Exhibit 99.1

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL RESULTS

Our Management’s Discussion and Analysis (“MD&A”) is provided to enable a reader to assess our results of operations and financial condition for the fiscal year ended December 31, 2014. This MD&A should be read in conjunction with our 2014 annual consolidated financial statements and related notes and is dated March 26, 2015. Unless the context indicates otherwise, references in this MD&A to “the Corporation” refer to Brookfield Asset Management Inc., and references to “Brookfield,” “us,” “we,” “our” or “the company” refer to the Corporation and its direct and indirect subsidiaries and consolidated entities. The company’s financial statements are in U.S. dollars, and are based on financial statements prepared in accordance with International Financial Reporting Standards (“IFRS”), as issued by the International Accounting Standards Board.

Additional information about the company, including our 2014 Annual Information Form, is available on our website at www.brookfield.com, on the Canadian Securities Administrators’ website at www.sedar.com and on the EDGAR section of the U.S. Securities and Exchange Commission’s (“SEC”) website at www.sec.gov. We are a “foreign private issuer” as such term is defined in Rule 405 under the U.S. Securities Act of 1933, as amended, and Rule 3b-4 under the U.S. Securities Exchange Act of 1934, as amended. As a result, among other things, we prepare our financial statements in accordance with applicable Canadian laws and do not apply U.S. GAAP to our financial statements or reconcile our financial statements to U.S. GAAP. In addition, we are an eligible issuer under the Multijurisdictional Disclosure System (“MJDS”). Pursuant to MJDS, we comply with U.S. continuous reporting requirements by filing our Canadian disclosure documents with the SEC.

Organization of the MD&A

Part 1 provides an overview of our business, including a discussion of our strategy, and the economic environment and outlook at the time of writing. This section also contains information on the basis of presentation of financial information and key financial measures contained in the MD&A.

Part 2 discusses our annual and fourth quarter financial results utilizing key financial measures contained in our Consolidated Statements of Operations, Consolidated Statements of Comprehensive Income and Consolidated Balance Sheets.

Part 3 discusses the results of our various operating segments based on segmented financial measures, including Funds from Operations and Common Equity by Segment, certain of which are non-IFRS measures.

Part 4 reviews our capitalization and liquidity profile.

Part 5 discusses our operating capabilities and a number of key risks associated with our business and our issued securities. Further information on risks is contained in our Annual Information Form.

Part 6 contains additional information on our accounting policies, internal control environment and related party transactions.

STATEMENT REGARDING FORWARD-LOOKING STATEMENTS AND USE OF NON-IFRS MEASURES

This MD&A to Shareholders contains forward-looking information within the meaning of Canadian provincial securities laws and applicable regulations and “forward-looking statements” within the meaning of the “safe harbor” provisions of the United States Private Securities Litigation Reform Act of 1995. We may make such statements in the Report, in other filings with Canadian regulators or the U.S. Securities and Exchange Commission or in other communications. See “Cautionary Statement Regarding Forward-Looking Statements and Information” on page 150.

We disclose a number of financial measures in this MD&A that are calculated and presented using methodologies other than IFRS. We utilize these measures in managing the business, including performance measurement, capital allocation and for valuation and believe that providing these performance measures on a supplemental basis to our IFRS results is helpful to investors in assessing the overall performance of our businesses. These financial measures should not be considered as a substitute for similar financial measures calculated in accordance with IFRS. We caution readers that these non-IFRS financial measures may differ from the calculations disclosed by other businesses, and as a result, may not be comparable to similar measures presented by others. Reconciliations of these non-IFRS financial measures to the most directly comparable financial measures calculated and presented in accordance with IFRS, where applicable, are included within the MD&A.

Information contained in or otherwise accessible through the websites mentioned does not form part of this Report. All references in this Report to websites are inactive textual references and are not incorporated by reference.

10 BROOKFIELD ASSET MANAGEMENT

PART 1 – OVERVIEW AND OUTLOOK

OUR BUSINESS

Brookfield is a global alternative asset manager with over $200 billion in assets under management. For more than 100 years we have owned and operated assets on behalf of shareholders and clients with a focus on property, renewable energy, infrastructure and private equity.

We manage a wide range of investment funds and other entities that enable institutional and retail clients to invest in these assets. We earn asset management income including fees, carried interests and other forms of performance income for doing so. As at December 31, 2014, our managed funds and listed partnerships represented $89 billion of invested and committed fee bearing capital. These products include publicly listed partnerships that are listed on major stock exchanges as well as private institutional partnerships that are available to accredited investors, typically pension funds, endowments and other institutional investors. We also manage portfolios of listed securities through a series of segregated accounts and mutual funds.

We align our interests with clients’ by investing alongside them and have $27 billion of capital invested in our listed partnerships and private funds, based on IFRS carrying values.

Our business model is simple: (i) raise pools of capital from ourselves and clients that target attractive investment strategies, (ii) utilize our global reach to identify and acquire high-quality assets at favourable valuations, (iii) finance them on a long-term basis, (iv) enhance the cash flows and values of these assets through our operating platforms to earn reliable, attractive long-term total returns, and (v) realize capital from asset sales or refinancings when opportunities arise.

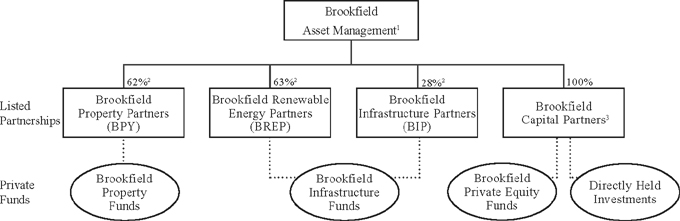

Organization Structure

Our operations are organized into five principal groups (“operating platforms”). Our property, renewable energy, infrastructure and private equity platforms are responsible for operating the assets owned by our various funds and investee companies. The equity capital invested in these assets is provided by a series of listed partnerships and private funds which are managed by us and are funded with capital from ourselves and our clients. A fifth group operates our public markets business, which manages portfolios of listed securities on behalf of clients.

We have formed a large capitalization listed partnership entity in each of our property, renewable energy and infrastructure groups, which serves as the primary vehicle through which we invest in each respective segment. As well as owning assets directly, these partnerships serve as the cornerstone investors in our private funds, alongside capital committed by institutional investors. This approach enables us to attract a broad range of public and private investment capital and the ability to match our various investment strategies with the most appropriate form of capital. Our private equity business is conducted primarily through private funds with capital provided by institutions and ourselves.

Our balance sheet capital is invested primarily in our three flagship listed partnerships, Brookfield Property Partners L.P. (“BPY” or “Brookfield Property Partners”); Brookfield Renewable Energy Partners L.P. (“BREP” or “Brookfield Renewable Energy Partners”); and Brookfield Infrastructure Partners L.P. (“BIP” or “Brookfield Infrastructure Partners”), our private equity funds, and in several directly held investments and businesses.

The following chart is a condensed version of our organizational structure:

| 1. | Includes asset management and corporate activities |

| 2. | Economic ownership interest, see page 34 for further details |

| 3. | Privately held, includes private equity, residential development and service activities |

2014 ANNUAL REPORT 11

STRATEGY AND VALUE CREATION

Our business is centred around the ownership and operation of real assets, which we define as long-life, physical assets that form the critical backbone of economic activity, including property, renewable energy and infrastructure facilities. Whether they provide high-quality office or retail space in major urban markets, generate reliable clean electricity, or transport goods and resources between key locations, these assets play an essential role within the global economy. Additionally, these assets typically benefit from some form of barrier to entry, regulatory regime or other competitive advantage that provide for relatively stable cash flow streams, strong operating margins and value appreciation over the longer term.

We currently own and manage one of the world’s largest portfolios of real assets. We have established a variety of investment products through which our clients can invest in these assets, including both listed entities and private funds. We actively invest our own capital alongside our clients, ensuring a meaningful alignment of interests.

We are active managers of capital. We strive to add value by judiciously and opportunistically reallocating capital to continuously increase returns. Our operating platforms include approximately 30,000 employees worldwide who are instrumental in maximizing the value and cash flows from our assets. As real asset operations tend to be industry specific and often driven by complex regulations, we believe operational experience is necessary in order to maximize efficiency, productivity and returns. Our track record shows that we can add meaningful value and cash flow through “hands-on” operational expertise, whether through the negotiation of property leases, energy contracts or regulatory agreements, or through a focus on optimizing asset development, operations or other activities.

We strive to finance our operations on a long-term, investment-grade basis, and most of our capital consists of equity and stand-alone asset-by-asset financing with minimal recourse to other parts of the organization. We also strive to maintain excess liquidity at all times in order to respond to opportunities as they arise. This provides us with considerable stability and enables our management teams to focus on operations and other growth initiatives. It also improves our ability to withstand financial downturns and provides the strength and flexibility to capitalize upon attractive opportunities.

We prefer to invest when capital is less available to a specific market or industry and in situations that tend to require a broader range of expertise and be more challenging to execute. We believe these situations provide much more attractive valuations than competitive auctions and we have considerable experience in this specialized field.

We maintain development and capital expansion capabilities and a large pipeline of attractive opportunities. This provides flexibility in deploying capital, as we can invest in both acquisitions and organic developments, depending on the relative attractiveness of returns.

As an asset manager, we create value for shareholders in the following ways:

| • | We offer attractive investment opportunities to our clients through our managed funds and entities that will, in turn, enable us to earn base management fees based on the amount of capital that we manage, and additional returns such as incentive distributions and carried interests based on our performance. Accordingly, we create value by increasing the amount of capital under management and by achieving strong investment performance that leads to increased cash flows and asset values. |

| • | We invest significant amounts of our own capital, alongside our clients in the same assets. This differentiates us from many of our competitors, creates a strong alignment of interest with our clients and enables us to create value by directly participating in the cash flows and value increases generated by these assets, in addition to the performance returns that we earn as the manager. |

| • | Our operating capabilities enable us to increase the value of the assets within our businesses, and the cash flows they produce. Through our operating expertise, development capabilities and effective financing, we believe our specialized real asset experience can help to ensure that an investment’s full value creation potential is realized. We believe this is one of our most important competitive advantages as an asset manager. |

| • | We aim to finance assets effectively, using a prudent amount of leverage. We believe the majority of our assets are well suited to support an appropriate level of investment-grade secured debt with long-dated maturities given the predictability of the cash flows and tendency of these assets to retain substantial value throughout economic cycles. This is reflected in our return on net capital deployed, our overall return on capital and our cost of capital. While we tend to hold our assets for extended periods of time, we endeavour to own our businesses in a manner that maximizes our ability to realize the value and liquidity of our assets on short notice and without disrupting our operations. |

| • | Finally, as an investor and capital allocator with a value investing culture and expertise in recapitalizations and operational turnarounds, we strive to invest at attractive valuations, particularly in situations that create opportunities for superior valuation gains and cash flow returns. |

12 BROOKFIELD ASSET MANAGEMENT

ECONOMIC AND MARKET REVIEW AND OUTLOOK

(As at January 31, 2015)

The predictions and forecasts within our Economic and Market Review and Outlook are based on information and assumptions from sources we consider reliable. If this information or these assumptions are not accurate, actual economic outcomes may differ materially from the outlook presented in this section. For details on risk factors from general business and economic conditions that may affect our business and financial results, refer to Part 5 – Operating Capabilities, Environment and Risks.

Overview and Outlook

Despite a weak start to the year, the recovery in the U.S. now seems firmly entrenched and could deliver 3.0% growth over the next couple of years as lower oil prices drive consumer activity and residential construction picks up to match household formation and other positive trends. In contrast, lower oil prices will be negative for real GDP growth in Canada, which will see growth slow to 2.0% and economic activity rotate from Western commodity-oriented provinces to Eastern manufacturing-oriented ones. The recovery in the United Kingdom continues and it should achieve growth of about 2.5% in 2015. The Eurozone struggles to generate growth and will likely only expand by about 1.0% in 2015. Inflation remains extremely weak and is trending lower, and while a more aggressive European Central Bank should offset the risks of a deflationary spiral, lower oil prices will keep inflation measures subdued for most of 2015. Brazil is also struggling to grow as a number of near-term challenges are weighing on economic activity. Forecasters are rightly pessimistic that Brazil will see weak real GDP growth in 2015 below 1% but they have become overly pessimistic about Brazil’s long-term prospects. Real GDP growth in China slowed to 7.4% in 2014 and will slow further in 2015 as the economy transitions away from an investment-led, export-driven economic model to a more balanced model where domestic demand and consumption play an increasingly important role. Australia is being caught up in this transition and it too will have to adjust to a slowdown in mining investment that had been supporting China’s rapidly increasing demand for commodities. Lower oil prices and a weaker Australian dollar will ease the adjustment somewhat, but growth will still likely slow to 2.5% this year.

United States

While the contraction in U.S. real GDP at the start of 2014 caused some to question the robustness of the U.S. recovery, a strong back half of the year suggests the U.S. is now growing at about 3.0%, a solid rate for the world’s largest economy. This is in spite of the fact that U.S. housing starts remain stuck around 1 million units, about 500,000 units below levels consistent with long-term support for population growth and household formation. In addition, the sharp decline in oil prices at the end of the year will be a net positive for U.S. growth, even if lower oil prices takes some momentum out of investment in the U.S. energy sector. These factors reinforce our view that the U.S. is on track to achieve 3.0% or higher growth in 2015. The strength of the U.S. economy has correlated to a much stronger U.S. dollar, which has appreciated more than 10-15% on a trade-weighted basis since mid-2014. Most of the appreciation is supported by interest rate spreads favouring the U.S. dollar at the front end of relative rates curves, with many global central banks cutting rates in response to weaker commodity prices and sluggish domestic growth. The global divergence in monetary policy will continue into 2015 and should be supportive of further gains in the U.S. dollar. Given the structure of the U.S. current account, we do not see this as a major risk to the U.S. recovery.

Canada

Canada recorded 2.4% real GDP growth in 2014 but this will likely slow to about 2.0% in 2015 as the sharp fall in oil prices and the nearly 20% decline of the Canadian dollar will see the drivers of GDP growth in Canada shift from western commodity-oriented provinces to eastern manufacturing-oriented provinces. This adjustment will take some time, as investment in the oil and gas sector – representing about 30% of total business investment – is reduced. The negative impact of these cuts will initially only be partly offset by an improvement in non-energy export sector, which will benefit from stronger U.S. growth and a weaker Canadian dollar. Encouragingly, non-energy exports were already picking up in the second half of 2014 but a fuller transition is a multi-year process. As would be expected, the weaker growth outlook in Canada is driving a further wedge between expectations for Canadian and U.S. interest rates, particularly following the surprise rate cut by the Bank of Canada in January, and this will continue to put downward pressures on the Canadian dollar in 2015.

United Kingdom

Real GDP in the UK grew by 2.7% in 2014, its fastest pace of growth since 2007 and capping a year that saw growth and employment surprise on the upside. Despite stronger economic activity, wage growth and inflationary pressures remain muted. Both headline and core inflation are below the Bank of England’s 2% target and the fall in oil prices will see headline inflation fall well below 1% in 2015. Longer term, lower oil prices will be positive for growth in the UK due to the benefit for consumers, but renewed volatility in the Eurozone and a general election in May could mean that the Bank of England maintains its short-term interest rate at 0.5% for the rest of 2015, as markets are currently pricing. While we expect real GDP growth in the UK to be a steady 2.5% in 2015, we are conscious of the risks created by large fiscal and current account deficits. The United Kingdom’s fiscal deficit-to-GDP stood at 5.2% in 2014 and the current account balance was approximately 5.1% of GDP. At the moment, it is difficult to foresee a scenario where London financial markets and UK assets lose their attractiveness as a haven for global capital flows. However, lower reserve accumulation in energy exporting nations (mainly Middle East and Russia) as

2014 ANNUAL REPORT 13

well as potential headline political risks surrounding the May election raise our level of concern about the durability of external financing of the twin deficits at current exchange rates.

Eurozone

The Eurozone continued to see sluggish growth of only 0.8% in 2014 and the sharp decline in oil prices pushed inflation to -0.6% on a year-over-year basis at the start of 2015. As was widely expected, the European Central Bank officially launched its quantitative easing program – committing to monthly purchases of €60 billion of government bonds and asset-backed securities until September 2016. The timing of the European Central Bank’s program comes at a time when the Eurozone continues to struggle to generate growth. While low interest rates, a weakening of the Euro and lower oil prices will help boost Eurozone growth, member states still need to address high debt levels and more has to be done to address the fundamental structural constraints of the currency union. Greece’s debt-to-GDP ratio is still 175% and Portugal and Italy have debt-to-GDP ratios above 130%. The current confrontation between Greece and its creditors is the latest, and probably most extreme, manifestation of this underlying problem but we believe the economic and political fallout from these high debts will continue to be a prominent theme in the Eurozone for many years to come. We are patiently watching private sector credit measures for signs that monetary policy measures are inducing credit expansion within the Eurozone. While the deleveraging continues, its pace has slowed and points to an expansion in early to mid-2015. This will be a necessary condition for Eurozone inflation and growth to resume.

Brazil

Brazil’s real GDP slowed to just 0.2% in 2014 as manufacturing and investment contracted, causing forecasters to become even more pessimistic about Brazil’s outlook. Measures of confidence in the Brazilian economy have fallen below levels seen during the global financial crisis. Many near-term challenges remain, including the extremely dry conditions which have sent spot electricity prices to historic highs given the hydro-dominated nature of Brazil’s electricity supply. High power prices have caused certain electricity-intensive industrials to shut down production and sell power back to the grid. Another factor behind the pessimism is the uncertain impact that the decline in commodity prices will have on Brazil’s economy, whose exports have increasingly become dominated by commodities. The price of iron ore, Brazil’s largest commodity export, has fallen over 60% over the past three years and soybean prices are down 25%. Despite stagnant GDP growth, inflationary pressures have remained high, regularly exceeding the upper limit of the Brazilian Central Bank’s inflation target and reflecting a structural deficit in investment. This has not only prevented the central bank from being more accommodative, but actually forced it to raise its interest rate (SELIC) by 175 bps in 2014 and by a further 50 bps in early 2015, which has slowed domestic credit growth and weighed on consumption. Public finances have also deteriorated in 2014, with Brazil recording its first primary deficit since 2001. Longer term, we are still confident that growth will return to Brazil’s 3-4% potential. It will take time to work through current challenges but the weakening of exchange rates should increase the competitiveness of domestic industries and improve Brazil’s trade balance. The currency has already fallen approximately 40% since 2011 and we are beginning to see a positive contribution to GDP from net exports.

China

China’s real GDP growth slowed to 7.4% in 2014 and is expected to slow further in 2015, with many suggesting growth could come in below 7.0% in 2015 and continue to slow as the economy rebalances away from a model that has become overly dependent on investment. While slowing investment by China in heavy industrials, infrastructure and real estate will contribute to lower GDP growth numbers over coming years, we believe this to be a necessary adjustment that will ultimately put the Chinese market on a more sustainable path even if the transition is not entirely smooth. Still, we believe the Chinese market presents significant opportunities over the long term. China’s GDP of $10.4 trillion in 2014 is second only to the United States’ GDP of $17.4 trillion and while still far below average wealth and income levels seen in more developed economies, China’s GDP per capita has risen from just US$950 in 2000 to almost US$7,500 in 2014, with some provinces such as Shanghai more than double that.

Australia

Australian GDP growth ended the year on a weaker note, at 1.9% in the fourth quarter as the decline in commodity prices started to affect consumer sentiment and government and business planning. Concerns over the economy and job security mean that consumer sentiment is already low and may be dragged down further by the need for tougher measures aimed at plugging the budget gap. The government recently revealed a significant widening of the budget deficit gap, brought about predominantly by a drop in iron ore related royalties and taxes. The Australian dollar has weakened to US$0.78 against the U.S. dollar and we believe it will weaken further. The benign inflation outlook and cooling house prices has allowed the Reserve Bank of Australia to provide additional support to the economy with a lower interest rate and the depreciation of the Australian dollar is already providing significant stimulus. The weaker Australian dollar and lower oil prices will ease the transition of the Australian economy away from mining and heavy construction, toward home building, retail, tourism, education and manufacturing.

14 BROOKFIELD ASSET MANAGEMENT

BASIS OF PRESENTATION AND USE OF NON-IFRS MEASURES

Basis of Accounting

We are a Canadian corporation and, as such, we prepare our consolidated financial statements in accordance with International Financial Reporting Standards (“IFRS”), as issued by the International Accounting Standards Board. We are listed on the Toronto Stock Exchange, New York Stock Exchange and Euronext and recognize that IFRS may not be the generally used accounting methodology for all readers of this report. The following discussion contains a summary of two key features of IFRS that we believe are particularly relevant to users of our financial statements. Our significant accounting policies are described in Note 2 to our consolidated financial statements, which also contains a summary of critical judgments and estimates.

Election of Fair Value Accounting

We account for a number of our consolidated assets at fair value including our commercial properties, renewable energy assets, and certain of our infrastructure and financial assets. Property, plant and equipment and inventory included within our private equity and residential development operations are typically recorded at amortized historic cost or the lower of cost and net realizable value. Public service concessions within our infrastructure operations are considered intangible assets and are amortized over the life of the concession. Other intangible assets and goodwill are recorded at amortized cost or cost. Equity accounted investments follow the same accounting principles as our consolidated operations and accordingly, include amounts recorded at fair value and amounts recorded at amortized cost or cost, depending on the nature of the underlying assets.

We classify the vast majority of our property assets within our office, retail, industrial and multifamily portfolios as investment properties. We have elected to record our investment properties at fair value, and accordingly our investment properties are revalued on a quarterly basis and changes in value are recorded as fair value changes within net income. Standing timber and agricultural assets are classified as sustainable resources and accounted for in a similar manner as investment properties. Depreciation is not recorded on investment properties or sustainable resources that are fair valued.

Our renewable energy facilities, certain of our infrastructure assets and our hotel assets within our property portfolio are classified as property, plant and equipment and we have elected to record these assets at fair value using the revaluation method. Unlike investment properties, these assets are revalued on an annual basis and changes in value are recorded as revaluation surplus within other comprehensive income and accumulated within common equity. Depreciation is determined on the revalued carrying values at the beginning of each year and recorded in net income. If a revaluation results in the fair value declining below the depreciated cost of the asset, then an impairment is charged to net income. Impairments of this nature may be subsequently reversed through increases in value.

A significant portion of our infrastructure operation’s assets are classified as intangible assets and reflect the fair value of the regulatory rate base or other characteristics at acquisition. Intangible assets are carried at amortized cost, subject to impairment tests, and are amortized over their useful lives unless they are determined to have an indefinite life, in which case amortization is not recorded.

Financial assets, financial contracts and other contractual arrangements that are treated as derivatives are recorded at fair value in our financial statements and changes in their value are recorded in net income or other comprehensive income, depending on their nature and business purpose (i.e., whether a security is held for trading, classified as available-for-sale, or whether a financial contract qualifies for hedge accounting or not). The more significant and more common financial contracts and contractual arrangements employed in our business that are fair valued include: interest rate contracts, foreign exchange contracts, and agreements for the sale of electricity.

Consolidated Financial Information

We consolidate a number of entities even though we hold only a minority economic interest. This is the result of our exercising control, as determined under IFRS, over the affairs of these entities due to contractual arrangements and our significant economic interest in these entities. As a result, we include 100% of the revenues and expenses of consolidated entities in our consolidated statement of operations, even though a substantial portion of the net income of the entity is attributable to non-controlling interests. On the other hand, revenues and expenses between consolidated entities, such as asset management fees, are eliminated in our consolidated statement of operations; however these items impact the allocation of net income between shareholders and non-controlling interests.

Interests in entities over which we exercise significant influence, but where we do not exercise control, are accounted for as equity accounted investments. We record our proportionate share of their net income on a “one-line” basis as equity accounted income within net income and “two-lines” within other comprehensive income as equity accounted income that will be reclassified to net income and equity accounted income that will not be reclassified to net income. As a result, our share of items such as fair value changes, that would be included within fair value changes if the entity was consolidated, are instead included within equity accounted income.

2014 ANNUAL REPORT 15

Certain of our consolidated subsidiaries and equity accounted investments do not utilize IFRS for their own statutory reporting purposes. The comprehensive income utilized by us for these entities is determined using IFRS and may differ significantly from the comprehensive income pursuant to the accounting principles reported by the investee. For example, IFRS provides a reporting issuer a policy election to fair value its investment properties, as described above, whereas other accounting principles such as U.S. GAAP may not. Accordingly, their statutory financial statements, which may be publicly available, may differ from those which we consolidate.

Foreign Currency Translation

Changes in the rate of exchange between the U.S. dollar and the currencies in which we conduct our non-U.S. operations will typically impact our operating results and our financial position. As a general rule, changes in the average annual rate of exchange will impact the value at which the results of non-U.S. operations are included in consolidated net income, whereas changes in the spot rates will impact the values at which non-U.S. assets and liabilities are included in our consolidated balance sheet. Please refer to Note 2(e) of our consolidated financial statements (Significant Accounting Policies – Foreign Currency Translation).

The most significant exchange rates that impact our business are shown in the following table:

| Year-end Spot Rate | Change | Average Annual Rate | Change | |||||||||||||||||||||||||||||||||||||

| 2014 | 2013 | 2012 | 2014 vs 2013 |

2013 vs 2012 |

2014 | 2013 | 2012 | 2014 vs 2013 |

2013 vs 2012 |

|||||||||||||||||||||||||||||||

| Australian dollar |

0.8172 | 0.8918 | 1.0395 | (8)% | (14)% | 0.9023 | 0.9682 | 1.0357 | (7)% | (7)% | ||||||||||||||||||||||||||||||

| Brazilian real |

2.6504 | 2.3635 | 2.0435 | (12)% | (16)% | 2.3469 | 2.1505 | 1.9546 | (9)% | (10)% | ||||||||||||||||||||||||||||||

| British pound |

1.5577 | 1.6556 | 1.6248 | (6)% | 2% | 1.6478 | 1.5647 | 1.5852 | 5% | (1)% | ||||||||||||||||||||||||||||||

| Canadian dollar |

0.8608 | 0.9414 | 1.0079 | (9)% | (7)% | 0.9057 | 0.9713 | 1.0004 | (7)% | (3)% | ||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

The average foreign currency exchange rate relative to the U.S dollar during 2014 was lower than in 2013 and lower than 2012, in several of our major regions, mostly Australia, Brazil and Canada. As a result of these rate variations, the U.S. dollar equivalent of the contributions from our subsidiaries and investments in these regions were lower in 2014 than 2013 and 2012, all other things being equal.

We provide further details on our foreign currency profile within Part 2 of this MD&A on page 25.

Use of Non-IFRS Measures

We disclose a number of financial measures in this Report that are calculated and presented using methodologies other than in accordance with IFRS. These measures are used primarily in Part 3 of the MD&A. We utilize these non-IFRS measures in managing the business, including performance measurement, capital allocation and valuation and believe that providing these performance measures on a supplemental basis to our IFRS results is helpful to investors in assessing the overall performance of our businesses. These financial measures should not be considered as a substitute for similar financial measures calculated in accordance with IFRS. We caution readers that these non-IFRS financial measures may differ from the calculations disclosed by other businesses, and as a result, may not be comparable to similar measures presented by others. Reconciliations of these non-IFRS financial measures to the most directly comparable financial measures calculated and presented in accordance with IFRS, where applicable, are included within Part 3 of this MD&A and elsewhere as appropriate.

16 BROOKFIELD ASSET MANAGEMENT

PART 2 – FINANCIAL PERFORMANCE REVIEW

SELECTED ANNUAL FINANCIAL INFORMATION

| Change | ||||||||||||||||||||

| FOR THE YEARS ENDED DECEMBER 31 (MILLIONS, EXCEPT PER SHARE AMOUNTS) |

2014 | 2013 | 2012 | 2014 vs 2013 | 2013 vs 2012 | |||||||||||||||

| CONDENSED STATEMENT |

||||||||||||||||||||

| Revenues |

$ | 18,364 | $ | 20,093 | $ | 18,696 | $ | (1,729) | $ | 1,397 | ||||||||||

| Direct costs |

(13,118) | (13,928) | (13,961) | 810 | 33 | |||||||||||||||

| Other income and gains |

190 | 1,262 | 70 | (1,072) | 1,192 | |||||||||||||||

| Equity accounted income |

1,594 | 759 | 1,237 | 835 | (478) | |||||||||||||||

| Expenses |

||||||||||||||||||||

| Interest |

(2,579) | (2,553) | (2,500) | (26) | (53) | |||||||||||||||

| Corporate costs |

(123) | (152) | (158) | 29 | 6 | |||||||||||||||

| Fair value changes |

3,674 | 663 | 1,153 | 3,011 | (490) | |||||||||||||||

| Depreciation and amortization |

(1,470) | (1,455) | (1,263) | (15) | (192) | |||||||||||||||

| Income taxes |

(1,323) | (845) | (519) | (478) | (326) | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income |

5,209 | 3,844 | 2,755 | 1,365 | 1,089 | |||||||||||||||

| Non-controlling interests |

(2,099) | (1,724) | (1,375) | (375) | (349) | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income attributable to shareholders |

$ | 3,110 | $ | 2,120 | $ | 1,380 | $ | 990 | $ | 740 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income per share |

$ | 4.67 | $ | 3.12 | $ | 1.97 | ||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||

| CONDENSED STATEMENT OF OTHER |

||||||||||||||||||||

| Revaluation of property, plant and equipment |

$ | 2,998 | $ | 825 | $ | 1,491 | $ | 2,173 | $ | (666) | ||||||||||

| Financial contracts and power sales agreements |

(301) | 442 | (17) | (743) | 459 | |||||||||||||||

| Foreign currency translation |

(1,717) | (2,429) | (110) | 712 | (2,319) | |||||||||||||||

| Equity accounted investments and other |

41 | 241 | 144 | (200) | 97 | |||||||||||||||

| Taxes on above items |

(610) | (280) | (432) | (330) | 152 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Other comprehensive income |

411 | (1,201) | 1,076 | 1,612 | (2,277) | |||||||||||||||

| Non-controlling interests |

(110) | 406 | (563) | (516) | 969 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Other comprehensive income |

301 | (795) | 513 | 1,096 | (1,308) | |||||||||||||||

| Comprehensive income attributable |

$ | 3,411 | $ | 1,325 | $ | 1,893 | $ | 2,086 | $ | (568) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| SELECT BALANCE SHEET INFORMATION

AS AT DECEMBER 31 (MILLIONS) |

||||||||||||||||||||

| Consolidated assets |

$ | 129,480 | $ | 112,745 | $ | 108,862 | $ | 16,735 | $ | 3,883 | ||||||||||

| Borrowings and other non-current |

60,663 | 53,061 | 51,887 | 7,602 | 1,174 | |||||||||||||||

| Equity |

53,247 | 47,526 | 44,338 | 5,721 | 3,188 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

Dividends declared for each class of issued securities for the three most recently completed years are presented on page 32.

2014 ANNUAL REPORT 17

ANNUAL FINANCIAL PERFORMANCE

The following section contains a discussion and analysis of line items presented within our consolidated financial statements. We have disaggregated several of the line items into the amounts that are attributable to our eight operating segments in order to facilitate the review of variances. The financial data in this section has been prepared in accordance with IFRS for each of the three most recently completed financial years.

Overview

2014 vs. 2013

Consolidated net income was $5.2 billion for the year ended December 31, 2014, representing a $1.4 billion increase from the $3.8 billion recorded in 2013. The largest variance was the significant increase in fair value gains recognized on investment properties held within consolidated subsidiaries and equity accounted investments as valuations for many of our office and retail properties benefitted from lower discount rates and increasing cash flows, reflecting strengthening leasing environments. We recorded a lower amount of other income and gains, which in 2013 included $1,189 million of gains on the sale of an investment and the settlement of a long dated interest rate swap. Revenues less direct costs decreased by $919 million in aggregate, as 2013 included $558 million of additional realized carried interests on the wind up of a private fund consortium and we sold two private equity investments and non-core timberlands, which contributed revenues less direct costs of $348 million in the prior year. Interest expense was relatively unchanged, notwithstanding additional debt associated with acquisitions because the interest expense on new debt was offset by the impact of lower rates on debt refinancings. Income taxes increased by $478 million due to a $320 million non-recurring deferred tax expense related to a change in tax laws in one of our core property operations, as well as deferred taxes associated within a higher level of investment property fair value gains.

Net income on a per share basis increased by $1.55 to $4.67 in the current year. Net income attributable to shareholders increased by a greater proportion than on a consolidated basis primarily due to our increased ownership interest in our office property portfolio in 2014, which meant that shareholders participated to a greater extent in the significant fair value gains recognized during the year.

2013 vs. 2012

The $1.1 billion increase in net income in 2013 compared to 2012 was primarily due to an increase in revenue less direct costs of $1,430 million and two large gains totaling $1,189 million recorded within other income and gains. Revenue increased due to the realization of $565 million of carried interests, higher generation levels within our renewable energy operations and the contribution from assets acquired. Other income and gains included a $664 million gain on the sale of an investment within our private equity operations ($261 million attributable to shareholders) and we recorded $525 million of other income on the settlement of a long-dated interest rate swap. We recorded a lower level of fair value gains on consolidated investment properties as well as those held through equity accounted investments, resulting in a decrease of $490 million in fair value changes and a decrease of $478 million in equity accounted income compared to 2012. Our provision for income taxes increased by $326 million due primarily to the recognition of deferred income tax expenses attributed to the formation of BPY and a higher amount of disposition gains.

Net income per share was $3.12 for 2013 and $1.97 in 2012. Net income attributable to shareholders increased by $740 million primarily due to the recognition of carried interest, which was entirely attributable to shareholders.

18 BROOKFIELD ASSET MANAGEMENT

Statements of Operations

Revenues and Direct Costs

The following tables present consolidated revenues and direct costs, which we have disaggregated into our operating segments in order to facilitate a review of year-over-year variances.

| Change | ||||||||||||||||||||

| FOR THE YEARS ENDED DECEMBER 31 (MILLIONS) |

2014 | 2013 | 2012 | 2014 vs 2013 | 2013 vs 2012 | |||||||||||||||

| Revenues |

||||||||||||||||||||

| Asset management |

$ | 771 | $ | 1,183 | $ | 450 | $ | (412) | $ | 733 | ||||||||||

| Property |

5,010 | 4,569 | 3,982 | 441 | 587 | |||||||||||||||

| Renewable energy |

1,679 | 1,620 | 1,179 | 59 | 441 | |||||||||||||||

| Infrastructure |

2,193 | 2,326 | 2,178 | (133) | 148 | |||||||||||||||

| Private equity |

2,559 | 4,124 | 4,424 | (1,565) | (300) | |||||||||||||||

| Residential development |

2,912 | 2,521 | 2,476 | 391 | 45 | |||||||||||||||

| Service activities |

3,599 | 3,817 | 4,070 | (218) | (253) | |||||||||||||||

| Corporate activities |

199 | 352 | 260 | (153) | 92 | |||||||||||||||

| Eliminations and adjustments1 |

(558) | (419) | (323) | (139) | (96) | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total consolidated revenues |

$ | 18,364 | $ | 20,093 | $ | 18,696 | $ | (1,729) | $ | 1,397 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| 1. Adjustment to eliminate base management fees and interest income earned from entities that we consolidate. See Note 3 to our Consolidated Financial Statements |

| |||||||||||||||||||

| Change | ||||||||||||||||||||

| FOR THE YEARS ENDED DECEMBER 31 (MILLIONS) |

2014 | 2013 | 2012 | 2014 vs 2013 | 2013 vs 2012 | |||||||||||||||

| Direct costs |

||||||||||||||||||||

| Asset management |

$ | 390 | $ | 318 | $ | 260 | $ | 72 | $ | 58 | ||||||||||

| Property |

2,628 | 2,333 | 1,812 | 295 | 521 | |||||||||||||||

| Renewable energy |

530 | 550 | 475 | (20) | 75 | |||||||||||||||

| Infrastructure |

991 | 1,125 | 1,190 | (134) | (65) | |||||||||||||||

| Private equity |

2,244 | 3,391 | 3,826 | (1,147) | (435) | |||||||||||||||

| Residential development |

2,519 | 2,297 | 2,279 | 222 | 18 | |||||||||||||||

| Service activities |

3,472 | 3,687 | 3,911 | (215) | (224) | |||||||||||||||

| Corporate activities |

108 | 66 | 114 | 42 | (48) | |||||||||||||||

| Eliminations and adjustments1 |

236 | 161 | 94 | 75 | 67 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| $ | 13,118 | $ | 13,928 | $ | 13,961 | $ | (810) | $ | (33) | |||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| 1. | Adjustment to reallocate unallocated segment costs |

2014 vs. 2013

Asset management: Revenues decreased by $412 million in 2014 due to the recognition of $558 million of carried interest in the prior year, upon crystallizing a large client investment gain. Fee bearing capital increased by 20%, which contributed to a $123 million increase in base management fees to $625 million. Direct costs increased by $72 million to $390 million due to the expansion of our asset management operations.

Property: Commercial property revenue increased by $441 million (10%) reflecting the addition of revenues from recent acquisitions in our multifamily and industrial businesses and a portfolio of triple net lease assets. These increases were partially offset by lower revenues in our office business due to a significant lease expiry in downtown New York City in October 2013 and the elimination of revenues on mature assets that had been sold. Direct costs increased by $295 million (13%) due to the inclusion of costs associated with newly acquired assets.

Renewable energy: Revenues increased by $59 million (4%). Newly acquired or commissioned assets, along with a full year’s contribution from facilities acquired in 2013, contributed $151 million of additional revenue. This more than offset the reduction in revenue from facilities owned throughout both years due to a contractual price decrease in a previously high priced contract, limited operations of a gas-fired plant in 2014 and the impact of lower exchange rates on facilities in Canada and Brazil. Direct costs are largely fixed and the impact of lower exchange rates on non-U.S. operations was partially offset by additional operating costs from recently acquired facilities.

2014 ANNUAL REPORT 19

Infrastructure: Revenues decreased by $133 million (6%) due to the elimination of $304 million of revenues from Pacific Northwest timberlands that were sold in July 2013. This decrease was partially offset by revenues generated from recently completed development projects and acquisitions as well as higher volumes across our transport businesses. Direct operating costs decreased by $134 million (12%). The sale of our Pacific Northwest timberlands decreased costs by $173 million. This was partially offset by acquisitions and capital expansions completed in the last year which increased operating costs by approximately $50 million.

Private equity: Revenues decreased by $1,565 million (38%) and direct costs decreased by $1,147 million (34%) as a result of the elimination of revenues and costs following sale of two forest products investments which contributed $1,439 million of revenues and $1,222 million of direct costs in 2013. In addition, a 31% decline in panelboard prices compared to the prior year decreased revenues by a further $250 million. These decreases were partially offset by higher sales volumes at our energy-related investments due to higher natural gas production compared to the prior year.

Residential development: Revenues and direct costs increased by $391 million (16%) and $222 million (10%), respectively, reflecting the completion and delivery of a larger number of projects in our Brazilian operations. Our North American operations revenues increased by $120 million due to increased U.S. housing sales and stronger pricing. We also sold two commercial properties within our North American operations in the first quarter of 2014, which generated revenues of $83 million.

Service activities: Revenues and direct costs decreased in our service activities by $218 million (6%) and $215 million (6%), respectively. Construction revenues and direct costs decreased by $551 million and $541 million, respectively. These operations recognize revenue using the percentage-of-completion methodology and project delays experienced in the first three quarters of 2014 across several geographies reduced construction progress and the associated revenue recognition. In addition, the majority of these revenues and costs are earned and incurred in Australia and were impacted by the 7% decline in that currency.

Corporate activities: Revenues declined in our corporate activities due to reduced investment gains in our portfolio of financial assets during 2014 compared to 2013.

2013 vs. 2012

Asset management: Revenues increased by $733 million with carried interests contributing $549 million of the increase. Base management fees increased by $150 million to $502 million. Fee bearing capital increased by 32% following the formation of Brookfield Property Partners and increases in capital committed to property and infrastructure funds. The increase in direct costs reflects the higher level of fee bearing capital and the reallocation of costs from our corporate activities segment to our asset management segment following the formation of Brookfield Property Partners to match them with the associated fee revenues.

Property: Revenues and direct costs increased by $587 million (15%) and $521 million (29%), respectively, due to the inclusion of a full year of results of a large hotel resort property that was acquired in April 2012 and the revenues and costs of industrial and logistics businesses acquired in 2013 and during the latter part of 2012.

Renewable energy: Generation revenues were $441 million (37%) higher. Revenue from facilities owned throughout both years increased by $209 million from a return to near normal hydrology conditions in North America, compared to very dry conditions in 2012, which resulted in generation that was 12% below long-term averages. Newly acquired or commissioned assets contributed an additional $218 million of revenues. Direct costs increased by $75 million (16%) reflecting the costs associated with new assets.

Infrastructure: Revenues increased by $148 million (7%) due to additional revenues from recently completed capital expansions initiatives, including our Australian rail expansion, and acquisitions of a utility business in the United Kingdom and toll roads in South America. This was partially offset by lower timber revenues following the sale of our Pacific Northwest timberlands during the third quarter of the year. Direct costs decreased by $65 million (5%), following the sale of Pacific Northwest timberlands which was partially offset by costs incurred within recently acquired or expanded businesses.

Private equity: Revenues decreased by $300 million (7%) and direct costs by $435 million (11%), primarily as a result of the elimination of revenue following the sale of a paper and packaging business midway through 2013. This decrease was partially offset by the impact of higher prices and increased volumes within our wood-based panel production and forestry operations.

Residential development: The increase in residential revenues of $45 million (2%) is due to an increase in home closings combined with an increase in average home selling prices resulting in higher housing margins. The increase in revenues from home closings was offset by decreased land sales revenue. We completed a larger volume of lots and multifamily acre parcel sales in 2012. Direct costs increased by $18 million (1%) reflecting the costs incurred in respect of increased home sales.

Service activities: Revenues decreased by $253 million (6%), the majority of which reflects the absence of revenues and costs following the partial sale of an Australian property services business in early 2013 and the majority sale of a large U.S. property brokerage business in late 2012 which resulted in both of these operations being deconsolidated. These decreases were partially offset by higher construction revenues relating to increases in the number and scale of projects under construction.

20 BROOKFIELD ASSET MANAGEMENT

Corporate activities: Revenues increased, primarily from stronger capital market performance within our cash and financial asset portfolio.

Other Income and Gains

Other income and gains were $190 million in 2014 compared to $1,262 million in the prior year. Other income and gains in the current year include a $143 million gain on the repayment of a distressed debt investment in a European office portfolio. The prior year included a $525 million gain on the termination of a long-dated interest rate swap contract as well as a $664 million gain on the sale of a pulp and paper investment. Other income and gains in 2012 represent a gain on the partial sale and deconsolidation of a property services operation.

Equity Accounted Income

Equity accounted income represents our share of the net income recorded by investments over which we exercise significant influence and is reported as a single line item in our consolidated statement of operations. The following table disaggregates consolidated equity accounted income to facilitate analysis:

| Change | ||||||||||||||||||||

| FOR THE YEARS ENDED DECEMBER 31 (MILLIONS) |

2014 | 2013 | 2012 | 2014 vs 2013 | 2013 vs 2012 | |||||||||||||||

| General Growth Properties |

$ | 1,006 | $ | 426 | $ | 979 | $ | 580 | $ | (553) | ||||||||||

| Other property operations |

387 | 447 | 198 | (60) | 249 | |||||||||||||||

| Infrastructure operations |

81 | (193) | 9 | 274 | (202) | |||||||||||||||

| Other |

120 | 79 | 51 | 41 | 28 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| $ | 1,594 | $ | 759 | $ | 1,237 | $ | 835 | $ | (478) | |||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

Our share of General Growth Properties Inc.’s (“General Growth Properties” or “GGP”) equity accounted income increased from 2013 to 2014 due to a 6% increase in our weighted average ownership interest in GGP from 23% to 29% in December 2013. GGP’s net income increased year-over-year as a result of higher amount of appraisal gains continued strength in its leasing activity and improving market conditions for Class A malls, which led to lower discount rates and terminal capitalization rates compared to the prior year. This was partially offset by our share of the mark-to-market loss recorded by GGP in respect of outstanding warrants. Our share of GGP’s appraisal gains in 2014, 2013 and 2012 were $417 million, $127 million and $707 million, respectively. In addition, current year equity accounted income includes the reversal of a $249 million impairment loss recognized in 2013. This reversal followed a 40% increase in GGP’s share price from $20.07 to $28.13 at December 31, 2014, compared to our carrying value of approximately $27 per share.

Equity accounted income from other property operations decreased by $60 million in 2014 compared to an increase of $249 million in 2013. The decrease in 2014 was due primarily to a $34 million decrease in our share of net income at Rouse Properties Inc. (“Rouse Properties”), as a result of a higher level of appraisal gains being recorded in 2013 than in 2014. The $249 million increase in other property operations over 2012 was primarily due to a larger number of property operations being equity accounted in 2013.

Infrastructure equity accounted income increased by $274 million compared to 2013. In 2013 we recorded a valuation charge of $275 million against the carrying value of our North American natural gas pipeline investment reflecting weaker market fundamentals. These conditions persisted through 2014 impacting our equity accounted earnings from this investment. This decrease was partially offset by equity accounted earnings associated with our higher ownership percentage at our Brazilian toll road investment and the acquisition of an equity accounted Brazilian integrated logistics business during the year.

Other equity accounted income in 2014 of $120 million includes $66 million of equity accounted income within our North American and Brazilian residential operations, due to increased sales and deliveries compared to the prior years.

Interest Expense

The following table presents interest expense organized by the balance sheet classification of the associated liability:

| Change | ||||||||||||||||||||

| FOR THE YEARS ENDED DECEMBER 31 (MILLIONS) |

2014 | 2013 | 2012 | 2014 vs 2013 | 2013 vs 2012 | |||||||||||||||

| Corporate borrowings |

$ | 228 | $ | 204 | $ | 209 | $ | 24 | $ | (5) | ||||||||||

| Non-recourse borrowings |

||||||||||||||||||||

| Property-specific mortgages |

2,047 | 1,837 | 1,808 | 210 | 29 | |||||||||||||||

| Subsidiary borrowings |

272 | 464 | 408 | (192) | 56 | |||||||||||||||

| Subsidiary equity obligations |

32 | 48 | 75 | (16) | (27) | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| $ | 2,579 | $ | 2,553 | $ | 2,500 | $ | 26 | $ | 53 | |||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

2014 ANNUAL REPORT 21

We refinanced high cost subsidiary borrowings in the third quarter of 2013 with lower coupon corporate debt, which decreased subsidiary borrowings interest expense by $87 million in the current year and consolidated interest expense by $60 million in aggregate. Subsidiary borrowings also decreased between 2014 and 2013 as we replaced unsecured debt at subsidiaries with asset-secured non-recourse financings.

Interest expense on property-specific mortgages increased by $210 million over the prior year reflecting additional borrowings associated with acquisitions and capital projects in our property, renewable energy and infrastructure operations as well as increased borrowing levels on property specific mortgage refinancings albeit at reduced rates. Property-specific borrowing costs remained stable between 2013 and 2012 as increased borrowings to finance acquisitions was largely offset by lower borrowing costs on recent refinancings.

Fair Value Changes

The following table disaggregates fair value changes into major components to facilitate analysis:

| Change | ||||||||||||||||||||

| FOR THE YEARS ENDED DECEMBER 31 (MILLIONS) |

2014 | 2013 | 2012 | 2014 vs 2013 | 2013 vs 2012 | |||||||||||||||

| Investment properties |

$ | 3,266 | $ | 1,031 | $ | 1,276 | $ | 2,235 | $ | (245) | ||||||||||

| General Growth Properties warrants |

526 | 53 | (47) | 473 | 100 | |||||||||||||||

| Investment in Canary Wharf |

319 | 89 | 20 | 230 | 69 | |||||||||||||||

| Forest products investment |

230 | — | — | 230 | — | |||||||||||||||

| Power contracts |

(13) | (134) | 9 | 121 | (143) | |||||||||||||||

| Other private equity investments |

(31) | (94) | (119) | 63 | 25 | |||||||||||||||

| Redeemable fund units |

(283) | (20) | (11) | (263) | (9) | |||||||||||||||

| Impairments of goodwill, inventory and other |

(340) | (262) | 25 | (78) | (287) | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| $ | 3,674 | $ | 663 | $ | 1,153 | $ | 3,011 | $ | (490) | |||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

Investment Properties

Investment properties contributed appraisal gains totalling $3.3 billion in 2014 compared to $1.0 billion in 2013 and $1.3 billion in 2012. In each year the gains related primarily to our office properties. Asset values benefitted from continued declines in discount rates and terminal capitalization rates, each of which declined by approximately 30 basis points on average in 2014, reflecting a continued favourable investment climate for high-quality commercial office properties. Gains also reflected improvements in projected cash flows based on tenant profile and local market conditions at each year end, based on improvements in local economic conditions, tenant leasing profiles, and rental markets. The decline in rates contributed approximately 55% of the gains, while improvements in projected cash flows contributed approximately 45% of the gains.

Fair value gains were lower in 2013 compared to 2012 due to relatively smaller declines in discount rates and terminal capitalization rates which declined in each of our principal regions by approximately 10 basis points, on average. The changes in rates during 2013 contributed approximately half of the gains, while increases in projected cash flows contributed the remainder.

In 2012 average discount rates declined in each of our principal regions by 20 to 30 basis points, while terminal capitalization rates decreased in Australia and Canada by 40 basis points and 50 basis points, respectively. The changes in rates contributed approximately 70% of the gains, while increases in projected cash flows contributed the remainder.

We discuss the key valuation inputs of our investment properties on page 26.

General Growth Properties Warrants

The fair value of our GGP warrants increased by $526 million during 2014 primarily due to a 40% increase in the GGP’s share price during 2014. This gain was partially offset by our share of GGP’s mark-to-market loss on the warrants, which is included within equity accounted income. These warrants are convertible into 70 million common shares of GGP.

Investment in Canary Wharf

Development activities, improved net operating income, and the impact of lower discount rates on projected cash flows gave rise to an increase in the value of our investment in Canary Wharf Group plc (“Canary Wharf”) of $319 million during the year, higher than the $89 million and $20 million in 2013 and 2012, respectively.

Forest Products Investment

During the first quarter of 2014 we disposed of a partial interest in a private equity investee company, resulting in us deconsolidating the business from our results and revaluing our retained interest based on its quoted market price at the time of our loss of control. This gave rise to a $230 million revaluation gain relating to the excess of fair value over our IFRS book value of our retained interest.

22 BROOKFIELD ASSET MANAGEMENT

Power Contracts

Certain of our long-term power contracts are accounted for as derivatives with changes in fair value recorded in net income. These contracts generally relate to the future sale of electricity at fixed prices and therefore increase in value when prices decline, and vice versa. We recorded an aggregate mark-to-market loss of $13 million in the current year on these contracts due to increased projections for future electricity prices, compared to $134 million of losses and $9 million of gains in 2013 and 2012, respectively.

Other Private Equity Investments

Private equity fair value changes reflect impairments from lower oil and gas reserves and valuations at investee companies in the energy sector, due to reductions in well performance and pricing.

Redeemable Funds Units

Fair value changes on redeemable fund units contributed a valuation charge of $283 million in 2014 that related primarily to increases in the value of units held by others in these funds where these units are classified as liabilities, rather than equity. A large portion of these units relate to our partners’ interests in our Los Angeles office portfolio, and accordingly this mark-to-market loss reflects unitholders’ interests in the investment property appraisal gains.

Impairments of Goodwill and Other

We recognized an $87 million impairment of the goodwill associated with our Brazilian residential operations, which are experiencing weaker market fundamentals. This has resulted in a decrease in margins relating to cost overruns and a slowing consumer demand. We also recognized a $121 million impairment of these operations’ inventory, as certain projects are no longer profitable.

Depreciation and Amortization

Depreciation and amortization includes the depreciation of property, plant and equipment as well as the amortization of intangible assets. The two largest contributions to depreciation and amortization come from our renewable energy and infrastructure facilities, many of which are revalued annually in other comprehensive income (“OCI”); but which are depreciated in net income. Depreciation on many of these assets is based on their fair value at the beginning of each year to the extent they are revalued. We do not record depreciation on assets that are classified as investment properties (i.e., commercial office and retail properties) or biological assets (for example our timberlands and agricultural assets). The amount of depreciation and amortization is generally consistent year-over-year with large changes typically due to the addition or removal of depreciable assets and revaluation of their carrying values.

Depreciation and amortization is summarized in the following table:

| Change | ||||||||||||||||||||

| FOR THE YEARS ENDED DECEMBER 31 (MILLIONS) |

2014 | 2013 | 2012 | 2014 vs 2013 | 2013 vs 2012 | |||||||||||||||

| Renewable energy |

$ | 566 | $ | 553 | $ | 499 | $ | 13 | $ | 54 | ||||||||||

| Infrastructure |

395 | 346 | 248 | 49 | 98 | |||||||||||||||

| Private equity |

225 | 275 | 282 | (50) | (7) | |||||||||||||||

| Property |

261 | 256 | 225 | 5 | 31 | |||||||||||||||

| Other |

23 | 25 | 9 | (2) | 16 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| $ | 1,470 | $ | 1,455 | $ | 1,263 | $ | 15 | $ | 192 | |||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

Infrastructure depreciation and amortization increased by $49 million between 2014 and 2013, following a $98 million increase between 2013 and 2012. The increase in 2014 was due to increased asset valuations and depreciation on acquired property, plant and equipment while the increase in 2013 relates to depreciation on completed developments including those at our Australian rail operations.

Our private equity operations sold a forest products business in 2014, eliminating the depreciation on the asset, and our property operations recorded less amortization of intangibles associated with hotel assets following the sale of a resort operation.

Income Taxes

Income tax expense increased by $478 million to $1,323 million in 2014. We recorded deferred income taxes associated with the $3.3 billion investment property valuation increases in 2014, which were significantly higher than in 2013. The current year also includes a $320 million non-recurring deferred income tax expense that resulted from a change in tax laws that affected our North American office property operations in the first quarter of 2014. Income tax expense in the current year includes the recognition of previously unrecognized tax losses within our North American residential operations, offset by the derecognition of deferred tax assets within our Brazil residential operations. The prior year included $178 million of deferred income taxes related to the formation of Brookfield Property Partners.

2014 ANNUAL REPORT 23

Our effective tax rate in 2014 was 20% (2013 – 18%; 2012 – 16%), while our Canadian domestic statutory income tax rate remained constant at 26% (2013 – 26%; 2012 – 26%). The differences are primarily attributable to our role as a global asset manager. As an asset manager, many of our operations and the associated net income occur within partially owned, “flow through” entities such as partnerships, and any tax liability is incurred by the investors as opposed to the entity. As a result, while our consolidated net income includes income attributable to non-controlling ownership interest in these entities, our consolidated tax provision includes only our proportionate share of the tax provision of these entities. In other words, we are consolidating all of their net income, but only our share of their tax provision. This gave rise to a 5% (2013 – 7%) reduction in our effective tax rate.

In addition, as a global company, we operate in countries with different tax rates, most of which vary from our domestic statutory rate and we also benefit from tax incentives introduced in various countries to encourage economic activity. Differences in global tax rates gave rise to a 5% (2013 – 3%) reduction in our effective tax rate. The difference will vary from year to year depending on the relative proportion of income in each country.

The tax provision includes both a current and deferred tax provision. The current tax provision represents the portion of the provision that gives rise to a current tax liability. The deferred tax provision arises from income that is subject to tax in future periods (commonly referred to as “timing differences”) and the utilization of existing tax assets such as accumulated tax losses.

In our case, the deferred tax provision relates principally to fair value gains, which are not taxable until the assets are sold, and therefore do not give rise to a current tax liability, as well as the depreciation of assets which are depreciated for tax purposes at rates that differ from the rates used in our financial statements.

Our income tax provision does not include a number of non-income taxes paid that are recorded elsewhere in our financial statements. For example, a number of our operations in Brazil are required to pay non-recoverable taxes on revenue, which are included in direct costs as opposed to income taxes. In addition, we pay considerable property, payroll and other taxes that represent an important component of the tax base in the jurisdictions in which we operate.

Non-controlling Interests

Non-controlling interests represent the portion of net income of consolidated entities that is attributable to other investors. Non-controlling interests totalled $2.1 billion in 2014 compared to $1.7 billion in 2013 and $1.4 billion in 2012, representing 40%, 45% and 50% of consolidated net income, respectively, in each of these years. The variances between these three years reflect the overall change in consolidated net income with income attributable to shareholders increasing more than on a consolidated basis in 2014 primarily due to the privatization of our office property portfolio which increased our ownership percentage and our share of the fair value gains recognized during the year, and in 2013 due to the recognition of a large gain and carried interests which were recorded in wholly owned operations.

Other Comprehensive Income (“OCI”)

Revaluation of Property, Plant and Equipment

The following table summarizes revaluations of property, plant and equipment:

| Change | ||||||||||||||||||||

| FOR THE YEARS ENDED DECEMBER 31 (MILLIONS) |

2014 | 2013 | 2012 | 2014 vs 2013 | 2013 vs 2012 | |||||||||||||||

| Renewable energy |

$ | 1,966 | $ | (151) | $ | 825 | $ | 2,117 | $ | (976) | ||||||||||

| Infrastructure |

708 | 781 | 611 | (73) | 170 | |||||||||||||||

| Property and other |

324 | 195 | 55 | 129 | 140 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| $ | 2,998 | $ | 825 | $ | 1,491 | $ | 2,173 | $ | (666) | |||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

Revaluations of property, plant and equipment totalled $3.0 billion in 2014, representing an increase from the $825 million recorded in 2013 and $1.5 billion in 2012. These revaluations are primarily influenced by estimated future cash flows and discount rates. Estimated future power prices are the primary determining factor of future cash flows in our renewable energy operations. In our infrastructure operations cash flows are driven by regulated rates of return on rate base in our utility assets and tariffs or capacity charges in our transport and energy assets, while expected hotel stays and room rates increase or decrease cash flows in our hotel assets within our property operations. In 2014 and 2012 decreases in long-term interest rates and increases in comparable assets gave rise to increased valuations of these assets. In 2013, expected future cash flows increased, however this was partially offset by increasing fixed-income yields which lowered asset values.

We discuss the key valuation inputs on page 27.

24 BROOKFIELD ASSET MANAGEMENT

Financial Contracts and Power Sales Agreements

We recorded $301 million of losses on our financial contracts and power sales agreements in 2014 compared to a gain of $442 million in 2013 and a loss of $17 million in 2012. We recorded $247 million of mark-to-market and realized losses on interest rate contracts that “lock-in” the benchmark interest rate on new financings, due to an overall decline in risk-free rates. In 2013, we recorded $185 million of gains on similar contracts as rates increased during the year.

Foreign Currency Translation

We record the impact of changes in foreign currencies on the carrying value of our net investments in non-U.S. operations in other comprehensive income. As at December 31, 2014, our IFRS net equity of $20.2 billion was invested in the following currencies, principally in the form of net investments which are revalued through other comprehensive income: United States – 52%; Brazil – 15%; Australia – 14%; United Kingdom – 10%; Canada – 5%; and other – 4%. From time to time, we utilize financial contracts to adjust these exposures. Changes in the value of currency contracts that qualify as hedges are included in foreign currency translation. During 2014, the value of our principal non-U.S. currencies (Australia, Brazil and Canada) all declined against the U.S. dollar (see table on page 16), giving rise to a total decrease of $1.7 billion after the mitigating impact of hedges, or $0.7 billion after non-controlling interests.

FINANCIAL PROFILE

Consolidated Assets

The following table presents our consolidated assets at December 31, 2014, compared to the two previous years:

| AS AT DECEMBER 31 (MILLIONS) |

2014 | 2013 | 2012 | |||||||||

| Investment properties |

$ | 46,083 | $ | 38,336 | $ | 33,161 | ||||||

| Property, plant and equipment |

34,617 | 31,019 | 31,148 | |||||||||

| Sustainable resources |

446 | 502 | 3,516 | |||||||||

| Equity accounted investments |

14,916 | 13,277 | 11,618 | |||||||||

| Cash and cash equivalents |

3,160 | 3,663 | 2,850 | |||||||||

| Financial assets |

6,285 | 4,947 | 3,111 | |||||||||

| Accounts receivable and other |

8,399 | 6,666 | 6,952 | |||||||||

| Inventory |

5,620 | 6,291 | 6,581 | |||||||||

| Intangible assets |

4,327 | 5,044 | 5,770 | |||||||||

| Goodwill |

1,406 | 1,588 | 2,490 | |||||||||

| Deferred income tax asset |

1,414 | 1,412 | 1,665 | |||||||||

| Assets held for sale |

2,807 | — | — | |||||||||

|

|

|

|

|

|

|

|||||||

| $ | 129,480 | $ | 112,745 | $ | 108,862 | |||||||

|

|

|

|

|

|

|

|||||||