THE INSTRUCTIONS ACCOMPANYING THIS LETTER OF TRANSMITTAL AND ELECTION FORM SHOULD BE READ CAREFULLY BEFORE THIS LETTER OF TRANSMITTAL AND ELECTION FORM IS COMPLETED. THIS LETTER OF TRANSMITTAL AND ELECTION FORM IS ONLY FOR USE BY REGISTERED HOLDERS OF CLASS A SHARES OF BROOKFIELD ASSET MANAGEMENT INC. IN CONNECTION WITH THE PROPOSED PLAN OF ARRANGEMENT INVOLVING BROOKFIELD ASSET MANAGEMENT INC., BROOKFIELD ASSET MANAGEMENT LTD. AND OTHERS AND RESULTING IN THE SEPARATION OF BROOKFIELD ASSET MANAGEMENT INC. INTO BROOKFIELD ASSET MANAGEMENT LTD. AND BROOKFIELD CORPORATION.

Letter of Transmittal

and Election Form

For Registered Holders of Class A Shares of

Brookfield Asset Management Inc.

In Connection with the Proposed Plan of Arrangement Involving

BROOKFIELD ASSET MANAGEMENT INC.

and

BROOKFIELD ASSET MANAGEMENT LTD.

together with others

Use this letter of transmittal and election form if:

You wish to elect to acquire Class A Shares for their fair market value and deposit certificate(s) or direct registration system (DRS) advice(s) representing Corporation Class A Shares in connection with the Arrangement.

Do not use this letter of transmittal if:

You are a Taxable Canadian Holder of Corporation Class A Shares. Such holders are not required to complete and return this letter of transmittal and election form and will be entitled to rollover treatment with respect to the Class A Shares under the Arrangement.

OR

You wish to deposit certificate(s) or DRS advice(s) representing Corporation Class A Preference Shares, Series 8 or Corporation Class A Preference Shares, Series 9 in connection with the Arrangement. Such Registered Holders should use the separate letter of transmittal for Registered Holders of Corporation Class A Preference Shares, Series 8 and Corporation Class A Preference Shares, Series 9

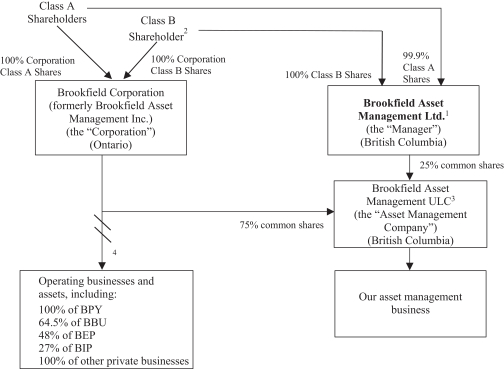

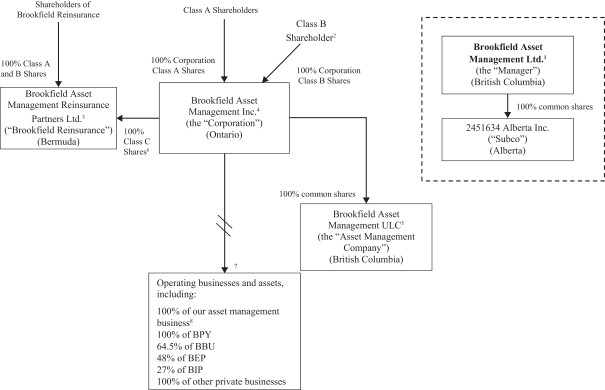

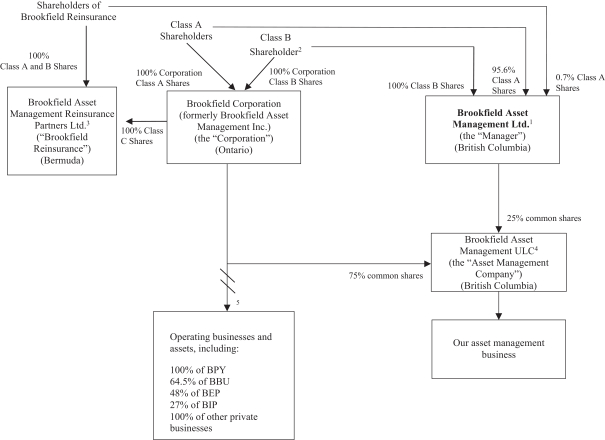

This letter of transmittal and election form (this “Letter of Transmittal”) (or a manually executed facsimile hereof), properly completed and duly executed in accordance with the instructions set out herein, together with all other required documents, is to be used by registered holders of class A limited voting shares (“Corporation Class A Shares”) of Brookfield Asset Management Inc. (“BAM”) in connection with an arrangement (the “Arrangement”) pursuant to section 182 of the Business Corporations Act (Ontario) being made pursuant to an arrangement agreement dated September 23, 2022 by and among BAM, Brookfield Asset Management Ltd. (the “Manager”), Brookfield Asset Management ULC and 2451634 Alberta Inc., whereby BAM will be separated through the separate listing and distribution of a 25% interest in its asset management business on a tax-free basis to both Canadian and U.S. shareholders, which Arrangement is being submitted for approval at the special meeting of holders of Corporation Class A Shares, class B limited voting shares, class A preference shares, Series 8 (“Corporation Class A Preference Shares, Series 8”) and class A preference shares, Series 9 (“Corporation Class A Preference Shares, Series 9”) of BAM (collectively, the “Shareholders”), to be held on November 9, 2022, or any adjournment(s) or postponement(s) thereof (the “Meeting”). Class A Shareholders are referred to the notice of special meeting of Shareholders and the circular dated September 23, 2022 (together, the “Circular”) accompanying this Letter of Transmittal.

This Letter of Transmittal or a manually executed facsimile hereof, properly completed and duly executed in accordance with the instructions set out herein, together with all other required documents, must be received by TSX Trust Company (the “Depositary”) at the office specified on the back page of this Letter of Transmittal no later than 5:00 p.m. (Toronto time) on the business day that is three (3) business days prior to the record date for the Arrangement (the “Election Deadline”).

Any Class A Shareholder whose completed Letter of Transmittal and all other required documents are not received by the Depositary prior to the Election Deadline will be treated as a Taxable Canadian Holder entitled to rollover treatment with respect to the Class A Shares under the Arrangement.

The terms described in the Circular are incorporated by reference into this Letter of Transmittal. The Circular contains important information, and Shareholders are urged to read the Circular in its entirety. Capitalized terms used but not defined in this Letter of Transmittal that are defined in the Circular have the respective meanings ascribed thereto in the Circular.

The issuance of the securities pursuant to the Arrangement will not be registered under the U.S. Securities Act and will be made in reliance on Section 3(a)(10) of the U.S. Securities Act, and in compliance with, or in reliance on an exemption from, the registration or qualification requirements of any state securities laws. Section 3(a)(10) of the U.S. Securities Act exempts from registration the offer and sale of a security which is issued in exchange for outstanding securities, claims or property interests, or partly in such exchange and partly for cash, where the terms and conditions of such issue and exchange are approved, after a hearing upon the fairness of such terms and conditions at which all persons to whom it is proposed to issue securities in such exchange have the right to appear, by a court or governmental authority expressly authorized by law to grant such approval. The Final Order, if granted, will constitute the basis for the Section 3(a)(10) exemption from the registration requirements of the U.S. Securities Act with respect to the securities issued in connection with the Arrangement. In connection with the hearing for the Interim Order, the Court will be advised that the securities will be issued in reliance on the Section 3(a)(10) exemption. The U.S. Securities Act will impose certain restrictions on resale on the Class A Shares to be received by a Shareholder who will be an “affiliate” of the Manager after the Arrangement. Please read the Circular for more information.

The Depositary (the address and telephone number of which are located on the back page of this Letter of Transmittal) or your broker or other financial advisor can assist you in completing this Letter of Transmittal.

You must sign this Letter of Transmittal in the appropriate space provided below. Delivery of this Letter of Transmittal to an address other than as set forth on the back page of this Letter of Transmittal will not constitute a valid delivery to the Depositary.

2

Please read carefully the Instructions set forth below before completing this Letter of Transmittal.

| TO: | Brookfield Asset Management Inc., Brookfield Asset Management Ltd., Brookfield Asset Management ULC and 2451634 Alberta Inc. |

| AND TO: | TSX Trust Company, as Depositary |

Upon the terms described in the Circular and this Letter of Transmittal, the undersigned hereby irrevocably deposits the Deposited Corporation Class A Shares (as defined below) in connection with the Arrangement and, effective immediately following the time when the Corporation Class A Shares are exchanged in connection with the Arrangement (the “Effective Time”), irrevocably sells, assigns and transfers to Brookfield Asset Management Inc. all of the right, title and interest of the undersigned in and to the Deposited Corporation Class A Shares. The term “Deposited Corporation Class A Shares” refers to the Corporation Class A Shares identified below as being deposited in connection with the Arrangement and all other rights and benefits arising from such Corporation Class A Shares.

| BOX 1 | ||||||

|

DESCRIPTION OF CORPORATION CLASS A SHARES DEPOSITED (Please print or type. If space is insufficient, please attach a list to this Letter of Transmittal in the form below.) | ||||||

|

Certificate Number(s) (if available) |

Name(s) in Which Certificate(s) and/or DRS Advice(s) is (are) Registered (please print and fill in exactly as name(s) appear(s) on certificate(s) and/or DRS advice(s)) |

Number of Corporation Class A Shares Represented by Certificate(s) and/or DRS Advice(s) |

Number of Corporation Class A Shares Deposited | |||

| TOTAL: | ||||||

3

| BOX 2

For Canadian purposes, all holders of Corporation Class A Shares will be entitled to rollover treatment with respect to the Class A Shares issued pursuant to the Arrangement, but Tax-Exempt Shareholders and Non-Resident Shareholders will not benefit from such treatment. Accordingly, by completing this Letter of Transmittal and indicating that you are (i) Tax-Exempt Shareholder or (ii) a Non-Resident Shareholder, you will, for Canadian purposes, acquire the Class A Shares for their fair market value and the Manager will acquire the holder’s butterfly class A common shares issued pursuant to the Arrangement at a cost equal to their fair market value.

Taxable Canadian Holders of Corporation Class A Shares are not required to complete this Letter of Transmittal and any holder of Corporation Class A Shares that does not do so will be treated as a Taxable Canadian Holder entitled to rollover treatment with respect to the Class A Shares under the Arrangement.

By execution of this Letter of Transmittal, the undersigned hereby represents and warrants that the undersigned is (please check appropriate box):

☐ Tax-Exempt Shareholder (Shareholder who is exempt from tax under Part I of the Tax Act) – OR – ☐ Non-Resident Shareholder (Shareholder who is non-resident of Canada for Canadian federal income tax purposes)

indicate country of residence:

Note: A Shareholder that is a partnership that has any non-resident partner(s) (either directly or indirectly through one or more other partnerships) should represent and warrant above that, for the purposes of the Tax Act, it is a “non-resident”.

|

| BOX 3 | BOX 4 | |||

| Issue DRS advice in the name of: (please print) | Send DRS advice to: (please print) | |||

|

(Name) |

(Name) | |||

|

(Street Address and Number) |

(Street Address and Number) | |||

|

(City and Province or State) |

(City and Province or State) | |||

|

(Country and Postal (Zip) Code) |

(Country and Postal (Zip) Code) | |||

|

(Telephone – Business Hours) |

(Telephone – Business Hours) | |||

|

(Social Insurance or Social Security Number) |

(Social Insurance or Social Security Number) |

4

GENERAL TERMS

By completing and signing this Letter of Transmittal:

| 1. | The undersigned understands that, upon the later of: (i) receipt by the Depositary of this Letter of Transmittal, the certificate(s) and/or DRS advice(s) representing the Deposited Corporation Class A Shares and all other required documentation and (ii) completion of the Arrangement, the Depositary will, as soon as practicable, cancel the certificates(s) and/or DRS advice(s) described above and send to the undersigned the consideration which it is entitled to receive in respect of the Deposited Corporation Class A Shares under the Arrangement. |

| 2. | The undersigned hereby represents and warrants in favor of BAM, as of the date hereof and as of the Effective Time, that: (i) it is the owner of the Deposited Corporation Class A Shares, (ii) it has good title to the Deposited Corporation Class A Shares free and clear of all mortgages, liens, charges, encumbrances, restrictions, security interests and adverse claims, (iii) it has full power and authority to execute and deliver this Letter of Transmittal, (iv) the Deposited Corporation Class A Shares have not been sold, assigned or transferred, nor has any agreement been entered into to sell, assign or transfer any of the Deposited Corporation Class A Shares to any other person, other than pursuant to the Arrangement, (v) the surrender of the Deposited Corporation Class A Shares complies with applicable Laws, and (vi) all information inserted by the undersigned into this Letter of Transmittal is accurate. These representations and warranties will survive the completion of the Arrangement. |

| 3. | The undersigned acknowledges that at the Effective Time, all its rights, title and interest in the Deposited Corporation Class A Shares will be directly or indirectly assigned and transferred to BAM in exchange for the consideration the undersigned is entitled to receive under the Arrangement. |

| 4. | The undersigned irrevocably appoints the Depositary as its agent to effect the exchange and delivery pursuant to the instructions hereto and the Arrangement. All authority conferred or agreed to be conferred in this Letter of Transmittal shall be binding upon the undersigned’s successors, assigns, heirs, executors, administrators and legal representatives and shall not be affected by, and shall survive, the undersigned’s death or incapacity. |

| 5. | The undersigned acknowledges that in the event that the Arrangement is not completed for any reason, the certificate(s) and/or DRS advice(s) that accompany this Letter of Transmittal will be returned, at BAM’s expense, to the undersigned as soon as practicable after the Election Deadline by sending certificates and/or DRS advices representing such Deposited Corporation Class A Shares by first class mail to the address of the depositing Shareholder specified in this Letter of Transmittal or, if such name or address is not so specified, in such name and to such address as shown on the share register maintained by BAM’s registrar and transfer agent. |

| 6. | The undersigned acknowledges and agrees that the method of delivery of the certificate(s) and/or DRS advice(s) representing the Deposited Corporation Class A Shares and all other required documents is at the election and risk of the undersigned. |

| 7. | The undersigned agrees that all questions as to validity, form, eligibility (including timely receipt) and acceptance of any Corporation Class A Shares deposited in connection with the Arrangement and the propriety of the completion and execution of this Letter of Transmittal will be determined by BAM in its sole discretion and that such determinations will be final and binding and acknowledges that: (i) BAM reserves the absolute right to reject any and all deposits of Corporation Class A Shares that BAM determines not to be in proper form or that may be unlawful to accept under the laws of any jurisdiction, (ii) BAM reserves the absolute right to waive any defects or irregularities in the deposit of any Corporation Class A Shares, (iii) there shall be no duty or obligation of BAM or the Depositary or any other person to give notice of any defect or irregularity in any deposit and no liability shall be incurred by any of them for failure to give such notice, (iv) BAM’s interpretation of the terms described in the Circular and this Letter of Transmittal shall be final and binding, and (v) BAM reserves the right to accept the deposit of Corporation |

5

| Class A Shares in connection with the Arrangement in any manner in addition to those set forth in the Circular. |

| 8. | By reason of the use by the undersigned of an English language form of Letter of Transmittal, the undersigned shall be deemed to have required that any contract evidenced by this Letter of Transmittal, as well as all documents related thereto, be drawn exclusively in the English language. En raison de l’usage d’une lettre d’envoi en langue anglaise par le soussigné, le soussigné est réputé avoir requis que tout contrat attesté par la présent lettre d’envoi, de même que tous les documents qui s’y rapportent, soient rédigés exclusivement en langue anglaise. |

6

SHAREHOLDER INFORMATION AND INSTRUCTIONS

Before signing this Letter of Transmittal, please review carefully and complete the following boxes, as appropriate.

| BLOCK A | ||||||

| SHAREHOLDER SIGNATURE AND SIGNATURE GUARANTEE | ||||||

| By signing below, the undersigned expressly agrees to the terms and conditions set forth above.

This Letter of Transmittal must be signed below by the registered Shareholder(s) exactly as their name(s) appear(s) on the certificates and/or DRS advices representing the Deposited Corporation Class A Shares, or on a security position listing or by person(s) authorized to become registrant holder(s) by certificates and/or DRS advices and documents transmitted herewith, or, pursuant to Instruction 3, by a fiduciary or authorized representative. | ||||||

| Signature guaranteed by (if required under Instruction 2(b)(iii)): Dated: |

| |||||

|

|

|

|||||||

| Authorized Signature of Guarantor | Signature of Shareholder or Authorized Representative (see Instructions 2, 3 and 4) |

|||||||

|

|

|

|||||||

| Name of Guarantor (please print or type) | Name of Shareholder or Authorized Representative (please print or type) |

|||||||

|

|

|

|||||||

| Address of Guarantor (please print or type) | Daytime telephone number and facsimile number of Shareholder or Authorized Representative |

|||||||

|

|

||||||||

| Tax Identification, Social Insurance or Social Security Number of Shareholder or Authorized Representative |

||||||||

7

INSTRUCTIONS

1. Use of Letter of Transmittal

| (a) | This Letter of Transmittal (or a manually signed facsimile hereof), properly completed and duly executed, with the signature(s) guaranteed if required by Instruction 2(b)(iii) below, together with accompanying certificate(s) and/or DRS advice(s) representing the Deposited Corporation Class A Shares and all other documents required by the terms of the Circular and this Letter of Transmittal must be physically received by the Depositary at its office specified on the back page of this Letter of Transmittal at or prior to 5:00 p.m. (Toronto time) on the business day that is three (3) business days prior to the record date for the Arrangement, the Election Deadline. Any Shareholder whose completed Letter of Transmittal and all other required documents are not received by the Depositary prior to the Election Deadline will be treated as a taxable Canadian holder entitled to rollover treatment with respect to the Class A Shares under the Arrangement. |

| (b) | The method used to deliver this Letter of Transmittal, any accompanying certificate(s) and/or DRS advice(s) representing Deposited Corporation Class A Shares, and all other required documents is at the option and risk of the Shareholder depositing these documents and delivery will be deemed effective only when such documents are actually received by the Depositary at its office specified on the back page hereof. BAM recommends that the necessary documentation be delivered by hand to the Depositary and that a receipt be obtained or, if mailed, that registered mail, with return receipt requested, be used and that proper insurance be obtained. It is suggested that any such mailing be made sufficiently in advance of the Election Deadline to permit delivery to the Depositary at or prior to the Election Deadline. Delivery will only be effective upon physical receipt by the Depositary at its office specified on the back page hereof. |

2. Signatures

This Letter of Transmittal must be completed and executed by the Shareholder depositing Corporation Class A Shares in connection with the Arrangement described above or by such Shareholder’s duly authorized representative (in accordance with Instruction 3).

| (a) | If this Letter of Transmittal is signed by the registered holder(s) of the accompanying certificate(s) and/or DRS advice(s) representing the Deposited Corporation Class A Shares, such signature(s) on this Letter of Transmittal must correspond exactly with the name(s) as registered or, if applicable, as written on the face of such certificate(s) and/or DRS advice(s) representing the Deposited Corporation Class A Shares, in either case, without any change whatsoever, and any such certificate(s) and/or DRS advice(s) need not be endorsed. If any Deposited Corporation Class A Shares are owned of record by two or more joint holders, all such holders must sign this Letter of Transmittal. |

| (b) | If this Letter of Transmittal is executed by a person other than the registered holder(s) of the Deposited Corporation Class A Shares, or if the certificate(s) and/or DRS advice(s) representing Corporation Class A Shares the deposit of which is not being accepted is (are) to be returned to a person other than such registered holder(s) or sent to an address other than the address of the registered holder(s) shown on the securities register maintained by or on behalf of BAM: |

| (i) | the accompanying certificate(s) and/or DRS advice(s) must be endorsed or be accompanied by an appropriate stock transfer power of attorney, in either case, duly and properly completed by the registered holder(s); |

| (ii) | the signature(s) on the endorsement panel or stock transfer power of attorney must correspond exactly to the name(s) of the registered holder(s) as registered or as appearing on the face of the certificate(s) and/or DRS advice(s); and |

| (iii) | such signature(s) must be guaranteed by an Eligible Institution, or in some other manner satisfactory to the Depositary (except that no guarantee is required if the signature is that of an Eligible Institution). |

8

An “Eligible Institution” means a Canadian Schedule I chartered bank, a member of the Securities Transfer Agents Medallion Program (STAMP), a member of the Stock Exchange Medallion Program (SEMP) or a member of the New York Stock Exchange Inc. Medallion Signature Program (MSP), acceptable to the Depositary. Members of these programs are usually members of a recognized stock exchange in Canada and/or the United States, members of the Investment Industry Regulatory Organization of Canada, members of the Financial Industry Regulatory Authority, Inc. or banks or trust companies in Canada or the United States.

3. Fiduciaries, Representatives and Authorizations

Where this Letter of Transmittal or any share certificate or stock transfer power of attorney is executed by a person acting as an executor, administrator, trustee, guardian, or on behalf of a corporation, partnership or association or is executed by any other person acting in a representative or fiduciary capacity, such person should so indicate when signing and this Letter of Transmittal must be accompanied by satisfactory evidence of such person’s authority to act. BAM or the Depositary, at their sole discretion, may require additional evidence of authority or additional documentation.

4. Miscellaneous

| (a) | If Deposited Corporation Class A Shares are registered in different forms (e.g. “John Doe” and “J. Doe”), a separate Letter of Transmittal should be signed for each different registration. |

| (b) | No alternative, conditional or contingent deposits will be accepted. All depositing Shareholders, by execution of this Letter of Transmittal (or manually signed facsimile hereof), waive any right to receive any notice of the acceptance of Deposited Corporation Class A Shares, except as required by applicable Laws. |

| (c) | The Arrangement and all contracts in connection thereof shall be governed by and construed in accordance with the laws of the Province of Ontario and the federal laws of Canada applicable therein. Each party to any agreement in connection with the Arrangement unconditionally and irrevocably attorns to the exclusive jurisdiction of the courts of the Province of Ontario and all courts competent to hear appeals therefrom. |

| (d) | BAM will not pay any fees or commissions to any stockbroker, dealer or other person for soliciting deposits of Corporation Class A Shares in connection with the Arrangement, other than to the Depositary, except as otherwise set out in the accompanying Circular. |

| (e) | Before completing this Letter of Transmittal, you are urged to read the accompanying Circular. |

| (f) | All questions as to the validity, form, eligibility (including, without limitation, timely receipt) and acceptance of any Corporation Class A Shares deposited in connection with the Arrangement will be determined by BAM in its sole discretion. Depositing Shareholders agree that such determination will be final and binding. BAM reserves the absolute right to reject any and all deposits that they determine not to be in proper form or that may be unlawful to accept under the laws of any jurisdiction. BAM reserves the absolute right to waive any defects or irregularities in the deposit of any Corporation Class A Shares. There shall be no duty or obligation of BAM, the Depositary or any other person to give notice of any defects or irregularities in any deposit and no liability shall be incurred or suffered by any of them for failure to give any such notice. BAM’s interpretation of the terms described in the Circular, this Letter of Transmittal and any other related documents will be final and binding. BAM reserves the right to accept the deposit of Corporation Class A Shares in connection with the Arrangement in a manner in addition to those set forth in the Circular. |

| (g) | Additional copies of the Circular and this Letter of Transmittal may be obtained without charge on request from the Depositary at its address specified on the back page of this Letter of Transmittal. |

9

5. Lost Certificates

If a certificate representing Corporation Class A Shares has been lost or destroyed, this Letter of Transmittal should be completed as fully as possible and forwarded, together with a letter describing the loss and providing your telephone number, to the Depositary at its office specified in this Letter of Transmittal. The Depositary will forward such letter to BAM’s registrar and transfer agent so that the registrar and transfer agent may provide replacement instructions. If a certificate representing Corporation Class A Shares has been lost, destroyed, mutilated or mislaid, the foregoing action must be taken sufficiently in advance of the Election Deadline in order to obtain a replacement certificate in sufficient time to permit the Corporation Class A Shares represented by the replacement certificate to be deposited in connection with the Arrangement prior to the Election Deadline.

6. Privacy Notice

The Depositary is committed to protecting your personal information. In the course of providing services to you and its corporate clients, the Depositary receives non-public personal information about you from transactions performed by the Depositary for you, forms you send to the Depositary, other communications the Depositary has with you or your representatives, etc. This information could include your name, address, social insurance number or Social Security Number, securities holdings and other financial information. The Depositary uses this information to administer your account, to better serve your and its clients’ needs and for other lawful purposes relating to its services. Some of your information may be transferred to servicers in the U.S. for data processing and/or storage. The Depositary will use the information you are providing in order to process your request and will treat your signature(s) as your consent to us so doing.

7. Assistance

Questions or requests for assistance concerning the Arrangement, completing this Letter of Transmittal and depositing the Corporation Class A Shares with the Depositary may be directed to the Depositary. The Depositary’s contact details are provided on the back page of this Letter of Transmittal. Shareholders may also contact their brokers, dealers, commercial banks, trust companies or other nominees for assistance concerning the Arrangement.

10

The Depositary for the Arrangement is:

TSX Trust Company

By Mail (Except Registered Mail)

P. O. Box 1036

Adelaide Street Postal Station

Toronto, Ontario

M5C 2K4

Attention: Corporate Actions

By Hand, Courier or Registered Mail

1 Toronto Street

Suite 1200

Toronto, Ontario

M5C 2V6

Attention: Corporate Actions

Telephone: (416) 682-3860

Toll Free: 1-800-387-0825

E-mail: shareholderinquiries@tmx.com

Any questions or requests for assistance or additional copies of this Letter of Transmittal and related Arrangement documents may be directed by Shareholders to the Depositary at its telephone number.