UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form

(Mark One)

|

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended

or

|

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number

DEVON ENERGY CORPORATION

(Exact name of registrant as specified in its charter)

|

|

|

|

|

(State or other jurisdiction of incorporation or organization) |

|

(I.R.S. Employer identification No.) |

|

|

|

|

|

|

|

|

|

(Address of principal executive offices) |

|

(Zip code) |

Registrant’s telephone number, including area code: (

Securities registered pursuant to Section 12(b) of the Act:

|

|

Title of each class |

|

Trading Symbol |

|

Name of each exchange on which registered |

|

|

|

|

|

|

|

|

|

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

|

|

☑ |

Accelerated filer |

|

☐ |

Non-accelerated filer |

|

☐ |

|

Smaller reporting company |

|

|

Emerging growth company |

|

|

|

|

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes

The aggregate market value of the voting common stock held by non-affiliates of the registrant as of June 30, 2020 was approximately $

DOCUMENTS INCORPORATED BY REFERENCE

DEVON ENERGY CORPORATION

FORM 10-K

TABLE OF CONTENTS

2

DEFINITIONS

Unless the context otherwise indicates, references to “us,” “we,” “our,” “ours,” “Devon,” the “Company” and “Registrant” refer to Devon Energy Corporation and its consolidated subsidiaries. All monetary values, other than per unit and per share amounts, are stated in millions of U.S. dollars unless otherwise specified. In addition, the following are other abbreviations and definitions of certain terms used within this Annual Report on Form 10-K:

“2015 Plan” means the Devon Energy Corporation 2015 Long-Term Incentive Plan.

“2017 Plan” means the Devon Energy Corporation 2017 Long-Term Incentive Plan.

“ASC” means Accounting Standards Codification.

“ASU” means Accounting Standards Update.

“Bbl” or “Bbls” means barrel or barrels.

“Bcf” means billion cubic feet.

“BKV” means Banpu Kalnin Ventures.

“BLM” means the United States Bureau of Land Management.

“Boe” means barrel of oil equivalent. Gas proved reserves and production are converted to Boe, at the pressure and temperature base standard of each respective state in which the gas is produced, at the rate of six Mcf of gas per Bbl of oil, based upon the approximate relative energy content of gas and oil. Bitumen and NGL proved reserves and production are converted to Boe on a one-to-one basis with oil.

“Btu” means British thermal units, a measure of heating value.

“Canada” means the division of Devon encompassing oil and gas properties located in Canada. All dollar amounts associated with Canada are in U.S. dollars, unless stated otherwise.

“CDM” means Cotton Draw Midstream, L.L.C.

“DD&A” means depreciation, depletion and amortization expenses.

“Devon Financing” means Devon Financing Company, L.L.C.

“Devon Plan” means Devon Energy Corporation Incentive Savings Plan.

“EnLink” means EnLink Midstream Partners, LP, a master limited partnership.

“EPA” means the United States Environmental Protection Agency.

“Federal Funds Rate” means the interest rate at which depository institutions lend balances at the Federal Reserve to other depository institutions overnight.

“G&A” means general and administrative expenses.

“GAAP” means U.S. generally accepted accounting principles.

“General Partner” means EnLink Midstream, LLC, the indirect general partner entity of EnLink, and, unless the context otherwise indicates, EnLink Midstream Manager, LLC, the managing member of EnLink Midstream, LLC.

“Inside FERC” refers to the publication Inside F.E.R.C.’s Gas Market Report.

“LIBOR” means London Interbank Offered Rate.

“LOE” means lease operating expenses.

“MBbls” means thousand barrels.

“MBoe” means thousand Boe.

“Mcf” means thousand cubic feet.

“Merger” means the merger of Merger Sub with and into WPX, with WPX continuing as the surviving corporation and a wholly-owned subsidiary of the Company, pursuant to the terms of the Merger Agreement.

3

“Merger Agreement” means that certain Agreement and Plan of Merger, dated September 26, 2020, by and among the Company, Merger Sub and WPX.

“Merger Sub” means East Merger Sub, Inc., a wholly-owned subsidiary of the Company.

“MMBbls” means million barrels.

“MMBoe” means million Boe.

“MMBtu” means million Btu.

“MMcf” means million cubic feet.

“N/M” means not meaningful.

“NGL” or “NGLs” means natural gas liquids.

“NYMEX” means New York Mercantile Exchange.

“NYSE” means New York Stock Exchange.

“OPEC” means Organization of the Petroleum Exporting Countries.

“SEC” means United States Securities and Exchange Commission.

“Senior Credit Facility” means Devon’s syndicated unsecured revolving line of credit, effective as of October 5, 2018.

“Standardized measure” means the present value of after-tax future net revenues discounted at 10% per annum.

“S&P 500 Index” means Standard and Poor’s 500 index.

“TSR” means total shareholder return.

“U.S.” means United States of America.

“VIE” means variable interest entity.

“WPX” means WPX Energy, Inc.

“WTI” means West Texas Intermediate.

“/Bbl” means per barrel.

“/d” means per day.

“/MMBtu” means per MMBtu.

4

INFORMATION REGARDING FORWARD-LOOKING STATEMENTS

This report includes “forward-looking statements” as defined by the SEC. Such statements include those concerning strategic plans, our expectations and objectives for future operations, as well as other future events or conditions, and are often identified by use of the words and phrases “expects,” “believes,” “will,” “would,” “could,” “continue,” “may,” “aims,” “likely to be,” “intends,” “forecasts,” “projections,” “estimates,” “plans,” “expectations,” “targets,” “opportunities,” “potential,” “anticipates,” “outlook” and other similar terminology. All statements, other than statements of historical facts, included in this report that address activities, events or developments that Devon expects, believes or anticipates will or may occur in the future are forward-looking statements. Such statements are subject to a number of assumptions, risks and uncertainties, many of which are beyond our control. Consequently, actual future results could differ materially and adversely from our expectations due to a number of factors, including, but not limited to:

|

|

• |

the volatility of oil, gas and NGL prices; |

|

|

• |

risks relating to the COVID-19 pandemic or other future pandemics; |

|

|

• |

uncertainties inherent in estimating oil, gas and NGL reserves; |

|

|

• |

the extent to which we are successful in acquiring and discovering additional reserves; |

|

|

• |

regulatory restrictions, compliance costs and other risks relating to governmental regulation, including with respect to environmental matters; |

|

|

• |

risks related to regulatory, social and market efforts to address climate change; |

|

|

• |

the uncertainties, costs and risks involved in our operations, including as a result of employee misconduct; |

|

|

• |

risks related to our hedging activities; |

|

|

• |

counterparty credit risks; |

|

|

• |

risks relating to our indebtedness; |

|

|

• |

cyberattack risks; |

|

|

• |

our limited control over third parties who operate some of our oil and gas properties; |

|

|

• |

midstream capacity constraints and potential interruptions in production; |

|

|

• |

the extent to which insurance covers any losses we may experience; |

|

|

• |

competition for assets, materials, people and capital; |

|

|

• |

risks related to investors attempting to effect change; |

|

|

• |

our ability to successfully complete mergers, acquisitions and divestitures; |

|

|

• |

risks related to the Merger, including the risk that we may not realize the anticipated benefits of the Merger or successfully integrate the two legacy businesses; and |

|

|

• |

any of the other risks and uncertainties discussed in this report. |

The forward-looking statements included in this filing speak only as of the date of this report, represent current reasonable management’s expectations as of the date of this filing and are subject to the risks and uncertainties identified above as well as those described elsewhere in this report and in other documents we file from time to time with the SEC. We cannot guarantee the accuracy of our forward-looking statements, and readers are urged to carefully review and consider the various disclosures made in this report and in other documents we file from time to time with the SEC. All subsequent written and oral forward-looking statements attributable to Devon, or persons acting on its behalf, are expressly qualified in their entirety by the cautionary statements above. We do not undertake, and expressly disclaim, any duty to update or revise our forward-looking statements based on new information, future events or otherwise.

5

PART I

Items 1 and 2. Business and Properties

General

A Delaware corporation formed in 1971 and publicly held since 1988, Devon (NYSE: DVN) is an independent energy company engaged primarily in the exploration, development and production of oil, natural gas and NGLs. Our operations are concentrated in various onshore areas in the U.S. In October 2020, we completed the sale of our Barnett Shale assets.

On January 7, 2021, Devon and WPX completed an all-stock merger of equals. WPX is an oil and gas exploration and production company with assets in the Delaware Basin in Texas and New Mexico and the Williston Basin in North Dakota. This merger enhances the scale of our operations, builds a leading position in the Delaware Basin and accelerates our cash-return business model that prioritizes free cash flow generation and the return of capital to shareholders. In accordance with the Merger Agreement, WPX shareholders received a fixed exchange of 0.5165 shares of Devon common stock for each share of WPX common stock owned. The combined company continues to operate under the name Devon. Our principal and administrative offices are located at 333 West Sheridan, Oklahoma City, OK 73102-5015 (telephone 405-235-3611).

Devon files or furnishes annual reports on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K, as well as any amendments to these reports, with the SEC. Through our website, www.devonenergy.com, we make available electronic copies of the documents we file or furnish to the SEC, the charters of the committees of our Board of Directors and other documents related to our corporate governance. The corporate governance documents available on our website include our Code of Ethics for Chief Executive Officer, Chief Financial Officer and Chief Accounting Officer, and any amendments to and waivers from any provision of that Code will also be posted on our website. Access to these electronic filings is available free of charge as soon as reasonably practicable after filing or furnishing them to the SEC. Printed copies of our committee charters or other governance documents and filings can be requested by writing to our corporate secretary at the address on the cover of this report. Reports filed with the SEC are also made available on its website at www.sec.gov.

Our Strategy

Our business strategy is focused on delivering a consistently competitive shareholder return among our peer group. Because the business of exploring for, developing and producing oil and natural gas is capital intensive, delivering sustainable, capital efficient cash flow growth is a key tenant to our success. While our cash flow is highly dependent on volatile and uncertain commodity prices, we pursue our strategy throughout all commodity price cycles with four fundamental principles.

Proven and responsible operator – We operate our business with the interests of our stakeholders and our environmental, social and governance values in mind. With our vision to be a premier independent oil and natural gas exploration and production company, the work our employees do every day contributes to the local, national and global economies. We produce a valuable commodity that is fundamental to society, and we endeavor to do so in a safe, environmentally responsible and ethical way, while striving to deliver strong returns to our shareholders. We have an ongoing commitment to transparency in reporting our environmental, social and governance performance. See our Sustainability Report published on our company website for performance highlights and additional information. Information contained in our Sustainability Report is not incorporated by reference into, and does not constitute a part of, this Annual Report on Form 10-K.

Premier, sustainable portfolio of assets – As discussed later in this section of this Annual Report, we own a portfolio of assets located in the United States. We strive to own premier assets capable of generating cash flows in excess of our capital and operating requirements, as well as competitive rates of return. We also desire to own a portfolio of assets that can provide sustainable production extending many years into the future. Due to the strength of oil prices relative to natural gas, we have positioned our portfolio to be more heavily weighted to U.S. oil assets in recent years.

During 2019, we sold our Canadian business, generating $2.6 billion in proceeds. During 2020, we sold our Barnett Shale assets, generating proceeds of $490 million and contingent earnout payments to Devon of up to $260 million based upon future commodity prices, with upside participation beginning at a $2.75 Henry Hub natural gas price or a $50 WTI oil price. On January 7, 2021, Devon and WPX completed an all-stock merger of equals. WPX is an oil and gas exploration and production company with assets in the Delaware Basin in Texas and New Mexico and the Williston Basin in North Dakota. As a result of these transactions, our oil production, price realizations and field-level margins will all improve, as we sharpen our focus on five U.S. oil and liquids plays located in the Delaware Basin, Powder River Basin, Anadarko Basin, Williston Basin and Eagle Ford.

Superior execution – As we pursue cash flow growth, we continually work to optimize the efficiency of our capital programs and production operations, with an underlying objective of reducing absolute and per unit costs and enhancing our returns. We also strive to leverage our culture of health, safety and environmental stewardship in all aspects of our business.

With the WPX Merger and continuous improvement initiatives, we are building a scalable, multi-basin portfolio of U.S. oil assets and aggressively improving our cost structure to further expand margins. We have realized annualized cost savings by reducing well costs, production expense, financing costs and G&A costs.

6

Financial strength and flexibility – Commodity prices are uncertain and volatile, so we strive to maintain a strong balance sheet, as well as adequate liquidity and financial flexibility, in order to operate competitively in all commodity price cycles. Our capital allocation decisions are made with attention to these financial stewardship principles, as well as the priorities of funding our core operations, protecting our investment-grade credit ratings, and paying and growing our shareholder dividend.

Human Capital

Delivering strong operational and financial results in a safe, environmentally and socially responsible way requires the expertise and positive contributions of every Devon employee. Consequently, our people are the Company’s most important resource and we seek to hire the best people who share our core values of doing the right thing, delivering results and being good team members and neighbors to our communities. To develop our workforce, we focus on training, safety, wellness, inclusion, diversity and equality. As of December 31, 2020, Devon and its consolidated subsidiaries had approximately 1,400 employees, all located in the U.S.

Employee Safety and Wellness

We prepare our workforce to work safely with comprehensive training and orientation, on-the-job guidance and tools, safety engagements, recognition and other resources. Employees and contractors are expected to comply with safety rules and regulations and are accountable to stopping at-risk work, immediately reporting incidents and near-miss events and informing visitors of emergency alarms and evacuation plans. To safeguard workers on our well sites and neighbors nearby, we plan, design, drill, complete and produce wells using proven best practices, technologies, tools and materials.

In response to the COVID-19 pandemic, we have developed and implemented a number of safety measures to help our employees manage their work and personal responsibilities, with a strong focus on employee well-being, health and safety. Refer to “COVID-19” included in Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations” for information on actions taken by Devon to protect and support its employees during the COVID-19 pandemic.

Beyond employee safety, Devon also prioritizes the physical, mental and financial wellness of our employees. We offer competitive health and financial benefits with incentives designed to promote wellbeing. For example, we encourage employees to take advantage of our wellness programs and activities by getting an annual physical exam or completing a financial wellness series at no cost to employees.

Employee Compensation, Benefits and Development

We strive to attract and retain high-performing individuals across our workforce. One way we do this is by providing competitive compensation and benefits, including annual bonuses; a 401(k) savings plan with a Devon match; stock awards; medical, dental and vision health care coverage; health savings and dependent-care flexible spending accounts; maternity and parental leave for the birth or adoption of a child; an adoption assistance program; alternate work schedules; flexible work hours; part-time work options; telecommuting support; among other benefits.

Devon also looks to our core values to build the workforce we need. We develop our employees’ knowledge and creativity and advance continual learning and career development through ongoing performance, training and development conversations.

Inclusion and Diversity

Devon’s success depends on employees who demonstrate integrity, accountability, perseverance and a passion for building our business and delivering results. Our efforts to create a workforce with these qualities start with offering equal opportunity in all aspects of employment. We do this with employee-led organizations and corporate policies.

We promote inclusion and diversity throughout the Company to bring a range of thoughts, experiences and points of view to our problem-solving and decision-making processes. Devon has an Inclusion and Diversity Leadership Team, which consists of senior leaders who support others by coaching, motivating and breaking down barriers. The Inclusion and Diversity Leadership Team works together with Devon’s all-volunteer Inclusion Action Team to proactively increase diversity and inclusion awareness, identify challenges and find innovative ways to achieve Devon’s inclusion and diversity vision and strategy.

All Devon employees must act in accordance with our Code of Business Conduct and Ethics (“Code”), which sets forth current business practices and guidance to ensure ongoing compliance. Our Code covers topics such as anti-corruption, harassment, discrimination, privacy, cybersecurity, confidential information and how to report Code violations. On an annual basis, Devon employees are required to acknowledge and agree to abide by our Code, as well as complete a training course on the Code and its related policies. Additionally, our directors, officers and employees are required to comply with policies such as our Zero Tolerance Anti-Harassment Policy, Anti-Corruption Policy and Procedure, Conflicts of Interest Policy and Employee Gifts and Entertainment Declaration Policy.

7

Additional information regarding Devon’s human capital measures and objectives is contained in Devon’s Sustainability Report published on our company website. Information contained in our Sustainability Report is not incorporated by reference into, and does not constitute a part of, this Annual Report on Form 10-K.

Oil and Gas Properties

WPX Merger Assets

On January 7, 2021, Devon and WPX completed an all-stock merger of equals. WPX is an oil and gas exploration and production company with assets in the Delaware Basin in Texas and New Mexico and the Williston Basin in North Dakota. Financial and operational data, such as reserves, production, wells and acreage, provided in this document exclude amounts related to WPX’s assets unless otherwise noted due to the Merger closing subsequent to December 31, 2020. For additional information, please see Note 2 in “Item 8. Financial Statements and Supplementary Data” of this report.

Canadian Business and Barnett Shale Assets – Discontinued Operations

As a result of our divestment of substantially all of our oil and gas assets and operations in Canada, as well as the divestiture of our Barnett Shale assets, amounts associated with these assets are presented as discontinued operations. The financial and operational data, such as reserves, production, wells and acreage, provided in this document exclude amounts related to our Canadian and Barnett Shale assets unless otherwise noted. Included within the amounts presented as discontinued operations associated with the Barnett Shale are properties divested in previous reporting periods located primarily in Johnson and Wise counties, Texas. For additional information, please see Note 2 in “Item 8. Financial Statements and Supplementary Data” of this report.

8

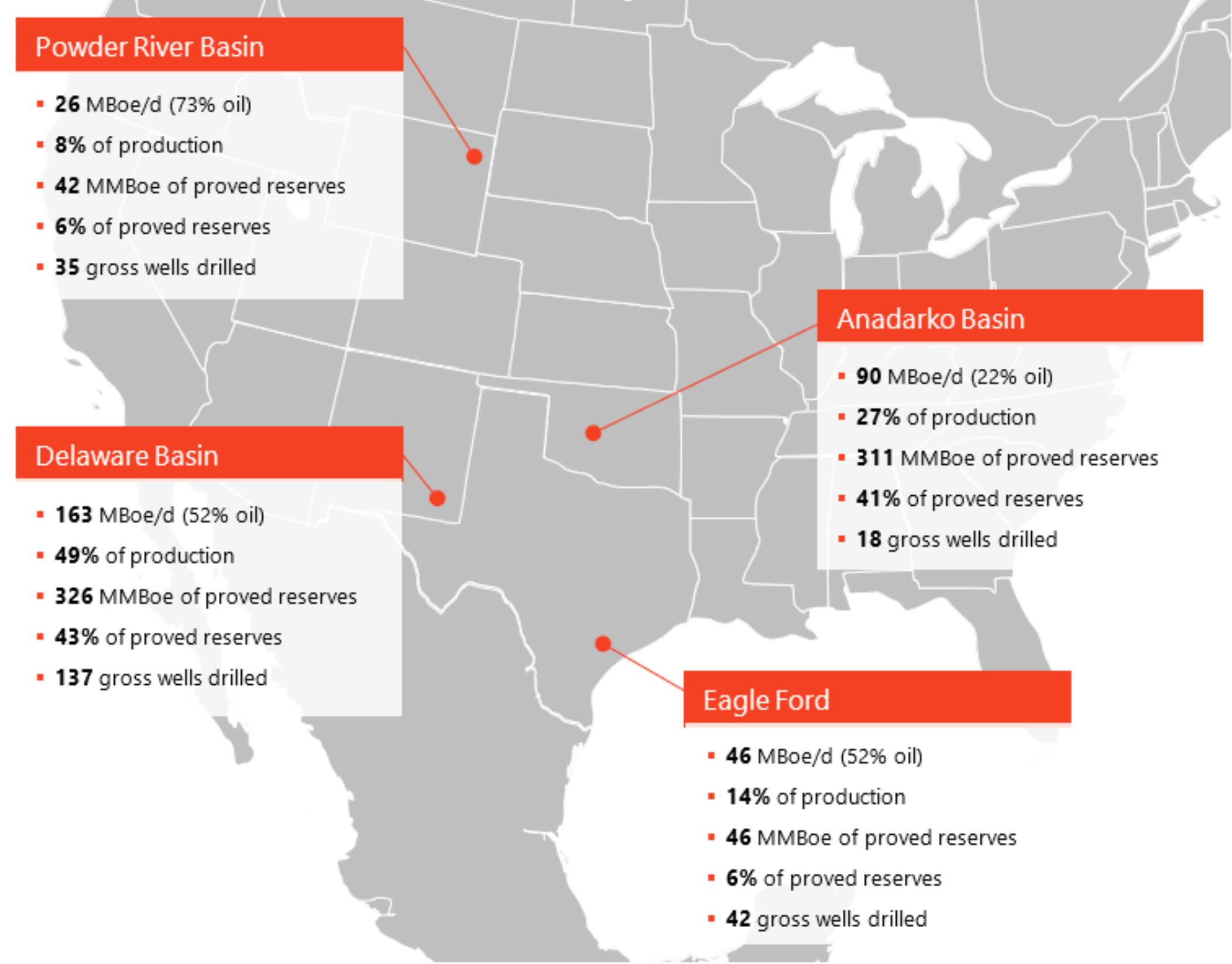

Property Profiles

Key summary data from each of our areas of operation as of and for the year ended December 31, 2020 are detailed in the map below.

Delaware Basin – The Delaware Basin is Devon’s most active program in the portfolio. Through capital-efficient drilling programs, it offers exploration and low-risk development opportunities from many geologic reservoirs and play types, including the oil-rich Wolfcamp, Bone Spring, Leonard and Delaware formations. With a significant inventory of oil and liquids-rich drilling opportunities that have multi-zone development potential, Devon has a robust platform to deliver high-margin drilling programs for many years to come. At December 31, 2020, we had eight operated rigs developing this asset in the Wolfcamp and Bone Spring formations. Combined with the Delaware Basin assets acquired in the WPX merger, we plan to invest approximately $1.5 billion of capital in the Delaware Basin in 2021, making it the top-funded asset in the portfolio.

Powder River Basin – This asset is focused on emerging oil opportunities in the Powder River Basin. Devon is currently targeting several Cretaceous oil objectives, including the Turner, Parkman, Teapot and Niobrara formations. Recent drilling success in this basin has expanded our drilling inventory, and we expect further growth as we accelerate activity and continue to de-risk this emerging light-oil opportunity. Devon has several uncompleted wells in its Powder River Basin inventory and has resumed capital activity in early 2021. In 2021, we plan approximately $80 million of capital investment.

Eagle Ford – We acquired our position in the Eagle Ford in 2014. Since acquiring these assets, we have delivered tremendous results driven by our development in DeWitt County, Texas located in the economic core of the play. Our Eagle Ford production is leveraged to oil and has low-cost access to premium Gulf Coast pricing, providing for solid operating margins. As a result of the COVID-19 pandemic and related significant decrease to oil pricing in early 2020, Devon did not pursue any drilling and completion

9

activity in the latter half of 2020 for these assets. Devon has several uncompleted wells in its Eagle Ford inventory and has resumed capital activity in early 2021. In 2021, we plan approximately $110 million of capital investment.

Anadarko Basin – Our Anadarko Basin development, located primarily in Oklahoma’s Canadian, Kingfisher and Blaine counties, provides long-term optionality through its significant inventory. Our Anadarko Basin position is one of the largest in the industry, providing visible long-term production. At the end of 2019, we announced an agreement with Dow to jointly develop a portion of our Anadarko Basin acreage. This joint venture activity was delayed in response to the challenged macro-economic environment resulting from the COVID pandemic. However, due to improvements in natural gas pricing, the joint venture has commenced in the first quarter of 2021 with a two operated rig program. Dow will fund approximately 65% of the partnership capital requirements through a drilling carry of $100 million over the next four years. In 2021, we plan approximately $75 million of capital investment, net to Devon.

Proved Reserves

Proved oil and gas reserves are those quantities of oil, gas and NGLs which can be estimated with reasonable certainty to be economically producible from known reservoirs under existing economic conditions, operating methods and government regulations. To be considered proved, oil and gas reserves must be economically producible before contracts providing the right to operate expire, unless evidence indicates that renewal is reasonably certain. Also, the project to extract the hydrocarbons must have commenced or the operator must be reasonably certain that it will commence the project within a reasonable time. We establish our proved reserves estimates using standard geological and engineering technologies and computational methods, which are generally accepted by the petroleum industry. We primarily prepare our proved reserves additions by analogy using type curves that are based on decline curve analysis of wells in analogous reservoirs. We further establish reasonable certainty of our proved reserves estimates by using one or more of the following methods: geological and geophysical information to establish reservoir continuity between penetrations, rate-transient analysis, analytical and numerical simulations, or other proprietary technical and statistical methods. For estimates of our proved developed and proved undeveloped reserves and the discussion of the contribution by each property, see Note 22 in “Item 8. Financial Statements and Supplementary Data” of this report.

The process of estimating oil, gas and NGL reserves is complex and requires significant judgment, as discussed in “Item 1A. Risk Factors” of this report. As a result, we have developed internal policies for estimating and recording reserves in compliance with applicable SEC definitions and guidance. Our policies assign responsibilities for compliance in reserves bookings to our Reserve Evaluation Group (the “Group”). The Group, which is led by Devon’s Director of Reserves and Economics, is responsible for the internal review and certification of reserves estimates. We ensure the Director and key members of the Group have appropriate technical qualifications to oversee the preparation of reserves estimates and are independent of the operating groups. The Director of the Group has over 30 years of industry experience, a degree in engineering and is a registered professional engineer. The Group also oversees audits and reserves estimates performed by qualified third-party petroleum consulting firms. During 2020, we engaged LaRoche Petroleum Consultants, Ltd. to audit approximately 88% of our proved reserves. Additionally, we have a Reserves Committee that provides additional oversight of our reserves process. The committee consists of five independent members of our Board of Directors with education or business backgrounds relevant to the reserves estimation process.

The following tables present production, price and cost information for each significant field in our asset portfolio and the total company.

|

|

|

Production |

|

|||||||||||||

|

Year Ended December 31, |

|

Oil (MMBbls) |

|

|

Gas (Bcf) |

|

|

NGLs (MMBbls) |

|

|

Total (MMBoe) |

|

||||

|

2020 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Anadarko Basin |

|

|

7 |

|

|

|

92 |

|

|

|

10 |

|

|

|

33 |

|

|

Delaware Basin |

|

|

31 |

|

|

|

91 |

|

|

|

13 |

|

|

|

60 |

|

|

Total |

|

|

57 |

|

|

|

221 |

|

|

|

29 |

|

|

|

122 |

|

|

2019 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Anadarko Basin |

|

|

11 |

|

|

|

114 |

|

|

|

13 |

|

|

|

43 |

|

|

Delaware Basin |

|

|

26 |

|

|

|

65 |

|

|

|

10 |

|

|

|

46 |

|

|

Total |

|

|

55 |

|

|

|

219 |

|

|

|

28 |

|

|

|

119 |

|

|

2018 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Anadarko Basin |

|

|

12 |

|

|

|

121 |

|

|

|

14 |

|

|

|

45 |

|

|

Delaware Basin |

|

|

16 |

|

|

|

42 |

|

|

|

6 |

|

|

|

30 |

|

|

Total |

|

|

47 |

|

|

|

206 |

|

|

|

26 |

|

|

|

108 |

|

10

|

|

|

Average Sales Price |

|

|

|

|

|

|||||||||

|

Year Ended December 31, |

|

Oil (Per Bbl) |

|

|

Gas (Per Mcf) |

|

|

NGLs (Per Bbl) |

|

|

Production Cost (Per Boe) (1) |

|

||||

|

2020 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Anadarko Basin (2) |

|

$ |

35.80 |

|

|

$ |

1.66 |

|

|

$ |

12.11 |

|

|

$ |

9.61 |

|

|

Delaware Basin |

|

$ |

37.25 |

|

|

$ |

1.08 |

|

|

$ |

10.64 |

|

|

$ |

5.76 |

|

|

Total |

|

$ |

35.95 |

|

|

$ |

1.48 |

|

|

$ |

11.72 |

|

|

$ |

7.66 |

|

|

2019 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Anadarko Basin |

|

$ |

55.13 |

|

|

$ |

1.97 |

|

|

$ |

15.90 |

|

|

$ |

7.36 |

|

|

Delaware Basin |

|

$ |

54.01 |

|

|

$ |

0.99 |

|

|

$ |

13.54 |

|

|

$ |

6.43 |

|

|

Total |

|

$ |

54.73 |

|

|

$ |

1.79 |

|

|

$ |

15.21 |

|

|

$ |

7.75 |

|

|

2018 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Anadarko Basin |

|

$ |

63.81 |

|

|

$ |

2.29 |

|

|

$ |

25.53 |

|

|

$ |

7.16 |

|

|

Delaware Basin |

|

$ |

57.24 |

|

|

$ |

1.80 |

|

|

$ |

24.05 |

|

|

$ |

8.15 |

|

|

Total |

|

$ |

61.96 |

|

|

$ |

2.34 |

|

|

$ |

25.47 |

|

|

$ |

8.22 |

|

|

|

(1) |

Represents production expense per Boe excluding production and property taxes. |

|

|

(2) |

Production cost per Boe was higher in 2020 due to volume commitments which expired at the end of 2020. |

Drilling Statistics

The following table summarizes our development and exploratory drilling results.

|

|

|

Development Wells (1) |

|

|

Exploratory Wells (1) |

|

|

Total Wells (1) |

|

|||||||||||||||||||

|

Year Ended December 31, |

|

Productive |

|

|

Dry |

|

|

Productive |

|

|

Dry |

|

|

Productive |

|

|

Dry |

|

|

Total |

|

|||||||

|

2020 |

|

|

106.5 |

|

|

|

— |

|

|

|

26.6 |

|

|

|

— |

|

|

|

133.2 |

|

|

|

— |

|

|

|

133.2 |

|

|

2019 |

|

|

161.7 |

|

|

|

— |

|

|

|

27.2 |

|

|

|

— |

|

|

|

188.9 |

|

|

|

— |

|

|

|

188.9 |

|

|

2018 |

|

|

154.9 |

|

|

|

3.1 |

|

|

|

69.4 |

|

|

|

— |

|

|

|

224.3 |

|

|

|

3.1 |

|

|

|

227.4 |

|

|

(1) |

Well counts represent net wells completed during each year. Net wells are gross wells multiplied by our fractional working interests. |

As of December 31, 2020, there were 156 gross and 77.6 net wells that have been spud and are in the process of drilling, completing or waiting on completion. To effectively manage capital expenditures and provide flexibility in managing drilling rig and well completion schedules, we have a large inventory of drilled but not completed wells. Gross wells are the sum of all wells in which we own a working interest. Net wells are gross wells multiplied by our fractional working interests in each well.

Productive Wells

The following table sets forth our producing wells as of December 31, 2020.

|

|

|

Oil Wells |

|

|

Natural Gas Wells |

|

|

Total Wells |

|

|||||||||||||||

|

|

|

Gross (1)(3) |

|

|

Net (2) |

|

|

Gross (1)(3) |

|

|

Net (2) |

|

|

Gross (1)(3) |

|

|

Net (2) |

|

||||||

|

Total |

|

|

7,752 |

|

|

|

2,385 |

|

|

|

2,980 |

|

|

|

1,201 |

|

|

|

10,732 |

|

|

|

3,586 |

|

|

(1) |

Gross wells are the sum of all wells in which we own a working interest. |

|

(2) |

Net wells are gross wells multiplied by our fractional working interests in each well. |

|

(3) |

Includes 45 and 57 gross oil and gas wells, respectively, which had multiple completions. |

The day-to-day operations of oil and gas properties are the responsibility of an operator designated under pooling or operating agreements. The operator supervises production, maintains production records, employs field personnel and performs other functions. We are the operator of approximately 3,942 gross wells. As operator, we receive reimbursement for direct expenses incurred to perform our duties, as well as monthly per-well producing, drilling, and construction overhead reimbursement at rates customarily charged in the respective areas. In presenting our financial data, we record the monthly overhead reimbursements as a reduction of G&A, which is a common industry practice.

11

Acreage Statistics

The following table sets forth our developed and undeveloped lease and mineral acreage as of December 31, 2020. Of our 1.8 million net acres, approximately 1.0 million acres are held by production. The acreage in the table includes approximately 0.1 million net acres subject to leases that are scheduled to expire during 2021, 2022 and 2023. Of the 0.1 million net acres set to expire by December 31, 2023, we anticipate performing operational and administrative actions to continue the lease terms for portions of the acreage that we intend to further assess. However, we do expect to allow a portion of the acreage to expire in the normal course of business. Subsequent to our merger with WPX, less than 20% of our total net acres are located on federal lands.

|

|

|

Developed |

|

|

Undeveloped |

|

|

Total |

|

|||||||||||||||

|

|

|

Gross (1) |

|

|

Net (2) |

|

|

Gross (1) |

|

|

Net (2) |

|

|

Gross (1) |

|

|

Net (2) |

|

||||||

|

|

|

(Thousands) |

|

|||||||||||||||||||||

|

Total |

|

|

953 |

|

|

|

504 |

|

|

|

2,994 |

|

|

|

1,267 |

|

|

|

3,947 |

|

|

|

1,771 |

|

|

(1) |

Gross acres are the sum of all acres in which we own a working interest. |

|

(2) |

Net acres are gross acres multiplied by our fractional working interests in the acreage. |

Title to Properties

Title to properties is subject to contractual arrangements customary in the oil and gas industry, liens for taxes not yet due and, in some instances, other encumbrances. We believe that such burdens do not materially detract from the value of properties or from the respective interests therein or materially interfere with their use in the operation of the business.

As is customary in the industry, a preliminary title investigation, typically consisting of a review of local title records, is made at the time of acquisitions of undeveloped properties. More thorough title investigations, which generally include a review of title records and the preparation of title opinions by outside legal counsel, are made prior to the consummation of an acquisition of producing properties and before commencement of drilling operations on undeveloped properties.

Marketing Activities

Oil, Gas and NGL Marketing

The spot markets for oil, gas and NGLs are subject to volatility as supply and demand factors fluctuate. As detailed below, we sell our production under both long-term (one year or more) and short-term (less than one year) agreements at prices negotiated with third parties. Regardless of the term of the contract, the vast majority of our production is sold at variable, or market-sensitive, prices.

Additionally, we may enter into financial hedging arrangements or fixed-price contracts associated with a portion of our oil, gas and NGL production. These activities are intended to support targeted price levels and to manage our exposure to price fluctuations. See Note 3 in “Item 8. Financial Statements and Supplementary Data” of this report for further information.

As of January 2021, our production was sold under the following contract terms.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Short-Term |

|

|

Long-Term |

|

||||||||||

|

|

|

Variable |

|

|

Fixed |

|

|

Variable |

|

|

Fixed |

|

||||

|

Oil |

|

|

45 |

% |

|

|

5 |

% |

|

|

50 |

% |

|

|

— |

|

|

Natural gas |

|

|

56 |

% |

|

|

3 |

% |

|

|

41 |

% |

|

|

— |

|

|

NGLs |

|

|

63 |

% |

|

|

25 |

% |

|

|

12 |

% |

|

|

— |

|

12

Delivery Commitments

A portion of our production is sold under certain contractual arrangements that specify the delivery of a fixed and determinable quantity. As of December 31, 2020, we were committed to deliver the following fixed quantities of production.

|

|

|

Total |

|

|

Less Than 1 Year |

|

|

1-3 Years |

|

|

3-5 Years |

|

|

More Than 5 Years |

|

|||||

|

Natural gas (Bcf) |

|

|

174 |

|

|

|

90 |

|

|

|

52 |

|

|

|

32 |

|

|

|

— |

|

|

NGLs (MMBbls) |

|

|

7 |

|

|

|

7 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

Total (MMBoe) |

|

|

36 |

|

|

|

22 |

|

|

|

9 |

|

|

|

5 |

|

|

|

— |

|

We expect to fulfill our delivery commitments primarily with production from our proved developed reserves. Moreover, our proved reserves have generally been sufficient to satisfy our delivery commitments during the three most recent years, and we expect such reserves will continue to be the primary means of fulfilling our future commitments. However, where our proved reserves are not sufficient to satisfy our delivery commitments, we can and may use spot market purchases to satisfy the commitments.

Competition

See “Item 1A. Risk Factors.”

Public Policy and Government Regulation

Our industry is subject to a wide range of regulations. Laws, rules, regulations, taxes, fees and other policy implementation actions affecting our industry have been pervasive and are under constant review for amendment or expansion. Numerous government agencies have issued extensive regulations which are binding on our industry and its individual members, some of which carry substantial penalties for failure to comply. These laws and regulations increase the cost of doing business and consequently affect profitability. Because public policy changes are commonplace, and existing laws and regulations are frequently amended, we are unable to predict the future cost or impact of compliance. However, we do not expect that any of these laws and regulations will affect our operations materially differently than they would affect other companies with similar operations, size and financial strength. The following are significant areas of government control and regulation affecting our operations.

Exploration and Production Regulation

Our operations are subject to federal, state and local laws and regulations. These laws and regulations relate to matters that include:

|

|

• |

acquisition of seismic data; |

|

|

• |

location, drilling and casing of wells; |

|

|

• |

well design; |

|

|

• |

hydraulic fracturing; |

|

|

• |

well production; |

|

|

• |

spill prevention plans; |

|

|

• |

emissions and discharge permitting; |

|

|

• |

use, transportation, storage and disposal of fluids and materials incidental to oil and gas operations; |

|

|

• |

surface usage and the restoration of properties upon which wells have been drilled; |

|

|

• |

calculation and disbursement of royalty payments and production taxes; |

|

|

• |

plugging and abandoning of wells; |

|

|

• |

transportation of production; and |

|

|

• |

endangered species and habitat. |

13

Our operations also are subject to conservation regulations, including the regulation of the size of drilling and spacing units or proration units; the number of wells that may be drilled in a unit; the rate of production allowable from oil and gas wells; and the unitization or pooling of oil and gas properties. In the U.S., some states allow the forced pooling or unitization of tracts to facilitate exploration, while other states rely on voluntary pooling of lands and leases, which may make it more difficult to develop oil and gas properties. In addition, federal and state conservation laws generally limit the venting or flaring of natural gas, and state conservation laws impose certain requirements regarding the ratable purchase of production. These regulations limit the amounts of oil and gas we can produce from our wells and the number of wells or the locations at which we can drill.

Certain of our U.S. natural gas and oil leases are granted or approved by the federal government and administered by the BLM or Bureau of Indian Affairs of the Department of the Interior. Such leases require compliance with detailed federal regulations and orders that regulate, among other matters, drilling and operations on lands covered by these leases and calculation and disbursement of royalty payments to the federal government, tribes or tribal members. Moreover, the permitting process for oil and gas activities on federal lands can sometimes be subject to delay, which can stall development activities or otherwise adversely impact operations. The federal government has, from time to time, evaluated and, in some cases, promulgated new rules and regulations regarding competitive lease bidding, venting and flaring, oil and gas measurement and royalty payment obligations for production from federal lands. In addition, President Biden and certain members of his administration have expressed support for, and have taken steps to implement, additional restrictions on oil and gas activities on federal lands, including orders temporarily limiting the approval of new leases and drilling permits to certain high-ranking officials within the Department of the Interior, as well as a pause on entering into future oil and gas leases on public lands.

Environmental, Pipeline Safety and Occupational Regulations

We strive to conduct our operations in a socially and environmentally responsible manner, which includes compliance with applicable law. We are subject to many federal, state, and local laws and regulations concerning occupational safety and health as well as the discharge of materials into, and the protection of, the environment and natural resources. Environmental laws and regulations relate to:

|

|

• |

the discharge of pollutants into federal and state waters; |

|

|

• |

assessing the environmental impact of seismic acquisition, drilling or construction activities; |

|

|

• |

the generation, storage, transportation and disposal of waste materials, including hazardous substances and wastes; |

|

|

• |

the emission of certain gases into the atmosphere; |

|

|

• |

the monitoring, abandonment, reclamation and remediation of well and other sites, including sites of former operations; |

|

|

• |

the development of emergency response and spill contingency plans; |

|

|

• |

the monitoring, repair and design of pipelines used for the transportation of oil and natural gas; |

|

|

• |

the protection of threatened and endangered species; and |

|

|

• |

worker protection. |

Failure to comply with these laws and regulations can lead to the imposition of remedial liabilities, administrative, civil or criminal fines or penalties or injunctions limiting our operations in affected areas. Moreover, multiple environmental laws provide for citizen suits, which can allow environmental organizations to sue operators for alleged violations of environmental law. Environmental organizations also can assert legal and administrative challenges to certain actions of oil and gas regulators, such as the BLM, for allegedly failing to comply with environmental laws, which can result in delays in obtaining permits or other necessary authorizations. Environmental protection and health and safety compliance are necessary, manageable parts of our business. We have been able to plan for and comply with environmental, safety and health initiatives without materially altering our operating strategy or incurring significant unreimbursed expenditures. However, based on regulatory trends and increasingly stringent laws and permitting requirements, our capital expenditures and operating expenses related to the protection of the environment and safety and health compliance have increased over the years and may continue to increase.

Item 1A. Risk Factors

Our business and operations, and our industry in general, are subject to a variety of risks. The risks described below may not be the only risks we face, as our business and operations may also be subject to risks that we do not yet know of, or that we currently

14

believe are immaterial. If any of the following risks should occur, our business, financial condition, results of operations and liquidity could be materially and adversely impacted. As a result, holders of our securities could lose part or all of their investment in Devon.

Volatile Oil, Gas and NGL Prices Significantly Impact Our Business

Our financial condition, results of operations and the value of our properties are highly dependent on the general supply and demand for oil, gas and NGLs, which impact the prices we ultimately realize on our sales of these commodities. Historically, market prices and our realized prices have been volatile. For example, over the last five years, monthly NYMEX WTI oil and NYMEX Henry Hub gas prices ranged from highs of over $67 per Bbl and $4.80 per MMBtu, respectively, to lows of under $30 per Bbl and $1.50 per MMBtu, respectively. Such volatility is likely to continue in the future due to numerous factors beyond our control, including, but not limited to:

|

|

• |

the domestic and worldwide supply of and demand for oil, gas and NGLs; |

|

|

• |

volatility and trading patterns in the commodity-futures markets; |

|

|

• |

conservation and environmental protection efforts; |

|

|

• |

production levels of members of OPEC, Russia, the U.S. or other producing countries; |

|

|

• |

geopolitical risks, including political and civil unrest in the Middle East, Africa and South America; |

|

|

• |

adverse weather conditions, natural disasters, public health crises and other catastrophic events, such as tornadoes, earthquakes, hurricanes and epidemics of infectious diseases; |

|

|

• |

regional pricing differentials, including in the Delaware Basin and other areas of our operations; |

|

|

• |

differing quality of production, including NGL content of gas produced; |

|

|

• |

the level of imports and exports of oil, gas and NGLs and the level of global oil, gas and NGL inventories; |

|

|

• |

the price and availability of alternative energy sources; |

|

|

• |

technological advances affecting energy consumption and production, including with respect to electric vehicles; |

|

|

• |

stockholder activism or activities by non-governmental organizations to restrict the exploration and production of oil and natural gas in order to reduce greenhouse gas emissions; |

|

|

• |

the overall economic environment; |

|

|

• |

changes in trade relations and policies, including the imposition of tariffs by the U.S. or China; and |

|

|

• |

other governmental regulations and taxes. |

Our Business Has Been Adversely Impacted by the COVID-19 Pandemic, and We May Experience Continuing or Worsening Adverse Effects From This or Other Pandemics

The COVID-19 pandemic and related economic repercussions have created significant volatility, uncertainty and turmoil in the oil and gas industry. This outbreak and the related responses of governmental authorities and others to limit the spread of the virus significantly reduced global economic activity, resulting in an unprecedented decline in the demand for oil and other commodities during 2020. Combined with other factors, this decline in demand caused a swift and material deterioration in commodity prices in early 2020, which adversely impacted our results of operations for 2020 and contributed to our recognition of a material asset impairment to our oil and gas assets during the first quarter of 2020. The negative effects of COVID-19 on economic prospects across the world have contributed to concerns for the potential of a prolonged economic slowdown and recession. Any such downturns, or protracted periods of depressed commodity prices, could have significant adverse consequences for our financial condition and liquidity. Moreover, any such downturns could also result in similar financial constraints for our non-operating partners, purchasers of our production and other counterparties, thereby increasing the risk that such counterparties default on their obligations to us. Such defaults or more general supply chain disruptions due to the pandemic may also jeopardize the supply of materials, equipment or services for our operations.

The COVID-19 pandemic and related restrictions aimed at mitigating its spread have caused us to modify certain of our business practices, including limiting employee travel, encouraging work-from-home practices and other social distancing measures. There is no certainty that these or any other future measures will be sufficient to mitigate the risks posed by the disease, including the risk of infection of key employees, and our ability to perform certain functions could be disrupted or otherwise impaired by these new

15

business practices. For example, our reliance on technology has necessarily increased due to our encouragement of remote communications and other work-from-home practices, which could make us more vulnerable to cyber attacks.

The COVID-19 pandemic and its related effects continue to evolve. The ultimate extent of the impact of the COVID-19 pandemic and any other future pandemic on our business will depend on future developments, including, but not limited to, the nature, duration and spread of the disease, the vaccination and other responsive actions to stop its spread or address its effects and the duration, timing and severity of the related consequences on commodity prices and the economy more generally, including any recession resulting from the pandemic. Any extended period of depressed commodity prices or general economic disruption as a result of a pandemic would adversely affect our business, financial condition and results of operations.

Estimates of Oil, Gas and NGL Reserves Are Uncertain and May Be Subject to Revision

The process of estimating oil, gas and NGL reserves is complex and requires significant judgment in the evaluation of available geological, engineering and economic data for each reservoir, particularly for new discoveries. Because of the high degree of judgment involved, different reserve engineers may develop different estimates of reserve quantities and related revenue based on the same data. In addition, the reserve estimates for a given reservoir may change substantially over time as a result of several factors, including additional development and appraisal activity, the viability of production under varying economic conditions, including commodity price declines, and variations in production levels and associated costs. Consequently, material revisions to existing reserves estimates may occur as a result of changes in any of these factors. Such revisions to proved reserves could have an adverse effect on our financial condition and the value of our properties, as well as the estimates of our future net revenue and profitability. Our policies and internal controls related to estimating and recording reserves are included in “Items 1 and 2. Business and Properties” of this report.

Discoveries or Acquisitions of Reserves Are Needed to Avoid a Material Decline in Reserves and Production

The production rates from oil and gas properties generally decline as reserves are depleted, while related per unit production costs generally increase due to decreasing reservoir pressures and other factors. Moreover, our current development activity is focused on unconventional oil and gas assets, which generally have significantly higher decline rates as compared to conventional assets. Therefore, our estimated proved reserves and future oil, gas and NGL production will decline materially as reserves are produced unless we conduct successful exploration and development activities, such as identifying additional producing zones in existing wells, utilizing secondary or tertiary recovery techniques or acquiring additional properties containing proved reserves. Consequently, our future oil, gas and NGL production and related per unit production costs are highly dependent upon our level of success in finding or acquiring additional reserves.

We Are Subject to Extensive Governmental Regulation, Which Can Change and Could Adversely Impact Our Business

Our operations are subject to extensive federal, state, local and other laws, rules and regulations, including with respect to environmental matters, worker health and safety, wildlife conservation, the gathering and transportation of oil, gas and NGLs, conservation policies, reporting obligations, royalty payments, unclaimed property and the imposition of taxes. Such regulations include requirements for permits to drill and to conduct other operations and for provision of financial assurances (such as bonds) covering drilling, completion and well operations and decommissioning obligations. If permits are not issued, or if unfavorable restrictions or conditions are imposed on our drilling or completion activities, we may not be able to conduct our operations as planned. In addition, we may be required to make large expenditures to comply with applicable governmental laws, rules, regulations, permits or orders. For example, certain regulations require the plugging and abandonment of wells and removal of production facilities by current and former operators, including corporate successors of former operators. These requirements may result in significant costs associated with the removal of tangible equipment and other restorative actions.

In addition, changes in public policy have affected, and in the future could further affect, our operations. For example, President Biden and certain members of his administration and Congress have expressed support for, and have taken steps to implement, efforts to transition the economy away from fossil fuels and to promote stricter environmental regulations, and such proposals could impose new and more onerous burdens on our industry and business. These and other regulatory and public policy developments could, among other things, restrict production levels, delay necessary permitting, impose price controls, change environmental protection requirements, impose restrictions on pipelines or other necessary infrastructure and increase taxes, royalties and other amounts payable to governments or governmental agencies. Our operating and other compliance costs could increase further if existing laws and regulations are revised or reinterpreted, or if new laws and regulations become applicable to our operations. In addition, changes in public policy may indirectly impact our operations by, among other things, increasing the cost of supplies and equipment and

16

fostering general economic uncertainty. Although we are unable to predict changes to existing laws and regulations, such changes could significantly impact our profitability, financial condition and liquidity, particularly changes related to leasing and permitting on federal lands, hydraulic fracturing, environmental matters more generally, seismic activity and income taxes, as discussed below.

Federal Lands – President Biden and certain members of his administration have expressed support for, and have taken steps to implement, additional regulation of oil and gas leasing and permitting on federal lands. Such proposals range from more onerous permitting requirements to an outright moratorium on new oil and gas leasing and permitting on federal lands. For example, on January 20, 2021, the Acting Secretary of the Department of the Interior issued an order temporarily limiting the authority to approve certain fossil fuel authorizations on federal lands, including the approval of new leases and new drilling permits, to certain high-ranking officials within the Department of the Interior. In addition, President Biden issued an executive order on January 27, 2021 directing the Secretary of the Interior to pause on entering new oil and gas leases on public lands to the extent possible and to launch a rigorous review of all existing leasing and permitting practices related to fossil fuel development on public lands. While it is not possible at this time to predict the ultimate impact of these or any other future regulatory changes, any additional restrictions or prohibitions on our ability to operate on federal lands could adversely impact our business in the Delaware and Powder River Basins, as well as other areas where we operate under federal leases. Post-merger, less than 20% of our total leasehold resides on federal lands primarily located in the Delaware and Powder River Basins.

Hydraulic Fracturing – In recent years, various federal agencies have asserted regulatory authority over certain aspects of the hydraulic fracturing process. For example, the EPA has issued regulations under the federal Clean Air Act establishing performance standards for oil and gas activities, including standards for the capture of air emissions released during hydraulic fracturing, and it finalized in 2016 regulations that prohibit the discharge of wastewater from hydraulic fracturing operations to publicly owned wastewater treatment plants. The EPA also released a report in 2016 finding that certain aspects of hydraulic fracturing, such as water withdrawals and wastewater management practices, could result in impacts to water resources in certain circumstances. The BLM previously finalized regulations to regulate hydraulic fracturing on federal lands but subsequently issued a repeal of those regulations in 2017. Moreover, several states in which we operate have adopted, or stated intentions to adopt, laws or regulations that mandate further restrictions on hydraulic fracturing, such as requiring disclosure of chemicals used in hydraulic fracturing, imposing more stringent permitting, disclosure and well-construction requirements on hydraulic fracturing operations and establishing standards for the capture of air emissions released during hydraulic fracturing. In addition to state laws, local land use restrictions, such as city ordinances, may restrict drilling in general or hydraulic fracturing in particular.

Beyond these regulatory efforts, various policy makers, regulatory agencies and political leaders at the federal, state and local levels have proposed implementing even further restrictions on hydraulic fracturing, including prohibiting the technology outright. Although it is not possible at this time to predict the outcome of these or other proposals, any new restrictions on hydraulic fracturing that may be imposed in areas in which we conduct business could potentially result in increased compliance costs, delays or cessation in development or other restrictions on our operations.

Environmental Laws Generally – In addition to regulatory efforts focused on hydraulic fracturing, we are subject to various other federal, state and local laws and regulations relating to discharge of materials into, and protection of, the environment. These laws and regulations may, among other things, impose liability on us for the cost of remediating pollution that results from our operations or prior operations on assets we have acquired. Environmental laws may impose strict, joint and several liability, and failure to comply with environmental laws and regulations can result in the imposition of administrative, civil or criminal fines and penalties, as well as injunctions limiting operations in affected areas. Any future environmental costs of fulfilling our commitments to the environment are uncertain and will be governed by several factors, including future changes to regulatory requirements. Any such changes could have a significant impact on our operations and profitability.

Seismic Activity – Earthquakes in northern and central Oklahoma, southeastern New Mexico, western Texas and elsewhere have prompted concerns about seismic activity and possible relationships with the oil and gas industry. Legislative and regulatory initiatives intended to address these concerns may result in additional levels of regulation or other requirements that could lead to operational delays, increase our operating and compliance costs or otherwise adversely affect our operations. In addition, we are currently defending against certain third-party lawsuits and could be subject to additional claims, seeking alleged property damages or other remedies as a result of alleged induced seismic activity in our areas of operation.

Changes to Tax Laws – We are subject to U.S. federal income tax as well as income or capital taxes in various state and foreign jurisdictions, and our operating cash flow is sensitive to the amount of income taxes we must pay. In the jurisdictions in which we operate or previously operated, income taxes are assessed on our earnings after consideration of all allowable deductions and credits. Changes in the types of earnings that are subject to income tax, the types of costs that are considered allowable deductions (such as

17

intangible drilling costs) and the timing of such deductions, or the rates assessed on our taxable earnings would all impact our income taxes and resulting operating cash flow.

Concerns About Climate Change and Related Regulatory, Social and Market Actions May Adversely Affect Our Business

Continuing and increasing political and social attention to the issue of climate change has resulted in legislative, regulatory and other initiatives, including international agreements, to reduce greenhouse gas emissions, such as carbon dioxide and methane. Policy makers and regulators at both the U.S. federal and state levels have already imposed, or stated intentions to impose, laws and regulations designed to quantify and limit the emission of greenhouse gases. For example, both the EPA and the BLM have issued regulations for the control of methane emissions, which also include leak detection and repair requirements, for the oil and gas industry; although the methane specific requirements of some of these regulations have been repealed, similar or more stringent emissions requirements may be imposed by the Biden Administration. In addition, several states where we operate, including Wyoming, New Mexico and Texas, have already imposed, or stated intentions to impose, laws or regulations designed to reduce methane emissions from oil and gas exploration and production activities. With respect to more comprehensive regulation, policy makers and political leaders have made, or expressed support for, a variety of proposals, such as the development of cap-and-trade or carbon tax programs. In addition, President Biden has highlighted addressing climate change as a priority of his administration, and he previously released an energy plan calling for a number of sweeping changes to address climate change, including, among other measures, a national mobilization effort to achieve net-zero emissions for the U.S. economy by 2050, through increased use of renewable power, stricter fuel-efficiency standards and support for zero-emission vehicles. President Biden issued a number of executive orders in January 2021 with the purpose of implementing certain of these changes, including the rejoining of the Paris Agreement, a call for the issuance of more stringent methane emissions regulations for oil and gas facilities and an order directing federal agencies to procure electric vehicles. Although the full impact of these orders is uncertain at this time, the adoption and implementation of these or other initiatives may result in the restriction or cancellation of oil and natural gas activities, greater costs of compliance or consumption (thereby reducing demand for our products) or an impairment in our ability to continue our operations in an economic manner.

In addition to regulatory risk, other market and social initiatives resulting from the changing perception of climate change present risks for our business. For example, in an effort to promote a lower-carbon economy, there are various public and private initiatives subsidizing the development and adoption of alternative energy sources and technologies, including by mandating the use of specific fuels or technologies. These initiatives may reduce the competitiveness of carbon-based fuels, such as oil and gas. Moreover, an increasing number of financial institutions, funds and other sources of capital have begun restricting or eliminating their investment in oil and natural gas activities due to their concern regarding climate change. Such restrictions in capital could decrease the value of our business and make it more difficult to fund our operations. Finally, governmental entities and other plaintiffs have brought, and may continue to bring, claims against us and other oil and gas companies for purported damages caused by the alleged effects of climate change. These and the other regulatory, social and market risks relating to climate change described above could result in unexpected costs, increase our operating expense and reduce the demand for our products, which in turn could lower the value of our reserves and have an adverse effect on our profitability, financial condition and liquidity.

Our Operations Are Uncertain and Involve Substantial Costs and Risks

Our operating activities are subject to numerous costs and risks, including the risk that we will not encounter commercially productive oil or gas reservoirs. Drilling for oil, gas and NGLs can be unprofitable, not only from dry holes, but from productive wells that do not return a profit because of insufficient revenue from production or high costs. Substantial costs are required to locate, acquire and develop oil and gas properties, and we are often uncertain as to the amount and timing of those costs. Our cost of drilling, completing, equipping and operating wells is often uncertain before drilling commences. Declines in commodity prices and overruns in budgeted expenditures are common risks that can make a particular project uneconomic or less economic than forecasted. While both exploratory and developmental drilling activities involve these risks, exploratory drilling involves greater risks of dry holes or failure to find commercial quantities of hydrocarbons. In addition, our oil and gas properties can become damaged, our operations may be curtailed, delayed or canceled and the costs of such operations may increase as a result of a variety of factors, including, but not limited to:

|

|

• |

unexpected drilling conditions, pressure conditions or irregularities in reservoir formations; |

|

|

• |

equipment failures or accidents; |

|

|

• |

fires, explosions, blowouts, cratering or loss of well control, as well as the mishandling or underground migration of fluids and chemicals; |

18

|

|

• |

adverse weather conditions and natural disasters, such as tornadoes, earthquakes, hurricanes and extreme temperatures; |

|

|

• |

issues with title or in receiving governmental permits or approvals; |

|

|

• |

restricted takeaway capacity for our production, including due to inadequate midstream infrastructure or constrained downstream markets; |

|

|

• |

environmental hazards or liabilities; |

|

|

• |

restrictions in access to, or disposal of, water used or produced in drilling and completion operations; and |

|

|

• |

shortages or delays in the availability of services or delivery of equipment. |

The occurrence of one or more of these factors could result in a partial or total loss of our investment in a particular property, as well as significant liabilities. Moreover, certain of these events could result in environmental pollution and impact to third parties, including persons living in proximity to our operations, our employees and employees of our contractors, leading to possible injuries, death or significant damage to property and natural resources. For example, we have from time to time experienced well-control events that have resulted in various remediation and clean-up costs and certain of the other impacts described above.

In addition, we rely on our employees, consultants and sub-contractors to conduct our operations in compliance with applicable laws and standards. Any violation of such laws or standards by these individuals, whether through negligence, harassment, discrimination or other misconduct, could result in significant liability for us and adversely affect our business. For example, negligent operations by employees could result in serious injury, death or property damage, and sexual harassment or racial and gender discrimination could result in legal claims and reputational harm.

Our Hedging Activities Limit Participation in Commodity Price Increases and Involve Other Risks