UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

____________________________

FORM 10-Q

_____________________________________

| Quarterly Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 | |||||

For the quarterly period ended | |||||

OR

| Transition Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 | |||||

Commission File Number: 1-11859

____________________________

(Exact name of Registrant as specified in its charter)

____________________________

| (State or other jurisdiction of incorporation or organization) | (IRS Employer Identification No.) | ||||

(Address of principal executive offices, including zip code)

(617 ) 374-9600

(Registrant’s telephone number, including area code)

____________________________

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading symbol(s) | Name of each exchange on which registered | ||||||

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the Registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the Registrant was required to submit such files). Yes x No ¨

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

x | Accelerated filer | ☐ | Non-accelerated filer | ☐ | Smaller reporting company | Emerging growth company | |||||||||||||||||||||||

If an emerging growth company, indicate by check mark if the Registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

There were 82,961,204 shares of the Registrant’s common stock, $0.01 par value per share, outstanding on April 19, 2023.

PEGASYSTEMS INC.

QUARTERLY REPORT ON FORM 10-Q

TABLE OF CONTENTS

Page | |||||

| PART I - FINANCIAL INFORMATION | |||||

| Item 1. Financial Statements | |||||

Unaudited Condensed Consolidated Balance Sheets as of March 31, 2023 and December 31, 2022 | |||||

Unaudited Condensed Consolidated Statements of Operations for the three months ended March 31, 2023 and 2022 | |||||

Unaudited Condensed Consolidated Statements of Comprehensive (Loss) for the three months ended March 31, 2023 and 2022 | |||||

Unaudited Condensed Consolidated Statements of Stockholders’ Equity for the three months ended March 31, 2023 and 2022 | |||||

Unaudited Condensed Consolidated Statements of Cash Flows for the three months ended March 31, 2023 and 2022 | |||||

| Notes to Unaudited Condensed Consolidated Financial Statements | |||||

| Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations | |||||

| Item 3. Quantitative and Qualitative Disclosures About Market Risk | |||||

| Item 4. Controls and Procedures | |||||

| PART II - OTHER INFORMATION | |||||

| Item 1. Legal Proceedings | |||||

| Item 1A. Risk Factors | |||||

| Item 2. Unregistered Sales of Equity Securities and Use of Proceeds | |||||

| Item 5. Other Information | |||||

| Item 6. Exhibits | |||||

| Signature | |||||

2

PART I - FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENTS

PEGASYSTEMS INC. UNAUDITED CONDENSED CONSOLIDATED BALANCE SHEETS (in thousands) | |||||||||||

| March 31, 2023 | December 31, 2022 | ||||||||||

| Assets | |||||||||||

| Current assets: | |||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

| Marketable securities | |||||||||||

| Total cash, cash equivalents, and marketable securities | |||||||||||

| Accounts receivable | |||||||||||

| Unbilled receivables | |||||||||||

| Other current assets | |||||||||||

| Total current assets | |||||||||||

Unbilled receivables | |||||||||||

| Goodwill | |||||||||||

| Other long-term assets | |||||||||||

| Total assets | $ | $ | |||||||||

| Liabilities and stockholders’ equity | |||||||||||

| Current liabilities: | |||||||||||

| Accounts payable | $ | $ | |||||||||

| Accrued expenses | |||||||||||

| Accrued compensation and related expenses | |||||||||||

| Deferred revenue | |||||||||||

| Other current liabilities | |||||||||||

| Total current liabilities | |||||||||||

| Convertible senior notes, net | |||||||||||

| Operating lease liabilities | |||||||||||

| Other long-term liabilities | |||||||||||

| Total liabilities | |||||||||||

| Commitments and contingencies (Note 15) | |||||||||||

| Stockholders’ equity: | |||||||||||

Preferred stock, | |||||||||||

Common stock, March 31, 2023 and December 31, 2022, respectively | |||||||||||

| Additional paid-in capital | |||||||||||

Accumulated deficit | ( | ( | |||||||||

| Accumulated other comprehensive (loss) | ( | ( | |||||||||

| Total stockholders’ equity | |||||||||||

| Total liabilities and stockholders’ equity | $ | $ | |||||||||

See notes to unaudited condensed consolidated financial statements.

3

PEGASYSTEMS INC. UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS (in thousands, except per share amounts) | |||||||||||

| Three Months Ended March 31, | |||||||||||

| 2023 | 2022 | ||||||||||

| Revenue | |||||||||||

| Subscription services | $ | $ | |||||||||

| Subscription license | |||||||||||

| Consulting | |||||||||||

| Perpetual license | |||||||||||

| Total revenue | |||||||||||

| Cost of revenue | |||||||||||

| Subscription services | |||||||||||

| Subscription license | |||||||||||

| Consulting | |||||||||||

| Perpetual license | |||||||||||

| Total cost of revenue | |||||||||||

| Gross profit | |||||||||||

| Operating expenses | |||||||||||

| Selling and marketing | |||||||||||

| Research and development | |||||||||||

| General and administrative | |||||||||||

| Restructuring | |||||||||||

| Total operating expenses | |||||||||||

| (Loss) income from operations | ( | ||||||||||

| Foreign currency transaction (loss) gain | ( | ||||||||||

| Interest income | |||||||||||

| Interest expense | ( | ( | |||||||||

| Gain (loss) on capped call transactions | ( | ||||||||||

| Other income, net | |||||||||||

| (Loss) before provision for (benefit from) income taxes | ( | ( | |||||||||

| Provision for (benefit from) income taxes | ( | ||||||||||

| Net (loss) | $ | ( | $ | ( | |||||||

| (Loss) per share | |||||||||||

| Basic | $ | ( | $ | ||||||||

| Diluted | $ | ( | $ | ||||||||

| Weighted-average number of common shares outstanding | |||||||||||

| Basic | |||||||||||

| Diluted | |||||||||||

See notes to unaudited condensed consolidated financial statements.

4

PEGASYSTEMS INC. UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE (LOSS) (in thousands) | |||||||||||

| Three Months Ended March 31, | |||||||||||

| 2023 | 2022 | ||||||||||

| Net (loss) | $ | ( | $ | ( | |||||||

| Other comprehensive income (loss), net of tax | |||||||||||

| Unrealized (loss) gain on available-for-sale securities | ( | ||||||||||

| Foreign currency translation adjustments | ( | ||||||||||

| Total other comprehensive income (loss), net of tax | ( | ||||||||||

| Comprehensive (loss) | $ | ( | $ | ( | |||||||

See notes to unaudited condensed consolidated financial statements.

5

| PEGASYSTEMS INC. UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF STOCKHOLDERS’ EQUITY (in thousands, except per share amounts) | |||||||||||||||||||||||||||||||||||

Common Stock | Additional Paid-In Capital | Retained Earnings (Accumulated Deficit) | Accumulated Other Comprehensive (Loss) | Total Stockholders’ Equity | |||||||||||||||||||||||||||||||

| Number of Shares | Amount | ||||||||||||||||||||||||||||||||||

| December 31, 2021 | $ | $ | $ | $ | ( | $ | |||||||||||||||||||||||||||||

| Repurchase of common stock | ( | ( | ( | — | — | ( | |||||||||||||||||||||||||||||

| Issuance of common stock for stock compensation plans | ( | — | — | ( | |||||||||||||||||||||||||||||||

| Issuance of common stock under the employee stock purchase plan | — | — | — | ||||||||||||||||||||||||||||||||

| Stock-based compensation | — | — | — | — | |||||||||||||||||||||||||||||||

Cash dividends declared ($ | — | — | — | ( | — | ( | |||||||||||||||||||||||||||||

| Other comprehensive (loss) | — | — | — | — | ( | ( | |||||||||||||||||||||||||||||

| Net (loss) | — | — | — | ( | — | ( | |||||||||||||||||||||||||||||

| March 31, 2022 | $ | $ | $ | $ | ( | $ | |||||||||||||||||||||||||||||

| December 31, 2022 | $ | $ | $ | ( | $ | ( | $ | ||||||||||||||||||||||||||||

| Issuance of common stock for stock compensation plans | — | — | |||||||||||||||||||||||||||||||||

| Issuance of common stock under the employee stock purchase plan | — | — | |||||||||||||||||||||||||||||||||

| Stock-based compensation | — | — | — | — | |||||||||||||||||||||||||||||||

Cash dividends declared ($ | — | — | ( | — | — | ( | |||||||||||||||||||||||||||||

| Other comprehensive income | — | — | — | — | |||||||||||||||||||||||||||||||

| Net (loss) | — | — | — | ( | — | ( | |||||||||||||||||||||||||||||

| March 31, 2023 | $ | $ | $ | ( | $ | ( | $ | ||||||||||||||||||||||||||||

See notes to unaudited condensed consolidated financial statements.

6

PEGASYSTEMS INC. UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS (in thousands) | |||||||||||

| Three Months Ended March 31, | |||||||||||

| 2023 | 2022 | ||||||||||

| Operating activities | |||||||||||

| Net (loss) | $ | ( | $ | ( | |||||||

| Adjustments to reconcile net (loss) to cash provided by operating activities | |||||||||||

| Stock-based compensation | |||||||||||

| Deferred income taxes | ( | ( | |||||||||

| (Gain) loss on capped call transactions | ( | ||||||||||

| Amortization of deferred commissions | |||||||||||

| Lease expense | |||||||||||

| Amortization of intangible assets and depreciation | |||||||||||

| Foreign currency transaction loss (gain) | ( | ||||||||||

| Other non-cash | ( | ( | |||||||||

| Change in operating assets and liabilities, net | ( | ||||||||||

| Cash provided by operating activities | |||||||||||

| Investing activities | |||||||||||

| Purchases of investments | ( | ( | |||||||||

| Proceeds from maturities and called investments | |||||||||||

| Sales of investments | |||||||||||

| Investment in property and equipment | ( | ( | |||||||||

| Cash (used in) investing activities | ( | ( | |||||||||

| Financing activities | |||||||||||

| Repurchases of convertible senior notes | ( | ||||||||||

| Proceeds from settlement of capped calls transactions | |||||||||||

| Dividend payments to stockholders | ( | ( | |||||||||

| Proceeds from employee stock purchase plan | |||||||||||

| Proceeds from stock option exercises | |||||||||||

| Common stock repurchases | ( | ( | |||||||||

| Cash (used in) financing activities | ( | ( | |||||||||

| Effect of exchange rate changes on cash, cash equivalents, and restricted cash | ( | ||||||||||

| Net increase (decrease) in cash, cash equivalents, and restricted cash | ( | ||||||||||

| Cash, cash equivalents, and restricted cash, beginning of period | |||||||||||

| Cash, cash equivalents, and restricted cash, end of period | $ | $ | |||||||||

| Cash and cash equivalents | $ | $ | |||||||||

| Restricted cash included in other long-term assets | |||||||||||

| Total cash, cash equivalents and restricted cash | $ | $ | |||||||||

See notes to unaudited condensed consolidated financial statements.

7

PEGASYSTEMS INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

NOTE 1. BASIS OF PRESENTATION

Pegasystems Inc. (together with its subsidiaries, “the Company”) has prepared the accompanying unaudited condensed consolidated financial statements pursuant to the rules and regulations of the U.S. Securities and Exchange Commission (“SEC”) regarding interim financial reporting. Accordingly, they do not include all the information required by accounting principles generally accepted in the United States of America (“U.S.”) for complete financial statements and should be read in conjunction with the Company’s audited financial statements included in the Annual Report on Form 10-K for the year ended December 31, 2022.

In the opinion of management, the Company has prepared the accompanying unaudited condensed consolidated financial statements on the same basis as its audited financial statements, and these financial statements include all adjustments, consisting only of normal recurring adjustments, necessary for a fair presentation of the results of the interim periods presented.

All intercompany transactions and balances were eliminated in consolidation. The operating results for the interim periods presented do not necessarily indicate the expected results for the full year 2023.

NOTE 2. MARKETABLE SECURITIES

| March 31, 2023 | December 31, 2022 | ||||||||||||||||||||||||||||||||||||||||||||||

| (in thousands) | Amortized Cost | Unrealized Gains | Unrealized Losses | Fair Value | Amortized Cost | Unrealized Gains | Unrealized Losses | Fair Value | |||||||||||||||||||||||||||||||||||||||

| Government debt | $ | $ | $ | ( | $ | $ | $ | $ | ( | $ | |||||||||||||||||||||||||||||||||||||

| Corporate debt | ( | ( | |||||||||||||||||||||||||||||||||||||||||||||

| $ | $ | $ | ( | $ | $ | $ | $ | ( | $ | ||||||||||||||||||||||||||||||||||||||

As of March 31, 2023, marketable securities’ maturities ranged from April 2023 to January 2026, with a weighted-average remaining maturity of 0.5 years.

NOTE 3. RECEIVABLES, CONTRACT ASSETS, AND DEFERRED REVENUE

(in thousands) | March 31, 2023 | December 31, 2022 | |||||||||

| Accounts receivable | $ | $ | |||||||||

| Unbilled receivables | |||||||||||

| Long-term unbilled receivables | |||||||||||

| $ | $ | ||||||||||

Unbilled receivables

Unbilled receivables are client-committed amounts for which revenue recognition precedes billing, and billing is solely subject to the passage of time.

(Dollars in thousands) | March 31, 2023 | |||||||

| 1 year or less | $ | % | ||||||

| 1-2 years | % | |||||||

| 2-5 years | % | |||||||

| $ | % | |||||||

(Dollars in thousands) | March 31, 2023 | |||||||

| 2023 | $ | % | ||||||

| 2022 | % | |||||||

| 2021 | % | |||||||

| 2020 | % | |||||||

| 2019 and prior | % | |||||||

| $ | % | |||||||

8

PEGASYSTEMS INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

Contract assets

Contract assets are client-committed amounts for which revenue recognized exceeds the amount billed to the client, and billing is subject to conditions other than the passage of time, such as the completion of a related performance obligation.

(in thousands) | March 31, 2023 | December 31, 2022 | |||||||||

Contract assets (1) | $ | $ | |||||||||

Long-term contract assets (2) | |||||||||||

| $ | $ | ||||||||||

(1) Included in other current assets. (2) Included in other long-term assets.

Deferred revenue

Deferred revenue consists of billings and payments received in advance of revenue recognition.

(in thousands) | March 31, 2023 | December 31, 2022 | |||||||||

| Deferred revenue | $ | $ | |||||||||

Long-term deferred revenue (1) | |||||||||||

| $ | $ | ||||||||||

(1) Included in other long-term liabilities.

The increase in deferred revenue in the three months ended March 31, 2023 was primarily due to new billings in advance of revenue recognition exceeding the $139.7 million of revenue recognized during the period that was included in deferred revenue as of December 31, 2022.

NOTE 4. DEFERRED COMMISSIONS

(in thousands) | March 31, 2023 | December 31, 2022 | |||||||||

Deferred commissions (1) | $ | $ | |||||||||

| Three Months Ended March 31, | |||||||||||

| (in thousands) | 2023 | 2022 | |||||||||

Amortization of deferred commissions (1) | $ | $ | |||||||||

NOTE 5. GOODWILL AND OTHER INTANGIBLES

Goodwill

| Three Months Ended March 31, | |||||||||||

(in thousands) | 2023 | 2022 | |||||||||

| January 1, | $ | $ | |||||||||

| Currency translation adjustments | |||||||||||

| March 31, | $ | $ | |||||||||

Intangibles

Intangible assets are recorded at cost and amortized using the straight-line method over their estimated useful lives.

| March 31, 2023 | |||||||||||||||||||||||

| (in thousands) | Useful Lives | Cost | Accumulated Amortization | Net Book Value (1) | |||||||||||||||||||

Client-related | $ | $ | ( | $ | |||||||||||||||||||

Technology | ( | ||||||||||||||||||||||

Other | ( | ||||||||||||||||||||||

| $ | $ | ( | $ | ||||||||||||||||||||

(1) Included in other long-term assets.

9

PEGASYSTEMS INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

| December 31, 2022 | |||||||||||||||||||||||

| (in thousands) | Useful Lives | Cost | Accumulated Amortization | Net Book Value (1) | |||||||||||||||||||

| Client-related | $ | $ | ( | $ | |||||||||||||||||||

| Technology | ( | ||||||||||||||||||||||

| Other | ( | ||||||||||||||||||||||

| $ | $ | ( | $ | ||||||||||||||||||||

(1) Included in other long-term assets.

(in thousands) | March 31, 2023 | ||||

| Remainder of 2023 | $ | ||||

| 2024 | |||||

| 2025 | |||||

| 2026 | |||||

| 2027 | |||||

| $ | |||||

| Three Months Ended March 31, | |||||||||||

| (in thousands) | 2023 | 2022 | |||||||||

Cost of revenue | $ | $ | |||||||||

Selling and marketing | |||||||||||

| $ | $ | ||||||||||

NOTE 6. OTHER ASSETS AND LIABILITIES

Other current assets

| (in thousands) | March 31, 2023 | December 31, 2022 | |||||||||

| Income tax receivables | $ | $ | |||||||||

| Contract assets | |||||||||||

| Other | |||||||||||

| $ | $ | ||||||||||

Other long-term assets

| (in thousands) | March 31, 2023 | December 31, 2022 | |||||||||

| Deferred commissions | $ | $ | |||||||||

| Right of use assets | |||||||||||

| Property and equipment | |||||||||||

| Venture investments | |||||||||||

| Contract assets | |||||||||||

| Intangible assets | |||||||||||

| Capped call transactions | |||||||||||

| Deferred income taxes | |||||||||||

| Restricted cash | |||||||||||

| Other | |||||||||||

| $ | $ | ||||||||||

Other current liabilities

| (in thousands) | March 31, 2023 | December 31, 2022 | |||||||||

| Operating lease liabilities | $ | $ | |||||||||

| Dividends payable | |||||||||||

| $ | $ | ||||||||||

10

PEGASYSTEMS INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

Other long-term liabilities

| (in thousands) | March 31, 2023 | December 31, 2022 | |||||||||

| Deferred revenue | $ | $ | |||||||||

| Income taxes payable | |||||||||||

| Other | |||||||||||

| $ | $ | ||||||||||

NOTE 7. LEASES

Expense

| Three Months Ended March 31, | |||||||||||

| (in thousands) | 2023 | 2022 | |||||||||

| Fixed lease costs | $ | $ | |||||||||

| Short-term lease costs | |||||||||||

| Variable lease costs | |||||||||||

| $ | $ | ||||||||||

Right of use assets and lease liabilities

| (in thousands) | March 31, 2023 | December 31, 2022 | |||||||||

| $ | $ | ||||||||||

| $ | $ | ||||||||||

| Long-term operating lease liabilities | $ | $ | |||||||||

(1) Included in other long-term assets.

(2) Included in other current liabilities.

Weighted-average remaining lease term and discount rate for the Company’s leases were:

| March 31, 2023 | December 31, 2022 | ||||||||||

| Weighted-average remaining lease term | |||||||||||

Weighted-average discount rate (1) | % | % | |||||||||

(1) The rates implicit in most of the Company’s leases are not readily determinable. Therefore, the Company uses its incremental borrowing rate as the discount rate when measuring operating lease liabilities. The incremental borrowing rate represents an estimate of the interest rate the Company would incur to borrow an amount equal to the lease payments on a collateralized basis over the lease term in a similar economic environment.

Maturities of lease liabilities:

| (in thousands) | March 31, 2023 | ||||

| Remainder of 2023 | $ | ||||

| 2024 | |||||

| 2025 | |||||

| 2026 | |||||

| 2027 | |||||

| 2028 | |||||

| Thereafter | |||||

| Total lease payments | |||||

Less: imputed interest (1) | ( | ||||

| $ | |||||

(1) Lease liabilities are measured at the present value of the remaining lease payments using a discount rate determined at lease commencement unless the discount rate is updated due to a lease reassessment event.

Cash flow information

| Three Months Ended March 31, | |||||||||||

| (in thousands) | 2023 | 2022 | |||||||||

| Cash paid for operating leases, net of tenant improvement allowances | $ | $ | |||||||||

| Right of use assets recognized for new leases and amendments (non-cash) | $ | $ | |||||||||

11

PEGASYSTEMS INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

NOTE 8. DEBT

Convertible senior notes and capped calls

Convertible senior notes

In February 2020, the Company issued Convertible Senior Notes (the "Notes") with an aggregate principal of $600 million, due March 1, 2025, in a private placement. No principal payments are due before maturity. The Notes accrue interest at an annual rate of 0.75 %, payable semi-annually in arrears on March 1 and September 1, beginning on September 1, 2020.

In the three months ended March 31, 2023, the Company recorded a gain of $2.8 million in other income, net from the repurchase of Notes representing $33 million in aggregate principal amount.

Conversion rights

The conversion rate is 7.4045 shares of common stock per $1,000 principal amount of the Notes, representing an initial conversion price of $135.05 per share of common stock. The Company will settle conversions by paying or delivering cash, shares of its common stock, or a combination of cash and shares of its common stock, at the Company’s election, based on the applicable conversion rate. The conversion rate will be adjusted upon certain events, including spin-offs, tender offers, exchange offers, and certain stockholder distributions.

Beginning on September 1, 2024, noteholders may convert their Notes at any time at their election.

Before September 1, 2024, noteholders may convert their Notes in the following circumstances:

•During any calendar quarter beginning after June 30, 2020 (and only during such calendar quarter), if the last reported sale price per share of the Company’s common stock exceeds 130 % of the conversion price for each of at least 20 trading days (whether or not consecutive) during the 30 consecutive trading days ending on, and including, the last trading day of the immediately preceding calendar quarter.

•During the five consecutive business days immediately after any five consecutive trading day period (the “Measurement Period”), if the trading price per $1,000 principal amount of Notes for each trading day of the Measurement Period was less than 98 % of the product of the last reported sale price per share of common stock on such trading day and the conversion rate on such trading day.

•Upon certain corporate events or distributions or if the Company calls any Notes for redemption, noteholders may convert before the close of business on the business day immediately before the related redemption date (or, if the Company fails to pay the redemption price in full on the redemption date, until the Company pays the redemption price).

As of March 31, 2023, the Notes were not eligible for conversion.

Repurchase rights

On or after March 1, 2023 and on or before the 40 th scheduled trading day immediately before the maturity date, the Company may redeem for cash all or part of the Notes at a repurchase price equal to 100 % of the principal amount, plus accrued and unpaid interest, if the last reported sale price of the Company’s common stock exceeded 130 % of the conversion price then in effect for at least 20 trading days (whether or not consecutive) during any 30 consecutive trading day period ending on, and including, the trading day immediately preceding the date on which the Company provides a redemption notice.

If certain corporate events that constitute a “Fundamental Change” occur, each noteholder will have the right to require the Company to repurchase for cash all of such noteholder’s Notes, or any portion of the principal thereof that is equal to $1,000 or a multiple of $1,000, at a repurchase price equal to 100 % of the principal amount thereof, plus accrued and unpaid interest. A Fundamental Change relates to mergers, changes in control of the Company, liquidation/dissolution of the Company, or the delisting of the Company’s common stock.

Carrying value of the Notes:

| (in thousands) | March 31, 2023 | December 31, 2022 | |||||||||

| Principal | $ | $ | |||||||||

| Unamortized issuance costs | ( | ( | |||||||||

| Convertible senior notes, net | $ | $ | |||||||||

Interest expense related to the Notes:

| Three Months Ended March 31, | |||||||||||

| (in thousands) | 2023 | 2022 | |||||||||

Contractual interest expense ( | $ | $ | |||||||||

Amortization of issuance costs | |||||||||||

| $ | $ | ||||||||||

12

PEGASYSTEMS INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

The average interest rate on the Notes in the three months ended March 31, 2023 and 2022 was 1.2

| March 31, 2023 | |||||||||||||||||

| (in thousands) | Principal | Interest | Total | ||||||||||||||

| Remainder of 2023 | $ | $ | $ | ||||||||||||||

| 2024 | |||||||||||||||||

| 2025 | |||||||||||||||||

| $ | $ | $ | |||||||||||||||

Capped call transactions

In February 2020, the Company entered into privately negotiated capped call transactions (the “Capped Call Transactions”) with certain financial institutions. The Capped Call Transactions covered approximately 4.4 million shares (representing the number of shares for which the Notes were initially convertible) of the Company’s common stock. In the three months ended March 31, 2023, Capped Call Transactions covering approximately 0.2 million shares were settled for proceeds of $0.2 million.

As of March 31, 2023, Capped Call Transactions representing approximately 4.2 million shares were outstanding.

The Capped Call Transactions are expected to reduce common stock dilution and/or offset any potential cash payments the Company must make, other than for principal and interest, upon conversion of the Notes, with such reduction and/or offset subject to a cap of $196.44 . The cap price of the Capped Call Transactions is subject to adjustment upon specified extraordinary events affecting the Company, including mergers and tender offers.

The Capped Call Transactions are accounted for as derivative instruments and do not qualify for the Company’s own equity scope exception in ASC 815 since, in some cases of early settlement, the settlement value of the Capped Call Transactions, calculated following the governing documents, may not represent a fair value measurement. The Capped Call Transactions are classified as other long-term assets and remeasured to fair value each reporting period, resulting in a non-operating gain or loss.

| Three Months Ended March 31, | |||||||||||

| (in thousands) | 2023 | 2022 | |||||||||

| January 1, | $ | $ | |||||||||

| Settlements | ( | ||||||||||

| Fair value adjustment | ( | ||||||||||

| March 31, | $ | $ | |||||||||

Credit facility

In November 2019, and as since amended, the Company entered into a five-year $100 million senior secured revolving credit agreement (the “Credit Facility”) with PNC Bank, National Association. The Company may use borrowings for general corporate purposes and to finance working capital needs. Subject to specific conditions and the agreement of the financial institutions lending the additional amount, the aggregate commitment may be increased to $200 million. The commitments expire on November 4, 2024, and any outstanding loans will be payable on such date. The Credit Facility, as amended, contains customary covenants, including, but not limited to, those relating to additional indebtedness, liens, asset divestitures, and affiliate transactions.

The Company is required to comply with financial covenants, including:

•Beginning with the fiscal quarter ended March 31, 2022 and ending with the fiscal quarter ended December 31, 2023, Pegasystems Inc. must maintain at least $200 million in cash, investments, and availability under the Revolving Credit Loan.

•Beginning with the fiscal quarter ended March 31, 2023 and ending with the fiscal year ended December 31, 2023, maintain

| Year to Date | |||||||||||||||||||||||

| (in thousands) | March 31, 2023 | June 30, 2023 | September 30, 2023 | December 31, 2023 | |||||||||||||||||||

| Minimum Consolidated EBITDA (as defined in the Credit Facility) | $ | $ | $ | $ | |||||||||||||||||||

•Beginning with the fiscal quarter ended March 31, 2024, a maximum net consolidated leverage ratio of 3.5 to 1.0 (with a step-up for certain acquisitions) and a minimum consolidated interest coverage ratio of 3.5 to 1.0.

As of March 31, 2023 and December 31, 2022, the Company had no

As of March 31, 2023, the Company had $27.3 million in outstanding letters of credit, which reduce the Company’s available borrowing capacity under the Credit Facility.

13

PEGASYSTEMS INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

NOTE 9. RESTRUCTURING

Go-to-market plan and Salem office

During the fourth quarter of 2022, management committed to a restructuring plan aligned with the Company’s target organization go-to-market strategy. The plan resulted in a restructuring expense of $21.7 million, primarily associated with severance and benefits for impacted employees and expenses incurred as a result of the closure of the Company’s Salem, New Hampshire office.

Accrued employee severance and related benefits:

| (in thousands) | 2023 | ||||

| January 1, | $ | ||||

| Costs incurred | |||||

| Cash disbursements | ( | ||||

| Currency translation adjustments | |||||

| March 31, | $ | ||||

2023 office space closure

In the three months ended March 31, 2023, the Company recognized an impairment of $1.2 million on its operating lease right of use assets primarily due to the closure of leased office space in Poland.

NOTE 10. FAIR VALUE MEASUREMENTS

Assets and liabilities measured at fair value on a recurring basis

The Company records its cash equivalents, marketable securities, Capped Call Transactions, and venture investments at fair value on a recurring basis. Fair value is an exit price, representing the amount that would be received from the sale of an asset or paid to transfer a liability in an orderly transaction between market participants based on assumptions that market participants would use in pricing an asset or liability.

As a basis for classifying the fair value measurements, a three-tier fair value hierarchy, which classifies the fair value measurements based on the inputs used in measuring fair value, was established as follows:

•Level 1 - observable inputs, such as quoted prices in active markets for identical assets or liabilities;

•Level 2 - significant other inputs that are observable either directly or indirectly; and

•Level 3 - significant unobservable inputs on which there is little or no market data, which require the Company to develop its own assumptions.

This hierarchy requires the Company to use observable market data, when available, and minimize unobservable inputs when determining fair value.

The fair value of the Capped Call Transactions at the end of each reporting period is determined using a Black-Scholes option-pricing model. The valuation model uses various market-based inputs, including stock price, remaining contractual term, expected volatility, risk-free interest rate, and expected dividend yield. The Company applies judgment when determining expected volatility. The Company considers the underlying equity security’s historical and implied volatility levels. The Company’s venture investments are recorded at fair value based on multiple valuation methods, including observable public companies and transaction prices and unobservable inputs, including the volatility, rights, and obligations of the securities the Company holds.

Assets and liabilities measured at fair value on a recurring basis:

| March 31, 2023 | December 31, 2022 | ||||||||||||||||||||||||||||||||||||||||||||||

| (in thousands) | Level 1 | Level 2 | Level 3 | Total | Level 1 | Level 2 | Level 3 | Total | |||||||||||||||||||||||||||||||||||||||

| Cash equivalents | $ | $ | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||

| Marketable securities | $ | $ | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||

Capped Call Transactions (1) | $ | $ | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||

Venture investments (1) (2) | $ | $ | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||

(1) Included in other long-term assets. (2) Investments in privately-held companies.

14

PEGASYSTEMS INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

| Three Months Ended March 31, | |||||||||||

| (in thousands) | 2023 | 2022 | |||||||||

| January 1, | $ | $ | |||||||||

| New investments | |||||||||||

| Changes in foreign exchange rates | ( | ||||||||||

| Changes in fair value: | |||||||||||

included in other income, net | |||||||||||

included in other comprehensive (loss) | ( | ||||||||||

| March 31, | $ | $ | |||||||||

The carrying value of certain other financial instruments, including receivables and accounts payable, approximates fair value due to these items’ short maturities.

Fair value of the Notes

The fair value of the Notes outstanding (including the embedded conversion feature) was $507.8 million as of March 31, 2023 and $521.1 million as of December 31, 2022. In the three months ended March 31, 2023 the Company repurchased Notes representing $33 million in aggregate principal amount.

The fair value was determined based on the Notes’ quoted price in an over-the-counter market on the last trading day of the reporting period and classified within Level 2 in the fair value hierarchy.

NOTE 11. REVENUE

| Three Months Ended March 31, | |||||||||||||||||

(Dollars in thousands) | 2023 | 2022 | |||||||||||||||

| U.S. | $ | % | $ | % | |||||||||||||

| Other Americas | % | % | |||||||||||||||

| United Kingdom (“U.K.”) | % | % | |||||||||||||||

| Europe (excluding U.K.), Middle East, and Africa | % | % | |||||||||||||||

| Asia-Pacific | % | % | |||||||||||||||

| $ | % | $ | % | ||||||||||||||

Revenue streams

| Three Months Ended March 31, | |||||||||||

(in thousands) | 2023 | 2022 | |||||||||

| Perpetual license | $ | $ | |||||||||

| Subscription license | |||||||||||

| Revenue recognized at a point in time | |||||||||||

| Maintenance | |||||||||||

| Pega Cloud | |||||||||||

| Consulting | |||||||||||

| Revenue recognized over time | |||||||||||

| Total revenue | $ | $ | |||||||||

15

PEGASYSTEMS INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

| Three Months Ended March 31, | |||||||||||

| (in thousands) | 2023 | 2022 | |||||||||

| Pega Cloud | $ | $ | |||||||||

| Maintenance | |||||||||||

| Subscription services | |||||||||||

| Subscription license | |||||||||||

| Subscription | |||||||||||

| Perpetual license | |||||||||||

| Consulting | |||||||||||

| $ | $ | ||||||||||

Remaining performance obligations ("Backlog")

Expected future revenue from existing non-cancellable contracts:

As of March 31, 2023:

| (Dollars in thousands) | Subscription services | Subscription license | Perpetual license | Consulting | Total | |||||||||||||||||||||||||||||||||

| Maintenance | Pega Cloud | |||||||||||||||||||||||||||||||||||||

1 year or less | $ | $ | $ | $ | $ | $ | % | |||||||||||||||||||||||||||||||

1-2 years | % | |||||||||||||||||||||||||||||||||||||

2-3 years | % | |||||||||||||||||||||||||||||||||||||

Greater than 3 years | % | |||||||||||||||||||||||||||||||||||||

| $ | $ | $ | $ | $ | $ | % | ||||||||||||||||||||||||||||||||

As of March 31, 2022:

| (Dollars in thousands) | Subscription services | Subscription license | Perpetual license | Consulting | Total | |||||||||||||||||||||||||||||||||

| Maintenance | Pega Cloud | |||||||||||||||||||||||||||||||||||||

1 year or less | $ | $ | $ | $ | $ | $ | % | |||||||||||||||||||||||||||||||

1-2 years | % | |||||||||||||||||||||||||||||||||||||

2-3 years | % | |||||||||||||||||||||||||||||||||||||

Greater than 3 years | % | |||||||||||||||||||||||||||||||||||||

| $ | $ | $ | $ | $ | $ | % | ||||||||||||||||||||||||||||||||

NOTE 12. STOCK-BASED COMPENSATION

Expense

| Three Months Ended March 31, | |||||||||||

| (in thousands) | 2023 | 2022 | |||||||||

Cost of revenue | $ | $ | |||||||||

Selling and marketing | |||||||||||

Research and development | |||||||||||

General and administrative | |||||||||||

| $ | $ | ||||||||||

Income tax benefit | $ | ( | $ | ( | |||||||

As of March 31, 2023, the Company had $178.6 million of unrecognized stock-based compensation expense, net of estimated forfeitures, which is expected to be recognized over a weighted-average period of 2 years.

| Three Months Ended March 31, 2023 | |||||||||||

| (in thousands) | Shares | Total Fair Value | |||||||||

Restricted stock units | $ | ||||||||||

Non-qualified stock options | $ | ||||||||||

16

PEGASYSTEMS INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

NOTE 13. INCOME TAXES

Effective income tax rate

| Three Months Ended March 31, | |||||||||||

| (Dollars in thousands) | 2023 | 2022 | |||||||||

| Provision for (benefit from) income taxes | $ | $ | ( | ||||||||

| Effective income tax rate | ( | % | % | ||||||||

The effective income tax rate in the three months ended March 31, 2023 was impacted by the valuation allowance on the Company’s U.S. and U.K. deferred tax assets and current taxes payable in the U.S. as a result of projecting taxable income that cannot be fully offset by net operating losses and available tax credits.

The Company recognizes deferred tax assets to the extent that it believes that these assets are more likely than not to be realized. Future realization of deferred tax assets ultimately depends on sufficient taxable income within the available carryback or carryforward periods. The Company’s deferred tax valuation allowance requires significant judgment and uncertainties, including assumptions about future taxable income based on historical and projected information. On a quarterly basis, the Company reassesses the need for a valuation allowance on its existing net deferred tax assets by tax-paying jurisdiction, weighing positive and negative evidence to assess its recoverability. In making such a determination, the Company considers all available and objectively verifiable negative and positive evidence, including future reversals of existing taxable temporary differences, committed contractual backlog (“Backlog”), projected future taxable income inclusive of the impact of enacted legislation, tax-planning strategies, and results of recent operations. The weight given to the potential effect of negative and positive evidence is commensurate with the extent to which it can be objectively verified.

The Company intends to continue maintaining a full valuation allowance on the Company’s U.S and U.K. deferred tax assets until there is sufficient evidence to support the realization of these deferred tax assets.

NOTE 14. (LOSS) PER SHARE

Basic (loss) per share is calculated using the weighted-average number of common shares outstanding during the period. Diluted (loss) per share is calculated using the weighted-average number of common shares outstanding during the period, plus the dilutive effect of outstanding stock options, RSUs, and convertible senior notes.

Calculation of (loss) per share:

| Three Months Ended March 31, | |||||||||||

| (in thousands, except per share amounts) | 2023 | 2022 | |||||||||

| Net (loss) | $ | ( | $ | ( | |||||||

| Weighted-average common shares outstanding | |||||||||||

| (Loss) per share, basic | $ | ( | $ | ||||||||

| Net (loss) | $ | ( | $ | ( | |||||||

Weighted-average common shares outstanding, assuming dilution (1) (2) (3) | |||||||||||

| (Loss) per share, diluted | $ | ( | $ | ||||||||

Outstanding anti-dilutive stock options and RSUs (4) | |||||||||||

(1) In periods of loss, all dilutive securities are excluded as their inclusion would be anti-dilutive.

(2) The shares underlying the conversion options in the Company’s Notes are included using the if-converted method, if dilutive in the period. If the outstanding conversion options were fully exercised, the Company would issue approximately 4.2 million shares as of March 31, 2023.

(3) The Company’s Capped Call Transactions represent the equivalent of approximately 4.2 million shares of the Company’s common stock (representing the number of shares for which the Notes are initially convertible) as of March 31, 2023. The Capped Call Transactions are expected to reduce common stock dilution and/or offset any potential cash payments the Company must make, other than for principal and interest, upon conversion of the Notes, with such reduction and/or offset subject to a cap of $196.44 . The Capped Call Transactions are excluded from weighted-average common shares outstanding, assuming dilution, in all periods as their effect would be anti-dilutive.

(4) Outstanding stock options and RSUs that were anti-dilutive under the treasury stock method in the period were excluded from the computation of diluted (loss) per share. These awards may be dilutive in the future.

NOTE 15. COMMITMENTS AND CONTINGENCIES

Commitments

See "Note 7. Leases" for additional information.

17

PEGASYSTEMS INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

Legal proceedings

In addition to the matters below, the Company is or may become involved in a variety of claims, demands, suits, investigations, and proceedings that arise from time to time relating to matters incidental to the ordinary course of the Company’s business, including actions concerning contracts, intellectual property, employment, benefits, and securities matters. Regardless of the outcome, legal disputes can have a material effect on the Company because of defense and settlement costs, diversion of management resources, and other factors.

In addition, as the Company is a party to ongoing litigation, it is at least reasonably possible that the Company’s estimates will change in the near term, and the effect may be material.

The Company had no accrued losses for litigation as of March 31, 2023 and December 31, 2022.

Appian Corp. v. Pegasystems Inc. & Youyong Zou

As previously reported, the Company is a defendant in litigation brought by Appian in the Circuit Court of Fairfax County, Virginia (the “Court”) titled Appian Corp. v. Pegasystems Inc. & Youyong Zou, No. 2020-07216 (Fairfax Cty. Ct.). On May 9, 2022, the jury rendered its verdict finding that the Company had misappropriated one or more of Appian’s trade secrets, that the Company had violated the Virginia Computer Crimes Act, and that the trade secret misappropriation was willful and malicious. The jury awarded damages of $2,036,860,045 for trade secret misappropriation and $1.00 for violating the Virginia Computer Crimes Act. On September 15, 2022, the circuit court of Fairfax County entered judgment of $2,060,479,287 , consisting of the damages previously awarded by the jury plus attorneys’ fees and costs, and stating that the judgment is subject to post-judgment interest at a rate of 6.0 % per annum, from the date of the jury verdict (May 9, 2022) as to the amount of the jury verdict and from September 15, 2022 as to the amount of the award of attorneys’ fees and costs. On September 15, 2022, the Company filed a notice of appeal from the judgment. On September 29, 2022, the circuit court of Fairfax County approved a $25,000,000 letter of credit obtained by the Company to secure the judgment and entered an order suspending the judgment during the pendency of the Company’s appeal. Appellate briefing is currently in process. Although it is not possible to predict timing, this appeals process could potentially take years to complete. The Company continues to believe that it did not misappropriate any alleged trade secrets and that its sales of the Company’s products at issue were not caused by, or the result of, any alleged misappropriation of trade secrets. The Company is unable to reasonably estimate possible damages because of, among other things, uncertainty as to the outcome of appellate proceedings and/or any potential new trial resulting from the appellate proceedings.

City of Fort Lauderdale Police and Firefighters’ Retirement System, Individually and on Behalf of All Others Similarly Situated v. Pegasystems Inc., Alan Trefler, and Kenneth Stillwell

On May 19, 2022, a lawsuit was filed against the Company, the Company’s chief executive officer and the Company’s chief operating and financial officer in the United States District Court for the Eastern District of Virginia Alexandria Division, captioned City of Fort Lauderdale Police and Firefighters’ Retirement System, Individually and on Behalf of All Others Similarly Situated v. Pegasystems Inc., Alan Trefler, and Kenneth Stillwell (Case 1:22-cv-00578-LMB-IDD). The complaint generally alleges, among other things, that the defendants violated Section 10(b) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”) and Rule 10b-5 promulgated thereunder and that the individual defendants violated Section 20(a) of the Exchange Act, in each case by allegedly making materially false and/or misleading statements, as well as allegedly failing to disclose material adverse facts about the Company’s business, operations, and prospects, which caused the Company’s securities to trade at artificially inflated prices. The complaint seeks unspecified damages on behalf of a class of purchasers of the Company’s securities between May 29, 2020 and May 9, 2022. The litigation has since been transferred to the United States District Court for the District of Massachusetts (Case 1:22-cv-11220-WGY), and lead plaintiff class representatives—Central Pennsylvania Teamsters Pension Fund - Defined Benefit Plan, Central Pennsylvania Teamsters Pension Fund - Retirement Income Plan 1987, and Construction Industry Laborers Pension Fund—have been appointed. On October 18, 2022, a consolidated amended complaint was filed that does not add any new parties or legal claims, is based upon the same general factual allegations as the original complaint, and now seeks unspecified damages on behalf of a class of purchasers of the Company’s securities between June 16, 2020 and May 9, 2022. The Company moved to dismiss the consolidated amended complaint on December 19, 2022. The hearing on the motion to dismiss is scheduled for May 17, 2023. The Company believes the claims brought against the defendants are without merit and intends to defend against these claims vigorously. The Company is unable to reasonably estimate possible damages or a range of possible damages in this matter given the stage of the lawsuit, the Company’s belief that the claims are without merit, and there being no specified quantum of damages sought in the complaint.

18

PEGASYSTEMS INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

Mary Larkin, derivatively on behalf of nominal defendant Pegasystems Inc. v. Peter Gyenes, Richard Jones, Christopher Lafond, Dianne Ledingham, Sharon Rowlands, Alan Trefler, Larry Weber, and Kenneth Stillwell, defendants, and Pegasystems Inc., nominal defendant

On November 21, 2022, a lawsuit was filed against the members of the Company’s board of directors, the Company’s chief operating and financial officer and the Company in the United States District Court for the District of Massachusetts, captioned Mary Larkin, derivatively on behalf of nominal defendant Pegasystems Inc. v. Peter Gyenes, Richard Jones, Christopher Lafond, Dianne Ledingham, Sharon Rowlands, Alan Trefler, Larry Weber, and Kenneth Stillwell, defendants, and Pegasystems Inc., nominal defendant (Case 1:22-cv-11985). The complaint generally alleges the defendants sold shares of the Company while in possession of material nonpublic information relating to (i) the litigation brought by Appian in the Circuit Court of Fairfax County, Virginia, described above, and (ii) alleged misconduct by Company employees alleged in that litigation. On January 10, 2023, the Court entered an order staying the matter until after a final judgment dismissing the City of Fort Lauderdale matter referenced above, the denial of a motion to dismiss in the City of Fort Lauderdale action, or if any related derivative complaint is filed and not stayed for the same or longer duration. The Company believes the claims brought against the defendants are without merit and intends to defend against these claims vigorously. The Company is unable to reasonably estimate possible damages or a range of possible damages in this matter given the stage of the lawsuit, the Company’s belief that the claims are without merit, and there being no specified quantum of damages sought in the complaint.

SEC Inquiry

Beginning in March 2023, the U.S. Securities and Exchange Commission (“SEC”) has requested certain information relating to, among other things, the accounting treatment of the Company’s above-described litigation with Appian Corporation. The Company is fully cooperating with the SEC’s requests.

19

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

FORWARD-LOOKING STATEMENTS

This Quarterly Report on Form 10-Q (“Quarterly Report”) contains or incorporates forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995.

Words such as expects, anticipates, intends, plans, believes, will, could, should, estimates, may, targets, strategies, projects, forecasts, guidance, likely, and usually, or variations of such words and other similar expressions identify forward-looking statements, which are based on current expectations and assumptions.

Forward-looking statements deal with future events and are subject to risks and uncertainties that are difficult to predict, including, but not limited to:

•our future financial performance and business plans;

•the adequacy of our liquidity and capital resources;

•the continued payment of our quarterly dividends;

•the timing of revenue recognition;

•management of our transition to a more subscription-based business model;

•variation in demand for our products and services, including among clients in the public sector;

•reliance on key personnel;

•global economic and political conditions and uncertainty, including impacts from public health emergencies and the war in Ukraine;

•reliance on third-party service providers, including hosting providers;

•compliance with our debt obligations and covenants;

•the potential impact of our convertible senior notes and Capped Call Transactions;

•foreign currency exchange rates;

•the potential legal and financial liabilities and damage to our reputation due to cyber-attacks;

•security breaches and security flaws;

•our ability to protect our intellectual property rights, costs associated with defending such rights, intellectual property rights claims, and other related claims by third parties against us, including related costs, damages, and other relief that may be granted against us;

•our ongoing litigation with Appian Corp.;

•our client retention rate; and

•management of our growth.

These risks and others that may cause actual results to differ materially from those expressed in such forward-looking statements are described further in Part I of our Annual Report on Form 10-K for the year ended December 31, 2022, Part II of this Quarterly Report on Form 10-Q, and other filings we make with the U.S. Securities and Exchange Commission (“SEC”).

Except as required by applicable law, we do not undertake and expressly disclaim any obligation to update or revise these forward-looking statements publicly, whether due to new information, future events, or otherwise.

The forward-looking statements in this Quarterly Report represent our views as of April 26, 2023.

BUSINESS OVERVIEW

We develop, market, license, host, and support enterprise software that helps organizations build agility into their business so they can adapt to change. Our powerful low-code platform for workflow automation and artificial intelligence-powered decisioning enables the world’s leading brands and government agencies to hyper-personalize customer experiences, streamline customer service, and automate mission-critical business processes and workflows. With Pega, our clients can leverage our intelligent technology and scalable architecture to accelerate their digital transformation. In addition, our client success teams, world-class partners, and clients leverage our Pega Express™ methodology to design and deploy mission-critical applications quickly and collaboratively.

Our target clients are Global 2000 organizations and government agencies that require solutions to distinguish themselves in the markets they serve. Our solutions achieve and facilitate differentiation by increasing business agility, driving growth, improving productivity, attracting and retaining customers, and reducing risk. Along with our partners, we deliver solutions tailored to the specific industry needs of our clients.

Subscription transition

We are transitioning our business to sell software primarily through subscription arrangements. Until we fully complete our subscription transition, which we expect will occur in 2023, our operating results may be impacted. Operating performance, revenue mix, and new arrangements in each period can fluctuate based on client preferences for our perpetual and subscription offerings. See the “Risk Factors” section of our Annual Report on Form 10-K for the year ended December 31, 2022 for additional information.

20

Performance metrics

We use performance metrics to analyze and assess our overall performance, make operating decisions, and forecast and plan for future periods, including:

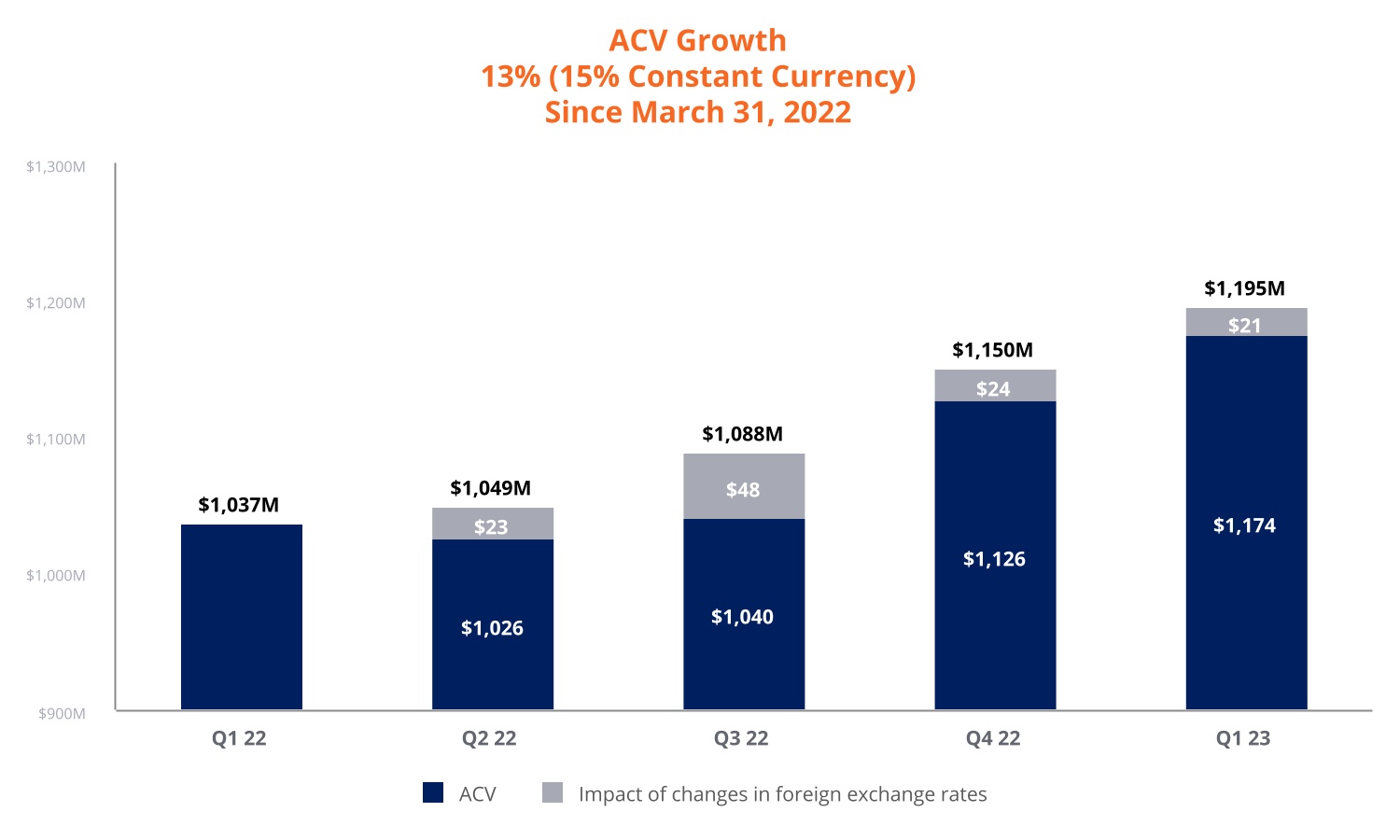

Annual contract value (“ACV”)

ACV represents the annualized value of our active contracts as of the measurement date. The contract's total value is divided by its duration in years to calculate ACV. ACV is a performance measure that we believe provides useful information to our management and investors.

In 2023, we changed our ACV calculation methodology for maintenance and all contracts less than 12 months to align with other contract types. Previously disclosed ACV amounts have been updated to allow for comparability.

Constant currency ACV is calculated by applying the Q1 2022 foreign exchange rates to all periods shown.

21

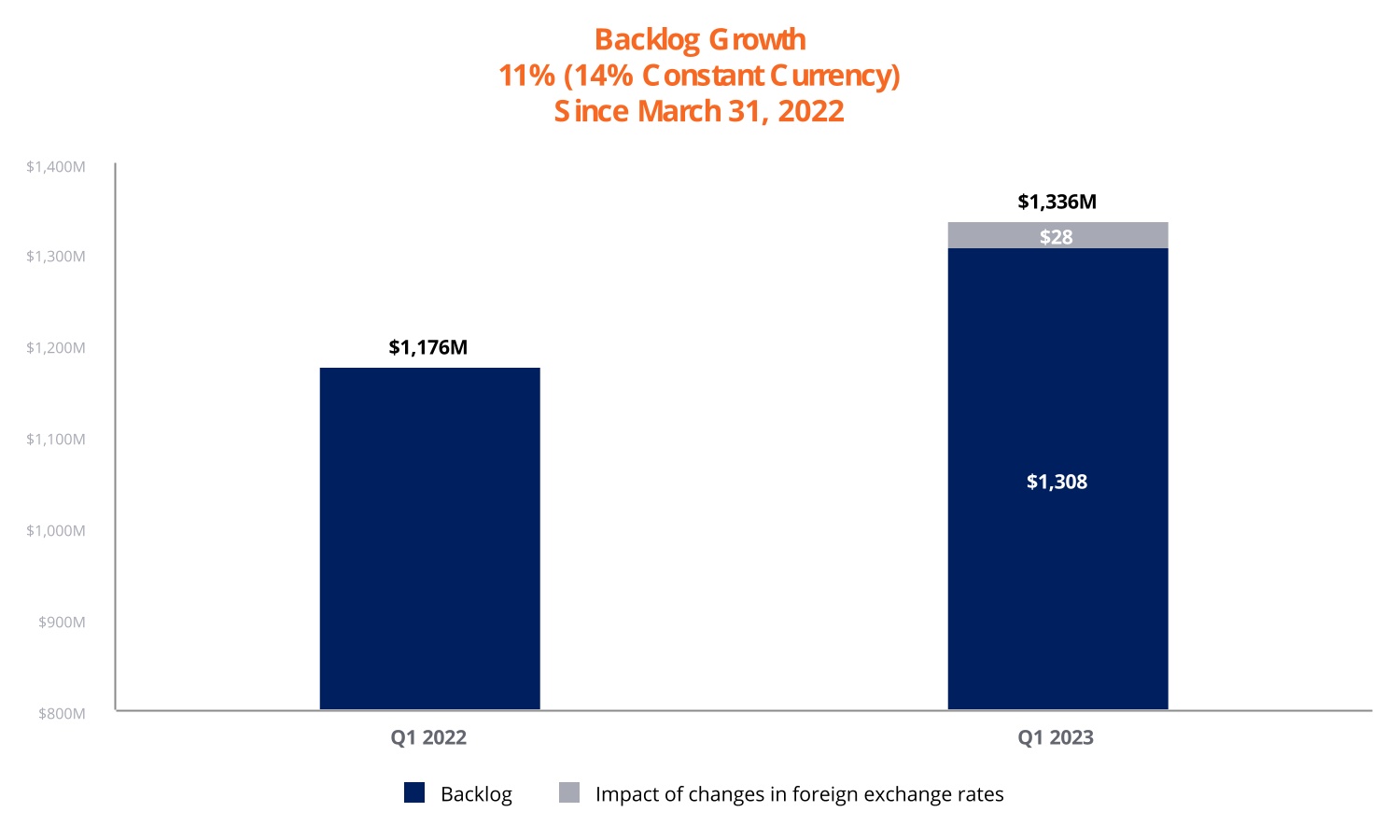

Remaining performance obligations (“Backlog”)

Reconciliation of GAAP Backlog and Constant Currency Backlog

| (in millions, except percentages) | Q1 2023 | 1 Year Growth Rate | |||||||||

| Backlog | $ | 1,308 | 11 | % | |||||||

| Impact of changes in foreign exchange rates | 28 | 3 | % | ||||||||

| Backlog - Constant Currency | $ | 1,336 | 14 | % | |||||||

Constant currency Backlog is calculated by applying the Q1 2022 foreign exchange rates to all periods shown.

We believe that non-GAAP financial measures help investors understand our core operating results and prospects, consistent with how management measures and forecasts our performance without the effect of often one-time charges and other items outside our normal operations. The supplementary non-GAAP financial measures are not meant to be superior to or a substitute for financial measures prepared under U.S. GAAP.

22

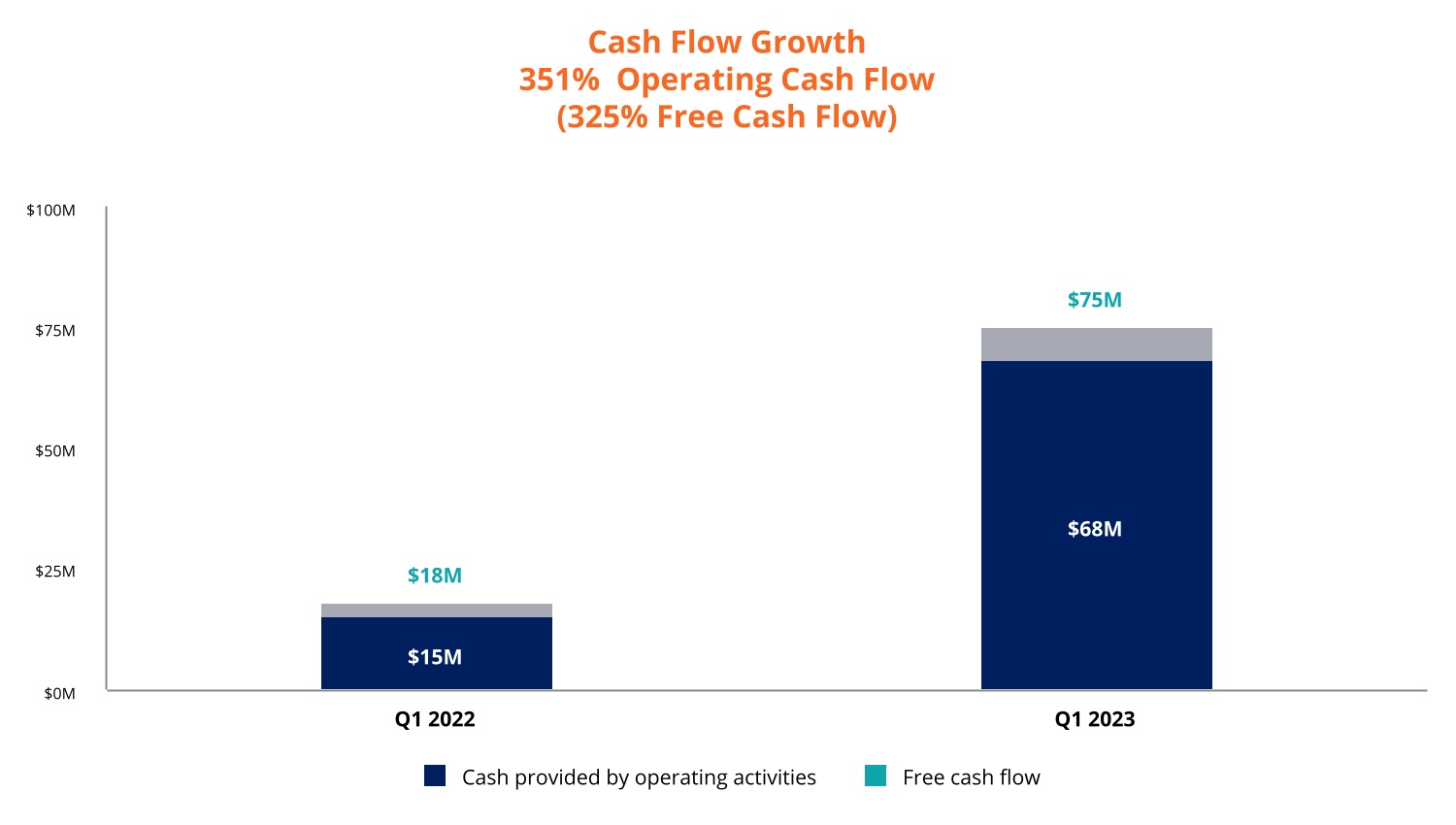

Free cash flow (1)

| (in thousands, except percentages) | Three Months Ended March 31, | ||||||||||||||||

| 2023 | 2022 | Change | |||||||||||||||

| Cash provided by operating activities | $ | 68,107 | $ | 15,116 | 351 | % | |||||||||||

| Investment in property and equipment | (11,487) | (6,657) | |||||||||||||||

| Legal fees | 1,515 | 6,887 | |||||||||||||||

| Restructuring | 14,458 | — | |||||||||||||||

| Interest on convertible senior notes | 2,250 | 2,250 | |||||||||||||||

| Free cash flow | $ | 74,843 | $ | 17,596 | 325 | % | |||||||||||

| Total revenue | $ | 325,472 | $ | 376,307 | |||||||||||||

| Free cash flow margin | 23 | % | 5 | % | |||||||||||||

(1) We believe that non-GAAP financial measures help investors understand our core operating results and prospects, consistent with how management measures and forecasts our performance without the effect of often one-time charges and other items outside our normal operations. The supplementary non-GAAP financial measures are not meant to be superior to or a substitute for financial measures prepared under U.S. GAAP. Our non-GAAP free cash flow measures reflect the following adjustments:

•Investment in property and equipment: Investment in property and equipment fluctuates in amount and frequency and is significantly affected by the timing and size of investments in our facilities. We believe excluding these amounts provides a useful comparison of our operational performance in different periods.

•Legal fees: Includes legal and related fees arising from proceedings outside of the ordinary course of business. We believe excluding these amounts from our non-GAAP financial measures is useful to investors as the disputes giving rise to them are not representative of our core business operations and ongoing operational performance.

•Restructuring: We have excluded restructuring from our non-GAAP financial measures. Restructuring fluctuates in amount and frequency and is significantly affected by the timing and size of our restructuring activities. We believe excluding the impact from our non-GAAP financial measures is useful to investors as these amounts are not representative of our core business operations and ongoing operational performance.

•Interest on convertible senior notes: In February 2020, we issued convertible senior notes, due March 1, 2025, in a private placement. We believe excluding the interest payments provides a useful comparison of our operational performance in different periods.

23

CRITICAL ACCOUNTING POLICIES

Management’s Discussion and Analysis of Financial Condition and Results of Operations is based upon our unaudited condensed consolidated financial statements, which have been prepared following accounting principles generally accepted in the United States of America (“U.S.”) and the rules and regulations of the SEC for interim financial reporting. Preparing these financial statements requires us to make estimates and judgments that affect the reported amounts of assets, liabilities, revenues, expenses, and the related disclosure of contingent assets and liabilities. We base our estimates and judgments on historical experience, knowledge of current conditions, and expectations of what could occur in the future given the available information.

For more information about our critical accounting policies, we encourage you to read the discussion in the following locations in our Annual Report on Form 10-K for the year ended December 31, 2022:

•“Critical Accounting Estimates and Significant Judgments” in Item 7; and

•“Note 2. Significant Accounting Policies” in Item 8.

There have been no other significant changes to our critical accounting policies as disclosed in our Annual Report on Form 10-K for the year ended December 31, 2022.

RESULTS OF OPERATIONS

Revenue

Subscription transition

We are transitioning our business to sell software primarily through subscription arrangements.

This transition has impacted revenue growth as revenue from subscription service arrangements, which includes Pega Cloud and maintenance, is typically recognized over the contract term, while revenue from license sales is recognized when the license rights become effective, typically upfront.

| (Dollars in thousands) | Three Months Ended March 31, | Change | ||||||||||||||||||||||||

| 2023 | 2022 | |||||||||||||||||||||||||

| Pega Cloud | $ | 107,879 | 33 | % | $ | 90,317 | 24 | % | $ | 17,562 | 19 | % | ||||||||||||||

| Maintenance | 79,630 | 25 | % | 79,716 | 21 | % | (86) | — | % | |||||||||||||||||

| Subscription services | 187,509 | 58 | % | 170,033 | 45 | % | 17,476 | 10 | % | |||||||||||||||||

| Subscription license | 84,527 | 26 | % | 137,533 | 37 | % | (53,006) | (39) | % | |||||||||||||||||

| Subscription | 272,036 | 84 | % | 307,566 | 82 | % | (35,530) | (12) | % | |||||||||||||||||

| Perpetual license | 403 | — | % | 7,440 | 2 | % | (7,037) | (95) | % | |||||||||||||||||

| Consulting | 53,033 | 16 | % | 61,301 | 16 | % | (8,268) | (13) | % | |||||||||||||||||

| $ | 325,472 | 100 | % | $ | 376,307 | 100 | % | $ | (50,835) | (14) | % | |||||||||||||||

The revenue changes in the three months ended March 31, 2023 generally reflect the impact of our subscription transition. Other factors impacting our revenue include:

•The decrease in subscription license revenue in the three months ended March 31, 2023 was primarily due to several large software license contracts recognized in revenue in the three months ended March 31, 2022.

•The decrease in consulting revenue in the three months ended March 31, 2023 was primarily due to a decrease in billable hours and realization rates.

Gross profit

| (Dollars in thousands) | Three Months Ended March 31, | Change | ||||||||||||||||||||||||

| 2023 | 2022 | |||||||||||||||||||||||||

| Pega Cloud | $ | 77,629 | 72 | % | $ | 63,418 | 70 | % | $ | 14,211 | 22 | % | ||||||||||||||

| Maintenance | 73,016 | 92 | % | 74,585 | 94 | % | (1,569) | (2) | % | |||||||||||||||||

| Subscription services | 150,645 | 80 | % | 138,003 | 81 | % | 12,642 | 9 | % | |||||||||||||||||

| Subscription license | 83,808 | 99 | % | 136,911 | 100 | % | (53,103) | (39) | % | |||||||||||||||||

| Subscription | 234,453 | 86 | % | 274,914 | 89 | % | (40,461) | (15) | % | |||||||||||||||||

| Perpetual license | 400 | 99 | % | 7,406 | 100 | % | (7,006) | (95) | % | |||||||||||||||||

| Consulting | (7,315) | (14) | % | 5,790 | 9 | % | (13,105) | * | ||||||||||||||||||

| $ | 227,538 | 70 | % | $ | 288,110 | 77 | % | $ | (60,572) | (21) | % | |||||||||||||||

* not meaningful

The gross profit percent changes in the three months ended March 31, 2023 were primarily due to a shift in the revenue mix.

24

•The increase in Pega Cloud gross profit percent in the three months ended March 31, 2023 was primarily due to cost-efficiency gains as Pega Cloud continues to grow and scale.

•The decrease in maintenance gross profit percent in the three months ended March 31, 2023 was primarily due to an increase in compensation and benefits due to increased headcount.

•The decrease in consulting gross profit percent in the three months ended March 31, 2023 was due to a decrease in realization rates and consultant utilization.

Operating expenses

| (Dollars in thousands) | Three Months Ended March 31, | Change | ||||||||||||||||||||||||

| 2023 | 2022 | |||||||||||||||||||||||||

| % of Revenue | % of Revenue | |||||||||||||||||||||||||

| Selling and marketing | $ | 149,797 | 46 | % | $ | 162,236 | 43 | % | $ | (12,439) | (8) | % | ||||||||||||||

| Research and development | $ | 75,376 | 23 | % | $ | 71,490 | 19 | % | $ | 3,886 | 5 | % | ||||||||||||||

| General and administrative | $ | 23,110 | 7 | % | $ | 35,764 | 10 | % | $ | (12,654) | (35) | % | ||||||||||||||

| Restructuring | $ | 1,461 | — | $ | — | — | $ | 1,461 | 100 | % | ||||||||||||||||

•The decrease in selling and marketing in the three months ended March 31, 2023 was primarily due to a decrease in compensation and benefits of $12.2 million.

•The increase in research and development in the three months ended March 31, 2023 was primarily due to an increase in compensation and benefits of $2.5 million, attributable to increases in headcount and incentive compensation. The increase in headcount reflects additional investments in developing our solutions.

•The decrease in general and administrative in the three months ended March 31, 2023 was primarily due to a decrease in legal fees and related expenses arising from litigation proceedings outside the ordinary course of business of $15.9 million. We expect to continue to incur additional costs for these proceedings. See "Note 15. Commitments and Contingencies" in Part I, Item 1 of this Quarterly Report and “Risk Factors” in Part I, Item 1A of our Annual Report for the year ended December 31, 2022.

•The increase in restructuring in the three months ended March 31, 2023 was primarily due to an impairment of $1.2 million on our operating lease right of use assets primarily due to the closure of leased office space in Poland.

Other income and expenses

| (Dollars in thousands) | Three Months Ended March 31, | Change | ||||||||||||||||||

| 2023 | 2022 | |||||||||||||||||||

| Foreign currency transaction (loss) gain | $ | (2,675) | $ | 2,876 | $ | (5,551) | * | |||||||||||||

| Interest income | 1,485 | 207 | 1,278 | 617 | % | |||||||||||||||

| Interest expense | (1,918) | (1,946) | 28 | 1 | % | |||||||||||||||

| Gain (loss) on capped call transactions | 3,206 | (30,560) | 33,766 | * | ||||||||||||||||

| Other income, net | 6,583 | 2,741 | 3,842 | 140 | % | |||||||||||||||

| $ | 6,681 | $ | (26,682) | $ | 33,363 | * | ||||||||||||||

* not meaningful

•The decrease in foreign currency transaction (loss) gain in the three months ended March 31, 2023 was primarily due to the impact of fluctuations in foreign currency exchange rates associated with foreign currency-denominated cash and receivables held by our subsidiary in the United Kingdom.

•The increase in interest income in the three months ended March 31, 2023 was primarily due to an increase in market interest rates.

•The change in gain (loss) on capped call transactions in the three months ended March 31, 2023 was due to fair value adjustments for our capped call transactions.

•The increase in other income, net in the three months ended March 31, 2023 was due to a gain from the repurchase of convertible senior notes and from our venture investments portfolio.

25

Provision for (benefit from) income taxes

| Three Months Ended March 31, | |||||||||||

| (Dollars in thousands) | 2023 | 2022 | |||||||||

| Provision for (benefit from) income taxes | $ | 5,249 | $ | (7,683) | |||||||

| Effective income tax rate | (34) | % | 95 | % | |||||||

The effective income tax rate in the three months ended March 31, 2023 was impacted by the valuation allowance on our U.S. and U.K. deferred tax assets and current taxes payable in the U.S. as a result of projecting taxable income that cannot be fully offset by net operating losses and available tax credits.

LIQUIDITY AND CAPITAL RESOURCES

| Three Months Ended March 31, | |||||||||||

| (in thousands) | 2023 | 2022 | |||||||||

| Cash provided by (used in): | |||||||||||

| Operating activities | $ | 68,107 | $ | 15,116 | |||||||

| Investing activities | (14,413) | (6,082) | |||||||||

| Financing activities | (29,372) | (35,918) | |||||||||

| Effect of exchange rate changes on cash, cash equivalents, and restricted cash | 782 | (310) | |||||||||

| Net increase (decrease) in cash, cash equivalents, and restricted cash | $ | 25,104 | $ | (27,194) | |||||||

(in thousands) | March 31, 2023 | December 31, 2022 | |||||||||

Held by U.S. entities | $ | 229,214 | $ | 248,389 | |||||||

Held by foreign entities | 94,668 | 48,832 | |||||||||

Total cash, cash equivalents, and marketable securities | $ | 323,882 | $ | 297,221 | |||||||

We believe that our current cash, cash flow from operations, borrowing capacity, and ability to engage in capital market transactions will be sufficient to fund our operations, stock repurchases, and quarterly cash dividends for at least the next 12 months and to meet our known long-term cash requirements. Whether these resources are adequate to meet our liquidity needs beyond that period will depend on our future growth, operating results, and the investments needed to support our operations. We may utilize available funds or seek external financing if we require additional capital resources.

If it becomes necessary or desirable to repatriate foreign funds, we may be required to pay federal, state, and local income and foreign withholding taxes upon repatriation. However, due to the complexity of income tax laws and regulations, it is impracticable to estimate the amount of taxes we would have to pay.

Operating activities

We are transitioning our business to sell software primarily through subscription arrangements. This transition has impacted and is expected to continue impacting our billings and cash collections. Subscription licenses and services are typically billed and collected over the contract term, while perpetual license arrangements are generally billed and collected upfront when the license rights become effective.

The change in cash provided by operating activities in the three months ended March 31, 2023 was primarily due to our subscription transition and improved client collections. In addition, in the three months ended March 31, 2023 and 2022, we paid $1.5 million and $6.9 million in legal fees and related expenses arising from proceedings that originated outside of the ordinary course of business. We expect to continue to incur additional costs for these proceedings. See "Note 15. Commitments and Contingencies" in Part I, Item 1 of this Quarterly Report for additional information.

Investing activities

The change in cash (used in) investing activities in the three months ended March 31, 2023 was primarily driven by an increase in office space-related capital expenditures.

26

Financing activities

Debt financing

In February 2020, we issued $600 million in aggregate principal amount of convertible senior notes, which mature on March 1, 2025. In the three months ended March 31, 2023, we paid $29.9 million to repurchase $33 million in aggregate principal amount of convertible senior notes. As of March 31, 2023, we had $567 million in aggregate principal amount of convertible senior notes outstanding.

See "Note 8. Debt" in Part I, Item 1 of this Quarterly Report for additional information.

In November 2019, and as since amended, we entered into a five-year $100 million senior secured revolving credit agreement (the “Credit Facility”) with PNC Bank, National Association. As of March 31, 2023, we had no outstanding cash borrowings under the Credit Facility but had $27.3 million in outstanding letters of credit which reduces our available borrowing capacity. See "Note 8. Debt" in Part I, Item 1 of this Quarterly Report for additional information.

Stock repurchase program

Changes in the remaining stock repurchase authority:

| (in thousands) | Three Months Ended March 31, 2023 | ||||

| December 31, 2022 | $ | 58,075 | |||

Authorizations (1) | — | ||||

| March 31, 2023 | $ | 58,075 | |||

(1) On April 25, 2023, our Board of Directors extended the expiration date of our current share repurchase program to June 30, 2024, and the amount of stock we are authorized to repurchase has been increased to $60 million.

Common stock repurchases

| Three Months Ended March 31, | |||||||||||||||||||||||

| 2023 | 2022 | ||||||||||||||||||||||

| (in thousands) | Shares | Amount | Shares | Amount | |||||||||||||||||||

| Repurchases paid | — | $ | — | 242 | $ | 22,583 | |||||||||||||||||

| Stock repurchase program | — | — | 242 | 22,583 | |||||||||||||||||||

| Tax withholdings for net settlement of equity awards | 27 | 1,107 | 141 | 12,128 | |||||||||||||||||||

| 27 | $ | 1,107 | 383 | $ | 34,711 | ||||||||||||||||||

In the three months ended March 31, 2023 and 2022, instead of receiving cash from the equity holders, we withheld shares with a value of $0.6 million and $6.1 million, respectively, for the exercise price of options. These amounts are not included in the table above.

Dividends

We intend to pay a quarterly cash dividend of $0.03 per share. However, the Board of Directors may terminate or modify the dividend program without prior notice.

| Three Months Ended March 31, | |||||||||||

| (in thousands) | 2023 | 2022 | |||||||||

| Dividend payments to stockholders | $ | 2,474 | $ | 2,454 | |||||||

Contractual obligations

As of March 31, 2023, our contractual obligations were:

| Payments due by period | |||||||||||||||||||||||||||||||||||||||||||||||

| (in thousands) | Remainder of 2023 | 2024 | 2025 | 2026 | 2027 | 2028 and after | Other | Total | |||||||||||||||||||||||||||||||||||||||

Convertible senior notes (1) | $ | 1,772 | $ | 4,253 | $ | 569,126 | $ | — | $ | — | $ | — | $ | — | $ | 575,151 | |||||||||||||||||||||||||||||||

Purchase obligations (2) | 98,303 | 117,729 | 127,367 | 131,146 | 133,500 | 14 | — | 608,059 | |||||||||||||||||||||||||||||||||||||||

| Operating lease obligations | 14,003 | 17,642 | 14,562 | 10,917 | 9,863 | 39,380 | — | 106,367 | |||||||||||||||||||||||||||||||||||||||

| Investment commitments | 1,000 | — | — | — | — | — | — | 1,000 | |||||||||||||||||||||||||||||||||||||||

Liability for uncertain tax positions (3) | — | — | — | — | — | — | 3,578 | 3,578 | |||||||||||||||||||||||||||||||||||||||

| $ | 115,078 | $ | 139,624 | $ | 711,055 | $ | 142,063 | $ | 143,363 | $ | 39,394 | $ | 3,578 | $ | 1,294,155 | ||||||||||||||||||||||||||||||||

(1) Includes principal and interest.

(2) Represents the fixed or minimum amounts due under purchase obligations for hosting services and sales and marketing programs.

(3) We cannot reasonably estimate the timing of this cash outflow due to uncertainties in the timing of the effective settlement of tax positions.

27

ITEM 3. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

Market risk is the risk of loss from adverse changes in financial market prices and rates.

Foreign currency exposure

Translation risk

Our international operations’ operating expenses are primarily denominated in foreign currencies. However, our international sales are also primarily denominated in foreign currencies, which partially offsets our foreign currency exposure.

A hypothetical 10% strengthening in the U.S. dollar against other currencies would have resulted in:

| Three Months Ended March 31, | |||||||||||

| 2023 | 2022 | ||||||||||

| (Decrease) increase in revenue | (4) | % | (3) | % | |||||||

| Increase (decrease) in net income | 1 | % | 186 | % | |||||||

Remeasurement risk

We incur transaction gains and losses from the remeasurement of monetary assets and liabilities denominated in currencies other than the functional currency of the entities in which they are recorded.

We are primarily exposed to changes in foreign currency exchange rates associated with the Australian dollar, Euro, and U.S. dollar-denominated cash, cash equivalents, receivables, and intercompany balances held by our U.K. subsidiary, a British pound functional entity.