||||||||||||||

| Beginning Account Value (12/01/12) | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | ||||||||||||||

| Ending Account Value (5/31/13) | $ | 982.20 | $ | 978.70 | $ | 983.30 | $ | 1,020.89 | $ | 1,018.15 | $ | 1,021.89 | ||||||||||||||

| Expenses Incurred During Period | $ | 4.00 | $ | 6.71 | $ | 3.02 | $ | 4.08 | $ | 6.84 | $ | 3.07 | ||||||||||||||

For each class of the Fund, expenses are equal to the Fund’s annualized net expense ratio of .81%, 1.36% and .61% for Classes A, C and I, respectively, multiplied by the average account value over the period, multiplied by 182/365 (to reflect the one-half year period).

Nuveen Kentucky Municipal Bond Fund

| Hypothetical Performance | ||||||||||||||||||||||||||||||||||

| Actual Performance | (5% annualized return before expenses) | |||||||||||||||||||||||||||||||||

| A Shares | B Shares | C Shares | I Shares | A Shares | B Shares | C Shares | I Shares | |||||||||||||||||||||||||||

| Beginning Account Value (12/01/12) | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | ||||||||||||||||||

| Ending Account Value (5/31/13) | $ | 988.60 | $ | 985.00 | $ | 985.20 | $ | 989.70 | $ | 1,021.09 | $ | 1,017.35 | $ | 1,018.35 | $ | 1,022.09 | ||||||||||||||||||

| Expenses Incurred During Period | $ | 3.82 | $ | 7.52 | $ | 6.53 | $ | 2.83 | $ | 3.88 | $ | 7.64 | $ | 6.64 | $ | 2.87 | ||||||||||||||||||

For each class of the Fund, expenses are equal to the Fund’s annualized net expense ratio of .77%, 1.52%, 1.32% and .57% for Classes A, B, C and I, respectively, multiplied by the average account value over the period, multiplied by 182/365 (to reflect the one-half year period).

Nuveen Michigan Municipal Bond Fund

| Hypothetical Performance | ||||||||||||||||||||||||||

| Actual Performance | (5% annualized return before expenses) | |||||||||||||||||||||||||

| A Shares | C Shares | I Shares | A Shares | C Shares | I Shares | |||||||||||||||||||||

| Beginning Account Value (12/01/12) | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | ||||||||||||||

| Ending Account Value (5/31/13) | $ | 991.30 | $ | 988.70 | $ | 993.10 | $ | 1,020.89 | $ | 1,018.15 | $ | 1,021.89 | ||||||||||||||

| Expenses Incurred During Period | $ | 4.02 | $ | 6.74 | $ | 3.03 | $ | 4.08 | $ | 6.84 | $ | 3.07 | ||||||||||||||

For each class of the Fund, expenses are equal to the Fund’s annualized net expense ratio of .81%, 1.36% and .61% for Classes A, C and I, respectively, multiplied by the average account value over the period, multiplied by 182/365 (to reflect the one-half year period).

| 32 | Nuveen Investments |

Nuveen Missouri Municipal Bond Fund

| Hypothetical Performance | ||||||||||||||||||||||||||||||||||

| Actual Performance | (5% annualized return before expenses) | |||||||||||||||||||||||||||||||||

| A Shares | B Shares | C Shares | I Shares | A Shares | B Shares | C Shares | I Shares | |||||||||||||||||||||||||||