UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| (Mark One) | ||

ý |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the fiscal year ended December 31, 2012 |

||

or |

||

o |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the transition period from to

Commission File Number 001-13711

WALTER ENERGY, INC.

(Exact name of registrant as specified in its charter)

| Delaware (State or other jurisdiction of incorporation or organization) |

13-3429953 (I.R.S. Employer Identification No.) |

|

3000 Riverchase Galleria, Suite 1700 Birmingham, Alabama (Address of principal executive offices) |

35244 (Zip Code) |

|

(205) 745-2000 Registrant's telephone number, including area code: |

||

Securities registered pursuant to Section 12(b) of the Act: |

||

Title of Each Class |

Name of Exchange on Which Registered |

|

| Common Stock, par value $0.01 | New York Stock Exchange Toronto Stock Exchange |

|

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ý No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ý | Accelerated filer o | Non-accelerated filer o (Do not check if a smaller reporting company) |

Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No ý

The aggregate market value of voting stock held by non-affiliates of the registrant, based on the closing price of the Common Stock on June 30, 2012, the registrant's most recently completed second fiscal quarter, as reported by the New York Stock Exchange, was approximately $2.8 billion.

Number of shares of common stock outstanding as of January 31, 2013: 62,522,420

Documents Incorporated by Reference

Applicable portions of the Proxy Statement for the 2013 Annual Meeting of Stockholders of the Company are incorporated by reference in Part III of this Form 10-K.

WALTER ENERGY, INC. AND SUBSIDIARIES

ANNUAL REPORT ON FORM 10-K

TABLE OF CONTENTS

i

CAUTIONARY NOTE REGARDING FORWARD LOOKING STATEMENTS

This report includes statements of our expectations, intentions, plans and beliefs that constitute "forward-looking statements" within the meaning of Section 27A of the Securities Act of 1933, as amended (the "Securities Act") and Section 21E of the Securities Exchange Act of 1934, as amended (the "Exchange Act"), and are intended to come within the safe harbor protection provided by those sections. These statements, which involve risks and uncertainties, relate to analyses and other information that are based on forecasts of future results and estimates of amounts not yet determinable and may also relate to our future prospects, developments and business strategies. We have used the words "anticipate," "believe," "could," "estimate," "expect," "intend," "may," "plan," "predict," "project," "should" and similar terms and phrases, including references to assumptions, in this report to identify forward-looking statements. These forward-looking statements are made based on expectations and beliefs concerning future events affecting us and are subject to uncertainties and factors relating to our operations and business environment, all of which are difficult to predict and many of which are beyond our control, that could cause our actual results to differ materially from those matters expressed in or implied by these forward-looking statements. These risks and uncertainties include, but are not limited to:

- •

- Unfavorable economic, financial and business conditions;

- •

- Global economic crisis;

- •

- Market conditions beyond our control;

- •

- Prolonged decline in the price of coal;

- •

- Decline in global coal or steel demand;

- •

- Prolonged or dramatic shortages or difficulties in coal production;

- •

- Our customer's refusal to honor or renew contracts;

- •

- Our ability to collect payments from our customers;

- •

- Weather patterns and conditions affecting production;

- •

- Geological, equipment and other operational risks associated with mining;

- •

- Availability of adequate skilled employees and other labor relations matters;

- •

- Title defects preventing us from (or resulting in additional costs for) mining our mineral interests;

- •

- Availability of licenses, permits, and other authorizations may be subject to challenges;

- •

- Concentration of our mineral operations in a limited number of areas subjects us to risk;

- •

- A significant reduction of, or loss of purchases by our largest customer;

- •

- Unavailability of cost-effective transportation for our coal;

- •

- Availability, performance and costs of railroad, barge, truck and other transportation;

- •

- Disruptions or delays at the port facilities used by the Company;

- •

- Risks associated with our reclamation and mine closure obligations; including failure to obtain or renew surety bonds;

- •

- Inaccuracies in our estimates of coal reserves;

- •

- Estimates concerning economically recoverable coal reserves;

1

- •

- Significant cost increases and delays in the delivery of raw materials, mining equipment and purchased components;

- •

- Failure to meet project development and expansion targets;

- •

- Risks associated with operating in foreign jurisdictions;

- •

- Significant increase in competitive pressures and foreign currency fluctuations;

- •

- New laws and regulations to reduce greenhouse gas emissions that impact the demand for our coal reserves;

- •

- Greater than anticipated costs incurred for compliance with environmental liabilities or limitations on our ability to

produce or sell coal;

- •

- Future regulations that may increase our costs or limit our ability to produce coal;

- •

- Risks related to our indebtedness and our ability to generate cash for our financial obligations;

- •

- Inability to access needed capital;

- •

- Events beyond our control may result in an event of default under one or more of our debt instruments;

- •

- Costs related to our post-retirement benefit obligations and workers' compensation obligations;

- •

- Downgrade in our credit rating;

- •

- Adverse rulings in current or future litigation;

- •

- Our ability to attract and retain key personnel;

- •

- Our ability to identify suitable acquisition candidates to promote growth;

- •

- Our ability to successfully integrate acquisitions, including the acquisition of Western Coal Corp.;

- •

- Volatility in the price of our common stock;

- •

- Our ability to pay regular dividends to stockholders;

- •

- Our exposure to indemnification obligations; and

- •

- Other factors, including the other factors discussed in Item 1A, "Risk Factors," as updated by any subsequent Form 10-Qs or other documents that are on file with the Securities and Exchange Commission.

When considering forward-looking statements made by us in this Annual Report on Form 10-K ("Form 10-K"), or elsewhere, such statements speak only as of the date on which we make them. New risks and uncertainties arise from time to time, and it is impossible for us to predict these events or how they may affect us. We have no duty to, and do not intend to, update or revise the forward-looking statements in this Form 10-K after the date of this Form 10-K, except as may be required by law. In light of these risks and uncertainties, keep in mind that any forward-looking statement made in this Form 10-K or elsewhere might not occur.

2

GLOSSARY OF SELECTED MINING TERMS

Anthracite coal. A hard natural coal containing few volatile hydrocarbons which burns slowly and gives intense heat almost without flame.

Ash. Impurities consisting of silica, iron, alumina and other incombustible matter that are contained in coal. Since ash increases the weight of coal, it adds to the cost of handling and can affect the burning characteristics of coal.

Assigned reserves. Coal that is planned to be mined at an operation that is currently operating, currently idled, or for which permits have been submitted and plans are eventually to develop the mine and begin mining operations.

Bituminous coal. A common type of coal with moisture content less than 20% by weight. It is dense and black and often has well-defined bands of bright and dull material.

British thermal unit, or "Btu". A measure of the thermal energy required to raise the temperature of one pound of pure liquid water one degree Fahrenheit at the temperature at which water has its greatest density (39 degrees Fahrenheit).

Coal seam. Coal deposits occur in layers. Each layer is called a "seam."

Coke. A hard, dry carbon substance produced by heating coal to a very high temperature in the absence of air. Coke is used in the manufacture of iron and steel. Its production results in a number of useful by-products.

Compliance coal. Coal which, when burned, emits 1.2 pounds or less of sulfur dioxide per million Btus, as required by Phase II of the Clean Air Act.

Continuous miner. A machine used in underground mining to cut coal from the seam and load onto conveyers or shuttle cars in a continuous operation. In contrast, a conventional mining unit must stop extracting in order to begin loading.

Continuous mining. A form of underground mining that cuts the coal from the seam and loads the coal on to a conveyor system continuously, thus eliminating the separate cycles of cutting, drilling, shooting and loading.

Hard coking coal. Hard coking coal is a type of metallurgical coal that is a necessary ingredient in the production of strong coke. It is evaluated based on the strength, yield and size distribution of coke produced from such coal which is dependent on rank and plastic properties of the coal. Hard coking coals trade at a premium to other coals due to their importance in producing strong coke and as they are a limited resource.

Industrial coal. Coal generally used as a heat source in the production of lime, cement, or for other industrial uses and is not considered thermal coal or metallurgical coal.

Longwall mining. A form of underground mining that employs a shearer with two rotating drums pulled mechanically back and forth across a long exposed coal face. A hydraulic system supports the roof of the mine while the drums are mining the coal. Conveyors move the loosened coal to an underground mine conveyor which transports to the surface. Longwall mining is the most efficient underground mining method.

Metallurgical coal. The various grades of coal with suitable carbonization properties to make coke or be used as a pulverized injection ingredient for steel manufacture, including hard coking coal (see definition above), semi-soft coking coal (SSCC) and PCI coal (see definition below). Also known as "met" coal, its quality depends on four important criteria: (1) volatility, which affects coke yield; (2) the

3

level of impurities including sulfur and ash, which affect coke quality; (3) composition, which affects coke strength; and (4) other basic characteristics that affect coke oven safety. Met coal typically has particularly high Btu characteristics but low ash and sulfur content.

Nitrogen oxide (NOx). Produced as a gaseous by-product of coal combustion. It is a harmful pollutant that contributes to smog.

Overburden. Layers of earth and rock covering a coal seam. In surface mining operations, overburden must be removed prior to coal extraction.

PCI Coal. Coal used by steelmakers for pulverized coal injection (PCI) into blast furnaces to use in combination with the coke used to produce steel. The use of PCI allows a steel maker to reduce the amount of coke needed in the steel making process.

Preparation plant. Preparation plants are usually located on a mine site, although one plant may serve several mines. A preparation plant is a facility for crushing, sizing and washing coal to remove impurities and prepare it for use by a particular customer. The washing process has the added benefit of removing some of the coal's sulfur content.

Probable reserves. Reserves for which quantity and grade and/or quality are computed from information similar to that used for proven reserves, but the sites for inspection, sampling and measurement are farther apart or are otherwise less adequately spaced. The degree of assurance, although lower than that for proven reserves, is high enough to assume continuity between points of observation.

Proven reserves. Reserves for which: (a) quantity is computed from dimensions revealed in outcrops (part of a rock formation that appears at the surface of the ground), trenches, workings or drill holes; (b) grade and/or quality are computed from the results of detailed sampling; and (c) the sites for inspection, sampling and measurement are spaced so closely and the geologic character is so well defined that size, shape, depth and mineral content of reserves are well-established.

Recoverable reserves. Tons of mineable coal which can be extracted and marketed after deduction for coal to be left behind within the seam (i.e. pillars left to hold up the ceiling, coal not economical to recover within the mine, etc.) and adjusted for reasonable preparation and handling losses.

Reclamation. The process of restoring land and the environment to their original or otherwise rehabilitated state following mining activities. The process commonly includes "recontouring" or reshaping the land to its approximate original appearance, restoring topsoil and planting native grass and ground covers. Reclamation operations are usually underway before the mining of a particular site is completed. Reclamation is closely regulated by both state and federal law.

Reserve. That part of a mineral deposit that could be economically and legally extracted or produced at the time of the reserve determination.

Roof. The stratum of rock or other mineral above a coal seam; the overhead surface of a coal working place.

Sulfur. One of the elements present in varying quantities in coal that contributes to environmental degradation when coal is burned. Sulfur dioxide is produced as a gaseous by-product of coal combustion.

Surface mine. A mine in which the coal lies near the surface and can be extracted by removing the covering layer of soil (see "Overburden") without tunneling underground. About two-thirds of total U.S. coal production comes from surface mines.

4

Thermal coal. Coal used by power plants and industrial steam boilers to produce electricity, steam or both. It generally is lower in Btu heat content and higher in volatile matter than metallurgical coal.

Tons. A "short" or net ton is equal to 2,000 pounds. A "metric" ton is approximately 2,205 pounds; a "long" or British ton is equal to 2,240 pounds. Unless otherwise indicated, the metric ton is the unit of measure referred to in this document. The international standard for quoting price per ton is based in U.S. dollars per metric ton.

Unassigned reserves. Coal that is likely to be mined in the future, but which is not considered Assigned reserves.

Underground mine. Also known as a "deep" mine, it is usually located several hundred feet or more below the earth's surface, an underground mine's coal is typically removed mechanically and transferred by shuttle car and conveyor to the surface. Underground mines account for about one-third of annual U.S. coal production.

5

Introduction and History

We are a leading producer and exporter of metallurgical coal for the global steel industry and also produce thermal coal and industrial coal, anthracite, metallurgical coke, coal bed methane gas ("natural gas") and other related products. We trace our roots back to 1946 when Jim Walter began a homebuilding business in Tampa, Florida. Although initially focused on Homebuilding, the company Mr. Walter founded later became Jim Walter Corporation and branched out into different businesses, including the 1972 development of four underground coal mines in the Blue Creek coal seam near Brookwood, Alabama. In 1987 a group of investors that included Jim Walter formed a new company, subsequently named Walter Industries, Inc., and the following year completed a leveraged buyout of most of the businesses of Jim Walter Corporation. In 1997, Walter Industries, Inc. began trading on the New York Stock Exchange. In 2009 we closed our Homebuilding business, spun off our Financing business and certain other businesses and closed others to focus on the operations related to mining. With our remaining businesses concentrated in coal and natural gas, we changed our name to Walter Energy, Inc. in April 2009.

On April 1, 2011, we completed the acquisition of all the outstanding common shares of Western Coal Corp. ("Western Coal"). The acquisition included high quality metallurgical coal mines in Northeast British Columbia (Canada), high quality metallurgical coal and compliant thermal coal from mines in West Virginia (United States), and high quality anthracite coal and compliant thermal coal from the mines in South Wales (United Kingdom, "U.K."). The acquisition of Western Coal substantially increased our reserves available for future production, the majority of which is metallurgical coal, and created a diverse geographical footprint with strategic access to high-growth steel-producing countries in both the Atlantic and Pacific basins.

On May 6, 2011, we acquired mineral rights for approximately 68 million metric tons of recoverable Blue Creek metallurgical coal reserves to the Northwest of our existing Alabama mines from a subsidiary of Chevron Corporation. The mineral leases form the core of the Blue Creek Energy Project which is a planned new underground metallurgical coal mine. In addition, we acquired Chevron Corporation's existing North River thermal coal mine in Fayette and Tuscaloosa Counties of Alabama and a barge load-out facility near the Port of Mobile terminal in Mobile, Alabama.

Overview

Our primary business, the mining and exporting of metallurgical coal for the steel industry, is conducted by two business segments, our U.S. Operations segment and our Canadian and U.K. Operations segment. Beginning with the second quarter of 2011, as a result of the Western Coal acquisition, the Company revised its reportable segments by arranging them geographically. We now report all of our operations located in the U.S. under the U.S. Operations segment, including the West Virginia mining operations acquired through the acquisition of Western Coal. We report our mining operations acquired through the Western Coal acquisition located in Northeast British Columbia and South Wales under the Canadian and U.K. Operations segment.

The U.S. Operations segment includes the operations of our underground mines, surface mines, coke plant and natural gas operations located in Alabama and our underground and surface mining operations located in West Virginia. Our Alabama mining operations mine metallurgical coal from both underground and surface mines. At our legacy Alabama underground mining operations we mine high quality metallurgical coal from the Blue Creek coal seam. Our legacy Alabama underground mines are 1,400 to 2,100 feet underground, making them some of the deepest vertical shaft coal mines in North America. Metallurgical coal mined from the Blue Creek seam contains very low sulfur, has strong

6

coking properties and high heat value making it ideally suited as a coking coal for steel makers. The Alabama operations also mine thermal coal for sale to industrial and electric utility customers at our surface mines and the underground North River Mine. Our Alabama mining operations have convenient access to the port of Mobile, Alabama through barge and railroad allowing us to minimize our transportation costs. In 2012, the Alabama mining operations produced 6.5 million metric tons of hard coking coal and 2.7 million metric tons of thermal coal.

The U.S. Operations segment also extracts methane gas, principally from the Blue Creek coal seam. Our natural gas business represents one of the most extensive and comprehensive commercial programs for coal seam degasification in the country, producing approximately 50 million cubic feet of gas daily from over 1,740 wells.

Through the acquisition of Western Coal, we acquired two underground and two surface mines located in West Virginia, which produce both metallurgical coal and thermal coal. The West Virginia mining operations lie within the Appalachian coal-producing region. In 2011 and 2012, we temporarily idled the underground and surface operations, respectively, at the Gauley Eagle properties until such time as coal prices improve. Our West Virginia mining operations operate a rail-loading facility and utilize an extensive network of public roads to transport coal to markets or independent river terminals for transfer to barges along the Kanawha River. In 2012, the West Virginia mining operations produced approximately 480 thousand metric tons of metallurgical coal and 390 thousand metric tons of thermal coal.

The Canadian and U.K. Operations segment includes the operations of surface mines in Northeast British Columbia (Canada) and an underground mine and surface mine in South Wales (U.K.) The Canadian operations consist of three surface mines that produce primarily hard coking and low-volatile PCI coals. The Canadian mines are located adjacent to or nearby existing infrastructure established for the Northeast British Columbia coalfields, including established rail and road networks that are available all year round. Coal produced from the mines is shipped by rail to a coal terminal facility at the Port of Prince Rupert, British Columbia. The U.K. mining operation mined anthracite coal from its underground mine and thermal coal from its surface mine. In 2012, the Company idled the development of the underground operations until such future time as coal prices adequately rebound and in 2013 the surface mine operations will be closed. All coal mined is processed at the Company's nearby preparation plants where both road and rail coal transportation are available. In 2012, the Canadian and U.K. mining operations produced 2.0 million metric tons of hard coking coal and 2.5 million metric tons of low volatile PCI coal.

The financial results of our industry segments are included in Note 21 of "Notes to Consolidated Financial Statements" included in this Form 10-K.

Business Strategy

Our objective is to increase shareholder value through sustained earnings growth and free cash flow generation. Our key strategies to achieve this objective are described below:

Increasing Metallurgical Coal Production Capacity. Full year 2012 metallurgical coal production was 11.5 million metric tons, of which 78% was hard coking coal and the remainder low-volatile PCI coal. We expect full year 2013 metallurgical coal production to be in line with production levels in 2012. We believe we are well positioned to increase production when market conditions warrant. Our long-term production growth is expected to be balanced between existing production assets and growth assets such as Blue Creek Energy, Belcourt-Saxon and Aberpergwm.

Capitalizing on Favorable Long-Term Industry Dynamics. Although coal prices have been volatile over the past several years, we believe the long-term fundamentals of the global metallurgical coal industry are favorable. Given our premium product and diverse operations, we believe we are well

7

positioned to capitalize on the expected growth by delivering high quality metallurgical coal to the European, Asian and Latin American markets.

Focusing on Reducing Costs. We seek to maintain our focus on reducing costs. We plan on leveraging our infrastructure to increase production and to drive down our cost per ton through economies of scale. We anticipate reducing costs further through, among other initiatives, increased utilization of the Falling Creek Connector Road in Canada, longer panels on the Blue Creek No. 4 mine in Alabama, efficiencies from transitioning Brule to an owner-operated mine and a more centralized supply chain. We anticipate these improvements, combined with competitive transportation costs and a premium product, will expand our margins further.

Continuing to Provide a Mix of Coal Types and Quantities to Satisfy Our Customers' Needs Across a Variety of Geographic Markets. By having the ability to produce a variety of metallurgical coal types in three different countries with direct access to Atlantic and Pacific markets, we are able to source and blend our coal from multiple mines to meet the specific needs of our customers. Our broad geographic scope and mix of coal qualities provide us with the opportunities to work with leading steel producers across the globe and provide premium met coal to regions with high and/or growing demand for coal.

Upholding Our Commitment to Excellence in Safety and Environmental Stewardship. We intend to maintain our recognized leadership in operating safe mines and in achieving environmental excellence. In addition, our ability to minimize workplace incidents and environmental violations improves our operating efficiency, which directly improves our cost structure and operational performance.

The Coal Industry

Coal is one of the most important energy sources in the world, providing approximately 30% of the world's primary energy needs according to the World Coal Association ("WCA"). Per the WCA, the largest coal users are in China, the U.S., India, Russia and Japan. The most significant uses for coal are for electricity generation, steel production, cement manufacturing and as a liquid fuel. According to the WCA, approximately 70% of global steel production relies directly on inputs of metallurgical coal. After coking coal is converted to coke it is used in blast furnaces to smelt iron ore which is subsequently used to produce steel. The steel industry uses coking coal which is distinguishable from other types of coal by its characteristics: lower volatility, lower sulfur and ash content and favorable coking characteristics (higher coke strength). Additionally, metallurgical coal has a higher Btu value. Approximately 29% of steel is also produced in electric arc furnaces. The top five steel producing countries are China, Japan, the United States, India and Russia. In 2012, approximately 1.5 billion metric tons of steel was produced globally, relatively equal to that in 2011.

According to the WCA, approximately 41% of the world's electricity is generated from coal while its use is expected to rise to over 50% to 2030 primarily to meet the expanded use of electricity. According to the International Energy Agency ("IEA"), during 2012, coal was used to generate approximately 45% of the electricity in the United States. Per the IEA, coal's share of the global energy mix will continue to rise, and by 2017 coal will come close to surpassing oil as the world's top energy source.

Coal reserves, primarily thermal, are available in almost every country worldwide, with recoverable reserves in around 70 countries. According to the WCA it has been estimated that there are over 861 billion tons of proven coal reserves worldwide, which is enough coal to last approximately 112 years at current rates of consumption. The largest coal reserves are in the U.S., Russia, China and India. Coal's appeal is that it is readily available from a wide variety of sources; its prices have been lower and more stable than oil and gas prices over the long-term; and it is likely to remain the most affordable fuel available for power generation in many developing and industrialized nations for several decades per the WCA.

8

U.S. coal production declined 6.9% in 2012 driven by the decrease in domestic consumption, according to the Energy Information Administration's ("EIA") short-term energy outlook. U.S. coal production is expected to decline by a further 1.2% in 2013, as drawdowns for stock piled inventory combined with a small increase in coal imports are used to meet the small anticipated consumption increase in 2013. The top five coal producing countries in the world are China, the United States, India, Australia and Indonesia.

Coal is traded all over the world, with coal shipped significant distances by sea to reach certain markets. Over the last 20 years, seaborne trade in thermal coal has increased on average by about 7% each year and seaborne coking coal trade has increased by 1.6% per year, according to the WCA. According to the WCA, the largest exporters of coal in 2012 were Australia, Indonesia, Russia and the United States. The leading exporters of metallurgical coal for steel making, per the WCA, are Australia, the United States and Canada. According to the EIA, U.S. coal exports are currently projected to total a record 125 million short tons in 2012 and are anticipated to decline in 2013. Although exports are anticipated to decline in 2013, exports are still expected to remain in excess of 100 million short tons making 2013 the third straight year at such levels. The primary reasons for the expected decline in coal exports include anticipated continuing economic weakness in Europe, lower international coal prices, and increasing production in Asia.

Coal Characteristics

Coal is generally classified as either metallurgical coal or thermal coal (also known as steam and industrial coal). Sulfur, ash and moisture content as well as coking characteristics are key attributes in grading metallurgical coal while heat value, ash and sulfur content are important variables in rating thermal coal. We currently mine, process, market and ship coal with the characteristics described below.

Heat Value: The heating value of coal is supplied by its carbon content and volatile matter and commonly measured in British thermal units ("Btus"). Coal deposits are generally classified into four categories, ranging from lignite, subbituminous, bituminous and anthracite, reflecting their response to increasing heat and pressure. We primarily mine bituminous coal which is used to make coke and PCI coal for the steel industry or generate electricity with a heating value ranging between 10,500 and 15,500 Btus per pound. Anthracite coal has the highest carbon content and a heat value nearing 15,000 Btus per pound. Approximately 89% of our proven and probable reserves have heat value characteristics above 13,500 Btus per pound, which make it very desirable to our customers.

Sulfur Content: Although sulfur content can differ from seam to seam, approximately 95% of our estimated 401.0 million metric tons of proven and probable reserves are low sulfur coals, which are preferred by our customers. Low sulfur coals have a sulfur content of 1.5% or less. Coal produces undesirable sulfur dioxide when it burns, the amount of which depends on the concentration of sulfur in the coal as well as the chemical composition of the coal itself.

Ash and Moisture Content: Ash is the residue that remains after the combustion of coal. Low ash is desirable because businesses must dispose of ash after the coal is used. High moisture content decreases the heat value of the coal and increases the coal's weight both of which are undesirable. Our metallurgical coal, particularly the coal from the Blue Creek seam in Alabama, has a low ash rating and moisture content which is highly desirable to our customers.

Coking Characteristics (metallurgical coal only): Two important coking characteristics are coke strength and volatility. Volatility of coking coal is used to determine the percentage of coke that a given type of coal would produce. This measure is known as coke yield. A low volatility results in a higher coke yield. Our metallurgical coal, particularly the coal from the Blue Creek seam in Alabama, has both a high rating for coke strength as well as a low measure of volatility.

9

Types of Coal

Metallurgical coal is classified into three major categories of hard coking coal ("HCC"), semi-soft coking coal, and pulverized coal injection coal ("PCI"). Coking coals are the basic ingredients for manufacture of metallurgical coke. PCI coal is not used in coke making but is rather injected directly into the lower region of blast furnaces to supply both energy and carbon for iron reduction. The use of PCI can be a substitute for some of the metallurgical coke that would otherwise have been used.

Thermal and industrial coal is the most abundant form of coal and is commonly referred to as steam coal. Such coal has a relatively high heat value and has long been used for steam generation in electric power and industrial boiler plants.

Anthracite coal is commonly used as a reduction agent for various applications such as briquetting, charcoal and iron ore pellets. Due to our low production levels of anthracite thus far, we have been selling anthracite primarily as a domestic fuel in either hand fired stoker or automatic stoker furnaces. Once the Aberpergwm mine development is completed, our intent is to sell anthracite coal into the PCI coal market. Anthracite is a crossover coal and has been successfully used in the PCI coal market.

Coal Mining Methods

We mine coal using both underground and surface mining methods. The mining methods that we employ are determined by the geological characteristics of our coal reserves.

Underground Mining: We employ underground mining methods when our coal reserves are located deep beneath the surface. Our underground mines typically use the two different mining techniques of longwall mining and room-and-pillar mining. In 2012, approximately 60% of the coal we produced was from underground mining operations.

In longwall mining, mechanized shearers are used to cut and remove the coal from long rectangular blocks of medium to thick seams. Continuous miners are used to develop access to these coal blocks. After the coal is removed, it drops onto a conveyor system, that will ultimately take the coal to production shafts or slopes where it will be hoisted to the surface. In longwall mining, mobile hydraulic powered roof supports hold up the roof throughout the extraction process. This method of mining has proven to be more efficient than other mining methods, with an extraction rate of nearly 100 percent. The equipment is however more expensive than that for other conventional mining methods and cannot be used in all geological circumstances. In longwall mining, only the gate entries are bolted. The longwall panel is allowed to collapse behind the shields which hold the roof as coal is extracted and the shields progress through the coal block.

Underground mining with longwall technology drives greater production efficiency, improved safety, higher coal recovery and lower production costs. We currently operate four longwall mining systems at our Alabama underground mining operations for primary production and four to six continuous miner sections in each mine for the development of main and longwall panel entries. Our operating plan is a longwall to continuous miner production ratio of approximately 80% to 20%.

In room-and-pillar mining, a network of rooms are cut into the coal seam by remote-controlled continuous miners, while also leaving a series of coal pillars to support the mine roof. Shuttle cars and battery coal haulers transport coal to conveyor belt systems for further transportation to the surface. Ultimate seam recovery is typically less than that achieved with longwall mining as the pillars left behind as part of this mining method can constitute up to 40% of the total coal seam. We employ this method to mine smaller blocks of coal where longwall mining is not feasible.

Surface Mining: We employ surface mining methods when our coal reserves are located close to the surface. In 2012, approximately 40% of the coal we produced came from surface mining operations.

10

Surface mining involves removing the topsoil followed by a process of drilling and blasting the earth (overburden) covering the coal seam with explosives. The overburden is then removed with heavy earth-moving equipment such as draglines, power shovels, excavators and loaders exposing the coal seam. Once exposed, the coal seam is extracted and loaded into haul trucks for transportation to a preparation plant or load-out facility. After the coal is removed as part of our normal mining activities, we use the topsoil and overburden removed at the beginning of the process to backfill the excavated coal pits and reclaims disturbed areas. Once we replace the overburden and topsoil, we reestablish vegetation and plant life into the reclaimed area and make other improvements that provide local community and environmental benefits. Ultimate seam recovery for surface mining typically exceeds 80% and is dependent on overburden, coal thickness, geological factors, and equipment used.

Description of Our Business

We operate our business through two principal business segments of the U.S. Operations and Canadian and U.K. Operations. Our business segment financial information is included in Note 21 within the "Notes to Consolidated Financial Statements" included herein. During 2012, we actively operated 11 mines. For a comprehensive summary of all of our coal properties and of our coal reserves and production levels, see the tables summarizing our coal reserves and production in "Item 2. Properties" contained within this Form 10-K.

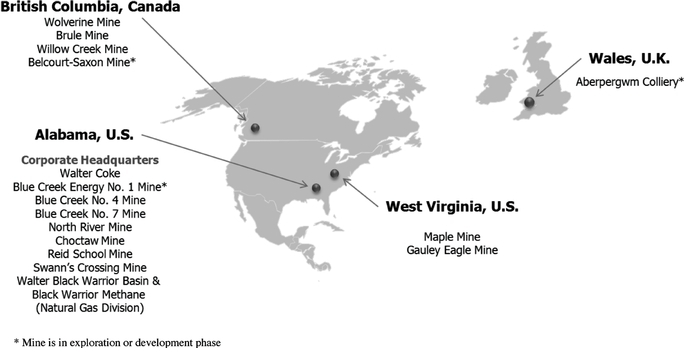

The following map shows the major locations of our mining operations:

U.S. Operations

The U.S. Operations segment includes hard coking coal and thermal coal mines in both Alabama and West Virginia, a coke plant in Alabama, and coal bed methane extraction operations also located in Alabama. Metallurgical coal production totaled 7.0 million metric tons and thermal coal production totaled 3.1 million metric tons in 2012.

11

Alabama Operations: Our mining operations in Alabama consist of two underground hard coking coal mines in Southern Appalachia's Blue Creek coal seam (the No. 7 Mine, which includes No. 7 East, and the No. 4 Mine), one underground thermal coal mine (the North River Mine), one surface hard coking coal mine (the Reid School Mine) and two surface hard coking and thermal coal mines (the Swann's Crossing Mine and the Choctaw Mine).

Our Alabama underground mining operations are headquartered in Brookwood, Alabama and as of December 31, 2012 were estimated to have approximately 203.4 million metric tons of recoverable reserves located in west central Alabama between the cities of Birmingham and Tuscaloosa. Operating at approximately 2,000 feet below the surface, the No. 4 and No. 7 mines are two of the deepest underground coal mines in North America. The coal is mined using longwall extraction technology with development support from continuous miners. We extract coal primarily from Alabama's Blue Creek seam, which contains high-quality bituminous coal. Blue Creek coal offers high coking strength with low coking pressure, low sulfur and low-to-medium ash content with high Btu values that can be sold either as hard coking coal (used to produce coke) or as compliance thermal coal (used by electric utilities because it meets current environmental compliance specifications).

The coal from our No. 4 and 7 mines is currently sold as a high quality low and mid-vol hard coking coal. At forecasted production levels, we estimate the current reserves at these mines to have a 20 to 29 year life. As described previously, in May 2011 we acquired mineral rights for approximately 68 million additional metric tons of recoverable Blue Creek hard coking coal reserves located to the northwest of our No. 4 mine. The related mineral leases are expected to form the core of the Blue Creek Energy Project which is for the development of a new underground hard coking coal mine that has an estimated life of 40 to 45 years. Mines No. 4 and No.7 are located near Brookwood, Alabama, and are serviced by CSX rail. Both mines also have access to our barge load-out facility on the Black Warrior River. Service via both rail and barge culminates in delivery to the Port of Mobile, where shipments are exported to our international customers via ocean vessels. Approximately 96% of the hard coking coal sales from our Alabama underground mining operations consist of sales to international customers.

A coal producer is typically responsible for transporting the coal from the mine to an export coal-loading facility. Exported coal is usually sold at the loading port, with the buyer responsible for further transportation from the port to their location. Our Alabama mines are conveniently located near both river barge load-out facilities and railroad transportation (CSX rail) with direct access to the Port of Mobile, minimizing our transportation costs.

In May 2011 we acquired Chevron Corporation's existing North River thermal coal mine in Alabama. The North River Mine is near the end of its life and mining is currently expected to be completed in 2014.

Our Alabama natural gas operations extract and sell coal bed methane gas from the coal seams owned or leased by the Company and others. Prior to May 2010, our natural gas operations consisted solely of the Black Warrior Methane Corp., an equal ownership venture with E&P Company, a subsidiary of EP Energy LLC (EP Energy). In May 2010, we acquired HighMount Exploration and Production Alabama, LLC's coal bed methane business. The acquisition of this business included approximately 1,300 conventional gas wells, pipeline infrastructure and related equipment located adjacent to our existing underground mining and coal bed methane business. In addition, these wells degasify methane from the area where our new Blue Creek Energy mine is located. As of December 31, 2012, we had 1,746 wells that produced approximately 18.1 billion cubic feet of natural gas in 2012. The degasification operations have improved mining operations and safety by reducing methane gas levels in our mines.

We are currently operating three surface mines in Alabama. The Choctaw Mine is located near Parrish in Walker County, Alabama and produces thermal and hard coking coal. The mine has an

12

onsite rail facility serviced by Norfolk Southern rail. Access to Highway 269 provides delivery access to local customers via truck. The Reid School Mine is located in Blount County, Alabama and primarily produces hard coking coal. Access to Highway 79 provides delivery to local customers via truck. Hard coking coal mined at the Reid School Mine is primarily sold to our Coke plant and underground mining operations for resale. The Swann's Crossing Mine is located in Tuscaloosa County near Brookwood, Alabama and produces both hard coking and thermal coal. The mine has access to our barge load-out facility on the Black Warrior River.

We also own other surface mine coal reserves including the Flat Top surface mine that is a thermal mine and is ready for operation once market conditions permit. This mine is located in Adamsville, Alabama near Highway 78 and expectations are that any coal produced would be delivered to local customers via truck.

Additionally, we operate the, Walter Coke Plant, located in Birmingham, Alabama. The plant's major product line is metallurgical coke, which includes coke for furnace and foundry applications. Foundry coke is marketed to ductile iron pipe plants and foundries producing castings, such as for the automotive and agricultural equipment industries. Furnace coke is sold to the domestic and international steel industry for producing steel in blast furnaces. The plant utilizes up to 120 coke ovens with a capacity to annually produce up to 381,000 tons of metallurgical coke and is the second largest merchant foundry coke producer in the United States.

West Virginia Operations: We acquired four mines on two properties in West Virginia through the acquisition of Western Coal on April 1, 2011. Mines on these properties produce both hard coking and thermal coal. The two properties are the Gauley Eagle and Maple properties and each has an underground mine and surface mine.

The Maple Coal mines, located in Fayette and Kanawha counties and the Gauley Eagle mines located in Nicholas and Webster counties of West Virginia are estimated to contain approximately 46.3 million metric tons of recoverable reserves within the Appalachian coal-producing region as of December 31, 2012. The Maple underground coal mine mines in the Eagle coal seam and employs room-and-pillar mining method with continuous miners to produce premium high volatile coking coal, which can be used in the steelmaking process. Due to the challenges in the short-term market outlook and the weak backdrop in demand in 2012, we reduced production at the Maple underground mine. The Gauley Eagle underground mine also employs the room-and-pillar mining method to produce a semisoft coking coal, which can be used in the steelmaking process or as a premium low-sulfur thermal coal. Coal produced at the Maple and Gauley Eagle surface mines is primarily sold in the thermal market. The Gauley Eagle underground mine and Gauley Eagle surface mine were temporarily idled in mid-2011 and mid-2012; respectively, due to economic conditions. The personnel and equipment at these mines was reallocated to the Maple underground and surface mines. At forecasted production levels, we estimate the current reserves in these properties to have a 20-25 year life.

Coal from the Gauley Eagle and Maple mines is either transported by rail or by barge on the river systems to our customers. Coal shipped from our rail load-out facility can access regional markets and ports on the eastern U.S. seaboard. Coal shipped by barge on the river systems is trucked to the Kanawha River and shipped locally or offshore via the Mississippi River or Tennessee-Tombigbee river system. The transportation infrastructure and strategic location of the mines near its customers, ensures continuous and reliable delivery of our products.

The coking coal produced by our West Virginia operations is sold to domestic coke plants and international steel mills, while the thermal coal is sold domestically to regional electrical power plants on the eastern U.S. seaboard. Production comes from approximately 20 mineable seams which allow us to blend coal to many quality specifications that our customers request.

13

Canadian and U.K. Operations

Canadian Operations: The Canadian mining operations currently operate three surface metallurgical coal mines in Northeast British Columbia's coalfields (the Wolverine Mine, the Brule Mine, and the Willow Creek Mine). Within British Columbia, the Company holds the right to two large multi-deposit coal property groups: the Wolverine group, including the Perry Creek (Wolverine Mine), EB and Hermann deposits; and the Brazion group, including the Brule Mine and the Willow Creek Mine and less explored portions of these properties and adjacent properties. We also have a 50% interest in the Belcourt-Saxon multi-deposit coal property groups described below.

Our Canadian surface mining operations are located in Northeast British Columbia near the towns of Tumbler Ridge and Chetwynd. Our Canadian operations are estimated to have approximately 135.8 million metric tons of recoverable coal reserves including 72.1 million metric tons at potential future mine sites as of December 31, 2012. The Wolverine surface mine is located near the town of Tumbler Ridge and produces a high grade hard coking coal. We expect mining at the Wolverine mine to continue until approximately 2017. Future projects at Wolverine include the EB and Hermann surface mines which are currently expected to each have lives of 10 years. The Brule surface mine is located near the town of Chetwynd and produces a premium grade low-volatile PCI coal. We expect mining at the Brule mine to continue until approximately 2023. The Willow Creek surface mine, also located near the town of Chetwynd, produces metallurgical coal with production plans of one third hard coking coal and two thirds low-volatile PCI coal over the mine's life which is currently expected to be through 2024.

A key strategic advantage of the Canadian operations is the proximity to existing infrastructure. Our wholly-owned properties are located near rail and port infrastructure that is operational all year around. The rail line covers approximately 590 miles from our mines to the port at Prince Rupert, British Columbia. From the port facility, shipments are exported to our international customers via ocean vessels. This combined infrastructure provides cost effective and reliable delivery of our products to our customers.

Our Falling Creek connector road project was substantially commissioned near the end of the 2011 third quarter and truck hauling volumes on the road have continued to increase throughout 2012. The road connects the Brule mine to the Willow Creek mine where Brule's coal is processed and loaded at the rail load-out facility. The new road allowed us to increase our hauling capacity per truck and reduces the hauling distance as compared to the previous route from just over 62 miles down to 37 miles.

The metallurgical coal produced by our Canadian operations is sold to international customers located primarily in Asia to meet the demand for steel produced in the region. Our Wolverine mine's hard coking coal forms a key coke oven blend component with many of the leading steel mills in Asia. The Brule and Willow Creek low-volatile PCI coal is ranked as a premium PCI coal and can replace up to 30% of the coke requirement in a blast furnace. Willow Creek also has hard coking coal reserves that we began to mine in 2012. These high quality metallurgical coals, in conjunction with the infrastructure present in Northeast British Columbia, provide us with an opportunity to grow and diversify our customer base.

Additionally, we have a 50% interest in the Belcourt Saxon Coal Limited Partnership which includes two multi-deposit metallurgical coal properties comprising approximately 28.5 million metric tons of recoverable reserves which are located approximately 40 to 80 miles south of our Wolverine mine. We believe that the area has the potential to support significant mining operations and we expect that the partnership will develop these properties in the future. We also own or hold an interest in a number of other property assets located in Southeast British Columbia that are in the early stages of development.

14

Mine planning is progressing for the proposed EB and Hermann mines located near our existing Wolverine mine. These mines have approximately 19 million metric tons of recoverable high quality metallurgical coal reserves. Exploration has been completed within the proposed mining areas and production is expected to commence in EB as early as 2016.

U.K. Operation: Our U.K. mining operation consists of an underground and surface mine located in South Wales.

Our U.K. underground operation is estimated to have approximately 15.5 million metric tons of recoverable reserves as of December 31, 2012. The U.K. operation's primary activity has been the development and expansion of the Aberpergwm underground coal mine located at Glynneath in the Neath Valley. In the fall of 2011, we stopped continuous miner development operations to allow us to focus our attention on completing the new drift opening. While we were able to complete the upper section of the drift during 2012, due to challenges related to an oversupply of coal and decreased demand, we took steps to reduce development spending in this U.K. mine until market conditions improve. This mine produces anthracite coal, which can be sold as a low-volatile PCI coal. The surface mine operations produced thermal coal and were temporarily idled in 2012 until such future time as coal prices adequately rebound.

The U.K. operation is well located to take advantage of improved demand from U.K. steel mills and the European export market upon recovery of the global economy. Coal is processed in the operation's new preparation plant and loaded at a nearby rail load-out facility or transported to customers by road. In 2012 the mine supplied thermal coal and anthracite coal to a nearby electrical power plant and for various other commercial purposes.

Coal Preparation and Blending

Our coal mines have coal preparation and blending facilities convenient to each mine. The coal preparation and blending facilities receive, blend, process and ship coal that is produced from the mines. Using these facilities, we are able to ensure a consistent quality and efficiently blend our coal to meet our customers' specifications.

Marketing, Sales and Customers

Coal prices differ substantially by region and are impacted by many factors including the overall economy, demand for steel, demand for electricity, location, market, quality and type of coal, mine operation costs and the cost of customer alternatives. The major factors influencing our business are the economy and the demand for steel. Our Alabama operations' high quality Blue Creek coal and our Canadian operations' high quality hard coking coal are considered among the highest quality coals in the world and are preferred as a base coal in our customers' blends. The low-volatile PCI coal produced by our Canadian operations has proven itself in the marketplace as a desired source for our Asian steel makers. Our marketing strategy is to focus on international markets mostly in Europe, South America and Asia where we have a transportation cost advantage and where our coal is in high demand.

During 2012, approximately 48% of our metallurgical coal shipments were to customers in Europe, approximately 33% to Asia and approximately 16% to South America. We focus on long-term customer relationships where we have a competitive advantage. We sell most of our metallurgical coal under fixed price supply contracts primarily with terms of three months. Some of our sales of metallurgical coal can, however, occur in the spot market as dictated by available supply and market demand.

15

The Company's revenues by coal destination for the year ended December 31, 2012, were as follows:

| |

December 31, 2012 (in thousands) |

|||

|---|---|---|---|---|

Europe |

$ | 922,727 | ||

Asia |

633,162 | |||

North America |

532,078 | |||

South America |

311,928 | |||

Total |

$ | 2,399,895 | ||

During 2012, our five largest customers represented approximately 27% of our sales and, for the year ended December 31, 2012, no single customer accounted for 10% or more of our consolidated revenues. Even in this challenging economy we believe that the loss of these customers would not have a material adverse effect on our results of operations as we believe the loss of volume from these customers would be replaced with sales to other existing or new customers due to the demand for our metallurgical coal.

Our thermal coal is primarily marketed to customers in the United States, generally under long-term contracts.

Trade Names, Trademarks and Patents

The names of each of our subsidiaries are well established in the respective markets they serve. Management believes that customer recognition of such trade names is of significant importance. Our subsidiaries have numerous trademarks. Management does not believe, however, that any one such trademark is material to our individual segments or to the business as a whole.

Competition

Virtually all of our metallurgical coal sales are exported. Our major competitors are businesses that sell into our core business areas of Europe, South America and Asia. We primarily compete with producers of premium metallurgical coal from Australia, Canada and the United States. The principal factors on which we compete are coal prices at the port of shipment, coal quality and characteristics, customer relationships and the reliability of supply. The demand for our hard coking coal is significantly dependent on the general economy and the worldwide demand for steel. Although there are significant challenges in this current difficult economy, we believe that we have competitive strengths in our business areas that provide us with distinct advantages.

Competitive Strengths

Leading "Pure-Play" Metallurgical Coal Producer. We are a leading, global, publicly traded producer and exporter of metallurgical coal for the global steel industry. We had total coal reserves of 401.0 million metric tons as of December 31, 2012, which primarily consists of high quality, premium metallurgical coal. We expect 2013 metallurgical coal production to be in line with production levels in 2012. We believe we are well positioned to increase production when market conditions warrant.

Premium, High Quality Product. Blue Creek coal from our Alabama mining operations is recognized to be among the highest quality coals in the world. Its characteristics include very low sulfur, low ash and low volatility. These high quality characteristics and high heat value make it ideally suited for steel makers as a coking coal. Contract prices for our premium hard coking coal are consistently equal to the benchmark for premium coking coals. Hard coking coal produced from the Canadian mining operations has been well accepted by steel makers, currently having six of the top ten

16

largest steel mills in the region served as customers. The low-volatile PCI coal from the Canadian operations has also been widely accepted by customers.

Attractive Industry Dynamics. We expect that international demand for our metallurgical coal will increase in the future, driven by favorable projected global growth trends and the high quality of our coal compared to many other coal producing regions around the world. Metallurgical coal demand is underpinned by projected growth in world steel production of 3.2% in 2013, according to the World Steel Association. Steel producers are also rebuilding inventories and new supply of metallurgical coal is constrained by rail and port capacity in emerging supply basins.

Sales and Geographic Diversification. We operate up to twelve mines in three countries and have access to both the Atlantic and Pacific Seaborne markets. This geographical advantage provides important diversity in terms of production, markets, transportation and labor. We have operational flexibility due to this diversification, which makes us less reliant on any single mine for a significant portion of our earnings or cash flows. We believe the diversity of our operations and reserves also provides us with a significant advantage over competitors with operations in a single coal producing region as it allows us to diversify our customer base, with no one customer responsible for a significant portion of our revenues. This geographic diversification also allows us to source the high quality coals we produce from multiple sources and to blend to meet the exact specifications of our customers. In addition, with access to both the Atlantic and the Pacific markets, we believe that we are well positioned to take advantage of any growth in the seaborne coal market and to supply metallurgical coal to Latin America, Asia and Europe.

Significant Organic Growth Opportunities. We believe that our organic growth opportunities in metallurgical coal are well balanced between existing production assets and growth development projects such as Willow Creek, Aberpergwm, Blue Creek Energy and Belcourt Saxon. As the demand for high quality metallurgical coal in the global marketplace grows, we expect that we will be able to provide customers with increasing quantities of premium metallurgical coal.

Strong Financial Profile. Our premium priced coal and emphasis on low cost production provides strong margins and free cash flow generation over the long-term. As of December 31, 2012, we had $444.8 million of cash on hand and undrawn capacity under our revolving credit facility and no significant amount of debt maturing until 2015. With a significant portion of total debt prepayable, we expect to further enhance our credit profile through deleveraging.

Port Capacity and Low Cost Transportation Infrastructure. We believe we have sufficient port capacity to ship all of our current production and forecasted production growth. We have an agreement with the Port of Mobile in Alabama through July 31, 2016 with current capacity of approximately 6.5 million metric tons a year and capability to develop our port location properties to add additional capacity as needed. In Canada, Ridley Terminals, located in the port utilized by our Canadian operations, can handle 12 million metric tons per year of coal with the potential to expand to 24 million metric tons per year. We are able to minimize transportation costs due to the close proximity of our mines to our ports, as well as leverage our transportation infrastructure. Our principal mines in our Alabama operations are located a short distance from the Port of Mobile and are serviced by CSX rail. We also have port access through our barge load-out facility on the Black Warrior River. Because customers for our Alabama hard coking coal are primarily in Europe and South America, we are able to ship our coal quickly and at a relatively favorable cost. Our Canadian operations are located on CN Rail's rail lines, minimizing transportation costs to Ridley Terminal.

Highly Regarded and Experienced Management Team. Our top nine officers have an average of more than 30 years of experience. Our management team has demonstrated a history of increasing productivity, increasing production and maintaining strong customer relationships. We are committed to the safety and well-being of our employees and communities, respecting the environment in which we

17

do business, the continued growth of the Company's assets, and putting in place a conservative capital structure while creating long-term shareholder value.

We maintain excellent relationships with our customers. Customers want high quality products, delivered on a timely basis at a fair price. Given our premium products and our production and transportation efficiencies, we have historically been able to reliably deliver premium products at competitive prices on a timely basis. As a result, we have maintained excellent relationships with our customers over many years.

We are able to purchase and blend coal to the customer's specifications. To meet the exact needs of our customers, we are able to blend the high quality coals we produce to meet our customer's requirements at competitive prices.

Environmental and Other Regulatory Matters

Our businesses are subject to numerous federal, state, provincial and local laws and regulations with respect to matters such as permitting and licensing, employee health and safety, reclamation and restoration of property and protection of the environment. In the United States, environmental laws and regulations include, but are not limited to, the federal Clean Air Act ("CAA") and its state and local counterparts with respect to air emissions; the Clean Water Act ("CWA") and its state counterparts with respect to water discharges; the Resource Conservation and Recovery Act ("RCRA") and its state counterparts with respect to solid and hazardous waste generation, treatment, storage and disposal, as well as the regulation of underground storage tanks; and the Comprehensive Environmental Response, Compensation and Liability Act ("CERCLA") and its state counterparts with respect to releases, threatened releases, and remediation of hazardous substances. In Canada, the Company's operations are primarily regulated by provincial legislation, with some regional and federal authorizations required. Applicable environmental laws and regulations include, but are not limited to, the federal Fisheries Act with respect to protection of fish and fish habitat; the Species at Risk Act ("SARA") with respect to protection of identified species at risk, particularly caribou; the British Columbia Environmental Assessment Act with respect to conditions of applicable environmental assessment certificates; the Canadian Environmental Assessment Act with respect to potential federal environmental assessment processes; the British Columbia Mines Act (including the Health, Safety and Reclamation Code); the British Columbia Environmental Management Act and associated regulations with respect to waste discharges, air emissions, hazardous waste disposal, contaminated sites and spills; and the British Columbia Greenhouse Gas Reduction (Cap and Trade) Act with respect to reporting greenhouse gas emissions. Other environmental laws and regulations require reporting, even though the impact of that reporting is unknown. Compliance with these laws and regulations may be costly and time-consuming and may delay commencement, continuation or expansion of exploration or production at our operations. These laws are constantly evolving and becoming increasingly stringent. The ultimate impact of complying with existing laws and regulations is not always clearly known or determinable due in part to the fact that certain implementing regulations for these environmental laws have not yet been promulgated and in certain instances are undergoing revision. These laws and regulations, particularly new legislative or administrative proposals (or judicial interpretations of existing laws and regulations) related to the protection of the environment, could result in substantially increased capital, operating and compliance costs and could have a material adverse effect on our operations and/or our customers' ability to use our products.

We strive to conduct our mining, natural gas and coke operations in compliance with all applicable federal, provincial, state and local laws and regulations. However, due in part to the extensive and comprehensive regulatory requirements, along with changing interpretations of these requirements, violations occur from time to time in our industry and at our operations. In recent years, expenditures for regulatory or environmental obligations in the United States have been mainly for safety or process changes, although some expenditures continue to be made at several facilities to comply with ongoing

18

monitoring or investigation obligations. Expenditures relating to environmental compliance are a major cost consideration for our operations and environmental compliance is a significant factor in mine design, both to meet regulatory requirements and to minimize long-term environmental liabilities. To the extent these expenditures, as with all costs, are not ultimately reflected in the prices of our products and services, operating results will be reduced. We believe that our major North American competitors are confronted by substantially similar conditions and thus do not believe that our relative position with regard to such competitors is materially affected by the impact of environmental laws and regulations. However, the costs and operating restrictions necessary for compliance with environmental laws and regulations may have an adverse effect on our competitive position with regard to foreign producers and operators who may not be required to undertake equivalent costs in their operations. In addition, the specific impact on each competitor may vary depending on a number of factors, including the age and location of its operating facilities, applicable legislation and its production methods.

Permitting and Approvals

Numerous governmental permits and approvals are required for mining operations. We are required to prepare and present to federal, state, provincial and local authorities data pertaining to the effect or impact that any proposed exploration project for production of coal or gas may have upon the environment, the public and our employees. In addition, we must also submit a comprehensive plan for mining and restoring, upon the completion of mining operations, the mined property to its prior state, productive use or other permitted condition. The requirements are costly and time-consuming and may delay commencement or continuation of exploration, production or expansion at our operations. Typically we submit necessary mining permit applications several months, or even years, before we anticipate mining a new area.

Our coking operation is subject to numerous regulatory permits and approvals, including air and water permits. These permits subject us to certain monitoring and reporting requirements. We typically submit necessary permit renewal applications several months prior to expiration.

Applications for permits and permit renewals at our mining, coking and gas operations are subject to public comment and may be subject to litigation from third parties seeking to deny issuance of a permit or to overturn the agency's grant of the permit application, which may also delay commencement, continuation or expansion of our mining, coking and gas operations. Further, regulations provide that applications for certain permits or permit modifications in the United States can be delayed, refused or revoked if an officer, director or a stockholder with a 10% or greater interest in the entity is affiliated with or is in a position to control another entity that has outstanding permit violations. In the current regulatory environment, we anticipate approvals will take even longer than previously experienced, and some permits may not be issued at all. Significant delays in obtaining, or denial of, permits could have a material adverse effect on our business.

U.S. Operations

Mine Safety and Health

The Mine Safety and Health Administration ("MSHA") under the Federal Mine Safety and Health Act of 1977 (the "Mine Act"), and the Mine Improvement and New Emergency Response Act of 2006 (the "MINER Act"), as well as regulations adopted under these federal laws, impose rigorous safety and health standards on mining operations. Such standards are comprehensive and affect numerous aspects of mining operations, including but not limited to: training of mine personnel, mining procedures, ventilation, blasting, use of mining equipment, dust and noise control, communications, and emergency response procedures. MSHA monitors compliance with these laws and standards by regularly inspecting mining operations and taking enforcement actions where MSHA believes there to be non-compliance. Maximum civil penalties for violations of these laws and standards are $70,000 per violation, unless the violation is deemed to be flagrant which can result in a maximum civil penalty of

19

$220,000. These federal mine safety and health laws and regulations have a significant effect on our operating costs.

The MINER Act mandated increased regulations in some of the areas listed above, and some of those regulations are now effective. The MINER Act and other legislative and regulatory initiatives, such as the Dodd-Frank Wall Street Reform and Consumer Protection Act (the "Dodd-Frank Act") passed by the U.S. Congress and signed into law on July 21, 2010 are still ongoing. While the Dodd-Frank Act is focused primarily on the regulation and oversight of financial institutions, it also provides for regulatory compliance requirements related to mining safety and health matters. Section 1503 of the Dodd-Frank Act requires public companies that own or operate a "coal or other mine" in the United States to include certain specified disclosures regarding health and safety violations that may have previously been considered immaterial in their periodic reports filed under the Exchange Act. Section 1503 of the Dodd-Frank Act also requires a reporting company operating coal mines or with subsidiaries that operate coal mines to file a Current Report on Form 8-K upon receipt of written notice from MSHA of an imminent danger order under Section 107(a) of the Mine Act or of any warning from MHSA that the mine either has a pattern of health or safety violations, or has the potential for such a pattern. On August 13, 2012, our wholly-owned subsidiary, Jim Walter Resources, Inc. and the operator of our No. 7 Mine, received imminent danger Order No. 8522884 (the "Order") under section 107(a) of the Mine Act. In the Order, MSHA asserted that methane was allowed to accumulate in a roof cavity in a long crosscut on the underground No. 8 Continuous Miner Section. Shortly thereafter, according to the Order, a line curtain was used "to sweep the methane out," and the Order was quickly terminated. No injuries resulted from the condition described in the Order. See "Exhibit 95" included in this Form 10-K for information concerning mine safety violations and other regulatory matters pursuant to the requirements of Section 1503(a) of the Dodd-Frank Act and Item 104 of Regulation S-K (17 CFR 229.104).

Workers' Compensation and Black Lung

We are insured for workers' compensation benefits for work related injuries that occur within our U.S. operations. We retain the first $1 million to $2 million per accident for all of our U.S. subsidiaries and are insured above the deductible for statutory limits, with the exception of Jim Walter Resources located in Alabama, where we retain any amount in excess of $10 million per accident. Workers' compensation liabilities, including those related to claims incurred but not reported, are recorded principally using annual valuations based on discounted future expected payments using historical data of the division or combined insurance industry data when historical data is limited. In addition, certain of our subsidiaries are responsible for medical and disability benefits for black lung disease under the Federal Coal Mine Health and Safety Act of 1969 and the Mine Act, as amended, and are self-insured against black lung related claims. We perform periodic evaluations of our black lung liability, using assumptions regarding rates of successful claims, discount factors, benefit increases and mortality rates, among others. See "Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations and Financial Condition" for further information on assumptions utilized.

Surface Mining Control and Reclamation Act

The Surface Mining Control and Reclamation Act of 1977 ("SMCRA"), requires that comprehensive environmental protection and reclamation standards be met during the course of and following completion of mining activities. Permits for all mining operations must be obtained from the Federal Office of Surface Mining Reclamation and Enforcement or, where state regulatory agencies have adopted federally approved state programs under the Act, the appropriate state regulatory authority. In Alabama, the Alabama Surface Mining Commission reviews and approves SMCRA permits and the West Virginia Department of Environmental Protection reviews and approves SMCRA permits in West Virginia.

20

SMCRA permit provisions include requirements for coal prospecting, mine plan development, topsoil removal, storage and replacement, selective handling of overburden materials, mine pit backfilling and grading, subsidence control for underground mines, surface drainage control, mine drainage and mine discharge control, treatment and revegetation. These requirements seek to limit the adverse impacts of coal mining and more restrictive requirements may be adopted from time to time.

Before a SMCRA permit is issued, a mine operator must submit a bond or otherwise secure the performance of reclamation obligations. The Abandoned Mine Land Fund, which is part of SMCRA, imposes a general funding fee on all coal produced. The proceeds are used to reclaim mine lands closed or abandoned prior to 1977. On December 7, 2006, the Abandoned Mine Land Program was extended for another 15 years.

SMCRA stipulates compliance with many other major environmental statutes, including: the Clean Air Act, the Clean Water Act, the Resource Conservation and Recovery Act, and the Comprehensive Environmental Response, Compensation and Liability Act.