UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-Q

For the quarterly period ended September 30, 2023

OR

For the transition period from to .

Commission File No. 000-26770

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||||||||||

| (Address of principal executive offices) | (Zip code) | ||||||||||

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

Indicate by check mark whether the Registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| x | Accelerated Filer | o | |||||||||

| Non-accelerated filer | o | Smaller reporting company | |||||||||

| Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No x

The number of shares outstanding of the Registrant's Common Stock, $0.01 par value, was 118,790,222 as of October 31, 2023.

NOVAVAX, INC.

TABLE OF CONTENTS

| Page No. | ||||||||

Item 1A. | ||||||||

Item 2. | ||||||||

i

PART I. FINANCIAL INFORMATION

Item 1. Financial Statements

1

NOVAVAX, INC.

CONSOLIDATED STATEMENTS OF OPERATIONS

(in thousands, except per share information)

(unaudited)

| For the Three Months Ended September 30, | For the Nine Months Ended September 30, | ||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | ||||||||||||||||||||

| Revenue: | |||||||||||||||||||||||

| Product sales | $ | $ | $ | $ | |||||||||||||||||||

| Grants | |||||||||||||||||||||||

| Royalties and other | |||||||||||||||||||||||

| Total revenue | |||||||||||||||||||||||

| Expenses: | |||||||||||||||||||||||

| Cost of sales | |||||||||||||||||||||||

| Research and development | |||||||||||||||||||||||

| Selling, general, and administrative | |||||||||||||||||||||||

| Total expenses | |||||||||||||||||||||||

Loss from operations | ( | ( | ( | ( | |||||||||||||||||||

| Other income (expense): | |||||||||||||||||||||||

| Interest expense | ( | ( | ( | ( | |||||||||||||||||||

| Other income (expense) | ( | ( | ( | ||||||||||||||||||||

Loss before income taxes | ( | ( | ( | ( | |||||||||||||||||||

Income tax expense (benefit) | ( | ||||||||||||||||||||||

Net loss | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||

Net loss per share: | |||||||||||||||||||||||

Basic and diluted | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||

| Weighted average number of common shares outstanding | |||||||||||||||||||||||

Basic and diluted | |||||||||||||||||||||||

CONSOLIDATED STATEMENTS OF COMPREHENSIVE LOSS

(in thousands)

(unaudited)

| For the Three Months Ended September 30, | For the Nine Months Ended September 30, | ||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | ||||||||||||||||||||

Net loss | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||

Other comprehensive loss: | |||||||||||||||||||||||

| Foreign currency translation adjustment | ( | ( | ( | ( | |||||||||||||||||||

Other comprehensive loss | ( | ( | ( | ( | |||||||||||||||||||

Comprehensive loss | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||

The accompanying notes are an integral part of these financial statements.

2

NOVAVAX, INC.

CONSOLIDATED BALANCE SHEETS

(in thousands, except share and per share information)

| September 30, 2023 | December 31, 2022 | ||||||||||

| (unaudited) | |||||||||||

| ASSETS | |||||||||||

| Current assets: | |||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

| Restricted cash | |||||||||||

| Accounts receivable | |||||||||||

| Inventory | |||||||||||

| Prepaid expenses and other current assets | |||||||||||

| Total current assets | |||||||||||

| Property and equipment, net | |||||||||||

| Right of use asset, net | |||||||||||

| Goodwill | |||||||||||

| Other non-current assets | |||||||||||

| Total assets | $ | $ | |||||||||

| LIABILITIES AND STOCKHOLDERS’ DEFICIT | |||||||||||

| Current liabilities: | |||||||||||

| Accounts payable | $ | $ | |||||||||

| Accrued expenses | |||||||||||

| Deferred revenue | |||||||||||

| Current portion of finance lease liabilities | |||||||||||

| Convertible notes payable | |||||||||||

| Other current liabilities | |||||||||||

| Total current liabilities | |||||||||||

| Deferred revenue | |||||||||||

| Convertible notes payable | |||||||||||

| Non-current finance lease liabilities | |||||||||||

| Other non-current liabilities | |||||||||||

| Total liabilities | |||||||||||

Commitments and contingencies (Note 14) | |||||||||||

Preferred stock, $ | |||||||||||

| Stockholders' deficit: | |||||||||||

Common stock, $ | |||||||||||

| Additional paid-in capital | |||||||||||

| Accumulated deficit | ( | ( | |||||||||

Treasury stock, cost basis, | ( | ( | |||||||||

| Accumulated other comprehensive loss | ( | ( | |||||||||

| Total stockholders’ deficit | ( | ( | |||||||||

| Total liabilities and stockholders’ deficit | $ | $ | |||||||||

The accompanying notes are an integral part of these financial statements.

3

NOVAVAX, INC.

CONSOLIDATED STATEMENTS OF CHANGES IN STOCKHOLDERS' DEFICIT

Three and Nine Ended September 30, 2023 and 2022

(in thousands, except share information)

(unaudited)

| Common Stock | Additional Paid-in Capital | Accumulated Deficit | Treasury Stock | Accumulated Other Comprehensive Loss | Total Stockholders' Deficit | ||||||||||||||||||||||||||||||||||||

| Shares | Amount | ||||||||||||||||||||||||||||||||||||||||

| Balance at June 30, 2023 | $ | $ | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||||||||||||||||||

| Stock-based compensation | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||

| Stock issued under incentive programs | — | ( | — | ||||||||||||||||||||||||||||||||||||||

Issuance of common stock, net of issuance costs $ | — | — | — | ||||||||||||||||||||||||||||||||||||||

| Foreign currency translation adjustment | — | — | — | — | — | ( | ( | ||||||||||||||||||||||||||||||||||

Net loss | — | — | — | ( | — | — | ( | ||||||||||||||||||||||||||||||||||

| Balance at September 30, 2023 | $ | $ | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||||||||||||||||||

| Balance at June 30, 2022 | $ | $ | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||||||||||||||||||

| Stock-based compensation | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||

| Stock issued under incentive programs | — | ( | — | ( | |||||||||||||||||||||||||||||||||||||

| Foreign currency translation adjustment | — | — | — | — | — | ( | ( | ||||||||||||||||||||||||||||||||||

| Net loss | — | — | — | ( | — | — | ( | ||||||||||||||||||||||||||||||||||

| Balance at September 30, 2022 | $ | $ | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||||||||||||||||||

| Common Stock | Additional Paid-in Capital | Accumulated Deficit | Treasury Stock | Accumulated Other Comprehensive Loss | Total Stockholders' Deficit | ||||||||||||||||||||||||||||||||||||

| Shares | Amount | ||||||||||||||||||||||||||||||||||||||||

| Balance at December 31, 2022 | $ | $ | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||||||||||||||||||

| Stock-based compensation | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||

| Stock issued under incentive programs | — | ( | — | ||||||||||||||||||||||||||||||||||||||

Issuance of common stock, net of issuance costs of $ | — | — | — | ||||||||||||||||||||||||||||||||||||||

| Foreign currency translation adjustment | — | — | — | — | — | ( | ( | ||||||||||||||||||||||||||||||||||

| Net loss | — | — | — | ( | — | — | ( | ||||||||||||||||||||||||||||||||||

| Balance at September 30, 2023 | $ | $ | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||||||||||||||||||

| Balance at December 31, 2021 | $ | $ | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||||||||||||||||||

| Stock-based compensation | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||

| Stock issued under incentive programs | — | ( | — | ||||||||||||||||||||||||||||||||||||||

Issuance of common stock, net of issuance costs of $ | — | — | — | ||||||||||||||||||||||||||||||||||||||

| Foreign currency translation adjustment | — | — | — | — | — | ( | ( | ||||||||||||||||||||||||||||||||||

| Net loss | — | — | — | ( | — | — | ( | ||||||||||||||||||||||||||||||||||

| Balance at September 30, 2022 | $ | $ | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||||||||||||||||||

The accompanying notes are an integral part of these financial statements.

4

NOVAVAX, INC.

CONSOLIDATED STATEMENTS OF CASH FLOWS

(in thousands)

(unaudited)

| Nine Months Ended September 30, | |||||||||||

| 2023 | 2022 | ||||||||||

| Operating Activities: | |||||||||||

| Net loss | $ | ( | $ | ( | |||||||

| Reconciliation of net loss to net cash used in operating activities: | |||||||||||

| Depreciation and amortization | |||||||||||

| Non-cash stock-based compensation | |||||||||||

| Provision for excess and obsolete inventory | |||||||||||

| Impairment of long-lived assets | |||||||||||

| Right-of-use assets expensed, net of credits received | |||||||||||

| Other items, net | ( | ( | |||||||||

| Changes in operating assets and liabilities: | |||||||||||

| Inventory | ( | ( | |||||||||

| Accounts receivable, prepaid expenses, and other assets | ( | ||||||||||

| Accounts payable, accrued expenses, and other liabilities | ( | ||||||||||

| Deferred revenue | ( | ||||||||||

| Net cash used in operating activities | ( | ( | |||||||||

| Investing Activities: | |||||||||||

| Capital expenditures | ( | ( | |||||||||

| Internal-use software | ( | ( | |||||||||

| Net cash used in investing activities | ( | ( | |||||||||

| Financing Activities: | |||||||||||

| Net proceeds from sales of common stock | |||||||||||

| Net proceeds from the exercise of stock-based awards | |||||||||||

| Finance lease payments | ( | ( | |||||||||

| Repayment of 2023 Convertible notes | ( | ||||||||||

| Payments of costs related to issuance of 2027 Convertible notes | ( | ||||||||||

| Net cash provided by (used in) financing activities | ( | ||||||||||

| Effect of exchange rate on cash, cash equivalents, and restricted cash | |||||||||||

| Net decrease in cash, cash equivalents, and restricted cash | ( | ( | |||||||||

| Cash, cash equivalents, and restricted cash at beginning of period | |||||||||||

| Cash, cash equivalents, and restricted cash at end of period | $ | $ | |||||||||

| Supplemental disclosure of non-cash activities: | |||||||||||

| Right-of-use assets from new lease agreements | $ | $ | |||||||||

| Capital expenditures included in accounts payable and accrued expenses | $ | $ | |||||||||

Internal-use software included in accounts payable and accrued expenses | $ | $ | |||||||||

| Supplemental disclosure of cash flow information: | |||||||||||

| Cash interest payments, net of amounts capitalized | $ | $ | |||||||||

| Cash paid for income taxes | $ | $ | |||||||||

The accompanying notes are an integral part of these financial statements.

5

NOVAVAX, INC.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

September 30, 2023

(unaudited)

Note 1 – Organization and Business

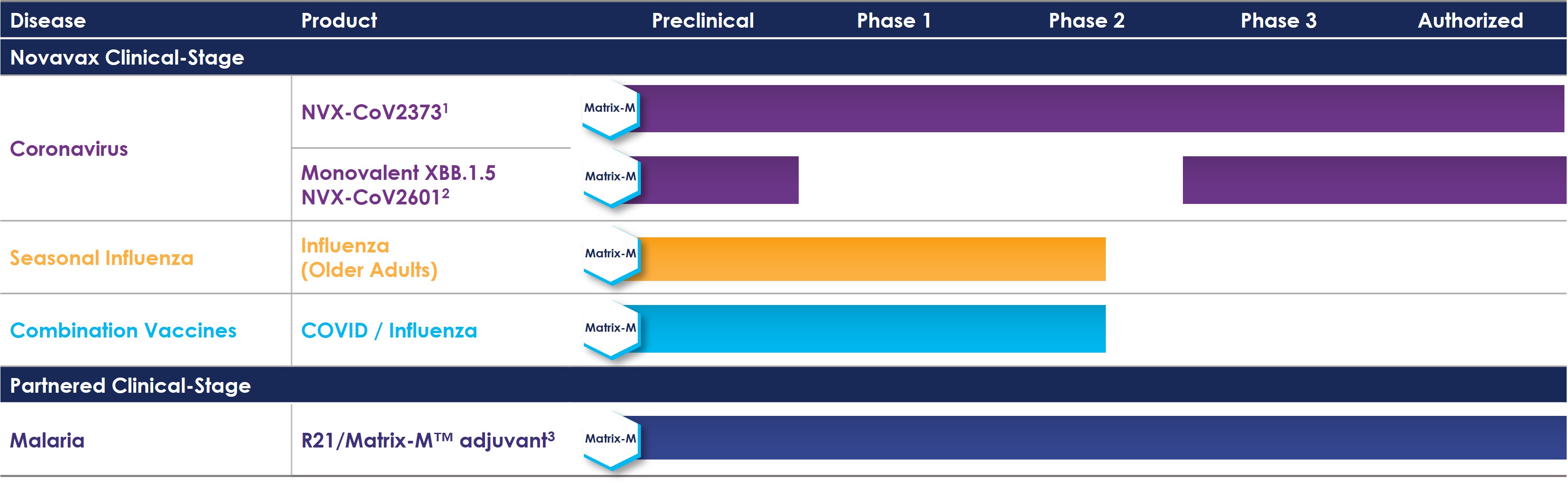

Novavax, Inc. (“Novavax,” and together with its wholly owned subsidiaries, the “Company”) is a biotechnology company that promotes improved health by discovering, developing, and commercializing innovative vaccines to prevent serious infectious diseases. Novavax offers a differentiated vaccine platform that combines a recombinant protein approach, innovative nanoparticle technology and patented Matrix-M™ adjuvant to enhance the immune response. Novavax currently has one commercial program, for vaccines to prevent COVID-19, which includes Nuvaxovid prototype COVID-19 vaccine ("NVX-CoV2373,” or “prototype vaccine”) and Nuvaxovid updated COVID-19 vaccine (“NVX-CoV2601,” or “updated vaccine”) (collectively, “COVID-19 Program,” or “COVID-19 Vaccine”). Local authorities have also specified nomenclature for the prototype and updated vaccines within their labeling (“Novavax COVID-19 Vaccine, Adjuvanted” and “Novavax COVID-19, Adjuvanted (2023-2024 Formula), respectively, for the U.S.). The Company’s partner, Serum Institute of India Pvt. Ltd. (“SIIPL”), markets NVX-CoV2373 as “Covovax™.”

Beginning in 2022, the Company received approval, interim authorization, provisional approval, conditional marketing authorization, and emergency use authorization (“EUA”) from multiple regulatory authorities globally for its prototype vaccine for both adult and adolescent populations as a primary series and for both homologous and heterologous booster indications in select territories. In October 2023, the U.S. Food and Drug Administration (“U.S. FDA”) amended the EUA for its prototype vaccine to include its updated vaccine. The amended EUA authorizes use of the Company’s updated vaccine in individuals 12 years and older. In October 2023, the European Commission (“EC”) granted approval for the Company’s updated vaccine for active immunization to prevent COVID-19 caused by SARS-CoV-2 in individuals aged 12 and older. The Company exclusively depends on its supply agreement with SIIPL and its subsidiary, Serum Life Sciences Limited (“SLS”), for co-formulation, filling and finishing (other than in Europe) and on its service agreement with PCI Pharma Services for finishing in Europe. The Company plans to rely on these arrangements to supply its updated vaccine during the 2023-2024 vaccination season and subsequently (see Note 4).

Novavax is advancing development of other vaccine candidates, including its influenza vaccine candidate, its COVID19-Influenza Combination (“CIC”) vaccine candidate and additional vaccine candidates. The Company’s COVID-19 Program and its other vaccine candidates incorporate the Company’s proprietary Matrix-M™ adjuvant to enhance the immune response and stimulate higher levels of functional antibodies and induce a cellular immune response.

Note 2 – Summary of Significant Accounting Policies

Basis of Presentation

The accompanying unaudited consolidated financial statements have been prepared in accordance with generally accepted accounting principles in the United States of America (“U.S. GAAP”) for interim financial information and the instructions to Form 10-Q and Article 10 of Regulation S-X. The consolidated financial statements are unaudited but include all adjustments (consisting of normal recurring adjustments) that the Company considers necessary for a fair presentation of the financial position, operating results, comprehensive loss, changes in stockholders’ deficit, and cash flows for the periods presented. Although the Company believes that the disclosures in these unaudited consolidated financial statements are adequate to make the information presented not misleading, certain information and footnote information normally included in consolidated financial statements prepared in accordance with U.S. GAAP have been condensed or omitted as permitted under the rules and regulations of the United States Securities and Exchange Commission (“SEC”).

The unaudited consolidated financial statements include the accounts of Novavax, Inc. and its wholly owned subsidiaries. All intercompany accounts and transactions have been eliminated in consolidation. Accumulated other comprehensive loss included a foreign currency translation loss of $11.9 million and $6.4 million at September 30, 2023 and December 31, 2022, respectively. The aggregate foreign currency transaction gains and losses resulting from the conversion of the transaction currency to functional currency were a $12.2 million loss and a $3.9 million gain, and a $38.6 million loss and $59.6 million loss for the three and nine months ended September 30, 2023 and 2022, respectively, which are reflected in Other income (expense).

6

Liquidity and Going Concern

The accompanying unaudited consolidated financial statements have been prepared assuming, subject to the disclosures herein, that the Company will continue as a going concern within one year after the date that the financial statements are issued. In addition, as of September 30, 2023, the Company had $666.4 million in cash and cash equivalents and restricted cash. Pursuant to the June 2023 Amendment to the advance purchase agreement between the Company and the Canadian government (the “Canada APA”), the Company expects to receive the second installment of $174.8 million from the Canadian government that is contingent and payable upon the Company’s delivery of vaccine doses in the fourth quarter of 2023 (see Note 3). During the nine months ended September 30, 2023, the Company incurred a net loss of $366.7 million and had net cash flows used in operating activities of $537.2 million.

In accordance with Accounting Standards Codification 205-40, Going Concern, the Company evaluated whether there are conditions and events, considered in the aggregate, that raise substantial doubt about its ability to continue as a going concern within one year after the date that these unaudited consolidated financial statements are issued. While the Company’s current cash flow forecast for the one-year going concern look forward period estimates that there will be sufficient capital available to fund operations, this forecast is subject to significant uncertainty, including as it relates to revenue for the next 12 months, the Company’s ability to execute on certain cost-cutting initiatives and a pending matter subject to arbitration proceedings. The Company’s revenue projections depend on its ability to successfully manufacture, distribute and market its updated vaccine for the 2023-2024 vaccination season, which is inherently uncertain and subject to a number of risks, including the Company’s ability to obtain regulatory authorizations, the incidence of COVID-19 during the 2023-2024 vaccination season, the Company’s ability to timely deliver doses and achieve commercial adoption and market acceptance of its updated vaccine.

Failure to meet regulatory milestones, timely obtain supportive recommendations from governmental advisory committees, or achieve product volume or delivery timing obligations under the Company’s advance purchase agreements (“APAs”) may require the Company to refund portions of upfront and other payments or result in reduced future payments which would adversely affect the Company’s ability to continue as a going concern. For example, if the Company fails to deliver its updated vaccine doses to the Canadian government in the fourth quarter of 2023, the second installment payment of $174.8 million will be terminated and not be payable to the Company. In addition, the Canadian government may terminate the Canada APA if the Company fails to achieve regulatory approval for use of the Biologics Manufacturing Centre, Inc. (“BMC”) for COVID-19 Vaccine production on or before December 31, 2024. Also, if the Company does not timely achieve supportive recommendations from the Joint Committee on Vaccination and Immunisation (the “JCVI”) of the government of the United Kingdom of Great Britain and Northern Ireland (the “Authority”) with respect to use of its COVID-19 Program for (a) the general adult population as part of a SARS-CoV-2 vaccine booster campaign in the United Kingdom or (b) the general adolescent population as part of a SARS-CoV-2 vaccine booster campaign in the United Kingdom or as a primary series SARS-CoV-2 vaccination, excluding where that recommendation relates only to one or more population groups comprising less than one million members in the United Kingdom, then the Company would be required to repay up to $112.5 696.4 million as of September 30, 2023 (see Note 3 and Note 14).

Management believes that, given the significance of these uncertainties, substantial doubt exists regarding the Company’s ability to continue as a going concern through one year from the date that these financial statements are issued.

7

In May 2023, the Company announced a global restructuring and cost reduction plan (the “Restructuring Plan”), which includes a more focused investment in its COVID-19 Program, reduction to its pipeline spending, the continued rationalization of its manufacturing network, a reduction to the Company’s global workforce, as well as the consolidation of facilities, and infrastructure. The workforce reduction plan included an approximately 25 % reduction in the Company’s global workforce, comprised of an approximately 20 % reduction in full-time Novavax employees and the remainder comprised of contractors and consultants. The Company has decided to progress its CIC vaccine candidate toward late-stage development and, as such, is assessing the impact on its workforce requirements. The Company expects the full annual impact of the cost savings from the Restructuring Plan to be realized in 2024 and approximately half of the annual impact to be realized in 2023 due to timing of implementing the measures, and the applicable laws, regulations, and other factors in the jurisdictions in which the Company operates. During the nine months ended September 30, 2023, the Company recorded a charge of $4.5 million related to one-time employee severance and benefit costs and recorded an impairment charge of $10.1 million related to the consolidation of facilities and infrastructure (see Note 15).

The Company’s ability to fund Company operations is dependent upon revenue related to vaccine sales for its products and product candidates, if such product candidates receive marketing approval and are successfully commercialized, and in particular the 2023-2024 vaccination season, which is inherently uncertain and subject to a number of risks, including the incidence of COVID-19 during the 2023-2024 vaccination season, regulatory authorization, ability to timely deliver doses and commercial adoption and market acceptance of its updated vaccine, the resolution of certain matters, including whether, when, and how the dispute with Gavi is resolved, and management’s plans, which includes cost reductions associated with the Restructuring Plan. Management’s plans may also include raising additional capital through a combination of equity and debt financing, collaborations, strategic alliances, asset sales, and marketing, distribution, or licensing arrangements. New financings may not be available to the Company on commercially acceptable terms, or at all. Also, any collaborations, strategic alliances, asset sales and marketing, distribution, or licensing arrangements may require the Company to give up some or all of its rights to a product or technology, which in some cases may be at less than the full potential value of such rights. In addition, the regulatory and commercial success of the Company’s COVID-19 Program and the Company’s other vaccine candidates, including an influenza vaccine candidate, and a CIC vaccine candidate, remains uncertain. Also, the impact of the Company’s more focused investment in its COVID-19 Program, reduction to its pipeline spending, continued rationalization of its manufacturing network, reduction to its global workforce, and consolidation of its facilities and infrastructure remain uncertain. If the Company is unable to obtain additional capital, the Company will assess its capital resources and may be required to delay, reduce the scope of, or eliminate some or all of its operations, or further downsize its organization, any of which may have a material adverse effect on its business, financial condition, results of operations, and ability to operate as a going concern.

Use of Estimates

The preparation of the consolidated financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the consolidated financial statements and the reported amounts of revenue and expenses during the reporting period. Actual results could differ materially from those estimates.

Restructuring

The Company recognizes restructuring charges when such costs are incurred. The Company’s restructuring charges consist of employee severance and other termination benefits related to the reduction of its workforce, the consolidation of facilities, and infrastructure and other costs. Termination benefits are expensed on the date the Company notifies the employee, unless the employee must provide future service, in which case the benefits are expensed ratably over the future service period. Ongoing benefits are expensed when restructuring activities are probable and the benefit estimable.

See Note 15 for additional information on the severance and employee benefit costs for terminated employees and impairment of assets in connection with the Company’s Restructuring Plan.

8

Recent Accounting Pronouncements

Adopted

In June 2016, the Financial Accounting Standards Board issued Accounting Standards Update (“ASU”) No. 2016-13, Financial Instruments - Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments (“ASU 2016-13”), with amendments in 2018, 2019, 2020, and 2022. The ASU sets forth a “current expected credit loss” model that requires companies to measure all expected credit losses for financial instruments held at the reporting date based on historical experience, current conditions, and reasonable supportable forecasts. ASU 2016-13 applies to financial instruments that are not measured at fair value, including receivables that result from revenue transactions. The Company adopted ASU 2020-06 on January 1, 2023, using a modified retrospective approach, and it did not have a material impact on the Company’s consolidated financial statements.

Note 3 – Revenue

The Company's accounts receivable included $71.1 million and $53.8 million related to amounts that were billed to customers and $52.6 million and $28.6 million related to amounts which had not yet been billed to customers as of September 30, 2023 and December 31, 2022, respectively. During the nine months ended September 30, 2023, and 2022, changes in the Company’s accounts receivables, allowance for doubtful accounts, and deferred revenue balances were as follows (in thousands):

| Balance, Beginning of Period | Additions | Deductions | Balance, End of Period | ||||||||||||||||||||

| Accounts receivable: | |||||||||||||||||||||||

| Nine Months Ended September 30, 2023 | $ | $ | $ | ( | $ | ||||||||||||||||||

| Nine Months Ended September 30, 2022 | ( | ||||||||||||||||||||||

Allowance for doubtful accounts(1): | |||||||||||||||||||||||

| Nine Months Ended September 30, 2023 | $ | ( | $ | $ | $ | ( | |||||||||||||||||

| Nine Months Ended September 30, 2022 | |||||||||||||||||||||||

Deferred revenue:(2) | |||||||||||||||||||||||

| Nine Months Ended September 30, 2023 | $ | $ | $ | ( | $ | ||||||||||||||||||

| Nine Months Ended September 30, 2022 | ( | ||||||||||||||||||||||

(1) There was no 6.2 million reversal of a bad debt allowance during the nine months ended September 30, 2023 due to the collection of a previously recognized allowance for doubtful accounts. To estimate the allowance for doubtful accounts, the Company evaluates the credit risk related to its customers based on historical loss experience, economic conditions, the aging of receivables, and customer-specific risks.

9

As of September 30, 2023, the aggregate amount of the transaction price allocated to performance obligations that were unsatisfied (or partially unsatisfied), excluding amounts related to sales-based royalties, the Gavi APA, and the reduction in doses related to the Amended and Restated SARS-CoV-2 Vaccine Supply Agreement, dated as of July 1, 2022 (as amended on September 26, 2022, the “Amended and Restated UK Supply Agreement”) between the Company and the Authority, which amended and restated the Original UK Supply Agreement, was approximately $2 billion of which $801.0 million was included in Deferred revenue. Failure to meet regulatory milestones, timely obtain supportive recommendations from governmental advisory committees, or achieve product volume or delivery timing obligations under the Company’s advance purchase agreements may require the Company to refund portions of upfront and other payments or result in reduced future payments, which could adversely impact the Company’s ability to realize revenue from its unsatisfied performance obligations. The timing to fulfill performance obligations related to grant agreements will depend on the results of the Company's research and development activities, including clinical trials. The timing to fulfill performance obligations related to APAs will depend on the timing of product manufacturing, receipt of marketing authorizations for additional indications, delivery of doses based on customer demand, and the ability of the customer to request the Company’s updated vaccine in place of the prototype vaccine under certain of the Company’s APAs.

Under the terms of the Gavi APA and a separate purchase agreement between Gavi and SIIPL, 1.1 billion doses of the prototype vaccine were to be made available to countries participating in the COVAX Facility. The Company expected to manufacture and distribute 350 million doses of the prototype vaccine to countries participating under the COVAX Facility. Under a separate purchase agreement with Gavi, SIIPL was expected to manufacture and deliver the balance of the 1.1 billion doses of the prototype vaccine for low- and middle-income countries participating in the COVAX Facility. The Company expected to deliver doses with antigen and adjuvant manufactured at facilities directly funded under the Company's funding agreement with Coalition for Epidemic Preparedness Innovations (“CEPI”), with initial doses supplied by SIIPL and SLS under a supply agreement. The Company expected to supply significant doses that Gavi would allocate to low-, middle- and high-income countries, subject to certain limitations, utilizing a tiered pricing schedule and Gavi could prioritize such doses to low- and middle- income countries, at lower prices. Additionally, the Company could provide additional doses of prototype vaccine, to the extent available from CEPI-funded manufacturing facilities, in the event that SIIPL could not materially deliver expected vaccine doses to the COVAX Facility. Under the agreement, the Company received an upfront payment of $350.0 million from Gavi in 2021 and an additional payment of $350.0 million in 2022 related to the Company’s achieving an emergency use license for the Company’s prototype vaccine by the World Health Organization (“WHO”) (the “Advance Payment Amount”). The Company maintains that its termination of the Advance Payment Amount was valid and denies that Gavi is entitled to a refund.

On November 18, 2022, the Company delivered written notice to Gavi to terminate the Gavi APA on the basis of Gavi’s failure to procure the purchase of 350 million doses of the Company’s prototype vaccine from the Company as required by the Gavi APA. As of November 18, 2022, the Company had only received orders under the Gavi APA for approximately 2 million doses. On December 2, 2022, Gavi issued a written notice purporting to terminate the Gavi APA based on Gavi’s contention that the Company repudiated the agreement and, therefore, materially breached the Gavi APA. Gavi also contends that, based on its purported termination of the Gavi APA, it is entitled to a refund of the Advance Payment Amount less any amounts that have been credited against the purchase price for binding orders placed by a buyer participating in the COVAX Facility. Since December 31, 2022, the remaining Gavi Advance Payment Amount, which is $696.4 million as of September 30, 2023, pending resolution of the dispute with Gavi related to a return of the remaining Advance Payment Amount, has been classified within Other current liabilities in the Company’s consolidated balance sheet. On January 24, 2023, Gavi filed a demand for arbitration with the International Court of Arbitration based on the claims described above. The Company filed its Answer and Counterclaims on March 2, 2023. On April 5, 2023, Gavi filed its Reply to the Company’s Counterclaims. The arbitration hearing is scheduled for July 2024, with a written decision to follow. Arbitration is inherently uncertain, and while the Company believes that it is entitled to retain the remaining Advance Payment Amount received from Gavi, it is possible that it could be required to refund all or a portion of the remaining Advance Payment Amount from Gavi.

10

Product Sales

Product sales by the Company’s customer’s geographic location was as follows (in thousands):

| Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | |||||||||||||||||

North America | $ | $ | $ | $ | ||||||||||||||||

| Europe | ||||||||||||||||||||

Rest of the world | ||||||||||||||||||||

| Total product sales revenue | $ | $ | $ | $ | ||||||||||||||||

In May 2023, the Company extended a credit for certain doses delivered in 2022 that qualified for replacement under the contract with the Australian government. This credit is the result of a single lot sold to the Australian government that upon pre-planned 6-month stability testing was found to have fallen below the defined specifications and the lot therefore was removed from the market. The credit will be applied against the future sale of doses to the customer and, during the nine months ended September 30, 2023, the Company recorded a reduction of $64.7 million in product sales, with a corresponding increase to Deferred revenue, non-current.

In April 2023, the Company amended the Canada APA to forfeit certain doses originally scheduled for delivery in 2022 for a payment of $100.4 million received in the second quarter of 2023. On June 30, 2023, the Company entered into an additional amendment (the “June 2023 Amendment”) to the Canada APA. Pursuant to the June 2023 Amendment, the parties revised the Canadian government’s previous commitment by (i) forfeiting certain doses of COVID-19 Vaccine previously scheduled for delivery, (ii) reducing the amount of doses of COVID-19 Vaccine due for delivery, (iii) revising the delivery schedule for the remaining doses of COVID-19 Vaccine to be delivered, and (iv) requiring use of the Biologics Manufacturing Centre (“BMC”) Inc. to produce bulk antigen for doses in 2024 and 2025. In connection with the forfeiture of doses of COVID-19 Vaccine, the Canadian government agreed to pay a total amount of $349.6 million to the Company in two equal installments in 2023, which total amount equals the remaining balance owed by the Canadian government with respect to such forfeited vaccine doses. The first installment was payable upon execution of the June 2023 Amendment and the second installment is contingent and payable upon the Company’s delivery of vaccine doses in the second half of 2023. The first installment of $174.8 million was received from the Canadian government in July 2023. If the Company fails to deliver COVID-19 Vaccine doses to the Canadian government in the fourth quarter of 2023, the second installment payment of $174.8 million will be terminated and not be payable to the Company. The Canadian government may terminate the Canada APA, as amended, if the Company fails to achieve regulatory approval for use of BMC for COVID-19 Vaccine production on or before December 31, 2024. The June 2023 Amendment maintained the total contract value of the original Canada APA. Pursuant to the June 2023 Amendment, the Company and the Canadian government will endeavor to expand the Company’s previously agreed in-country commitment to Canada and to further partner to provide health, economic, and future pandemic preparedness benefits to Canada, which value may be provided through a number of activities, including without limitation, capital investments, the performance of activities or services, or the provision of technology or intellectual property licenses. Further, the parties will endeavor to enter into a memorandum of understanding (the “MOU”) to illustrate the Company’s ability to deliver such benefits over a 15 -year period with an aggregate value of not less than 100 % of the amount remaining to be paid under the June 2023 Amendment and ultimately received by the Company. As of September 30, 2023, the Company is in the process of negotiating the MOU. The Company agreed to hold $20.0 million in escrow for the benefit of the Canadian government, which amount is the sole recourse available to the Canadian government in the event of non-performance under the MOU.

Grants

The Company’s U.S. government agreement consists of a Project Agreement (the “Project Agreement”) and a Base Agreement with Advanced Technology International, the Consortium Management Firm acting on behalf of the Medical CBRN Defense Consortium in connection with the partnership formerly known as Operation Warp Speed (the Base Agreement together with the Project Agreement the “USG Agreement”). In February 2023, in connection with the execution of Modification 17 to the Project Agreement (“Modification 17”), the U.S. government indicated to the Company that the award may not be extended past its current period of performance, which is December 31, 2023. Also, Modification 17 included provisions requiring that the payment of up to $60.0 million of consideration associated with manufacturing work now be contingent upon meeting certain milestones, including the delivery of up to 1.5 million doses of its prototype vaccine and

11

development and regulatory milestones related to commercial readiness, expansion of the EUA and development of multiple vial presentations. As of September 30, 2023, the Company now expects to be entitled to the full $1.8 billion-funding under the USG Agreement by December 31, 2023, and accordingly, the Company recognized a $43.8 million cumulative increase to grant revenue under the contract during the three months ended September 30, 2023.

Royalties and Other

Royalties and other includes royalty milestone payments, sales-based royalties, and Matrix-M™ adjuvant sales.

During the three and nine months ended September 30, 2023, the Company recognized $6.0 13.8 million and $17.0 million, respectively in revenue related to a Matrix-M™ adjuvant sales. During the three and nine months ended September 30, 2023, the Company did no

During the three and nine months ended September 30, 2022, the Company recognized no revenue and $20.0 million, respectively, related to milestone payments, $1.3 million and $10.5 million, respectively, related to sales-based royalties, and $1.0 million and $13.4 million, respectively, related to a Matrix-M™ adjuvant sales.

Note 4 – Collaboration, License, and Supply Agreements

SIIPL

The Company previously granted SIIPL exclusive and non-exclusive licenses for the development, co-formulation, filling and finishing, registration, and commercialization of its prototype vaccine, its proprietary COVID-19 variant antigen candidate(s), its quadrivalent influenza vaccine candidate, and its CIC vaccine candidate. SIIPL agreed to purchase the Company's Matrix-M™ adjuvant and the Company granted SIIPL a non-exclusive license to manufacture the antigen drug substance component of the Company’s COVID-19 Vaccine in SIIPL’s licensed territory solely for use in the manufacture of COVID-19 Vaccine. The Company and SIIPL equally split the revenue from SIIPL’s sale of COVID-19 Vaccine in its licensed territory, net of agreed costs. The Company also has a supply agreement with SIIPL and SLS under which SIIPL and SLS supply the Company with prototype vaccine, its proprietary COVID-19 variant antigen candidate(s), its quadrivalent influenza vaccine candidate, and its CIC vaccine candidate for commercialization and sale in certain territories, as well as a contract development manufacture agreement with SLS, under which SLS manufactures and supplies finished vaccine product to the Company using antigen drug substance and Matrix-M™ adjuvant supplied by the Company. In March 2020, the Company entered into an agreement with SIIPL that granted SIIPL a non-exclusive license for the use of Matrix-M™ adjuvant supplied by the Company to develop, manufacture, and commercialize R21, a malaria candidate developed by the Jenner Institute, University of Oxford (“R21/Malaria”). Under the agreement, SIIPL purchases the Company's Matrix-M™ adjuvant for use in development activities at cost and for commercial purposes at a tiered commercial supply price, and pays a royalty in the single-to low- double-digit range based on vaccine sales for a period of 15 years after the first commercial sale of the vaccine in each country.

Takeda Pharmaceutical Company Limited

The Company has a collaboration and license agreement with Takeda Pharmaceutical Company Limited (“Takeda”) under which the Company granted Takeda an exclusive license to develop, manufacture, and commercialize the Company’s COVID-19 Vaccine in Japan. Under the agreement, Takeda purchases Matrix-M™ adjuvant from the Company to manufacture doses of COVID-19 Vaccine, and the Company is entitled to receive milestone and sales-based royalty payments from Takeda based on the achievement of certain development and commercial milestones, as well as a portion of net profits from the sale of COVID-19 Vaccine. In September 2021, Takeda finalized an agreement with the Government of Japan’s Ministry of Health, Labour and Welfare ("MHLW") for the purchase of 150 million doses of its prototype vaccine. In February 2023, MHLW canceled the remainder of doses under its agreement with Takeda. As a result, it is uncertain whether the Company will receive future sales-based royalty payments from Takeda under the terms and conditions of their current collaboration and licensing agreement.

Bill & Melinda Gates Medical Research Institute

In May 2023, the Company entered into a 3-year agreement with the Bill & Melinda Gates Medical Research Institute

12

to provide the Company’s Matrix-M™ adjuvant for use in preclinical vaccine research.

SK bioscience, Co., Ltd

In February 2021, the Company entered into a Collaboration and License Agreement (“CLA”) with SK bioscience, Co., Ltd. (“SK”) to manufacture and commercialize its prototype vaccine for sale to the government of South Korea. The CLA was amended in December 2021 and July 2022 to include the sale of its prototype vaccine to Thailand and Vietnam and to supply the Company with the antigen component of prototype vaccine for use in the final drug product globally, including product to be distributed by the COVAX Facility. Under the CLA, as amended, SK agreed to pay the Company a royalty on the sale of its prototype vaccine in the low to middle double-digit range. The CLA was in addition to the Company's existing manufacturing arrangement with SK under a Development and Supply Agreement (“DSA”) entered into in August 2020. In July 2022, the Company signed an additional agreement with SK for the technology transfer of the Company’s proprietary COVID-19 variant antigen materials so that SK can manufacture the drug substance targeting COVID-19 variants, including the Omicron subvariants. The companies also signed an agreement to manufacture and supply its prototype vaccine in a prefilled syringe.

In June 2023, the Company entered into a material transfer agreement with SK for the use by SK of the Company’s Matrix-M™ adjuvant in preclinical vaccine experiments for shingles, influenza, and pan-COVID-19.

In August 2023, the Company and SK entered into a Settlement Agreement and General Release (the “Settlement Agreement”) regarding mutual release by the parties of all claims arising from or in relation to statements of work (“SOWs”) canceled by the Company under the DSA and the CLA (collectively the “Business Agreements”), and other SOWs under the Business Agreements (collectively, the “Subject SOWs”), in each case, in connection with the cessation of all drug substance and drug product manufacturing activity at SK for supply to the Company. Subject SOWs canceled by the Company under the Settlement Agreement included (i) Statement of Work No. 1 dated as of December 23, 2021 as amended to date under the CLA; (ii) Statement of Work No. 5 dated as of July 18, 2022 under the DSA; and (iii) Statement of Work No. 6 dated as of July 18, 2022, and as amended as of December 28, 2022 under the DSA.

Pursuant to the Settlement Agreement, the Company is responsible for payment of $149.8 million to SK in connection with the cancellation of manufacturing activity for the SOWs under the Business Agreements, of which (i) $130.4 million was paid in August 2023 and (ii) the remaining balance is to be paid on or before November 15, 2023. Under the Settlement Agreement, the Company and SK agreed to a wind down plan with respect to the remaining products, materials and equipment under the SOWs.

Under the Settlement Agreement, the Company and SK agreed to remove certain restrictions under the CLA that have been triggered by the launch of SK’s competing vaccine SKYCovione™ in the Republic of Korea. In addition, the Company agreed to extend the term of an exclusive license to SK under the CLA for the exploitation of antigen and vaccine products utilizing Company’s proprietary coronavirus vaccine antigens and Matrix-M adjuvant in certain territories. The Company recorded $4.0 million to Deferred revenue related to the extended licenses granted to SK under the Settlement Agreement.

In August 2023, the Company also entered into a Securities Subscription Agreement (the “Subscription Agreement”) with SK, pursuant to which the Company agreed to sell and issue to SK, in a private placement (the “Private Placement”), 6.5 million shares of the Company’s common stock, par value $0.01 per share (the “Shares”) at a price of $13.00 per share for aggregate gross proceeds to the Company of approximately $84.5 million. The closing of the Private Placement occurred on August 10, 2023. The fair value of the Company’s common stock on the date of closing, based on the quoted market price, was $46.5 million, which results in a premium paid by SK of approximately $38.0 million.

The Settlement Agreement and the Subscription Agreement were negotiated concurrently between the parties, and therefore were combined for accounting purposes and analyzed as a single arrangement. As a result, the Company recorded the $46.5 million fair value of common stock issued to SK, based on the quoted market price on the date of close, as an equity transaction. The remaining elements of the arrangement were deemed to relate to the settlement of the Company’s outstanding liabilities due to SK. These elements consist primarily of the cash payable to SK of $149.8 million, offset by the premium paid on the common stock purchase by SK of $38.0 million, which resulted in a net gain upon derecognition of the liabilities due to SK of $79.2 79.2 57.7 21.5 million, proportionally based on the where the underlying costs were originally recorded.

13

Other Supply Agreements

On September 30, 2022, the Company, FUJIFILM Diosynth Biotechnologies UK Limited (“FDBK”), FUJIFILM Diosynth Biotechnologies Texas, LLC (“FDBT”), and FUJIFILM Diosynth Biotechnologies USA, Inc. (“FDBU” and together with FDBK and FDBT, “Fujifilm”) entered into a Confidential Settlement Agreement and Release (the “Fujifilm Settlement Agreement”) regarding amounts due to Fujifilm in connection with the termination of manufacturing activity at FDBT under the Commercial Supply Agreement (the “CSA”) dated August 20, 2021 and Master Services Agreement dated June 30, 2020 and associated statements of work (the “MSA”) by and between the Company and Fujifilm. The MSA and CSA established the general terms and conditions applicable to Fujifilm’s manufacturing and supply activities related to the Company’s prototype vaccine under the associated statements of work.

Pursuant to the Fujifilm Settlement Agreement, the Company agreed to pay up to $185.0 million (the “Settlement Payment”) to Fujifilm in connection with cancellation of manufacturing activity at FDBT under the CSA, of which (i) $47.8 million, constituting the initial reservation fee under the CSA, was credited against the Settlement Payment on September 30, 2022 and (ii) the remaining balance is to be paid in four equal quarterly installments of $34.3 million each, which began on March 31, 2023. As of September 30, 2023, the remaining payment of $68.6 million was reflected in Accrued expenses. Under the Fujifilm Settlement Agreement, the final two quarterly installments due to Fujifilm were subject to Fujifilm’s obligation to use commercially reasonable efforts to mitigate losses associated with the vacant manufacturing capacity caused by the termination of manufacturing activities at FDBT under the CSA. Any replacement revenue achieved by Fujifilm’s mitigation efforts between July 1, 2023 and December 31, 2023 would offset the final two settlement payments owed by the Company. On October 2, 2023, the Company sent a notice of breach under the Fujifilm Settlement Agreement to Fujifilm setting forth the Company’s position that Fujifilm had not used commercially reasonable efforts to mitigate losses. The Company withheld the $34.3 million installment payment due to Fujifilm on September 30, 2023, pending resolution of the issues identified in the notice of breach. On October 30, 2023, FDBT filed a demand for arbitration with Judicial Arbitration and Mediation Services (“JAMS”) seeking payment of the third quarter installment of the Settlement Payment.

The Company continues to assess its manufacturing needs and intends to modify its global manufacturing footprint consistent with its contractual obligations to supply, and anticipated demand for, its COVID-19 Program, and in doing so, recognizes that significant costs may be incurred.

Note 5 – Cash, Cash Equivalents, and Restricted Cash

The following table provides a reconciliation of cash, cash equivalents, and restricted cash reported in the consolidated balance sheets that sums to the total of such amounts shown in the consolidated statements of cash flows (in thousands):

| September 30, 2023 | December 31, 2022 | ||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

| Restricted cash, current | |||||||||||

Restricted cash, non-current(1) | |||||||||||

| Cash, cash equivalents, and restricted cash | $ | $ | |||||||||

(1)Classified as Other non-current assets as of September 30, 2023 and December 31, 2022, on the consolidated balance sheets.

14

Note 6 – Fair Value Measurements

The following table represents the Company’s fair value hierarchy for its financial assets and liabilities (in thousands):

| Fair Value at September 30, 2023 | Fair Value at December 31, 2022 | ||||||||||||||||||||||||||||||||||

| Assets | Level 1 | Level 2 | Level 3 | Level 1 | Level 2 | Level 3 | |||||||||||||||||||||||||||||

Money market funds(1) | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||

Government-backed securities(1) | |||||||||||||||||||||||||||||||||||

Treasury securities(1) | |||||||||||||||||||||||||||||||||||

Corporate debt securities(1) | |||||||||||||||||||||||||||||||||||

Agency securities(1) | |||||||||||||||||||||||||||||||||||

| Total cash equivalents | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||

| Liabilities | |||||||||||||||||||||||||||||||||||

| $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||||||||||

| Total convertible notes payable | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||

Fixed-income investments categorized as Level 2 are valued at the custodian bank by a third-party pricing vendor’s valuation models that use verifiable observable market data, such as interest rates and yield curves observable at commonly quoted intervals and credit spreads, bids provided by brokers or dealers, or quoted prices of securities with similar characteristics. Pricing of the Company’s convertible notes has been estimated using observable inputs, including the price of the Company’s common stock, implied volatility, interest rates, and credit spreads.

During the nine months ended September 30, 2023 and 2022, the Company did not have any transfers between levels.

The amount in the Company’s consolidated balance sheets for accounts payable and accrued expenses approximates its fair value due to its short-term nature.

Note 7 – Inventory

Inventory consisted of the following (in thousands):

| September 30, 2023 | December 31, 2022 | ||||||||||

| Raw materials | $ | $ | |||||||||

| Semi-finished goods | |||||||||||

| Finished goods | |||||||||||

| Total inventory | $ | $ | |||||||||

Note 8 – Goodwill

15

2022. The change in the carrying amounts of goodwill for the nine months ended September 30, 2023 was as follows (in thousands):

| Amount | |||||

| Balance at December 31, 2022 | $ | ||||

| Currency translation adjustments | ( | ||||

| Balance at September 30, 2023 | $ | ||||

Note 9 – Leases

The Company has embedded leases related to supply agreements with contract manufacturing organizations (“CMOs”) and contract manufacturing and development organizations to manufacture its COVID-19 Vaccine, as well as leases for its research and development and manufacturing facilities, corporate headquarters and offices, and certain equipment. During the nine months ended September 30, 2023, the Company continued to align its global manufacturing footprint as a result of its ongoing assessment of manufacturing needs consistent with its contractual obligations related to the supply, and anticipated demand for, its COVID-19 Program.

During the three and nine months ended September 30, 2023, the Company recognized a short-term lease benefit of $39.5 million and $48.0 million, respectively, related to the reversal of previously recognized embedded lease expense on the settlement of CMO contracts. During the three and nine months ended September 30, 2022, the Company recognized a short-term lease benefit of $46.6 million and expense of $37.3 million respectively, related to its embedded leases and expensed $24.2 million and $44.0 million respectively, for the write off of right of use (“ROU”) assets that represented assets acquired for research and development activities that did not have an alternative future use at the commencement or modification of the lease ROU written off. There were no ROU assets written off during the three and nine months ended September 30, 2023, related to embedded leases.

During the three and nine months ended September 30, 2023, the Company recognized $0.5 million and $1.4 million of interest expense, respectively, on its finance lease liabilities. During the three and nine months ended September 30, 2022, the Company recognized $0.9 million and $4.3 million of interest expense, respectively, on its finance lease liabilities.

During the nine months ended September 30, 2023, the Company recorded an impairment charge of $5.9 million related to ROU facility leases used for research and development, manufacturing and offices space that are impacted by the Restructuring Plan (see Note 15).

16

Note 10 – Long-Term Debt

Total convertible notes payable consisted of the following (in thousands):

| September 30, 2023 | December 31, 2022 | ||||||||||

| Current portion: | |||||||||||

| $ | $ | ||||||||||

| Unamortized debt issuance costs | ( | ||||||||||

| Total current convertible notes payable | $ | $ | |||||||||

| Non-current portion: | |||||||||||

| $ | $ | ||||||||||

Unamortized debt issuance costs | ( | ( | |||||||||

| Total non-current convertible notes payable | $ | $ | |||||||||

In February 2023, the Company repaid the outstanding principal amount of $325.0 million on its 3.75 % Convertible notes due in 2023, together with accrued but unpaid interest on the maturity date. The repayment was funded by the issuance of the 5.00 % Convertible notes due 2027 and the concurrent common stock offering in December 2022, as well as cash on hand. The effective interest rate of the 2027 Convertible notes is 6.2 %.

The interest expense incurred in connection with the convertible notes payable consisted of the following (in thousands):

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | ||||||||||||||||||||

| Coupon interest | $ | $ | $ | $ | |||||||||||||||||||

| Amortization of debt issuance costs | |||||||||||||||||||||||

| Total interest expense on convertible notes payable | $ | $ | $ | $ | |||||||||||||||||||

Note 11 – Stockholders' Deficit

In August 2023, the Company entered into an At Market Issuance Sales Agreement (the "August 2023 Sales Agreement"), which allows it to issue and sell up to $500 million in gross proceeds of shares of its common stock, and terminated its then-existing At Market Issuance Sales agreement entered in June 2021 (the “June 2021 Sales Agreement”). During the three months ended September 30, 2023, the Company sold 17.8 million shares of its common stock under its August 2023 Sales Agreement resulting in net proceeds of approximately $143 million. During the nine months ended September 30, 2023, the Company sold 25.7 million shares of its common stock under its June 2021 and August 2023 Sales Agreement resulting in net proceeds of approximately $211 million. As of September 30, 2023, the remaining balance available under the August 2023 Sales Agreement was approximately $354 million.

During the nine months ended September 30, 2022, the Company sold 2.2 million shares of its common stock resulting in net proceeds of approximately $179 million, under its June 2021 Sales Agreement. There was no sale of shares of common stock recorded during the three months ended September 30, 2022.

In August 2023, pursuant to the Securities Subscription Agreement with SK, the Company agreed to sell and issue to SK 6.5 million shares of the Company’s common stock, par value $0.01 per share at a price of $13.00 per share (the “Shares”) in a Private Placement for aggregate gross proceeds to the Company of approximately $84.5 million. The Company recognized the Shares at the settlement date fair value of $46.5 million (see Note 4 for additional discussion of the Securities Subscription Agreement with SK). The closing of the Private Placement occurred on August 10, 2023.

17

Note 12 – Stock-Based Compensation

Equity Plans

In January 2023, the Company established the 2023 Inducement Plan (the “2023 Inducement Plan”), which provides for the granting of share-based awards to individuals who were not previously employees, or following a bona fide period of non-employment, as an inducement material to such individuals entering into employment with the Company. The Company reserved 1.0 million shares of common stock for grants under the 2023 Inducement Plan. As of September 30, 2023, there were 0.2 million shares available for issuance under the 2023 Inducement Plan.

The 2015 Stock Incentive Plan, as amended (“2015 Plan”), was approved at the Company’s annual meeting of stockholders in June 2015. Under the 2015 Plan, equity awards may be granted to officers, directors, employees, and consultants of and advisors to the Company and any present or future subsidiary. The 2015 Plan authorizes the issuance of up to 21.0 million shares of common stock under equity awards granted under the 2015 Plan, which includes an increase of 6.2 million shares approved for issuance under the 2015 Plan at the Company's 2023 annual meeting of stockholders. All such shares authorized for issuance under the 2015 Plan have been reserved. The 2015 Plan will expire on March 4, 2025. As of September 30, 2023, there were 7.1 million shares available for issuance under the 2015 Plan.

The Amended and Restated 2005 Stock Incentive Plan (“2005 Plan”) expired in February 2015 and no new awards may be made under such plan, although awards will continue to be outstanding in accordance with their terms.

The 2023 Inducement Plan and the 2015 Plan permit, and the 2005 Plan permitted, the grant of stock options (including incentive stock options), restricted stock, stock appreciation rights (“SARs”), and restricted stock units (“RSUs”). In addition, under the 2023 Inducement Plan and the 2015 Plan, unrestricted stock, stock units, and performance awards may be granted. Stock options and SARs generally have a maximum term of ten years and may be or were granted with an exercise price that is no less than 100 % of the fair market value of the Company’s common stock at the time of grant. Grants of share-based awards are generally subject to vesting over periods ranging from to four years .

The Company recorded stock-based compensation expense in the consolidated statements of operations as follows (in thousands):

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | ||||||||||||||||||||

| Cost of sales | $ | $ | $ | $ | |||||||||||||||||||

| Research and development | |||||||||||||||||||||||

| Selling, general, and administrative | |||||||||||||||||||||||

| Total stock-based compensation expense | $ | $ | $ | $ | |||||||||||||||||||

During the three and nine months ended September 30, 2023, total stock-based compensation capitalized in inventory was $0.5 1.7

As of September 30, 2023, there was approximately $102 million of total unrecognized compensation expense related to unvested stock options, SARs, RSUs, and the Company’s Employee Stock Purchase Plan, as amended (“ESPP”). This unrecognized non-cash compensation expense is expected to be recognized over a weighted-average period of approximately one year . This estimate does not include the impact of other possible stock-based awards that may be made during future periods.

The aggregate intrinsic value represents the total intrinsic value (the difference between the Company’s closing stock price on the last trading day of the period and the exercise price, multiplied by the number of in-the-money stock options and SARs) that would have been received by the holders had all stock option and SAR holders exercised their stock options and SARs on September 30, 2023. This amount is subject to change based on changes to the closing price of the Company's common stock. The aggregate intrinsic value of stock options and SARs exercises and vesting of RSUs for the nine months ended September 30, 2023 and 2022 was approximately $3 million and $19 million, respectively.

18

Stock Options and Stock Appreciation Rights

The following is a summary of stock options and SARs activity under the 2023 Inducement Plan, 2015 Plan, and 2005 Plan for the nine months ended September 30, 2023:

| 2023 Inducement Plan | 2015 Plan | 2005 Plan | |||||||||||||||||||||||||||||||||

| Stock Options | Weighted-Average Exercise Price | Stock Options | Weighted-Average Exercise Price | Stock Options | Weighted-Average Exercise Price | ||||||||||||||||||||||||||||||

| Outstanding at December 31, 2022 | $ | $ | $ | ||||||||||||||||||||||||||||||||

| Granted | |||||||||||||||||||||||||||||||||||

| Exercised | ( | ||||||||||||||||||||||||||||||||||

| Canceled | ( | ( | |||||||||||||||||||||||||||||||||

| Outstanding at September 30, 2023 | $ | $ | $ | ||||||||||||||||||||||||||||||||

| Shares exercisable at September 30, 2023 | $ | $ | $ | ||||||||||||||||||||||||||||||||

The fair value of stock options granted under the 2023 Inducement Plan and the 2015 Plan was estimated at the date of grant using the Black-Scholes option-pricing model with the following assumptions:

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | ||||||||||||||||||||

| Weighted average Black-Scholes fair value of stock options granted | $ | $ | $ | $ | |||||||||||||||||||

| Risk-free interest rate | |||||||||||||||||||||||

| Dividend yield | |||||||||||||||||||||||

| Volatility | |||||||||||||||||||||||

| Expected term (in years) | |||||||||||||||||||||||

The total aggregate intrinsic value and weighted-average remaining contractual term of stock options and SARs outstanding under the 2023 Inducement Plan, 2015 Plan and 2005 Plan as of September 30, 2023 was approximately $1.4 million and 7.1 years, respectively. The total aggregate intrinsic value and weighted-average remaining contractual term of stock options and SARs exercisable under the 2023 Inducement Plan, 2015 Plan and 2005 Plan as of September 30, 2023 was approximately $1.1 million and 6.1 years, respectively.

Restricted Stock Units

The following is a summary of RSU activity for the nine months ended September 30, 2023:

| 2023 Inducement Plan | 2015 Plan | ||||||||||||||||||||||

| Number of Shares | Per Share Weighted- Average Fair Value | Number of Shares | Per Share Weighted- Average Fair Value | ||||||||||||||||||||

| Outstanding and unvested at December 31, 2022 | $ | $ | |||||||||||||||||||||

| Granted | |||||||||||||||||||||||

| Vested | ( | ||||||||||||||||||||||

| Forfeited | ( | ||||||||||||||||||||||

| Outstanding and unvested at September 30, 2023 | $ | $ | |||||||||||||||||||||

19

Employee Stock Purchase Plan

The ESPP was approved at the Company’s annual meeting of stockholders in June 2013. The ESPP currently authorized an aggregate of 1.2 million shares of common stock to be purchased, and the aggregate amount of shares will continue to increase 5 % on each anniversary of its adoption up to a maximum of 1.65 million shares. The ESPP allows employees to purchase shares of common stock of the Company at each purchase date through payroll deductions of up to a maximum of 15 % of their compensation, at 85 % of the lesser of the market price of the shares at the time of purchase or the market price on the beginning date of an option period (or, if later, the date during the option period when the employee was first eligible to participate). As of September 30, 2023, there were 0.5 million shares available for issuance under the ESPP.

Note 13 – Income Taxes

The Company evaluates the available positive and negative evidence to estimate whether sufficient future taxable income will be generated to permit use of the existing deferred tax assets. A significant piece of objective evidence evaluated was the cumulative loss incurred over the three-year period ended September 30, 2023 and that the Company has historically generated pretax losses. Such objective evidence limits the ability to consider other subjective evidence, such as projections for future growth. On the basis of this evaluation, as of September 30, 2023, the Company continued to maintain a full valuation allowance against its deferred tax assets, except to the extent Net Operating Losses (“NOLs”) have been used to reduce taxable income. The Company’s remaining U.S. Federal NOLs are subject to limitation in accordance with the 2017 Tax Cuts and Jobs Act (“TCJA”), which limits allowable NOL deductions to 80% of federal taxable income.

Effective January 1, 2022, a provision of the TCJA has taken effect creating a significant change to the treatment of research and experimental expenditures under Section 174 of the IRC (“Sec. 174 expenses”). Historically, businesses have had the option of deducting Sec. 174 expenses in the year incurred or capitalizing and amortizing the costs over five years. The new TCJA provision, however, eliminates this option and will require Sec. 174 expenses associated with research conducted in the U.S. to be capitalized and amortized over a five-year period. For expenses associated with research outside of the U.S., Sec. 174 expenses will be capitalized and amortized over a 15-year period.

Note 14 – Commitments and Contingencies

Legal Matters

Stockholder Litigation

On November 12, 2021, Sothinathan Sinnathurai filed a purported securities class action in the U.S. District Court for the District of Maryland (the “Maryland Court”) against the Company and certain members of senior management, captioned Sothinathan Sinnathurai v. Novavax, Inc., et al., No. 8:21-cv-02910-TDC (the “Sinnathurai Action”). On January 26, 2022, the Maryland Court entered an order designating David Truong, Nuggehalli Balmukund Nandkumar, and Jeffrey Gabbert as co-lead plaintiffs in the Sinnathurai Action. The co-lead plaintiffs filed a consolidated amended complaint on March 11, 2022, alleging that the defendants made certain purportedly false and misleading statements concerning the Company’s ability to manufacture prototype vaccine on a commercial scale and to secure the prototype vaccine’s regulatory approval. The amended complaint defines the purported class as those stockholders who purchased the Company’s securities between February 24, 2021 and October 19, 2021. On April 25, 2022, the defendants filed a motion to dismiss the consolidated amended complaint. On December 12, 2022, the Maryland Court issued a ruling granting in part and denying in part defendants’ motion to dismiss. The Maryland Court dismissed all claims against two individual defendants and claims based on certain public statements challenged in the consolidated amended complaint. The Maryland Court denied the motion to dismiss as to the remaining claims and defendants, and directed the Company and other remaining defendants to answer within fourteen days . On December 27, 2022, the Company filed its answer and affirmative defenses. On March 16, 2023, the plaintiffs filed a motion for class certification and to appoint class representatives and counsel. The Company filed its opposition to the plaintiffs’ motion on September 22, 2023.

20

After the Sinnathurai Action was filed, eight derivative lawsuits were filed: (i) Robert E. Meyer v. Stanley C. Erck, et al., No. 8:21-cv-02996-TDC (the “Meyer Action”), (ii) Shui Shing Yung v. Stanley C. Erck, et al., No. 8:21-cv-03248-TDC (the “Yung Action”), (iii) William Kirst, et al. v. Stanley C. Erck, et al., No. C-15-CV-21-000618 (the “Kirst Action”), (iv) Amy Snyder v. Stanley C. Erck, et al., No. 8:22-cv-01415-TDC (the “Snyder Action”), (v) Charles R. Blackburn, et al. v. Stanley C. Erck, et al., No. 1:22-cv-01417-TDC (the “Blackburn Action”), (vi) Diego J. Mesa v. Stanley C. Erck, et al., No. 2022-0770-NAC (the “Mesa Action”), (vii) Sean Acosta v. Stanley C. Erck, et al., No. 2022-1133-NAC (the “Acosta Action”), and (viii) Jared Needelman v. Stanley C. Erck, et al., No. C-15-CV-23-001550 (the “Needelman Action”). The Meyer, Yung, Snyder, and Blackburn Actions were filed in the Maryland Court. The Kirst Action was filed in the Circuit Court for Montgomery County, Maryland, and shortly thereafter removed to the Maryland Court by the defendants. The Needleman Action was also filed in the Circuit Court for Montgomery County, Maryland. The Mesa and Acosta Actions were filed in the Delaware Court of Chancery (the “Delaware Court”). The derivative lawsuits name members of the Company’s board of directors and certain members of senior management as defendants. The Company is deemed a nominal defendant. The plaintiffs assert derivative claims arising out of substantially the same alleged facts and circumstances as the Sinnathurai Action. Collectively, the derivative complaints assert claims for breach of fiduciary duty, insider selling, unjust enrichment, violation of federal securities law, abuse of control, waste, and mismanagement. Plaintiffs seek declaratory and injunctive relief, as well as an award of monetary damages and attorneys’ fees.

On February 7, 2022, the Maryland Court entered an order consolidating the Meyer and Yung Actions (the “First Consolidated Derivative Action”). The plaintiffs in the First Consolidated Derivative Action filed their consolidated derivative complaint on April 25, 2022. On May 10, 2022, the Maryland Court entered an order granting the parties’ request to stay all proceedings and deadlines pending the earlier of dismissal or the filing of an answer in the Sinnathurai Action. On June 10, 2022, the Snyder and Blackburn Actions were filed. On October 5, 2022, the Maryland Court entered an order granting a request by the plaintiffs in the First Consolidated Derivative Action and the Snyder and Blackburn Actions to consolidate all three actions and appoint co-lead plaintiffs and co-lead and liaison counsel (the “Second Consolidated Derivative Action”). The co-lead plaintiffs in the Second Consolidated Derivative Action filed a consolidated amended complaint on November 21, 2022. On February 10, 2023, defendants filed a motion to dismiss the Second Consolidated Derivative Action. The plaintiffs filed their opposition to the motion to dismiss on April 11, 2023. Defendants filed their reply brief in further support of their motion to dismiss on May 11, 2023. On August 21, 2023, the court entered an order granting in part and denying in part the motion to dismiss. On September 5, 2023, the Company filed an Answer to the consolidated amended complaint. On September 6, 2023, the court entered an order granting the individual defendants an extension of time to file their answer until November 6, 2023. On October 6, 2023, the Board of Directors of the Company formed a Special Litigation Committee (“SLC”) with full and exclusive power and authority of the Board to, among other things, investigate, review, and analyze the facts and circumstances surrounding the claims asserted in the pending derivative actions, including the claims that remain following the court’s order on the motion to dismiss in the Second Consolidated Derivative Action. On November 7, 2023, the court entered an order granting the parties’ request to stay the Second Consolidated Derivative Action for up to six months from the date of entry of the order. This includes staying the deadline for the individual defendants to respond to the consolidated amended complaint.

On July 21, 2022, the Maryland Court issued a memorandum opinion and order remanding the Kirst Action to state court. On December 6, 2022, the parties to the Kirst Action filed a stipulated schedule pursuant to which the plaintiffs were expected to file an amended complaint on December 22, 2022, and either (i) the parties would file a stipulated stay of the Kirst Action or (ii) the defendants would file a motion to stay the case by January 23, 2023. The plaintiffs filed an amended complaint on December 30, 2022. On January 23, 2023, defendants filed a motion to stay the Kirst action. On February 22, 2023, the parties in the Kirst Action filed for the Court’s approval of a stipulation staying the Kirst Action pending the resolution of defendants’ motion to dismiss in the Second Consolidated Derivative Action. On March 22, 2023, the Court entered an order staying the Kirst Action pending resolution of the motion to dismiss in the Second Consolidated Derivative Action. The parties continue to discuss next steps in the litigation following the Maryland Court’s ruling on the motion to dismiss the Second Consolidated Derivative Action.

On August 30, 2022, the Mesa Action was filed. On October 3, 2022, the Delaware Court entered an order granting the parties’ request to stay all proceedings and deadlines in the Mesa Action pending the earlier of dismissal of the Sinnathurai Action or the filing of an answer to the operative complaint in the Sinnathurai Action. On January 9, 2023, following the ruling on the motion to dismiss the Sinnathurai Action, the Delaware Court entered an order granting the Mesa Action parties’ request to set a briefing schedule in connection with a motion to stay by defendants. On February 28, 2023, the court granted the defendants’ motion and stayed the Mesa Action pending the entry of a final, non-appealable judgment in the Second Consolidated Derivative Action. On August 31, 2023, the Mesa plaintiffs filed a motion to lift the stay in the Mesa Action. On October 6, 2023, the Company filed an opposition to plaintiff’s motion to lift the stay. On October 17, 2023, the Mesa plaintiff filed his reply in further support of his motion to lift the stay.

21