UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

| Quarterly Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 | |||||

| For the quarterly period ended | ||||||||

| or | ||||||||

| Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 | ||||||||

| For the transition period from _______________ to _______________ | ||||||||

Commission File No. 1-13998

Insperity, Inc.

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

| (Address of principal executive offices) | ||||||||

(Registrant’s Telephone Number, Including Area Code): (281 ) 358-8986

| Securities registered pursuant to Section 12(b) of the Act: | ||||||||

| Title of each class | Ticker symbol(s) | Name of each exchange on which registered | ||||||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See definition of “large accelerated filer,” “accelerated filer”, “non-accelerated filer”, “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| ☒ | Accelerated filer | ☐ | |||||||||

| Non-accelerated filer | ☐ | Emerging growth company | |||||||||

| Smaller reporting company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ☐ No ☒

As of April 19, 2022, 38,307,974 shares of the registrant’s common stock, par value $0.01 per share, were outstanding.

TABLE OF CONTENTS | ||

| Page | ||||||||

| Part I, Item 1. | ||||||||

| Part I, Item 2. | ||||||||

| Part I, Item 3. | ||||||||

| Part I, Item 4. | ||||||||

| Part II, Item 1. | ||||||||

| Part II, Item 1A. | ||||||||

| Part II, Item 2. | ||||||||

| Part II, Item 6. | ||||||||

| FORWARD LOOKING STATEMENTS | ||

The statements contained herein that are not historical facts are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. You can identify such forward-looking statements by the words “anticipates,” “expects,” “intends,” “plans,” “projects,” “believes,” “estimates,” “likely,” “possibly,” “probably,” “could,” “goal,” “opportunity,” “objective,” “target,” “assume,” “outlook,” “guidance,” “predicts,” “appears,” “indicator” and similar expressions. Forward-looking statements involve a number of risks and uncertainties. In the normal course of business, in an effort to help keep our stockholders and the public informed about our operations, from time to time, we may issue such forward-looking statements, either orally or in writing. Generally, these statements relate to business plans or strategies; projected or anticipated benefits or other consequences of such plans or strategies; or projections involving anticipated revenues, earnings, average number of worksite employees (“WSEEs”), benefits and workers’ compensation costs, or other operating results. We base the forward-looking statements on our current expectations, estimates and projections. We caution you that these statements are not guarantees of future performance and involve risks, uncertainties and assumptions that we cannot predict. In addition, we have based many of these forward-looking statements on assumptions about future events that may prove to be inaccurate. Therefore, the actual results of the future events described in such forward-looking statements could differ materially from those stated in such forward-looking statements. Among the factors that could cause actual results to differ materially are:

•adverse economic conditions;

•impact of the COVID-19 pandemic, or other future pandemics, including the scope, severity and duration of the pandemic; government responses; regulatory developments; and the related disruptions and economic impact to our business and the small and medium-sized businesses that we serve;

•labor shortages and increasing competition for highly skilled workers;

•impact of inflation;

•vulnerability to regional economic factors because of our geographic market concentration;

•failure to comply with covenants under our credit facility;

•our liability for WSEE payroll, payroll taxes and benefits costs, or other liabilities associated with actions of our client companies or WSEEs;

•increases in health insurance costs and workers’ compensation rates and underlying claims trends, health care reform, financial solvency of workers’ compensation carriers, other insurers or financial institutions, state unemployment tax rates, liabilities for employee and client actions or payroll-related claims;

•an adverse determination regarding our status as the employer of our WSEEs for tax and benefit purposes and an inability to offer alternative benefit plans following such a determination;

•cancellation of client contracts on short notice, or the inability to renew client contracts or attract new clients;

•the ability to secure competitive replacement contracts for health insurance and workers’ compensation insurance at expiration of current contracts;

•regulatory and tax developments and possible adverse application of various federal, state and local regulations;

•failure to manage growth of our operations and the effectiveness of our sales and marketing efforts;

•the impact of the competitive environment and other developments in the human resources services industry, including the professional employer organization (or PEO) industry, on our growth and/or profitability;

•an adverse final judgment or settlement of claims against Insperity;

•disruptions of our information technology systems or failure to enhance our service and technology offerings to address new regulations or client expectations;

•our liability or damage to our reputation relating to disclosure of sensitive or private information as a result of data theft, cyberattacks or security vulnerabilities;

Insperity | 2022 First Quarter Form 10-Q | 4 | ||||

| FORWARD LOOKING STATEMENTS | ||

•failure of third-party providers, data centers or cloud service providers; and

•our ability to integrate or realize expected returns on our acquisitions.

These factors are discussed in further detail in our Annual Report on Form 10-K for the year ended December 31, 2021 under “Item 1A. Risk Factors” in Part I and “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations” in Part II, and elsewhere in this report. Any of these factors, or a combination of such factors, could materially affect the results of our operations and whether forward-looking statements we make ultimately prove to be accurate.

Any forward-looking statements are made only as of the date hereof and, unless otherwise required by applicable securities laws, we undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

Insperity | 2022 First Quarter Form 10-Q | 5 | ||||

| FINANCIAL STATEMENTS (Unaudited) | ||

PART I

Item 1. Financial Statements

CONDENSED CONSOLIDATED BALANCE SHEETS

| (in thousands) | March 31, 2022 | December 31, 2021 | |||||||||

| Assets | |||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

| Restricted cash | |||||||||||

| Marketable securities | |||||||||||

| Accounts receivable, net | |||||||||||

| Prepaid insurance | |||||||||||

| Other current assets | |||||||||||

| Income taxes receivable | |||||||||||

| Total current assets | |||||||||||

| Property and equipment, net of accumulated depreciation | |||||||||||

| Right-of-use (“ROU”) leased assets | |||||||||||

| Prepaid health insurance | |||||||||||

| Deposits – health insurance | |||||||||||

| Deposits – workers’ compensation | |||||||||||

| Goodwill and other intangible assets, net | |||||||||||

| Deferred income taxes, net | |||||||||||

| Other assets | |||||||||||

| Total assets | $ | $ | |||||||||

| Liabilities and stockholders' equity | |||||||||||

| Accounts payable | $ | $ | |||||||||

| Payroll taxes and other payroll deductions payable | |||||||||||

| Accrued worksite employee payroll cost | |||||||||||

| Accrued health insurance costs | |||||||||||

| Accrued workers’ compensation costs | |||||||||||

| Accrued corporate payroll and commissions | |||||||||||

| Other accrued liabilities | |||||||||||

| Income taxes payable | |||||||||||

| Total current liabilities | |||||||||||

| Accrued workers’ compensation cost, net of current | |||||||||||

| Long-term debt | |||||||||||

| Operating lease liabilities, net of current | |||||||||||

| Deferred income taxes, net | |||||||||||

| Total noncurrent liabilities | |||||||||||

| Commitments and contingencies | |||||||||||

| Common stock | |||||||||||

| Additional paid-in capital | |||||||||||

| Treasury stock, at cost | ( | ( | |||||||||

| Retained earnings | |||||||||||

| Total stockholders’ equity (deficit) | ( | ||||||||||

| Total liabilities and stockholders’ equity | $ | $ | |||||||||

See accompanying notes.

Insperity | 2022 First Quarter Form 10-Q | 6 | ||||

| FINANCIAL STATEMENTS (Unaudited) | ||

CONSOLIDATED STATEMENTS OF OPERATIONS

| Three Months Ended March 31, | ||||||||

| (in thousands, except per share amounts) | 2022 | 2021 | ||||||

Revenues(1) | $ | $ | ||||||

Payroll taxes, benefits and workers’ compensation costs | ||||||||

| Gross profit | ||||||||

| Salaries, wages and payroll taxes | ||||||||

| Stock-based compensation | ||||||||

| Commissions | ||||||||

| Advertising | ||||||||

| General and administrative expenses | ||||||||

| Depreciation and amortization | ||||||||

| Total operating expenses | ||||||||

| Operating income | ||||||||

| Other income (expense): | ||||||||

| Interest income | ||||||||

| Interest expense | ( | ( | ||||||

| Income before income tax expense | ||||||||

| Income tax expense | ||||||||

| Net income | $ | $ | ||||||

Less distributed and undistributed earnings allocated to participating securities | ( | ( | ||||||

| Net income allocated to common shares | $ | $ | ||||||

| Net income per share of common stock | ||||||||

| Basic | $ | $ | ||||||

| Diluted | $ | $ | ||||||

____________________________________

(1)Revenues are comprised of gross billings less WSEE payroll costs as follows:

| Three Months Ended March 31, | ||||||||

| (in thousands) | 2022 | 2021 | ||||||

| Gross billings | $ | $ | ||||||

| Less: WSEE payroll cost | ||||||||

| Revenues | $ | $ | ||||||

See accompanying notes.

Insperity | 2022 First Quarter Form 10-Q | 7 | ||||

| FINANCIAL STATEMENTS (Unaudited) | ||

CONSOLIDATED STATEMENTS OF CASH FLOWS

| Three Months Ended March 31, | |||||||||||

| (in thousands) | 2022 | 2021 | |||||||||

| Cash flows from operating activities | |||||||||||

| Net income | $ | $ | |||||||||

| Adjustments to reconcile net income to net cash provided by operating activities: | |||||||||||

| Depreciation and amortization | |||||||||||

| Stock-based compensation | |||||||||||

| Deferred income taxes | |||||||||||

| Changes in operating assets and liabilities: | |||||||||||

| Accounts receivable | ( | ( | |||||||||

| Prepaid insurance | ( | ( | |||||||||

| Other current assets | ( | ( | |||||||||

| Other assets and ROU assets | ( | ||||||||||

| Accounts payable | ( | ||||||||||

| Payroll taxes and other payroll deductions payable | ( | ( | |||||||||

| Accrued worksite employee payroll expense | |||||||||||

| Accrued health insurance costs | |||||||||||

| Accrued workers’ compensation costs | ( | ( | |||||||||

| Accrued corporate payroll, commissions and other accrued liabilities | ( | ( | |||||||||

| Income taxes payable/receivable | ( | ||||||||||

| Total adjustments | ( | ( | |||||||||

| Net cash provided by operating activities | |||||||||||

| Cash flows from investing activities | |||||||||||

| Marketable securities: | |||||||||||

| Purchases | ( | ( | |||||||||

| Proceeds from maturities | |||||||||||

| Property and equipment: | |||||||||||

| Purchases | ( | ( | |||||||||

| Net cash used in investing activities | ( | ( | |||||||||

| Cash flows from financing activities | |||||||||||

| Purchase of treasury stock | ( | ( | |||||||||

| Dividends paid | ( | ( | |||||||||

| Other | |||||||||||

| Net cash used in financing activities | ( | ( | |||||||||

| Net increase (decrease) in cash, cash equivalents and restricted cash | ( | ||||||||||

| Cash, cash equivalents and restricted cash beginning of period | |||||||||||

| Cash, cash equivalents and restricted cash end of period | $ | $ | |||||||||

Insperity | 2022 First Quarter Form 10-Q | 8 | ||||

| FINANCIAL STATEMENTS (Unaudited) | ||

CONSOLIDATED STATEMENTS OF CASH FLOWS (Continued)

| Three Months Ended March 31, | |||||||||||

| (in thousands) | 2022 | 2021 | |||||||||

Supplemental schedule of cash and cash equivalents and restricted cash | |||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

| Restricted cash | |||||||||||

| Deposits – workers’ compensation | |||||||||||

| Cash, cash equivalents and restricted cash beginning of period | $ | $ | |||||||||

| Cash and cash equivalents | $ | $ | |||||||||

| Restricted cash | |||||||||||

| Deposits – workers’ compensation | |||||||||||

| Cash, cash equivalents and restricted cash end of period | $ | $ | |||||||||

Supplemental operating lease cash flow information: | |||||||||||

| ROU assets obtained in exchange for lease obligations | $ | $ | |||||||||

See accompanying notes.

Insperity | 2022 First Quarter Form 10-Q | 9 | ||||

| FINANCIAL STATEMENTS (Unaudited) | ||

CONSOLIDATED STATEMENTS OF STOCKHOLDERS’ EQUITY

For the Three Months Ended March 31, 2022 and 2021

| Common Stock Issued | Additional Paid-In Capital | Treasury Stock | Retained Earnings and AOCI | Total | ||||||||||||||||

| (in thousands) | Shares | Amount | ||||||||||||||||||

| Balance at December 31, 2021 | 55,489 | $ | 555 | $ | 109,179 | $ | (665,089) | $ | 553,581 | $ | (1,774) | |||||||||

| Purchase of treasury stock, at cost | — | — | — | (27,441) | — | (27,441) | ||||||||||||||

| Issuance of equity-based incentive awards and dividend equivalents | — | — | (9,214) | 10,365 | (1,151) | — | ||||||||||||||

| Stock-based compensation expense | — | — | 9,575 | 271 | — | 9,846 | ||||||||||||||

| Other | — | — | 513 | 269 | — | 782 | ||||||||||||||

| Dividends paid | — | — | — | — | (17,244) | (17,244) | ||||||||||||||

| Unrealized loss on marketable securities, net of tax | — | — | — | — | (92) | (92) | ||||||||||||||

| Net income | — | — | — | — | 69,884 | 69,884 | ||||||||||||||

| Balance at March 31, 2022 | 55,489 | $ | 555 | $ | 110,053 | $ | (681,625) | $ | 604,978 | $ | 33,961 | |||||||||

| Balance at December 31, 2020 | 55,489 | $ | 555 | $ | 95,528 | $ | (626,984) | $ | 575,033 | $ | 44,132 | |||||||||

| Purchase of treasury stock, at cost | — | — | — | (29,686) | — | (29,686) | ||||||||||||||

| Issuance of equity-based incentive awards and dividend equivalents | — | — | (25,085) | 26,421 | (1,336) | — | ||||||||||||||

| Stock-based compensation expense | — | — | 10,851 | 971 | — | 11,822 | ||||||||||||||

| Exercise of stock options | — | — | (329) | 569 | — | 240 | ||||||||||||||

| Other | — | — | 364 | 318 | — | 682 | ||||||||||||||

| Dividends paid | — | — | — | — | (15,461) | (15,461) | ||||||||||||||

| Unrealized loss on marketable securities, net of tax | — | — | — | — | (7) | (7) | ||||||||||||||

| Net income | — | — | — | — | 61,922 | 61,922 | ||||||||||||||

| Balance at March 31, 2021 | 55,489 | $ | 555 | $ | 81,329 | $ | (628,391) | $ | 620,151 | $ | 73,644 | |||||||||

Insperity | 2022 First Quarter Form 10-Q | 10 | ||||

| NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Unaudited) | ||

| 1. | Basis of Presentation | ||||

Insperity, Inc., a Delaware corporation (“Insperity,” “we,” “our,” and “us”), provides an array of human resources (“HR”) and business solutions designed to help improve business performance. Our most comprehensive HR services offerings are provided through our professional employer organization (“PEO”) services, known as Workforce Optimization® and Workforce SynchronizationTM solutions (together, our “PEO HR Outsourcing solutions”), which we provide by entering into a co-employment relationship with our clients. Our PEO HR Outsourcing solutions encompass a broad range of HR functions, including payroll and employment administration, employee benefits, workers’ compensation, government compliance, performance management, and training and development services, along with our cloud-based human capital management solution, the Insperity PremierTM platform.

In addition to our PEO HR Outsourcing solutions, we offer a comprehensive traditional payroll and human capital management solution, known as our Workforce AccelerationTM solution. We also offer a number of other business performance solutions, including Performance Management, Organizational Planning, Recruiting Services, Employment Screening, Retirement Services, and Insurance Services, many of which are offered as a cloud-based software solution. These other products or services are offered separately or with our other solutions.

The Consolidated Financial Statements include the accounts of Insperity, Inc. and its wholly owned subsidiaries. Intercompany accounts and transactions have been eliminated in consolidation.

The preparation of financial statements in conformity with accounting principles generally accepted in the United States (“GAAP”) requires management to make estimates and assumptions that affect the amounts reported in the financial statements and accompanying notes. Actual results could differ from those estimates.

The accompanying Consolidated Financial Statements should be read in conjunction with our audited Consolidated Financial Statements at and for the year ended December 31, 2021. Our Condensed Consolidated Balance Sheet at December 31, 2021 has been derived from the audited financial statements at that date, but does not include all of the information or footnotes required by GAAP for complete financial statements. Our Condensed Consolidated Balance Sheet at March 31, 2022 and our Consolidated Statements of Operations for the three month periods ended March 31, 2022 and 2021, our Consolidated Statements of Cash Flows for the three month periods ended March 31, 2022 and 2021 and our Consolidated Statements of Stockholders’ Equity for the three month periods ended March 31, 2022 and 2021, have been prepared by us without audit. In the opinion of management, all adjustments necessary to present fairly the consolidated financial position, results of operations and cash flows have been made, and all such adjustments are of a normal recurring nature. Certain prior year amounts have been reclassified to conform to the 2022 presentation.

The results of operations for the interim periods are not necessarily indicative of the operating results for a full year or of future operations.

| 2. | Accounting Policies | ||||

Health Insurance Costs

We provide group health insurance coverage to our WSEEs in our PEO HR Outsourcing solutions through a national network of carriers, including UnitedHealthcare (“United”), UnitedHealthcare of California, Kaiser Permanente, Blue Shield of California, HMSA BlueCross BlueShield of Hawaii, and Tufts, all of which provide fully insured policies or service contracts.

The policy with United provides approximately 87 % of our participants’ health insurance coverage. While the policy with United is a fully-insured plan, as a result of certain contractual terms, we have accounted for this plan since its inception using a partially self-funded insurance accounting model. Effective January 1, 2020, under the amended agreement with United, we no longer have financial responsibilities for a participant’s annual claim costs that exceed $1 million. Accordingly, we record the costs of the United plan, including an estimate of the incurred claims, taxes and administrative fees (collectively the “Plan Costs”), as benefits expense, which is a component of direct costs, in our Consolidated Statements of Operations. The estimated incurred claims are based upon: (1) the level of claims processed during the quarter; (2) estimated completion rates based upon recent claim development patterns under

Insperity | 2022 First Quarter Form 10-Q | 11 | ||||

| NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Unaudited) | ||

the plan; and (3) the number of participants in the plan, including both active and COBRA enrollees. Each reporting period, changes in the estimated ultimate costs resulting from claim trends, plan design and migration, participant demographics, and other factors are incorporated into the benefits costs, which requires a significant level of judgment.

Additionally, since the plan’s inception, under the terms of the contract, United establishes cash funding rates 90 days in advance of the beginning of a reporting quarter. If the Plan Costs for a reporting quarter are greater than the premiums paid and owed to United, a deficit in the plan would be incurred and a liability for the excess costs would be accrued in our Condensed Consolidated Balance Sheets. On the other hand, if the Plan Costs for the reporting quarter are less than the premiums paid and owed to United, a surplus in the plan would be incurred and we would record an asset for the excess premiums in our Condensed Consolidated Balance Sheets. The terms of the arrangement require us to maintain an accumulated cash surplus in the plan of $9.0 million, which is reported as long-term prepaid insurance. In addition, United requires a deposit equal to approximately one day of claims funding activity, which was $6.5 million at March 31, 2022, and is included in deposits - health insurance as a long-term asset on our Condensed Consolidated Balance Sheets. As of March 31, 2022, Plan Costs were less than the net premiums paid and owed to United by $13.3 million. As this amount is in excess of the agreed-upon $9.0 million surplus maintenance level, the $4.3 million difference is included in prepaid insurance, a current asset, in our Condensed Consolidated Balance Sheets. The premiums, including the additional quarterly premiums, owed to United at March 31, 2022 were $55.0 million, which is included in accrued health insurance costs, a current liability in our Condensed Consolidated Balance Sheets. Our benefits costs incurred in the first three months of 2022 included an increase of $0.8 million for changes in estimated run-off related to prior periods. Our benefits costs incurred in the first three months of 2021 included an increase of $5.5 million for changes in estimated run-off related to prior periods.

Workers’ Compensation Costs

Our workers’ compensation coverage for our WSEEs in our PEO HR Outsourcing solutions is provided through an arrangement with the Chubb Group of Insurance Companies or its predecessors (the “Chubb Program”). The Chubb Program is fully insured in that Chubb has the responsibility to pay all claims incurred under the policy regardless of whether we satisfy our responsibilities. Under the Chubb Program for claims incurred on or before September 30, 2019, we have financial responsibility to Chubb for the first $1 million layer of claims per occurrence and, for claims over $1 million, up to a maximum aggregate amount of $6 million per policy year for claims that exceed $1 million. Chubb bears the financial responsibility for all claims in excess of these levels. Effective for claims incurred on or after October 1, 2019, we have financial responsibility to Chubb for the first $1.5 million layer of claims per occurrence and, for claims over $1.5 million, up to a maximum aggregate amount of $6 million per policy year for claims that exceed $1.5 million.

Because we bear the financial responsibility for claims up to the levels noted above, such claims, which are the primary component of our workers’ compensation costs, are recorded in the period incurred. Workers’ compensation insurance includes ongoing health care and indemnity coverage whereby claims are paid over numerous years following the date of injury. Accordingly, the accrual of related incurred costs in each reporting period includes estimates, which take into account the ongoing development of claims and therefore requires a significant level of judgment.

We utilize a third-party actuary to estimate our loss development rate, which is primarily based upon the nature of WSEEs’ job responsibilities, the location of WSEEs, the historical frequency and severity of workers’ compensation claims, and an estimate of future cost trends. Each reporting period, changes in the actuarial assumptions resulting from changes in actual claims experience and other trends are incorporated into our workers’ compensation claims cost estimates. During the three months ended March 31, 2022 and 2021, we reduced accrued workers’ compensation costs by $14.9 million and $13.2 million, respectively, for changes in estimated losses related to prior reporting periods. Workers’ compensation cost estimates are discounted to present value at a rate based upon the U.S. Treasury rates that correspond with the weighted average estimated claim payout period (the average discount rate utilized in the 2022 period was 1.5 % and in the 2021 period was 0.5 %) and are accreted over the estimated claim payment period and included as a component of direct costs in our Consolidated Statements of Operations.

Insperity | 2022 First Quarter Form 10-Q | 12 | ||||

| NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Unaudited) | ||

The following table provides the activity and balances related to incurred but not paid workers’ compensation claims:

| Three Months Ended March 31, | |||||||||||

| (in thousands) | 2022 | 2021 | |||||||||

| Beginning balance, January 1, | $ | $ | |||||||||

| Accrued claims | |||||||||||

| Present value discount, net of accretion | ( | ( | |||||||||

| Paid claims | ( | ( | |||||||||

| Ending balance | $ | $ | |||||||||

| Current portion of accrued claims | $ | $ | |||||||||

| Long-term portion of accrued claims | |||||||||||

| Total accrued claims | $ | $ | |||||||||

The current portion of accrued workers’ compensation costs on our Condensed Consolidated Balance Sheets at March 31, 2022 includes $3.9 million of workers’ compensation administrative fees.

As of March 31, 2022 and 2021, the undiscounted accrued workers’ compensation costs were $248.0 million and $253.2 million, respectively.

At the beginning of each policy period, the workers’ compensation insurance carrier establishes monthly funding requirements comprised of premium costs and funds to be set aside for payment of future claims (“claim funds”). The level of claim funds is primarily based upon anticipated WSEE payroll levels and expected workers’ compensation loss rates, as determined by the insurance carrier. Monies funded into the program for incurred claims expected to be paid within one year are recorded as restricted cash, a short-term asset, while the remainder of claim funds are included in deposits – workers’ compensation, a long-term asset in our Condensed Consolidated Balance Sheets. At March 31, 2022, we had restricted cash of $49.4 million and deposits – workers’ compensation of $190.8 million.

Our estimate of incurred claim costs expected to be paid within one year is included in short-term liabilities, while our estimate of incurred claim costs expected to be paid beyond one year is included in long-term liabilities on our Condensed Consolidated Balance Sheets.

Revenue and Direct Cost Recognition

We enter into contracts with our customers for human resources services based on a stated rate and price in the contract. Our contracts generally establish pricing for a period of 12 months, and are generally cancellable at any time by either party with 30-days’ notice. Our performance obligations are satisfied as services are rendered each month. The term between invoicing and when our performance obligations are satisfied is not significant. Payment terms are typically due concurrently with the invoicing of our PEO services. We do not have significant financing components or significant payment terms.

Our revenue is generally recognized ratably over the payroll period as WSEEs perform their service at the client worksite. Customers are invoiced concurrently with each periodic payroll of its WSEEs. Revenues that have been recognized but unbilled of $655.3 million and $490.5 million at March 31, 2022 and December 31, 2021, respectively, are included in accounts receivable, net on our Condensed Consolidated Balance Sheets.

Pursuant to the “practical expedients” provided under Accounting Standards Update No 2014-09, we expense sales commissions when incurred because the terms of our contracts generally are cancellable by either party with a 30-day notice. These costs are recorded in commissions in our Consolidated Statements of Operations.

Insperity | 2022 First Quarter Form 10-Q | 13 | ||||

| NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Unaudited) | ||

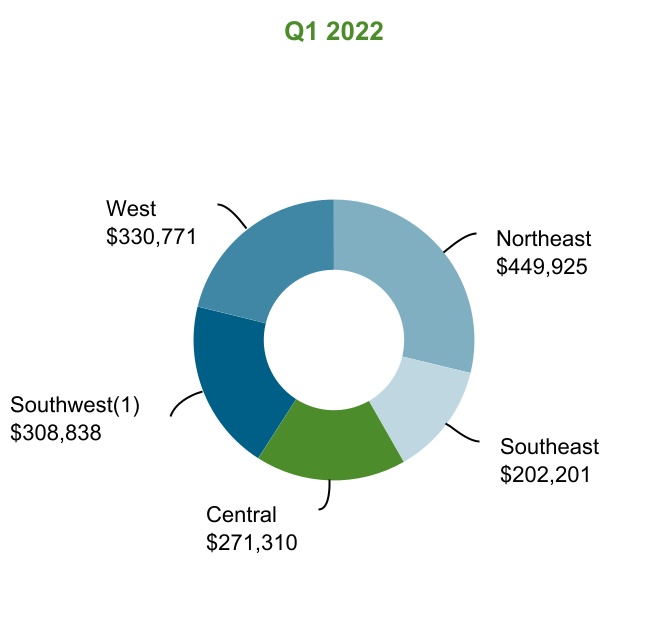

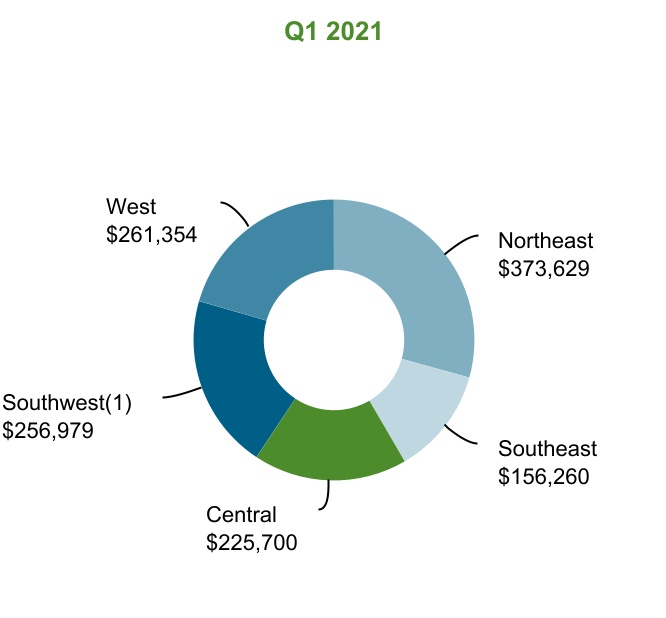

Our revenue for our PEO HR Outsourcing solutions by geographic region and for our other products and services offerings are as follows:

| Three Months Ended March 31, | |||||||||||

| (in thousands) | 2022 | 2021 | % Change | ||||||||

| Northeast | $ | $ | 20.4 | % | |||||||

| Southeast | 29.4 | % | |||||||||

| Central | 20.2 | % | |||||||||

| Southwest | 20.2 | % | |||||||||

| West | 26.6 | % | |||||||||

| 1,563,045 | 1,273,922 | 22.7 | % | ||||||||

| Other revenue | 14.6 | % | |||||||||

| Total revenue | $ | $ | 22.6 | % | |||||||

| 3. | Cash, Cash Equivalents and Marketable Securities | ||||

The following table summarizes our cash and investments in cash equivalents and marketable securities held by investment managers and overnight investments:

| March 31, 2022 | December 31, 2021 | ||||||||||||||||||||||

| (in thousands) | Cash & Cash Equivalents | Marketable Securities | Total | Cash & Cash Equivalents | Marketable Securities | Total | |||||||||||||||||

| Overnight holdings | $ | $ | $ | $ | $ | $ | |||||||||||||||||

| Investment holdings | |||||||||||||||||||||||

| Cash in demand accounts | |||||||||||||||||||||||

| Outstanding checks | ( | ( | ( | ( | |||||||||||||||||||

| Total | $ | $ | $ | $ | $ | $ | |||||||||||||||||

Our cash and overnight holdings fluctuate based on the timing of clients’ payroll processing cycles. Our cash, cash equivalents and marketable securities at March 31, 2022 and December 31, 2021 included $338.3 million and $424.8 million, respectively, of funds associated with federal and state income tax withholdings, employment taxes, and other payroll deductions, as well as $117.8 million and $20.1 million, respectively, in client prepayments.

| 4. | Fair Value Measurements | ||||

We account for our financial assets in accordance with Accounting Standard Codification 820, Fair Value Measurement. This standard defines fair value, establishes a framework for measuring fair value and expands disclosures about fair value measurements. The fair value measurement disclosures are grouped into three levels based on valuation factors:

•Level 1 - quoted prices in active markets using identical assets

•Level 2 - significant other observable inputs, such as quoted prices for similar assets or liabilities, quoted prices in markets that are not active, or other observable inputs

•Level 3 - significant unobservable inputs

Insperity | 2022 First Quarter Form 10-Q | 14 | ||||

| NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Unaudited) | ||

Fair Value of Instruments Measured and Recognized at Fair Value

The following table summarizes the levels of fair value measurements of our financial assets:

| March 31, 2022 | December 31, 2021 | ||||||||||||||||||||||

| (in thousands) | Total | Level 1 | Level 2 | Total | Level 1 | Level 2 | |||||||||||||||||

| Money market funds | $ | $ | $ | $ | $ | $ | |||||||||||||||||

| U.S. Treasury bills | |||||||||||||||||||||||

| Municipal bonds | |||||||||||||||||||||||

| Total | $ | $ | $ | $ | $ | $ | |||||||||||||||||

The municipal bond securities valued as Level 2 are primarily pre-refunded municipal bonds that are secured by escrow funds containing U.S. government securities. Our valuation techniques used to measure fair value for these securities during the period consisted primarily of third-party pricing services that utilized actual market data such as trades of comparable bond issues, broker/dealer quotations for the same or similar investments in active markets and other observable inputs.

The following is a summary of our available-for-sale marketable securities:

| (in thousands) | Amortized Cost | Gross Unrealized Gains | Gross Unrealized Losses | Estimated Fair Value | ||||||||||

| March 31, 2022 | ||||||||||||||

| U.S. Treasury bills | $ | $ | $ | ( | $ | |||||||||

| Municipal bonds | ( | |||||||||||||

| December 31, 2021 | ||||||||||||||

| U.S. Treasury bills | $ | $ | $ | ( | $ | |||||||||

| Municipal bonds | ( | |||||||||||||

Fair Value of Other Financial Instruments

The carrying amounts of cash, cash equivalents, restricted cash, accounts receivable, deposits and accounts payable approximate their fair values due to the short-term maturities of these instruments.

As of March 31, 2022, the carrying value of borrowings under our revolving credit facility approximates fair value and was classified as Level 2 in the fair value hierarchy. Please read Note 5, “Long-Term Debt,” for additional information.

| 5. | Long-Term Debt | ||||

We have a revolving credit facility (the “Facility”) with borrowing capacity of up to $500 million. The Facility may be further increased to $550 million based on the terms and subject to the conditions set forth in the agreement relating to the Facility (as amended, the “Credit Agreement”). The Facility is available for working capital and general corporate purposes, including acquisitions, stock repurchases and issuances of letters of credit. Our obligations under the Facility are secured by 65 % of the stock of our captive insurance subsidiary and are guaranteed by all of our domestic subsidiaries other than certain excluded subsidiaries. At March 31, 2022, our outstanding balance on the Facility was $369.4 million, and we had an outstanding $1.0 million letter of credit issued under the Facility, resulting in an available borrowing capacity of $129.6 million.

Insperity | 2022 First Quarter Form 10-Q | 15 | ||||

| NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Unaudited) | ||

The Facility matures on September 13, 2024. Borrowings under the Facility bear interest at an annual rate equal to an alternate base rate or LIBOR, at our option, plus an applicable margin. Depending on our leverage ratio, the applicable margin varies (1) in the case of LIBOR loans, from 1.50 % to 2.25 % and (2) in the case of alternate base rate loans, from 0.00 % to 0.50 %. The alternate base rate is the highest of (1) the prime rate most recently published in The Wall Street Journal, (2) the federal funds rate plus 0.50 % and (3) the 30-day LIBOR rate plus 2.00 %. We also pay an unused commitment fee on the average daily unused portion of the Facility at a rate of 0.25 % per year. The average interest rate for the three month period ended March 31, 2022 was 1.9 %. Interest expense and unused commitment fees are recorded in other income (expense). Following early opt-in by us or our lenders or such other time as LIBOR rates have permanently or indefinitely ceased to be published by the regulatory supervisory authority of LIBOR, then LIBOR will be replaced by a rate per annum equal to the secured overnight financing rate published by the Federal Reserve Bank of New York or such other benchmark as determined in accordance with the Credit Agreement.

The Facility contains both affirmative and negative covenants that we believe are customary for arrangements of this nature. Covenants include, but are not limited to, limitations on our ability to incur additional indebtedness, sell material assets, retire, redeem or otherwise reacquire our capital stock, acquire the capital stock or assets of another business, make investments and pay dividends. In addition, the Credit Agreement requires us to comply with financial covenants limiting our total funded debt, minimum interest coverage ratio, and maximum leverage ratio. We were in compliance with all financial covenants under the Credit Agreement at March 31, 2022.

| 6. | Stockholders' Equity | ||||

During the first three months of 2022, we repurchased or withheld an aggregate of 308,057 shares of our common stock, as described below.

Repurchase Program

Our Board of Directors (the “Board”) has authorized a program to repurchase shares of our outstanding common stock (“Repurchase Program”). The purchases may be made from time to time in the open market or directly from stockholders at prevailing market prices based on market conditions and other factors. During the three months ended March 31, 2022, 209,841 shares were repurchased under the Repurchase Program. As of March 31, 2022, we were authorized to repurchase an additional 1,493,787 shares under the Repurchase Program.

Withheld Shares

During the three months ended March 31, 2022, we withheld 98,216 shares to satisfy tax withholding obligations for the vesting of long-term incentive and restricted stock awards.

Dividends

The Board declared quarterly dividends as follows:

| (amounts per share) | 2022 | 2021 | |||||||||

| First quarter | $ | $ | |||||||||

During the three months ended March 31, 2022 and 2021, we paid dividends totaling $17.2 million and $15.5 million, respectively.

Insperity | 2022 First Quarter Form 10-Q | 16 | ||||

| NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Unaudited) | ||

| 7. | Net Income Per Share | ||||

We utilize the two-class method to compute net income per share. The two-class method allocates a portion of net income to participating securities, which includes unvested awards of share-based payments with non-forfeitable rights to receive dividends. Net income allocated to unvested share-based payments is excluded from net income allocated to common shares. Any undistributed losses resulting from dividends exceeding net income are not allocated to participating securities. Basic net income per share is computed by dividing net income allocated to common shares by the weighted average number of common shares outstanding during the period. Diluted net income per share is computed by dividing net income allocated to common shares by the weighted average number of common shares outstanding during the period, plus the dilutive effect of time-vested and performance-based restricted stock units (“RSUs”).

The following table summarizes the net income allocated to common shares and the basic and diluted shares used in the net income per share computations:

| Three Months Ended March 31, | ||||||||

| (in thousands) | 2022 | 2021 | ||||||

| Net income | $ | $ | ||||||

Less distributed and undistributed earnings allocated to participating securities | ( | ( | ||||||

Net income allocated to common shares | $ | $ | ||||||

| Weighted average common shares outstanding | ||||||||

| Incremental shares from assumed time-vested and performance-based RSU awards | ||||||||

| Adjusted weighted average common shares outstanding | ||||||||

| Potentially dilutive securities not included in weighted average share calculation due to anti-dilutive effect | ||||||||

| 8. | Commitments and Contingencies | ||||

Securities Class Action Lawsuit

In July 2020, a federal securities class action was filed against us and certain of our officers in the United States District Court for the Southern District of New York. The name of the case is Building Trades Pension Fund of Western Pennsylvania v. Insperity, Inc. et al., Case No. 1:20-cv-05635-NRB. On October 23, 2020, the court issued an order appointing Oakland County Employees’ Retirement System and Oakland County Voluntary Employees’ Beneficiary Association Trust as lead plaintiff (“Lead Plaintiff”). On December 22, 2020, the Lead Plaintiff filed its consolidated complaint alleging that we made materially false and misleading statements regarding our business and operations in violation of the federal securities laws and seeking unspecified damages, attorneys’ fees, costs, equitable/injunctive relief, and such other relief that may be deemed proper. On April 26, 2021, the defendants moved to dismiss the consolidated complaint with prejudice. The Lead Plaintiff filed its opposition to the motion to dismiss on June 10, 2021, and the defendants filed their reply in support of the motion to dismiss on July 12, 2021. On March 15, 2022, the court granted the defendants’ motion to dismiss with prejudice and the deadline to appeal has passed.

Other Litigation

We are a defendant in various other lawsuits and claims arising in the normal course of business. Management believes it has valid defenses in these cases and is defending them vigorously. While the results of litigation cannot be predicted with certainty, management believes the final outcome of such litigation will not have a material adverse effect on our financial position or results of operations.

Insperity | 2022 First Quarter Form 10-Q | 17 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | ||

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

You should read the following discussion in conjunction with our Annual Report on Form 10-K for the year ended December 31, 2021, as well as our Consolidated Financial Statements and notes thereto included in this Quarterly Report on Form 10-Q.

Executive Summary

Overview

Insperity, Inc. (“Insperity,” “we,” “our,” and “us”) provides an array of human resources (“HR”) and business solutions designed to help improve business performance. Our most comprehensive HR services offerings are provided through our professional employer organization (“PEO”) services, known as Workforce Optimization® and Workforce SynchronizationTM solutions (together, our “PEO HR Outsourcing solutions”), which we provide by entering into a co-employment relationship with our clients. Our PEO HR Outsourcing solutions encompass a broad range of HR functions, including payroll and employment administration, employee benefits, workers’ compensation, government compliance, performance management, and training and development services, along with our cloud-based human capital management solution, the Insperity PremierTM platform.

COVID-19 Pandemic

The effects of the COVID-19 pandemic, including actions taken by businesses and governments, have resulted in significant changes in U.S. economic activity and to the workplace in general. While uncertainties continue regarding the pandemic, including its duration, future variants, and its longer-term impacts, we believe that we are positioned to continue to adjust our business plans and workforce practices as conditions change. In response to the pandemic’s impact on the workplace, we implemented flexible remote working arrangements for our employees. To serve our clients, we have instituted a number of service offerings and developed COVID-19 resources to assist clients with obtaining government provided tax credits, tax deferrals, loans and loan forgiveness and to provide guidance to assist clients with addressing the challenges faced by employers as a result of the pandemic. These service offerings and guidance to assist clients with the impacts of the pandemic include additional benefits support; remote workforce transition; monitoring and educating on regulatory changes, including vaccine mandates; return to the workplace; and workplace safety.

In the first quarter of 2022 (“Q1 2022”), the average number of WSEEs paid per month increased 19.5% year-over-year as the Q1 2022 increase in WSEEs paid at existing clients combined with WSEEs paid from new sales and client retention all exceeded the first quarter of 2021 (“Q1 2021”) levels. We expect the average number of paid WSEEs per month to increase between 18% and 19% in the second quarter of 2022 as compared to the second quarter of 2021, which, if achieved, would equate to the average number of paid WSEEs per month growing 3% to 4% sequentially from the first quarter of 2022.

We experienced a 7.4% increase in the year-over-year benefits costs per covered employee during Q1 2022 as compared to Q1 2021. During Q1 2021, we experienced a 1.8% increase in the year-over-year benefits costs per covered employee as compared to Q1 2020. During 2022 and possibly beyond 2022, benefits costs are expected to continue to be affected by the dynamics of the pandemic, including the impact on healthcare utilization and incremental COVID-19 testing, vaccination and treatment costs. This may result in a higher level of healthcare claims costs than our historical claim cost trends. While we have experienced a reduced frequency in workers’ compensation claims during the COVID-19 pandemic, the COVID-19 pandemic has not had a material impact on our workers’ compensation cost estimate; however, the ultimate impact of COVID-19 on our workers’ compensation program remains uncertain.

The extent to which our future results are affected by the COVID-19 pandemic will depend on various factors and consequences beyond our control, such as the scope, duration and magnitude of the pandemic, impacts of changes in or variants of the COVID-19 virus, actions by businesses and governments in response to the pandemic, including programs designed to assist small and medium-sized businesses with the economic impact of the pandemic; and the speed and effectiveness of responses to combat the virus, including the development, availability and acceptance of therapeutics and vaccines. See Item 1A. “Risk Factors” included in Part I of our Annual Report on Form 10-K for teh year ended December 31, 2021.

Insperity | 2022 First Quarter Form 10-Q | 18 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | ||

2022 Highlights

First Quarter 2022 Compared to First Quarter 2021

•Average number of WSEEs paid per month increased 19.5%

•Net income and diluted earnings per share (“diluted EPS”) increased 12.9% and 13.2% to $69.9 million and $1.80, respectively

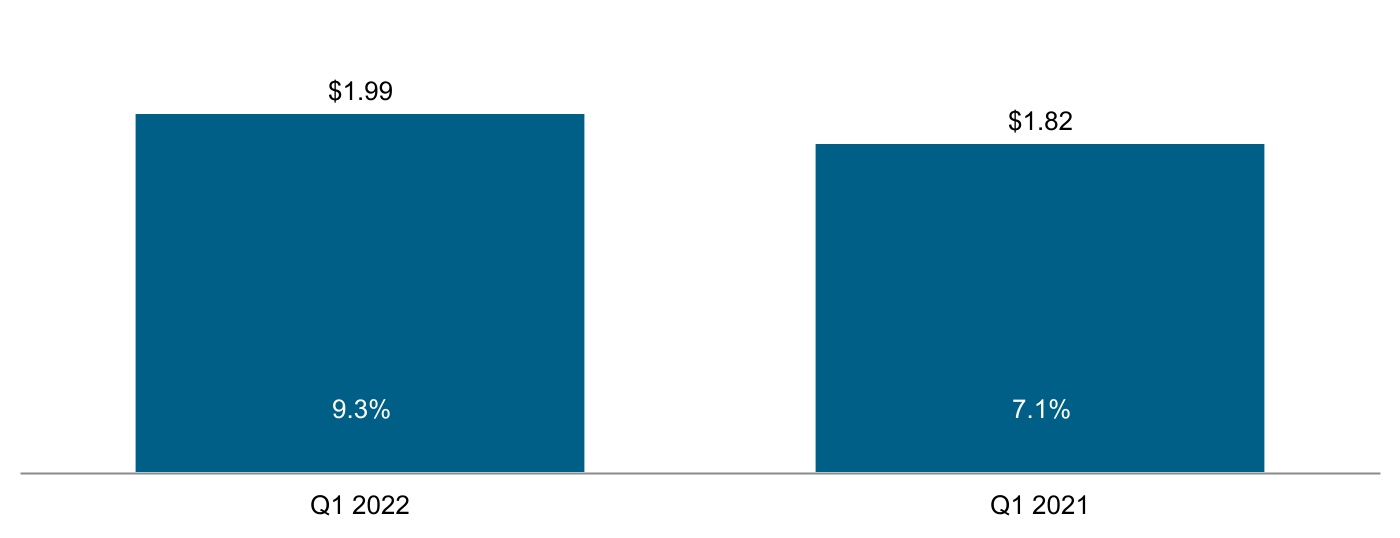

•Adjusted EPS increased 9.3% to $1.99

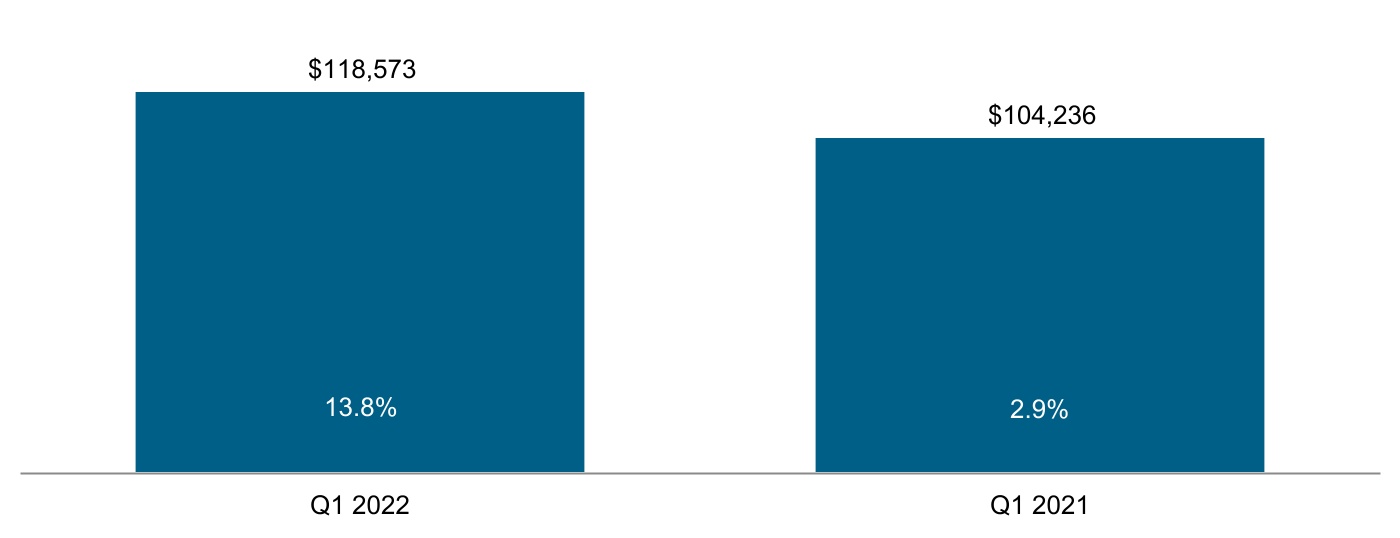

•Adjusted EBITDA increased 13.8% to $118.6 million

Key Financial and Statistical Data

(in thousands, except per share, WSEE and statistical data) | Three Months Ended March 31, | ||||||||||

| 2022 | 2021 | % Change | |||||||||

Financial data: | |||||||||||

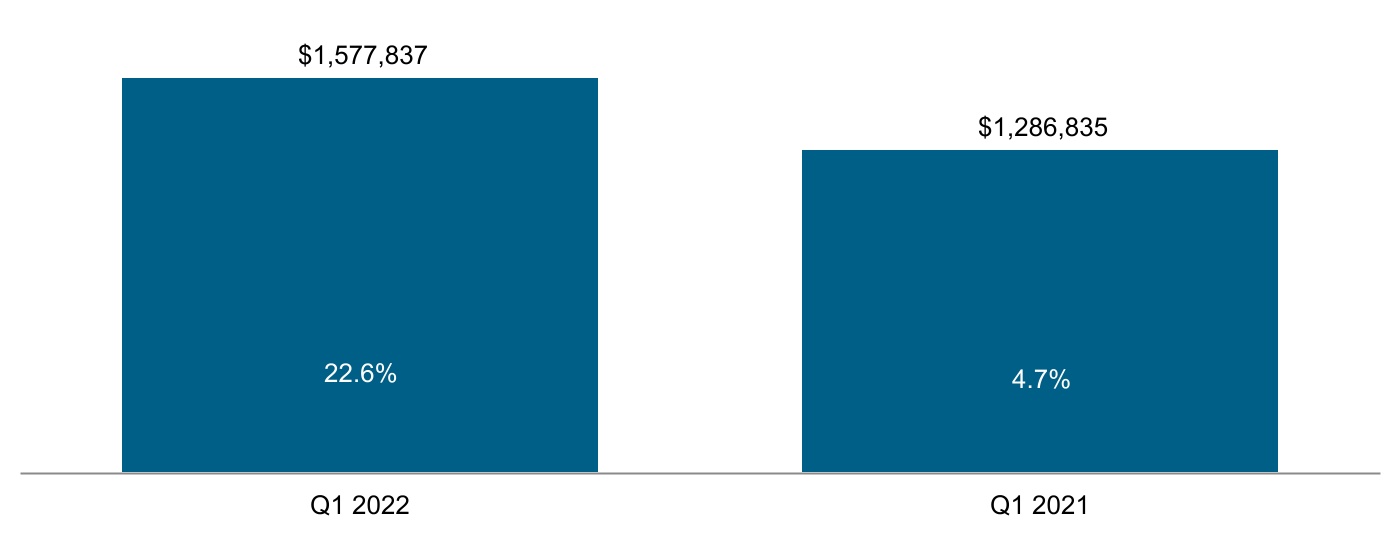

Revenues | $ | 1,577,837 | $ | 1,286,835 | 22.6 | % | |||||

| Gross profit | 285,774 | 251,445 | 13.7 | % | |||||||

| Operating expenses | 187,379 | 167,621 | 11.8 | % | |||||||

| Operating income | 98,395 | 83,824 | 17.4 | % | |||||||

| Other expense | (1,777) | (1,056) | 68.3 | % | |||||||

| Net income | 69,884 | 61,922 | 12.9 | % | |||||||

Diluted EPS | 1.80 | 1.59 | 13.2 | % | |||||||

Non-GAAP financial measures(1): | |||||||||||

| Adjusted net income | $ | 77,006 | $ | 70,766 | 8.8 | % | |||||

| Adjusted EBITDA | 118,573 | 104,236 | 13.8 | % | |||||||

Adjusted EPS | 1.99 | 1.82 | 9.3 | % | |||||||

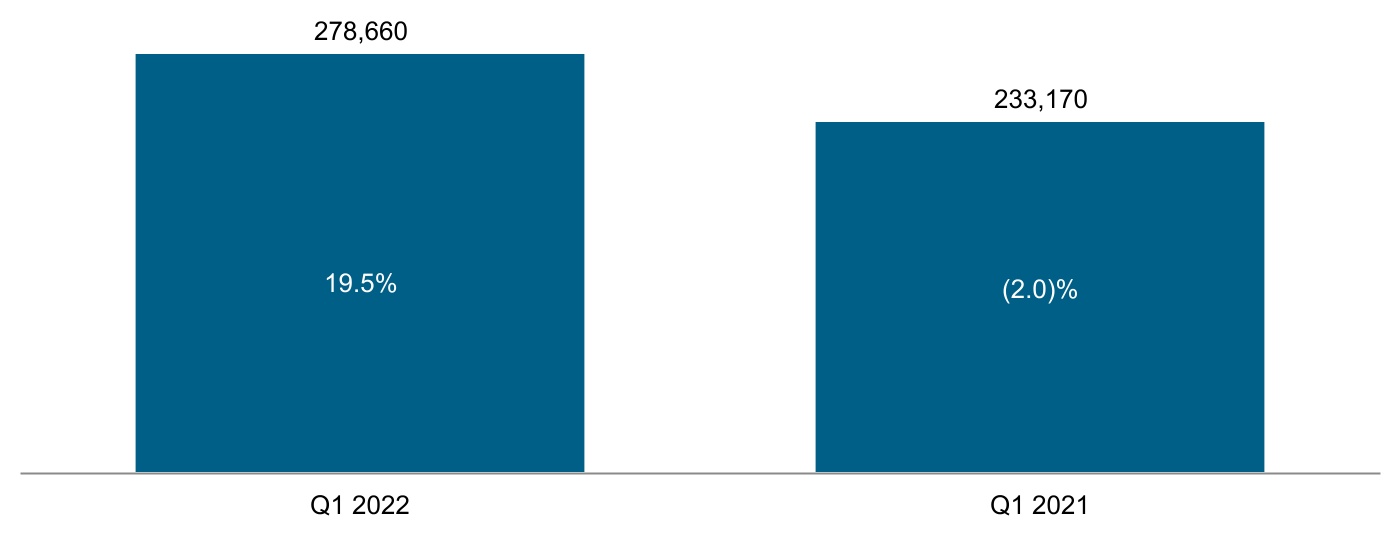

| Average WSEEs paid | 278,660 | 233,170 | 19.5 | % | |||||||

Statistical data (per WSEE per month): | |||||||||||

Revenues(2) | $ | 1,887 | $ | 1,840 | 2.6 | % | |||||

| Gross profit | 342 | 359 | (4.7) | % | |||||||

Operating expenses | 224 | 240 | (6.7) | % | |||||||

Operating income | 118 | 120 | (1.7) | % | |||||||

| Net income | 84 | 89 | (5.6) | % | |||||||

____________________________________

(1)Please read “Non-GAAP Financial Measures” for a reconciliation of the non-GAAP financial measures to their most directly comparable financial measures calculated and presented in accordance with GAAP.

(2)Revenues per WSEE per month are comprised of gross billings per WSEE per month less WSEE payroll costs per WSEE per month as follows:

| Three Months Ended March 31, | ||||||||

| (per WSEE per month) | 2022 | 2021 | ||||||

| Gross billings | $ | 12,390 | $ | 11,509 | ||||

| Less: WSEE payroll cost | 10,503 | 9,669 | ||||||

| Revenues | $ | 1,887 | $ | 1,840 | ||||

Insperity | 2022 First Quarter Form 10-Q | 19 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | ||

Results of Operations

Key Operating Metrics

We monitor certain key metrics to measure our performance, including:

•WSEEs

•Adjusted EBITDA

•Adjusted EPS

Our growth in the number of WSEEs paid is affected by three primary sources: new client sales, client retention and the net change in WSEEs paid at existing clients through new hires and layoffs.

•During Q1 2022, WSEEs paid increased 19.5% compared to Q1 2021. The number of WSEEs paid from new client sales, the net gain (loss) in our client base and client retention all improved compared to Q1 2021.

Average WSEEs Paid and

Year-over-Year Growth Percentage

Insperity | 2022 First Quarter Form 10-Q | 20 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | ||

Adjusted EBITDA and Year-over-Year Growth Percentage (in thousands) | |||||

Adjusted EPS and Year-over-Year Growth Percentage (amounts per share) | |||||

Revenues

Our PEO HR Outsourcing solutions revenues are primarily derived from our gross billings, which are based on (1) the payroll cost of our WSEEs and (2) a monthly markup component.

Our revenues are primarily dependent on the number of clients enrolled, the resulting number of WSEEs paid each period and the number of WSEEs enrolled in our benefit plans. Because our monthly markup is computed in part as a percentage of payroll cost, certain revenues are also affected by the payroll cost of WSEEs, which may fluctuate based on the composition of the WSEE base, inflationary effects on wage levels and differences in the local economies of our markets.

Insperity | 2022 First Quarter Form 10-Q | 21 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | ||

Revenue and

Year-over-Year Growth Percentage

(in thousands)

First Quarter 2022 Compared to First Quarter 2021

Our revenues for Q1 2022 were $1.6 billion, an increase of 22.6%, primarily due to the following:

•Average WSEEs paid increased 19.5%.

•Revenues per WSEE per month increased 2.6%, or $47.

We provide our PEO HR Outsourcing solutions to small and medium-sized businesses throughout the United States. Our PEO HR Outsourcing solutions revenue distribution by region follows:

PEO HR Outsourcing Solutions Revenue by Region

(in thousands)

________________________________________________________

(1)The Southwest region includes Texas.

Insperity | 2022 First Quarter Form 10-Q | 22 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | ||

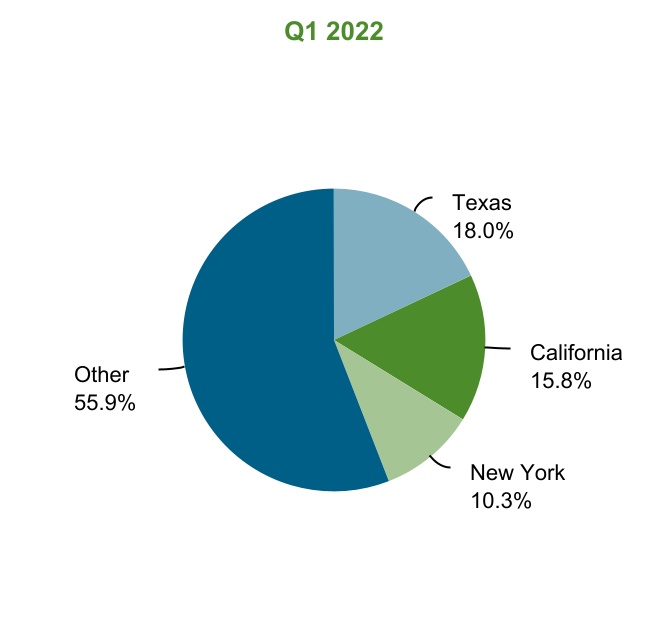

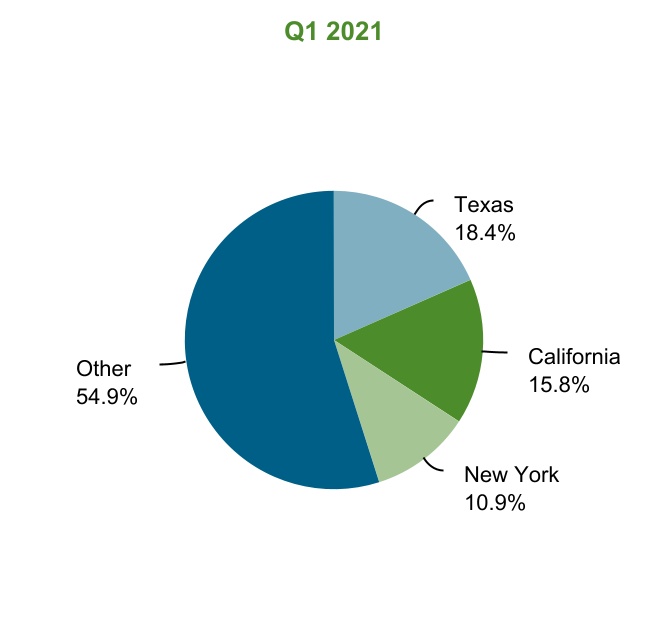

The percentage of total PEO HR Outsourcing solutions revenue in our significant markets includes the following:

Significant Markets

We believe the middle market sector, which we generally define as those companies with employees ranging from approximately 150 to 5,000 WSEEs, has historically been under-served by the PEO industry. Currently, we have a dedicated sales management, service personnel, and consulting staff who concentrate solely on the middle market sector. Our average number of WSEEs per month in our middle market sector increased 23.1% during Q1 2022 compared to Q1 2021, representing approximately 24.0% and 23.3% of our total average paid WSEEs during Q1 2022 and Q1 2021, respectively.

Gross Profit

In determining the pricing of the markup component of our gross billings, we take into consideration our estimates of the costs directly associated with our WSEEs, including payroll taxes, benefits and workers’ compensation costs, plus an acceptable gross profit margin. As a result, our operating results are significantly impacted by our ability to accurately estimate, control and manage our direct costs relative to the revenues derived from the markup component of our gross billings.

Our gross profit per WSEE is primarily determined by our ability to accurately estimate and control direct costs and our ability to incorporate changes in these costs into the gross billings charged to PEO HR Outsourcing solutions clients, which are subject to pricing arrangements that are typically renewed annually. We use gross profit per WSEE per month as our principal measurement of relative performance at the gross profit level.

Insperity | 2022 First Quarter Form 10-Q | 23 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | ||

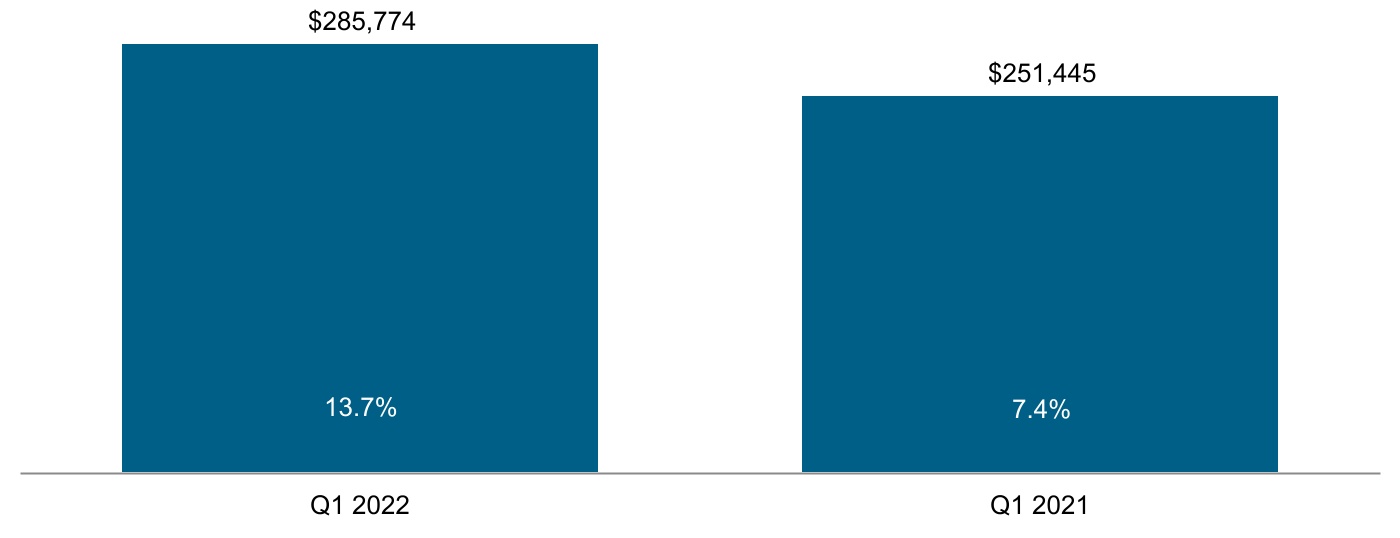

Gross Profit and Year-over-Year Growth Percentage (in thousands) | |||||

| Gross Profit per WSEE per Month and Year-over-Year Growth Percentage | |||||

First Quarter 2022 Compared to First Quarter 2021

Gross profit for Q1 2022 increased 13.7% to $285.8 million compared to $251.4 million in Q1 2021. Gross profit per WSEE per month for Q1 2022 decreased $17 to $342 compared to $359 in Q1 2021 due primarily to higher direct costs, offset in part by higher average pricing, as discussed below.

Our pricing objectives attempt to achieve a level of revenue per WSEE that matches or exceeds changes in primary direct costs and operating expenses. Our revenues per WSEE per month increased $47 due to higher average pricing.

The net decrease in direct costs between Q1 2022 and Q1 2021 attributable to the changes in cost estimates for benefits and workers’ compensation totaled $6.4 million as discussed below. The $64 per WSEE per month increase in direct costs is due primarily to the direct cost components changes as follows:

Insperity | 2022 First Quarter Form 10-Q | 24 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | ||

Benefits costs

•The cost of group health insurance and related employee benefits increased $35 per WSEE per month and increased 7.4% on a cost per covered employee basis.

•The percentage of WSEEs covered under our health insurance plans was 66.3% in Q1 2022 compared to 67.8% in Q1 2021.

•Reported results include changes in estimated claims run-off related to prior periods, which was an increase in costs of $0.8 million, or $1 per WSEE per month, in Q1 2022 compared to an increase in costs of $5.5 million, or $8 per WSEE per month, in Q1 2021.

Please read Note 2 to the Consolidated Financial Statements, “Accounting Policies – Health Insurance Costs,” for a discussion of our accounting for health insurance costs.

Workers’ compensation costs

Our continued discipline around our client selection, safety and claims management has allowed for claims within our policy periods to be closed out at amounts below our original cost estimates.

•Workers’ compensation costs decreased 3.4%, or $4 per WSEE per month, in Q1 2022 compared to Q1 2021 on a 27.2% increase in non-bonus payroll costs.

•As a percentage of non-bonus payroll cost, workers’ compensation costs were 0.20% in Q1 2022 and 0.26% Q1 2021.

•We recorded a reduction in workers’ compensation costs of $14.9 million, or 0.22% of non-bonus payroll costs, in Q1 2022 compared to a reduction of $13.2 million, or 0.25% of non-bonus payroll costs, in Q1 2021, primarily as a result of closing out claims at lower than expected costs.

Please read Note 2 to the Consolidated Financial Statements, “Accounting Policies – Workers’ Compensation Costs,” for a discussion of our accounting for workers’ compensation costs.

Payroll tax costs

•Payroll taxes increased 25.4% on a 29.8% increase in payroll costs, or $37 per WSEE per month, primarily due to the non-recurrence of the Q1 2021 collection of a $5.5 million federal payroll tax refund related to a prior year.

•Payroll taxes as a percentage of payroll costs decreased to 7.5% in Q1 2022 compared to 7.8% Q1 2021.

Operating Expenses

•Salaries, wages and payroll taxes — Salaries, wages and payroll taxes (“Salaries”) are primarily a function of the number of corporate employees, their associated average pay and any additional incentive compensation.

•Stock-based compensation — Our stock-based compensation relates to the recognition of non-cash compensation expense over the requisite service period of time-vested and performance-based awards.

•Commissions — Commissions expense consists primarily of amounts paid to sales managers and other sales personnel, including business performance advisors (“BPAs”), as well as, channel referral fees. Commissions are based on new accounts sold and a percentage of revenue generated by such personnel.

•Advertising — Advertising expense primarily consists of media advertising and other business promotions in our current and anticipated sales markets.

•General and administrative expenses — Our general and administrative expenses primarily include:

◦rent expenses related to our service centers and sales offices

◦outside professional service fees related to legal, consulting and accounting services

◦administrative costs, such as postage, printing and supplies

Insperity | 2022 First Quarter Form 10-Q | 25 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | ||

◦employee travel and training expenses

◦technology and facility costs, including repairs, maintenance and software-as-a-service (“SaaS”) licensing costs

•Depreciation and amortization — Depreciation and amortization expense is primarily a function of our capital investments in corporate facilities, service centers, sales offices, software development and technology infrastructure.

First Quarter 2022 Compared to First Quarter 2021

The following table presents certain information related to our operating expenses:

| Three Months Ended March 31, | |||||||||||||||||||||||

| per WSEE | |||||||||||||||||||||||

| (in thousands, except per WSEE) | 2022 | 2021 | % Change | 2022 | 2021 | % Change | |||||||||||||||||

| Salaries | $ | 107,439 | $ | 103,075 | 4.2 | % | $ | 129 | $ | 147 | (12.2) | % | |||||||||||

| Stock-based compensation | 9,846 | 11,822 | (16.7) | % | 12 | 17 | (29.4) | % | |||||||||||||||

| Commissions | 10,310 | 7,719 | 33.6 | % | 12 | 11 | 9.1 | % | |||||||||||||||

| Advertising | 8,595 | 5,322 | 61.5 | % | 10 | 8 | 25.0 | % | |||||||||||||||

| General and administrative | 41,005 | 31,636 | 29.6 | % | 49 | 45 | 8.9 | % | |||||||||||||||

| Depreciation and amortization | 10,184 | 8,047 | 26.6 | % | 12 | 12 | — | ||||||||||||||||

| Total operating expenses | $ | 187,379 | $ | 167,621 | 11.8 | % | $ | 224 | $ | 240 | (6.7) | % | |||||||||||

Operating expenses for Q1 2022 increased 11.8% to $187.4 million compared to $167.6 million in Q1 2021. Operating expenses per WSEE per month for Q1 2022 decreased 6.7% to $224 compared to $240 in Q1 2021.

•Salaries of corporate and sales staff for Q1 2022 increased 4.2% to $107.4 million, but decreased $18 on a per WSEE per month basis, compared to Q1 2021, on the 19.5% increase in WSEEs paid per month.

•Stock-based compensation expense for Q1 2022 decreased 16.7% to $9.8 million, or $5 per WSEE per month, compared to Q1 2021. The decrease was primarily due to the non-recurrence of stock-based compensation expense related to our 2020 short-term performance based awards that vested in Q1 2021.

•Commissions expense for Q1 2022 increased 33.6% to $10.3 million, or $1 per WSEE per month, compared to Q1 2021. The increase was primarily due to commissions associated with our PEO HR Outsourcing solutions, including a new incentive program for our BPAs, as well as an increase in the amount of sales channel referral fees paid during 2022.

•Advertising expense for Q1 2022 increased 61.5% to $8.6 million, or $2 per WSEE per month, compared to Q1 2021. The increase was primarily due to increases in radio, print and digital advertising and sponsorship costs.

•General and administrative expenses for Q1 2022 increased 29.6% to $41.0 million, or $4 per WSEE per month, compared to Q1 2021. The increase was primarily due to increased travel and event costs.

•Depreciation and amortization expense for Q1 2022 increased 26.6% to $10.2 million, but remained flat on a per WSEE per month basis, compared to Q1 2021. The increase was primarily due to the completion of a new facility on our corporate campus and increased capital expenditures related to software development costs.

Other Income (Expense)

Other Income (expense) for Q1 2022 was net expense of $1.8 million compared to net expense of $1.1 million in Q1 2021.

Insperity | 2022 First Quarter Form 10-Q | 26 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | ||

Income Tax Expense

| Three Months Ended March 31, | ||||||||

| 2022 | 2021 | |||||||

| Effective income tax rate | 27.7% | 25.2% | ||||||

For the three months ended March 31, 2022, our provision for income taxes differed from the U.S. statutory rate primarily due to state income taxes, non-deductible expenses and vesting of restricted and long-term incentive stock awards. During the first three months of 2022 and 2021, we recognized an income tax benefit of $0.5 million and $2.2 million, respectively, related to the vesting of short-term, long-term incentive, and restricted stock awards.

Non-GAAP Financial Measures

Non-GAAP financial measures are not prepared in accordance with GAAP and may be different from non-GAAP financial measures used by other companies. Non-GAAP financial measures should not be considered as a substitute for, or superior to, measures of financial performance prepared in accordance with GAAP. Investors are encouraged to review the reconciliation of the non-GAAP financial measures used to their most directly comparable GAAP financial measures as provided in the tables below.

| Non-GAAP Measure | Definition | Benefit of Non-GAAP Measure | ||||||

Non-bonus payroll cost | Non-bonus payroll cost is a non-GAAP financial measure that excludes the impact of bonus payrolls paid to our WSEEs. Bonus payroll cost varies from period to period, but has no direct impact to our ultimate workers’ compensation costs under the current program. | Our management refers to non-bonus payroll cost in analyzing, reporting and forecasting our workers’ compensation costs. We include these non-GAAP financial measures because we believe they are useful to investors in allowing for greater transparency related to the costs incurred under our current workers’ compensation program. | ||||||

Adjusted cash, cash equivalents and marketable securities | Excludes funds associated with: • federal and state income tax withholdings, • employment taxes, • other payroll deductions, and • client prepayments. | We believe that the exclusion of the identified items helps us reflect the fundamentals of our underlying business model and analyze results against our expectations, against prior periods, and to plan for future periods by focusing on our underlying operations. We believe that the adjusted results provide relevant and useful information for investors because they allow investors to view performance in a manner similar to the method used by management and improves their ability to understand and assess our operating performance. Adjusted EBITDA is used by our lenders to assess our leverage and ability to make interest payments. | ||||||

EBITDA | Represents net income computed in accordance with GAAP, plus: • interest expense, • income tax expense, • depreciation and amortization expense, and • amortization of SaaS implementation costs | |||||||

Adjusted EBITDA | Represents EBITDA plus: • non-cash stock-based compensation. | |||||||

| Adjusted net income | Represents net income computed in accordance with GAAP, excluding: • non-cash stock-based compensation. | |||||||

Adjusted EPS | Represents diluted net income per share computed in accordance with GAAP, excluding: • non-cash stock-based compensation. | |||||||

Insperity | 2022 First Quarter Form 10-Q | 27 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | ||

Following is a reconciliation of payroll cost (GAAP) to non-bonus payroll costs (non-GAAP):

| (in thousands, except per WSEE per month) | Three Months Ended March 31, | ||||||||||||||||

| 2022 | 2021 | ||||||||||||||||

| Per WSEE | Per WSEE | ||||||||||||||||

| Payroll cost | $ | 8,780,068 | $ | 10,503 | $ | 6,763,587 | $ | 9,669 | |||||||||

Less: Bonus payroll cost | 1,983,853 | 2,373 | 1,420,475 | 2,031 | |||||||||||||

Non-bonus payroll cost | $ | 6,796,215 | $ | 8,130 | $ | 5,343,112 | $ | 7,638 | |||||||||

% Change period over period | 27.2 | % | 6.4 | % | 3.6 | % | 5.8 | % | |||||||||

Following is a reconciliation of cash, cash equivalents and marketable securities (GAAP) to adjusted cash, cash equivalents and marketable securities (non-GAAP):

| (in thousands) | March 31, 2022 | December 31, 2021 | |||||||||

| Cash, cash equivalents and marketable securities | $ | 609,264 | $ | 607,603 | |||||||

Less: | |||||||||||

Amounts payable for withheld federal and state income taxes, employment taxes and other payroll deductions | 338,278 | 424,800 | |||||||||

Client prepayments | 117,807 | 20,054 | |||||||||

| Adjusted cash, cash equivalents and marketable securities | $ | 153,179 | $ | 162,749 | |||||||

Following is a reconciliation of net income (GAAP) to EBITDA (non-GAAP) and adjusted EBITDA (non-GAAP):

| Three Months Ended March 31, | |||||||||||||||||

| (in thousands, except per WSEE per month) | 2022 | 2021 | |||||||||||||||

| Per WSEE | Per WSEE | ||||||||||||||||

| Net income | $ | 69,884 | $ | 84 | $ | 61,922 | $ | 89 | |||||||||

| Income tax expense | 26,734 | 32 | 20,846 | 30 | |||||||||||||

| Interest expense | 1,925 | 2 | 1,599 | 2 | |||||||||||||

Depreciation and amortization | 10,184 | 12 | 8,047 | 11 | |||||||||||||

| EBITDA | 108,727 | 130 | 92,414 | 132 | |||||||||||||

Stock-based compensation | 9,846 | 12 | 11,822 | 17 | |||||||||||||

| Adjusted EBITDA | $ | 118,573 | $ | 142 | $ | 104,236 | $ | 149 | |||||||||

% Change period over period | 13.8 | % | (4.7) | % | 2.9 | % | 4.9 | % | |||||||||

Following is a reconciliation of net income (GAAP) to adjusted net income (non-GAAP):

| Three Months Ended March 31, | ||||||||

| (in thousands) | 2022 | 2021 | ||||||

| Net income | $ | 69,884 | $ | 61,922 | ||||

| Non-GAAP adjustments: | ||||||||

| Stock-based compensation | 9,846 | 11,822 | ||||||

| Tax effect | (2,724) | (2,978) | ||||||

| Total non-GAAP adjustments, net | 7,122 | 8,844 | ||||||

| Adjusted net income | $ | 77,006 | $ | 70,766 | ||||

| % Change period over period | 8.8 | % | 5.8 | % | ||||

Insperity | 2022 First Quarter Form 10-Q | 28 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | ||

Following is a reconciliation of diluted EPS (GAAP) to adjusted EPS (non-GAAP):

| Three Months Ended March 31, | ||||||||

| (amounts per share) | 2022 | 2021 | ||||||

| Diluted EPS | $ | 1.80 | $ | 1.59 | ||||

| Non-GAAP adjustments: | ||||||||

| Stock-based compensation | 0.25 | 0.30 | ||||||

| Tax effect | (0.06) | (0.07) | ||||||

| Total non-GAAP adjustments, net | 0.19 | 0.23 | ||||||

| Adjusted EPS | $ | 1.99 | $ | 1.82 | ||||

% Change period over period | 9.3 | % | 7.1 | % | ||||

Liquidity and Capital Resources

We periodically evaluate our liquidity requirements, capital needs and availability of resources in view of, among other things, our expansion plans, stock repurchases, potential acquisitions, debt service requirements and other operating cash needs. To meet short-term liquidity requirements, which are primarily the payment of direct costs and operating expenses, we rely primarily on cash from operations. Longer-term projects, large stock repurchases or significant acquisitions may be financed with public or private debt or equity. We have a $500 million revolving credit facility (“Facility”) with a syndicate of financial institutions. The Facility is available for working capital and general corporate purposes, including acquisitions and stock repurchases. We have in the past sought, and may in the future seek, to raise additional capital or take other steps to increase or manage our liquidity and capital resources.

We had $609.3 million in cash, cash equivalents and marketable securities at March 31, 2022, of which approximately $338.3 million was payable in early April 2022 for withheld federal and state income taxes, employment taxes and other payroll deductions, and approximately $117.8 million represented client prepayments that were payable in April 2022. At March 31, 2022, we had working capital of $145.3 million compared to $116.3 million at December 31, 2021. We currently believe that our cash on hand, marketable securities, cash flows from operations and availability under the Facility will be adequate to meet our liquidity requirements for the remainder of 2022. We intend to rely on these same sources, as well as public and private debt or equity financing, to meet our longer-term liquidity and capital needs, which we continually monitor in light of our strategic goals and the significant uncertainty related to the ongoing impacts of the COVID-19 pandemic.

As of March 31, 2022, we had an outstanding letter of credit and borrowings totaling $370.4 million under the Facility. Please read Note 5 to the Consolidated Financial Statements, “Long-Term Debt,” for additional information.

Cash Flows from Operating Activities

Net cash provided by operating activities in the first three months of 2022 was $58.8 million. Our primary source of cash from operations is the comprehensive service fee and payroll funding we collect from our clients. Our cash and cash equivalents, and thus our reported cash flows from operating activities, are significantly impacted by various external and internal factors, which are reflected in part by the changes in our balance sheet accounts. These include the following:

•Timing of client payments / payroll taxes – We typically collect our comprehensive service fee, along with the client’s payroll funding, from clients no later than the same day as the payment of WSEE payrolls and associated payroll taxes. Therefore, the last business day of a reporting period has a substantial impact on our reporting of operating cash flows. For example, many WSEEs are paid on Fridays; therefore, operating cash flows decrease in the reporting periods that end on a Friday or a Monday. In the period ended March 31, 2022, the last business day of the reporting period was a Thursday, client prepayments were $117.8 million and employment taxes and other deductions were $338.3 million. In the period ended March 31, 2021, the last business day of the reporting period was a Wednesday, client prepayments were $58.9 million and employment taxes and other deductions were $273.5 million.

Insperity | 2022 First Quarter Form 10-Q | 29 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | ||

•Medical plan funding – Our health care contract with United establishes participant cash funding rates 90 days in advance of the beginning of a reporting quarter. Therefore, changes in the participation level of the United plan have a direct impact on our operating cash flows. In addition, changes to the funding rates, which are solely determined by United based primarily upon recent claim history and anticipated cost trends, also have a significant impact on our operating cash flows. As of March 31, 2022, premiums owed and cash funded to United have exceeded the costs of the United plan, resulting in a $13.3 million surplus, $4.3 million of which is reflected as a current asset, and $9.0 million of which is reflected as a long-term asset on our Condensed Consolidated Balance Sheets. The premiums, including an additional quarterly premium, owed to United at March 31, 2022, were $55.0 million, which is included in accrued health insurance costs, a current liability, on our Condensed Consolidated Balance Sheets.

•Operating results – Our adjusted net income has a significant impact on our operating cash flows. Our adjusted net income increased 8.8% to $77.0 million in the first three months ended March 31, 2022, compared to $70.8 million in the first three months ended March 31, 2021. Please read “Results of Operations – First Three Months 2022 Compared to First Three Months 2021.”

Cash Flows from Investing Activities

Net cash flows used in investing activities were $5.9 million for the three months ended March 31, 2022, primarily due to property and equipment purchases of $4.7 million.

Cash Flows from Financing Activities

Net cash flows used in financing activities were $43.9 million for the three months ended March 31, 2022. We paid $17.2 million in dividends and repurchased or withheld $27.4 million in stock.

Insperity | 2022 First Quarter Form 10-Q | 30 | ||||

QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK AND CONTROLS AND PROCEDURES | ||

Item 3. Quantitative and Qualitative Disclosures About Market Risk

We are primarily exposed to market risks from fluctuations in interest rates and the effects of those fluctuations on the market values of our cash equivalent short-term investments, our available-for-sale marketable securities and our borrowings under our Facility, which bears interest at a variable market rate. As of March 31, 2022, we had outstanding letters of credit and borrowings totaling $370.4 million under the Facility. Please read Note 5 to the Consolidated Financial Statements, “Long-Term Debt,” for additional information.

The cash equivalent short-term investments consist primarily of overnight investments, which are not significantly exposed to interest rate risk, except to the extent that changes in interest rates will ultimately affect the amount of interest income earned on these investments. Our available-for-sale marketable securities are subject to interest rate risk because these securities generally include a fixed interest rate. As a result, the market values of these securities are affected by changes in prevailing interest rates.

We attempt to limit our exposure to interest rate risk primarily through diversification and low investment turnover. Our investment policy is designed to maximize after-tax interest income while preserving our principal investment. As a result, our marketable securities consist of tax-exempt short term and intermediate term debt securities, which are primarily U.S. Government Securities.

Item 4. Controls and Procedures

In accordance with Rules 13a-15 and 15d-15 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), we carried out an evaluation, under the supervision and with the participation of management, including our Chief Executive Officer and Chief Financial Officer, of the effectiveness of our disclosure controls and procedures as of the end of the period covered by this report. Based on that evaluation, our Chief Executive Officer and Chief Financial Officer concluded that our disclosure controls and procedures were effective as of March 31, 2022.

There has been no change in our internal controls over financial reporting that occurred during the three months ended March 31, 2022 that has materially affected, or is reasonably likely to materially affect, our internal controls over financial reporting.

Insperity | 2022 First Quarter Form 10-Q | 31 | ||||

OTHER INFORMATION | ||

PART II