Use these links to rapidly review the document

TABLE OF CONTENTS

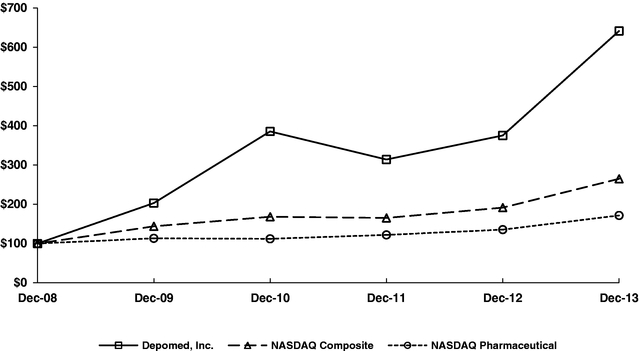

Financial Statements

TABLE OF CONTENTS2

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| (Mark one) | ||

ý |

Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

|

For the fiscal year ended December 31, 2013 |

||

OR |

||

o |

Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

|

For the transition period from: to |

||

Commission File Number: 001-13111

DEPOMED, INC.

(Exact Name of Registrant as Specified in its Charter)

| California (State or other jurisdiction of incorporation or organization) |

94-3229046 (I.R.S. Employer Identification No.) |

|

7999 Gateway Boulevard, Suite 300, Newark, California (Address of principal executive offices) |

94560 (Zip Code) |

Registrant's telephone number, including area code: (510) 744-8000

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |

|---|---|---|

| Common Stock, no par value | The NASDAQ Stock Market LLC |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer or a non-accelerated filer, as defined in Rule 12b-2 of the Exchange Act.

| Large accelerated filer o | Accelerated filer ý | Non-accelerated filer o (Do not check if a smaller reporting company) |

Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No ý

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant based upon the closing price of Common Stock on the Nasdaq Stock Market on June 30, 2013 was approximately $327,084,838. Shares of Common Stock held by each officer and director and by each person who owned 10% or more of the outstanding Common Stock as of June 30, 2013 have been excluded in that such persons may be deemed to be affiliates. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

The number of shares outstanding of the registrant's Common Stock, no par value, as of March 14, 2014 was 56,594,409.

Documents Incorporated by Reference

Portions of the registrant's Proxy Statement, which will be filed with the Securities and Exchange Commission (SEC) pursuant to Regulation 14A in connection with the registrant's 2014 Annual Meeting of Shareholders, expected to be held on or about May 20, 2014, are incorporated by reference in Part III of this Form 10-K.

DEPOMED, INC.

2013 ANNUAL FORM 10-K REPORT

TABLE OF CONTENTS

2

NOTE REGARDING FORWARD-LOOKING STATEMENTS

Statements made in this Annual Report on Form 10-K that are not statements of historical fact are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the Securities Act), and Section 21E of the Securities Exchange Act of 1934, as amended (the Exchange Act). We have based these forward-looking statements on our current expectations and projections about future events. Our actual results could differ materially from those discussed in, or implied by, these forward-looking statements. Forward-looking statements are identified by words such as "believe," "anticipate," "expect," "intend," "plan," "will," "may" and other similar expressions. In addition, any statements that refer to expectations, projections or other characterizations of future events or circumstances are forward-looking statements. Forward-looking statements include, but are not necessarily limited to, those relating to:

- •

- the commercial success and market acceptance of Gralise® (gabapentin), our once-daily product for the

management of postherpetic neuralgia, Zipsor® (diclofenac potassium) liquid filled capsules, our non-steroidal anti-inflammatory drug for the treatment of mild to moderate pain in adults,

CAMBIA® (diclofenac potassium for oral solution), our non-steroidal anti-inflammatory drug for the acute treatment of migraine attacks, Lazanda® (fentanyl) nasal spray, our

product for the management of breakthrough cancer pain in adult, opioid-tolerant cancer patients;

- •

- the results of our ongoing litigation against filers of Abbreviated New Drug Applications (each, an ANDA) to market

generic Gralise and Zipsor in the United States;

- •

- the results of our ongoing litigation with the U.S. Food and Drug Administration (FDA) to obtain orphan drug exclusivity

for Gralise in the United States;

- •

- the outcome of our ongoing patent infringement litigation against Purdue Pharma L.P. (Purdue) and Endo

Pharmaceuticals Inc. (Endo);

- •

- any additional patent infringement or other litigation that may be instituted related to Gralise, Zipsor, CAMBIA, Lazanda

or any other of our products or product candidates;

- •

- our and our collaborative partners' compliance or non-compliance with legal and regulatory requirements related to the

promotion of pharmaceutical products in the United States;

- •

- our plans to acquire, in-license or co-promote other products;

- •

- the results of our research and development efforts;

- •

- submission, acceptance and approval of regulatory filings;

- •

- our ability to raise additional capital; and

- •

- our collaborative partners' compliance or non-compliance with obligations under our collaboration agreements.

Factors that could cause actual results or conditions to differ from those anticipated by these and other forward-looking statements include those more fully described in the "ITEM 1A. RISK FACTORS" section and elsewhere in this Annual Report on Form 10-K. Except as required by law, we assume no obligation to update any forward- looking statement publicly, or to revise any forward-looking statement to reflect events or developments occurring after the date of this Annual Report on Form 10-K, even if new information becomes available in the future. Thus, you should not assume that our silence over time means that actual events are bearing out as expressed or implied in any such forward-looking statement.

3

CORPORATE INFORMATION

The address of our Internet website is http://www.depomed.com. We make available, free of charge through our website or upon written request, our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and other periodic SEC reports, along with amendments to all of those reports, as soon as reasonably practicable after we file the reports with the SEC.

Unless the context indicates otherwise, "Depomed," "the Company," "we," "our" and "us" refer to Depomed, Inc. Depomed was incorporated in the State of California on August 7, 1995. Our principal executive offices are located at 7999 Gateway Boulevard, Suite 300, Newark, California, 94560 and our telephone number is (510) 744-8000.

Depomed®, Gralise®, Zipsor®, CAMBIA®, Lazanda® and Acuform® are registered trademarks of Depomed. Glumetza® is a registered trademark of Valeant International (Barbados) SRL exclusively licensed in the United States to Depomed. All other trademarks and trade names referenced in this Annual Report on Form 10-K are the property of their respective owners.

4

COMPANY OVERVIEW

Depomed is a specialty pharmaceutical company focused on pain and other conditions and diseases of the central nervous system. The products that comprise our current specialty pharmaceutical business are Gralise® (gabapentin), a once-daily product for the management of postherpetic neuralgia (PHN) that we launched in October 2011, Zipsor® (diclofenac potassium) liquid filled capsules, our non-steriodal anti-inflammatory drug for the treatment of mild to moderate acute pain that we acquired in June 2012, CAMBIA® (diclofenac potassium for oral solution), our non-steriodal anti-inflammatory drug for the acute treatment of migraine attacks that we acquired in December 2013, and Lazanda® (fentanyl) nasal spray, our product for the management of breakthrough pain in cancer patients 18 years of age and older who are already receiving and who are tolerant to opioid therapy for their underlying persistent cancer pain that we acquired in July 2013.We actively seek to expand our product portfolio through in-licensing, acquiring or obtaining co-promotion rights to commercially available products or late-stage product candidates that could be marketed and sold effectively with our existing products through our sales and marketing capability.

We also have a portfolio of royalty and milestone producing license agreements based on our proprietary Acuform® gastroretentive drug delivery technology with Mallinckrodt Inc. (Mallinckrodt), Ironwood Pharmaceuticals, Inc. (Ironwood) and Janssen Pharmaceuticals, Inc.

In October 2013, we sold our interests in royalty and milestone payments under our license agreements in the Type 2 diabetes therapeutic area to PDL BioPharma, Inc. (PDL) for $240.5 million. The interests sold include royalty and milestone payments accruing from and after October 1, 2013: (a) from Santarus Inc. (Santarus) with respect to sales of Glumetza® (metformin HCL extended-release tablets) in the United States; (b) from Merck & Co., Inc. (Merck) with respect to sales of Janumet XR® (sitagliptin and metformin HCL extended-release); (c) from Janssen Pharmaceutica N.V. and Janssen Pharmaceuticals, Inc. (collectively, Janssen) with respect to potential future development milestones and sales of Janssen's investigational fixed-dose combination of Invokana® (canagliflozin) and extended-release metformin; (d) from Boehringer Ingelheim International GMBH (Boehringer Ingelheim) with respect to potential future development milestones and sales of the investigational fixed-dose combinations of drugs and extended-release metformin subject to our license agreement with Boehringer Ingelheim; and (e) from LG Life Sciences Ltd. (LG) and Valeant International Bermuda SRL (Valeant) for sales of extended-release metformin in Korea and Canada, respectively.

As of December 31, 2013, we have one product candidate under clinical development, DM-1992 for Parkinson's disease. DM-1992 completed a Phase 2 trial for Parkinson's disease, and we announced a summary of the results of that trial in November 2012. We continue to evaluate partnering opportunities for DM-1992 and monitor competitive developments.

SIGNIFICANT DEVELOPMENTS DURING 2013

Among the significant developments in our business during 2013 were the following:

- •

- In July 2013, we acquired Lazanda from Archimedes Pharma US Inc. (Archimedes) for $4 million in cash. Our

sales force began promoting Lazanda in August 2013.

- •

- In July 2013, the FDA accepted for filing a NDA from Mallinckrodt for XARTEMIS™ XR (oxycodone hydrochloride and acetaminophen) Extended-Release Tablets (CII), previously known as MNK-795, which is formulated with our Acuform® drug delivery technology. The NDA acceptance triggered a $5 million milestone payment to us which we received and recognized in the third quarter of 2013.

5

- •

- In October 2013, we sold our interests in royalty and milestone payments under license agreements in the Type 2

diabetes therapeutic area to PDL for $240.5 million.

- •

- In December 2013, we acquired CAMBIA from Nautilus Neurosciences, Inc. (Nautilus) for $48.7 million in cash.

- •

- Total revenues for the year ended December 31, 2013 were $134.2 million, including product revenues of

$58.3 million.

- •

- Cash, cash equivalents and marketable securities were $276.0 million as of December 31, 2013, prior to the payment of our taxes on the PDL transaction.

Commercialized Products and Product Candidate Development Pipeline

The following table summarizes our and our partners' commercialized products and product candidate development pipeline:

Depomed Commercialized Products

Product

|

Indication | Status | ||

|---|---|---|---|---|

Gralise® |

Management of postherpetic neuralgia | Currently sold in the United States Launched in October 2011 |

||

Zipsor® |

Mild to moderate acute pain in adults 18 years of age or older |

Currently sold in the United States |

||

CAMBIA® |

Acute treatment of migraine attacks in adults 18 years of age or older |

Currently sold in the United States |

||

Lazanda® |

Breakthrough pain in cancer patients 18 years of age and older who are already receiving and who are tolerant to continuous opioid therapy for their underlying persistent cancer pain |

Currently sold in the United States |

Partner Commercialized Products and Product Candidates

Product / Product Candidate

|

Indication | Partner | Status | |||

|---|---|---|---|---|---|---|

XARTEMIS™ XR (oxycodone hydrochloride and acetaminophen) |

Management of acute pain severe enough to require opioid treatment and in patients for whom alternative treatment options are ineffective, not tolerated or would otherwise be inadequate | Mallinckrodt | Approved by the FDA in March 2014 | |||

MNK-155 |

Pain |

Mallinckrodt |

Completed Phase 3 clinical trials |

6

Product / Product Candidate

|

Indication | Partner | Status | |||

|---|---|---|---|---|---|---|

NUCYNTA® ER |

Moderate to severe chronic pain; neuropathic pain associated with diabetic peripheral neuropathy (DPN) |

Janssen |

Currently sold in the United States and Canada; License covers sales of NUCYNTA® ER in the United States, Canada and Japan; |

|||

IW-3718 Refractory GERD program using Acuform® |

Refractory GERD |

Ironwood |

In clinical development |

Product

|

Indication | Status | ||

|---|---|---|---|---|

| DM-1992 | Parkinson's disease | Top-line results of Phase 2 study reported in November 2012 |

OUR BUSINESS OPERATIONS

As of December 31, 2013, our revenues are generated primarily from commercialized products and license and development arrangements.

Commercialized Products

Gralise® (Gabapentin) Tablets for the Management of PHN

Gralise is our proprietary, once-daily formulation of gabapentin for the management of PHN. We made Gralise commercially available in October 2011, following its FDA approval in January 2011 and our reacquisition of the product in March 2011 from Abbott Products, Inc. (Abbott Products), our former licensee. We received a $48 million approval milestone from Abbott in February 2011, and a settlement payment of $40 million in March 2011 in connection with the termination of our Gralise license agreement with Abbott.

Gralise product sales were $36.2 million for the year ended December 31, 2013, $17.3 million for the year ended December 31, 2012 and $0.5 million for the year ended December 31, 2011.

Postherpetic Neuralgia. PHN is a persistent pain condition caused by nerve damage during a shingles, or herpes zoster, viral infection. PHN afflicts approximately one in five patients diagnosed with shingles in the United States. The incidence of PHN increases in elderly patients. Three out of four shingles patients over 70 years old develop PHN. Approximately 200,000 Americans are affected by PHN each year. The pain associated with PHN can interfere with daily activities such as sleep and recreational activities for months, and can be associated with clinical depression.

The Centers for Disease Control and Prevention Advisory Committee on Immunization Practices recommends that adults 60 years of age and older be vaccinated with a shingles vaccine. While the shingles vaccine is not a treatment for PHN, it could impact the future market for therapies for PHN.

Orphan Drug Designation. In November 2010, the FDA granted Gralise Orphan Drug designation for the management of PHN based on a plausible hypothesis that Gralise is "clinically superior" to immediate release gabapentin due to the incidence of adverse events observed in Gralise clinical trials relative to the incidence of adverse events reported in the package insert for immediate release gabapentin. Generally, an Orphan-designated drug approved for marketing is eligible for seven years of regulatory exclusivity for the Orphan-designated indication. If granted, Orphan Drug exclusivity for Gralise will run for seven years from January 28, 2011. However, the FDA has not granted Orphan Drug exclusivity for Gralise on the basis of FDA's interpretation of the statute and regulations

7

governing Orphan Drug exclusivity. In September 2012, we filed an action in federal district court for the District of Columbia against the FDA seeking an order requiring the FDA to grant Gralise Orphan Drug exclusivity for the management of PHN. We believe Gralise is entitled to Orphan Drug exclusivity as a matter of law, and the FDA's action is not consistent with the statute or the FDA's regulations related to Orphan Drugs. The lawsuit seeks a determination by the court that Gralise is protected by Orphan Drug exclusivity, and an order that the FDA act accordingly. Briefing in the case was completed in March 2013. A hearing on our summary judgment motion was held in August 2013 and we are awaiting a decision.

Zipsor® (Diclofenac Potassium) Liquid-Filled Capsules for Treatment of Mild to Moderate Acute Pain

Zipsor is a non-steroidal anti-inflammatory drug (NSAID) indicated for relief of mild to moderate acute pain in adults. Zipsor uses proprietary ProSorb® delivery technology to deliver a finely dispersed, rapidly absorbed formulation of diclofenac. We acquired Zipsor in June 2012 from Xanodyne Pharmaceuticals, Inc. (Xanodyne) for $25.9 million in cash and the assumption of certain product-related liabilities.

We began promotion of Zipsor in July 2012. Our Zipsor product sales were $20.3 million for the year ended December 31, 2013 and $9.8 million for the year ended December 31, 2012.

Lazanda® (Fentanyl) Nasal Spray for the Management of Breakthrough Pain in Cancer Patients, 18 Years of Age and Older, who are already receiving and who are tolerant to opioid therapy for their underlying persistent cancer pain

Lazanda nasal spray is an intranasal fentanyl drug used to manage breakthrough pain in adults (18 years of age or older) who are already routinely taking other opioid pain medicines around-the-clock for cancer pain. We acquired Lazanda and certain related product inventory on July 29, 2013 from Archimedes Pharma US Inc., a Delaware corporation, Archimedes Pharma Ltd., a corporation registered under the laws of England and Wales, and Archimedes Development Ltd., a Company registered under the laws of England and Wales (collectively, Archimedes) for $4 million in cash and the assumption of certain product-related liabilities.

We began promotion of Lazanda in August 2013. Our Lazanda product sales were $1.2 million for the year ended December 31, 2013.

CAMBIA® (Diclofenac Potassium for Oral Solution) for the Acute Treatment of Migraine Attacks in Adults 18 Years of Age or Older

CAMBIA is a NSAID indicated for the acute treatment of migraine attacks with or without aura in adults 18 years of age or older. We acquired CAMBIA and related product inventory on December 17, 2013 from Nautilus Neurosciences, Inc., a Delaware corporation (Nautilus), for $48.7 million and the assumption of certain product-related liabilities. We also assumed certain annual third party royalty obligations totaling not more than 11% of CAMBIA net sales.

We began promotion of CAMBIA in late December 2013. Our CAMBIA product sales were $0.6 million for the year ended December 31, 2013, which includes approximately two weeks of sales.

License and Development Arrangements

Janssen—NUCYNTA® ER

In August 2012, we entered into a license agreement with Janssen that grants Janssen a non-exclusive license to certain patents and other intellectual property rights to our Acuform drug delivery technology for the development and commercialization of tapentadol extended release products, including NUCYNTA ER (tapentadol extended-release tablets). We received a $10 million upfront license fee and receive low single digit royalties on net sales of NUCYNTA ER in the U.S., Canada and Japan from and after July 2, 2012 through December 31, 2021.

8

Mallinckrodt (Formerly Covidien)—Acetaminophen/Opiate Combination Products

In November 2008, we entered into a license agreement related to two acetaminophen/opiate combination products with Mallinckrodt. The license agreement grants Mallinckrodt worldwide rights to utilize our Acuform technology for the exclusive development of up to four products containing acetaminophen in combination with opiates, two of which Mallinckrodt has elected to develop.

We have received $12.5 million in upfront fees and milestones under the agreement. The upfront fees included a $4.0 million upfront license fee and a $1.5 million advance payment for formulation work we performed under the agreement. The milestone payments include four $0.5 million clinical development milestones and $5 million following the FDA's July 2013 acceptance for filing of the NDA for XARTEMIS XR (oxycodone hydrochloride and acetaminophen) Extended-Release Tablets (CII), previously known as MNK-795. On March 12, 2014, the FDA approved XARTEMIS XR for the management of acute pain severe enough to require opioid treatment and in patients for whom alternative treatment options (e.g., non-opioid analgesics) are ineffective, not tolerated or would otherwise be inadequate. The approval of the NDA triggers a $10.0 million milestone payment to us, which is payable within 30 days. We will receive high single digit royalties on net sales of XARTEMIS XR.

Ironwood Pharmaceuticals, Inc.—IW-3718 for Refractory GERD

In July 2011, we entered into a collaboration and license agreement with Ironwood granting Ironwood a license for worldwide rights to certain patents and other intellectual property rights to our Acuform drug delivery technology for an IW-3718, an Ironwood product candidate under evaluation for refractory GERD. We have received $2.4 million under the agreement, which include an upfront payment, reimbursement for initial product formulation work, and two milestone payments.

Licensing and Development Agreements Sold to PDL in October 2013

In October 2013, we sold to PDL our milestone and royalty interests in our license agreements in the type 2 diabetes therapeutic area (and any replacements for the agreements) for $240.5 million. The material agreements included in the sale are described below. From and after October 1, 2013, PDL will receive all royalty and milestone payments due under the agreements until PDL has received payments equal to $481 million, after which we and PDL will share evenly all net payments received.

Santarus—Glumetza®

Glumetza is a once-daily extended release metformin product approved in the United States for type 2 diabetes that we have licensed to Santarus. We developed the 500mg Glumetza and licensed it to Biovail Laboratories, Inc. (now Valeant Pharmaceuticals International, Inc.) (Valeant) in 2002. In December 2005, we reacquired the U.S. rights to Glumetza from Valeant, including an exclusive U.S. license to the 1000mg strength of Glumetza, which was developed by Valeant utilizing proprietary Valeant drug delivery technology. The FDA approved Glumetza for marketing in the United States in 2005, and we began selling the 500mg Glumetza in 2006. In December 2007, the FDA approved the currently marketed 1000mg Glumetza, and we began selling it in June 2008. In July 2008, we entered into a promotion agreement with Santarus, granting Santarus exclusive right to promote Glumetza in the United States. Santarus began promoting Glumetza in October 2008. In August 2011, we restructured our agreement with Santarus and entered into a commercialization agreement that superseded the July 2008 promotion agreement. Under the commercialization agreement, we granted Santarus exclusive rights to manufacture and commercialize Glumetza in the United States in return for a royalty on Glumetza net sales.

9

During 2011, we distributed and sold Glumetza for the first eight months of the year, recognized Glumetza product sales and paid Santarus a promotion fee equal to 75% of Glumetza gross margin. In the final four months of the year, Santarus was responsible for Glumetza distribution and sales, recognized Glumetza product sales and paid us a royalty on net sales. During the first 8 months of 2011, we recognized $40.7 million in product sales of Glumetza, $3.8 million in cost of sales of Glumetza, and $27.3 million in promotion fee expense to Santarus. We recognized $9.6 million in royalty revenue during the final four months of 2011 under the commercialization agreement. Royalty revenue from Santarus for the year ended December 31, 2013 was $42.1 million, which includes royalties we received for the nine months ended September 30, 2013, and does not include royalties we sold to PDL.

Santarus pays royalties on Glumetza net product sales in the United States as follows: 26.5% in 2011; 29.5% in 2012; 32.0% in 2013 and 2014; and 34.5% in 2015 and beyond, prior to generic entry of a Glumetza product. In the event of generic entry of a Glumetza product in the United States, the parties will thereafter equally share Glumetza proceeds based on a gross margin split.

Merck—Janumet® XR

We have received $12.5 million in upfront and milestone payments and we receive royalties on Merck's net sales of Janumet® XR in the United States and other licensed territories through the expiration of the licensed patents under a July 2009 license agreement with Merck. The non-exclusive license agreement grants Merck a license as well as other rights to certain of our patents directed to metformin extended release technology for Janumet XR, Merck's fixed-dose combination product for type 2 diabetes containing sitagliptin and extended release metformin that was approved by the FDA in February 2012. Merck began selling Janumet XR during the first quarter of 2012.

Janssen—Canaglifozin/Metformin XR Combination Products

We have received $10 million in upfront and milestone payments, and are eligible for additional milestone payments and royalties under an August 2010 non-exclusive license agreement between us and Janssen related to fixed dose combinations of extended release metformin and Janssen's type 2 diabetes product candidate canagliflozin.

Under the agreement, we granted Janssen a license to certain patents related to our Acuform drug delivery technology to be used in developing the combination products. We also granted Janssen a right to reference the Glumetza NDA in Janssen's regulatory filings covering the products.

Boehringer Ingelheim—Undisclosed Compounds/Metformin XR Combination Products

We have received $12.5 million in upfront and milestone payments and may receive additional development milestones, as well as royalties, pursuant to a March 2011 license and service agreement with Boehringer Ingelheim related to fixed dose combinations of extended release metformin and proprietary Boehringer Ingelheim compounds in development for type 2 diabetes. Under the agreement, we granted Boehringer Ingelheim a license to certain patents related to our Acuform drug delivery technology to be used in developing the combination products. Boehringer Ingelheim was also granted a right to reference the Glumetza NDA in regulatory submissions for the products.

We received a $10.0 million upfront license payment and, in March 2012, we received an additional $2.5 million milestone payment upon delivery of experimental batches of prototype formulations that met agreed-upon specifications. The agreement provides for additional milestone payments based on regulatory filings and approval events, as well as royalties on worldwide net sales of products.

10

PRODUCT CANDIDATE

DM-1992 for Parkinson's Disease

In January 2012, we initiated a Phase 2 study to evaluate DM-1992 for the treatment of motor symptoms associated with Parkinson's disease. The trial was a randomized, active-controlled, open-label, crossover study testing DM-1992 dosed twice daily against a generic version of immediate-release carbidopa-levodopa dosed as needed. The trial enrolled 34 patients at 8 U.S. centers. The study assessed efficacy, safety and pharmacokinetic variables. The primary endpoint for the study was change in off time as measured by patient self-assessment and clinician assessment.

Enrollment was completed in July 2012 and the study was completed in September 2012. In November 2012, we reported top-line results of the Phase 2 study, which we continue to evaluate as we consider partnering opportunities for DM-1992 and monitor competitive developments.

OUR DRUG DELIVERY TECHNOLOGIES

The Acuform technology is based on our proprietary oral drug delivery technologies and is designed to include formulations of drug-containing polymeric tablets that allow multi-hour delivery of an incorporated drug. Although our formulations are proprietary, the polymers utilized in the Acuform technology are commonly used in the food and drug industries and are included in the list of inert substances approved by the FDA for use in oral pharmaceuticals. By using different formulations of the polymers, we believe that the Acuform technology is able to provide continuous, controlled delivery of drugs of varying molecular complexity and solubility. With the use of different polymers and polymers of varying molecular weight, our Acuform tablet technology can deliver drugs by diffusion, tablet erosion, or from a bi-layer matrix. In addition, our technology allows for the delivery of more than one drug from a single tablet. If taken with a meal, these polymeric tablets remain in the stomach for an extended period of time to provide continuous, controlled delivery of an incorporated drug.

The Acuform technology's design is based in part on principles of human gastric emptying and gastrointestinal transit. Following a meal, liquids and small particles flow continuously from the stomach into the intestine, leaving behind the larger undigested particles until the digestive process is complete. As a result, drugs in liquid or dissolved form or those consisting of small particles tend to empty rapidly from the stomach and continue into the small intestine and on into the large intestine, often before the drug has time to act locally or to be absorbed in the stomach and/or upper small intestine. The drug-containing polymeric tablets of the Acuform technology are formulated into easily swallowed shapes and are designed to swell upon ingestion. The tablets attain a size after ingestion sufficient to be retained in the stomach for multiple hours during the digestive process while delivering the drug content at a controlled rate. After drug delivery is complete, the polymeric tablet dissolves and becomes a watery gel, which is safely eliminated through the intestine sight unseen.

The Acuform technology is designed to address certain limitations of drug delivery and to provide for orally-administered, conveniently-dosed, cost-effective drug therapy that provides continuous, controlled-delivery of a drug over a multi-hour period. We believe that the Acuform technology can provide one or more of the following advantages over conventional methods of drug administration:

- •

- Greater Patient and Caregiver Convenience. We believe that

the Acuform technology may offer once-daily or reduced frequency dosing for certain drugs that are currently required to be administered several times daily.

- •

- Enhanced Safety and Efficacy through Controlled Delivery. We believe that the Acuform technology may improve the ratio of therapeutic effect to toxicity by decreasing the initial peak concentrations of a drug associated with toxicity, while maintaining levels of the drug at therapeutic, subtoxic concentrations for an extended period of time.

11

- •

- More Efficient Gastrointestinal Drug Absorption. We

believe that the Acuform technology can be used for improved oral administration of drugs that are inadequately absorbed when delivered as conventional tablets or capsules. Many drugs are primarily

absorbed in the stomach, duodenum or upper small intestine regions, through which drugs administered in conventional oral dosage forms transit quickly. In contrast, the Acuform technology is designed

to be retained in the stomach, allowing for multi-hour flow of drugs to these regions of the gastrointestinal tract.

- •

- Rational Drug Combinations. We believe that the Acuform technology may allow for rational combinations of drugs with different biological half-lives. Physicians frequently prescribe multiple drugs for treatment of a single medical condition. By appropriately incorporating different drugs into an Acuform technology we believe that we can provide for the release of each incorporated drug continuously at a rate and duration (dose) appropriately adjusted for the specific biological half-lives of the drugs.

RESEARCH AND DEVELOPMENT EXPENSES

Our research and development expenses were $8.1 million in 2013, $15.5 million in 2012 and $15.2 million in 2011. We expect research and development expense in 2014 to increase from 2013 levels, primarily as a result of pediatric studies relating to Zipsor and CAMBIA that we intend to undertake in 2014.

PATENTS AND PROPRIETARY RIGHTS

The material issued United States patents we own or have licensed, and the products they cover, are as follows:

Product

|

U.S. Patent Nos. (Exp. Dates) | |

|---|---|---|

| Gralise | 7,438,927 (February 26, 2024) | |

7,731,989 (October 25, 2022) |

||

8,192,756 (October 25, 2022) |

||

8,252,332(October 25, 2022) |

||

8,333,992 (October 25, 2022) |

||

6,723,340 (October 25, 2021) |

||

6,488,962 (June 20, 2020) |

||

6,340,475 and 6,635,280 (September 19, 2016) |

||

Zipsor |

7,662,858 (February 24, 2029) |

|

7,884,095 (February 24, 2029) |

||

7,939,518 (February 24, 2029) |

||

8,110,606 (February 24, 2029) |

||

8,623,920 (February 24, 2029) |

||

6,365,180 (July 15, 2019) |

||

CAMBIA |

7,759,394* and 8,097,651* (June 16, 2026) |

|

6,974,595* and 7,482,377* (May 15, 2017) |

||

Lazanda |

8,216,604 (October 3, 2024) |

|

6,432,440 (April 20, 2018) |

- *

- Patent rights are exclusively in-licensed by Depomed.

12

Our success will depend in part on our ability to obtain and maintain patent protection for our products and technologies. Our policy is to seek to protect our proprietary rights, by among other methods, filing patent applications in the United States and foreign jurisdictions to cover certain aspects of our technology. In addition to those patents noted on the above table, we have 19 patent applications pending in the United States. Our pending patent applications may lack priority over other applications or may not result in the issuance of patents. Even if issued, our patents may not be sufficiently broad to provide protection against competitors with similar technologies and may be challenged, invalidated or circumvented, which could limit our ability to stop competitors from marketing related products or may not provide us with competitive advantages against competing products. We also rely on trade secrets and proprietary know-how, which are difficult to protect. We seek to protect such information, in part, through entering into confidentiality agreements with employees, consultants, collaborative partners and others before such persons or entities have access to our proprietary trade secrets and know-how. These confidentiality agreements may not be effective in certain cases. In addition, our trade secrets may otherwise become known or be independently developed by competitors.

Our ability to develop our technologies and to make commercial sales of products using our technologies also depends on not infringing other patents or intellectual property rights. We are not aware of any intellectual property claims against us. However, the pharmaceutical industry has experienced extensive litigation regarding patents and other intellectual property rights. If claims concerning any of our products were to arise and it is determined that these products infringe a third party's proprietary rights, we could be subject to substantial damages for past infringement or be forced to stop or delay our activities with respect to any infringing product, unless we can obtain a license, or we may have to redesign our product so that it does not infringe upon such third party's patent rights, which may not be possible or could require substantial funds or time. Such a license may not be available on acceptable terms, or at all. Even if we, our collaborators or our licensors were able to obtain a license, the rights may be nonexclusive, which would give our competitors access to the same intellectual property.

From time to time, we may become aware of activities by third parties that may infringe our patents. We may need to engage in litigation to enforce any patents issued or licensed to us or to determine the scope and validity of third-party proprietary rights, such as litigation described in "Legal Proceedings". Our issued or licensed patents may not be held valid by a court of competent jurisdiction. Whether or not the outcome of litigation is favorable to us, defending a lawsuit takes significant time, may be expensive and may divert management attention from other business concerns. Adverse determinations in litigation or interference proceedings could require us to seek licenses which may not be available on commercially reasonable terms, or at all, or subject us to significant liabilities to third parties. If we need but cannot obtain a license, we may be prevented from marketing the affected product.

MARKETING AND SALES

We have developed capabilities in various aspects of our commercial organization through our commercialization of Gralise, Zipsor, CAMBIA and Lazanda, including sales, marketing, manufacturing, quality assurance, wholesale distribution, medical affairs, managed market contracting, government price reporting, compliance, maintenance of the product NDA and review and submission of promotional materials. Members of our commercial organization are also engaged in the commercial and marketing assessments of our other potential product candidates.

Our sales organization includes 180 full-time sales representatives. Our sales force primarily calls on pain specialists, neurologists and primary care physicians throughout most of the United States. Our marketing organization is comprised of professionals who have developed a variety of marketing

13

techniques and programs to promote our products, including promotional materials, speaker programs, industry publications, advertising and other media.

MANUFACTURING

Our facility is used for office and research and development (R&D) purposes. No commercial manufacturing takes place at our facility. The R&D work includes preclinical development of pharmaceutical formulations, their characterization, and the development of pharmaceutical processes for external commercial manufacturing. The total laboratory area includes the following individual labs: Analytical Development Lab, Formulation Dry Lab, Process Lab and Quality Lab.

We are responsible for the supply and distribution of our marketed products. For Gralise, we have entered into a manufacturing agreement with Patheon, as our sole commercial supplier. Accucaps Industries Limited (Accucaps) is our sole supplier for Zipsor pursuant to a manufacturing agreement we assumed in connection with our acquisition of Zipsor from Xanodyne in June 2012. DPT Lakewood, Inc. (DPT) is our sole supplier for Lazanda pursuant to a manufacturing and supply agreement that we assumed in connection with our July 2013 acquisition of Lazanda. MiPharm, S.p.A. (MiPharm) is our sole supplier for CAMBIA pursuant to a manufacturing and supply agreement that we assumed in connection with our December 2013 acquisition of CAMBIA.

We have two qualified suppliers for the active pharmaceutical ingredient in Gralise. We have a supply agreement with one of the suppliers, and obtain the active pharmaceutical ingredient from the other supplier on a purchase order basis only. We also obtain polyethylene oxide, one of the excipients common to Gralise and products under development by our partners, on a purchase order basis from Dow Chemical, our sole source for polyethylene oxide. We currently have no long-term supply arrangement with respect to polyethylene oxide.

Applicable current Good Manufacturing Practices (cGMP) requirements and other rules and regulations prescribed by foreign regulatory authorities apply to the manufacture of our products, including products using the Acuform technology. We depend on the manufacturers of our products to comply with cGMP and applicable foreign standards. Any failure by a manufacturer to maintain cGMP or comply with applicable foreign standards could delay or prevent the initial or continued commercial sale of our products and the products being sold or developed by parties with whom we have license or development agreements.

COMPETITION

General. We believe that we compete favorably in the markets described above on the basis of the safety and efficacy of our products and product candidates, and in some cases on the basis of the price of our products. However, competition in pharmaceutical products and drug delivery technologies is intense, and we expect competition to increase. There may be other companies developing products competitive with ours of which we are unaware. Competing product or technologies developed in the future may prove superior to our products or technologies, either generally or in particular market segments. These developments could make our products or technologies noncompetitive or obsolete.

Most of our principal competitors have substantially greater financial, sales, marketing, personnel and research and development resources than we do. In addition, many of our potential collaborative partners have devoted, and continue to devote, significant resources to the development of their own products and drug delivery technologies.

Gralise for Postherpetic Neuralgia. Gabapentin is currently marketed by Pfizer Inc. (Pfizer) as Neurontin and by several generic manufacturers for adjunctive therapy for epileptic seizures and for postherpetic pain. In addition, Pfizer's product Lyrica ® (pregabalin) has been approved for marketing in the United States and the European Union for the management of PHN, diabetic nerve pain, spinal

14

cord injury nerve pain, fibromyalgia, and for therapy in partial onset seizures. Gralise competes against these products and other neuropathic pain treatments, such as anti-depressants, anti-convulsants, local anesthetics used as regional nerve blockers, anti-arrythmics and opioids.

Zipsor for Mild to Moderate Pain. Diclofenac, the active pharmaceutical ingredient in Zipsor, is a NSAID that is approved in the United States for the treatment of mild to moderate pain and inflammation, including the symptoms of arthritis. Both branded and generic versions of diclofenac are marketed in the United States. Zipsor competes against other drugs that are widely used to treat mild to moderate pain in the acute setting. In addition, a number of other companies are developing NSAIDs in a variety of dosage forms for the treatment of mild to moderate pain and related indications. Other drugs are in clinical development to treat acute pain.

Lazanda for the Management of Breakthrough Pain in Cancer Patients. Lazanda (fentanyl) nasal spray is an intranasal fentanyl drug used to manage breakthrough pain in adults (18 years of age or older) who are already routinely taking other opioid pain medicines around-the-clock for cancer pain. Fentanyl, an opioid analgesic, is currently sold by a number of companies for the treatment of breakthrough pain in opioid-tolerant cancer patients. Branded fentanyl products against which Lazanda currently competes include Subsys®, which is sold by Insys Therapeutics, Inc. (Insys), Fentora® and Actiq®, which are sold by Cephalon, Inc. (Cephalon), Abstral®, which is sold by Galena Biopharma, Inc. (Galena) and Onsolis®, which is sold by BioDelivery Sciences International, Inc. (BDSI). Generic fentanyl products against which Lazanda currently competes are sold by Mallinckrodt, Par Pharmaceutical Companies, Inc. (Par) and Actavis, Inc. (Actavis).

CAMBIA for the Acute Treatment of Migraine Attacks. Diclofenac, the active pharmaceutical ingredient in CAMBIA, is a NSAID approved in the United States for the acute treatment of migraine in adults. CAMBIA competes with a number of triptans which are used to treat migraine and certain other headaches. Currently, seven triptans are available and sold in the United States (almotriptan, eletriptan, frovatriptan, naratriptan, rizatriptan, sumatriptan and zolmitriptan), as well as a fixed-dose combination product containing sumatriptan plus naproxen. There are other products prescribed for or under development for the treatment of migraines which are now or may become competitive with CAMBIA.

Drug Delivery Technologies. Other companies that have oral drug delivery technologies competitive with the Acuform technology include Elan Corporation, Bristol-Myers Squibb, Teva Pharmaceutical Industries Ltd., Johnson & Johnson, SkyePharma plc, Valeant, Flamel Technologies S.A., Ranbaxy Laboratories, Ltd. and Intec Pharma, all of which develop oral tablet products designed to release the incorporated drugs over time. Each of these companies has patented technologies with attributes different from ours, and in some cases with different sites of delivery to the gastrointestinal tract.

GOVERNMENT REGULATION

Product Development

Numerous governmental authorities in the United States and other countries regulate our research and development activities and those of our collaborative partners. Governmental approval is required of all potential pharmaceutical products using the Acuform technology and the manufacture and marketing of products using the Acuform technology prior to the commercial use of those products. The regulatory process takes several years and requires substantial funds. If new products using the Acuform technology do not receive the required regulatory approvals or if such approvals are delayed, our business would be materially adversely affected. We cannot be certain that the requisite regulatory approvals will be obtained without lengthy delays, if at all.

In the United States, the FDA rigorously regulates pharmaceutical products, including any drugs using the Acuform technology. If a company fails to comply with applicable requirements, the FDA or

15

the courts may impose sanctions. These sanctions may include civil penalties, criminal prosecution of the company or its officers and employees, injunctions, product seizure or detention, product recalls and total or partial suspension of production. The FDA may withdraw approved applications or refuse to approve pending new drug applications, premarket approval applications, or supplements to approved applications.

We may be required to conduct preclinical testing on laboratory animals of new pharmaceutical products prior to commencement of clinical studies involving human beings. These studies evaluate the potential efficacy and safety of the product. If preclinical testing is required, we must submit the results of the studies to the FDA as part of an Investigational New Drug Application, which must become effective before beginning clinical testing in humans.

The products we develop generally are or will be submitted for approval under Section 505(b)(2) of the FDCA which was enacted as part of the Drug Price Competition and Patent Term Restoration Act of 1984, otherwise known as the Hatch-Waxman Act. Section 505(b)(2) permits the submission of a NDA where at least some of the information required for approval comes from studies not conducted by or for the applicant and for which the applicant has not obtained a right of reference. For instance, the NDA for Gralise relies on the FDA's prior approval of Neurontin® (gabapentin), the immediate release formulation of gabapentin initially approved by the FDA.

Typically, human clinical evaluation involves a time-consuming and costly three-phase process:

- •

- In Phase 1, we conduct clinical trials with a small number of subjects to determine a drug's early safety profile

and its pharmacokinetic pattern.

- •

- In Phase 2, we conduct limited clinical trials with groups of patients afflicted with a specific disease in order

to determine preliminary efficacy, optimal dosages and further evidence of safety.

- •

- In Phase 3, we conduct large-scale, multi-center, comparative trials with patients afflicted with a target disease in order to provide enough data to statistically evaluate the efficacy and safety of the product candidate, as required by the FDA.

The FDA closely monitors the progress of each phase of clinical testing. The FDA may, at its discretion, re-evaluate, alter, suspend or terminate testing based upon the data accumulated to that point and the FDA's assessment of the risk/benefit ratio to patients. The FDA may also require additional clinical trials after approvals, which are known as Phase 4 trials. We expect to conduct Phase 4 trials for Lazanda and CAMBIA during 2014.

The results of preclinical and clinical testing are submitted to the FDA in the form of a NDA, for approval prior to commercialization. A NDA requires that our products are compliant with cGMP. Failure to achieve or maintain cGMP standards for our products would adversely impact their marketability. In responding to a NDA, the FDA may grant marketing approval, request additional information or deny the application. Failure to receive approval for any products using the Acuform technology would have a material adverse effect on us.

Foreign regulatory approval of a product must also be obtained prior to marketing the product internationally. Foreign approval procedures vary from country to country. The time required for approval may delay or prevent marketing in certain countries. In certain instances we or our collaborative partners may seek approval to market and sell certain products outside of the United States before submitting an application for United States approval to the FDA. The clinical testing requirements and the time required to obtain foreign regulatory approvals may differ from that required for FDA approval. Although there is now a centralized European Union (EU) approval mechanism in place, each EU country may nonetheless impose its own procedures and requirements. Many of these procedures and requirements are time-consuming and expensive. Some EU countries

16

require price approval as part of the regulatory process. These constraints can cause substantial delays in obtaining required approval from both the FDA and foreign regulatory authorities after the relevant applications are filed, and approval in any single country may not meaningfully indicate that another country will approve the product.

Reimbursement

Sales of pharmaceutical products in the United States depend in significant part on the extent of coverage and reimbursement from government programs, including Medicare and Medicaid, as well as other third party payers. Third party payers are undertaking efforts to control the cost of pharmaceutical products, including by implementing cost containment measures to control, restrict access to, or influence the purchase of drugs and other health care products and services.

Government programs may regulate reimbursement, pricing, and coverage of products in order to control costs or to affect levels of use of certain products. Private health insurance plans may restrict coverage of some products, such as by using payer formularies under which only selected drugs are covered, variable co-payments that make drugs that are not preferred by the payer more expensive for patients, and by employing utilization management controls, such as requirements for prior authorization or prior failure on another type of treatment.

Fraud and Abuse

Pharmaceutical companies that participate in federal healthcare programs are subject to various U.S. federal and state laws pertaining to healthcare "fraud and abuse," including anti-kickback and false claims laws. Violations of U.S. federal and state fraud and abuse laws may be punishable by criminal or civil sanctions, including fines, civil monetary penalties and exclusion from federal healthcare programs (including Medicare and Medicaid).

Federal statutes that apply to us include the federal Anti-Kickback Statute, which prohibits persons from knowingly and willfully soliciting, offering, receiving, or providing remuneration in exchange for or to generate business, including the purchase or prescription of a drug, that is reimbursable by a federal healthcare program such as Medicare and Medicaid, and the Federal False Claims Act (FCA), which generally prohibits knowingly and willingly presenting, or causing to be presented, for payment to the federal government any false, fraudulent or medically unnecessary claims for reimbursed drugs or services. Government enforcement agencies and private whistleblowers have asserted liability under the FCA for claims submitted involving inadequate care, kickbacks, improper promotion of off-label uses and misreporting of drug prices to federal agencies.

Similar state laws and regulations, such as state anti-kickback and false claims laws, may apply to sales or marketing arrangements and claims involving healthcare items or services reimbursed by non-governmental payers, including private insurers. These state laws may be broader in scope than their federal analogues, such as state false claims laws that apply where a claim is submitted to any third-party payer, regardless of whether the payer is a private health insurer or a government healthcare program, and state laws that require pharmaceutical companies to certify compliance with the pharmaceutical industry's voluntary compliance guidelines.

Federal and state authorities have increased enforcement of fraud and abuse laws within the pharmaceutical industry, and private individuals have been active in alleging violations of the law and bringing suits on behalf of the government under the FCA. These laws are broad in scope and there may not be regulations, guidance, or court decisions that definitively interpret these laws and apply them to particular industry practices. In addition, these laws and their interpretations are subject to change.

17

Other U.S. Healthcare Laws

The Patient Protection and Affordable Care Act, as amended by the Health Care and Education Reconciliation Act of 2010 (collectively, the ACA) contains provisions that have or could potentially impact our business, including (a) an increase in the minimum Medicaid rebate to states participating in the Medicaid program on branded prescription drugs; (b) the extension of the Medicaid rebate to managed care organizations that dispense drugs to Medicaid beneficiaries; and (c) the expansion of the 340B Public Health Service Act drug pricing program, which provides outpatient drugs at reduced rates, to include certain children's hospitals, free standing cancer hospitals, critical access hospitals and rural referral centers.

Additionally, the federal "sunshine" provisions, enacted in 2010 as part of ACA, require pharmaceutical manufacturers, among others, to disclose annually to the federal government (for re-disclosure to the public) certain payments made to physicians and certain other healthcare practitioners or to teaching hospitals. State laws may also require disclosure of pharmaceutical pricing information and marketing expenditures and impose penalties for failures to disclose. Many of these laws and regulations contain ambiguous requirements. As a result of the ambiguity in certain of these laws and their implementation, our reporting actions could be subject to the penalty provisions of the pertinent federal and state laws and regulations.

Our operations and business are subject to a number of other laws and regulations, including those relating to the workplace, privacy, laboratory practices and the purchase, storage, movement, import and export and use and disposal of hazardous or potentially hazardous substances as well as controlled substances. In addition, state laws may also govern the privacy and security of health information in some circumstances and may contain different or broader privacy protections than the federal provisions.

EMPLOYEES

As of March 14, 2014, we had 308 full-time employees. At December 31, 2013, we had 291 full-time employees. None of our employees are represented by a collective bargaining agreement, nor have we experienced any work stoppage. We believe that our relations with our employees are good.

In addition to other information in this report, the following factors should be considered carefully in evaluating an investment in our securities. If any of the risks or uncertainties described in this Form 10-K actually occurs, our business, results of operations or financial condition could be materially adversely affected. The risks and uncertainties described in this Form 10-K are not the only ones facing us. Additional risks and uncertainties of which we are unaware or that we currently deem immaterial may also become important factors that may harm our business, results of operations and financial condition.

If we do not successfully commercialize Gralise, Zipsor, Lazanda and CAMBIA, our business will suffer.

In October 2011, we began commercial sales of Gralise. In June 2012, we acquired Zipsor, and we began commercial promotion of Zipsor in late July 2012. In July 2013, we acquired and began commercial promotion of Lazanda. In December 2013, we acquired and began commercial promotion of CAMBIA. As a company, we have limited experience selling and marketing pharmaceutical products. In addition to the risks discussed elsewhere in this section, our ability to successfully

18

commercialize and generate revenues from Gralise, Zipsor, Lazanda and CAMBIA depend on a number of factors, including, but not limited to our ability to:

- •

- develop and execute our sales and marketing strategies for our products;

- •

- achieve market acceptance of our products;

- •

- obtain and maintain adequate coverage, reimbursement and pricing from managed care, government and other third-party

payers;

- •

- to maintain, manage or scale the necessary sales, marketing, manufacturing, managed markets and other capabilities and

infrastructure that are required to successfully commercialize our products;

- •

- to maintain intellectual property protection for our products; and

- •

- to comply with applicable regulatory requirements.

If we are unable to successfully achieve or perform these functions, we will not be able to maintain or increase our revenues from Gralise, Zipsor, Lazanda and CAMBIA and our business will suffer.

If generic manufacturers use litigation and regulatory means to obtain approval for generic versions of our products, our business will suffer.

Under the Federal Food, Drug and Cosmetics Act (FDCA), the FDA can approve an Abbreviated New Drug Application (ANDA) for a generic version of a branded drug without the ANDA applicant undertaking the clinical testing necessary to obtain approval to market a new drug. In place of such clinical studies, an ANDA applicant usually needs only to submit data demonstrating that its product has the same active ingredient(s) and is bioequivalent to the branded product, in addition to any data necessary to establish that any difference in strength, dosage form, inactive ingredients, or delivery mechanism does not result in different safety or efficacy profiles, as compared to the reference drug.

The FDCA requires an applicant for a drug that relies, at least in part, on the patent of one of our branded drugs to notify us of their application and potential infringement of our patent rights. Upon receipt of this notice we have 45 days to bring a patent infringement suit in federal district court against the company seeking approval of a product covered by one of our patents. The discovery, trial and appeals process in such suits can take several years. If such a suit is commenced, the FDCA provides a 30-month stay on the FDA's approval of the competitor's application. Such litigation is often time-consuming and quite costly and may result in generic competition if the patents at issue are not upheld or if the generic competitor is found not to infringe such patents. If the litigation is resolved in favor of the applicant or the challenged patent expires during the 30-month stay period, the stay is lifted and the FDA may thereafter approve the application based on the standards for approval of ANDAs.

We are currently involved in patent infringement litigation against filers of three ANDAs to Gralise in connection with lawsuits consolidated in the United States District Court for the District of New Jersey, as described in greater detail under "LEGAL PROCEEDINGS" below. The lawsuits were filed in March 2012 and May 2012 against ANDA filers Actavis Elizabeth LLC (Actavis), Incepta Pharmaceuticals (Incepta), and Zydus Pharmaceuticals USA and Cadila Healthcare Limited (collectively, Zydus) for infringement of nine U.S. patents listed in the Patent and Exclusivity Information Addendum of FDA's publication, Approved Drug Products with Therapeutic Equivalence Evaluations (commonly known as the "Orange Book") for Gralise. We commenced the lawsuits within the 45 days required to automatically stay, or bar, the FDA from approving the ANDAs for 30 months or until a district court decision that is adverse to the asserted patents, whichever may occur earlier. The 30-month stays expire between July 2014 and October 2014. If the litigation is still ongoing after expiration of the applicable 30-month stay, the termination of the stay could result in the introduction

19

of one or more products generic to Gralise prior to resolution of the litigation. Any introduction of one or more products generic to Gralise would harm our business, financial condition and results of operations.

On June 28, 2013, we received from Banner Pharmacaps Inc. (Banner) a Notice of Certification for U.S. Patent Nos. 6,365,180; 7,662,858; 7,884,095; 7,939,518 and 8,110,606 under 21 U.S.C. § 355 (j)(2)(A)(vii)(IV) (Zipsor Paragraph IV Letter) certifying that Banner has submitted and the FDA has accepted for filing an ANDA for diclofenac potassium capsules, 25 mg (Banner ANDA Product). The letter states that the Banner ANDA Product contains the required bioavailability or bioequivalence data to Zipsor and certifies that Banner intends to obtain FDA approval to engage in commercial manufacture, use or sale of Banner's ANDA product before the expiration of the above identified patents, which are listed for Zipsor in the Orange Book. We commenced the lawsuit within the 45 days required to automatically bar the FDA from approving the Banner ANDA Product for 30 months or until a district court decision that is adverse to the asserted patents, whichever may occur earlier. Absent a court order, the 30-month stay is expected to expire in December 2015.

Any introduction of one or more products generic to Gralise, Zipsor, Lazanda or CAMBIA would harm our business, financial condition and results of operations. The filing of the ANDAs described above, or any other ANDA or similar application in respect to any of our products could have an adverse impact on our stock price. Moreover, if the patents covering our products were not upheld in litigation or if a generic competitor is found not to infringe these patents, the resulting generic competition would have a material adverse effect on our business, results of operations and financial condition.

We may be unable to compete successfully in the pharmaceutical industry.

Gabapentin is currently sold by Pfizer as Neurontin® for adjunctive therapy for epileptic seizures and for PHN. Pfizer's basic U.S. patents relating to Neurontin have expired, and numerous companies have received approval to market generic versions of the immediate release product. Pfizer has also developed Lyrica® (pregabalin), which has been approved for marketing in the United States for post herpetic pain, fibromyalgia, diabetic nerve pain, adjunctive therapy, epileptic seizures and nerve pain associated with spinal cord injury. In June 2012, GlaxoSmithKline and Xenoport, Inc. received approval to market Horizant™ (gabapentin enacarbil extended-release tablets) for the management of PHN. There are other products prescribed for or under development for PHN which are now or may become competitive with Gralise.

Diclofenac, the active pharmaceutical ingredient in Zipsor, is a NSAID that is approved in the United States for the treatment of mild to moderate pain in adults, including the symptoms of arthritis. Both branded and generic versions of diclofenac are marketed in the U.S. Zipsor competes against other drugs that are widely used to treat mild to moderate pain in the acute setting. In addition, a number of other companies are developing NSAIDs in a variety of dosage forms for the treatment of mild to moderate pain and related indications. Other drugs are in clinical development to treat acute pain.

An alternate formulation of diclofenac is the active ingredient in CAMBIA that is approved in the United States for the acute treatment of migraine in adults. CAMBIA competes with a number of triptans which are used to treat migraine and certain other headaches. Currently, seven triptans are available and sold in the United States (almotriptan, eletriptan, frovatriptan, naratriptan, rizatriptan, sumatriptan and zolmitriptan), as well as a fixed-dose combination product containing sumatriptan plus naproxen. There are other products prescribed for or under development for the treatment of migraines which are now or may become competitive with CAMBIA.

Fentanyl, an opioid analgesic, is currently sold by a number of companies for the treatment of breakthrough pain in opioid-tolerant cancer patients. Branded fentanyl products against which Lazanda

20

currently competes include Subsys®, which is sold by Insys, Fentora® and Actiq®, which are sold by Cephalon, Abstral®, which is sold by Galena and Onsolis®, which is sold by BDSI. Generic fentanyl products against which Lazanda currently competes are sold by Mallinckrodt, Par and Actavis.

Competition in the pharmaceutical industry is intense. We expect competition to increase. Competing products developed in the future may prove superior to our products. Most of our principal competitors have substantially greater financial, sales, marketing, personnel and research and development resources than we do.

If we are unable to negotiate acceptable pricing or obtain adequate reimbursement for our products from third-party payers, our business will suffer.

Sales of our products will depend in part on the availability of acceptable pricing and adequate reimbursement from third-party payers such as:

- •

- government health administration authorities;

- •

- private health insurers;

- •

- health maintenance organizations;

- •

- managed care organizations;

- •

- pharmacy benefit management companies; and

- •

- other healthcare-related organizations.

If reimbursement is not available for our products or product candidates, demand for these products may be limited. Further, any delay in receiving approval for reimbursement from third-party payers could have an adverse effect on our future revenues. Third-party payers are increasingly challenging the price and cost-effectiveness of medical products and services. Significant uncertainty exists as to the reimbursement status of newly approved healthcare products, including pharmaceuticals. Our products may not be considered cost effective, and adequate third-party reimbursement may be unavailable to enable us to maintain price levels sufficient to realize an acceptable return on our investment.

Federal and state governments in the United States continue to propose and pass new legislation, such as the ACA, that is designed to contain or reduce the cost of healthcare. Cost control initiatives could decrease the price that we receive for our products and any product that we may develop or acquire.

If we do not obtain Orphan Drug exclusivity for Gralise in PHN, our business could suffer.

In November 2010, the FDA granted Gralise Orphan Drug designation for the management of PHN based on a plausible hypothesis that Gralise is "clinically superior" to immediate release gabapentin due to the incidence of adverse events observed in Gralise clinical trials relative to the incidence of adverse events reported in the package insert for immediate release gabapentin. Generally, an Orphan-designated drug approved for marketing is eligible for seven years of regulatory exclusivity for the Orphan-designated indication. If granted, Orphan Drug exclusivity for Gralise will run for seven years from January 28, 2011. However, the FDA has not granted Orphan Drug exclusivity based on the FDA's interpretation of the statute and regulations governing Orphan Drug exclusivity. In September 2012, we filed an action in federal district court for the District of Columbia against the FDA seeking an order requiring the FDA to grant Gralise Orphan Drug exclusivity for the management of PHN. We believe Gralise is entitled to Orphan Drug exclusivity as a matter of law, and the FDA's action is not consistent with the statute or the FDA's regulations related to Orphan Drugs. The lawsuit seeks a

21

determination by the court that Gralise is protected by Orphan Drug exclusivity, and an order that the FDA act accordingly.

If we do not secure Orphan Drug exclusivity in PHN for Gralise, the period of market exclusivity in the United States for Gralise may be reduced, which would adversely affect our business, results of operations and financial condition.

Health care reform could increase our expenses and adversely affect the commercial success of our products.

The ACA includes numerous provisions that affect pharmaceutical companies, some of which became effective immediately upon President Obama signing the law, and others of which will take effect over the next several years. For example, the ACA seeks to expand healthcare coverage to the uninsured through private health insurance reforms and an expansion of Medicaid. The ACA also imposes substantial costs on pharmaceutical manufacturers, such as an increase in liability for rebates paid to Medicaid, new drug discounts that must be offered to certain enrollees in the Medicare prescription drug benefit and an annual fee imposed on all manufacturers of brand prescription drugs in the U.S. The ACA also requires increased disclosure obligations and an expansion of an existing program requiring pharmaceutical discounts to certain types of hospitals and federally subsidized clinics and contains cost-containment measures that could reduce reimbursement levels for pharmaceutical products. The ACA also includes provisions known as the Physician Payments Sunshine Act, which require manufacturers of drugs, biologics, devices and medical supplies covered under Medicare and Medicaid starting in 2013 to record any transfers of value to physicians and teaching hospitals and to report this data beginning in 2014 to the Centers for Medicare and Medicaid Services for subsequent public disclosure. Similar reporting requirements have also been enacted on the state level domestically, and an increasing number of countries worldwide either have adopted or are considering similar laws requiring transparency of interactions with health care professionals. Failure to report appropriate data may result in civil or criminal fines and/or penalties. These and other aspects of the ACA, including the regulations that may be imposed in connection with the implementation of the ACA, could increase our expenses and adversely affect our ability to successfully commercialize our products and product candidates.

Acquisition of new and complementary businesses, products and technologies is a key element of our corporate strategy. If we are unable to successfully identify and acquire such businesses, products or technologies, our business and prospects will be limited.

Since June 2012, we have acquired Zipsor, Lazanda and CAMBIA. An important element of our business strategy is to actively seek to acquire products or companies and to in-license or seek co-promotion rights to products that could be sold by our sales force. We cannot be certain that we will be able to successfully pursue and complete any further acquisitions, or whether we would be able to successfully integrate any acquired business, product or technology or retain any key employees. Integrating any business, product or technology we may acquire could be expensive and time consuming, disrupt our ongoing business and distract our management. If we are unable to enhance and broaden our product offerings, unable to effectively integrate any acquired businesses, products or technologies, or achieve the anticipated benefits of any acquired business, product or technology, our business and prospects will be limited. In addition, any amortization or charges resulting from the costs of such acquisitions will adversely affect our operating results.

If we engage in strategic transactions that fail to achieve the anticipated results and synergies, our business will suffer.

We may seek to engage in strategic transactions with third parties, such as company acquisitions, strategic partnerships, joint ventures, divestitures or business combinations. We may face significant competition in seeking potential strategic partners and transactions, and the negotiation process for

22

acquiring any product or engaging in strategic transactions can be time-consuming and complex. Engaging in strategic transactions may require us to incur non-recurring and other charges, increase our near and long-term expenditures, pose integration challenges and fail to achieve the anticipated results or synergies or distract our management and business, which may harm our business.

Pharmaceutical marketing is subject to substantial regulation in the United States and any failure by us or our collaborative partners to comply with applicable statutes or regulations could adversely affect our business.