EX-99.4

Exhibit 99.4

THOMSON REUTERS STREETEVENTS

EDITED TRANSCRIPT

ANF—Q1 2012 Abercrombie & Fitch Co. Earnings Conference Call

EVENT DATE/TIME: MAY 16, 2012 / 12:30PM GMT

OVERVIEW:

Management discussed 1Q12 results, reporting diluted EPS of $0.03 on net sales of $921m and reiterated 2012 EPS guidance of $3.50-3.75.

|

|

|

| THOMSON REUTERS STREETEVENTS | www.streetevents.com | Contact Us

©2012 Thomson Reuters. All rights reserved. Republication or redistribution of

Thomson Reuters content, including by framing or similar means, is prohibited without the prior written consent of Thomson Reuters. ‘Thomson Reuters’ and the Thomson Reuters logo are registered trademarks of Thomson Reuters and its

affiliated companies. |

|

|

MAY 16, 2012 / 12:30PM, ANF—Q1 2012 Abercrombie & Fitch Co. Earnings Conference Call

CORPORATE PARTICIPANTS

Eric

Cerny Abercrombie & Fitch Co.—Senior Manager, IR

Mike Jeffries Abercrombie & Fitch

Co.—Chairman & CEO

Jonathan Ramsden Abercrombie & Fitch Co.—EVP & CFO

CONFERENCE CALL PARTICIPANTS

Jeff Klinefelter Piper Jaffray—Analyst

Dana Telsey

Telsey Advisory Group—Analyst

Lorraine Hutchinson BofA Merrill Lynch—Analyst

Amanda Sigmund Jefferies & Co.—Analyst

Brian Tunick JPMorgan—Analyst

Robin Murchison SunTrust

Robinson Humphrey—Analyst

Janet Kloppenburg JJK Research—Analyst

Omar Saad ISI Group—Analyst

Liz Dunn Macquarie Research—Analyst

Kimberly

Greenberger Morgan Stanley—Analyst

Barbara Wyckoff CLSA—Analyst

Paul Lejuez Nomura Asset Management—Analyst

Marni Shapiro The Retail Tracker—Analyst

Dave Weiner

Duetsche Bank—Analyst

John Kernan Cowen and Company—Analyst

Roxanne Meyer UBS—Analyst

PRESENTATION

Operator

Good day, everyone, and welcome to the Abercrombie & Fitch first-quarter earnings results conference call.Today’s conference is being recorded. (Operator Instructions). We will open the call

to take your questions at the end of the presentation. We ask that you limit yourself to one question during the question-and-answer session. At this time I would like to turn the conference over to Mr. Eric Cerny. Mr. Cerny, please go

ahead, Sir.

Eric Cerny—Abercrombie & Fitch Co.—Senior Manager, IR

Thank you, good morning, and welcome to our first-quarter earnings call. Earlier today we released our first-quarter sales and earnings, income statement,

balance sheet, store opening and closing summary and an updated financial history. Please feel free to reference these materials available on our website.

Also available on our website is an investor presentation which we will be referring to in our comments during this call. This call is being recorded and the replay may be accessed through the Internet at

Abercrombie.com under the Investor Relations section.

|

|

|

| THOMSON REUTERS STREETEVENTS | www.streetevents.com | Contact Us

©2012 Thomson Reuters. All rights reserved. Republication or redistribution of

Thomson Reuters content, including by framing or similar means, is prohibited without the prior written consent of Thomson Reuters. ‘Thomson Reuters’ and the Thomson Reuters logo are registered trademarks of Thomson Reuters and its

affiliated companies. |

|

|

2

MAY 16, 2012 / 12:30PM, ANF—Q1 2012 Abercrombie & Fitch Co. Earnings Conference Call

Before we begin I remind you that any forward-looking statements we may make

today are subject to the Safe Harbor statement found in our SEC filings. Today’s earnings call will be limited to one hour. Joining me today on the call are Mike Jeffries and Jonathan Ramsden. We will begin the call with a few brief remarks

from Mike followed by a review of the financial performance for the quarter from Jonathan. After our prepared comments we will be available to take your questions for as long as time permits. Now to Mike.

Mike Jeffries—Abercrombie & Fitch Co.—Chairman & CEO

Good morning, everyone; thank you for joining us today. While we are disappointed that European sales trends remain challenging in a very difficult

macroeconomic environment, we are largely satisfied with our overall performance for the quarter in that context.

Our US business, including

direct-to-consumer increased 4% on a comparable basis on top of a strong performance last year. Our international business comped negatively, but the economics remain strong and we delivered overall international sales growth of 42% including a

strong performance in direct-to-consumer.

With cotton cost issues now largely behind us we look forward to strong year-over-year earnings

growth in the back half of the year.

In that context I would like to spend a few minutes reviewing some highlights for the quarter.

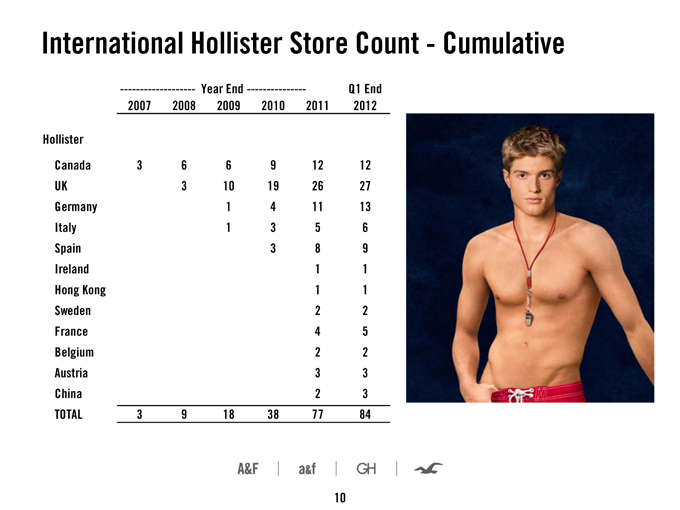

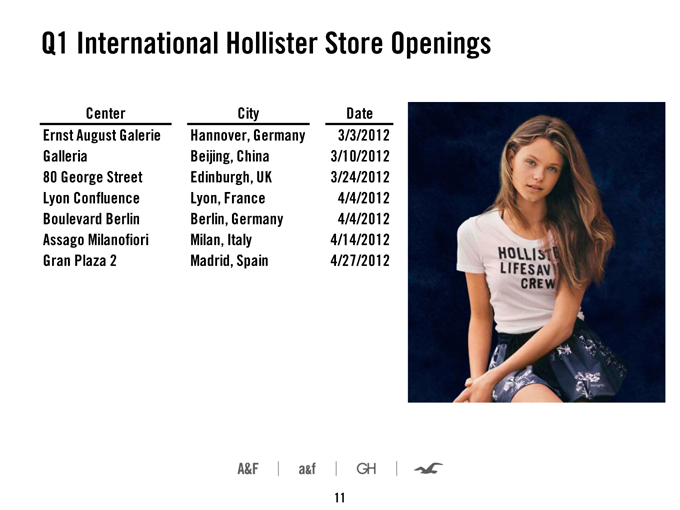

Starting with international, we opened seven new Hollister stores during the quarter including our third store in China. China remains a

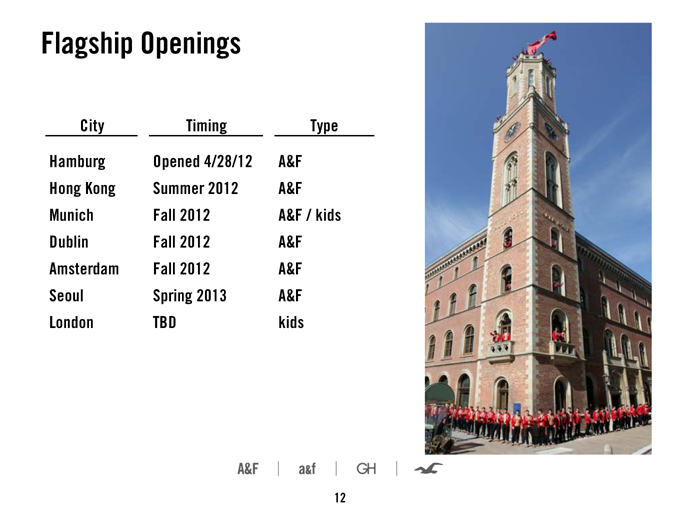

major priority for us this year with another two or three Hollister openings anticipated. In addition, we expect our Hong Kong A&F flagship opening in August to play a key role in raising awareness of our brands in Mainland China.

Moving back to Europe, at the very end of the quarter we opened our Hamburg A&F flagship in the iconic Alte Post building. We look forward to opening

our third German A&F store in Munich later in the year.

Subsequent to quarter end we made a big splash in London with the opening of a

combined Hollister and Gilly Hicks store on Regent Street and three new Gilly Hicks mall stores around London. These stores all opened on Saturday and are a big statement about our intentions for the Gilly Hicks brand. We had a lot of fun with the

openings and I encourage all of you to check out the pictures and videos available on our Facebook pages that captured the energy and excitement of the day.

Turning to direct-to-consumer, we are pleased with our continued strong growth of 40% for the quarter, which was on top of 32% growth in the comparable period last year. We are even more pleased that our

international business grew faster than the overall rate of growth.

This quarter marks the ninth consecutive quarter of increases in

direct-to-consumer of greater than 25%. Our margins in the direct-to-consumer channel remain strong and we expect to continue driving strong growth both through growing awareness of our brands internationally and through multiple investments we are

making in the channel.

As I mentioned a moment ago, our overall US retail segment comps were up 4% on top of strong growth last year. We were

able to do this while getting our AUR up slightly. Continuing to make progress on AUR is an important goal for us going forward.

With regard

to our stores and the assortment, we are very happy with our spring merchandise. As many of you have noted in your store checks, we feel very much like spring with bright colors throughout the assortments.

While it will not fully manifest itself until later in the year, we are also very pleased with the progress we have made on sourcing costs, which will

give us a strong tailwind starting in the middle of Q2.This has been a major area of focus over the past six months and our merchant sourcing and planning teams have done a great job. This benefit is giving us a significant insulation against the

impact of macro driven top-line trends for the remainder of the year.

|

|

|

| THOMSON REUTERS STREETEVENTS | www.streetevents.com | Contact Us

©2012 Thomson Reuters. All rights reserved. Republication or redistribution of

Thomson Reuters content, including by framing or similar means, is prohibited without the prior written consent of Thomson Reuters. ‘Thomson Reuters’ and the Thomson Reuters logo are registered trademarks of Thomson Reuters and its

affiliated companies. |

|

|

3

MAY 16, 2012 / 12:30PM, ANF—Q1 2012 Abercrombie & Fitch Co. Earnings Conference Call

Coming back to our international stores, we spend a lot of time analyzing and

understanding the trends in these stores and making sure we have incorporated the appropriate takeaways in our longer-term strategy. We are committed to remaining disciplined in our approach to this strategy and opening stores that meet our margin

criteria based on conservative volume assumptions.

We believe that the macro environment in Europe has been a significant factor in the

recent trends we have seen. Cannibalization has also been a factor. However, it is important to note that given the extraordinarily strong start we made in Europe and putting aside the current cyclical macroeconomic factors at play, we have long

been prepared for a period of negative same-store sales.

When we look at the current trends in Europe the questions we ask ourselves

are—first, are our stores continuing to stand out from the mall in terms of excitement and energy and in terms of traffic and productivity? Second, are the new store volumes consistent with the volumes at which we approved the deals? Third, are

we achieving our annualized target 30% four wall margins at the current trend and after cannibalization? Last, is our international direct-to-consumer business continuing to grow at a healthy rate?

Despite the downtrend we have experienced, at this point the answer to all of those questions is yes in aggregate and yes individually for the majority

of our European stores. Based on that, while we will continue to review trends closely and be very disciplined in how we approach new store openings, we believe the current economics of our business in Europe strongly affirm our long-term strategy.

We also believe that the other key components of our strategy are on track, these include—one, continuing to provide high-quality trend

right merchandise and a compelling and differentiated store experience; two, continuing to close underperforming US chain stores; three, investing in our DTC business, particularly the international business; and four, continuing to seek ways to

operate more efficiently and reduce expenses.

There are things that are not under our control, most notably the macro environment. But we

believe we are doing the right things where we do have control. And we look forward to moving into a period of sustained year-over-year EPS growth even in a challenged environment. With that I will hand you over to Jonathan, but we’ll be

available to answer your questions in a few minutes.

Jonathan Ramsden—Abercrombie & Fitch

Co.—EVP & CFO

Thanks, Mike, and good morning, everyone. I’ll start with a short summary of our results for the quarter

and then give an update on our outlook for the full year.

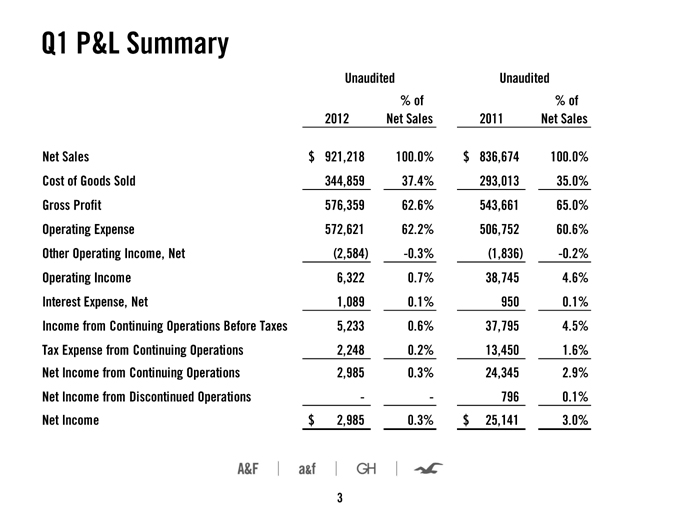

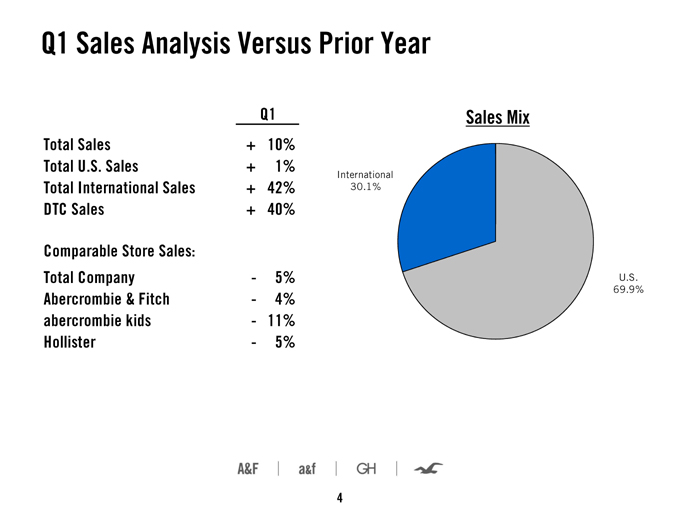

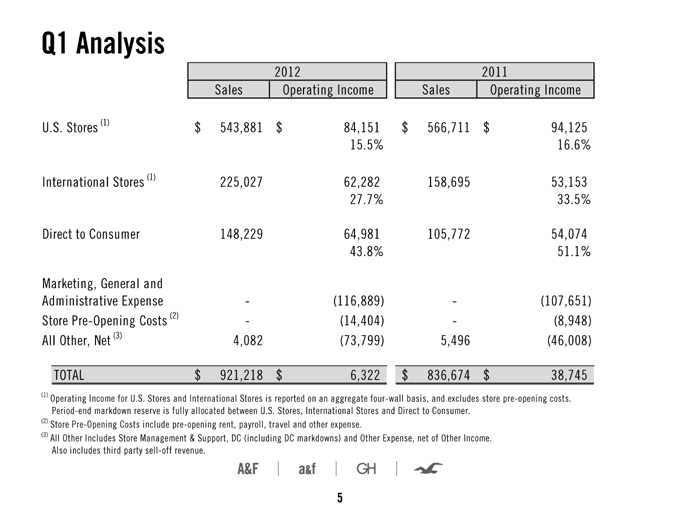

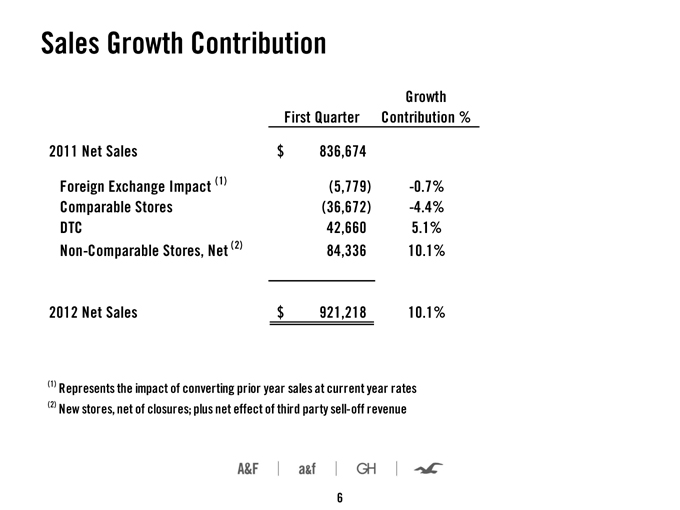

For the quarter the Company’s net sales increased 10% to $921 million while

comp store sales were down 5% to last year with men’s and women’s performing comparably. Comp sales were up slightly in US chain stores but significantly down across international and US tourist stores in a tough macroeconomic environment

in Europe and as we lapped strong sales a year ago. Cannibalization also had a meaningful impact on international comp store sales.

Total US

sales including DTC were up 1% with the effect of store closures offsetting most of the comparable sales growth of 4%—comp sales growth 4%. International sales for the quarter including DTC were up 42% and total DTC sales were up 40%.

International sales as a share of our overall business reached 30% for the first time. Foreign currency changes for the quarter were insignificant to sales on a year-over-year basis.

Despite lower sales than planned, gross margin erosion of 240 basis points was less than expected at the beginning of the quarter due to modest growth in AUR in a somewhat less promotional environment and

a lower quarter end markdown reserve than anticipated.

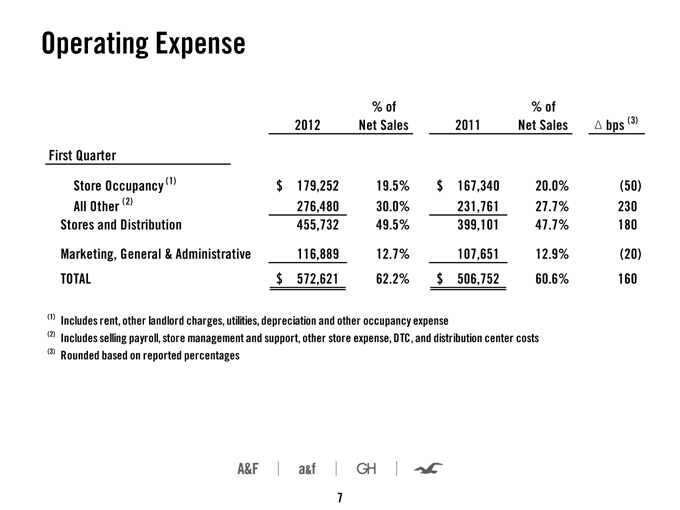

A summary of our fiscal quarter operating expenses can be found on page 6 of the

investor presentation. MG&A for the quarter was $116.9 million and up approximately 9% compared to last year. The increase in MG&A for the quarter was due to increases in marketing expense, equity comp, and other expense.

Stores and distribution expense for the quarter was $455.7 million and up approximately 14% compared to last year. Store occupancy costs were

approximately $179 million and all other stores and distribution costs represented 30% of sales, 230 basis points above the percentage of sales they represented last year, including the effect of higher direct-to-consumer expense, store payroll and

store management expense.

|

|

|

| THOMSON REUTERS STREETEVENTS | www.streetevents.com | Contact Us

©2012 Thomson Reuters. All rights reserved. Republication or redistribution of

Thomson Reuters content, including by framing or similar means, is prohibited without the prior written consent of Thomson Reuters. ‘Thomson Reuters’ and the Thomson Reuters logo are registered trademarks of Thomson Reuters and its

affiliated companies. |

|

|

4

MAY 16, 2012 / 12:30PM, ANF—Q1 2012 Abercrombie & Fitch Co. Earnings Conference Call

Stores and distribution expense for the quarter included approximately $2

million of accelerated depreciation from our DC consolidation, lower than previously anticipated due to an extension in the expected service life of our second DC.

Operating income for the quarter was $6.3 million versus $38.7 million a year ago. Operating margin fell 390 basis points with expense deleverage of 160 basis points adding to the gross margin erosion.

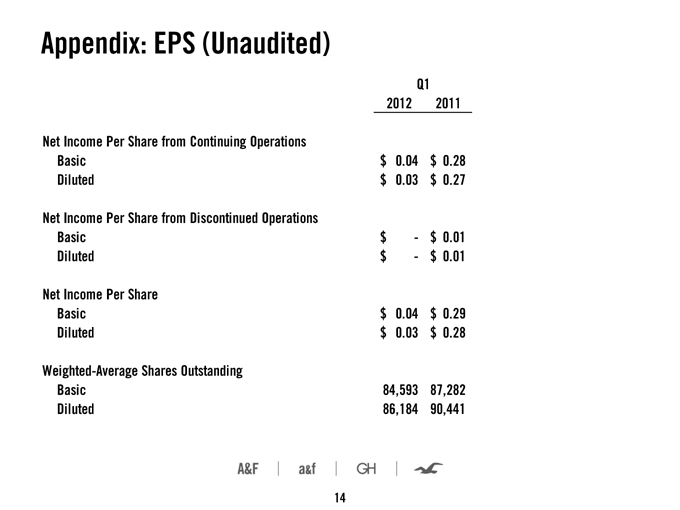

The tax rate for the quarter was 43% and diluted EPS for the quarter was $0.03 versus $0.28 for the prior year quarter.

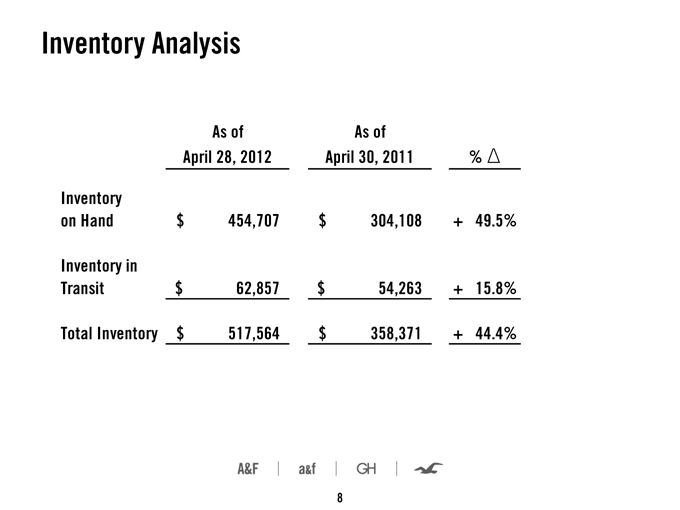

Turning to the

balance sheet, we ended the quarter with total inventory at cost up 44% versus a year ago. This was higher than planned due to a lower sales trend. However, we continue to expect a significantly moderated rate of growth at the end of the spring

season and have adjusted our receipts for the balance of the year to reflect the current sales trend.

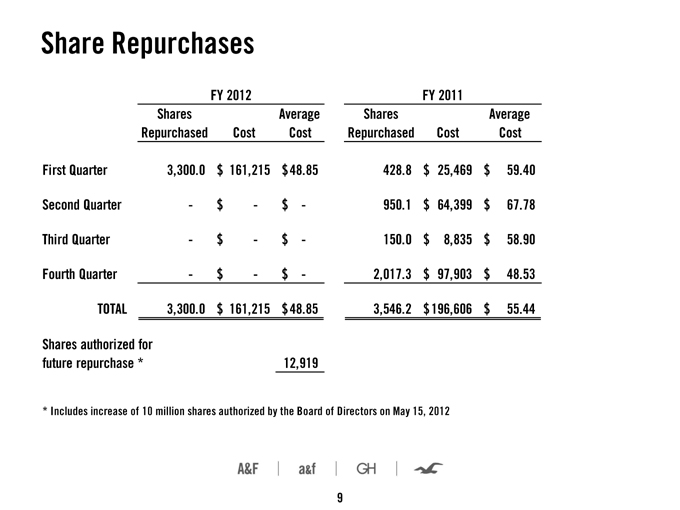

During the quarter we repurchased

approximately 3.3 million shares at an average cost of around $49 per share bringing our total repurchases to 8.4 million shares in the past two years. We ended the quarter with $321.6 million in cash and cash equivalents and $37.9 million

of current marketable securities. In addition, we have available $349 million under our revolving credit facility and $300 million under our term loan facility. During the quarter we liquidated 62.4 million of our auction rate securities.

At our Board meeting yesterday the Board approved the addition of 10 million shares to our share repurchase authorization bringing our

total outstanding authorization to 12.9 million shares.

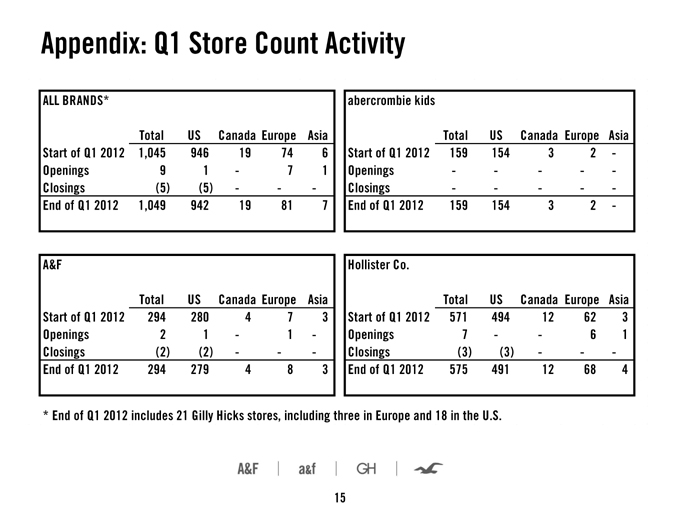

As Mike mentioned, we opened one flagship and seven international Hollister

stores during the quarter. Details of Hollister openings for the quarter are included on page 10 of the investor presentation. In the US we closed five stores during the quarter.

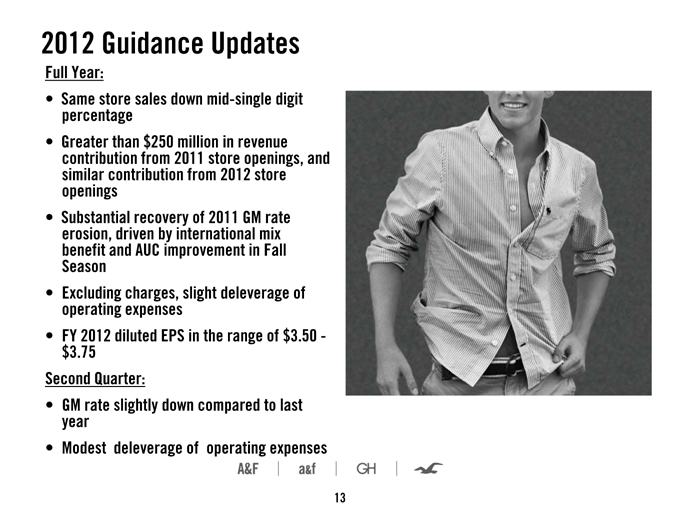

With regard to our expectations for the fiscal year, based on the first-quarter trend we are now planning for mid-single-digit negative [likes] for the full year comprising modestly positive same-store

sales for US chain stores and mid-teen negative likes for international and US tourist stores.

This projection is based on the trend over the

last quarter and does not include any further slowing from that trend. However, it also does not include any benefit from lapping of more favorable compares later in the year.

We have revised our non-comp store sales projections consistent with the lower trend for comp stores and now anticipate the sales growth contribution for the year from new stores to be around $500

million. Our lower sales projection is partially offset by a higher projected gross margin rate and lower expenses.

The higher gross margin

rate reflects continued progress on AUC reductions and the fact that a much higher percentage of our commitments is now locked in. A lower operating income projection for the year is offset by a lower share count at the end of the first quarter, as

a result of which we are leaving our EPS guidance of full-year diluted EPS in the range of $3.50 to $3.75 unchanged. The greatest sensitivity in this projection remains the sales trend.

With regard to the second quarter, we expect the gross margin rate to be slightly down versus last year, we expect modest expense deleverage based on our current sales projection. Again, this is based on

the sales trend for the past quarter. We will report second-quarter sales and earnings on Wednesday, August 15, 2012.

This concludes our

prepared comment section of the call and we are now available to take your questions. Thank you.

QUESTIONS AND ANSWERS

Operator

(Operator Instructions). Jeff

Klinefelter, Piper Jaffray.

|

|

|

| THOMSON REUTERS STREETEVENTS | www.streetevents.com | Contact Us

©2012 Thomson Reuters. All rights reserved. Republication or redistribution of

Thomson Reuters content, including by framing or similar means, is prohibited without the prior written consent of Thomson Reuters. ‘Thomson Reuters’ and the Thomson Reuters logo are registered trademarks of Thomson Reuters and its

affiliated companies. |

|

|

5

MAY 16, 2012 / 12:30PM, ANF—Q1 2012 Abercrombie & Fitch Co. Earnings Conference Call

Jeff Klinefelter—Piper Jaffray—Analyst

A few questions, this morning, one on Europe. Mike and Jonathan, I’m wondering if you could just give a little bit more color and

what you’re experiencing, recognizing the headwinds—the economic headwinds, kind of on a sequential basis between Hollister and your flags, particularly the key London, Milan and any updates on Asia or Tokyo?

And then with respect to Hollister specifically, it seems like that’s really where more of the sequential deterioration has come from. Could you

talk about that and then how you’re viewing traffic trends into the second half of the year for those businesses? And then just a couple housekeeping issues. Jonathan, tax rate—are you forecasting the tax rate from Q1 through the balance

of the year in your guidance and then also inventory units versus dollars? Thank you.

Jonathan

Ramsden—Abercrombie & Fitch Co.—EVP & CFO

Maybe I’ll start with the last (inaudible). The tax rate

guidance for the year is the same as we had given out in February which was slightly below 35% for the full year. The Q1 rate is just distorted because of the low absolute level of operating income and some of the discrete period items, so that

isn’t reflective of what we would anticipate for the full year.

I think just going back to your question on trends; clearly the overall

environment in Europe and the trend of our business was tougher in this quarter than it was in the fourth quarter. Hollister did move from having comped positively to comping negatively. Having said that, we were up against very strong comps in the

first couple of quarters of last year, I think 20% plus for Hollister Europe although relatively few stores in the comp base. So we were cycling against that.

As we said in the guidance for the year, we’re basically assuming the run rate for the trend in Q1 continues on a full-year basis, so we’re projecting down mid-single-digit comps for the full

year. As we said, that doesn’t allow for any potential further deterioration in the trend, but it also doesn’t allow any benefit for the lapping of the sequentially easier compares as we get into the latter part of the year.

Jeff Klinefelter—Piper Jaffray—Analyst

I guess I’m curious about any changes that you’re observing in terms of overall competitive promotional cadence. You mentioned cannibalization in terms of impacting your comps, although you also

said that you’ve been factoring in a lot of these trends in your modeling for new stores.

I think that’s probably the greatest

concern that people would have is what is factored in in terms of top-line tolerance in stress testing these new stores. So I was just wondering if you could share a little bit about the environment that you’re observing and then also what kind

of downside protection you have in your model.

Jonathan Ramsden—Abercrombie & Fitch Co.—EVP &

CFO

I think the key point, Jeff, is—as Mike said in his comments, when we open new stores we want to be confident that we can hit

that 30% four wall margin, even after allowing for the effect of cannibalization of other stores. So we take that into account when we look at those stores and we put a conservative volume on it, or one that we believe is conservative.

And as of today as we’re opening new stores we’re looking at volumes based on the current trends of the business. So, a key point remains that

we want to be opening stores that incrementally are delivering a 30% margin on a conservative volume figure. And as Mike said, if you look at the great majority of our stores, or certainly if you look at our stores in aggregate and the majority of

our stores, today they are operating above that 30% four wall margin.

|

|

|

| THOMSON REUTERS STREETEVENTS | www.streetevents.com | Contact Us

©2012 Thomson Reuters. All rights reserved. Republication or redistribution of

Thomson Reuters content, including by framing or similar means, is prohibited without the prior written consent of Thomson Reuters. ‘Thomson Reuters’ and the Thomson Reuters logo are registered trademarks of Thomson Reuters and its

affiliated companies. |

|

|

6

MAY 16, 2012 / 12:30PM, ANF—Q1 2012 Abercrombie & Fitch Co. Earnings Conference Call

Jeff Klinefelter—Piper Jaffray—Analyst

Thank you.

Mike

Jeffries—Abercrombie & Fitch Co.—Chairman & CEO

We are finding, Jeff, that we are probably our biggest

competitor internally in Europe.

Operator

Dana Telsey,Telsey Advisory Group.

Dana Telsey—Telsey Advisory

Group—Analyst

By the way, I was in the Paris store on Saturday and it looks terrific. And wanted to just get some more color. As you

think about Europe, macro versus cannibalization, how do you think about the slicing and dicing of the environment and just cannibalization?

And then also, as you think about inventory levels, how do you see inventories progressing? And as the inventories—is it more US or international?

And just lastly on prices, I think you’re going to adjust prices in Europe have they been adjusted or what you see there? Thank you.

Mike Jeffries—Abercrombie & Fitch Co.—Chairman & CEO

Okay, macro versus cannibalization. I think the biggest factor in the downtrend in Europe is clearly macro. Cannibalization would come second and then I

think the third issue is the incredible opening rate and the fact that it was—some of these rates weren’t sustainable.

We are, as

Jonathan said, planning cannibalization into our future model and it is a factor. We are planning the macro environment to stay the way it is, we’re not planning for it to get worse. But our assumption is that it’s going to stay the same

for the rest of the year. Want to talk about inventory levels?

Jonathan Ramsden—Abercrombie & Fitch

Co.—EVP & CFO

Sure. In terms of inventory, Dana, we do expect the rate of growth to moderate significantly at the end of Q2.

Part of what you see at the end of Q1 is essentially a timing effect.

We have a lot of the spring goods sitting there today and as we look to

the balance of the year we are planning based on that negative mid-single digit like assumption in terms of how we are planning inventory to the end of the year. So on that basis we have reduced receipts over the last couple of months on a full-year

basis, although that has limited impact on where we were at the end of Q1.

Mike Jeffries—Abercrombie & Fitch

Co.—Chairman & CEO

The last part of the question pricing; in Europe we are slightly above last year for the spring season,

will be slightly below for the fall season.

Dana Telsey—Telsey Advisory Group—Analyst

Thank you.

|

|

|

| THOMSON REUTERS STREETEVENTS | www.streetevents.com | Contact Us

©2012 Thomson Reuters. All rights reserved. Republication or redistribution of

Thomson Reuters content, including by framing or similar means, is prohibited without the prior written consent of Thomson Reuters. ‘Thomson Reuters’ and the Thomson Reuters logo are registered trademarks of Thomson Reuters and its

affiliated companies. |

|

|

7

MAY 16, 2012 / 12:30PM, ANF—Q1 2012 Abercrombie & Fitch Co. Earnings Conference Call

Operator

Lorraine Hutchinson, Bank of America.

Lorraine Hutchinson—BofA Merrill

Lynch—Analyst

Just wanted to follow up on the gross margin, it was significantly better than your plan. And I was just wondering if

you could give us a little bit more information, how much of that was that the competitive environment was better? How much of that was AURs sticking and what we should expect going forward?

Jonathan Ramsden—Abercrombie & Fitch Co.—EVP & CFO

Lorraine, I think as we said when we came into the quarter, we were counting on that sort of aggressive environment we saw in the fourth quarter

continuing and our AUR assumption was based on that. In reality as it turned out we were able to do better than that on AUR and get our AUR in the US business up a little bit. So that helped.

And then in terms of the impact on the quarter in mark-down reserve, that effect kind of flowed through into that. And I think clearly given everything we’ve seen in the fourth quarter we had a

fairly conservative mindset coming into the season about AUR and gross margin.

Lorraine Hutchinson—BofA Merrill

Lynch—Analyst

Thank you.

Operator

Randy Connick, Jefferies.

Amanda Sigmund—Jefferies & Co.—Analyst

Hi, good morning, this is Amanda Sigmund on for Randy. Just a question to follow up on that. Given the less promotional environment you saw in the first quarter, does that change your thinking for the

promotional cadence for the balance of this year?

And then just a question on the share repurchases; that was stepped up nicely in the

quarter and obviously you increased the authorization. Is there any further buy back baked into the outlook now for the $3.50 to $3.75? Thank you.

Mike Jeffries—Abercrombie & Fitch Co.—Chairman & CEO

I’ll take the first part of the question. We were hoping and pushing to raise the AUR for the balance of the year.

Jonathan Ramsden—Abercrombie & Fitch Co.—EVP & CFO

On the second part, Amanda, we don’t count in any further buybacks relative to where we ended Q1 in terms of what’s baked into the guidance.

|

|

|

| THOMSON REUTERS STREETEVENTS | www.streetevents.com | Contact Us

©2012 Thomson Reuters. All rights reserved. Republication or redistribution of

Thomson Reuters content, including by framing or similar means, is prohibited without the prior written consent of Thomson Reuters. ‘Thomson Reuters’ and the Thomson Reuters logo are registered trademarks of Thomson Reuters and its

affiliated companies. |

|

|

8

MAY 16, 2012 / 12:30PM, ANF—Q1 2012 Abercrombie & Fitch Co. Earnings Conference Call

Amanda Sigmund—Jefferies & Co.—Analyst

Thank you.

Operator

Brian Tunick, JPMorgan.

Brian Tunick—JPMorgan—Analyst

Thanks, good morning, guys. One for John and one for Mike. I guess, John, it felt like at the beginning of the year we thought you guys cut your guidance from $4.75 down to that $3.50, $3.70 level because

of taking comp guidance down to flat. And now it sounds like you’re taking comps down again, but keeping that $3.50 to $3.75.

So just

hoping to get a little more color on what the offset is there and is it mostly gross margins. And then if Mike could just comment sort of on how you’re viewing I guess China differently from Japan and what sort of market research you guys have

done and what you think will be different from the outcome there? Thanks very much, guys.

Jonathan

Ramsden—Abercrombie & Fitch Co.—EVP & CFO

On the first part, gross margin is a significant driver of

the offset to the lower sales trend. A big piece of that is that we now have a much higher confidence level in our AUC reductions for the full year. We were feeling very fairly positive about that back in February, but now much of the commitment is

locked in and we have continued to make progress in terms of the reductions we’re seeing there.

So we feel very good about AUC and now

that is substantially locked in for the year at this point, there is still some open for Christmas. So that was one piece of it. Expenses also came down obviously in part as an offset to sales and then the share count is lower by several million

shares than we had assumed back at the time of the guidance in February.

So there really were three principle drivers. And then the other

piece that’s having a little bit of an impact is a slightly higher AUR assumption than we had back in February just based on what we’ve seen in the first quarter.

Mike Jeffries—Abercrombie & Fitch Co.—Chairman & CEO

Let me comment on the second question, Brian. First, let me give you a little more color on Japan. We are doing a lot of business in our Ginza flagship. Our problem in that flagship is that we

made—in an effort to get into Japan quickly, we made a deal that was not very economic. In our rational economic deal in that site we’d be making a lot of money.

We understand more about Japan than we have in the past. There will be Hollister mall stores in Japan. China is a very huge focus of ours and we have been looking at it extensively, we are off to, we

think, a very good start. We’re, as a company, really engaged. And we’ve engaged many, many people in China to figure this market out.

As I said this morning, we think opening the Hong Kong flagship will be very meaningful to China and we are negotiating for a flagship in China for next year. We’re taking this very seriously; we

think there’s a lots of business to be done in China.

Operator

Robin Murchison, SunTrust.

|

|

|

| THOMSON REUTERS STREETEVENTS | www.streetevents.com | Contact Us

©2012 Thomson Reuters. All rights reserved. Republication or redistribution of

Thomson Reuters content, including by framing or similar means, is prohibited without the prior written consent of Thomson Reuters. ‘Thomson Reuters’ and the Thomson Reuters logo are registered trademarks of Thomson Reuters and its

affiliated companies. |

|

|

9

MAY 16, 2012 / 12:30PM, ANF—Q1 2012 Abercrombie & Fitch Co. Earnings Conference Call

Robin Murchison—SunTrust Robinson Humphrey—Analyst

Two questions. Can you parse out the UK from Continental Europe if there is a difference in performance? And secondly, regarding

cannibalization, does that suggest anything for forward unit growth in Europe? Thank you.

Mike

Jeffries—Abercrombie & Fitch Co.—Chairman & CEO

I don’t know that we want to comment on

country-by-country performance. Jonathan, what do you think?

Jonathan Ramsden—Abercrombie & Fitch

Co.—EVP & CFO

I mean I think we haven’t seen some of the big discrepancies you’ve heard other people talking

about. I mean we haven’t seen that necessarily same divide between Northern and Southern Europe, we could probably say that. But I’m not sure there’s much else we can add on that.

Mike Jeffries—Abercrombie & Fitch Co.—Chairman & CEO

Unit growth?

Jonathan

Ramsden—Abercrombie & Fitch Co.—EVP & CFO

I’m not sure I really understood the question, Robin, on

the cannibalization (inaudible) on unit growth.

Robin Murchison—SunTrust Robinson Humphrey—Analyst

Sorry, the question gets to if there’s cannibalization does that change your thinking at all in terms of unit growth in Europe?

Jonathan Ramsden—Abercrombie & Fitch Co.—EVP & CFO

Okay. Well again, it all comes back to that 30% four wall margin and if we could open the store and then net of the effects of cannibalization it can

deliver that 30% on a conservative volume assumption we would continue to go ahead. Based on—looking at what’s in the plan today, we don’t foresee for Hollister that having any significant impact on score store count plans.

Most of the stores even after cannibalization are comfortably beating the hurdle rate even with that negative likes we’ve seen over the

past quarter for Hollister. For A&F we have pulled back on a couple of instances where we weren’t satisfied that we were going to meet the hurdle rate. So a little bit of an adjustment there, but overall not a major adjustment to the plan.

Mike Jeffries—Abercrombie & Fitch Co.—Chairman & CEO

But we’re looking at it (technical difficulty) point — we’re looking at it very hard in a very disciplined way.

Robin Murchison—SunTrust Robinson Humphrey—Analyst

Good, thank you.

|

|

|

| THOMSON REUTERS STREETEVENTS | www.streetevents.com | Contact Us

©2012 Thomson Reuters. All rights reserved. Republication or redistribution of

Thomson Reuters content, including by framing or similar means, is prohibited without the prior written consent of Thomson Reuters. ‘Thomson Reuters’ and the Thomson Reuters logo are registered trademarks of Thomson Reuters and its

affiliated companies. |

|

|

10

MAY 16, 2012 / 12:30PM, ANF—Q1 2012 Abercrombie & Fitch Co. Earnings Conference Call

Operator

Janet Kloppenburg, JJA Research.

Janet Kloppenburg—JJK

Research—Analyst

Mike, I wondered if you could talk a little bit about any progress you’re seeing at the European flagship since

you’ve adjusted the AUCs. I know you just said that you expect some progress as the year goes by, but I was wondering if you could talk a little bit about that mix shift in price points there.

And you also said that you felt good about China, but given that there’s some Hollister stores that have been open for a while, I wondered if you

could talk a little bit about the performance there vis-a-vis how the initial stores opened in Europe. That would be an interesting analysis if we could learn more about how they’re ramping.

And Jonathan, I don’t know if you answered Jeff’s question about tax rate, but maybe you could help us with our tax rate number. And at the

expense line, can you maybe help me understand on both the store and operating and the MG&A line whether the rate of increase in expenses will continue to be the same or if it should moderate as we go through the year? And I had one more

question just about the operating margin rate of the direct business, which seems to be coming down. Thanks.

Mike

Jeffries—Abercrombie & Fitch Co.—Chairman & CEO

Okay, let’s go through the list.

Janet Kloppenburg—JJK Research—Analyst

Sorry.

Mike Jeffries—Abercrombie & Fitch

Co.—Chairman & CEO

That’s okay. Pricing in the flagships. We have adjusted that mix and it’s very difficult to

tell what that result is candidly. We think it’s the right thing to do in terms of positioning of the stores, but looking at the reductions and the mix it’s very difficult to have a direct correlation. But we think we’re doing the

right things.

China, we’re pleased with how we’ve started China. I think what we’re learning in China is from a real estate

perspective we have to treat China the same way we did Europe, which was to be in the best centers. We opened in—the first China store is in Shanghai, it is a good store, it’s gaining momentum, it would be ranked as a good Hollister store

anywhere in the world.

We opened in Shenzhen which is a secondary city and we’re meeting our plan, which wasn’t as aggressive as

Shanghai. And we opened our first store in Beijing in a mall where we shouldn’t have opened. And our lesson there is that our first store in Beijing should not have been in kind of a fair grade mall. So we’re optimistic about China,

we’re optimistic about all of the brands there. I think that’s all I can say about China.

Jonathan

Ramsden—Abercrombie & Fitch Co.—EVP & CFO

Janet, on the other part, the tax rate we’re saying

still slightly below—we didn’t update the guidance we gave in February which was slightly below 35% for the full year. On expense what we’re saying in the presentation is modest deleveraging Q2 and modest data de-leverage for the full

year. So better than what we saw in Q1 but still some deleverage now on a full-year basis.

|

|

|

| THOMSON REUTERS STREETEVENTS | www.streetevents.com | Contact Us

©2012 Thomson Reuters. All rights reserved. Republication or redistribution of

Thomson Reuters content, including by framing or similar means, is prohibited without the prior written consent of Thomson Reuters. ‘Thomson Reuters’ and the Thomson Reuters logo are registered trademarks of Thomson Reuters and its

affiliated companies. |

|

|

11

MAY 16, 2012 / 12:30PM, ANF—Q1 2012 Abercrombie & Fitch Co. Earnings Conference Call

And then in terms of the operating margin on direct, I think we had said on

the last earnings call that we anticipated mid-40s would be a reasonable run rate going forward. What you have baked into that margin and for the other channels too, is still that significant year-over-year costing impact in Q1 which will turn

around nicely over the next couple of quarters. But we still think that mid-40s run rate for direct-to-consumer is about the right ball park going forward.

Janet Kloppenburg—JJK Research—Analyst

So we should look for it to

be maintained here, right, Jonathan, around this level?

Jonathan Ramsden—Abercrombie & Fitch

Co.—EVP & CFO

Yes, I think we said—we’d see it being in the mid-40s on a go-forward basis, and obviously on a

full-year basis there are some quarterly swings in all of the channels. And what you’re seeing for international stores, clearly they were below 30% for Q1 but adjusting for the costing effect and the seasonalization, that would still put us

above 30% on a full-year basis.

Janet Kloppenburg—JJK Research—Analyst

Okay, thanks so much and good luck.

Mike Jeffries—Abercrombie & Fitch Co.—Chairman & CEO

I think I have one more store for you that’s our Hollister store in Hong Kong and Festival Walk is a phenomenal store; it would be rated up at the

—somewhere at the top of our store list.

Janet Kloppenburg—JJK Research—Analyst

Great. Lots of luck. Thank you.

Operator

Evren Kopelman,Wells Fargo.

Unidentified Participant

Hi, thanks,

it’s Marin in for Evren. Just quickly, when we look at the US stores, in terms of the significant comp decline in the tourist stores do you think that’s because there’s fewer tourists or do you think it’s more of a brand issue?

Thanks.

Mike Jeffries—Abercrombie & Fitch Co.—Chairman & CEO

A, fewer tourists.

Unidentified Participant

Okay.

|

|

|

| THOMSON REUTERS STREETEVENTS | www.streetevents.com | Contact Us

©2012 Thomson Reuters. All rights reserved. Republication or redistribution of

Thomson Reuters content, including by framing or similar means, is prohibited without the prior written consent of Thomson Reuters. ‘Thomson Reuters’ and the Thomson Reuters logo are registered trademarks of Thomson Reuters and its

affiliated companies. |

|

|

12

MAY 16, 2012 / 12:30PM, ANF—Q1 2012 Abercrombie & Fitch Co. Earnings Conference Call

Operator

Omar Saad, ISI Group.

Omar Saad—ISI Group—Analyst

Thanks for all the information. I wanted to ask you guys as you’re looking at the European stores and some of the tourist stores in the US, what kind

of information are you seeing and patterns are you seeing with the consumers? Are you seeing a lot of repeat customers and they’re buying less? Are you seeing less repeat customers?

We can still see that there’s lines in front of a lot of these doors, so there’s still clearly a lot of demand. But is on the margin causing that negative like for like in the store? How much of

it is traffic and how much of it is losing customers? Have you done that kind of level of analysis with the consumers that are flowing through there? Thank you.

Mike Jeffries—Abercrombie & Fitch Co.—Chairman & CEO

It’s very—we do not have that level of detail, hope to develop that capability. And measuring traffic in our flagship stores is really impossible because of the level of traffic. But we see that

traffic is down in those stores and that’s what is driving the volume. We clearly see that in the US tourist stores.

Omar

Saad—ISI Group—Analyst

Got you, all right, thanks.

Operator

Liz Dunn, Macquarie.

Liz Dunn—Macquarie Research—Analyst

Just a point of clarification

on the comp guidance for international of mid-teens decline going forward. Is that a constant currency comp or—because just when we do the math it looks like the comp decline in the first quarter in the international stores was a bit sharper

than that.

And then my second question relates to real estate decisions. You know, you talked about some missed steps in Japan and in China.

How are you changing your real estate decision making process or the team? How are you adjusting so that some of these missteps don’t happen in the future? Thanks.

Jonathan Ramsden—Abercrombie & Fitch Co.—EVP & CFO

Liz, [this is on the first point]. We report comps on a constant currency basis and that applies both to what we reported for Q1 and what we’re

projecting for the full year. I’m looking to Brian to confirm that.

Unidentified Company Representative

That’s correct.

|

|

|

| THOMSON REUTERS STREETEVENTS | www.streetevents.com | Contact Us

©2012 Thomson Reuters. All rights reserved. Republication or redistribution of

Thomson Reuters content, including by framing or similar means, is prohibited without the prior written consent of Thomson Reuters. ‘Thomson Reuters’ and the Thomson Reuters logo are registered trademarks of Thomson Reuters and its

affiliated companies. |

|

|

13

MAY 16, 2012 / 12:30PM, ANF—Q1 2012 Abercrombie & Fitch Co. Earnings Conference Call

Jonathan Ramsden—Abercrombie & Fitch

Co.—EVP & CFO

So I think that answers the first part.

Liz Dunn—Macquarie Research—Analyst

But, can you break out what

that currency hit to the sales or to the comp was?

Jonathan Ramsden—Abercrombie & Fitch

Co.—EVP & CFO

Yes, I mean the currency effect is shown, if you look at it—if you go to page 5 of our investor

presentation, the foreign exchange impact was less than 1% year over year in the first quarter. So it was negative. But we separate that out from the impact of comp store sales which are then stated on a constant currency basis.

Liz Dunn—Macquarie Research—Analyst

Okay, great. Got it.

Mike Jeffries—Abercrombie & Fitch

Co.—Chairman & CEO

The answer to the second part of your question is that we have essentially a new real estate group. And

to be transparent about this, obtaining real estate globally is a different matter from obtaining real estate in malls in the United States. And we had to change our team in terms of level of experience. And actually the amount of oversight that

we’re giving that part of the business today. I feel comfortable that we’re making the right decisions.

Liz

Dunn—Macquarie Research—Analyst

Great, thanks. Good luck.

Operator

Kimberly Greenberger, MSB.

Kimberly Greenberger—Morgan Stanley—Analyst

Morgan Stanley. This morning I think, Jonathan, you said that US comps are running up 4%. I wasn’t—I think I missed the international comp, if you could just remind me what that was. And my

question is on the divisional margins.

We saw about a 730 basis point decline in the direct-to-consumer operating income rate. I’m

wondering if you can just help us understand the big drivers behind that. And also, I presume that the 580 basis point decline in the international store operating income rate is driven by the negative comp, but if there are other factors in there

as well I would be interested to hear that. Thank you so much.

|

|

|

| THOMSON REUTERS STREETEVENTS | www.streetevents.com | Contact Us

©2012 Thomson Reuters. All rights reserved. Republication or redistribution of

Thomson Reuters content, including by framing or similar means, is prohibited without the prior written consent of Thomson Reuters. ‘Thomson Reuters’ and the Thomson Reuters logo are registered trademarks of Thomson Reuters and its

affiliated companies. |

|

|

14

MAY 16, 2012 / 12:30PM, ANF—Q1 2012 Abercrombie & Fitch Co. Earnings Conference Call

Jonathan Ramsden—Abercrombie & Fitch

Co.—EVP & CFO

Okay, Kimberly, thanks. On the US comps, what we said was the total retail segment comps including DTC were up

4%. So same-store sales [in the U.S. chain] (added by company after the call) were up 1% and then DTC took it up 4%, which we think is an appropriate way to look at it from a US standpoint. The overall comp we gave of down 5% is purely same-store

sales.

And we don’t include DTC in that partly because we think it’s problematic to do that in terms of looking at our global DTC

business and including all of that in a comp number as we expand our new stores significantly internationally. But you can kind of do the math and if you added our global DTC growth back to the negative 5 comp you’d be sort of flattish on an

overall comp basis if you did include all of that DTC growth.

With regard to the DTC operating income rate, I think we touched on that in the

answer to Janet’s question. A big piece of it is the sourcing cost impact year over year which is affecting all of the channels. But I think we’ve also said that the rates we had in 2011 were probably not sustainable anyway and that we

anticipate a go-forward rate closer to the mid-40s for direct, particularly given some of the investments we’re making in the channel, which are necessary to drive the continued growth.

Then the third part of the question, the decline in international—a big piece of that, again, was the sourcing cost issue year over year. That would have been the biggest single component and then

some deleveraging of expenses as a result of the negative comps.

Kimberly Greenberger—Morgan Stanley—Analyst

I’m just wondering why there was so little impact in the US store. We saw only about a 110 basis points decline in the operating

income rate. But I would have thought that you would see a similar kind of sourcing cost inflation within each channel, but the profit rate in US stores was much, much, much closer to last year. So I’m just trying to understand the disparity of

results by channel; if there’s an easy explanation, that would be great.

Jonathan Ramsden—Abercrombie &

Fitch Co.—EVP & CFO

Unfortunately there isn’t an easy explanation, Kimberly, it’s a little bit complicated due to

the markdown reserve issue, which is sort of abnormally—having an abnormal impact on this quarter. So essentially the mark-down reserve we took at the end of the fourth quarter disproportionately benefited the US stores in Q1 in terms of how

that margin is coming through.

I think we’ve included this analysis and we intend to include it going forward quarter by quarter. I

think it is a little bit distorted by that effect in this particular quarter, but that effect should go away or certainly be less significant on a full-year basis.

Kimberly Greenberger—Morgan Stanley—Analyst

Thank you so much.

Operator

Barbara Wyckoff,

CLSA.

Barbara Wyckoff—CLSA—Analyst

A question for Mike. Can you talk about women’s bottoms and the women’s bottoms business, denim versus colored twill, silhouettes? How do you see this going forward; how are shorts performing;

talk about skirts and dresses, please?

|

|

|

| THOMSON REUTERS STREETEVENTS | www.streetevents.com | Contact Us

©2012 Thomson Reuters. All rights reserved. Republication or redistribution of

Thomson Reuters content, including by framing or similar means, is prohibited without the prior written consent of Thomson Reuters. ‘Thomson Reuters’ and the Thomson Reuters logo are registered trademarks of Thomson Reuters and its

affiliated companies. |

|

|

15

MAY 16, 2012 / 12:30PM, ANF—Q1 2012 Abercrombie & Fitch Co. Earnings Conference Call

Mike Jeffries—Abercrombie & Fitch

Co.—Chairman & CEO

Oh, Barbara, I would love to talk to you about this, but really can’t. The women’s bottom

business is good. I don’t want to give you forward projections. The short business is good, women’s bottoms business is good.

Barbara Wyckoff—CLSA—Analyst

Okay.

Operator

Paul Lejuez, Nomura.

Paul Lejuez—Nomura Asset Management—Analyst

Just wondering if you could share with us, and sorry if I missed this, the AUR in the US versus the European business? Also was wondering

what kind of AUC reductions you are looking for, just ballpark; just wondering if you will see down double digits at some point this year?

And also trying to understand the view of gross margins getting a little bit better with the inventory levels up where they are. I think you said the

markdown reserve was lower at the end of the quarter here. Just wondering what that was, if you can share that with us, versus last year. Thanks.

Jonathan Ramsden—Abercrombie & Fitch Co.—EVP & CFO

I guess in terms of AUR, Paul, we said US AURs were up slightly. And then internationally it was a little bit more, so the overall AUR was up modestly for

the quarter in total. AUC, we’d said on the last earnings call we expected to be into the double-digit reductions in the back half of the year. And as we said earlier on, we’ve made continued progress on that and that is now substantially

locked in. So we feel very good about that.

With regard to inventory, as we said we have aligned our receipts for the balance of the year to

that negative mid-single-digit trend that we have talked about on a full-year basis. That is what we are now buying to. And then in terms of the markdown reserve at the end of Q1, I don’t have that number to hand. It was lower than we had

anticipated coming into the quarter, primarily reflecting some of the progress we are making in continuing to seek to get AURs up. But we will obviously publish that number as part of the Q.

Paul Lejuez—Nomura Asset Management—Analyst

But was it actually

done versus last year, the mark-down reserve?

Jonathan Ramsden—Abercrombie & Fitch Co.—EVP & CFO

(Multiple speakers).

Paul Lejuez—Nomura Asset Management—Analyst

Relative to your plan.

|

|

|

| THOMSON REUTERS STREETEVENTS | www.streetevents.com | Contact Us

©2012 Thomson Reuters. All rights reserved. Republication or redistribution of

Thomson Reuters content, including by framing or similar means, is prohibited without the prior written consent of Thomson Reuters. ‘Thomson Reuters’ and the Thomson Reuters logo are registered trademarks of Thomson Reuters and its

affiliated companies. |

|

|

16

MAY 16, 2012 / 12:30PM, ANF—Q1 2012 Abercrombie & Fitch Co. Earnings Conference Call

Jonathan Ramsden—Abercrombie & Fitch

Co.—EVP & CFO

It was down a little to last year is what Brian is saying.

Paul Lejuez—Nomura Asset Management—Analyst

Got you. And when you say your inventory is lined up to down mid-single-digit, you’re talking inventory dollars, correct?

Jonathan Ramsden—Abercrombie & Fitch Co.—EVP & CFO

Yes, in effect, in terms of what we’re buying to. And obviously we’re not buying to minus 5 in total because clearly there is new store sales

growth and direct-to-consumer growth. But in terms of how we build up the buy we start from that negative mid-single-digit comp on a dollar basis.

Paul Lejuez—Nomura Asset Management—Analyst

Which means units

would be down mid-teens on a comp store basis?

Jonathan Ramsden—Abercrombie & Fitch Co.—EVP &

CFO

No, I don’t think we’re going to get into the AUR assumption baked in to that.

Paul Lejuez—Nomura Asset Management—Analyst

Just—I was talking from a cost perspective. If your costs or AUC is going to be down double-digits wouldn’t that imply that units would be down somewhere in the mid-teens?

Jonathan Ramsden—Abercrombie & Fitch Co.—EVP & CFO

I’m not sure I’m following the logic.

Paul Lejuez—Nomura Asset Management—Analyst

You’re matching dollars down mid-single-digit on a comp store basis and your average costs per unit are going to be down double-digits.

Jonathan Ramsden—Abercrombie & Fitch Co.—EVP & CFO

That’s what we said for the back half of the year, yes, from a (multiple speakers).

Paul Lejuez—Nomura Asset Management—Analyst

So units would have to

be down double-digits, correct?

|

|

|

| THOMSON REUTERS STREETEVENTS | www.streetevents.com | Contact Us

©2012 Thomson Reuters. All rights reserved. Republication or redistribution of

Thomson Reuters content, including by framing or similar means, is prohibited without the prior written consent of Thomson Reuters. ‘Thomson Reuters’ and the Thomson Reuters logo are registered trademarks of Thomson Reuters and its

affiliated companies. |

|

|

17

MAY 16, 2012 / 12:30PM, ANF—Q1 2012 Abercrombie & Fitch Co. Earnings Conference Call

Jonathan Ramsden—Abercrombie & Fitch

Co.—EVP & CFO

Well, I don’t think you can say that on units. I mean I guess what affects the units is the comp trend

and the AUR assumption. And what we’re saying is the comp trend we’re planning for negative mid-single-digits and AUR we just previously said flat for the US chain business. We’re hoping to make a bit of progress on that as we did in

the first quarter.

For international it’s a bit of a different story because we were up in the first half of the year, year over year.

But as Mike alluded to earlier, we would expect that to turn slightly negative for the back half of the year. So I don’t think AUC really has a bearing on—(multiple speakers).

Paul Lejuez—Nomura Asset Management—Analyst

That’s right, it

could actually be up a bit now that I think about it. Sorry, I was just doing the math of the wrong way there. Okay, got you. Thank you.

Jonathan Ramsden—Abercrombie & Fitch Co.—EVP & CFO

Thank you.

Operator

Marni Shapiro,The Retail Tracker.

Marni Shapiro—The Retail Tracker—Analyst

I think the stores look very happy. So I have a couple of just quick questions. First, I want—you had a trend where the fashion has outpaced what I call more of the core business, the T-shirts and

sweats, and you were sort of chasing into that business. I wonder how you feel about your comfort level with keeping up with the fashion there; it does seem to still be outpacing the core on the sales.

And if you can talk just a little bit—and it feels as well—the promotions definitely feel very light this spring compared to what we’ve

seen over the last couple of months and seasons, particularly on the fashion side. And I want to make sure what I’m seeing is right there, particularly at Hollister, it feels even lighter than the other stores, which has been the more

promotional.

And just one last question on marketing. If you can just give us an update—has anything changed on the marketing side or

does it remain focused on the direct business and that part of the—that channel?

Mike

Jeffries—Abercrombie & Fitch Co.—Chairman & CEO

First part of the question, I feel that we continue to

make progress in fashion. So if I’m understanding the question correctly, I feel that that business will continue at a good rate (multiple speakers).

Marni Shapiro—The Retail Tracker—Analyst

You were in sort of a

[taste] mode on the fashion because it was selling faster, trying to get the balance a little better. Are you feeling good about that?

Mike Jeffries—Abercrombie & Fitch Co.—Chairman & CEO

Yes. But I think, Marni, that we’re always in chase mode for fashion. And I think that’s a good thing.

Marni Shapiro—The Retail Tracker—Analyst

Yes, I agree.

|

|

|

| THOMSON REUTERS STREETEVENTS | www.streetevents.com | Contact Us

©2012 Thomson Reuters. All rights reserved. Republication or redistribution of

Thomson Reuters content, including by framing or similar means, is prohibited without the prior written consent of Thomson Reuters. ‘Thomson Reuters’ and the Thomson Reuters logo are registered trademarks of Thomson Reuters and its

affiliated companies. |

|

|

18

MAY 16, 2012 / 12:30PM, ANF—Q1 2012 Abercrombie & Fitch Co. Earnings Conference Call

Mike Jeffries—Abercrombie & Fitch

Co.—Chairman & CEO

The promotions—I think we are less promotional and we anticipate being less. And from a marketing

perspective it is directed to the direct business, it continues to be.

Marni Shapiro—The Retail Tracker—Analyst

Is that true in Europe and China as well?

Mike Jeffries—Abercrombie & Fitch Co.—Chairman & CEO

Well, we don’t really market — our marketing is done in store. So we clearly have websites. I’m not sure I understand the question.

Marni Shapiro—The Retail Tracker—Analyst

Females, for example, are

a big marketing part for you guys, even Facebook here in the United States, I’m constantly seeing updates on Facebook from you guys. Are you doing things like that in Europe and China and Japan?

Jonathan Ramsden—Abercrombie & Fitch Co.—EVP & CFO

Well, we’re getting started, Marni, I mean we’re doing a lot more interactive marketing over here. We are getting started particularly in China

now. But we’re a long way away from where we are in the US. The only thing we do do in China in particular is focus on those new store openings and Hong Kong we’re making, as we mentioned earlier, a big push around that opening in terms of

creating awareness in Mainland China.

Mike Jeffries—Abercrombie & Fitch Co.—Chairman & CEO

And really look at Facebook to see what happened in London last weekend, that’s where our marketing effort is.

Marni Shapiro—The Retail Tracker—Analyst

And on the mobile side, are you guys pushing into the mobile technology at all, particularly in Japan and China? Or you’ll get there in time?

Jonathan Ramsden—Abercrombie & Fitch Co.—EVP & CFO

Yes is the answer. I mean we’re working so that all of our online interaction is sort of mobile enabled; that would apply not just in the US but also

internationally. I think we’ve said in the past that around 20% of our traffic online is already coming through mobile so clearly it has to be.

|

|

|

| THOMSON REUTERS STREETEVENTS | www.streetevents.com | Contact Us

©2012 Thomson Reuters. All rights reserved. Republication or redistribution of

Thomson Reuters content, including by framing or similar means, is prohibited without the prior written consent of Thomson Reuters. ‘Thomson Reuters’ and the Thomson Reuters logo are registered trademarks of Thomson Reuters and its

affiliated companies. |

|

|

19

MAY 16, 2012 / 12:30PM, ANF—Q1 2012 Abercrombie & Fitch Co. Earnings Conference Call

Marni Shapiro—The Retail Tracker—Analyst

Exactly, great. Congratulations, guys, good luck with summer.

Mike Jeffries—Abercrombie & Fitch Co.—Chairman & CEO

Thank you.

Jonathan Ramsden—Abercrombie & Fitch

Co.—EVP & CFO

Thank you.

Operator

Dave Weiner, Deutsche Bank.

Dave Weiner—Duetsche Bank—Analyst

Can you hear me okay? I just wanted to follow up on an earlier question about pricing, I want to make sure I understood the answer. Basically I was curious, I think you said that pricing, and I don’t

know whether this was referring globally or to Europe specifically, was kind of up modestly in the first half, going to be down modestly in the back half. I guess if you could just confirm that’s the case. And within Europe, is there any way

you can break that out between Abercrombie and Hollister? Do you kind of need to do that same type of cadence for both brands?

Mike

Jeffries—Abercrombie & Fitch Co.—Chairman & CEO

The answer is that we were describing Europe and I said

that we’d be down—up slightly in spring and down slightly in fall. A little more aggressively down in Abercrombie & Fitch then Hollister for the fall season.

Dave Weiner—Duetsche Bank—Analyst

Got you. And I guess — I

mean the pricing obviously is a—seems to be a key lever here where you’re trying to gauge it an economy in Europe that’s kind of deteriorating; it’s in a state of flux. So I mean how do you figure out ahead of time—how are

you trying to analyze what the appropriate pricing level is? I mean it seems that that’s a real challenge especially since your brands have a relatively short track record versus others there in the malls and whatnot.

Mike Jeffries—Abercrombie & Fitch Co.—Chairman & CEO

We look at sales on a weekly basis and we look at trend. Pricing is an important part of what we do. But it’s—how do I describe this? I suppose

the answer to the question is first, our first driver of business is not price anyplace in the world. We drive the business through differentiated store experience, through trend right product and then price is something that follows. We’ve

never driven the business through price and we don’t in Europe.

So pricing is a factor, but, as I said to Janet earlier in the session,

reducing the AURs in the flagships in terms of mix we haven’t been able to really see a result. It’s a very complex issue, but it’s not the issue that we’re obsessing with. We’re obsessing with right stores, right product

— that’s success.

|

|

|

| THOMSON REUTERS STREETEVENTS | www.streetevents.com | Contact Us

©2012 Thomson Reuters. All rights reserved. Republication or redistribution of

Thomson Reuters content, including by framing or similar means, is prohibited without the prior written consent of Thomson Reuters. ‘Thomson Reuters’ and the Thomson Reuters logo are registered trademarks of Thomson Reuters and its

affiliated companies. |

|

|

20

MAY 16, 2012 / 12:30PM, ANF—Q1 2012 Abercrombie & Fitch Co. Earnings Conference Call

Dave Weiner—Duetsche Bank—Analyst

Right. And so that strategy in Europe would—kind of that focus not so much—that first focus not so much on price. That would apply as much to

the Hollister stores in the mall as to the flagships?

Mike Jeffries—Abercrombie & Fitch

Co.—Chairman & CEO

Absolutely, absolutely.

Dave Weiner—Duetsche Bank—Analyst

Okay, great.Thanks for your

help.

Operator

John Kernan,

Cowen.

John Kernan—Cowen and Company—Analyst

I was wondering if you could update us on the (technical difficulty) store closures domestically both for Abercrombie and Hollister the remainder of this year.

Jonathan Ramsden—Abercrombie & Fitch Co.—EVP & CFO

We’ve said on the last earnings call 180 approximately between now and 2015. We haven’t given a specific figure for this year yet and

there’s a lot of water to go under the bridge on that. We did close five stores in the first quarter. We’ll be in a better position to give an update on that as we get later into the year when we start engaging directly with the landlords

with regard to plans to renew or close stores, but there really isn’t anything new relative to what we had said in February at this point.

John Kernan—Cowen and Company—Analyst

And then maybe I missed this, but FX guidance related to the euro for the remainder of the year, what’s embedded in your assumptions?

Jonathan Ramsden—Abercrombie & Fitch Co.—EVP & CFO

We had said in February it was about a negative $50 million full-year effect. It’s a little less than that at this point based on the current rates,

but they’re pretty close. On a full-year basis somewhat below negative $50 million from a dollars sales standpoint.

John

Kernan—Cowen and Company—Analyst

But the actual euro rate that’s embedded in your assumption is lower—? A

little bit lower?

Jonathan Ramsden—Abercrombie & Fitch Co.—EVP & CFO

It’s pretty close to the current spot rate.

|

|

|

| THOMSON REUTERS STREETEVENTS | www.streetevents.com | Contact Us

©2012 Thomson Reuters. All rights reserved. Republication or redistribution of

Thomson Reuters content, including by framing or similar means, is prohibited without the prior written consent of Thomson Reuters. ‘Thomson Reuters’ and the Thomson Reuters logo are registered trademarks of Thomson Reuters and its

affiliated companies. |

|

|

21

MAY 16, 2012 / 12:30PM, ANF—Q1 2012 Abercrombie & Fitch Co. Earnings Conference Call

John Kernan—Cowen and Company—Analyst

Okay, thank you.

Operator

Roxanne Meyer, UBS.

Roxanne Meyer—UBS—Analyst

A couple of questions for you actually. One, just wanted to know what the sequential progression was in terms of comp performance throughout the quarter.

Second, if you could give us a little bit more color about how Hollister performed in the US relative to how it did internationally. And then within the

international landscape, any thoughts of separating out performance of Hollister versus A&F in terms out how they’re feeling out the macro weakness and impact?

And then last just on cannibalization, I mean I guess I’m curious to know how you see the end game. For a store like London, which continues to feel the pressure from cannibalization, what is it

that’s going to get the sales to stabilize and turn it around and maybe even get it to comp positive again at some point?

Jonathan Ramsden—Abercrombie & Fitch Co.—EVP & CFO

I guess in terms of the sequential trend during the first quarter, Roxanne, it was complicated by a number of factors including the Easter shift, there

were some weather things going on. So I think it’s tough for us to really add a lot of color to that.

Clearly we’ve changed the

guidance from flat to down mid-single-digits based on what we’ve seen during the quarter. I’m not sure there’s a whole lot more detail we can really add. I’m not sure I fully understood the second part of the question. Can you

elaborate?

Roxanne Meyer—UBS—Analyst

Yes. Just looking for any color you can provide as to how Hollister performed in the US versus outside of the US.

Jonathan Ramsden—Abercrombie & Fitch Co.—EVP & CFO

I guess in the US A&F versus Hollister, A&F was a little stronger in the first quarter relative to where they’ve been in the fourth quarter

than Hollister.

Roxanne Meyer—UBS—Analyst

But what about comparing just Hollister to Hollister US versus internationally how it’s doing?

|

|

|

| THOMSON REUTERS STREETEVENTS | www.streetevents.com | Contact Us

©2012 Thomson Reuters. All rights reserved. Republication or redistribution of

Thomson Reuters content, including by framing or similar means, is prohibited without the prior written consent of Thomson Reuters. ‘Thomson Reuters’ and the Thomson Reuters logo are registered trademarks of Thomson Reuters and its

affiliated companies. |

|

|

22

MAY 16, 2012 / 12:30PM, ANF—Q1 2012 Abercrombie & Fitch Co. Earnings Conference Call

Jonathan Ramsden—Abercrombie & Fitch

Co.—EVP & CFO

I’m not sure that’s a terribly meaningful comparison. I think you’ve got to look at what

they’re trending against from prior periods. We don’t really look at it that way. We look at what’s going on in each of the geographies rather than comparing them across geographies. And I think it would be tough to draw any

conclusions from looking across geographies for any of the brands frankly.

Going to the third point, I think the single most important point

on London is that volume there is today still far ahead of the volume we signed up for the store on which is linked to hitting a 30% margin. So even after all of the cannibalization we’ve seen in London and the negative trend it’s still an

extremely healthy and profitable store. And I think that’s the single most important point about London, and it’s true of the other flagships too for the most part.

Roxanne Meyer—UBS—Analyst

Okay, great. Thanks a lot and best of

luck.

Operator

Erika

Maschmeyer, Robert W. Baird.

Unidentified Participant

(technical difficulty) on for Erika. Just if you could speak about the environment a little bit. Given your comments about pushing for AUR increases in the US for the balance of the year, what do you

expect other retailers to do with the cost benefits everyone should be seeing in the second half? And how fast could you react should the environment dictate declines in AUR?

Mike Jeffries—Abercrombie & Fitch Co.—Chairman & CEO

We are anticipating that we can raise our AURs. If we find that the competition is lowering prices progressively and that is affecting our business we can respond very quickly.

Unidentified Participant

Okay thank

you. And then a follow-up on Gilly Hicks, is that a sign of acceleration of that strategy and expansion internationally? And then can you talk about those recent store openings?

Mike Jeffries—Abercrombie & Fitch Co.—Chairman & CEO

Yes, I think everyone should take a look at them because they were a lot of fun last Saturday. Gilly performed very well within the first quarter on comps — [big] on a comp basis. We are still

learning a lot about the brand and the categories. And within the openings in Europe we have different formats. So I will not say that this is signaling that we are on a roll out mode with Gilly at this point, but we’re very happy with the

progress and continuing to learn a lot about the business.

Unidentified Participant

Great, thank you. I’ll hand it over.

|

|

|

| THOMSON REUTERS STREETEVENTS | www.streetevents.com | Contact Us

©2012 Thomson Reuters. All rights reserved. Republication or redistribution of

Thomson Reuters content, including by framing or similar means, is prohibited without the prior written consent of Thomson Reuters. ‘Thomson Reuters’ and the Thomson Reuters logo are registered trademarks of Thomson Reuters and its

affiliated companies. |

|

|

23

MAY 16, 2012 / 12:30PM, ANF—Q1 2012 Abercrombie & Fitch Co. Earnings Conference Call

Operator

And, ladies and gentlemen, due to time constraints this will conclude our question-and-answer session and this does conclude our conference call. Thank you for your participation. You may disconnect at

this time.

DISCLAIMER

Thomson Reuters reserves the right to make changes to documents, content, or other information on this web site without obligation to notify any person of

such changes.

In the conference calls upon which Event Transcripts are based, companies may make projections or other forward-looking

statements regarding a variety of items. Such forward-looking statements are based upon current expectations and involve risks and uncertainties. Actual results may differ materially from those stated in any forward-looking statement based on a

number of important factors and risks, which are more specifically identified in the companies’ most recent SEC filings. Although the companies may indicate and believe that the assumptions underlying the forward-looking statements are

reasonable, any of the assumptions could prove inaccurate or incorrect and, therefore, there can be no assurance that the results contemplated in the forward-looking statements will be realized.

THE INFORMATION CONTAINED IN EVENT TRANSCRIPTS IS A TEXTUAL REPRESENTATION OF THE APPLICABLE COMPANY’S CONFERENCE CALL AND WHILE EFFORTS ARE MADE TO

PROVIDE AN ACCURATE TRANSCRIPTION, THERE MAY BE MATERIAL ERRORS, OMISSIONS, OR INACCURACIES IN THE REPORTING OF THE SUBSTANCE OF THE CONFERENCE CALLS. IN NO WAY DOES THOMSON REUTERS OR THE APPLICABLE COMPANY ASSUME ANY RESPONSIBILITY FOR ANY

INVESTMENT OR OTHER DECISIONS MADE BASED UPON THE INFORMATION PROVIDED ON THIS WEB SITE OR IN ANY EVENT TRANSCRIPT. USERS ARE ADVISED TO REVIEW THE APPLICABLE COMPANY’S CONFERENCE CALL ITSELF AND THE APPLICABLE COMPANY’S SEC FILINGS BEFORE

MAKING ANY INVESTMENT OR OTHER DECISIONS.

©2012, Thomson Reuters. All Rights Reserved.

|

|

|

| THOMSON REUTERS STREETEVENTS | www.streetevents.com | Contact Us

©2012 Thomson Reuters. All rights reserved. Republication or redistribution of

Thomson Reuters content, including by framing or similar means, is prohibited without the prior written consent of Thomson Reuters. ‘Thomson Reuters’ and the Thomson Reuters logo are registered trademarks of Thomson Reuters and its

affiliated companies. |

|

|

24