UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT

OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-07537

Name of Registrant: Royce Capital Fund

Address of Registrant: 745 Fifth Avenue

New York, NY 10151

| Name and address of agent for service: | John E. Denneen, Esq. 745 Fifth Avenue New York, NY 10151 |

Registrant's telephone number, including area code: (212) 508-4500

Date of fiscal year end: December 31, 2018

Date of reporting period: January 1, 2018 – June 30, 2018

Item 1. Reports to Shareholders.

|

| JUNE 30, 2018 | ||

| 2018 Semiannual | ||

| Review and Report to Shareholders | ||

| Royce Capital Fund– | |||

| Micro-Cap Portfolio | |||

| Royce Capital Fund– | |||

| Small-Cap Portfolio | |||

| roycefunds.com |  |

||

| Table of Contents | |||

| Semiannual Review | |||

| Letter to Our Shareholders | 1 | ||

| Performance and Expenses | 5 | ||

| Semiannual Report to Shareholders | |||

| Managers’ Discussions of Fund Performance and Schedules of Investments | |||

Royce Capital Fund–Micro-Cap Portfolio |

6 | ||

Royce Capital Fund–Small-Cap Portfolio |

12 | ||

| Financial Statements | 16 | ||

| Notes to Financial Statements | 20 | ||

| Understanding Your Fund’s Expenses | 24 | ||

| Trustees and Officers | 25 | ||

| Board Approval of Investment Advisory Agreement | 26 | ||

| Notes to Performance and Other Important Information | 27 |

| This page is not part of the Royce Capital Fund 2018 Semiannual Report to Shareholders |

Letter to Our Shareholders

|

| Small-Cap is represented by Russell 2000; Small-Cap Value is represented by Russell 2000 Value, Small-Cap Growth is represented by Russell 2000 Growth, Large-Cap is represented by Russell 1000, Micro-Cap is represented by Russell Microcap. For details on The Royce Funds’ performance in the period, please turn to the Managers’ Discussions that begin on page 8. Past performance is no guarantee of future results. |

| 1 Not annualized. |

| This page is not part of the Royce Capital Fund 2018 Semiannual Report to Shareholders | 1 |

LETTER TO OUR SHAREHOLDERS

| 2 | This page is not part of the Royce Capital Fund 2018 Semiannual Report to Shareholders |

LETTER TO OUR SHAREHOLDERS

| This page is not part of the Royce Capital Fund 2018 Semiannual Report to Shareholders | 3 |

LETTER TO OUR SHAREHOLDERS

| Sincerely, |

|

|

|

||

| Charles M. Royce | Christopher D. Clark | Francis D. Gannon | ||

| Chairman, | Chief Executive Officer, and | Co-Chief Investment Officer, | ||

| Royce & Associates, LP | Co-Chief Investment Officer, | Royce & Associates, LP | ||

| Royce & Associates, LP | ||||

| July 30, 2018 |

| 4 | This page is not part of the Royce Capital Fund 2018 Semiannual Report to Shareholders |

Performance and Expenses

| Performance and Expenses |

| As of June 30, 2018 |

| YTD1 | 1-YR | 3-YR | 5-YR | 10-YR | 15-YR | 20-YR | SINCE INCEPTION (12/27/96) |

ANNUAL OPERATING EXPENSES (%) |

||||||||||||||

| Royce Capital Fund–Micro-Cap Portfolio | 10.31 | 14.08 | 7.11 | 6.55 | 5.34 | 8.04 | 9.63 | 10.21 | 1.42 | |||||||||||||

| Royce Capital Fund–Small-Cap Portfolio | 7.06 | 17.72 | 6.48 | 8.29 | 7.81 | 10.00 | 10.13 | 10.80 | 1.08 | |||||||||||||

INDEX |

||||||||||||||||||||||

| Russell Microcap Index | 10.71 | 20.21 | 10.49 | 12.78 | 10.63 | 9.44 | N/A | N/A | N/A | |||||||||||||

| Russell 2000 Index | 7.66 | 17.57 | 10.96 | 12.46 | 10.60 | 10.50 | 8.03 | N/A | N/A | |||||||||||||

| 1 Not annualized. | ||||||||||||||||||||||

Important Performance, Expense, and Risk Information

All performance information in this Review and Report reflects past performance, is presented on a total return basis, reflects the reinvestment of distributions, and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, so that shares may be worth more or less than their original cost when redeemed. Current performance may be higher or lower than performance quoted and may be obtained at www.roycefunds.com. The Funds’ total returns do not reflect any deduction for charges or expenses of the variable contracts investing in the Funds. All performance and expense information reflects the result for each Fund’s Investment Class Shares. Gross annual operating expenses reflect each Fund’s gross total annual operating expenses and include management fees, operating expenses, and any applicable acquired fund fees and expenses. Net annual operating expenses reflect contractual fee waivers and/or expense reimbursements. All expense information is reported as of each fund’s most current prospectus. Royce & Associates has contractually agreed to waive fees and/or reimburse operating expenses, excluding brokerage commissions, taxes, interest litigation expenses, acquired fund fees and expenses, and other expenses not borne in the ordinary cost of business, to the extent necessary to maintain net operating expenses at or below 1.33% for Royce Capital Fund–Micro-Cap Portfolio, and at or below 1.08% for Royce Capital Fund–Small-Cap Portfolio through April 30, 2019. Acquired fund fees and expenses reflect the estimated amount of fees and expenses incurred indirectly by the Fund through its investment in mutual funds, hedge funds, private equity funds, and other investment companies.

Service Class Shares bear an annual distribution expense that is not borne by the Investment Class; if those expenses were reflected, total returns would have been lower. Royce Micro-Cap Portfolio invests primarily in micro-cap companies while Royce Small-Cap Portfolio invests primarily in small-cap companies. Investments in micro-cap and small-cap companies may involve considerably more risk than investments in securities of larger-cap companies. (Please see “Primary Risks for Fund Investors” in the prospectus.) Each series of Royce Capital Fund may invest up to 25% of its net assets in foreign securities. Investments in foreign securities may involve political, economic, currency, and other risks not encountered in U.S. investments. (Please see “Investing in Foreign Securities” in the prospectus.) As of 6/30/18, Royce Small-Cap Portfolio invested a significant portion of its assets in a limited number of stocks, which may involve considerably more risk than a more broadly diversified portfolio because a decline in the value of any one of these stocks would cause the Portfolio’s overall value to decline to a greater degree. Royce Micro-Cap Portfolio’s broadly diversified portfolio does not ensure a profit or guarantee against loss. (Please see “Primary Risks for Fund Investors” in the prospectus.) This Review and Report must be preceded or accompanied by a prospectus. Please read the prospectus carefully before investing or sending money. Russell Investment Group is the source and owner of the trademarks, service marks, and copyrights related to the Russell Indexes. Russell® is a trademark of Russell Investment Group. The Russell Microcap Index includes 1,000 of the smallest securities in the small-cap Russell 2000 Index along with the next smallest eligible securities as determined by Russell. The Russell 2000 Index is an unmanaged, capitalization-weighted index of domestic small-cap stocks. It measures the performance of the 2,000 smallest publicly traded U.S. companies in the Russell 3000 Index. The performance of an index does not represent exactly any particular investment, as you cannot invest directly in an index. Distributor: Royce Fund Services, LLC.

| This page is not part of the Royce Capital Fund 2018 Semiannual Report to Shareholders | 5 |

| MANAGERS’ DISCUSSION |

| Royce Capital Fund–Micro-Cap Portfolio (RCM) |

|

| Jim Stoeffel Brendan Hartman |

| FUND PERFORMANCE |

| Royce Capital Fund–Micro Cap Portfolio increased 10.3% for the year-to-date period ended June 30, 2018, ahead of the small-cap Russell 2000 Index, which was up 7.7%, but narrowly behind its benchmark, the Russell Microcap Index, which increased 10.7% for the same period. Micro-cap stocks were the top-performing U.S. asset class in the first half of the year, as the greater reliance on U.S. growth left small- and micro-cap stocks better positioned for superior performance relative to large-caps in the first half of the year. |

| WHAT WORKED... AND WHAT DIDN’T |

| The Fund boasted strong sector contributions from Information Technology, Health Care, and Consumer Discretionary, while two healthcare companies made strong positive impacts at the position level. Tactile Systems, which makes medical devices used to treat lymphedema, grew its sales force and introduced new products, such as its new system targeted at head and neck lymphedema. Seeing low market penetration and a favorable competitive environment, we continued to hold shares after making modest trims as its stock price rose. Medical device company Surmodics, which specializes in coronary stents and catheters, was another notable pick for the portfolio. A recent agreement gave Abbot Laboratories exclusive global commercialization rights for the company’s SurVeil drug. We saw an extended pipeline of interesting products and therefore maintained our position in the company’s shares. |

| We reduced our stake in Profire Energy, an oilfield technology specialist in burner management systems that was the portfolio’s top contributor overall. It benefited from the resurgence in oil field activity fueled by higher oil prices. We held our stock in Attunity, a leading provider of data management software, because we saw an increased adoption of its core software platform across an ever increasing number of enterprises. The company’s software addresses new paradigms in data management, which we believed were in the very early stages of adoption. Stoneridge, which supplies electrical components to cars and trucks, was winning new business across several product lines, such as its MirrorEye camera system that offers safety and fuel economy benefits by replacing side mirrors on trucks. We sold a portion of our shares as its share price rose steadily. We also saw positive contributions to return on these positions in relation to the Russell Microcap. |

| Thanks to effective stock selection, Consumer Discretionary and Information Technology were the areas that contributed most to performance versus the benchmark, while Energy and Financials were the largest detractors—both due to poor stock picking. One position significantly detracted from performance on both an absolute and relative basis: Basic Energy Services, a leading provider of well site services in the oil and gas industry, saw increased pricing pressure as well as project delays in certain markets. We increased our stake slightly within the first six months of the year based on the belief that these pressures were transitory given ongoing strength in underlying energy prices. Gulf Island Fabrication makes specialized structures and marine vessels used in the energy sector. Its shares have been pressured as its off-shore oil well platform business remained sluggish while it also experienced cost overruns on a major marine vessel contract. |

| Atlas Financial, which provides insurance for taxis, limos, ride share services, and paratransit transportation firms, was another impactful detractor on an absolute and relative basis. For a second year in a row, Atlas recorded a surprise fourth-quarter loss due to an increase in loss reserves for prior year accidents. Our belief that the first surprise loss was an anomaly and that the company’s market niche could provide high returns on equity was proven incorrect. We sold all of our shares as a result. Shares of Paratek Pharmaceuticals fell due to concerns over incremental FDA approval scrutiny, the potential for a slow commercial ramp up, and a capital raise in April. We increased our position in the first half because of the large market opportunity for a new antibiotic associated with the increased human resistance to older varieties. We chose to trim our position in U.S. Concrete, which saw its shares pressured as poor weather impacted certain large markets and the company had some early execution shortfalls digesting a large acquisition. |

| Top Contributors to Performance | ||||

| Year-to-Date Through 6/30/18 (%)1 | ||||

| Profire Energy | 0.60 | |||

| Tactile Systems Technology | 0.58 | |||

| Surmodics | 0.58 | |||

| Attunity | 0.54 | |||

| Stoneridge | 0.49 | |||

| 1 Includes dividends | ||||

| Top Detractors from Performance | ||||

| Year-to-Date Through 6/30/18 (%)2 | ||||

| Atlas Financial Holdings | -0.46 | |||

| Basic Energy Services | -0.40 | |||

| U.S. Concrete | -0.29 | |||

| Paratek Pharmaceuticals | -0.27 | |||

| Gulf Island Fabrication | -0.24 | |||

| 2 Net of dividends | ||||

| CURRENT POSITIONING AND OUTLOOK |

| We did not make any major changes to portfolio positioning in the first half of 2018. Despite the increasing uncertainty around trade, we remained generally constructive on the U.S. economy, which supported underlying growth and valuations in our overweight sectors, such as Information Technology, Industrials, and Consumer Discretionary. These sectors were also our largest overweights relative to the Russell Microcap. Health Care, particularly biotechnology, continued to be among our largest underweights by nearly 50%. We remained optimistic about micro-cap stocks in anticipation of an increasingly less restrictive regulatory environment. Considering the accelerated pace of U.S. economic growth, lower corporate tax rates, and the slower pace of global economic growth, we were particularly focused on micro-cap companies that had a disproportionate exposure to the U.S. economy. |

| 6 | Royce Capital Fund 2018 Semiannual Report to Shareholders |

| PERFORMANCE AND PORTFOLIO REVIEW | TICKER SYMBOLS RCMCX RCMSX |

| Performance and Expenses | ||||||||||||||||

| Average Annual Total Return (%) Through 6/30/18 | ||||||||||||||||

| JAN-JUN 20181 | 1-YR | 3-YR | 5-YR | 10-YR | 15-YR | 20-YR | SINCE INCEPTION (12/27/96) | |||||||||

| RCM | 10.31 | 14.08 | 7.11 | 6.55 | 5.34 | 8.04 | 9.63 | 10.21 | ||||||||

| Annual Gross Operating Expenses: 1.47% Annual Net Operating Expenses: 1.42% | ||||||||||||||||

| 1 Not annualized | ||||||||||||||||

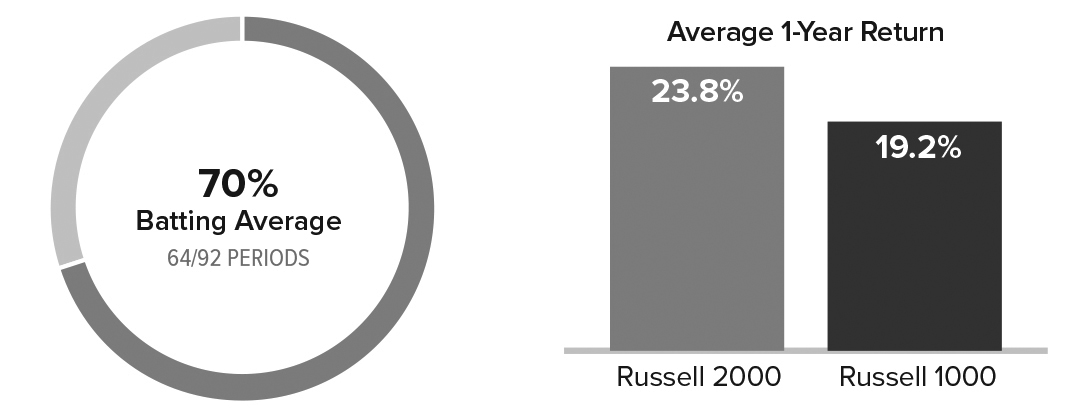

Relative Returns: Monthly Rolling Average Annual Return Periods

| On a monthly rolling basis, the Fund outperformed the Russell Microcap in 57% of all 10-year periods; 58% of all 5-year periods; and 48% of all 1-year periods. |

| PERIODS BEATING THE INDEX | FUND AVG (%)1 | INDEX AVG (%)1 | ||||||||||

| 10-year | 55/97 | 57% | 6.8 | 6.4 | ||||||||

| 5-year | 91/157 | 58% | 7.7 | 8.3 | ||||||||

| 1-year | 99/205 | 48% | 10.4 | 10.8 | ||||||||

The Morningstar Style Map is the Morningstar

Style BoxTM with the center 75% of

fund holdings plotted as the Morningstar

Ownership ZoneTM. The Morningstar Style Box is designed to reveal a

fund’s investment strategy. The Morningstar Ownership Zone provides

detail about a portfolio’s investment style by showing the range of

stock sizes and styles. The Ownership Zone is derived by plotting each

stock in the portfolio within the proprietary Morningstar Style Box.

Over time, the shape and location of a fund's ownership zone may vary.

See page 27 for additional information. |

Value of $10,000

as of 6/30/18 ($)

Includes reinvestment of distributions.

| Top 10 Positions | ||

| % of Net Assets | ||

| AtriCure | 1.2 | |

| Attunity | 1.1 | |

| Stoneridge | 1.1 | |

| Shoe Carnival | 1.1 | |

| Surmodics | 1.1 | |

| CryoLife | 1.1 | |

| PC Connection | 1.0 | |

| Red Lion Hotels | 1.0 | |

| QAD Cl. A | 1.0 | |

| Vishay Precision Group | 1.0 | |

| Portfolio Sector Breakdown | ||

| % of Net Assets | ||

| Information Technology | 19.6 | |

| Industrials | 19.2 | |

| Financials | 15.2 | |

| Consumer Discretionary | 14.3 | |

| Health Care | 11.4 | |

| Energy | 6.3 | |

| Materials | 4.5 | |

| Consumer Staples | 2.4 | |

| Real Estate | 2.4 | |

| Telecommunication Services | 0.6 | |

| Cash and Cash Equivalents | 4.1 | |

| Calendar Year Total Returns (%) | ||

| YEAR | RCM | |

| 2017 | 5.2 | |

| 2016 | 19.7 | |

| 2015 | -12.5 | |

| 2014 | -3.6 | |

| 2013 | 21.0 | |

| 2012 | 7.6 | |

| 2011 | -12.1 | |

| 2010 | 30.1 | |

| 2009 | 57.9 | |

| 2008 | -43.3 | |

| 2007 | 4.0 | |

| 2006 | 21.1 | |

| 2005 | 11.6 | |

| 2004 | 13.8 | |

| 2003 | 49.2 | |

| Upside/Downside Capture Ratios | ||||

| Periods Ended 6/30/18 (%) | ||||

| UPSIDE | DOWNSIDE | |||

| 10-Year | 76 | 99 | ||

| From 6/30/00 (Russell Microcap Inception) |

88 | 77 | ||

| Portfolio Diagnostics | ||

| Fund Net Assets | $195 million | |

| Number of Holdings | 145 | |

| Turnover Rate | 14% | |

| Average Market Capitalization1 | $485 million | |

| Weighted Average P/E Ratio2,3 | 23.6x | |

| Weighted Average P/B Ratio2 | 2.1x | |

| Active Share4 | 90% | |

| U.S. Investments (% of Net Assets) | 84.2% | |

| Non-U.S. Investments (% of Net Assets) | 11.7% | |

| 1 | Geometric Average. This weighted calculation uses each portfolio

holding’s market cap in a way designed to not skew the effect of

very large or small holdings; instead, it aims to better identify

the portfolio’s center, which Royce believes offers a more accurate

measure of average market cap than a simple mean or median. |

| 2 | Harmonic Average. This weighted calculation evaluates a portfolio

as if it were a single stock and measures it overall. It compares the

total market value of the portfolio to the portfolio’s share in the

earnings or book value, as the case may be, of its underlying stocks. |

| 3 | The Fund’s P/E ratio calculation excludes companies with zero or

negative earnings (27% of portfolio holdings as of 6/30/18). |

| 4 | Active Share is the sum of the absolute values of the different

weightings of each holding in the Fund versus each holding in the

benchmark, divided by two. |

| Important Performance and Expense Information

All performance information in this Report reflects past performance, is presented on a total return basis, reflects the reinvestment of distributions, and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, so that shares may be worth more or less than their original cost when redeemed. Current performance may be higher or lower than performance quoted. The Fund’s total returns do not reflect any deduction for charges or expenses of the variable contracts investing in the Fund. Returns as of the most recent month-end may be obtained at www.roycefunds.com. All performance and risk information reflects the result of the Investment Class (its oldest class). Shares of RCM’s Service Class bear an annual distribution expense that is not borne by the Investment Class; if those expenses were reflected, total returns would have been lower. Certain immaterial adjustments were made to the net assets of Royce Capital Fund-Micro-Cap Portfolio at 12/31/17 for financial reporting purposes, and as a result the calendar year total returns based on those net assets values differ from the adjusted net values and calendar year total returns reported in the Financial Highlights. The Fund’s total returns do not reflect any deduction for charges or expenses of the variable contracts investing in the Fund. Gross operating expenses reflect the Fund’s total gross operating expenses for the Investment Class and include management fees, other expenses, and acquired fund fees and expenses. Net operating expenses reflect contractual fee waivers and/or expense reimbursements. All expense information is reported as of the Fund’s most current prospectus. Royce & Associates has contractually agreed, without right of termination, to waive fees and/or reimburse expenses to the extent necessary to maintain the Investment Class’s net annual operating expenses (excluding brokerage commissions, taxes, interest, litigation expenses, acquired fund fees and expenses, and other expenses not borne in the ordinary course of business) at or below 1.33% through April 30, 2019. Acquired fund fees and expenses reflect the estimated amount of the fees and expenses incurred indirectly by the Fund through its investments in mutual funds, hedge funds, private equity funds, and other investment companies. Regarding the “Top Contributors” and “Top Detractors” tables shown above, the sum of all contributors to, and all detractors from, performance for all securities in the portfolio would approximate the Fund’s year-to-date performance for 2018. Upside Capture Ratio measures a manager’s performance in up markets relative to the Fund’s benchmark. It is calculated by measuring the Fund’s performance in quarters when the benchmark went up and dividing it by the benchmark’s return in those quarters. Downside Capture Ratio measures a manager’s performance in down markets relative to the Fund’s benchmark (Russell Microcap). It is calculated by measuring the Fund’s performance in quarters when the benchmark goes down and dividing it by the benchmark’s return in those quarters. |

| Royce Capital Fund 2018 Semiannual Report to Shareholders | 7 |

Schedule of Investments

| Royce Capital Fund - Micro-Cap Portfolio | |||||||

| Common Stocks – 95.9% | |||||||

| SHARES | VALUE | ||||||

| CONSUMER DISCRETIONARY – 14.3% | |||||||

| AUTO COMPONENTS - 3.4% | |||||||

Fox Factory Holding 1 |

33,800 | $ | 1,573,390 | ||||

Standard Motor Products |

31,100 | 1,503,374 | |||||

Stoneridge 1 |

62,100 | 2,182,194 | |||||

Unique Fabricating |

153,300 | 1,339,842 | |||||

| 6,598,800 | |||||||

| HOTELS, RESTAURANTS & LEISURE - 1.9% | |||||||

Del Taco Restaurants 1 |

121,400 | 1,721,452 | |||||

| 13,400 | 177,550 | ||||||

Red Lion Hotels 1 |

161,800 | 1,884,970 | |||||

| 3,783,972 | |||||||

| HOUSEHOLD DURABLES - 1.1% | |||||||

Cavco Industries 1 |

6,404 | 1,329,791 | |||||

| 39,000 | 809,250 | ||||||

| 2,139,041 | |||||||

| INTERNET & DIRECT MARKETING RETAIL - 0.7% | |||||||

Gaia Cl. A 1 |

62,100 | 1,257,525 | |||||

| LEISURE PRODUCTS - 1.7% | |||||||

MCBC Holdings 1 |

59,117 | 1,711,437 | |||||

Nautilus 1 |

106,900 | 1,678,330 | |||||

| 3,389,767 | |||||||

| SPECIALTY RETAIL - 4.2% | |||||||

Build-A-Bear Workshop 1 |

132,500 | 1,007,000 | |||||

Citi Trends |

55,886 | 1,533,512 | |||||

Francesca’s Holdings 1 |

101,400 | 765,570 | |||||

Haverty Furniture |

66,300 | 1,432,080 | |||||

Kirkland’s 1 |

103,000 | 1,198,920 | |||||

Shoe Carnival |

66,700 | 2,164,415 | |||||

| 8,101,497 | |||||||

| TEXTILES, APPAREL & LUXURY GOODS - 1.3% | |||||||

Culp |

30,649 | 752,433 | |||||

Vera Bradley 1 |

129,300 | 1,815,372 | |||||

| 2,567,805 | |||||||

| Total (Cost $19,207,817) | 27,838,407 | ||||||

| CONSUMER STAPLES – 2.4% | |||||||

| BEVERAGES - 0.9% | |||||||

Primo Water 1 |

100,500 | 1,757,745 | |||||

| FOOD PRODUCTS - 1.5% | |||||||

Farmer Bros. 1 |

47,800 | 1,460,290 | |||||

John B. Sanfilippo & Son |

20,900 | 1,556,005 | |||||

| 3,016,295 | |||||||

| Total (Cost $3,811,088) | 4,774,040 | ||||||

| ENERGY – 6.3% | |||||||

| ENERGY EQUIPMENT & SERVICES - 4.9% | |||||||

Basic Energy Services 1 |

72,000 | 799,920 | |||||

Computer Modelling Group |

133,400 | 1,024,866 | |||||

Gulf Island Fabrication |

92,634 | 833,706 | |||||

Independence Contract Drilling 1 |

316,500 | 1,303,980 | |||||

Natural Gas Services Group 1 |

60,800 | 1,434,880 | |||||

Newpark Resources 1 |

158,400 | 1,718,640 | |||||

Profire Energy 1 |

423,729 | 1,432,204 | |||||

Total Energy Services |

123,500 | 1,091,598 | |||||

| 9,639,794 | |||||||

| OIL, GAS & CONSUMABLE FUELS - 1.4% | |||||||

Ardmore Shipping 1 |

205,800 | 1,687,560 | |||||

Panhandle Oil and Gas Cl. A |

53,800 | 1,027,580 | |||||

| 2,715,140 | |||||||

| Total (Cost $11,425,618) | 12,354,934 | ||||||

| FINANCIALS – 15.2% | |||||||

| BANKS - 6.5% | |||||||

Allegiance Bancshares 1 |

31,200 | 1,352,520 | |||||

| 8,782 | 217,354 | ||||||

Blue Hills Bancorp |

76,400 | 1,696,080 | |||||

Brookline Bancorp |

64,200 | 1,194,120 | |||||

Caribbean Investment Holdings 1 |

1,751,547 | 404,531 | |||||

County Bancorp |

50,200 | 1,380,500 | |||||

HarborOne Bancorp 1 |

77,200 | 1,462,168 | |||||

| 7,500 | 211,125 | ||||||

†Investar Holding |

27,500 | 760,375 | |||||

| 1,751,577 | 0 | ||||||

Stewardship Financial |

92,000 | 1,071,800 | |||||

TriState Capital Holdings 1 |

56,072 | 1,463,479 | |||||

Two River Bancorp |

72,400 | 1,385,012 | |||||

| 12,599,064 | |||||||

| CAPITAL MARKETS - 4.4% | |||||||

B. Riley Financial |

57,800 | 1,303,390 | |||||

Canaccord Genuity Group |

291,800 | 1,611,431 | |||||

GAIN Capital Holdings |

141,600 | 1,069,080 | |||||

Gluskin Sheff + Associates |

117,300 | 1,465,079 | |||||

Silvercrest Asset Management Group Cl. A |

103,900 | 1,693,570 | |||||

Westwood Holdings Group |

25,727 | 1,531,786 | |||||

| 8,674,336 | |||||||

| DIVERSIFIED FINANCIAL SERVICES - 0.2% | |||||||

| 1,302,000 | 390,600 | ||||||

| INSURANCE - 1.0% | |||||||

Blue Capital Reinsurance Holdings |

75,292 | 831,977 | |||||

| 34,900 | 1,129,015 | ||||||

| 1,960,992 | |||||||

| THRIFTS & MORTGAGE FINANCE - 3.1% | |||||||

Federal Agricultural Mortgage |

17,700 | 1,583,796 | |||||

PCSB Financial |

70,400 | 1,398,848 | |||||

Territorial Bancorp |

45,900 | 1,422,900 | |||||

Western New England Bancorp |

139,954 | 1,539,494 | |||||

| 5,945,038 | |||||||

| Total (Cost $26,988,927) | 29,570,030 | ||||||

| HEALTH CARE – 11.4% | |||||||

| BIOTECHNOLOGY - 2.1% | |||||||

BioSpecifics Technologies 1 |

31,500 | 1,413,090 | |||||

Progenics Pharmaceuticals 1 |

173,800 | 1,397,352 | |||||

Zealand Pharma 1 |

92,658 | 1,219,958 | |||||

| 4,030,400 | |||||||

| HEALTH CARE EQUIPMENT & SUPPLIES - 5.6% | |||||||

AtriCure 1 |

84,600 | 2,288,430 | |||||

| 132,900 | 1,475,190 | ||||||

CryoLife 1 |

74,889 | 2,085,659 | |||||

OrthoPediatrics Corporation 1 |

41,200 | 1,097,568 | |||||

Surmodics 1 |

38,078 | 2,101,905 | |||||

| 34,800 | 1,809,600 | ||||||

| 10,858,352 | |||||||

| LIFE SCIENCES TOOLS & SERVICES - 2.0% | |||||||

Harvard Bioscience 1 |

321,568 | 1,720,389 | |||||

| 8 | Royce Capital Fund 2018 Semiannual Report to Shareholders | THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS |

| June 30, 2018 (unaudited) |

| Royce Capital Fund - Micro-Cap Portfolio (continued) | |||||||

| SHARES | VALUE | ||||||

| HEALTH CARE (continued) | |||||||

| LIFE SCIENCES TOOLS & SERVICES (continued) | |||||||

NeoGenomics 1 |

99,400 | $ | 1,303,134 | ||||

| 67,800 | 973,608 | ||||||

| 3,997,131 | |||||||

| PHARMACEUTICALS - 1.7% | |||||||

BioDelivery Sciences International 1 |

411,700 | 1,214,515 | |||||

| 134,400 | 1,076,544 | ||||||

Paratek Pharmaceuticals 1 |

78,600 | 801,720 | |||||

| 246,900 | 0 | ||||||

| 75,800 | 270,606 | ||||||

| 3,363,385 | |||||||

| Total (Cost $14,554,300) | 22,249,268 | ||||||

| INDUSTRIALS – 19.2% | |||||||

| AEROSPACE & DEFENSE - 1.5% | |||||||

Astronics Corporation 1 |

28,545 | 1,026,764 | |||||

CPI Aerostructures 1 |

174,344 | 1,830,612 | |||||

| 2,857,376 | |||||||

| COMMERCIAL SERVICES & SUPPLIES - 1.7% | |||||||

Acme United |

45,065 | 935,099 | |||||

Heritage-Crystal Clean 1 |

48,834 | 981,563 | |||||

Viad Corporation |

24,100 | 1,307,425 | |||||

| 3,224,087 | |||||||

| CONSTRUCTION & ENGINEERING - 1.2% | |||||||

| 50,000 | 658,500 | ||||||

Northwest Pipe 1 |

86,700 | 1,679,379 | |||||

| 2,337,879 | |||||||

| ELECTRICAL EQUIPMENT - 1.3% | |||||||

| 169,500 | 1,186,500 | ||||||

Encore Wire |

30,100 | 1,428,245 | |||||

| 2,614,745 | |||||||

| INDUSTRIAL CONGLOMERATES - 0.6% | |||||||

Raven Industries |

32,900 | 1,265,005 | |||||

| MACHINERY - 7.8% | |||||||

Alimak Group |

84,600 | 1,295,908 | |||||

Exco Technologies |

156,700 | 1,059,645 | |||||

FreightCar America 1 |

79,691 | 1,338,012 | |||||

Global Brass and Copper Holdings |

39,900 | 1,250,865 | |||||

Graham Corporation |

67,020 | 1,729,786 | |||||

Greenbrier Companies (The) |

21,600 | 1,139,400 | |||||

Kadant |

16,331 | 1,570,226 | |||||

| 97,600 | 1,737,280 | ||||||

Lindsay Corporation |

16,700 | 1,619,733 | |||||

Lydall 1 |

33,300 | 1,453,545 | |||||

Sun Hydraulics |

21,100 | 1,016,809 | |||||

| 15,211,209 | |||||||

| MARINE - 0.6% | |||||||

Clarkson |

38,100 | 1,156,497 | |||||

| PROFESSIONAL SERVICES - 3.7% | |||||||

CRA International |

23,006 | 1,170,775 | |||||

GP Strategies 1 |

72,908 | 1,283,181 | |||||

Heidrick & Struggles International |

34,800 | 1,218,000 | |||||

Kforce |

51,800 | 1,776,740 | |||||

Resources Connection |

103,954 | 1,756,823 | |||||

| 7,205,519 | |||||||

| ROAD & RAIL - 0.8% | |||||||

Marten Transport |

66,341 | 1,555,696 | |||||

| Total (Cost $24,880,905) | 37,428,013 | ||||||

| INFORMATION TECHNOLOGY – 19.6% | |||||||

| COMMUNICATIONS EQUIPMENT - 1.0% | |||||||

Digi International 1 |

91,500 | 1,207,800 | |||||

EMCORE Corporation 1 |

134,300 | 678,215 | |||||

| 1,886,015 | |||||||

| ELECTRONIC EQUIPMENT, INSTRUMENTS & COMPONENTS - 6.5% | |||||||

| 63,500 | 583,565 | ||||||

CUI Global 1 |

298,762 | 887,323 | |||||

| 48,400 | 763,268 | ||||||

ePlus 1 |

14,692 | 1,382,517 | |||||

Fabrinet 1 |

45,569 | 1,681,041 | |||||

Mesa Laboratories |

8,600 | 1,815,288 | |||||

| 14,800 | 489,288 | ||||||

Novanta 1 |

21,400 | 1,333,220 | |||||

PC Connection |

56,900 | 1,889,080 | |||||

Vishay Precision Group 1 |

48,700 | 1,857,905 | |||||

| 12,682,495 | |||||||

| INTERNET SOFTWARE & SERVICES - 1.5% | |||||||

Amber Road 1 |

153,900 | 1,448,199 | |||||

QuinStreet 1 |

122,500 | 1,555,750 | |||||

| 3,003,949 | |||||||

| IT SERVICES - 1.4% | |||||||

Cass Information Systems |

23,540 | 1,620,023 | |||||

Computer Task Group 1 |

137,342 | 1,063,027 | |||||

| 2,683,050 | |||||||

| SEMICONDUCTORS & SEMICONDUCTOR EQUIPMENT - 5.3% | |||||||

Brooks Automation |

41,000 | 1,337,420 | |||||

| 92,500 | 825,100 | ||||||

NeoPhotonics Corporation 1 |

218,600 | 1,361,878 | |||||

| 46,300 | 1,261,675 | ||||||

Photronics 1 |

185,500 | 1,479,362 | |||||

Rudolph Technologies 1 |

43,093 | 1,275,553 | |||||

Silicon Motion Technology ADR |

26,900 | 1,422,741 | |||||

Ultra Clean Holdings 1 |

81,000 | 1,344,600 | |||||

| 10,308,329 | |||||||

| SOFTWARE - 3.0% | |||||||

Agilysys 1 |

45,200 | 700,600 | |||||

Attunity 1 |

188,100 | 2,183,841 | |||||

QAD Cl. A |

37,100 | 1,860,565 | |||||

SeaChange International 1 |

312,900 | 1,070,118 | |||||

| 5,815,124 | |||||||

| TECHNOLOGY HARDWARE, STORAGE & PERIPHERALS - 0.9% | |||||||

†AstroNova |

29,400 | 554,190 | |||||

Super Micro Computer 1 |

53,611 | 1,267,900 | |||||

| 1,822,090 | |||||||

| Total (Cost $28,288,657) | 38,201,052 | ||||||

| MATERIALS – 4.5% | |||||||

| CHEMICALS - 1.9% | |||||||

FutureFuel Corporation |

62,400 | 874,224 | |||||

Quaker Chemical |

7,588 | 1,175,154 | |||||

Trecora Resources 1 |

116,100 | 1,724,085 | |||||

| 3,773,463 | |||||||

| CONSTRUCTION MATERIALS - 0.5% | |||||||

U.S. Concrete 1 |

16,600 | 871,500 | |||||

| METALS & MINING - 2.1% | |||||||

Haynes International |

41,970 | 1,541,978 | |||||

Major Drilling Group International 1 |

240,900 | 1,271,704 | |||||

Schnitzer Steel Industries Cl. A |

37,500 | 1,263,750 | |||||

| 4,077,432 | |||||||

| Total (Cost $6,791,092) | 8,722,395 | ||||||

| THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS | Royce Capital Fund 2018 Semiannual Report to Shareholders | 9 |

| Schedule of Investments | June 30, 2018 (unaudited) |

| Royce Capital Fund - Micro-Cap Portfolio (continued) | |||||||

| SHARES | VALUE | ||||||

| REAL ESTATE – 2.4% | |||||||

| EQUITY REAL ESTATE INVESTMENT TRUSTS (REITS) - 0.8% | |||||||

Community Healthcare Trust |

53,100 | $ | 1,586,097 | ||||

| REAL ESTATE MANAGEMENT & DEVELOPMENT - 1.6% | |||||||

FRP Holdings 1 |

23,440 | 1,517,740 | |||||

Marcus & Millichap 1 |

41,600 | 1,622,816 | |||||

| 3,140,556 | |||||||

| Total (Cost $2,956,700) | 4,726,653 | ||||||

| TELECOMMUNICATION SERVICES – 0.6% | |||||||

| DIVERSIFIED TELECOMMUNICATION SERVICES - 0.6% | |||||||

ORBCOMM 1 |

117,500 | 1,186,750 | |||||

| Total (Cost $736,738) | 1,186,750 | ||||||

| TOTAL COMMON STOCKS | |||||||

| (Cost $139,641,842) | 187,051,542 | ||||||

| REPURCHASE AGREEMENT – 4.3% | |||||||

|

Fixed Income Clearing Corporation, 0.35% dated 6/29/18, due 7/2/18, maturity value

$8,427,246 (collateralized by obligations of various U.S. Government Agencies, 1.375% due 10/07/21, valued at $8,599,601) |

|||||||

| (Cost $8,427,000) | 8,427,000 | ||||||

| COLLATERAL RECEIVED FOR SECURITIES LOANED – 1.4% | |||||||

| Money Market Funds | |||||||

Federated Government Obligations Fund (7 day yield-1.7400%) |

|||||||

| (Cost $2,783,561) | 2,783,561 | ||||||

| TOTAL INVESTMENTS – 101.6% | |||||||

| (Cost $150,852,403) | 198,262,103 | ||||||

| LIABILITIES LESS CASH AND OTHER ASSETS – (1.6)% | (3,205,195 | ) | |||||

| NET ASSETS – 100.0% | $ | 195,056,908 | |||||

| † | New additions in 2018. | |

| 1 | Non-income producing. | |

| 2 | All or a portion of these securities were on loan at June 30, 2018. | |

| 3 | Securities for which market quotations are not readily available represent 0.2% of

net assets. These securities have been valued at their fair value under procedures

approved by the Fund’s Board of Trustees. These securities are defined as Level

3 securities due to the use of significant unobservable inputs in the determination

of fair value. See Notes to Financial Statements. |

|

| Bold indicates the Fund’s 20 largest equity holdings in terms of June 30, 2018, market value. | ||

| 10 | Royce Capital Fund 2018 Semiannual Report to Shareholders | THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS |

| This page is intentionally left blank. |

| Royce Capital Fund 2018 Semiannual Report to Shareholders | 11 |

| MANAGER’S DISCUSSION |

| Royce Capital Fund–Small-Cap Portfolio (RCS) |

|

| Jay Kaplan, CFA |

| FUND PERFORMANCE |

| Royce Capital Fund–Small-Cap Portfolio rose 7.1% for the year-to-date period ended June 30, 2018, trailing its small-cap benchmark, the Russell 2000 Index, which was up 7.7% for the same period. The Fund narrowly outpaced the small-cap index, however, for the one-year period ended June 30, 2018, up 17.7% versus 17.6%. |

| WHAT WORKED... AND WHAT DIDN’T |

| Information Technology and Consumer Discretionary were the top-contributing sectors by a wide margin, while Utilities, where we typically have very little exposure, detracted modestly. The portfolio’s two leading industry groups—electronic equipment, instruments & components and specialty retail—came from its two top-contributing sectors. The airlines group detracted most at the industry level, followed by commercial services & supplies—both groups are in the Industrials sector. |

| Three of the portfolio’s top five positive contributors came from the electronic instruments & components industry. Two more top-10 holdings from this same group—Vishay Intertechnology, which makes semiconductor and passive component equipment, and Celestica, a contract manufacturer that offers manufacturing, hardware platform, and supply chain solutions—were also strong performers. Another contract manufacturer, Fabrinet, specializes mostly in optical components. Its shares tend to be highly volatile, so we always try to trade effectively around its occasionally extreme moves. The company’s recent growth has been strong, spurred by the ongoing adoption of cloud storage solutions, which require optical components. Insight Enterprises and PC Connection are value-add distributors that provide a wide range of IT products and solutions. Global demand has been on the rise, which has kept revenues and earnings for both companies healthy. |

| Moving from tech to transportation, the portfolio also saw a strong contribution from Stoneridge, a manufacturer of highly engineered electrical and electronic components, modules, and systems for the commercial vehicle, automotive, and agricultural vehicle markets. New management, which joined the firm a few years ago, has rolled out new products, including MirrorEye, a camera monitor system that replaces the rear- and side-view mirrors on trucks. In May, the company reported increased 2018 guidance for sales and adjusted earnings per share while also reaffirming previous margin estimates. All of this combined to keep its shares rolling. |

| Asset management business Federated Investors detracted most at the

position level, as outflows from a large equity mutual fund combined

with increased competition in money market funds to keep investors

selling. We chose to hold our shares in the expectation that the firm will

be able to rebound. We built our position in low-cost carrier Spirit Airlines, one of three holdings in the airline industry that disappointed

in the first half. Spirit saw weakness in fares, to which its stock has

historically been vulnerable, through much of 2018’s first six months.

We like its profitability and long-term prospects and were encouraged

by a recent reversal in the direction of fares. Thor Industries is

another long-time Royce favorite and a leading manufacturer of RVs

(recreational vehicles) that has emerged as an innovative industry leader

over the last several years. The firm announced record fiscal second-quarter

sales in March, but also reported higher raw material and

commodity costs. Along with concerns that its industry may have hit a

sales peak, this was enough to drive investors away. Ever contrarian, we

chose to hold our position. First-half performance versus the benchmark suffered most from sector allocation—stock selection was a strength against the Russell 2000. The portfolio’s much lower weighting in Health Care, the top performer in the benchmark, hurt most, while our greater exposure to Industrials also detracted, largely due to our overweight in airlines, where, in addition to Spirit, Allegiant Travel and Hawaiian Holdings also disappointed. Stock picking in Financials also had a negative impact. Stock selection strength could be seen in a number of sectors, with the largest positive impact coming from holdings in Consumer Discretionary, with notable outperformance in the auto components and specialty retail industries. Holdings in Consumer Staples and Real Estate also contributed positively to relative results in the first half, with our lower weighting in the latter sector also helping. |

| Top Contributors to Performance | ||||

| Year-to-Date Through 6/30/18 (%)1 | ||||

| Fabrinet | 0.74 | |||

| Stoneridge | 0.73 | |||

| Insight Enterprises | 0.63 | |||

| PC Connection | 0.62 | |||

| Village Super Market Cl. A | 0.59 | |||

| 1 Includes dividends | ||||

| Top Detractors from Performance | ||||

| Year-to-Date Through 6/30/18 (%)2 | ||||

| Federated Investors Cl. B | -0.75 | |||

| Spirit Airlines | -0.39 | |||

| Thor Industries | -0.31 | |||

| Wabash National | -0.29 | |||

| Electro Scientific Industries | -0.26 | |||

| 2 Net of dividends | ||||

| CURRENT POSITIONING AND OUTLOOK |

| As interest rates continue to rise—and rise more consistently—valuations become more and more important. Most looked high to us at the end of June, especially with current and imminent challenges, some of which investors may be overlooking. In addition to a flattened yield curve and trade war noise, we have a more challenging climate for earnings growth now that the tax cuts have been reflected and a lack of quality in earnings can be discerned in many cases throughout the small-cap market. The approaching mid-term elections could generate a great deal of noise—and market volatility—all on their own. So while in general, we see more that is worth selling than buying, we have also seen pockets of value within technology in semiconductor and capital equipment makers, distributors, and contract manufacturers, as well as in banks. Moreover, with the expectation of increased volatility, we see a reasonable environment for our contrarian value approach taking shape. |

| 12 | Royce Capital Fund 2018 Semiannual Report to Shareholders |

| PERFORMANCE AND PORTFOLIO REVIEW | TICKER SYMBOLS RCPFX RCSSX |

| Performance and Expenses | ||||||||||||||||

| Average Annual Total Return (%) Through 6/30/18 | ||||||||||||||||

| JAN-JUN 20181 | 1-YR | 3-YR | 5-YR | 10-YR | 15-YR | 20-YR | SINCE INCEPTION (12/27/96) | |||||||||

| RCS | 7.06 | 17.72 | 6.48 | 8.29 | 7.81 | 10.00 | 10.13 | 10.80 | ||||||||

| Annual Gross Operating Expenses: 1.11% Annual Net Operating Expenses: 1.08% | ||||||||||||||||

| 1 Not annualized | ||||||||||||||||

Relative Returns: Monthly Rolling Average Annual Return Periods

| On a monthly rolling basis, the Fund outperformed the Russell 2000 in 69% of all 10-year periods; 64% of all 5-year periods; and 49% of all 1-year periods. |

| PERIODS BEATING THE INDEX | FUND AVG (%)1 | INDEX AVG (%)1 | ||||||||||

| 10-year | 83/121 | 69% | 8.9 | 6.9 | ||||||||

| 5-year | 116/181 | 64% | 10.5 | 8.7 | ||||||||

| 1-year | 112/229 | 49% | 12.1 | 10.4 | ||||||||

The Morningstar Style Map is the Morningstar

Style BoxTM

with the center 75% of fund holdings plotted as the Morningstar

Ownership ZoneTM. The Morningstar Style Box is designed to reveal a

fund’s investment strategy. The Morningstar Ownership Zone provides

detail about a portfolio’s investment style by showing the range of

stock sizes and styles. The Ownership Zone is derived by plotting each

stock in the portfolio within the proprietary Morningstar Style Box.

Over time, the shape and location of a fund’s ownership zone may vary.

See page 27 for additional information. |

Value of $10,000

Includes reinvestment of distributions.

| Top 10 Positions | ||

| % of Net Assets | ||

| PC Connection | 2.5 | |

| Insight Enterprises | 2.5 | |

| Kulicke & Soffa Industries | 2.5 | |

| Genworth MI Canada | 2.4 | |

| Village Super Market Cl. A | 2.3 | |

| Spirit Airlines | 2.3 | |

| Vishay Intertechnology | 2.2 | |

| Celestica | 2.2 | |

| Fabrinet | 2.0 | |

| Hawaiian Holdings | 2.0 | |

| Portfolio Sector Breakdown | ||

| % of Net Assets | ||

| Information Technology | 25.6 | |

| Industrials | 22.3 | |

| Financials | 21.3 | |

| Consumer Discretionary | 14.1 | |

| Consumer Staples | 2.3 | |

| Energy | 2.1 | |

| Real Estate | 1.5 | |

| Health Care | 1.4 | |

| Utilities | 0.4 | |

| Cash and Cash Equivalents | 9.0 | |

| Calendar Year Total Returns (%) | ||

| YEAR | RCS | |

| 2017 | 5.4 | |

| 2016 | 21.0 | |

| 2015 | -11.8 | |

| 2014 | 3.2 | |

| 2013 | 34.8 | |

| 2012 | 12.5 | |

| 2011 | -3.3 | |

| 2010 | 20.5 | |

| 2009 | 35.2 | |

| 2008 | -27.2 | |

| 2007 | -2.1 | |

| 2006 | 15.6 | |

| 2005 | 8.6 | |

| 2004 | 25.0 | |

| 2003 | 41.1 | |

| Upside/Downside Capture Ratios | ||||

| Periods Ended 6/30/18 (%) | ||||

| UPSIDE | DOWNSIDE | |||

| 10-Year | 77 | 82 | ||

| From 12/31/96 (Start of

Fund’s First Full Quarter) |

94 | 76 | ||

| Portfolio Diagnostics | ||

| Fund Net Assets | $478 million | |

| Number of Holdings | 79 | |

| Turnover Rate | 23% | |

| Average Market Capitalization1 | $1,295 million | |

| Weighted Average P/E Ratio2,3 | 15.2x | |

| Weighted Average P/B Ratio2 | 2.0x | |

| Active Share4 | 96% | |

| U.S. Investments (% of Net Assets) | 79.4% | |

| Non-U.S. Investments (% of Net Assets) | 11.6% | |

| 1 | Geometric Average. This weighted calculation uses each portfolio

holding’s market cap in a way designed to not skew the effect of

very large or small holdings; instead, it aims to better identify

the portfolio’s center, which Royce believes offers a more accurate

measure of average market cap than a simple mean or median. |

| 2 | Harmonic Average. This weighted calculation evaluates a portfolio

as if it were a single stock and measures it overall. It compares the

total market value of the portfolio to the portfolio’s share in the

earnings or book value, as the case may be, of its underlying stocks. |

| 3 | The Fund’s P/E ratio calculation excludes companies with zero or

negative earnings (6% of portfolio holdings as of 6/30/18). |

| 4 | Active Share is the sum of the absolute values of the different

weightings of each holding in the Fund versus each holding in the

benchmark, divided by two. |

| Important Performance and Expense Information

All performance information in this Report reflects past performance, is presented on a total return basis, reflects the reinvestment of distributions, and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, so that shares may be worth more or less than their original cost when redeemed. Current performance may be higher or lower than performance quoted. The Fund’s total returns do not reflect any deduction for charges or expenses of the variable contracts investing in the Fund. Returns as of the most recent month-end may be obtained at www.roycefunds.com. All performance and risk information reflects the result of the Investment Class (its oldest class). Shares of RCS’s Service Class bear an annual distribution expense that is not borne by the Investment Class; if those expenses were reflected, total returns would have been lower. Certain immaterial adjustments were made to the net assets of Royce Capital Fund-Small-Cap Portfolio at 12/31/17 for financial reporting purposes, and as a result the calendar year total returns based on those net assets values differ from the adjusted net values and calendar year total returns reported in the Financial Highlights. All performance information reflects past performance, is presented on a total return basis, reflects the reinvestment of distributions, and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, so that shares may be worth more or less than their original cost when redeemed. Current month-end performance may be higher or lower than performance quoted and may be obtained at www.roycefunds.com. The Fund’s total returns do not reflect any deduction for charges or expenses of the variable contracts investing in the Fund. Gross operating expenses reflect the Fund’s total gross operating expenses for the Investment Class and include management fees and other expenses. Net operating expenses reflect contractual fee waivers and/or expense reimbursements. All expense information is reported as of the Fund’s most current prospectus. Royce & Associates has contractually agreed, without right of termination, to waive fees and/or reimburse expenses to the extent necessary to maintain the Investment Class’s net annual operating expenses (excluding brokerage commissions, taxes, interest, litigation expenses, acquired fund fees and expenses, and other expenses not borne in the ordinary course of business) at or below 1.08% through April 30, 2019. Regarding the “Top Contributors” and “Top Detractors” tables shown above, the sum of all contributors to, and all detractors from, performance for all securities in the portfolio would approximate the Fund’s year-to-date performance for 2018. Upside Capture Ratio measures a manager’s performance in up markets relative to the Fund’s benchmark. It is calculated by measuring the Fund’s performance in quarters when the benchmark went up and dividing it by the benchmark’s return in those quarters. Downside Capture Ratio measures a manager’s performance in down markets relative to the Fund’s benchmark (Russell 2000). It is calculated by measuring the Fund’s performance in quarters when the benchmark goes down and dividing it by the benchmark’s return in those quarters. |

| Royce Capital Fund 2018 Semiannual Report to Shareholders | 13 |

| Schedule of Investments |

| Royce Capital Fund - Small-Cap Portfolio | |||||||

| Common Stocks – 91.0% | |||||||

| SHARES | VALUE | ||||||

| CONSUMER DISCRETIONARY – 14.1% | |||||||

| AUTO COMPONENTS - 2.5% | |||||||

Gentex Corporation |

289,616 | $ | 6,666,960 | ||||

Stoneridge 1 |

143,161 | 5,030,678 | |||||

| 11,697,638 | |||||||

| AUTOMOBILES - 0.5% | |||||||

Thor Industries |

26,600 | 2,590,574 | |||||

| HOTELS, RESTAURANTS & LEISURE - 0.5% | |||||||

Cheesecake Factory |

41,415 | 2,280,310 | |||||

| HOUSEHOLD DURABLES - 2.7% | |||||||

Bassett Furniture Industries |

58,122 | 1,601,261 | |||||

Flexsteel Industries |

105,743 | 4,219,146 | |||||

La-Z-Boy |

231,786 | 7,092,651 | |||||

| 12,913,058 | |||||||

| INTERNET & DIRECT MARKETING RETAIL - 1.1% | |||||||

†Nutrisystem |

139,900 | 5,386,150 | |||||

| MEDIA - 1.5% | |||||||

Saga Communications Cl. A |

191,107 | 7,357,620 | |||||

| SPECIALTY RETAIL - 4.3% | |||||||

American Eagle Outfitters |

286,765 | 6,667,286 | |||||

DSW Cl. A |

273,593 | 7,064,171 | |||||

Shoe Carnival |

206,346 | 6,695,928 | |||||

| 20,427,385 | |||||||

| TEXTILES, APPAREL & LUXURY GOODS - 1.0% | |||||||

Steven Madden |

89,071 | 4,729,670 | |||||

| Total (Cost $51,876,364) | 67,382,405 | ||||||

| CONSUMER STAPLES – 2.3% | |||||||

| FOOD & STAPLES RETAILING - 2.3% | |||||||

Village Super Market Cl. A |

369,177 | 10,875,955 | |||||

| Total (Cost $10,540,057) | 10,875,955 | ||||||

| ENERGY – 2.1% | |||||||

| ENERGY EQUIPMENT & SERVICES - 2.1% | |||||||

Helmerich & Payne |

82,700 | 5,272,952 | |||||

Unit Corporation 1 |

183,013 | 4,677,812 | |||||

| Total (Cost $7,325,817) | 9,950,764 | ||||||

| FINANCIALS – 21.3% | |||||||

| BANKS - 10.0% | |||||||

Ames National |

148,534 | 4,582,274 | |||||

†Bar Harbor Bankshares |

90,658 | 2,746,031 | |||||

Camden National |

153,882 | 7,033,946 | |||||

City Holding Company |

65,567 | 4,932,605 | |||||

CNB Financial |

186,126 | 5,594,948 | |||||

Codorus Valley Bancorp |

51,400 | 1,576,952 | |||||

Landmark Bancorp |

40,017 | 1,140,484 | |||||

MidWestOne Financial Group |

213,023 | 7,195,917 | |||||

National Bankshares |

128,639 | 5,968,850 | |||||

Northrim BanCorp |

127,481 | 5,041,873 | |||||

Unity Bancorp |

92,521 | 2,104,853 | |||||

| 47,918,733 | |||||||

| CAPITAL MARKETS - 3.2% | |||||||

Federated Investors Cl. B |

270,786 | 6,314,730 | |||||

Houlihan Lokey Cl. A |

92,269 | 4,726,018 | |||||

Moelis & Company Cl. A |

74,920 | 4,394,058 | |||||

| 15,434,806 | |||||||

| INSURANCE - 2.9% | |||||||

James River Group Holdings |

176,101 | 6,919,009 | |||||

Kingstone Companies |

119,288 | 2,015,967 | |||||

Reinsurance Group of America |

37,236 | 4,970,261 | |||||

| 13,905,237 | |||||||

| THRIFTS & MORTGAGE FINANCE - 5.2% | |||||||

Genworth MI Canada |

352,550 | 11,472,322 | |||||

Southern Missouri Bancorp |

40,987 | 1,599,313 | |||||

Timberland Bancorp |

119,932 | 4,478,261 | |||||

TrustCo Bank Corp. NY |

783,082 | 6,969,430 | |||||

| 24,519,326 | |||||||

| Total (Cost $73,329,150) | 101,778,102 | ||||||

| HEALTH CARE – 1.4% | |||||||

| HEALTH CARE PROVIDERS & SERVICES - 1.4% | |||||||

| 39,741 | 2,328,823 | ||||||

Ensign Group (The) |

126,314 | 4,524,567 | |||||

| Total (Cost $4,295,287) | 6,853,390 | ||||||

| INDUSTRIALS – 22.3% | |||||||

| AIRLINES - 5.8% | |||||||

Allegiant Travel |

51,899 | 7,211,366 | |||||

Hawaiian Holdings |

265,955 | 9,561,082 | |||||

| 298,953 | 10,866,942 | ||||||

| 27,639,390 | |||||||

| BUILDING PRODUCTS - 2.0% | |||||||

American Woodmark 1 |

22,543 | 2,063,812 | |||||

Apogee Enterprises |

156,017 | 7,515,339 | |||||

| 9,579,151 | |||||||

| COMMERCIAL SERVICES & SUPPLIES - 2.7% | |||||||

Herman Miller |

198,603 | 6,732,642 | |||||

Kimball International Cl. B |

392,482 | 6,342,509 | |||||

| 13,075,151 | |||||||

| CONSTRUCTION & ENGINEERING - 0.5% | |||||||

Comfort Systems USA |

49,969 | 2,288,580 | |||||

| ELECTRICAL EQUIPMENT - 1.2% | |||||||

EnerSys |

77,200 | 5,762,208 | |||||

| MACHINERY - 4.9% | |||||||

Alamo Group |

32,728 | 2,957,302 | |||||

Federal Signal |

96,841 | 2,255,427 | |||||

Miller Industries |

346,682 | 8,857,725 | |||||

Wabash National |

508,303 | 9,484,934 | |||||

| 23,555,388 | |||||||

| PROFESSIONAL SERVICES - 3.9% | |||||||

Heidrick & Struggles International |

63,162 | 2,210,670 | |||||

Kforce |

135,467 | 4,646,518 | |||||

Korn/Ferry International |

76,372 | 4,729,718 | |||||

Robert Half International |

69,100 | 4,498,410 | |||||

TrueBlue 1 |

85,271 | 2,298,053 | |||||

| 18,383,369 | |||||||

| ROAD & RAIL - 1.3% | |||||||

Old Dominion Freight Line |

14,704 | 2,190,308 | |||||

Saia 1 |

28,361 | 2,292,987 | |||||

Werner Enterprises |

47,961 | 1,800,935 | |||||

| 6,284,230 | |||||||

| Total (Cost $89,754,862) | 106,567,467 | ||||||

| INFORMATION TECHNOLOGY – 25.6% | |||||||

| COMMUNICATIONS EQUIPMENT - 0.4% | |||||||

NETGEAR 1 |

34,271 | 2,141,938 | |||||

| 14 | Royce Capital Fund 2018 Semiannual Report to Shareholders | THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS |

| June 30, 2018 (unaudited) |

| Royce Capital Fund - Small-Cap Portfolio (continued) | |||||||

| SHARES | VALUE | ||||||

| INFORMATION TECHNOLOGY (continued) | |||||||

| ELECTRONIC EQUIPMENT, INSTRUMENTS & COMPONENTS - 16.4% | |||||||

Benchmark Electronics |

240,435 | $ | 7,008,680 | ||||

Celestica 1 |

894,672 | 10,619,757 | |||||

| 446,309 | 7,038,293 | ||||||

Fabrinet 1 |

264,760 | 9,766,996 | |||||

Insight Enterprises 1 |

240,902 | 11,787,335 | |||||

Methode Electronics |

177,353 | 7,147,326 | |||||

PC Connection |

362,317 | 12,028,924 | |||||

Sanmina Corporation 1 |

76,044 | 2,228,089 | |||||

Vishay Intertechnology |

458,299 | 10,632,537 | |||||

| 78,257,937 | |||||||

| SEMICONDUCTORS & SEMICONDUCTOR EQUIPMENT - 7.9% | |||||||

Advanced Energy Industries 1 |

125,850 | 7,310,626 | |||||

†Cohu |

154,115 | 3,777,359 | |||||

Kulicke & Soffa Industries |

491,726 | 11,712,913 | |||||

MKS Instruments |

38,391 | 3,674,019 | |||||

Silicon Motion Technology ADR |

89,800 | 4,749,522 | |||||

| 458,600 | 6,406,642 | ||||||

| 37,631,081 | |||||||

| TECHNOLOGY HARDWARE, STORAGE & PERIPHERALS - 0.9% | |||||||

Super Micro Computer 1 |

179,883 | 4,254,233 | |||||

| Total (Cost $105,036,104) | 122,285,189 | ||||||

| REAL ESTATE – 1.5% | |||||||

| REAL ESTATE MANAGEMENT & DEVELOPMENT - 1.5% | |||||||

Marcus & Millichap 1 |

181,284 | 7,071,889 | |||||

| Total (Cost $4,644,978) | 7,071,889 | ||||||

| UTILITIES – 0.4% | |||||||

| GAS UTILITIES - 0.4% | |||||||

Star Group L.P. |

230,460 | 2,258,508 | |||||

| Total (Cost $2,158,098) | 2,258,508 | ||||||

| TOTAL COMMON STOCKS | |||||||

| (Cost $348,960,717) | 435,023,669 | ||||||

| REPURCHASE AGREEMENT– 8.4% | |||||||

|

Fixed Income Clearing Corporation, 0.35% dated 6/29/18, due 7/2/18, maturity value

$40,227,173 (collateralized by obligations of various U.S. Government Agencies, 1.375% due 10/07/21, valued at $41,030,868) |

|||||||

| (Cost $40,226,000) | 40,226,000 | ||||||

| COLLATERAL RECEIVED FOR SECURITIES LOANED – 0.6% | |||||||

| Money Market Funds | |||||||

Federated Government Obligations Fund (7 day yield-1.7400%) |

|||||||

| (Cost $2,957,094) | 2,957,094 | ||||||

| TOTAL INVESTMENTS – 100.0% | |||||||

| (Cost $392,143,811) | 478,206,763 | ||||||

| LIABILITIES LESS CASH AND OTHER ASSETS – (0.0)% | (133,940 | ) | |||||

| NET ASSETS – 100.0% | $ | 478,072,823 | |||||

| † | New additions in 2018. | |

| 1 | Non-income producing. | |

| 2 | All or a portion of these securities were on loan at June 30, 2018. | |

| Bold indicates the Fund’s 20 largest equity holdings in terms of June 30, 2018, market value. |

| THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS | Royce Capital Fund 2018 Semiannual Report to Shareholders | 15 |

| Statements of Assets and Liabilities | June 30, 2018 (unaudited) |

| Micro-Cap | Small-Cap | |||||||

| Portfolio | Portfolio | |||||||

| ASSETS: | ||||||||

| Investments at value (including collateral on loaned securities) 1 | $ | 189,835,103 | $ | 437,980,763 | ||||

| Repurchase agreements (at cost and value) | 8,427,000 | 40,226,000 | ||||||

| Cash and foreign currency | 43,366 | – | ||||||

| Receivable for investments sold | – | 4,386,362 | ||||||

| Receivable for capital shares sold | 215,227 | 157,672 | ||||||

| Receivable for dividends and interest | 142,621 | 373,932 | ||||||

| Receivable for securities lending income | 4,773 | 1,219 | ||||||

| Prepaid expenses and other assets | 640 | 7,722 | ||||||

| Total Assets | 198,668,730 | 483,133,670 | ||||||

| LIABILITIES: | ||||||||

| Payable for collateral on loaned securities | 2,783,561 | 2,957,094 | ||||||

| Payable to custodian for cash and foreign currency overdrawn | – | 33,430 | ||||||

| Payable for investments purchased | 338,917 | 1,248,244 | ||||||

| Payable for capital shares redeemed | 214,701 | 264,093 | ||||||

| Payable for investment advisory fees | 204,342 | 401,654 | ||||||

| Payable for trustees’ fees | 11,711 | 27,916 | ||||||

| Accrued expenses | 58,590 | 128,416 | ||||||

| Total Liabilities | 3,611,822 | 5,060,847 | ||||||

| Net Assets | $ | 195,056,908 | $ | 478,072,823 | ||||

| ANALYSIS OF NET ASSETS: | ||||||||

| Paid-in capital | $ | 132,447,821 | $ | 364,622,003 | ||||

| Undistributed net investment income (loss) | (170,679 | ) | 2,815,674 | |||||

| Accumulated net realized gain (loss) on investments and foreign currency | 15,370,047 | 24,572,194 | ||||||

| Net unrealized appreciation (depreciation) on investments and foreign currency | 47,409,719 | 86,062,952 | ||||||

| Net Assets | $ | 195,056,908 | $ | 478,072,823 | ||||

Investment Class |

$ | 162,857,359 | $ | 217,616,068 | ||||

Service Class |

32,199,549 | 260,456,755 | ||||||

| SHARES OUTSTANDING (unlimited number of $.001 par value): | ||||||||

Investment Class |

14,222,520 | 23,151,857 | ||||||

Service Class |

2,863,102 | 28,459,700 | ||||||

| NET ASSET VALUES (Net Assets ÷ Shares Outstanding): | ||||||||

(offering and redemption price per share) |

||||||||

Investment Class |

$11.45 | $9.40 | ||||||

Service Class |

11.25 | 9.15 | ||||||

| Investments at identified cost | $ | 142,425,403 | $ | 351,917,811 | ||||

| Market value of loaned securities 2 | 3,241,193 | 12,873,326 | ||||||

| 1 | See Notes to Financial Statements for additional collateral on loaned securities. |

| 2 | Market value of loaned securities backed by non-cash collateral is as of prior business day. |

| 16 | Royce Capital Fund 2018 Semiannual Report to Shareholders | THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS |

| Statements of Changes in Net Assets |

| Micro-Cap Portfolio | Small-Cap Portfolio | ||||||||||||||||

|

Six Months Ended 6/30/18 (unaudited) |

Year Ended 12/31/17 |

Six Months Ended 6/30/18 (unaudited) |

Year Ended 12/31/17 | ||||||||||||||

| INVESTMENT OPERATIONS: | |||||||||||||||||

| Net investment income (loss) | $ | (208,623 | ) | $ | (507,803 | ) | $ | 957,604 | $ | 1,986,132 | |||||||

| Net realized gain (loss) on investments and foreign currency | 8,016,787 | 8,353,077 | 21,982,524 | 7,868,418 | |||||||||||||

Net change in unrealized appreciation (depreciation) on investments and foreign currency |

10,668,687 | 1,752,552 | 9,524,788 | 2,459,022 | |||||||||||||

| Net increase (decrease) in net assets from investment operations | 18,476,851 | 9,597,826 | 32,464,916 | 12,313,572 | |||||||||||||

| DISTRIBUTIONS: | |||||||||||||||||

| Net investment income | |||||||||||||||||

Investment Class |

– | (1,090,893 | ) | – | (2,075,505 | ) | |||||||||||

Service Class |

– | (170,672 | ) | – | (2,047,296 | ) | |||||||||||

| Net realized gain on investments and foreign currency | |||||||||||||||||

Investment Class |

– | (17,091,597 | ) | – | – | ||||||||||||

Service Class |

– | (3,298,738 | ) | – | – | ||||||||||||

| Total distributions | – | (21,651,900 | ) | – | (4,122,801 | ) | |||||||||||

| CAPITAL SHARE TRANSACTIONS: | |||||||||||||||||

| Value of shares sold | |||||||||||||||||

Investment Class |

6,453,325 | 19,985,987 | 10,346,375 | 27,113,319 | |||||||||||||

Service Class |

6,728,550 | 8,994,660 | 896,650 | 193,204,040 | |||||||||||||

| Distributions reinvested | |||||||||||||||||

Investment Class |

– | 18,182,489 | – | 2,075,505 | |||||||||||||

Service Class |

– | 3,469,410 | – | 2,047,296 | |||||||||||||

| Value of shares redeemed | |||||||||||||||||

Investment Class |

(23,927,751 | ) | (41,333,398 | ) | (36,176,977 | ) | (57,799,564 | ) | |||||||||

Service Class |

(9,397,534 | ) | (12,640,986 | ) | (21,627,251 | ) | (198,351,118 | ) | |||||||||

Net increase (decrease) in net assets from capital share transactions |

(20,143,410 | ) | (3,341,838 | ) | (46,561,203 | ) | (31,710,522 | ) | |||||||||

| Net Increase (Decrease) in Net Assets | (1,666,559 | ) | (15,395,912 | ) | (14,096,287 | ) | (23,519,751 | ) | |||||||||

| NET ASSETS: | |||||||||||||||||

| Beginning of period | 196,723,467 | 212,119,379 | 492,169,110 | 515,688,861 | |||||||||||||

| End of period | $ | 195,056,908 | $ | 196,723,467 | $ | 478,072,823 | $ | 492,169,110 | |||||||||

| Undistributed Net Investment Income (Loss) at End of Period | $ | (170,679 | ) | $ | 37,944 | $ | 2,815,674 | $ | 1,858,071 | ||||||||

| THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS | Royce Capital Fund 2018 Semiannual Report to Shareholders | 17 |

| Statements of Operations | Six Months Ended June 30, 2018 (unaudited) |

| Micro-Cap | Small-Cap | |||||||

| Portfolio | Portfolio | |||||||

| INVESTMENT INCOME: | ||||||||

| INCOME: | ||||||||

| Dividends | $ | 995,907 | $ | 3,834,220 | ||||

| Foreign withholding tax | (30,582 | ) | (39,296 | ) | ||||

| Interest | 11,974 | 38,028 | ||||||

| Securities lending | 108,169 | 7,361 | ||||||

| Total income | 1,085,468 | 3,840,313 | ||||||

| EXPENSES: | ||||||||

| Investment advisory fees | 1,180,818 | 2,370,797 | ||||||

| Distribution fees | 37,701 | 322,248 | ||||||

| Shareholder reports | 33,800 | 38,127 | ||||||

| Administrative and office facilities | 27,442 | 64,085 | ||||||

| Trustees’ fees | 19,642 | 48,419 | ||||||

| Audit | 17,189 | 15,962 | ||||||

| Custody | 14,303 | 28,513 | ||||||

| Shareholder servicing | 6,874 | 6,745 | ||||||

| Legal | 2,594 | 6,028 | ||||||

| Other expenses | 6,606 | 14,131 | ||||||

| Total expenses | 1,346,969 | 2,915,055 | ||||||

| Compensating balance credits | (75 | ) | (197 | ) | ||||

| Fees waived by investment adviser | (12,122 | ) | – | |||||

| Expenses reimbursed by investment adviser | (40,681 | ) | (32,149 | ) | ||||

| Net expenses | 1,294,091 | 2,882,709 | ||||||

| Net investment income (loss) | (208,623 | ) | 957,604 | |||||

| REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS AND FOREIGN CURRENCY: | ||||||||

| NET REALIZED GAIN (LOSS): | ||||||||

| Investments | 8,017,164 | 21,985,910 | ||||||

| Foreign currency transactions | (377 | ) | (3,386 | ) | ||||

| NET CHANGE IN UNREALIZED APPRECIATION (DEPRECIATION): | ||||||||

| Investments and foreign currency translations | 10,670,029 | 9,524,788 | ||||||

| Other assets and liabilities denominated in foreign currency | (1,342 | ) | – | |||||

| Net realized and unrealized gain (loss) on investments and foreign currency | 18,685,474 | 31,507,312 | ||||||

| NET INCREASE (DECREASE) IN NET ASSETS FROM INVESTMENT OPERATIONS | $ | 18,476,851 | $ | 32,464,916 | ||||

| 18 | Royce Capital Fund 2018 Semiannual Report to Shareholders | THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS |

Financial Highlights

This table is presented to show selected data for a share outstanding throughout each year or other indicated period and to assist shareholders in evaluating a Fund’s performance for the periods presented. Per share amounts have been determined on the basis of the weighted average number of shares outstanding during the period.

| Ratio of Expenses to Average Net Assets | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Net Asset Value, Beginning of Period |

Net Investment Income (Loss) |

Net Realized and Unrealized Gain (Loss) on Investments and Foreign Currency |

Total from Investment Operations |

Distributions from Net Investment Income |

Distributions from Net Realized Gain on Investments and Foreign Currency |

Total Distributions |

Net Asset Value, End of Period |

Total Return |

Net Assets, End of Period (in thousands) |

Prior to Fee Waivers, Expense Reimbursements and Balance Credits |

Prior to Fee Waivers and Expense Reimbursements |

Net of Fee Waivers and Expense Reimbursements |

Ratio of Net Investment Income (Loss) to Average Net Assets |

Portfolio Turnover Rate |

|||||||||||||||||||||||||||||||||||||||||||||

| Micro-Cap Portfolio–Investment Class | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2018† | $ | 10.39 | $ | (0.01 | ) | $ | 1.07 | $ | 1.06 | $ | – | $ | – | $ | – | $ | 11.45 | 10.20 | %1 | $ | 162,857 | 1.39 | %2 | 1.39 | %2 | 1.33 | %2 | (0.18 | )%2 | 14 | % | ||||||||||||||||||||||||||||

| 2017 | 11.11 | (0.02 | ) | 0.58 | 0.56 | (0.08 | ) | (1.20 | ) | (1.28 | ) | 10.39 | 5.29 | 164,656 | 1.38 | 1.38 | 1.38 | (0.22 | ) | 30 | |||||||||||||||||||||||||||||||||||||||

| 2016 | 9.34 | 0.03 | 1.81 | 1.84 | (0.07 | ) | – | (0.07 | ) | 11.11 | 19.71 | 177,444 | 1.36 | 1.36 | 1.36 | 0.02 | 57 | ||||||||||||||||||||||||||||||||||||||||||

| 2015 | 11.37 | 0.03 | (1.45 | ) | (1.42 | ) | – | (0.61 | ) | (0.61 | ) | 9.34 | (12.46 | ) | 369,991 | 1.32 | 1.32 | 1.32 | 0.27 | 51 | |||||||||||||||||||||||||||||||||||||||

| 2014 | 12.83 | (0.04 | ) | (0.44 | ) | (0.48 | ) | – | (0.98 | ) | (0.98 | ) | 11.37 | (3.58 | ) | 485,434 | 1.30 | 1.30 | 1.30 | (0.32 | ) | 25 | |||||||||||||||||||||||||||||||||||||

| 2013 | 10.95 | (0.04 | ) | 2.32 | 2.28 | (0.06 | ) | (0.34 | ) | (0.40 | ) | 12.83 | 20.99 | 572,666 | 1.32 | 1.32 | 1.32 | (0.36 | ) | 30 | |||||||||||||||||||||||||||||||||||||||

| Micro-Cap Portfolio–Service Class | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2018† | $ | 10.21 | $ | (0.02 | ) | $ | 1.06 | $ | 1.04 | $ | – | $ | – | $ | – | $ | 11.25 | 10.19 | %1 | $ | 32,200 | 1.63 | %2 | 1.63 | %2 | 1.58 | %2 | (0.44 | )%2 | 14 | % | ||||||||||||||||||||||||||||

| 2017 | 10.93 | (0.04 | ) | 0.57 | 0.53 | (0.06 | ) | (1.19 | ) | (1.25 | ) | 10.21 | 5.02 | 32,067 | 1.64 | 1.64 | 1.58 | (0.43 | ) | 30 | |||||||||||||||||||||||||||||||||||||||

| 2016 | 9.20 | (0.02 | ) | 1.80 | 1.78 | (0.05 | ) | – | (0.05 | ) | 10.93 | 19.37 | 34,675 | 1.65 | 1.65 | 1.58 | (0.15 | ) | 57 | ||||||||||||||||||||||||||||||||||||||||

| 2015 | 11.23 | 0.00 | (1.42 | ) | (1.42 | ) | – | (0.61 | ) | (0.61 | ) | 9.20 | (12.61 | ) | 23,928 | 1.60 | 1.60 | 1.56 | 0.01 | 51 | |||||||||||||||||||||||||||||||||||||||

| 2014 | 12.72 | (0.07 | ) | (0.44 | ) | (0.51 | ) | – | (0.98 | ) | (0.98 | ) | 11.23 | (3.84 | ) | 27,362 | 1.57 | 1.57 | 1.57 | (0.60 | ) | 25 | |||||||||||||||||||||||||||||||||||||

| 2013 | 10.87 | (0.07 | ) | 2.30 | 2.23 | (0.04 | ) | (0.34 | ) | (0.38 | ) | 12.72 | 20.65 | 40,753 | 1.60 | 1.60 | 1.58 | (0.62 | ) | 30 | |||||||||||||||||||||||||||||||||||||||

| Small-Cap Portfolio–Investment Class | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2018† | $ | 8.77 | $ | 0.02 | $ | 0.61 | $ | 0.63 | $ | – | $ | – | $ | – | $ | 9.40 | 7.18 | %1 | $ | 217,616 | 1.10 | %2 | 1.10 | %2 | 1.08 | %2 | 0.54 | %2 | 23 | % | |||||||||||||||||||||||||||||

| 2017 | 8.41 | 0.05 | 0.39 | 0.44 | (0.08 | ) | – | (0.08 | ) | 8.77 | 5.26 | 228,620 | 1.11 | 1.11 | 1.11 | 0.55 | 91 | ||||||||||||||||||||||||||||||||||||||||||

| 2016 | 8.43 | 0.13 | 1.66 | 1.79 | (0.17 | ) | (1.64 | ) | (1.81 | ) | 8.41 | 20.96 | 248,244 | 1.09 | 1.09 | 1.09 | 0.89 | 78 | |||||||||||||||||||||||||||||||||||||||||

| 2015 | 12.65 | 0.17 | (1.66 | ) | (1.49 | ) | (0.09 | ) | (2.64 | ) | (2.73 | ) | 8.43 | (11.80 | ) | 356,258 | 1.06 | 1.06 | 1.06 | 1.26 | 59 | ||||||||||||||||||||||||||||||||||||||

| 2014 | 13.92 | 0.06 | 0.35 | 0.41 | (0.02 | ) | (1.66 | ) | (1.68 | ) | 12.65 | 3.24 | 577,222 | 1.05 | 1.05 | 1.05 | 0.44 | 36 | |||||||||||||||||||||||||||||||||||||||||

| 2013 | 11.03 | 0.03 | 3.75 | 3.78 | (0.14 | ) | (0.75 | ) | (0.89 | ) | 13.92 | 34.75 | 736,917 | 1.05 | 1.05 | 1.05 | 0.13 | 43 | |||||||||||||||||||||||||||||||||||||||||

| Small-Cap Portfolio–Service Class | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2018† | $ | 8.55 | $ | 0.01 | $ | 0.59 | $ | 0.60 | $ | – | $ | – | $ | – | $ | 9.15 | 7.02 | %1 | $ | 260,457 | 1.34 | %2 | 1.34 | %2 | 1.33 | %2 | 0.29 | %2 | 23 | % | |||||||||||||||||||||||||||||

| 2017 | 8.20 | 0.02 | 0.40 | 0.42 | (0.07 | ) | – | (0.07 | ) | 8.55 | 5.10 | 263,549 | 1.34 | 1.34 | 1.34 | 0.32 | 91 | ||||||||||||||||||||||||||||||||||||||||||

| 2016 | 8.27 | 0.03 | 1.69 | 1.72 | (0.15 | ) | (1.64 | ) | (1.79 | ) | 8.20 | 20.53 | 267,445 | 1.34 | 1.34 | 1.34 | 0.69 | 78 | |||||||||||||||||||||||||||||||||||||||||

| 2015 | 12.44 | 0.13 | (1.62 | ) | (1.49 | ) | (0.04 | ) | (2.64 | ) | (2.68 | ) | 8.27 | (11.97 | ) | 128,285 | 1.31 | 1.31 | 1.31 | 1.00 | 59 | ||||||||||||||||||||||||||||||||||||||

| 2014 | 13.74 | 0.03 | 0.33 | 0.36 | – | (1.66 | ) | (1.66 | ) | 12.44 | 2.92 | 218,175 | 1.30 | 1.30 | 1.30 | 0.21 | 36 | ||||||||||||||||||||||||||||||||||||||||||

| 2013 | 10.91 | (0.02 | ) | 3.73 | 3.71 | (0.13 | ) | (0.75 | ) | (0.88 | ) | 13.74 | 34.44 | 232,189 | 1.31 | 1.31 | 1.31 | (0.12 | ) | 43 | |||||||||||||||||||||||||||||||||||||||

| † | Six months ended June 30, 2018 (unaudited). |

| 1 | Not annualized |

| 2 | Annualized |

| THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS | Royce Capital Fund 2018 Semiannual Report to Shareholders | 19 |

Notes to Financial Statements (unaudited)

| Summary of Significant Accounting Policies: |

Royce Micro-Cap

Portfolio and Royce Small-Cap Portfolio (the “Fund” or “Funds”)

are the two series of Royce Capital Fund (the “Trust”), a diversified

open-end management investment company organized as a Delaware statutory trust.

Shares of the Funds are offered to life insurance companies for allocation to certain

separate accounts established for the purpose of funding qualified and non-qualified

variable annuity contracts and variable life insurance contracts. Micro-Cap Portfolio

and Small-Cap Portfolio commenced operations on December 27, 1996. |

Classes of

shares have equal rights as to earnings and assets, except that each class may bear

different fees and expenses for distribution, shareholder servicing, registration

and shareholder reports, and receive different compensating balance credits and

expense reimbursements. Investment income, realized and unrealized capital gains

or losses on investments and foreign currency, and expenses other than those attributable

to a specific class are allocated to each class of shares based on its relative

net assets. |

The preparation

of financial statements in conformity with accounting principles generally accepted

in the United States requires management to make estimates and assumptions that

affect the reported amounts of assets and liabilities and the disclosure of contingent

assets and liabilities at the date of the financial statements and the reported

amounts of income and expenses during the reporting period. Actual results could

differ from those estimates. |

Each Fund

is an investment company and accordingly follows the investment company accounting

and reporting guidance of the Financial Accounting Standards Board (FASB) Accounting

Standard Codification Topic 946 “Financial Services-Investment Companies”. |

| VALUATION OF INVESTMENTS: |

Securities

are valued as of the close of trading on the New York Stock Exchange (NYSE) (generally

4:00 p.m. Eastern time) on the valuation date. Securities that trade on an exchange,

and securities traded on Nasdaq’s Electronic Bulletin Board, are valued at

their last reported sales price or Nasdaq official closing price taken from the

primary market in which each security trades or, if no sale is reported for such

day, at their highest bid price. Other over-the-counter securities for which market

quotations are readily available are valued at their highest bid price, except in

the case of some bonds and other fixed income securities which may be valued by

reference to other securities with comparable ratings, interest rates and maturities,

using established independent pricing services. The Funds value their non-U.S. dollar

denominated securities in U.S. dollars daily at the prevailing foreign currency

exchange rates as quoted by a major bank. Securities for which market quotations