Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

| x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Quarterly Period Ended June 30, 2012

or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number 1-11921

E*TRADE Financial Corporation

(Exact Name of Registrant as Specified in its Charter)

| Delaware | 94-2844166 | |

| (State or Other Jurisdiction of Incorporation or Organization) |

(I.R.S. Employer Identification Number) |

1271 Avenue of the Americas, 14th Floor, New York, New York 10020

(Address of Principal Executive Offices and Zip Code)

(646) 521-4300

(Registrant’s Telephone Number, including Area Code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer x |

Accelerated filer ¨ | |||||

| Non-accelerated filer ¨ (Do not check if a smaller reporting company) |

Smaller reporting company ¨ | |||||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date:

As of July 27, 2012, there were 285,740,705 shares of common stock outstanding.

Table of Contents

E*TRADE FINANCIAL CORPORATION

FORM 10-Q QUARTERLY REPORT

For the Quarter Ended June 30, 2012

Unless otherwise indicated, references to “the Company,” “we,” “us,” “our” and “E*TRADE” mean E*TRADE Financial Corporation and its subsidiaries.

E*TRADE, E*TRADE Financial, E*TRADE Bank, Equity Edge, OptionsLink and the Converging Arrows logo are registered trademarks of E*TRADE Financial Corporation in the United States and in other countries.

2

Table of Contents

FORWARD-LOOKING STATEMENTS

This report contains forward-looking statements involving risks and uncertainties. These statements relate to our future plans, objectives, expectations and intentions. These statements may be identified by the use of words such as “expect,” “may,” “anticipate,” “intend,” “plan” and similar expressions. Our actual results could differ materially from those discussed in these forward-looking statements, and we caution that we do not undertake to update these statements. Factors that could contribute to our actual results differing from any forward-looking statements include those discussed under Risk Factors, Management’s Discussion and Analysis of Financial Condition and Results of Operations and elsewhere in this report. The cautionary statements made in this report should be read as being applicable to all forward-looking statements wherever they appear in this report. We further caution that there may be risks associated with owning our securities other than those discussed in our filings. Important factors that may cause actual results to differ materially from any forward-looking statements are set forth in Item 1A. Risk Factors in the Annual Report on Form 10-K for the year ended December 31, 2011, and as updated in this report.

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following discussion should be read in conjunction with the consolidated financial statements and the related notes that appear elsewhere in this document and with the Annual Report on Form 10-K for the year ended December 31, 2011.

GLOSSARY OF TERMS

In analyzing and discussing our business, we utilize certain metrics, ratios and other terms that are defined in the Glossary of Terms, which is located at the end of Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

Strategy

Our core business is our trading and investing customer franchise. Building on the strengths of this franchise, our strategy is focused on:

| • | Strengthening our overall financial and franchise position. We are focused on achieving and maintaining an enterprise-wide risk culture and platform consistent with industry best-practices and top tier regulatory guidelines and expectations. We plan on strengthening our overall capital structure by deleveraging the balance sheet and reducing costs. |

| • | Improving our market position in our retail brokerage business. We plan to grow our customer base by continuing to focus on developing innovative products and services, investing in our sales force, and continuously enhancing the customer experience. |

| • | Capitalizing on the value of our complementary brokerage businesses. Our corporate services and market making businesses enhance our strategy by allowing us to realize additional economic benefit from our retail brokerage business. |

| • | Enhancing our position in retirement and investing. We believe growing our retirement and investing products and services is key to our long term success. Our primary focus is to expand the reach of our brand along with the awareness of our products to this key customer segment. |

| • | Continuing to manage and de-risk the Bank. We are focused on optimizing the value of customer deposits, while continuing to mitigate credit losses in our loan portfolio. Our near term priorities are de-risking, de-leveraging and strengthening our risk management function. In addition, we do not plan to offer new banking products to customers, including mortgages. |

3

Table of Contents

Key Factors Affecting Financial Performance

Our financial performance is affected by a number of factors outside of our control, including:

| • | customer demand for financial products and services; |

| • | weakness or strength of the residential real estate and credit markets; |

| • | performance, volume and volatility of the equity and capital markets; |

| • | customer perception of the financial strength of our franchise; |

| • | market demand and liquidity in the secondary market for mortgage loans and securities; |

| • | market demand and liquidity in the wholesale borrowings market, including securities sold under agreements to repurchase; |

| • | our ability to obtain regulatory approval to move capital from our bank to our parent company; and |

| • | changes to the rules and regulations governing the financial services industry. |

In addition to the items noted above, our success in the future will depend upon, among other things, our ability to:

| • | have continued success in the acquisition, growth and retention of brokerage customers; |

| • | generate meaningful growth in the retirement and investing customer group; |

| • | strengthen our risk management function; |

| • | reduce credit costs and the size of the balance sheet; |

| • | generate capital sufficient to meet our operating needs at both our bank and our parent company; |

| • | assess and manage interest rate risk; and |

| • | have disciplined expense control and improved operational efficiency. |

Management monitors a number of metrics in evaluating the Company’s performance. The most significant of these are shown in the table and discussed in the text below:

| As of or For the Three Months Ended June 30, |

Variance | As of or For the Six Months Ended June 30, |

Variance | |||||||||||||||||||||

| 2012 | 2011 | 2012 vs. 2011 | 2012 | 2011 | 2012 vs. 2011 | |||||||||||||||||||

| Customer Activity Metrics: |

||||||||||||||||||||||||

| DARTs |

138,653 | 147,908 | (6 | )% | 147,747 | 162,476 | (9 | )% | ||||||||||||||||

| Average commission per trade |

$ | 10.68 | $ | 11.14 | (4 | )% | $ | 10.87 | $ | 11.24 | (3 | )% | ||||||||||||

| Margin receivables (dollars in billions) |

$ | 5.8 | $ | 5.7 | 2 | % | $ | 5.8 | $ | 5.7 | 2 | % | ||||||||||||

| End of period brokerage accounts |

2,874,605 | 2,759,773 | 4 | % | 2,874,605 | 2,759,773 | 4 | % | ||||||||||||||||

| Net new brokerage accounts |

45,599 | 24,950 | * | 91,593 | 75,462 | * | ||||||||||||||||||

| Customer assets (dollars in billions) |

$ | 192.5 | $ | 185.6 | 4 | % | $ | 192.5 | $ | 185.6 | 4 | % | ||||||||||||

| Net new brokerage assets (dollars in billions) |

$ | 2.2 | $ | 1.5 | * | $ | 6.2 | $ | 5.4 | * | ||||||||||||||

| Brokerage related cash (dollars in billions) |

$ | 29.2 | $ | 26.3 | 11 | % | $ | 29.2 | $ | 26.3 | 11 | % | ||||||||||||

| Company Financial Metrics: |

||||||||||||||||||||||||

| Corporate cash (dollars in millions) |

$ | 436.5 | $ | 423.7 | 3 | % | $ | 436.5 | $ | 423.7 | 3 | % | ||||||||||||

| E*TRADE Financial Tier 1 leverage ratio |

5.7 | % | 5.4 | % | 0.3 | % | 5.7 | % | 5.4 | % | 0.3 | % | ||||||||||||

| E*TRADE Financial Tier 1 common ratio |

10.2 | % | 8.4 | % | 1.8 | % | 10.2 | % | 8.4 | % | 1.8 | % | ||||||||||||

| E*TRADE Bank Tier 1 leverage ratio(1) |

7.9 | % | 7.9 | % | 0.0 | % | 7.9 | % | 7.9 | % | 0.0 | % | ||||||||||||

| Special mention loan delinquencies (dollars in millions) |

$ | 349.5 | $ | 461.3 | (24 | )% | $ | 349.5 | $ | 461.3 | (24 | )% | ||||||||||||

| Allowance for loan losses (dollars in millions) |

$ | 525.8 | $ | 878.6 | (40 | )% | $ | 525.8 | $ | 878.6 | (40 | )% | ||||||||||||

| Enterprise net interest spread |

2.44 | % | 2.89 | % | (0.45 | )% | 2.47 | % | 2.87 | % | (0.40 | )% | ||||||||||||

| Enterprise interest-earning assets (average dollars in billions) |

$ | 44.8 | $ | 42.9 | 4 | % | $ | 44.8 | $ | 42.8 | 5 | % | ||||||||||||

| * | Percentage not meaningful. |

| (1) | The Company transitioned from reporting under the Office of Thrift Supervision (“OTS”) reporting requirements to reporting under the Office of the Comptroller of the Currency (“OCC”) reporting requirements in the first quarter of 2012. The Tier 1 leverage ratio is the OCC Tier 1 leverage ratio as of June 30, 2012 and the OTS Tier 1 capital ratio at June 30, 2011. The OTS Tier 1 capital ratio and OCC Tier 1 leverage ratio are both calculated in the same manner using adjusted total assets. |

4

Table of Contents

Customer Activity Metrics

| • | DARTs are the predominant driver of commissions revenue from our customers. |

| • | Average commission per trade is an indicator of changes in our customer mix, product mix and/or product pricing. |

| • | Margin receivables represent credit extended to customers to finance their purchases of securities by borrowing against securities they own. Margin receivables are a key driver of net operating interest income. |

| • | End of period brokerage accounts and net new brokerage accounts are indicators of our ability to attract and retain brokerage customers. |

| • | Changes in customer assets are an indicator of the value of our relationship with the customer. An increase in customer assets generally indicates that the use of our products and services by existing and new customers is expanding. Changes in this metric are also driven by changes in the valuations of our customers’ underlying securities. |

| • | Net new brokerage assets are total inflows to all new and existing brokerage accounts less total outflows from all closed and existing brokerage accounts and are a general indicator of the use of our products and services by existing and new brokerage customers. |

| • | Brokerage related cash is an indicator of a deepening engagement with our brokerage customers and is a key driver of net operating interest income. |

Company Financial Metrics

| • | Corporate cash is an indicator of the liquidity at the parent company. It is the primary source of capital above and beyond the capital deployed in our regulated subsidiaries. |

| • | E*TRADE Financial Tier 1 leverage ratio is Tier 1 capital divided by average total assets for the parent company for leverage capital purposes. E*TRADE Financial Tier 1 common ratio is Tier 1 capital less elements of Tier 1 capital that are not in the form of common equity, such as trust preferred securities, divided by total risk-weighted assets for the holding company. The Tier 1 leverage and Tier 1 common ratios are non-GAAP measures as the parent company is not yet held to these regulatory capital requirements and are indications of E*TRADE Financial’s capital adequacy. See Liquidity and Capital Resources for a reconciliation of these non-GAAP measures to the comparable GAAP measures. |

| • | E*TRADE Bank Tier 1 leverage ratio is Tier 1 capital divided by adjusted total assets for E*TRADE Bank and is an indication of E*TRADE Bank’s capital adequacy. |

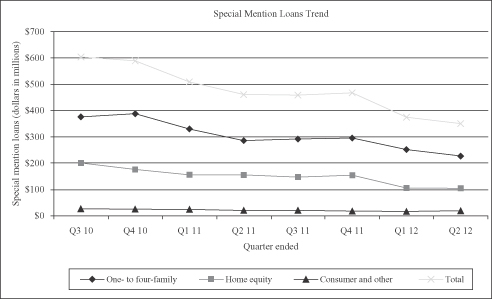

| • | Special mention loan delinquencies are loans 30-89 days past due and are an indicator of the expected trend for charge-offs in future periods as these loans have a greater propensity to migrate into nonaccrual status and ultimately charge-off. |

| • | Allowance for loan losses is an estimate of probable losses inherent in the loan portfolio as of the balance sheet date and is typically equal to management’s forecast of loan losses in the twelve months following the balance sheet date as well as the forecasted losses, including economic concessions to borrowers, over the estimated remaining life of loans modified as troubled debt restructurings (“TDR”). See Summary of Critical Accounting Policies and Estimates for a discussion of the estimates and assumptions used in the allowance for loan losses. |

| • | Enterprise interest-earning assets, in conjunction with our enterprise net interest spread, are indicators of our ability to generate net operating interest income. |

5

Table of Contents

Significant Events in the Second Quarter of 2012

Submission of Our Strategic and Capital Plan

| • | We submitted a long-term strategic and capital plan to the OCC and Federal Reserve, which included: our five-year business strategy; forecasts of our business results and capital ratios; capital distribution plans in current and adverse operating conditions; and internally developed stress tests. |

Enhancements to Our Trading and Investing Products and Services

| • | We enhanced our E*TRADE Pro platform by adding new tools including a trading ladder and strategy screeners and implemented changes to simplify the overall user experience on our customer website; |

| • | We continued to offer investor education with over 300,000 interactions during the quarter, comprising seminars, webinars and videos, both live and on-demand; and |

| • | We opened two new branches in Cupertino, California and New York, New York which increased our total network to 30 branches. |

We generated net income of $39.5 million and $102.1 million, or $0.14 and $0.35 per diluted share, on total net revenue of $452.4 million and $941.8 million for the three and six months ended June 30, 2012, respectively. Net operating interest income decreased 12% and 10% to $279.1 million and $564.0 million for the three and six months ended June 30, 2012, respectively, compared to the same periods in 2011, which was driven primarily by a decrease in enterprise net interest spread during the comparable periods. Commissions, fees and service charges, principal transactions and other revenue decreased 12% and 13% to $153.9 million and $327.1 million for the three and six months ended June 30, 2012, respectively, compared to the same periods in 2011, which was driven primarily by decreases in trading activity during the comparable periods. In addition, gains on loans and securities, net and net impairment decreased 31% and 7% to $19.4 million and $50.8 million for the three and six months ended June 30, 2012, respectively, compared to the same periods in 2011.

Provision for loan losses declined 35% and 36% to $67.3 million and $139.2 million for the three and six months ended June 30, 2012, respectively, compared to the same periods in 2011, driven primarily by improving credit trends and loan portfolio run-off. Total operating expenses decreased 3% to $281.5 million and decreased slightly to $587.7 million for the three and six months ended June 30, 2012, respectively, compared to the same periods in 2011. These decreases were driven primarily by decreases in clearing and servicing and other operating expenses offset by increases in compensation and benefits expense and FDIC insurance premiums for the three and six months ended June 30, 2012.

The following sections describe in detail the changes in key operating factors and other changes and events that affected net revenue, provision for loan losses, operating expense, other income (expense) and income tax expense.

6

Table of Contents

Revenue

The components of revenue and the resulting variances are as follows (dollars in millions):

| Three Months Ended June 30, |

Variance | Six Months Ended June 30, |

Variance | |||||||||||||||||||||||||||||

| 2012 vs. 2011 | 2012 vs. 2011 | |||||||||||||||||||||||||||||||

| 2012 | 2011 | Amount | % | 2012 | 2011 | Amount | % | |||||||||||||||||||||||||

| Net operating interest income |

$ | 279.1 | $ | 315.4 | $ | (36.3) | (12)% | $ | 564.0 | $ | 625.1 | $ | (61.1) | (10)% | ||||||||||||||||||

| Commissions |

93.3 | 103.8 | (10.5) | (10)% | 200.7 | 228.3 | (27.6) | (12)% | ||||||||||||||||||||||||

| Fees and service charges |

29.1 | 36.6 | (7.5) | (21)% | 61.1 | 73.9 | (12.8) | (17)% | ||||||||||||||||||||||||

| Principal transactions |

21.2 | 23.8 | (2.6) | (11)% | 45.4 | 53.3 | (7.9) | (15)% | ||||||||||||||||||||||||

| Gains on loans and securities, net |

24.7 | 31.0 | (6.3) | (20)% | 59.6 | 63.3 | (3.7) | (6)% | ||||||||||||||||||||||||

| Net impairment |

(5.3) | (2.9) | (2.4) | 83% | (8.8) | (8.9) | 0.1 | (2)% | ||||||||||||||||||||||||

| Other revenues |

10.3 | 9.9 | 0.4 | 4% | 19.8 | 19.3 | 0.5 | 3% | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

| Total non-interest income |

173.3 | 202.2 | (28.9) | (14)% | 377.8 | 429.2 | (51.4) | (12)% | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

| Total net revenue |

$ | 452.4 | $ | 517.6 | $ | (65.2) | (13)% | $ | 941.8 | $ | 1,054.3 | $ | (112.5) | (11)% | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

Net Operating Interest Income

Net operating interest income decreased 12% and 10% to $279.1 million and $564.0 million for the three and six months ended June 30, 2012, respectively, compared to the same periods in 2011. Net operating interest income is earned primarily through investing customer cash and deposits in enterprise interest-earning assets, which include: real estate loans, margin receivables, available-for-sale securities and held-to-maturity securities.

7

Table of Contents

The following tables present enterprise average balance sheet data and enterprise income and expense data for our operations, as well as the related net interest spread, yields and rates and have been prepared on the basis required by the SEC’s Industry Guide 3, “Statistical Disclosure by Bank Holding Companies” (dollars in millions):

| Three Months Ended June 30, | ||||||||||||||||||||||||

| 2012 | 2011 | |||||||||||||||||||||||

| Average Balance |

Operating Interest Inc./Exp. |

Average Yield/ Cost |

Average Balance |

Operating Interest Inc./Exp. |

Average Yield/ Cost |

|||||||||||||||||||

| Enterprise interest-earning assets: |

| |||||||||||||||||||||||

| Loans(1) |

$ | 12,324.6 | $ | 125.0 | 4.06 | % | $ | 15,030.0 | $ | 181.0 | 4.82 | % | ||||||||||||

| Margin receivables |

5,633.4 | 55.4 | 3.96 | % | 5,732.5 | 58.7 | 4.11 | % | ||||||||||||||||

| Available-for-sale securities |

16,336.1 | 98.6 | 2.41 | % | 15,428.2 | 107.0 | 2.78 | % | ||||||||||||||||

| Held-to-maturity securities |

8,108.5 | 60.3 | 2.97 | % | 3,950.3 | 32.9 | 3.34 | % | ||||||||||||||||

| Cash and equivalents |

1,115.7 | 0.5 | 0.19 | % | 1,489.2 | 0.8 | 0.20 | % | ||||||||||||||||

| Segregated cash |

741.8 | 0.1 | 0.06 | % | 638.6 | 0.2 | 0.09 | % | ||||||||||||||||

| Securities borrowed and other |

509.4 | 12.7 | 10.02 | % | 639.2 | 12.5 | 7.84 | % | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||||||

| Total enterprise interest-earning assets |

44,769.5 | 352.6 | 3.15 | % | 42,908.0 | 393.1 | 3.67 | % | ||||||||||||||||

|

|

|

|

|

|||||||||||||||||||||

| Non-operating interest-earning and non-interest earning assets(2) |

4,605.1 | 4,290.5 | ||||||||||||||||||||||

|

|

|

|

|

|||||||||||||||||||||

| Total assets |

$ | 49,374.6 | $ | 47,198.5 | ||||||||||||||||||||

|

|

|

|

|

|||||||||||||||||||||

| Three Months Ended June 30, | ||||||||||||||||||||||||

| 2012 | 2011 | |||||||||||||||||||||||

| Average Balance |

Operating Interest Inc./Exp. |

Average Yield/ Cost |

Average Balance |

Operating Interest Inc./Exp. |

Average Yield/ Cost |

|||||||||||||||||||

| Enterprise interest-bearing liabilities: |

| |||||||||||||||||||||||

| Deposits |

$ | 28,583.3 | 6.6 | 0.09 | % | $ | 26,091.5 | 11.8 | 0.18 | % | ||||||||||||||

| Customer payables |

5,303.4 | 2.9 | 0.22 | % | 5,489.3 | 2.1 | 0.16 | % | ||||||||||||||||

| Securities sold under agreements to repurchase |

4,802.8 | 40.5 | 3.33 | % | 5,369.1 | 38.0 | 2.80 | % | ||||||||||||||||

| Federal Home Loan Bank (“FHLB”) advances and other borrowings |

2,733.3 | 25.4 | 3.68 | % | 2,745.2 | 26.9 | 3.89 | % | ||||||||||||||||

| Securities loaned and other |

702.2 | 0.0 | 0.02 | % | 655.2 | 0.4 | 0.24 | % | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||||||

| Total enterprise interest-bearing liabilities |

42,125.0 | 75.4 | 0.71 | % | 40,350.3 | 79.2 | 0.78 | % | ||||||||||||||||

|

|

|

|

|

|||||||||||||||||||||

| Non-operating interest-bearing and non-interest bearing liabilities(3) |

2,197.2 | 2,208.5 | ||||||||||||||||||||||

|

|

|

|

|

|||||||||||||||||||||

| Total liabilities |

44,322.2 | 42,558.8 | ||||||||||||||||||||||

| Total shareholders’ equity |

5,052.4 | 4,639.7 | ||||||||||||||||||||||

|

|

|

|

|

|||||||||||||||||||||

| Total liabilities and shareholders’ equity |

$ | 49,374.6 | $ | 47,198.5 | ||||||||||||||||||||

|

|

|

|

|

|||||||||||||||||||||

| Excess of enterprise interest-earning assets over enterprise interest-bearing liabilities/Enterprise net interest income/Spread |

$ | 2,644.5 | $ | 277.2 | 2.44 | % | $ | 2,557.7 | $ | 313.9 | 2.89 | % | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||||||

| Enterprise net interest margin (net yield on enterprise interest-earning assets) |

|

2.48 | % | 2.93 | % | |||||||||||||||||||

| Ratio of enterprise interest-earning assets to enterprise interest-bearing liabilities |

|

106.28 | % | 106.34 | % | |||||||||||||||||||

| Return on average: |

||||||||||||||||||||||||

| Total assets |

0.32 | % | 0.40 | % | ||||||||||||||||||||

| Total shareholders’ equity |

3.13 | % | 4.06 | % | ||||||||||||||||||||

| Average equity to average total assets |

10.23 | % | 9.83 | % | ||||||||||||||||||||

Reconciliation from enterprise net interest income to net operating interest income (dollars in millions):

| Three Months Ended June 30, |

||||||||

| 2012 | 2011 | |||||||

| Enterprise net interest income |

$ | 277.2 | $ | 313.9 | ||||

| Taxable equivalent interest adjustment |

(0.3 | ) | (0.3 | ) | ||||

| Earnings on customer cash held by third parties and other(4) |

2.2 | 1.8 | ||||||

|

|

|

|

|

|||||

| Net operating interest income |

$ | 279.1 | $ | 315.4 | ||||

|

|

|

|

|

|||||

| (1) | Nonaccrual loans are included in the average loan balances. Interest payments received on nonaccrual loans are recognized on a cash basis in operating interest income until it is doubtful that full payment will be collected, at which point payments are applied to principal. |

| (2) | Non-operating interest-earning and non-interest earning assets consist of property and equipment, net, goodwill, other intangibles, net and other assets that do not generate operating interest income. Some of these assets generate corporate interest income. |

| (3) | Non-operating interest-bearing and non-interest bearing liabilities consist of corporate debt and other liabilities that do not generate operating interest expense. Some of these liabilities generate corporate interest expense. |

| (4) | Includes revenue earned on average customer assets of $3.6 billion and $3.7 billion for the three months ended June 30, 2012 and 2011, respectively, held by parties outside E*TRADE Financial, including third party money market funds and sweep deposit accounts at unaffiliated financial institutions. |

8

Table of Contents

| Six Months Ended June 30, | ||||||||||||||||||||||||

| 2012 | 2011 | |||||||||||||||||||||||

| Average Balance |

Operating Interest Inc./Exp. |

Average Yield/Cost |

Average Balance |

Operating Interest Inc./Exp. |

Average Yield/Cost |

|||||||||||||||||||

| Enterprise interest-earning assets: |

||||||||||||||||||||||||

| Loans(1) |

$ | 12,648.6 | $ | 264.5 | 4.18 | % | $ | 15,425.2 | $ | 367.3 | 4.76 | % | ||||||||||||

| Margin receivables |

5,245.4 | 103.4 | 3.96 | % | 5,588.7 | 115.0 | 4.15 | % | ||||||||||||||||

| Available-for-sale securities |

16,195.5 | 204.6 | 2.53 | % | 15,589.6 | 218.2 | 2.80 | % | ||||||||||||||||

| Held-to-maturity securities |

7,513.1 | 113.6 | 3.03 | % | 3,238.4 | 53.7 | 3.32 | % | ||||||||||||||||

| Cash and equivalents |

1,360.4 | 1.4 | 0.20 | % | 1,659.7 | 1.7 | 0.20 | % | ||||||||||||||||

| Segregated cash |

1,285.8 | 0.5 | 0.07 | % | 682.7 | 0.4 | 0.11 | % | ||||||||||||||||

| Securities borrowed and other |

581.2 | 25.3 | 8.77 | % | 641.5 | 22.3 | 7.00 | % | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total enterprise interest-earning assets |

44,830.0 | 713.3 | 3.19 | % | 42,825.8 | 778.6 | 3.64 | % | ||||||||||||||||

|

|

|

|

|

|||||||||||||||||||||

| Non-operating interest-earning and non-interest earning assets(2) |

4,522.9 | 4,381.0 | ||||||||||||||||||||||

|

|

|

|

|

|||||||||||||||||||||

| Total assets |

$ | 49,352.9 | $ | 47,206.8 | ||||||||||||||||||||

|

|

|

|

|

|||||||||||||||||||||

| Enterprise interest-bearing liabilities: |

||||||||||||||||||||||||

| Deposits |

$ | 28,255.6 | 15.0 | 0.11 | % | $ | 25,864.7 | 24.0 | 0.19 | % | ||||||||||||||

| Customer payables |

5,634.4 | 5.5 | 0.20 | % | 5,404.6 | 4.0 | 0.15 | % | ||||||||||||||||

| Securities sold under agreements to repurchase |

4,896.0 | 81.2 | 3.28 | % | 5,625.6 | 76.0 | 2.69 | % | ||||||||||||||||

| Federal Home Loan Bank (“FHLB”) advances and other borrowings |

2,732.7 | 50.8 | 3.68 | % | 2,748.7 | 52.2 | 3.78 | % | ||||||||||||||||

| Securities loaned and other |

645.4 | 0.2 | 0.06 | % | 670.0 | 0.7 | 0.22 | % | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||||||

| Total enterprise interest-bearing liabilities |

42,164.1 | 152.7 | 0.72 | % | 40,313.6 | 156.9 | 0.77 | % | ||||||||||||||||

|

|

|

|

|

|||||||||||||||||||||

| Non-operating interest-bearing and non-interest bearing liabilities(3) |

2,175.3 | 2,497.3 | ||||||||||||||||||||||

|

|

|

|

|

|||||||||||||||||||||

| Total liabilities |

44,339.4 | 42,810.9 | ||||||||||||||||||||||

| Total shareholders’ equity |

5,013.5 | 4,395.9 | ||||||||||||||||||||||

|

|

|

|

|

|||||||||||||||||||||

| Total liabilities and shareholders’ equity |

$ | 49,352.9 | $ | 47,206.8 | ||||||||||||||||||||

|

|

|

|

|

|||||||||||||||||||||

| Excess of enterprise interest-earning assets over enterprise interest-bearing liabilities/Enterprise net interest income/Spread |

$ | 2,665.9 | $ | 560.6 | 2.47 | % | $ | 2,512.2 | $ | 621.7 | 2.87 | % | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||||||

| Enterprise net interest margin (net yield on enterprise interest-earning assets) |

2.50 | % | 2.90 | % | ||||||||||||||||||||

| Ratio of enterprise interest-earning assets to enterprise interest-bearing liabilities |

106.32 | % | 106.23 | % | ||||||||||||||||||||

| Return on average: |

||||||||||||||||||||||||

| Total assets |

0.41 | % | 0.39 | % | ||||||||||||||||||||

| Total shareholders’ equity |

4.07 | % | 4.20 | % | ||||||||||||||||||||

| Average equity to average total assets |

10.16 | % | 9.31 | % | ||||||||||||||||||||

Reconciliation from enterprise net interest income to net operating interest income (dollars in millions):

| Six Months Ended June 30, |

||||||||

| 2012 | 2011 | |||||||

| Enterprise net interest income |

$ | 560.6 | $ | 621.7 | ||||

| Taxable equivalent interest adjustment |

(0.6 | ) | (0.6 | ) | ||||

| Earnings on customer cash held by third parties and other(4) |

4.0 | 4.0 | ||||||

|

|

|

|

|

|||||

| Net operating interest income |

$ | 564.0 | $ | 625.1 | ||||

|

|

|

|

|

|||||

| (1) | Nonaccrual loans are included in the average loan balances. Interest payments received on nonaccrual loans are recognized on a cash basis in operating interest income until it is doubtful that full payment will be collected, at which point payments are applied to principal. |

| (2) | Non-operating interest-earning and non-interest earning assets consist of property and equipment, net, goodwill, other intangibles, net and other assets that do not generate operating interest income. Some of these assets generate corporate interest income. |

| (3) | Non-operating interest-bearing and non-interest bearing liabilities consist of corporate debt and other liabilities that do not generate operating interest expense. Some of these liabilities generate corporate interest expense. |

| (4) | Includes revenue earned on average customer assets of $3.7 billion for both the six months ended June 30, 2012 and 2011, held by parties outside E*TRADE Financial, including third party money market funds and sweep deposit accounts at unaffiliated financial institutions. |

9

Table of Contents

The fluctuation in enterprise interest-earning assets is driven primarily by changes in enterprise interest-bearing liabilities, specifically customer cash and deposits. Average enterprise interest-earning assets increased 4% to $44.8 billion and 5% to $44.8 billion for the three and six months ended June 30, 2012, respectively, compared to the same periods in 2011. This was primarily a result of the increases in average segregated cash and average available-for-sale and held-to-maturity securities, offset by decreases in average loans and average margin receivables.

Average enterprise interest-bearing liabilities increased 4% to $42.1 billion and 5% to $42.2 billion for the three and six months ended June 30, 2012, respectively, compared to the same periods in 2011. The increase in average enterprise interest-bearing liabilities was due primarily to an increase in average deposits offset by a decrease in average securities sold under agreements to repurchase.

Enterprise net interest spread decreased by 45 basis points to 2.44% and by 40 basis points to 2.47% for the three and six months ended June 30, 2012, respectively, compared to the same periods in 2011, due primarily to lower yields on loans and the impact of the current interest rate environment, which remains challenging. We expect enterprise net interest spread to continue to decline during the remainder of 2012, averaging slightly above 2.40% for the full year; however, spread may fluctuate based on the size and mix of the balance sheet.

Commissions

Commissions revenue decreased 10% to $93.3 million and 12% to $200.7 million for the three and six months ended June 30, 2012, respectively, compared to the same periods in 2011. The main factors that affect commissions are DARTs, average commission per trade and the number of trading days during the period. Average commission per trade is impacted by customer mix and the different commission rates on various trade types (e.g. equities, options, fixed income, stock plan, exchange-traded funds, mutual funds, forex and cross border). Accordingly, changes in the mix of trade types will impact average commission per trade.

DART volume decreased 6% to 138,653 and 9% to 147,747 for the three and six months ended June 30, 2012, respectively, compared to the same periods in 2011. Option-related DARTs as a percentage of total DARTs represented 24% of trading volume for both the three and six months ended June 30, 2012, compared to 20% for the same periods in 2011. Exchange-traded funds-related DARTs as a percentage of total DARTs represented 9% and 8% of trading volume for the three and six months ended June 30, 2012, respectively, compared to 10% and 9% for the comparable periods in 2011.

Average commission per trade decreased 4% to $10.68 and 3% to $10.87 for the three and six months ended June 30, 2012, respectively, compared to the same periods in 2011. The decreases were driven primarily by changes in customer mix; specifically customers who have a higher commission per trade traded less during the three and six months ended June 30, 2012 compared to our active trader customers, who generally have lower commission per trade, when compared to the same periods in 2011.

10

Table of Contents

Fees and Service Charges

Fees and service charges decreased 21% to $29.1 million and 17% to $61.1 million for the three and six months ended June 30, 2012, respectively, compared to the same periods in 2011. The decrease was driven primarily by lower reorganization fee revenue related to a large public company reorganization in the second quarter of 2011 and by a decline in other fees and service charges due to decreased customer activity. The table below shows the components of fees and service charges and the resulting variances (dollars in millions):

| Three Months Ended June 30, |

Variance | Six Months Ended |

Variance | |||||||||||||||||||||||||||||

| 2012 vs. 2011 | 2012 vs. 2011 | |||||||||||||||||||||||||||||||

| 2012 | 2011 | Amount | % | 2012 | 2011 | Amount | % | |||||||||||||||||||||||||

| Order flow revenue |

$ | 13.2 | $ | 14.0 | $ | (0.8 | ) | (6 | )% | $ | 28.7 | $ | 30.8 | $ | (2.1 | ) | (7 | )% | ||||||||||||||

| Mutual fund service fees |

4.0 | 4.1 | (0.1 | ) | (2 | )% | 7.8 | 7.7 | 0.1 | 1 | % | |||||||||||||||||||||

| Foreign exchange revenue |

2.1 | 2.9 | (0.8 | ) | (28 | )% | 5.5 | 6.6 | (1.1 | ) | (17 | )% | ||||||||||||||||||||

| Reorganization fees |

2.0 | 6.6 | (4.6 | ) | (70 | )% | 3.6 | 9.5 | (5.9 | ) | (62 | )% | ||||||||||||||||||||

| Advisor management fees |

1.4 | 0.6 | 0.8 | 133 | % | 2.5 | 2.8 | (0.3 | ) | (11 | )% | |||||||||||||||||||||

| Other fees and service charges |

6.4 | 8.4 | (2.0 | ) | (24 | )% | 13.0 | 16.5 | (3.5 | ) | (21 | )% | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

| Total fees and service charges |

$ | 29.1 | $ | 36.6 | $ | (7.5 | ) | (21 | )% | $ | 61.1 | $ | 73.9 | $ | (12.8 | ) | (17 | )% | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

Principal Transactions

Principal transactions decreased 11% to $21.2 million and 15% to $45.4 million for the three and six months ended June 30, 2012, respectively, compared to the same periods in 2011. Principal transactions are derived from our market making business in which we act as a market-maker for our brokerage customers’ orders as well as orders from third party customers. The decrease in principal transactions revenue was driven primarily by a decrease in trading volume when compared to the same periods in 2011.

Gains on Loans and Securities, Net

Gains on loans and securities, net were $24.7 million and $59.6 million for the three and six months ended June 30, 2012 as shown in the following table (dollars in millions):

| Three Months Ended June 30, |

Variance | Six Months Ended |

Variance | |||||||||||||||||||||||||||||

| 2012 vs. 2011 | 2012 vs. 2011 | |||||||||||||||||||||||||||||||

| 2012 | 2011 | Amount | % | 2012 | 2011 | Amount | % | |||||||||||||||||||||||||

| Gains on loans, net |

$ | 0.2 | $ | 0.1 | $ | 0.1 | * | $ | 0.2 | $ | 0.1 | $ | 0.1 | * | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

| Gains on available-for-sale securities, net |

30.1 | 25.3 | 4.8 | 19 | % | 65.0 | 61.1 | 3.9 | 6 | % | ||||||||||||||||||||||

| Gains (losses) on trading securities, net |

(0.1 | ) | 0.3 | (0.4 | ) | * | (0.1 | ) | 0.9 | (1.0 | ) | * | ||||||||||||||||||||

| Hedge ineffectiveness |

(5.5 | ) | 5.3 | (10.8 | ) | * | (5.5 | ) | 1.2 | (6.7 | ) | * | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

| Gains on securities, net |

24.5 | 30.9 | (6.4 | ) | (21 | )% | 59.4 | 63.2 | (3.8 | ) | (6 | )% | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

| Gains on loans and securities, net |

$ | 24.7 | $ | 31.0 | $ | (6.3 | ) | (20 | )% | $ | 59.6 | $ | 63.3 | $ | (3.7 | ) | (6 | )% | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

| * | Percentage not meaningful. |

11

Table of Contents

Net Impairment

We recognized $5.3 million and $8.8 million of net impairment during the three and six months ended June 30, 2012, respectively, on certain securities in our non-agency CMO portfolio due to continued deterioration in the expected credit performance of the underlying loans in those specific securities. The gross other-than-temporary impairment (“OTTI”) and the noncredit portion of OTTI, which was or had been previously recorded through other comprehensive income, are shown in the table below (dollars in millions):

| Three Months Ended | Six Months Ended | |||||||||||||||

| June 30, | June 30, | |||||||||||||||

| 2012 | 2011 | 2012 | 2011 | |||||||||||||

| Other-than-temporary impairment (“OTTI”) |

$ | (1.4 | ) | $ | (2.0 | ) | $ | (14.1 | ) | $ | (6.9 | ) | ||||

| Less: noncredit portion of OTTI recognized into (out of) other comprehensive income (loss) (before tax) |

(3.9 | ) | (0.9 | ) | 5.3 | (2.0 | ) | |||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net impairment |

$ | (5.3 | ) | $ | (2.9 | ) | $ | (8.8 | ) | $ | (8.9 | ) | ||||

|

|

|

|

|

|

|

|

|

|||||||||

Provision for Loan Losses

Provision for loan losses decreased 35% to $67.3 million and 36% to $139.2 million for the three and six months ended June 30, 2012, respectively, compared to the same periods in 2011. The decrease in provision for loan losses was driven primarily by improving credit trends, as evidenced by the lower levels of delinquent loans in the one- to four-family and home equity loan portfolios, and loan portfolio run-off. The provision for loan losses has declined 87% from its peak of $517.8 million in the third quarter of 2008. We expect provision for loan losses to continue to decline over the long term, although it is subject to variability from quarter to quarter.

Operating Expense

The components of operating expense and the resulting variances are as follows (dollars in millions):

| Three Months Ended June 30, |

Variance | Six Months Ended June 30, |

Variance | |||||||||||||||||||||||||||||

| 2012 vs. 2011 | 2012 vs. 2011 | |||||||||||||||||||||||||||||||

| 2012 | 2011 | Amount | % | 2012 | 2011 | Amount | % | |||||||||||||||||||||||||

| Compensation and benefits |

$ | 85.6 | $ | 80.5 | $ | 5.1 | 6 | % | $ | 177.8 | $ | 164.5 | $ | 13.3 | 8 | % | ||||||||||||||||

| Clearing and servicing |

32.8 | 39.2 | (6.4 | ) | (16 | )% | 67.4 | 78.3 | (10.9 | ) | (14 | )% | ||||||||||||||||||||

| Advertising and market development |

36.6 | 37.0 | (0.4 | ) | (1 | )% | 84.1 | 81.4 | 2.7 | 3 | % | |||||||||||||||||||||

| FDIC insurance premiums |

27.2 | 24.0 | 3.2 | 13 | % | 55.6 | 44.6 | 11.0 | 25 | % | ||||||||||||||||||||||

| Professional services |

19.9 | 21.5 | (1.6 | ) | (7 | )% | 40.3 | 44.9 | (4.6 | ) | (10 | )% | ||||||||||||||||||||

| Occupancy and equipment |

18.2 | 17.2 | 1.0 | 6 | % | 36.1 | 34.0 | 2.1 | 6 | % | ||||||||||||||||||||||

| Communications |

18.4 | 17.2 | 1.2 | 7 | % | 37.5 | 32.8 | 4.7 | 14 | % | ||||||||||||||||||||||

| Depreciation and amortization |

23.1 | 22.7 | 0.4 | 2 | % | 45.3 | 44.8 | 0.5 | 1 | % | ||||||||||||||||||||||

| Amortization of other intangibles |

6.3 | 6.5 | (0.2 | ) | (4 | )% | 12.6 | 13.1 | (0.5 | ) | (4 | )% | ||||||||||||||||||||

| Facility restructuring and other exit activities |

1.6 | 2.1 | (0.5 | ) | * | 1.2 | 5.6 | (4.4 | ) | * | ||||||||||||||||||||||

| Other operating expenses |

11.8 | 23.0 | (11.2 | ) | (49 | )% | 29.8 | 44.9 | (15.1 | ) | (34 | )% | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

| Total operating expense |

$ | 281.5 | $ | 290.9 | $ | (9.4 | ) | (3 | )% | $ | 587.7 | $ | 588.9 | $ | (1.2 | ) | (0 | )% | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

| * | Percentage not meaningful. |

Compensation and Benefits

Compensation and benefits increased 6% to $85.6 million and 8% to $177.8 million for the three and six months ended June 30, 2012, respectively, compared to the same periods in 2011. The increase resulted primarily from higher compensation expense as a result of a 3% increase in the employee base from June 30, 2011 to June 30, 2012.

12

Table of Contents

Clearing and Servicing

Clearing and servicing decreased 16% to $32.8 million and 14% to $67.4 million for the three and six months ended June 30, 2012, respectively, compared to the same periods in 2011. These decreases resulted primarily from lower trading volumes and lower loan balances compared to the same periods in 2011.

FDIC Insurance Premiums

FDIC insurance premiums increased 13% to $27.2 million and 25% to $55.6 million for the three and six months ended June 30, 2012, respectively, compared to the same periods in 2011. The increases were due primarily to an industry wide change in the FDIC insurance premium assessment calculation, effective in the second quarter of 2011. The three and six months ended June 30, 2011 did not include approximately $6 million of FDIC insurance premium related to the new assessment calculation as it was not finalized and recorded until the third quarter of 2011.

Professional Services

Professional services decreased 7% to $19.9 million and 10% to $40.3 million for the three and six months ended June 30, 2012, respectively, compared to the same periods in 2011. The decreases were driven primarily by declines in legal expenses compared to the same periods in 2011.

Communications

Communications expense increased 7% to $18.4 million and 14% to $37.5 million for the three and six months ended June 30, 2012, respectively, compared to the same periods in 2011. This was driven primarily by increases in vendor service fees compared to the same periods in 2011.

Other Operating Expenses

Other operating expenses decreased 49% to $11.8 million and 34% to $29.8 million for the three and six months ended June 30, 2012, respectively, compared to the same periods in 2011. The decrease was driven by a $10.2 million benefit during the second quarter of 2012 related to our offer to purchase auction rate securities from eligible holders. The costs of this program, which expired on May 15, 2012, were approximately $10.2 million less than our previous estimate.

Other Income (Expense)

Other income (expense) increased 5% to $43.2 million and 4% to $88.4 million for the three and six months ended June 30, 2012, respectively, compared to the same periods in 2011 as shown in the following table (dollars in millions):

| Three Months Ended June 30, |

Variance | Six Months Ended June 30, |

Variance | |||||||||||||||||||||||||||||

| 2012 vs. 2011 | 2012 vs. 2011 | |||||||||||||||||||||||||||||||

| 2012 | 2011 | Amount | % | 2012 | 2011 | Amount | % | |||||||||||||||||||||||||

| Corporate interest income |

$ | — | $ | 0.1 | $ | (0.1 | ) | * | $ | — | $ | 0.7 | $ | (0.7 | ) | * | ||||||||||||||||

| Corporate interest expense |

(45.3 | ) | (44.8 | ) | (0.5 | ) | 1 | % | (90.4 | ) | (88.1 | ) | (2.3 | ) | 3 | % | ||||||||||||||||

| Gains on early extinguishment of debt |

— | 3.1 | (3.1 | ) | * | — | 3.1 | (3.1 | ) | * | ||||||||||||||||||||||

| Equity in income (loss) of investments and venture funds |

2.1 | 0.6 | 1.5 | * | 2.0 | (0.3 | ) | 2.3 | * | |||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

| Total other income (expense) |

$ | (43.2 | ) | $ | (41.0 | ) | $ | (2.2 | ) | 5 | % | $ | (88.4 | ) | $ | (84.6 | ) | $ | (3.8 | ) | 4 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

| * | Percentage not meaningful. |

13

Table of Contents

Total other income (expense) primarily consisted of corporate interest expense on interest-bearing corporate debt for the three and six months ended June 30, 2012. Corporate interest expense increased 1% and 3% to $45.3 million and $90.4 million for the three and six months ended June 30, 2012, respectively, compared to the same periods in 2011. In addition to the stated interest on corporate debt, the corporate interest expense line item included the benefit of discontinued fair value hedges on corporate debt, which decreased $0.8 million and $2.2 million for the three and six months ended June 30, 2012, respectively, compared to the same periods in 2011. Offsetting interest expense for the three and six months ended June 30, 2011 was a $3.1 million gain on early extinguishment of debt related to the call of the 7 3/8% Notes due September 2013 in the second quarter of 2011.

Income Tax Expense

For the three months ended June 30, 2012, income tax expense and the effective tax rate were $21.0 million and 34.7%, compared to $35.5 million and 43.0%, respectively for the same period in 2011. For the six months ended June 30, 2012, income tax expense and the effective tax rate were $24.4 million and 19.3%, compared to $69.2 million and 42.8%, respectively for the same period in 2011.

During the first quarter of 2012, we recorded an income tax benefit of $26.3 million related to certain losses on the 2009 Debt Exchange that were previously considered non-deductible. Through additional research completed in the first quarter of 2012, we identified that a portion of those losses were incorrectly treated as non-deductible in 2009 and were deductible for tax purposes. The $26.3 million tax benefit resulted in a corresponding increase to the deferred tax assets, which were $1.5 billion as of June 30, 2012. Without this benefit, our effective tax rate for the six months ended June 30, 2012 would have been 40.1%, calculated as follows (dollars in thousands):

| Pre-tax Income |

Tax Expense (Benefit) |

Tax Rate | ||||||||||

| Tax rate before tax benefit |

$ | 126,534 | $ | 50,717 | 40.1 | % | ||||||

| Income tax benefit related to certain losses on the 2009 Debt Exchange |

— | (26,284 | ) | N/A | ||||||||

|

|

|

|

|

|||||||||

| Total as reported |

$ | 126,534 | $ | 24,433 | 19.3 | % | ||||||

|

|

|

|

|

|||||||||

In addition, the three and six months ended June 30, 2012 included a benefit of $6.7 million, primarily related to state tax credits generated from software development.

Valuation Allowance

We are required to establish a valuation allowance for deferred tax assets and record a charge to income if we determine, based on available evidence at the time the determination is made, that it is more likely than not that some portion or all of the deferred tax assets will not be realized. If we did conclude that a valuation allowance was required, the resulting loss could have a material adverse effect on our financial condition and results of operations.

We did not establish any valuation allowance against federal deferred tax assets as of June 30, 2012 as we believe that it is more likely than not that all of these assets will be realized. We continue to maintain a valuation allowance for certain of our state, foreign country and charitable contribution deferred tax assets as it is more likely than not that they will not be realized.

Tax Ownership Change

During the third quarter of 2009, we exchanged $1.7 billion principal amount of interest-bearing debt for an equal principal amount of non-interest-bearing convertible debentures. Subsequent to the Debt Exchange, $592.3 million and $128.7 million debentures were converted into 57.2 million and 12.5 million shares of common stock during the third and fourth quarters of 2009, respectively. As a result of these conversions, we believe we experienced a tax ownership change during the third quarter of 2009.

14

Table of Contents

As of the date of the ownership change, we had federal net operating losses (“NOLs”) available to carry forward of approximately $1.4 billion. Section 382 imposes an annual limitation on the amount of post-ownership change taxable income a corporation may offset with pre-ownership change NOLs. We believe the tax ownership change will extend the period of time it will take to fully utilize our pre-ownership change NOLs, but will not limit the total amount of pre-ownership change NOLs we can utilize. Our updated estimate is that we will be subject to an overall annual limitation on the use of our pre-ownership change NOLs of approximately $194 million. The overall pre-ownership change NOLs, which were approximately $1.4 billion, have a statutory carry forward period of 20 years (the majority of which expire in 16 years). As a result, we believe we will be able to fully utilize these NOLs in future periods.

Our ability to utilize the pre-ownership change NOLs is dependent on our ability to generate sufficient taxable income over the duration of the carry forward periods and will not be impacted by our ability or inability to generate taxable income in an individual year.

We report operating results in two segments: 1) trading and investing; and 2) balance sheet management. Trading and investing includes retail brokerage products and services; investor-focused banking products; market making; and corporate services. Balance sheet management includes the management of asset allocation; loans previously originated by the Company or purchased from third parties; customer cash and deposits; and credit, liquidity and interest rate risk for the Company as described in the Risk Management section. Costs associated with certain functions that are centrally-managed are separately reported in a corporate/other category.

Trading and Investing

The following table summarizes trading and investing financial information and key metrics as of and for the three and six months ended June 30, 2012 and 2011 (dollars in millions, except for key metrics):

| Three Months Ended June 30, |

Variance | Six Months Ended June 30, |

Variance | |||||||||||||||||||||||||||||

| 2012 vs. 2011 | 2012 vs. 2011 | |||||||||||||||||||||||||||||||

| 2012 | 2011 | Amount | % | 2012 | 2011 | Amount | % | |||||||||||||||||||||||||

| Net operating interest income |

$ | 165.2 | $ | 191.8 | $ | (26.6 | ) | (14 | )% | $ | 335.7 | $ | 380.6 | $ | (44.9 | ) | (12 | )% | ||||||||||||||

| Commissions |

93.3 | 103.8 | (10.5 | ) | (10 | )% | 200.7 | 228.3 | (27.6 | ) | (12 | )% | ||||||||||||||||||||

| Fees and service charges |

28.4 | 35.8 | (7.4 | ) | (21 | )% | 59.4 | 71.9 | (12.5 | ) | (18 | )% | ||||||||||||||||||||

| Principal transactions |

21.2 | 23.8 | (2.6 | ) | (11 | )% | 45.4 | 53.3 | (7.9 | ) | (15 | )% | ||||||||||||||||||||

| Other revenues |

8.8 | 7.7 | 1.1 | 14 | % | 16.6 | 15.8 | 0.8 | 5 | % | ||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

| Total net revenue |

316.9 | 362.9 | (46.0 | ) | (13 | )% | 657.8 | 749.9 | (92.1 | ) | (12 | )% | ||||||||||||||||||||

| Total operating expense |

188.1 | 192.6 | (4.5 | ) | (2 | )% | 399.7 | 395.2 | 4.5 | 1 | % | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

| Trading and investing income |

$ | 128.8 | $ | 170.3 | $ | (41.5 | ) | (24 | )% | $ | 258.1 | $ | 354.7 | $ | (96.6 | ) | (27 | )% | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

| Key Metrics: |

||||||||||||||||||||||||||||||||

| DARTs |

138,653 | 147,908 | (9,255 | ) | (6 | )% | 147,747 | 162,476 | (14,729 | ) | (9 | )% | ||||||||||||||||||||

| Average commission per trade |

$ | 10.68 | $ | 11.14 | $ | (0.46 | ) | (4 | )% | $ | 10.87 | $ | 11.24 | $ | (0.37 | ) | (3 | )% | ||||||||||||||

| Margin receivables (dollars in billions) |

$ | 5.8 | $ | 5.7 | $ | 0.1 | 2 | % | $ | 5.8 | $ | 5.7 | $ | 0.1 | 2 | % | ||||||||||||||||

| End of period brokerage accounts |

2,874,605 | 2,759,773 | 114,832 | 4 | % | 2,874,605 | 2,759,773 | 114,832 | 4 | % | ||||||||||||||||||||||

| Net new brokerage accounts |

45,599 | 24,950 | 20,649 | * | 91,593 | 75,462 | 16,131 | * | ||||||||||||||||||||||||

| Customer assets (dollars in billions) |

$ | 192.5 | $ | 185.6 | $ | 6.9 | 4 | % | $ | 192.5 | $ | 185.6 | $ | 6.9 | 4 | % | ||||||||||||||||

| Net new brokerage assets (dollars in billions) |

$ | 2.2 | $ | 1.5 | $ | 0.7 | * | $ | 6.2 | $ | 5.4 | $ | 0.8 | * | ||||||||||||||||||

| Brokerage related cash (dollars in billions) |

$ | 29.2 | $ | 26.3 | $ | 2.9 | 11 | % | $ | 29.2 | $ | 26.3 | $ | 2.9 | 11 | % | ||||||||||||||||

| * | Percentage not meaningful. |

15

Table of Contents

The trading and investing segment offers products and services to individual retail investors, generating revenue from these brokerage and banking relationships and from market making and corporate services activities. This segment generates five main sources of revenue: net operating interest income; commissions; fees and service charges; principal transactions; and other revenues. Net operating interest income is generated primarily from margin receivables and from a deposit transfer pricing arrangement with the balance sheet management segment. The balance sheet management segment utilizes the vast majority of customer cash and deposits and compensates the trading and investing segment via a market-based transfer pricing arrangement. This compensation is reflected in segment results as operating interest income for the trading and investing segment and operating interest expense for the balance sheet management segment and is eliminated in consolidation. Customer cash and deposits utilized by the balance sheet management segment include retail deposits and customer payables. Other revenues include results from providing software and services for managing equity compensation plans from corporate customers, as we ultimately service retail investors through these corporate relationships.

Trading and investing income decreased 24% to $128.8 million and 27% to $258.1 million for the three and six months ended June 30, 2012, respectively, compared to the same periods in 2011. We continued to generate net new brokerage accounts, ending the quarter with 2.9 million accounts. Our brokerage related cash, which is one of our most profitable sources of funding, increased by $2.9 billion when compared to the same period in 2011.

Trading and investing commissions decreased by 10% to $93.3 million and 12% to $200.7 million for the three and six months ended June 30, 2012, respectively, compared to the same periods in 2011. These decreases in commissions were primarily the result of a decrease in DARTs of 6% to 138,653 and 9% to 147,747 for the three and six months ended June 30, 2012, respectively, compared to the same periods in 2011.

Trading and investing fees and service charges decreased 21% to $28.4 million and 18% to $59.4 million for the three and six months ended June 30, 2012, respectively, compared to the same periods in 2011. These decreases for the three and six months ended June 30, 2012 were driven by decreases in order flow revenue, reorganization fee revenue and foreign exchange fee revenue compared to the same periods in 2011.

Trading and investing principal transactions decreased 11% to $21.2 million and 15% to $45.4 million for the three and six months ended June 30, 2012, respectively, compared to the same periods in 2011. The decreases in principal transactions revenue were driven primarily by decreases in trading volume when compared to the same periods in 2011.

Trading and investing operating expense decreased 2% to $188.1 million and increased 1% to $399.7 million for the three and six months ended June 30, 2012, respectively, compared to the same periods in 2011. The decrease during the three months ended June 30, 2012 was driven by a $10.2 million benefit related to our offer to purchase auction rate securities from eligible holders which expired on May 15, 2012. The increase for the six months ended June 30, 2012 was driven primarily by an increase in compensation and benefits expense resulting from an increase in the employee base from June 30, 2011 to June 30, 2012, which was mostly offset by the $10.2 million benefit discussed above.

As of June 30, 2012, we had approximately 2.9 million brokerage accounts, 1.1 million stock plan accounts and 0.4 million banking accounts. For the three months ended June 30, 2012 and 2011, our brokerage products contributed 70% and 68%, respectively, and our banking products contributed 30% and 32%, respectively, of total trading and investing net revenue. For the six months ended June 30, 2012 and 2011, our brokerage products contributed 69% and 70%, respectively, and our banking products contributed 31% and 30%, respectively, of total trading and investing net revenue.

16

Table of Contents

Balance Sheet Management

The following table summarizes balance sheet management financial information and key metrics as of and for the three and six months ended June 30, 2012 and 2011 (dollars in millions):

| Three Months

Ended June 30, |

Variance | Six Months

Ended June 30, |

Variance | |||||||||||||||||||||||||||||

| 2012 vs. 2011 | 2012 vs. 2011 | |||||||||||||||||||||||||||||||

| 2012 | 2011 | Amount | % | 2012 | 2011 | Amount | % | |||||||||||||||||||||||||

| Net operating interest income |

$ | 113.9 | $ | 123.7 | $ | (9.8 | ) | (8 | )% | $ | 228.3 | $ | 244.5 | $ | (16.2 | ) | (7 | )% | ||||||||||||||

| Fees and service charges |

0.7 | 0.8 | (0.1 | ) | (16 | )% | 1.7 | 1.9 | (0.2 | ) | (10 | )% | ||||||||||||||||||||

| Gains on loans and securities, net |

24.8 | 31.4 | (6.6 | ) | (21 | )% | 59.8 | 63.6 | (3.8 | ) | (6 | )% | ||||||||||||||||||||

| Net impairment |

(5.3 | ) | (2.9 | ) | (2.4 | ) | 83 | % | (8.8 | ) | (8.9 | ) | 0.1 | (2 | )% | |||||||||||||||||

| Other revenues |

1.4 | 1.8 | (0.4 | ) | (23 | )% | 3.0 | 3.3 | (0.3 | ) | (9 | )% | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

| Total net revenue |

135.5 | 154.8 | (19.3 | ) | (12 | )% | 284.0 | 304.4 | (20.4 | ) | (7 | )% | ||||||||||||||||||||

| Provision for loan losses |

67.3 | 103.1 | (35.8 | ) | (35 | )% | 139.2 | 219.2 | (80.0 | ) | (36 | )% | ||||||||||||||||||||

| Total operating expense |

56.6 | 58.3 | (1.7 | ) | (3 | )% | 115.2 | 111.7 | 3.5 | 3 | % | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

| Balance sheet management income (loss) |

$ | 11.6 | $ | (6.6 | ) | $ | 18.2 | * | $ | 29.6 | $ | (26.5 | ) | $ | 56.1 | * | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

| Key Metrics: |

||||||||||||||||||||||||||||||||

| Special mention loan delinquencies |

$ | 349.5 | $ | 461.3 | $ | (111.8 | ) | (24 | )% | $ | 349.5 | $ | 461.3 | $ | (111.8 | ) | (24 | )% | ||||||||||||||

| Allowance for loan losses |

$ | 525.8 | $ | 878.6 | $ | (352.8 | ) | (40 | )% | $ | 525.8 | $ | 878.6 | $ | (352.8 | ) | (40 | )% | ||||||||||||||

| Allowance for loan losses as a % of gross loans receivable |

4.47 | % | 6.04 | % | * | (1.57 | )% | 4.47 | % | 6.04 | % | * | (1.57 | )% | ||||||||||||||||||

| * | Percentage not meaningful. |

The balance sheet management segment generates revenue from managing loans previously originated by the Company or purchased from third parties, as well as utilizing customer cash and deposits to generate additional net operating interest income. The balance sheet management segment utilizes customer cash and deposits from the trading and investing segment, wholesale borrowings and proceeds from loan pay-downs to invest in available-for-sale and held-to-maturity securities. Net operating interest income is generated from interest earned on available-for-sale and held-to-maturity securities and loans receivable, net of interest paid on wholesale borrowings and on a deposit transfer pricing arrangement with the trading and investing segment. The balance sheet management segment utilizes the vast majority of customer cash and deposits and compensates the trading and investing segment via a market-based transfer pricing arrangement. This compensation is reflected in segment results as operating interest income for the trading and investing segment and operating interest expense for the balance sheet management segment and is eliminated in consolidation. Customer cash and deposits utilized by the balance sheet management segment include retail deposits and customer payables.

The balance sheet management segment reported income of $11.6 million and $29.6 million for the three and six months ended June 30, 2012. The balance sheet management income was due primarily to a decrease in provision for loan losses of 35% to $67.3 million and 36% to $139.2 million for the three and six months ended June 30, 2012, respectively.

Gains on loans and securities, net were $24.8 million and $59.8 million for the three and six months ended June 30, 2012, respectively, compared to $31.4 million and $63.6 million for the same periods in 2011 due to gains on the sale of certain agency mortgage-backed securities and agency debentures.

We recognized $5.3 million and $8.8 million of net impairment during the three and six months ended June 30, 2012, respectively, on certain securities in the non-agency CMO portfolio due to continued deterioration in the expected credit performance of the underlying loans in those specific securities. The net impairment

17

Table of Contents

included gross OTTI of $1.4 million and $14.1 million for the three and six months ended June 30, 2012, respectively. The amount that had been previously recorded through other comprehensive income and was reclassified into earnings during the three months ended June 30, 2012 was $3.9 million. For the six months ended June 30, 2012, $5.3 million related to the noncredit portion of OTTI, which was recorded through other comprehensive income.

Provision for loan losses decreased 35% to $67.3 million and 36% to $139.2 million for the three and six months ended June 30, 2012, respectively, compared to the same periods in 2011. The decreases in provision for loan losses were driven primarily by improving credit trends, as evidenced by the lower levels of delinquent loans in the one- to four- family and home equity loan portfolios, and loan portfolio run-off.

Total balance sheet management operating expense decreased 3% to $56.6 million and increased 3% to $115.2 million for the three and six months ended June 30, 2012, respectively, compared to the same periods in 2011. The decrease in operating expense for the three months ended June 30, 2012 resulted primarily from lower clearing and servicing expense due to lower loan balances compared to the same period in 2011. The increase in operating expense for the six months ended June 30, 2012 was due primarily to increased FDIC insurance premiums as a result of an industry wide change in the FDIC insurance premium assessment calculation, effective in the second quarter of 2011, partially offset by lower clearing and servicing expense due to lower loan balances.

Corporate/Other

The following table summarizes corporate/other financial information for the three and six months ended June 30, 2012 and 2011 (dollars in millions):

| Three Months Ended June 30, |

Variance | Six Months Ended June 30, |

Variance | |||||||||||||||||||||||||||||

| 2012 vs. 2011 | 2012 vs. 2011 | |||||||||||||||||||||||||||||||

| 2012 | 2011 | Amount | % | 2012 | 2011 | Amount | % | |||||||||||||||||||||||||

| Total net revenue |

$ | — | $ | — | $ | — | * | $ | — | $ | — | $ | — | * | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

| Compensation and benefits |

16.4 | 17.3 | (0.9 | ) | (5 | )% | 34.8 | 35.0 | (0.2 | ) | (1 | )% | ||||||||||||||||||||

| Professional services |

8.0 | 8.0 | — | * | 15.2 | 17.5 | (2.3 | ) | (13 | )% | ||||||||||||||||||||||

| Occupancy and equipment |

1.3 | 0.8 | 0.5 | 62 | % | 2.2 | 1.8 | 0.4 | 24 | % | ||||||||||||||||||||||

| Communications |

0.4 | 0.4 | — | * | 0.8 | 0.7 | 0.1 | 22 | % | |||||||||||||||||||||||

| Depreciation and amortization |

4.0 | 4.7 | (0.7 | ) | (15 | )% | 8.3 | 9.4 | (1.1 | ) | (12 | )% | ||||||||||||||||||||

| Facility restructuring and |

||||||||||||||||||||||||||||||||

| other exit activities |

1.6 | 2.1 | (0.5 | ) | * | 1.2 | 5.6 | (4.4 | ) | * | ||||||||||||||||||||||

| Other operating expenses |

5.0 | 6.8 | (1.8 | ) | (26 | )% | 10.3 | 12.0 | (1.7 | ) | (14 | )% | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

| Total operating expense |

36.7 | 40.1 | (3.4 | ) | (8 | )% | 72.8 | 82.0 | (9.2 | ) | (11 | )% | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

| Operating loss |

(36.7 | ) | (40.1 | ) | 3.4 | (8 | )% | (72.8 | ) | (82.0 | ) | 9.2 | (11 | )% | ||||||||||||||||||

| Total other income (expense) |

(43.2 | ) | (41.0 | ) | (2.2 | ) | 5 | % | (88.4 | ) | (84.6 | ) | (3.8 | ) | 4 | % | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

| Corporate/other loss |

$ | (79.9 | ) | $ | (81.1 | ) | $ | 1.2 | (1 | )% | $ | (161.2 | ) | $ | (166.6 | ) | $ | 5.4 | (3 | )% | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

| * | Percentage not meaningful. |

The corporate/other category includes costs that are centrally-managed, technology related costs incurred to support centrally-managed functions, restructuring and other exit activities, corporate debt and corporate investments.

The corporate/other loss before income taxes was $79.9 million and $161.2 million for the three and six months ended June 30, 2012, compared to $81.1 million and $166.6 million, respectively, for the same periods in 2011. For the six months ended June 30, 2012, the decrease in the loss was due primarily to restructuring activities for the six months ended June 30, 2011, for which there were not similar activities in the current period.

18

Table of Contents

Total other income (expense) primarily consisted of corporate interest expense on interest-bearing corporate debt for the three and six months ended June 30, 2012. Corporate interest expense increased 1% to $45.3 million and 3% to $90.4 million for the three and six months ended June 30, 2012, respectively, compared to the same periods in 2011. In addition to the stated interest on corporate debt, the corporate interest expense line item included the benefit of discontinued fair value hedges on corporate debt, which decreased $0.8 million and $2.2 million, respectively, for the three and six months ended June 30, 2012 compared to the same periods in 2011. Offsetting interest expense for the three and six months ended June 30, 2011 was a $3.1 million gain on early extinguishment of debt related to the call of the 7 3/8% Notes due September 2013 in the second quarter of 2011.

The following table sets forth the significant components of the consolidated balance sheet (dollars in millions):

| Variance | ||||||||||||||||

| June

30, 2012 |

December

31, 2011 |

2012 vs. 2011 | ||||||||||||||

| Amount | % | |||||||||||||||

| Assets: |

||||||||||||||||

| Cash and equivalents |

$ | 1,378.5 | $ | 2,099.8 | $ | (721.3 | ) | (34 | )% | |||||||

| Segregated cash |

761.5 | 1,275.6 | (514.1 | ) | (40 | )% | ||||||||||

| Securities(1) |

24,646.5 | 21,785.4 | 2,861.1 | 13 | % | |||||||||||

| Margin receivables |

5,804.3 | 4,826.3 | 978.0 | 20 | % | |||||||||||

| Loans receivable, net |

11,225.8 | 12,332.8 | (1,107.0 | ) | (9 | )% | ||||||||||

| Investment in FHLB stock |

131.5 | 140.2 | (8.7 | ) | (6 | )% | ||||||||||

|

Other(2) |

5,207.7 | 5,480.4 | (272.7 | ) | (5 | )% | ||||||||||

|

|

|

|

|

|

|

|||||||||||

| Total assets |

$ | 49,155.8 | $ | 47,940.5 | $ | 1,215.3 | 3 | % | ||||||||

|

|

|

|

|

|

|

|||||||||||

| Liabilities and shareholders’ equity: |

||||||||||||||||

| Deposits |

$ | 27,911.1 | $ | 26,460.0 | $ | 1,451.1 | 5 | % | ||||||||

| Wholesale borrowings(3) |

7,459.0 | 7,752.4 | (293.4 | ) | (4 | )% | ||||||||||

| Customer payables |

5,128.7 | 5,590.9 | (462.2 | ) | (8 | )% | ||||||||||

| Corporate debt |

1,501.3 | 1,493.5 | 7.8 | 1 | % | |||||||||||

| Other liabilities |

2,076.1 | 1,715.7 | 360.4 | 21 | % | |||||||||||

|

|

|

|

|

|

|

|||||||||||

| Total liabilities |

44,076.2 | 43,012.5 | 1,063.7 | 2 | % | |||||||||||

| Shareholders’ equity |

5,079.6 | 4,928.0 | 151.6 | 3 | % | |||||||||||

|

|

|

|

|

|

|

|||||||||||

| Total liabilities and shareholders’ equity |

$ | 49,155.8 | $ | 47,940.5 | $ | 1,215.3 | 3 | % | ||||||||

|

|

|

|

|

|

|

|||||||||||

| (1) | Includes balance sheet line items trading, available-for-sale and held-to-maturity securities. |

| (2) | Includes balance sheet line items property and equipment, net, goodwill, other intangibles, net and other assets. |

| (3) | Includes balance sheet line items securities sold under agreements to repurchase and FHLB advances and other borrowings. |

Segregated Cash

Segregated cash decreased by $0.5 billion during the six months ended June 30, 2012. The level of cash required to be segregated under federal or other regulations, or segregated cash, is driven largely by customer cash and securities lending balances we hold as a liability in excess of the amount of margin receivables and securities borrowed balances we hold as an asset. The excess represents customer cash that we are required by our regulators to segregate for the exclusive benefit of our brokerage customers.

19

Table of Contents

Securities

Trading, available-for-sale and held-to-maturity securities are summarized as follows (dollars in millions):

| Variance | ||||||||||||||||

| June

30, 2012 |

December

31, 2011 |

2012 vs. 2011 | ||||||||||||||

| Amount | % | |||||||||||||||

| Trading securities |

$ | 60.1 | $ | 54.4 | $ | 5.7 | 10 | % | ||||||||

|

|

|

|

|

|

|

|||||||||||

| Available-for-sale securities: |

||||||||||||||||

| Residential mortgage-backed securities: |

||||||||||||||||

| Agency mortgage-backed securities and CMOs |

$ | 14,244.4 | $ | 13,965.7 | $ | 278.7 | 2 | % | ||||||||

| Non-agency CMOs |

314.2 | 341.6 | (27.4 | ) | (8 | )% | ||||||||||

|

|

|

|

|

|

|

|||||||||||

| Total residential mortgage-backed securities |

14,558.6 | 14,307.3 | 251.3 | 2 | % | |||||||||||

| Investment securities |

1,594.1 | 1,344.2 | 249.9 | 19 | % | |||||||||||

|

|

|

|

|

|

|

|||||||||||

| Total available-for-sale securities |

$ | 16,152.7 | $ | 15,651.5 | $ | 501.2 | 3 | % | ||||||||

|

|

|

|

|

|

|

|||||||||||

| Held-to-maturity securities: |

||||||||||||||||

| Residential mortgage-backed securities: |

||||||||||||||||

| Agency mortgage-backed securities and CMOs |

$ | 7,222.4 | $ | 5,296.5 | $ | 1,925.9 | 36 | % | ||||||||

| Investment securities |

1,211.3 | 783.0 | 428.3 | 55 | % | |||||||||||

|

|

|

|

|

|

|

|||||||||||

| Total held-to-maturity securities |

$ | 8,433.7 | $ | 6,079.5 | $ | 2,354.2 | 39 | % | ||||||||

|

|

|

|

|

|

|

|||||||||||

| Total securities |

$ | 24,646.5 | $ | 21,785.4 | $ | 2,861.1 | 13 | % | ||||||||

|

|

|

|

|

|

|

|||||||||||